Abstract

We consider the indefinite, linear-quadratic, mean-field-type stochastic zero-sum differential game for jump-diffusion models (I-LQ-MF-SZSDG-JD). Specifically, there are two players in the I-LQ-MF-SZSDG-JD, where Player 1 minimizes the objective functional, while Player 2 maximizes the same objective functional. In the I-LQ-MF-SZSDG-JD, the jump-diffusion-type state dynamics controlled by the two players and the objective functional include the mean-field variables, i.e., the expected values of state and control variables, and the parameters of the objective functional do not need to be (positive) definite matrices. These general settings of the I-LQ-MF-SZSDG-JD make the problem challenging, compared with the existing literature. By considering the interaction between two players and using the completion of the squares approach, we obtain the explicit feedback Nash equilibrium, which is linear in state and its expected value, and expressed as the coupled integro-Riccati differential equations (CIRDEs). Note that the interaction between the players is analyzed via a class of nonanticipative strategies and the “ordered interchangeability” property of multiple Nash equilibria in zero-sum games. We obtain explicit conditions to obtain the Nash equilibrium in terms of the CIRDEs. We also discuss the different solvability conditions of the CIRDEs, which lead to characterization of the Nash equilibrium for the I-LQ-MF-SZSDG-JD. Finally, our results are applied to the mean-field-type stochastic mean-variance differential game, for which the explicit Nash equilibrium is obtained and the simulation results are provided.

1. Introduction

The mean-field-type stochastic differential equation (MF-SDE) is known as a class of stochastic differential equations (SDEs), in which the expected values of state and control variables are included. In fact, the theory of MF-SDEs can be traced back to studying of McKean–Vlasov SDEs for analyzing interacting particle systems at the macroscopic level [1,2]. Since then, many researches have focused on studying McKean–Vlasov SDEs and MF-SDEs, and their applications in science and economics [3,4,5].

We note that as stated in [6], the main purposes of studying control problems and games for MF-SDEs are to reduce variations of random effects in the controlled state process and to analyze large-scale mean-field-interacting particle systems. Recently, stochastic optimal control and differential games for MF-SDEs with jump diffusions have been studied in [7,8,9,10,11,12,13]. Various stochastic maximum principles for mean-field-type jump-diffusion models were established [7,8,9,12,13]. Moreover, linear-quadratic (LQ) stochastic optimal control problems for (linear) mean-field-type jump-diffusion models were studied in [10,11]. We note that the references mentioned above considered only the mean-field-type stochastic control problem and nonzero-sum game for jump-diffusion models. In the optimal control case, this implies that there is only one player who minimizes (or maximizes) the objective functional. Moreover, in the nonzero-sum game case, this means that the explicit interaction of the players cannot be modeled. Hence, it is necessary to extend the earlier results mentioned above to the framework of stochastic zero-sum games in order to analyze a more complex interaction between the players through the dynamics and the objective functional in the mean-field sense using the concept of strategies. This is addressed in our paper; the precise problem formulation and a detailed comparison with the existing literature are given below.

In this paper, we consider the indefinite, linear-quadratic, mean-field-type stochastic zero-sum differential game for jump-diffusion models (I-LQ-MF-SZSDG-JD). Specifically, there are two players in the I-LQ-MF-SZSDG-JD; Player 1 minimizes the objective functional while Player 2 maximizes the same objective functional. In the I-LQ-MF-SZSDG-JD, the jump-diffusion state dynamics controlled by the two players and the objective functional include the mean-field variables, i.e., the expected value of state and control variables. Moreover, the parameters of the objective functional in the I-LQ-MF-SZSDG-JD do not need to be (positive) definite matrices.

By considering the interaction between two players and using the completion of squares approach, we obtain the explicit Nash feedback equilibrium, which is linear in state and its expected value, and expressed as the coupled integro-Riccati differential equations (CIRDEs) (see Theorems 1 and 2). Note that the interaction between the players is analyzed via a class of nonanticipative strategies and the “ordered interchangeability” property of multiple Nash equilibria in zero-sum games (see Corollary 1). We obtain explicit conditions to obtain the Nash equilibrium in terms of the CIRDEs. We also discuss the different solvability conditions of the CIRDEs, which lead to characterization of the Nash equilibrium for the I-LQ-MF-SZSDG-JD (see Proposition 1 and Theorem 3). As mentioned below, the approaches developed in this paper, including the solvability of the CIRDEs, are new and have not been studied in the existing literature.

