Self-Management Portfolio System with Adaptive Association Mining: A Practical Application on Taiwan Stock Market

Abstract

1. Introduction

2. Literature Review

2.1. Association Mining

2.2. Association Mining for Financial Trading (Related Work and Benchmarks)

2.3. Performance Indicators for Financial Trading

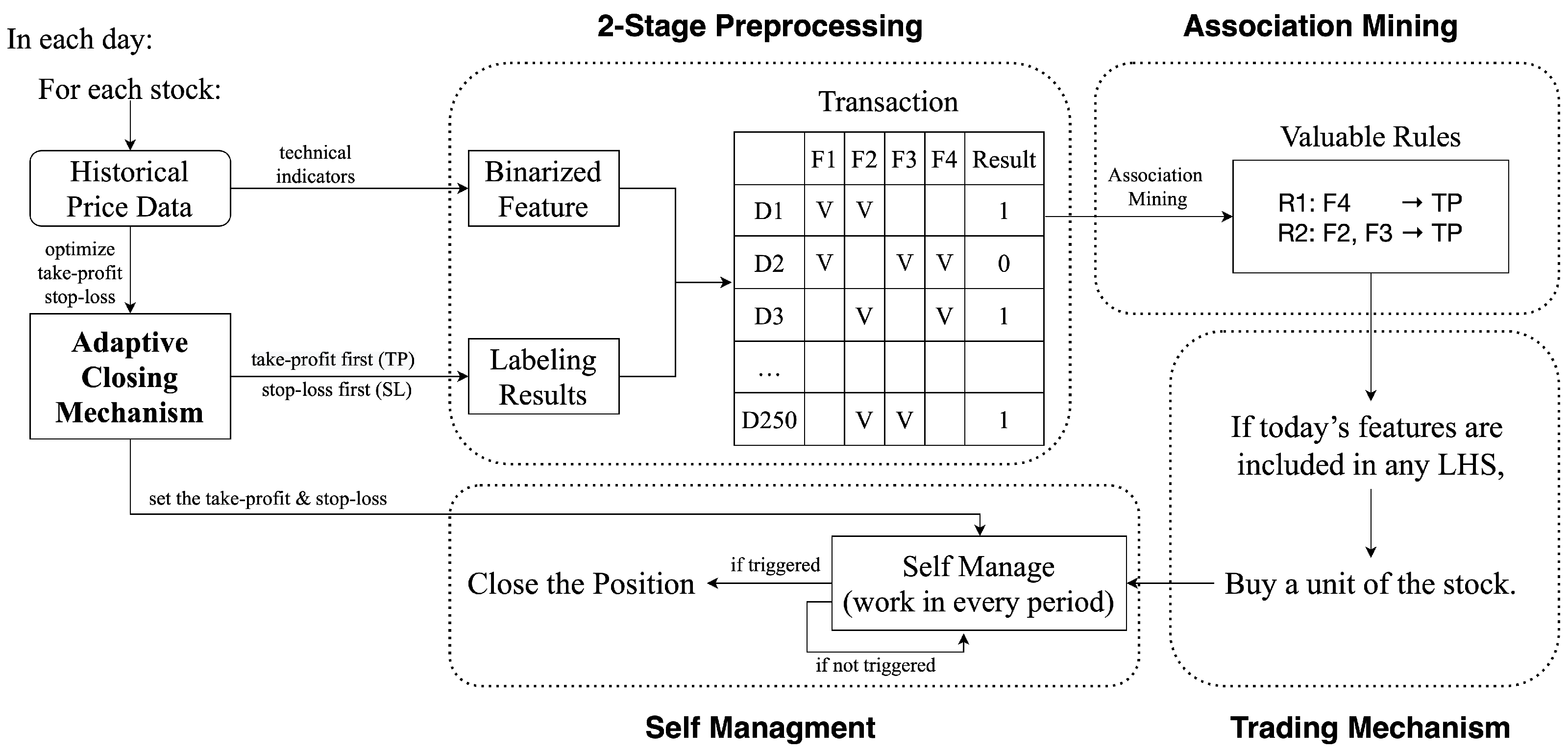

3. Proposed Self-Management Portfolio System

3.1. Trading Mechanism

3.1.1. Distributed Fund Unit

3.1.2. Details of Trading

3.2. Adaptive Closing Mechanism

3.2.1. Take-Profit and Stop-Loss Mechanisms

3.2.2. Adaptive Mechanisms

3.3. Self-Management

