Unsustainability Risk of Bid Bonds in Public Tenders

Abstract

1. Introduction

2. Elements of Suretyship Insurance and the Italian Public Tenders

- Contract bonds, intended to guarantee the performance of contractual obligations, mainly in the areas of public works and private construction projects;

- Commercial bonds, intended to secure the performance of legal or regulatory obligations.

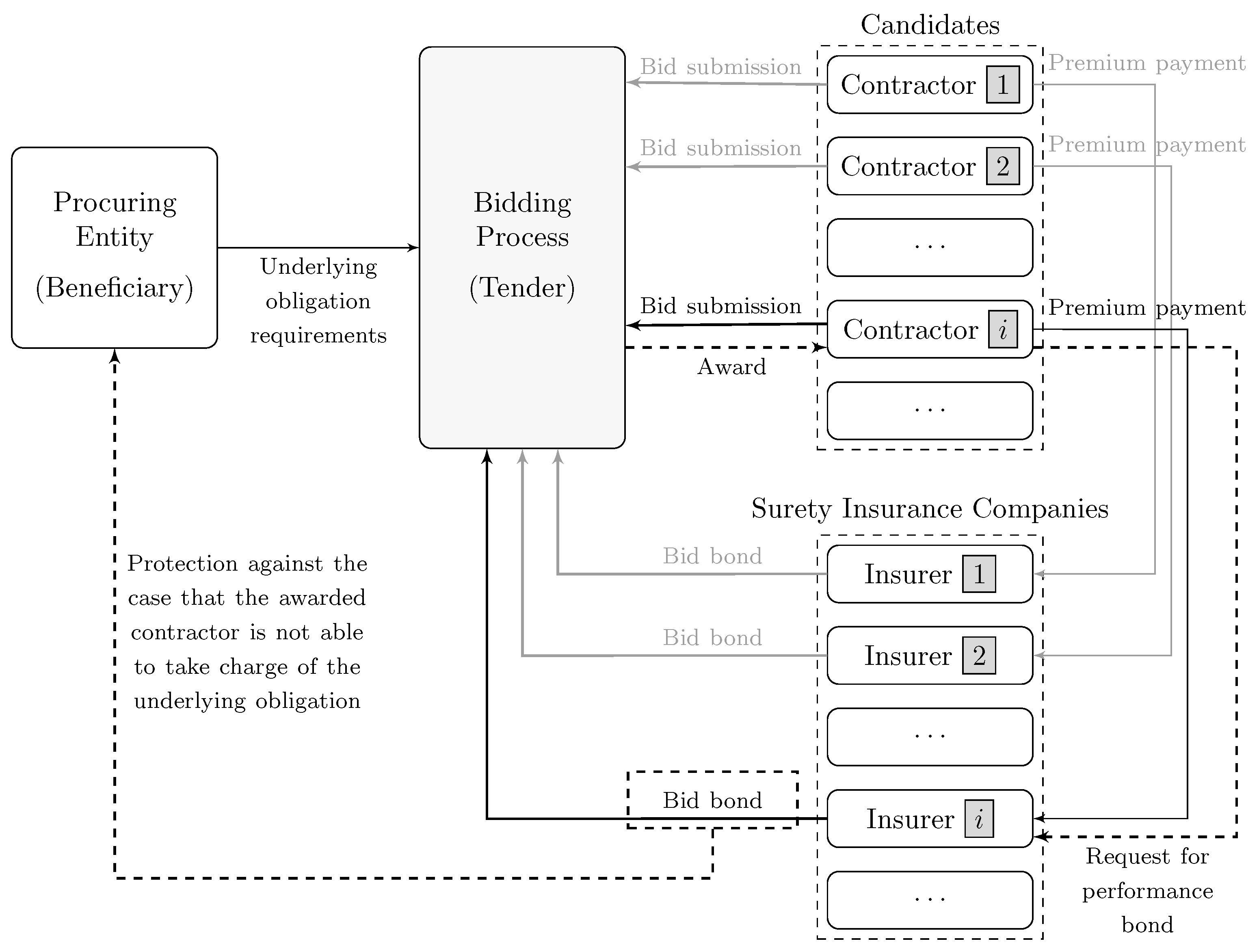

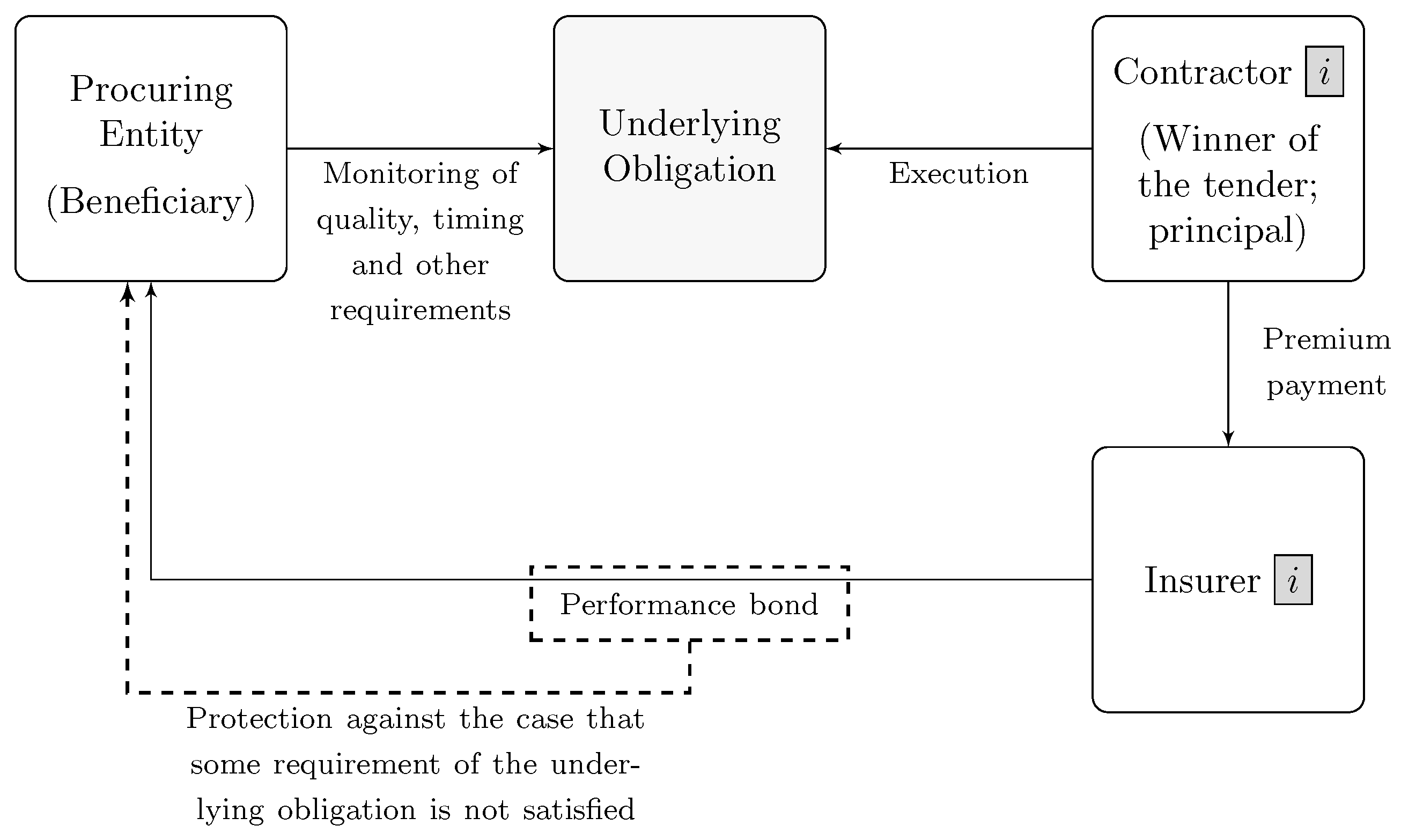

Bid and Performance Bonds: The Italian Case

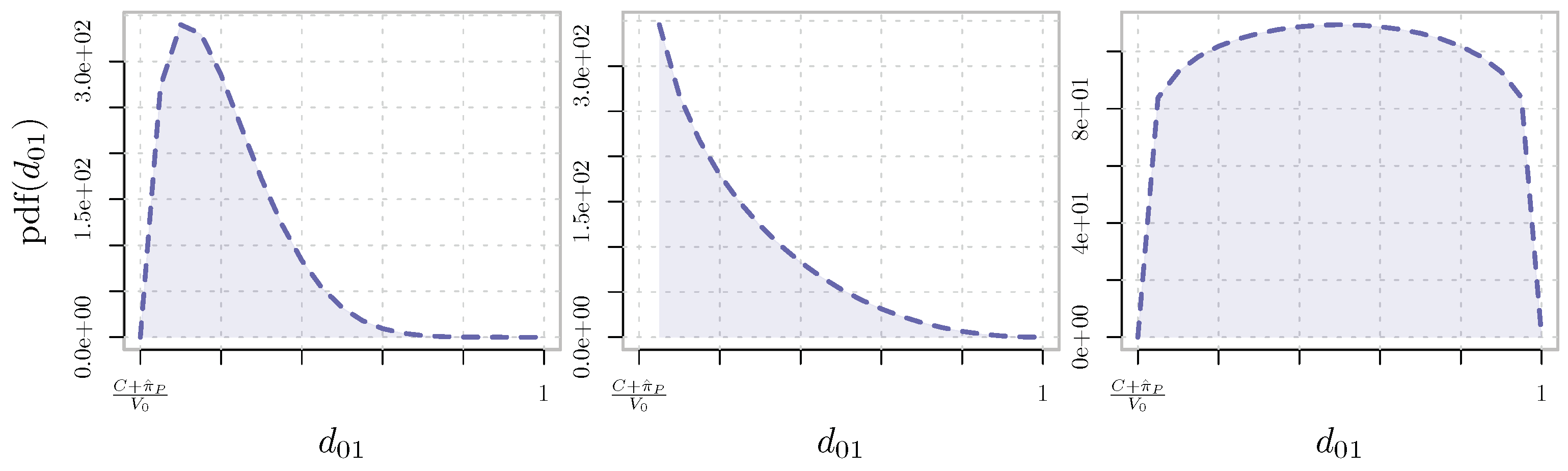

3. Sustainability of a Bid Bond

3.1. The Bidder’s Perspective

3.2. The Surety’s Perspective

- i.

- The Premium Risk, whose Solvency Capital Requirement (SCR) is measured aswhere and are the premiums earned in the last 12 months and the premiums to be earned in the next 12 months, respectively; and are the expected present value of the premiums to be earned after the following 12 months for existing contracts and for contracts whose initial recognition date falls in the following 12 months (for future contracts, premiums earned during the first 12 months after the initial recognition date are excluded from contribution to volume measure), respectively; and is the coefficient of variation associated to this sub-module of risk by the European regulator. The geographical diversification factor is not considered in Equation (11), since we are considering risks arising from Italian contractors only. The effect of reinsurance is ignored as well for this risk component and the next two listed below.

- ii.

- The Catastrophe Recession Risk, whose Solvency Capital Requirement (SCR) is measured as

- iii.

- The Catastrophe Default Risk, whose Solvency Capital Requirement (SCR) is measured aswhere () are the first and the second largest exposures in the considered portfolio and is a loss given default coefficient fixed by the European regulator.