Finally, we apply our results to the mean-field-type stochastic mean-variance differential game. Specifically, we are able to obtain the explicit Nash equilibrium for the mean-variance problem and the corresponding controlled wealth process by verifying the solvability of the CIRDEs. The simulation results are also provided.

We note that the problem formulation and the main results of this paper can be viewed as extensions of those in [6,14] to the LQ mean-field-type zero-sum game for jump-diffusion models. In particular, our paper generalizes the results of [6,14] to the framework of two-player games with the jump-diffusion models. Furthermore, unlike [11], we consider the situation of the two-player game, where the players interact with each other through the dynamics and the objective functional using nonanticipative strategies. The main differences between our paper and [6,11,14] are as follows:

- (a)

- We extend [6] to the two-player game framework; unlike [6], our cost parameters do not need to be definite matrices. We provide explicit conditions under which the Nash equilibrium can be characterized. Moreover, we provide the numerical example and simulation results to support our theoretical results.

- (b)

- We generalize [14] to the case of jump-diffusion models, where, unlike [14], our paper considers the case of multi-dimensional Brownian motion and Poisson process. Furthermore, the results of this paper were applied to the modified mean-variance stochastic differential game, whereas [14] provided only the simple simulation results.

- (c)

- The problem formulation and the results of this paper are different from those of [11]. Note that [11] considered the LQ nonzero-sum differential game for mean-field-type jump-diffusion models. However, due to the nonzero-sum game structure, reference [11] cannot explain the interaction between two-players captured by a class of nonanticipative strategies and the ordered interchangeability property of multiple Nash equilibria in zero-sum games. Moreover, unlike [11], we consider the general vector-valued jump-diffusion model and the case when the cost parameters are indefinite matrices. In addition, [11] did not provide any theoretical results on the solvability of the Riccati equation, whereas our paper provides an easy-to-check condition of the solvability of the CIRDEs, which leads to the explicit characterization of the Nash equilibrium for the I-LQ-MF-SZSDG-JD. Finally, we provide the extensive simulation results of the modified mean-variance optimization problem, whereas [11] did not provide any simulation results.

The generalizations in (a)–(c) turn out to be not straightforward due of (i) the inclusion of jump-diffusion processes, (ii) the interaction between the players modeled by nonanticipative strategies, and (iii) indefiniteness of cost parameters in the objective functional. As mentioned above, our paper addresses these challenges.

Before concluding this section, it should be mentioned that there are various applications of MF-SDEs. Specifically, MF-SDEs can be applied to mean-variance portfolio selection problems, economics with a large number of firms, mean cooperative dynamic model, and air conditioning control in building systems [7,8,15]. Moreover, MF-SDEs are closely related to mean-field games, in which a large number of players consider the optimal complex decision-making problem for interacting particle systems under stochastic uncertainty; see [16,17,18,19] and the references therein.

Our paper is organized as follows. The problem formulation is given in Section 2. The main results of the paper are given in Section 3, where the explicit characterization of the feedback Nash equilibria for the I-LQ-MF-SZSDG-JD is studied. The solvability of the CIRDEs is provided in Section 4. In Section 5, we apply our main results obtained in Section 3 and Section 4 to the mean-field-type stochastic mean-variance differential game. Concluding remarks are provided in Section 6.

2. Problem Formulation

We first introduce the notation used in this paper. Let be the n-dimensional Euclidean space. For , denotes the transpose of x, is the inner product, and . Let be the set of symmetric matrices. Let for and . Let be a complete probability space with the natural filtration generated by the one-dimensional Brownian motion , , and the E-marked right-continuous Poisson process , , which are mutually independent. (That is, , , is an E-marked right continuous Poisson random measure (process) defined on , where with is a Borel subset of equipped with its Borel -field ). Let be the compensated Poisson process of , , where is an -finite Lévy measure on , which satisfies .