3.4. Two-Stage Preprocessing

3.5. Association Mining

3.5.1. Transactions and Syntactic Constraint

3.5.2. Confidence Constraint

3.5.3. Lift Constraint

3.6. Illustrative Example

4. Experimental Results and Discussion

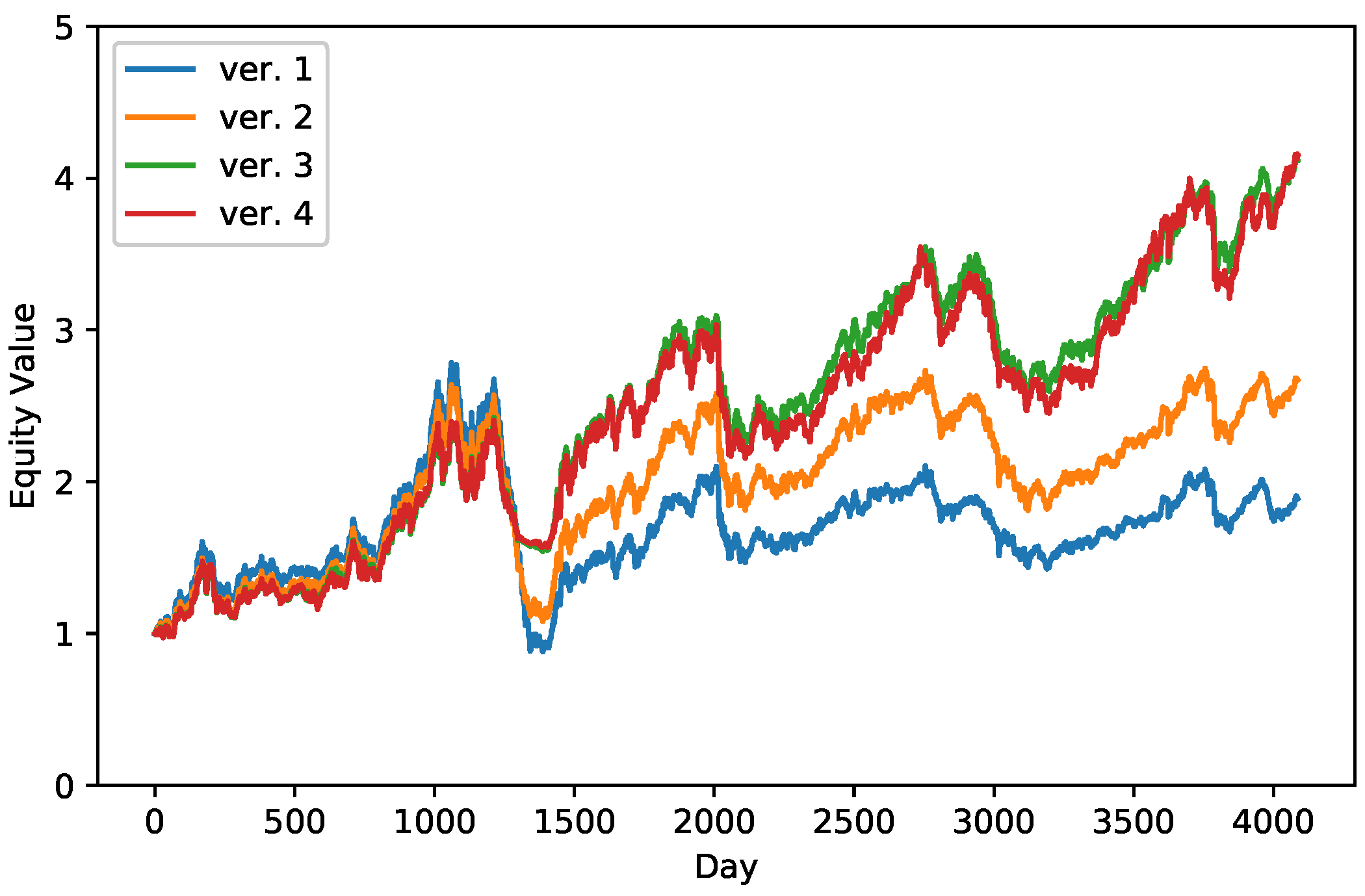

4.1. System Performance with Different Modules

4.2. Comparison between Benchmarks

4.3. Robustness Analysis on Random Stock Pools

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wu, M.E.; Syu, J.H.; Lin, J.C.W.; Ho, J.M. Portfolio management system in equity market neutral using reinforcement learning. Appl. Intell. 2021, 1–13. [Google Scholar] [CrossRef]