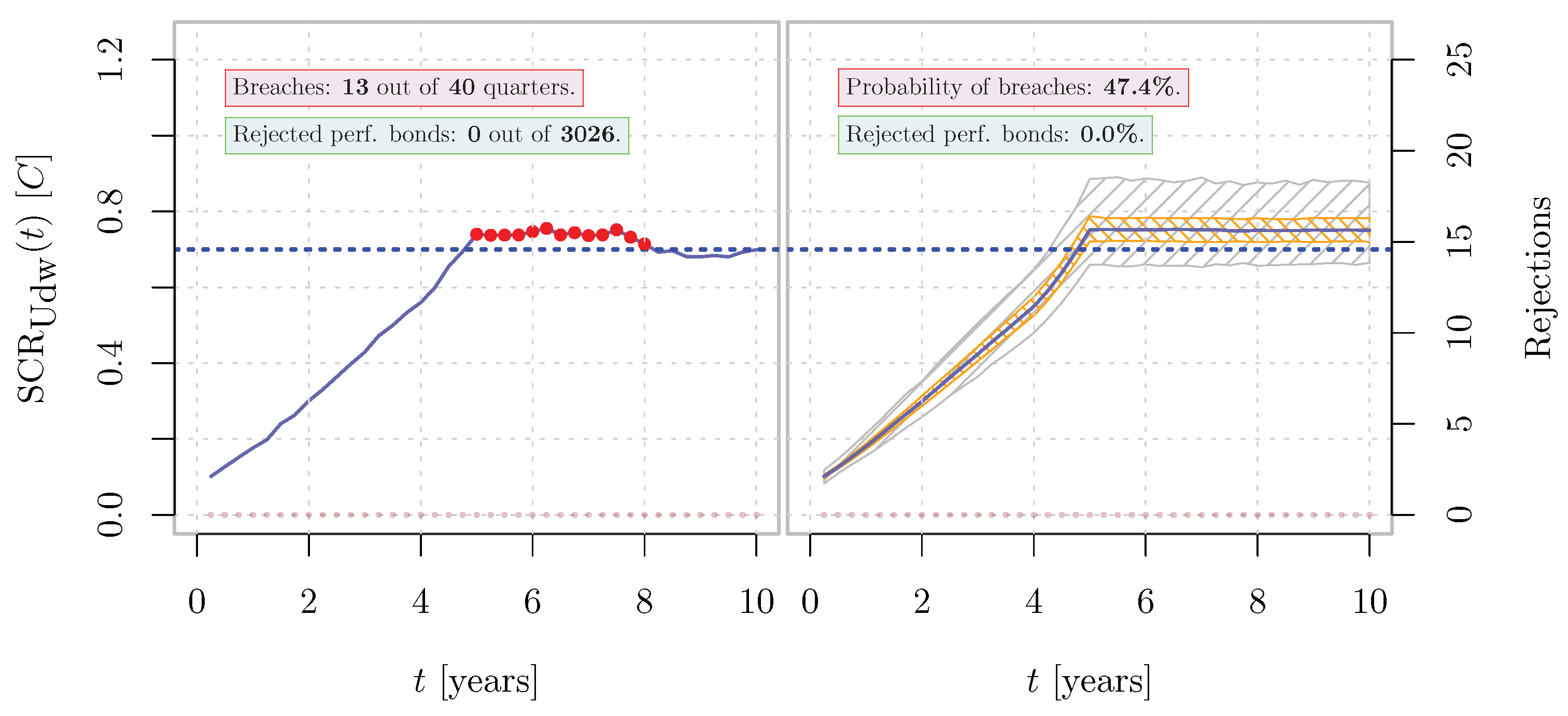

4. Measuring and Managing the Unsustainability Scenarios in Public Tenders

4.1. Simulation of Tenders from a Surety’s Perspective

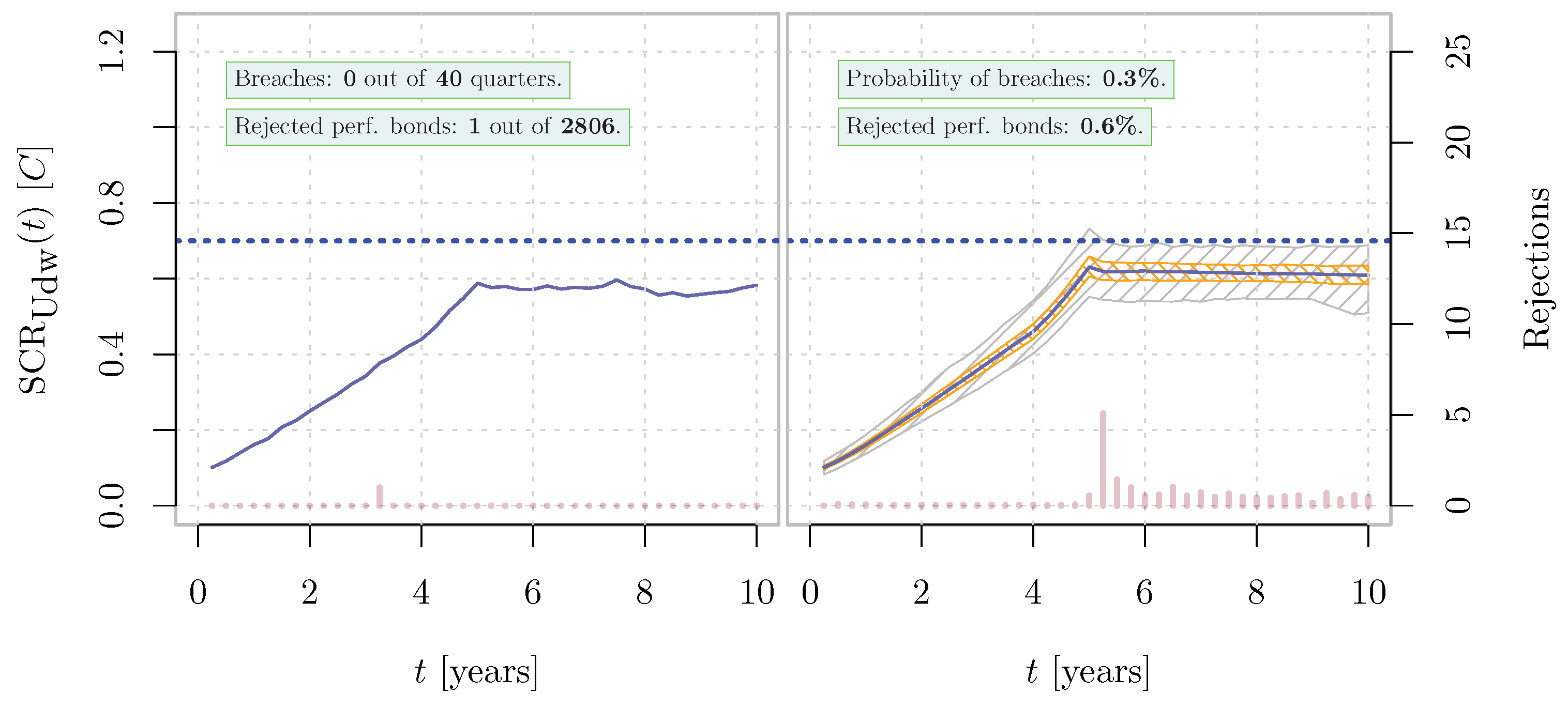

4.2. Dynamics of the Capital Requirement without Taking Management Actions

4.3. Dynamics of the Capital Requirement Adopting a Backward-Looking RAF