Consider the following mean-field-type SDE (MF-SDE) with jump diffusions on . (The SDE with jump diffusions is usually referred to as a class of SDEs driven by both Brownian motion and Poisson process; see ([20] page 383) and ([21], Chapter 1.3)):

where is the controlled state process, is the control of Player 1, and is the control of Player 2. In (1), for , and , , , , and are deterministic, which are continuous and uniformly bounded in . Let , , be a set of admissible controls for Player i, where is the space of -predictable -valued stochastic processes satisfying .

The objective functional that is minimized by Player 1 and maximized by Player 2 is given by (see also [14] for the MF-SZSDG without jumps, which is a special case of this paper)

where for , and are deterministic, which are continuous and uniformly bounded in , and , , are deterministic and bounded. We rewrite the conditions of the coefficients in (1) and (2) as follows:

Assumption 1.

In (1) and (2), for , and , , , , , and , are deterministic, which are continuous and uniformly bounded in . (Note that , where with and is the Borel σ-field generated by E, denotes the space of square integrable functions such that for , satisfies , where λ is an σ-finite Lévy measure on ). Additionally, , , in (2) are deterministic and bounded.

Remark 1.

Note that under Assumption 1, for any , (1) admits a unique solution which holds and càdlàg (right continuous with left limits) ([7], Lemma 4.1) (see also [8,20,21]). Moreover, in Assumption 1, the cost parameters Q, , , , M, and in (2) do not need to be (positive) definite matrices.

The above problem can then be referred to as the indefinite, linear-quadratic (LQ) stochastic zero-sum differential game for mean-field-type jump-diffusion systems (I-LQ-MF-SZSDG-JD), where the “indefinite” means that the cost parameters do not need to be (positive) definite matrices (see Remark 1).

Our main objective of this paper is to find a (feedback-type) Nash equilibrium , i.e., satisfies

If in (3) exists, we say that is an optimal game value of the I-LQ-MF-SZSDG-JD.

Now, to achieve the main goal of the I-LQ-MF-SZSDG-JD in this paper, we introduce the notion of nonanticipative strategies [22,23]:

Definition 1.

- (i)

- An admissible nonanticipative strategy for Player 1, denoted by , is a mapping defined such that (equivalently, for ) and for any -stopping time and any , with on , it holds that on . The space of admissible nonanticipative strategies for Player 1 is defined by .

- (ii)

- An admissible nonanticipative strategy for Player 2, (equivalently, for ) is defined in a similar way. The space of admissible nonanticipative strategies for Player 2 is defined by .

Note that the nonanticipative strategy of Player 1 (respectively, Player 2), , is a mapping, which is generated based on Player 2’s control (respectively, Player 1’s control ) [14,23,24]. We can see that if Player 1 (respectively, Player 2) cannot distinguish between the values of and of Player 2 (respectively, and of Player 1), then Player 1 (respectively, Player 2) cannot respond differently to those signals. Based on Definition 1 and [23], we may expand (3) as follows:

Definition 2.

- (i)

- The control-strategy pair constitutes the Nash equilibrium of the I-LQ-MF-SZSDG-JD if satisfies the following inequalities:The optimal game value of the I-LQ-MF-SZSDG-JD under is .

- (ii)

- The control-strategy pair constitutes the Nash equilibrium of the I-LQ-MF-SZSDG-JD if satisfies the following inequalities:The optimal game value of the I-LQ-MF-SZSDG-JD under is .

Remark 2.

- (i)

- In view of Definition 2, if (see (4)) and (see (5)) are Nash equilibria for the I-LQ-MF-SZSDG-JD, then the pair also constitutes a Nash equilibrium of the I-LQ-MF-SZSDG-JD satisfying (3). This follows from the the ordered interchangeability property of multiple Nash equilibria (or saddle-points) in zero-sum games (see ([25], page 302) and ([26], Lemma 2.4)).

- (ii)

- In this case, the optimal game value is given by . This fact can be shown easily. In particular, suppose that and are Nash equilibria of the I-LQ-MF-SZSDG-JD. This implies that . Note also that by Definition 1, the admissible strategy is an -valued mapping for . Then from (4) and (5) it follows that and . This shows that .

3. Main Results

In this section, we solve the I-LQ-MF-SZSDG-JD formulated in Section 2.