- Amit, R.; Livnat, J. Diversification and the risk-return trade-off. Acad. Manag. J. 1988, 31, 154–166. [Google Scholar] [CrossRef]

- Chong, Y.Y. Investment Risk Management; John Wiley & Sons: Hoboken, NJ, USA, 2004. [Google Scholar]

- Koellner, T.; Weber, O.; Fenchel, M.; Scholz, R. Principles for sustainability rating of investment funds. Bus. Strat. Environ. 2005, 14, 54–70. [Google Scholar] [CrossRef]

- Giudici, P.; Figini, S. Applied Data Mining for Business and Industry; Wiley Online Library: Hoboken, NJ, USA, 2009. [Google Scholar]

- Berry, M.J.; Linoff, G.S. Data Mining Techniques: For Marketing, Sales, and Customer Relationship Management; John Wiley & Sons: Hoboken, NJ, USA, 2004. [Google Scholar]

- Kovalerchuk, B.; Vityaev, E. Data Mining in Finance: Advances in Relational and Hybrid Methods; Springer Science & Business Media: New York, NY, USA, 2006; Volume 547. [Google Scholar]

- Grossman, R.L.; Kamath, C.; Kegelmeyer, P.; Kumar, V.; Namburu, R. Data Mining for Scientific and Engineering Applications; Springer Science & Business Media: New York, NY, USA, 2013; Volume 2. [Google Scholar]

- Tsai, C.W.; Lai, C.F.; Chiang, M.C.; Yang, L.T. Data mining for internet of things: A survey. IEEE Commun. Surv. Tutor. 2013, 16, 77–97. [Google Scholar] [CrossRef]

- Syu, J.H.; Wu, M.E.; Srivastava, G.; Chao, C.F.; Lin, J.C.W. An IoT-based Hedge System for Solar Power Generation. IEEE Int. Things J. 2021. [Google Scholar] [CrossRef]

- Lu, H.; Han, J.; Feng, L. Stock movement prediction and n-dimensional inter-transaction association rules. In Proceedings of the 1998 ACM SIGMOD Workshop on Research Issues on Data Mining and Knowledge Discovery, Seattle, WA, USA, 5 June 1998; ACM: New York, NY, USA, 1998. [Google Scholar]

- Liao, S.H.; Ho, H.H.; Lin, H.W. Mining stock category association and cluster on Taiwan stock market. Exp. Syst. Appl. 2008, 35, 19–29. [Google Scholar] [CrossRef]

- Paranjape-Voditel, P.; Deshpande, U. A stock market portfolio recommender system based on association rule mining. Appl. Soft Comput. 2013, 13, 1055–1063. [Google Scholar] [CrossRef]

- Agrawal, R.; Imieliński, T.; Swami, A. Mining association rules between sets of items in large databases. In Proceedings of the 1993 ACM SIGMOD International Conference on Management of Data, Washington, DC, USA, 26–28 May 1993; pp. 207–216. [Google Scholar]

- Lin, W.; Alvarez, S.A.; Ruiz, C. Efficient adaptive-support association rule mining for recommender systems. Data Mining Knowl. Discov. 2002, 6, 83–105. [Google Scholar] [CrossRef]

- Na, S.H.; Sohn, S.Y. Forecasting changes in Korea composite stock price index (KOSPI) using association rules. Exp. Syst. Appl. 2011, 38, 9046–9049. [Google Scholar] [CrossRef]

- Uyemura, D.G.; Kantor, C.C.; Pettit, J.M. EVA® for banks: Value creation, risk management, and profitability measurement. J. Appl. Corp. Financ. 1996, 9, 94–109. [Google Scholar] [CrossRef]

- Chen, J. Annual Return. 2019. Available online: http://investopedia.com/ (accessed on 15 April 2021).

- Magdon-Ismail, M.; Atiya, A.F. Maximum drawdown. Risk Mag. 2004, 17, 99–102. [Google Scholar]

- Sharpe, W.F. The Sharpe ratio. J. Portf. Manag. 1994, 21, 49–58. [Google Scholar] [CrossRef]

- Bailey, D.H.; Prado, M.L.d. The Sharpe ratio efficient frontier. J. Risk 2012, 15, 13. [Google Scholar] [CrossRef]

- Wu, M.E.; Syu, J.H.; Lin, J.C.W.; Ho, J.M. Evolutionary ORB-based model with protective closing strategies. Knowl. Based Syst. 2021, 216, 106769. [Google Scholar] [CrossRef]

- Syu, J.H.; Wu, M.E. Modifying ORB trading strategies using particle swarm optimization and multi-objective optimization. J. Ambient Intell. Humaniz. Comput. 2021, 1–13. [Google Scholar] [CrossRef]

- Taran Morosan, A. The relative strength index revisited. Afr. J. Bus. Manag. 2011, 5, 5855. [Google Scholar]

- Stochastic Oscillator. Available online: https://school.stockcharts.com/doku.php?id=technical_indicators:stochastic_oscillator_fast_slow_and_full (accessed on 15 April 2021).