4.4. Dynamics of the Capital Requirement Adopting a Forward-Looking RAF

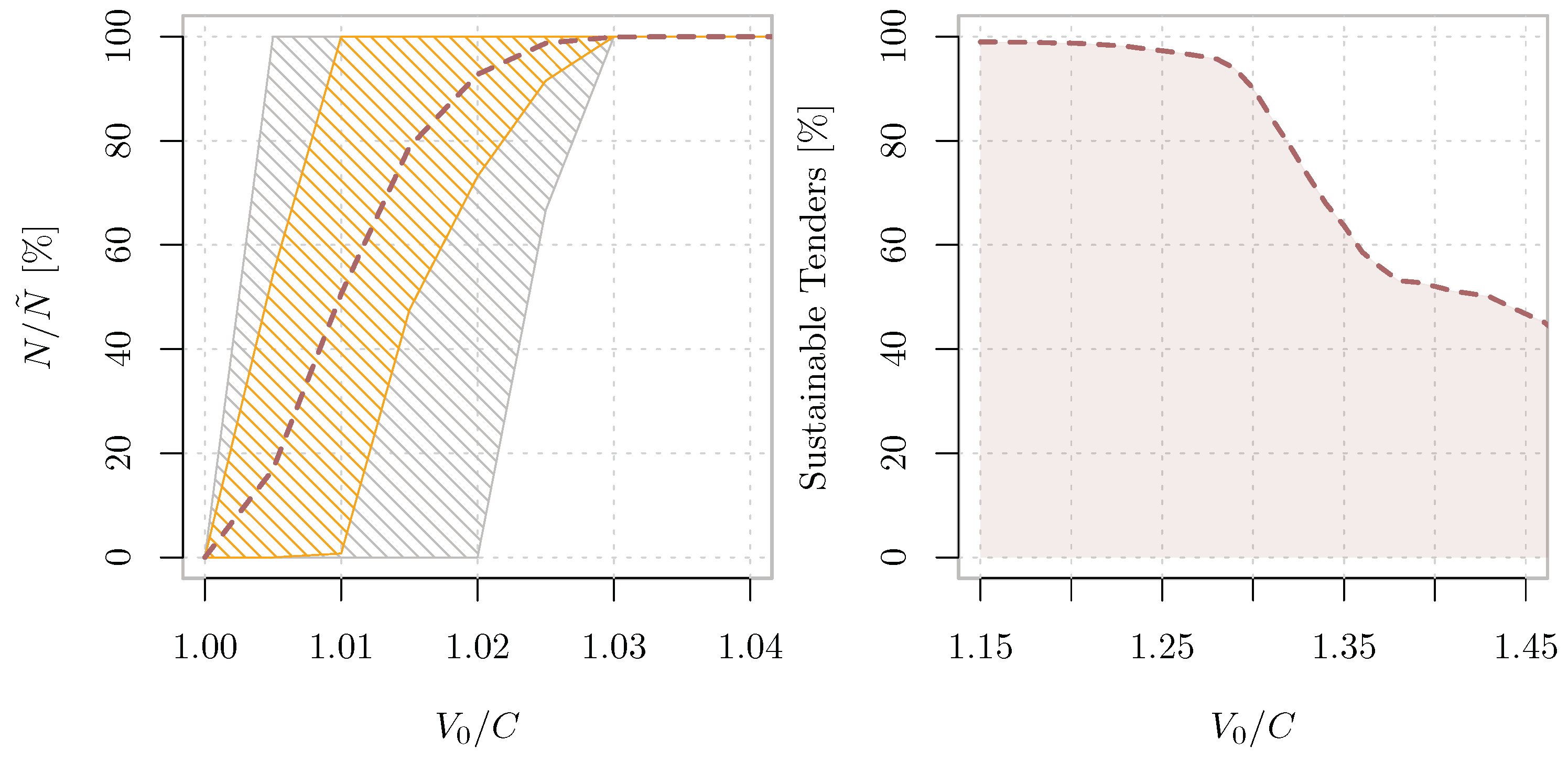

4.5. The Role of the Procuring Entity

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Luque González, A.; Coronado Martín, J.Á.; Vaca-Tapia, A.C.; Rivas, F. How Sustainability Is Defined: An Analysis of 100 Theoretical Approximations. Mathematics 2021, 9, 1308. [Google Scholar] [CrossRef]

- Directive 2014/24/EU of the European Parliament and of the Council of 26 February 2014 on Public Procurement and Repealing Directive 2004/18/EC. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:32014L0024 (accessed on 1 September 2021).