3.1. Coupled Integro-Riccati Differential Equations

We first introduce the following notation:

Consider the following coupled integro-Riccati differential equations (CIRDEs):

and

Notice that the solutions to (6) and (7) are -valued (symmetric) deterministic backward processes (due to terminal conditions).

For , we define

and

where

For the RDE in (6), we introduce

Similarly, for (7),

We now state the equivalence between (6), (10) and (11):

Lemma 1.

- (i)

- Assume that and − are invertible for all . Then in (9) is invertible for all . Moreover, the CIRDE in (6) can be written as the CIRDE in (10).

- (ii)

- Assume that and are invertible for all . Then in (9) is invertible for all . Moreover, the CIRDE in (6) can be written as the CIRDE in (11).

Proof.

We prove (i) only, since the proof for (ii) is similar to that for (i). Based on (8) and (9), the CIRDE in (6) can be rewritten as follows:

Note that due to the invertibility of in (i), we have

By the invertibility of in (i) and the block matrix inversion lemma ([27], Equation (0.7.3.1)) ([27], Equation (0.7.3.1)) is applied to obtain the inverse of and ), , the inverse of , exists for all , which can be written as (note that for , we have )

From (15), in (14) can be rewritten as follows

By substituting (16) into (14), we can see that the CIRDE in (14) (equivalently (6)) becomes equivalent to (10). This completes the proof for (i) of the lemma. Part (ii) of the lemma can be shown in a similar way with given by

Then by using the invertibility conditions of (ii), the rest of the proof is identical to that for (i). This completes the proof. □

Similarly to Lemma 1, the following lemma holds:

Lemma 2.

- (i)

- Assume that and are invertible for all . Then in (9) is invertible for all . Moreover, the CIRDE in (7) can be written as the CIRDE in (12).

- (ii)

- Assume that and are invertible for all . Then in (9) is invertible for all . Moreover, the CIRDE in (7) can be written as the CIRDE in (13).

Proof.

Using (8) and (9), the CIRDE in (7) can be written as

Then the proof of the lemma is similar to that for Lemma 1. This completes the proof. □

3.2. Characterization of Nash Equilibria

Let us define

Consider,

Note that in (17) depends on the control of Player 1. We can easily see that

and (18) corresponds to the control-strategy pair. We will consider the case of (17) when Player 1 selects and Player 2 observes , i.e., . Suppose that is applied to the MF-SDE with jump diffusions in (1):

where

We state the following lemma:

Lemma 3.

Assume that the CIRDEs in (6) and (7) admit unique symmetric (bounded) solutions on . Then the MF-SDE with jump diffusions in (19) admits a unique solution that satisfies and càdlàg (right continuous with left limits).

Proof.

The lemma follows from ([7], Lemma 4.1) (see also [8,20,21]) and the fact that the coefficients of (19) are bounded on (see also Remark 1). □

The following theorem is the first main result of this paper:

Theorem 1.

Assume that the CIRDEs in (6) and (7) admit unique symmetric (bounded) solutions on . Suppose that

- (i)

- and are (uniformly) negative definite for all ;

- (ii)

- and are (uniformly) positive definite for all .

Then the control-strategy pair in (18) constitutes the Nash equilibrium of the I-LQ-MF-SZSDG-JD in the sense of (4). Moreover, the optimal game value of the I-LQ-MF-SZSDG-JD is given by .

Proof.

Let and , . Note that . Then

and

where

From (i) of Lemmas 1 and 2, note that the CIRDEs in (6) and (7) are equivalent to (10) and (12), respectively, under (i) and (ii) of the theorem. Then using (20) and applying Itô’s formula for general Lévy-type stochastic integrals (see ([20], Theorems 4.4.7 and 4.4.13)) yield

and

Since the stochastic integrals with respect to the Brownian motion and the Poisson process in (22) are martingales (due to their bounded coefficients, see ([20], Chapter 4.3.2)), by noting the terminal condition of (6) and (7), we have

and

Recall the definition in (21). Then

By completing the integrands of the above expression with respect to and , , and noting the coefficients in (18), we have

We note the invertibility conditions in (i) and (ii) of the theorem. Assume that the players are with the control-strategy pair given in (18). Then (23) becomes