- DeMiguel, V.; Garlappi, L.; Uppal, R. Optimal versus naive diversification: How inefficient is the 1/N portfolio strategy? Rev. Financ. Stud. 2009, 22, 1915–1953. [Google Scholar] [CrossRef]

- Plyakha, Y.; Uppal, R.; Vilkov, G. Equal or value weighting? Implications for asset-pricing tests. Implic. Asset-Pricing Tests 2014. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| F1 | F2 | F3 | F4 | ⋯ | F18 | Label |

|---|---|---|---|---|---|---|

| 1 | 0 | 1 | 1 | ⋯ | 1 | +1 |

| 1 | 0 | 1 | 1 | ⋯ | 1 | +1 |

| 1 | 1 | 0 | 0 | ⋯ | 1 | −1 |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋱ | ⋮ |

| 0 | 0 | 1 | 0 | 1 | ⋯ | 0 |

| Systems | ver. 1 | ver. 2 | ver. 3 | ver. 4 |

|---|---|---|---|---|

| Confidence | Simple | Strong | Strong | Strong |

| Lift | No | No | Dynamic | Dynamic |

| Timer | No | No | No | Dynamic |

| Annual Return | 4.0% | 6.2% | 9.0% | 9.1% |

| Sharpe Ratio | 0.233 | 0.379 | 0.600 | 0.578 |

| MDD | 68.4% | 59.0% | 36.3% | 34.6% |

| Systems | Annual Return | Sharpe Ratio | MDD |

|---|---|---|---|

| Proposed System-ver. 4 | 9.1% | 0.578 | 34.6% |

| Proposed System-ver. 3 | 9.0% | 0.600 | 36.3% |

| Equal Weight | 6.8% | 0.431 | 55.1% |

| Taiwan-50 ETF (0050.TW) | 7.3% | 0.369 | 59.0% |

| Paranjape-Voditel and Umesh [13] | 5.5% | 0.235 | 69.0% |

| Systems | Annual Return | Sharpe Ratio | MDD |

|---|---|---|---|

| All stocks-ver. 3 | 9.0% | 0.600 | 36.3% |

| All stocks-ver. 4 | 9.1% | 0.578 | 34.6% |

| RS1-ver. 3 | 8.3% | 0.588 | 27.8% |

| RS1-ver. 4 | 8.1% | 0.562 | 32.8% |

| RS2-ver. 3 | 8.9% | 0.636 | 26.0% |

| RS2-ver. 4 | 8.5% | 0.604 | 29.1% |

| RS3-ver. 3 | 9.5% | 0.678 | 26.1% |

| RS3-ver. 4 | 8.7% | 0.619 | 26.4% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Syu, J.-H.; Yeh, Y.-R.; Wu, M.-E.; Ho, J.-M. Self-Management Portfolio System with Adaptive Association Mining: A Practical Application on Taiwan Stock Market. Mathematics 2021, 9, 1093. https://doi.org/10.3390/math9101093

Syu J-H, Yeh Y-R, Wu M-E, Ho J-M. Self-Management Portfolio System with Adaptive Association Mining: A Practical Application on Taiwan Stock Market. Mathematics. 2021; 9(10):1093. https://doi.org/10.3390/math9101093

Chicago/Turabian StyleSyu, Jia-Hao, Yi-Ren Yeh, Mu-En Wu, and Jan-Ming Ho. 2021. "Self-Management Portfolio System with Adaptive Association Mining: A Practical Application on Taiwan Stock Market" Mathematics 9, no. 10: 1093. https://doi.org/10.3390/math9101093

APA StyleSyu, J.-H., Yeh, Y.-R., Wu, M.-E., & Ho, J.-M. (2021). Self-Management Portfolio System with Adaptive Association Mining: A Practical Application on Taiwan Stock Market. Mathematics, 9(10), 1093. https://doi.org/10.3390/math9101093