- “Miller Act”, 24 August 1935. 49 stat. 793–794, ch. 642, Sec. 1–3. Codified as Amended in the Code of Laws of the United States of America, Title 40 Public Buildings, Property, and Works. Available online: https://www.law.cornell.edu/uscode/text/40 (accessed on 1 September 2021).

- People’s Republic of China-Ministry of Commerce Bids Law of the People’s Republic of China, order No.21 of the President of People’s Republic of China on 30 August 1999. Available online: http://english.mofcom.gov.cn/article/policyrelease/Businessregulations/201303/20130300046070.shtml (accessed on 1 September 2021).

- Federal Law No. 223-FZ. On Procurement of Goods, Works and Services by Certain Types of Legal Entities; Signed into Law by the Russian President on 18 July 2011. Available online: http://government.ru/docs/all/100084/ (accessed on 1 September 2021).

- Swiss RE. Trade credit Insurance & surety: Taking stock after the financial crisis. Econ. Res. Consult. 2014. Available online: https://www.swissre.com/institute/research/topics-and-risk-dialogues/economy-and-insurance-outlook/expertise-publication-trade-credit-insurance-surety.html (accessed on 1 September 2021).

- Glen Boswall, R. Construction Bonds Guide; Clark Wilson LLP: Vancouver, BC, Canada, 2010; Available online: https://www.cwilson.com/app/uploads/2010/09/construction-bonding-guide.pdf (accessed on 1 September 2021).

- Russell, J.S. Surety Bonds for Construction Contracts, 1st ed.; American Society of Civil Engineers-ASCE Press: Reston, VA, USA, 2000. [Google Scholar]

- Yesilyaprak, M.; Erkök, B. A new instrument in Turkish financial market: Surety bonds. Finansal Araştırmalar ve Çalışmalar Dergisi 2021, 13, 904–917. [Google Scholar] [CrossRef]

- Choudhry, R.M.; Iqbal, K. Identification of Risk Management System in Construction Industry in Pakistan. J. Manag. Eng. 2013, 29, 42–49. [Google Scholar] [CrossRef]

- Liu, J.; Li, B.; Lin, B.; Nguyen, V. Key issues and challenges of risk management and insurance in China’s construction industry: An empirical study. Ind. Manag. Data Syst. 2007, 107, 382–396. [Google Scholar] [CrossRef]

- Renault, B.Y.; Agumba, J.N. Risk management in the construction industry: A new literature review. MATEC Web Conf. 2016, 66, 00008. [Google Scholar] [CrossRef]

- Bezer, D. The Inadequacy Of Surety Bid Bonds In Public Construction Contracting. Public Contract Law J. 2010, 40, 87–146. Available online: http://www.jstor.org/stable/25755803 (accessed on 1 September 2021).

- Hassan, A.A.; Adnan, H. The problems and abuse of performance bond in the construction industry. IOP Conf. Ser. Earth Environ. Sci. 2018, 117, 012044. [Google Scholar] [CrossRef]

- Helw, A.A.; Ezeldin, A.S. Toward Better Applicability of Public Procurement Law: Delay Claims by the Contractor and Limit of Compensation under the Performance Guarantee. J. Leg. Aff. Disput. Resolut. Eng. Constr. 2021, 13, 04521023. [Google Scholar] [CrossRef]

- Calveras, A.; Ganuza, J.J.; Hauk, E. Wild bids. Gambling for resurrection in procurement contracts. J. Regul. Econ. 2004, 26, 41–68. [Google Scholar] [CrossRef]

- Wambach, A.; Engel, A.R. Surety Bonds with Fair and Unfair Pricing. Geneva Risk Insur. Rev. 2011, 36, 36–50. [Google Scholar] [CrossRef][Green Version]

- Codice dei Contratti Pubblici, D. Lgs. April 18, 2016, N. 50. Gazzetta Ufficiale n. 91 April 19, 2016, s.o. n.10. Art. 93, Subsection 1 (Bid Bonds); art. 103, Subsections 1–3, 5 (Performance Bonds). Available online: https://www.codicecontrattipubblici.com/ (accessed on 1 September 2021).