Moreover, since and are (uniformly) negative definite for all (see (i) of the theorem), using (23), we can observe that

Similarly, under (ii) of the theorem, using (23), it follows that

Then (24)–(26) imply that

Hence, (27) and Lemma 3 show that under (i) and (ii) of the theorem, the control-strategy pair given in (18) constitutes the Nash equilibrium in the sense of (4), and is the optimal game value of the I-LQ-MF-SZSDG-JD. This completes the proof. □

We now define

By symmetry, consider,

It can be easily seen that in (28) depends on the control of Player 2. Similarly to (18), we have

Analogously, we will consider the case when Player 2 selects and Player 1 observes , i.e., . Suppose that is applied to the MF-SDE with jump diffusions in (1):

where

Similarly to Lemma 3, we state the following lemma:

Lemma 4.

Assume that the CIRDEs in (6) and (7) admit unique symmetric (bounded) solutions on . Then the MF-SDE with jump diffusions in (30) admits a unique solution that holds and càdlàg (right continuous with left limits).

The following theorem is the second main result of this paper and is a counterpart of Theorem 1, which states that under suitable definiteness conditions of the coefficients (which is different from those for Theorem 1), the control-strategy pair given in (29) is the Nash equilibrium in the sense of (5).

Theorem 2.

Assume that the CIRDEs in (6) and (7) admit unique symmetric (bounded) solutions on . Suppose that

- (i)

- and are (uniformly) positive definite for all ;

- (ii)

- and are (uniformly) negative definite for all .

Then the control-strategy pair in (29) constitutes the Nash equilibrium of the I-LQ-MF-SZSDG-JD in the sense of (5). Moreover, the optimal game value of the I-LQ-MF-SZSDG-JD is given by .

Proof.

The proof of Theorem 2 is identical to that for Theorem 1. Specifically, in view of (ii) of Lemmas 1 and 2, under (i) and (ii) of the theorem, the CIRDEs in (6) and (7) are equivalent to (11) and (13), respectively. Then the rest of the proof is similar to that for Theorem 1. Note that in this proof, we need Lemma 4 instead of Lemma 3. We complete the proof. □

Based on Theorems 1 and 2 and Remark 2, the main result of this section can be stated as follows:

Corollary 1.

Assume that the CIRDEs in (6) and (7) admit unique symmetric (bounded) solutions on . Suppose that

- (i)

- and are (uniformly) positive definite for all ;

- (ii)

- and are (uniformly) negative definite for all .

Then the control-control pair given in (18) and (29) constitutes the Nash equilibrium of the I-LQ-MF-SZSDG-JD in the sense of (3). Moreover, the optimal game value of the I-LQ-MF-SZSDG-JD is given by .

Proof.

First, note that under (i) and (ii) of the corollary, the following holds:

- (i)

- and are (uniformly) positive definite for all ;

- (ii)

- and are (uniformly) negative definite for all .

That is, under the condition of the corollary, (ii) of Theorems 1 and 2 holds. This implies that (18) and (29) are Nash equilibria of the I-LQ-MF-SZSDG-JD, where the optimal game value is given by . Then from Remark 2, the corollary follows. We complete the proof. □

Remark 3.

From Corollary 1, we are able to obtain the (feedback-type) Nash equilibrium of the I-LQ-MF-SZSDG-JD in the sense of (3). In particular, the steps are as follows:

- (S.1)

- Given the parameters of the MF-SDE with jump diffusions in (1) and the objective functional in (2), check the solvability (existence and uniqueness of the solutions) of the CIRDEs in (6) and (7);

- (S.2)

- If the conditions of (i) and (ii) in Corollary 1 hold, then obtain the Nash equilibrium in given in (18) and (29) by using the parameters in (S.1).

4. Coupled Integro-Riccati Differential Equations: Solvability

In Theorems 1 and 2 and Corollary 1, it is assumed that the CIRDEs in (6) and (7) have unique symmetric bounded solutions. Then Theorems 1 and 2 and Corollary 1 lead to the characterization of the Nash equilibria for the I-LQ-MF-SZSDG-JD under suitable definiteness conditions. Hence, the solvability of the CIRDEs in (6) and (7) is crucial. In this section, we provide different conditions under which CIRDEs in (6) and (7) are uniquely solvable.

It should be noted that the general solvability of the CIRDEs in (6) and (7) is an open problem, which has not been studied in the existing literature. This is because of (i) the local integral term of the Lévy integral due to the jump process, (ii) the indefiniteness of the cost parameters in the objective functional, and (iii) the presence of the conjugate point (the finite-escape time) of the CIRDEs. Regarding (iii), even in the case of a process without jumps, there exists a conjugate point in RDEs in a class of zero-sum differential games, in which case its solution diverges in finite time (([28], Chapter 9) and [29]).

We mention that in [30], the solvability of the IRDE in (6) was discussed when , , , and were (uniformly) positive definite for all . However, this condition cannot be satisfied in the I-LQ-MF-SZSDG-JD. Specifically, assume that and are (uniformly) positive definite for all (equivalently is (uniformly) positive definite), in which case both and are (uniformly) positive definite for all . Hence, we can easily see that (ii) of Corollary 1 does not hold. This implies that we cannot simply impose the definiteness condition of and for the LQ-MF-SZSDG-JD. A similar argument can be applied to the IRDE in (7).

We first state the general existence result for the CIRDEs (6) and (7), which follows from ([31], Corollary 6.7.35)

Proposition 1.

Let us denote the CIRDEs in (6) and (7) as follows:

Suppose that and hold for all . Then implies that there exists a symmetric bounded solution of the CIRDE in (6) on . Furthermore, assume that the CIRDE in (6) admits a unique (symmetric) bounded solution on . If and hold for all and , then there exists a symmetric bounded solution of the CIRDE in (7) on .

Although Proposition 1 provides the general existence result, it is hard to check the conditions in Proposition 1. Below, we provide an easy-to-check condition characterized by the linear matrix inequality (LMI).

Theorem 3.

- (i)

- Suppose that for and . Let be an symmetric positive definite matrix, and . Assume that there exist and such that and . LetwhereIf (equivalently, is uniformly negative definite for all ), then there exists a unique symmetric bounded solution of the CIRDE in (6) on .

- (ii)

- Suppose that for and . Assume that the IRDE in (6) admits a unique symmetric bounded solution on such that is invertible for all . Let be an symmetric positive definite matrix, and . Assume that there exist and such that and . LetwhereIf (equivalently, is uniformly negative definite for all ), then there exists a unique symmetric bounded solution of the CIRDE in (7) on .

Proof.

We prove (ii) only, since the proof for (i) is similar to that of (ii). From ([31], Theorem 3.1.1 and Remark 3.1.1), we can write for , where

with

Note that since (31) is a linear differential equation, there exists a unique solution of (31) on ([32], Theorem 3.2). Below, it is shown that under the condition that is uniformly negative definite for all , is invertible for all .

For any , we define

We can check that and is quadratic in b. Note that

i.e., is positive definite, since , and are positive semidefinite in view of ([27], Theorem 7.2.7).

Then it follows that

which is equivalent to saying that is uniformly negative for all . This follows from the fact that is uniformly negative definite for all . Hence, is a monotonically decreasing function on , and since , we must have for all . From the definition of , this preceding analysis implies that is uniformly positive definite for all . Therefore, is invertible for all , and by the definition of , is invertible for all . This shows that there exists a unique symmetric bounded solution of the CIRDE in (6) on , thereby completing the proof. □

Remark 4.

- (i)

- Note that in Theorem 3, and , , are design parameters, which have to be selected to satisfy the conditions of Theorem 3. In particular, we can easily see that Δ is linear in and , and is linear in and . This implies that and in Theorem 3 can be viewed as LMIs. Hence, the conditions in Theorem 3 become equivalent to identifying the feasibility condition of LMIs via various semidefinite programming algorithms [33].

- (ii)

- If the assumptions of Theorem 3 and Corollary 1 hold, then the control-control pair given in (18) and (29) constitutes the Nash equilibrium of the I-LQ-MF-SZSDG-JD in the sense of (3).