- Codice Civile (Regio Decreto 16 Marzo 1942, n. 262), Art. 1916. Available online: https://www.gazzettaufficiale.it/anteprima/codici/codiceCivile (accessed on 1 September 2021).

- Directive 2009/138/EC of the European Parliament and of the Council of 25 November 2009. Available online: https://eur-lex.europa.eu/eli/dir/2009/138/oj (accessed on 1 September 2021).

- Commission Delegated Regulation (EU) 2015/35 of 10 October 2014 Supplementing Directive 2009/138/EC of the European Parliament and of the Council on the Taking-Up and Pursuit of the Business of Insurance and Reinsurance. Available online: https://eur-lex.europa.eu/eli/reg_del/2015/35/oj (accessed on 1 September 2021).

- Commission Delegated Regulation (EU) 2019/981 of 8 March 2019 Amending Delegated Regulation (EU) 2015/35 Supplementing Directive 2009/138/EC of the European Parliament and of the Council on the Taking-Up and Pursuit of the Business of Insurance and Reinsurance (Solvency II). Available online: https://eur-lex.europa.eu/eli/reg_del/2019/981/oj (accessed on 1 September 2021).

- Sandstrom, A. Handbook of Solvency for Actuaries and Risk Managers: Theory and Practice; Chapman&Hall/CRC Finance, Taylor&Francis Group: London, UK, 2011; ISBN 13-978-1439821305. [Google Scholar]

- Olivieri, A.; Pitacco, E. Introduction to Insurance Mathematics: Technical and Financial Features of Risk Transfers; Springer: Berlin/Heidelberg, Germany, 2011; ISBN 978-3-642-16028-8. [Google Scholar]

- IVASS Regulation No. 38 of 3 July 2018; Article 5, Paragraph 2, Letter E. Available online: https://www.ivass.it/normativa/nazionale/secondaria-ivass/regolamenti/2018/n38/ (accessed on 1 September 2021).

- Paulusch, J. The Solvency II Standard Formula, Linear Geometry, and Diversification. J. Risk Financ. Manag. 2017, 10, 11. [Google Scholar] [CrossRef]

- Baione, F.; De Angelis, P.; Granito, I. On a capital allocation principle coherent with the Solvency 2 Standard Formula. In Proceedings of the IVASS Conference on Insurance Research, Rome, Italy, 13 July 2017; Available online: https://www.ivass.it/pubblicazioni-e-statistiche/pubblicazioni/att-sem-conv/2017/conf-131407/ (accessed on 1 September 2021).

- Non-Performing Loans (NPLs) in Italy’s Banking System. 2017. Available online: https://www.bancaditalia.it/media/views/2017/npl/ (accessed on 1 August 2021).

- The Count of Newly Non-Performing Borrowers during the Period Series is Labelled as TRI30529_351121441. The Count of Performing Borrowers at the Beginning of the Period Series is Labelled as TRI30529_351122141. Data Are Filtered by the ATECO 2007 Economic Sector “F-Constructors”. Bank of Italy Statistical Database. Available online: https://infostat.bancaditalia.it/inquiry/ (accessed on 1 August 2021).

- Credit Suisse First Boston. CreditRisk+, A Credit Risk Management Framework; Credit Suisse First Boston: London, UK, 1998. [Google Scholar]

- Wilde, T. CreditRisk+. In Encyclopedia of Quantitative Finance; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Giacomelli, J.; Passalacqua, L. Calibrating the CreditRisk+ Model at Different Time Scales and in Presence of Temporal Autocorrelation. Mathematics 2021, 9, 1679. [Google Scholar] [CrossRef]

- Giacomelli, J.; Passalacqua, L. Improved precision in calibrating CreditRisk+ model for Credit Insurance applications. In Mathematical and Statistical Methods for Actuarial Sciences and Finance-eMAF 2020; Springer International Publishing: Berlin/Heidelberg, Germany, 2021. [Google Scholar] [CrossRef]

- Vandendorpe, A.; Ho, N.D.; Vanduffel, S.; Van Dooren, P. On the parameterization of the CreditRisk+ model for estimating credit portfolio risk. Insur. Math. Econ. 2008, 42, 736–745. [Google Scholar] [CrossRef]

- Higham, N. Computing the nearest correlation matrix—A problem from finance. IMA J. Numer. Anal. 2002, 22, 329–343. [Google Scholar] [CrossRef]

- Krishna, V. Auction Theory; Academic Press: San Diego, CA, USA, 2002; ISBN 978-0-12-426297-3. [Google Scholar]