5. Application: Mean-Field-Type Stochastic Mean-Variance Differential Game

This section considers the mean-field-type stochastic mean-variance differential game, for which we apply the main results in Section 3 and Section 4. The market consists of one non-risky and N risky asset stock processes. Specifically, we have the following non-risky asset (deterministic) process:

where for all is the (deterministic) interest rate at time . The qth, , risky asset stock process with jump diffusions can be written as follows:

where is the (deterministic) interest rate of the qth stock process at , which is positive on . Then , describes the dynamics of the complete financial market [34,35,36].

Let , , with be the amount of the Player 1’s wealth, which is invested in the qth stock process in (33). Then according to [34,35,36] (see ([35], Chapter 2.4)), under the assumptions that (i) the N stock processes are continuously traded over , (ii) there are no other expenses such as taxes and transaction costs, and (iii) the market satisfies the self-financing condition, the wealth process x controlled by Player 1 can be written as follows:

where we assume that the risk premium process holds for all and . Then the mean-variance optimization problem (for Player 1) is minimizing

subject to (34). Note that (35) is the one-player single optimization problem.

We consider the modified wealth process of (34), where nature (Player 2), denoted by , , is introduced:

The modified mean-variance problem of (35) now becomes the two-player zero-sum game for jump diffusions:

subject to (36). From Player 1’s perspective, the modified mean-variance problem in (37) corresponds to the worst-case situation by controlled by nature (Player 2), since Player 1 has to compete with nature (Player 2) in order to minimize the mean-variance objective functional. In particular, note that nature (Player 2) maximizes (37). Then Player 1 tries to minimize the worst-case mean-variance objective functional of (37) determined by nature (Player 2).

Let

Then (36) is equivalent to

which shows that the problem in (37) subject to (38) (equivalently (36)) can viewed as a special case of the I-LQ-SZSDG-JD studied in this paper. Hence, we may apply Theorems 1 and 2 and Corollary 1 to characterize explicit Nash equilibria for the mean-field-type stochastic mean-variance differential game of this section.

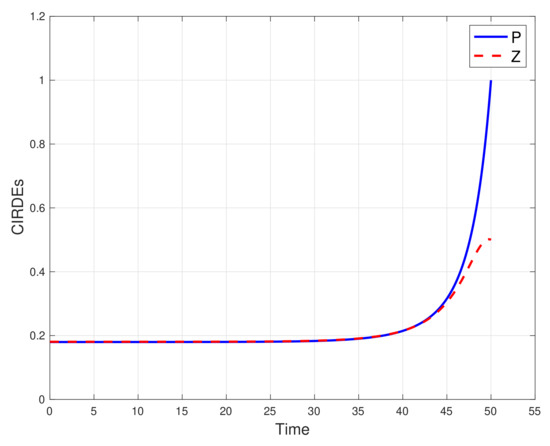

Let us assume that , i.e., the Poisson process has unit jumps, where the jump rate is . Let , , and . Suppose that , , , , , , , , and , where implies that the jump size of the Poisson process is of . Note that the parameters satisfy the conditions of Theorem 3. Now, we use the LMI toolbox in MATLAB, by which it is computed by

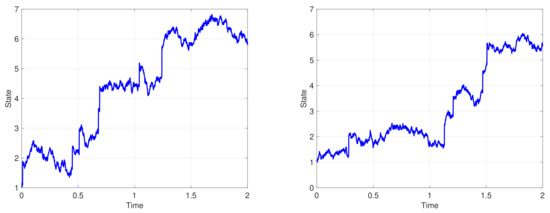

We can easily see that and are symmetric and positive definite. Hence, from Theorem 3, there exist unique bounded solutions of the CIRDEs in (6) and (7) on (note that the CIRDEs in our example are scalar and therefore are symmetric). The evolution of the CIRDEs is shown in Figure 1, which is obtained by the Euler’s method [37]. In Figure 1, we can see that the values of the CIRDEs converge to the steady-state values. This is closely related to the infinite-horizon problem of the I-LQ-MF-SZSDG-JD, which we will study in the near future. From Figure 1 and Theorem 3, we observe that the solutions of the CIRDEs for the modified mean-variance problem of this section are well defined. Hence, (S.1) holds and we are able to characterize the Nash equilibrium in Corollary 1. Specifically, note that (i) and (ii) of Corollary 1 hold, where and . Therefore, (S.2) holds and by Corollary 1, the control-control pair given in (18) and (29) constitutes the Nash equilibrium (in the sense of (3)) for the example of the mean-field-type stochastic mean-variance differential game studied in this section. Finally, the two different controlled same paths of the modified wealth process in (38) (equivalently (36)) under the Nash equilibrium characterized from Corollary 1 are shown in Figure 2. The simulation results are obtained based on the (stochastic) Euler’s method [38]. From Player 1’s perspective, Figure 2 shows the optimal wealth process controlled by Player 1, where Player 1 is completing with nature (Player 2) in order to minimize the worst-case modified mean-variance objective functional in (37).