- Milgrom, P. Putting Auction Theory to Work; Cambridge University Press: Cambridge, UK, 2004; ISBN 978-0-521-55184-7. [Google Scholar]

- Fisher, R.A.; Tippett, L.H.C. Limiting forms of the frequency distribution of the largest and smallest member of a sample. Proc. Camb. Phil. Soc. 1928, 24, 180–190. [Google Scholar] [CrossRef]

- Gnedenko, B.V. Sur la distribution limite du terme maximum d’une serie aleatoire. Ann. Math. 1943, 44, 423–453. [Google Scholar] [CrossRef]

- Suzuki, A. Investigating Pure Bundling in Japan’s Electricity Procurement Auctions. Mathematics 2021, 9, 1622. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Contract Bonds | |

|---|---|

| Bid bond | Guarantees that a contractor has submitted a bid in good faith and intends to enter the contract in case of award |

| Performance bond | Offers protection from the case that a contractor fails to fulfill the terms of the contract |

| Advance payment bond | Guarantees that the contractor will be able to repay the procuring entity any funds received in advance |

| Payment bond | Protects the credit of workers, subcontractors, and suppliers against the contractor |

| Maintenance bond | Guarantees against defective workmanship or materials |

| Commercial Bonds | |

| Customs bond | Assures customs authorities that an importer will pay the import duties required |

| Tax bond | Ensures the proper declaration and timely payment of taxes |

| License/permit bond | Guarantees the obligor’s compliance with laws |

| Court/fidelity bond | Guarantees the performance of fiduciaries’ duties and their compliance with court orders |

| s | g | h | 0 | 1 | 2 | 3 | 4 | 5 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | North-West | 1 | 0.0050 | 0.516 | 0.246 | 0.025 | 0 | 0.212 | 0 | |

| 1 | South | 2 | 0.0095 | 0.473 | 0.220 | 0.019 | 0.216 | 0 | 0.072 | |

| 1 | Islands | 3 | 0.0098 | 0.559 | 0.231 | 0 | 0.210 | 0 | 0 | |

| 1 | North-East | 4 | 0.0040 | 0.658 | 0.254 | 0.088 | 0 | 0 | 0 | |

| 1 | Center | 5 | 0.0079 | 0.026 | 0.234 | 0.070 | 0.432 | 0 | 0.238 | |

| 2 | North-West | 6 | 0.0079 | 0.509 | 0.228 | 0 | 0.028 | 0.235 | 0 | |

| 2 | South | 7 | 0.0137 | 0.651 | 0.292 | 0.057 | 0 | 0 | 0 | |

| 2 | Islands | 8 | 0.0158 | 0.455 | 0.266 | 0 | 0.036 | 0.237 | 0.005 | |

| 2 | North-East | 9 | 0.0073 | 0.628 | 0.281 | 0.086 | 0.006 | 0 | 0 | |

| 2 | Center | 10 | 0.0126 | 0.590 | 0.281 | 0.057 | 0.016 | 0 | 0.056 | |

| 3 | North-West | 11 | 0.0130 | 0.091 | 0.235 | 0 | 0.134 | 0.443 | 0.096 | |

| 3 | South | 12 | 0.0147 | 0.467 | 0.236 | 0.048 | 0 | 0.127 | 0.122 | |

| 3 | Islands | 13 | 0.0185 | 0.619 | 0.333 | 0 | 0 | 0 | 0.049 | |

| 3 | North-East | 14 | 0.0134 | 0.611 | 0.265 | 0.050 | 0 | 0.068 | 0.005 | |

| 3 | Center | 15 | 0.0178 | 0.325 | 0.251 | 0.099 | 0 | 0 | 0.326 | |

| 2.417 | 0.157 | 0.052 | 0.049 | 0.044 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Giacomelli, J.; Passalacqua, L. Unsustainability Risk of Bid Bonds in Public Tenders. Mathematics 2021, 9, 2385. https://doi.org/10.3390/math9192385

Giacomelli J, Passalacqua L. Unsustainability Risk of Bid Bonds in Public Tenders. Mathematics. 2021; 9(19):2385. https://doi.org/10.3390/math9192385

Chicago/Turabian StyleGiacomelli, Jacopo, and Luca Passalacqua. 2021. "Unsustainability Risk of Bid Bonds in Public Tenders" Mathematics 9, no. 19: 2385. https://doi.org/10.3390/math9192385

APA StyleGiacomelli, J., & Passalacqua, L. (2021). Unsustainability Risk of Bid Bonds in Public Tenders. Mathematics, 9(19), 2385. https://doi.org/10.3390/math9192385