Figure 1.

The evolution of the coupled integro-Riccati differential equations (CIRDEs) in (6) and (7) for the example of the mean-field-type mean-variance differential game.

Figure 2.

The two different controlled sample paths of the modified wealth process in (38) (equivalently (36)) under the Nash equilibrium for the example of the mean-field-type stochastic mean-variance differential game.

6. Conclusions

We have considered the indefinite, linear-quadratic, mean-field-type stochastic zero-sum differential game for jump-diffusion models (I-LQ-MF-SZSDG-JD), in which the cost parameters do not need to be definite matrices. As mentioned in Section 1, the major challenges of the I-LQ-MF-SZSDG-JD are (i) the inclusion of jump-diffusion processes in the SDE, (ii) the interaction between the players captured by nonanticipative strategies, and (iii) indefiniteness of cost parameters in the objective functional. We have addressed these challenges and characterized the explicit (feedback-type) Nash equilibrium of the LQ-MF-SZSDG-JD by using the completion of squares method and the “ordered interchangeability” property of multiple Nash equilibria in zero-sum games. Note that the Nash equilibrium of the I-LQ-MF-SZSDG-JD is linear in state and characterized by the coupled integro-Riccati differential equations (CIRDEs). We have also provided different solvability conditions of the CIRDEs, by which the Nash equilibrium of the I-LQ-MF-SZSDG-JD can be obtained. We have applied the main results of this paper to the modified mean-field-type stochastic mean-variance optimization problem.

One interesting future research problem is to consider a more general SDE of (1) including the Markov regime-switching jump-diffusion model, which can be viewed as an extension of [12]. Another future research problem would be the case of mean-field-type nonzero-sum differential games for jump-diffusion models including the solvability of the corresponding Riccati equation. This can be viewed as an extension of the results in [11].

Author Contributions

Both authors have contributed equally to this work. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by Institute of Information and Communications Technology Planning and Evaluation (IITP) grant funded by the Korea government (MSIT) (number 2020-0-01373, Artificial Intelligence Graduate School Program (Hanyang University)).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Kac, M. Foundation of Kinetic Theory. In Proceedings of the 3rd Berkeley Symposium on Mathematical Statistics and Probability, Berkeley, CA, USA, 1 January 1956; Volume 3, pp. 171–197. [Google Scholar]

- McKean, H.P. A class of Markov processes associated with nonlinear parabolic equations. Proc. Natl. Acad. Sci. USA 1966, 56, 1907–1911. [Google Scholar] [CrossRef] [PubMed]

- Chan, T. Dynamics of the McKean-Vlasov equation. Ann. Probab. 1994, 22, 431–441. [Google Scholar] [CrossRef]

- Dawson, D.A. Critical dynamics and fluctuations for a mean-field model of cooperative behavior. J. Stat. Phys. 1983, 31, 29–85. [Google Scholar] [CrossRef]

- Graham, G. McKean-Vlasov Ito-Skorohod Equations, and nonlinear diffusions with discrete jump sets. Stoch. Process. Appl. 1992, 40, 69–82. [Google Scholar] [CrossRef]

- Yong, J. Linear-Quadratic Optimal Control Problems for Mean-Field Stochastic Differential Equations. SIAM J. Control Optim. 2013, 51, 2809–2838. [Google Scholar] [CrossRef]

- Shen, Y.; Siu, T.K. The Maximum Principle for a Jump-Diffusion Mean-Field Model and Its Application to the Mean-Variance Problem. Nonlinear Anal. 2013, 86, 58–73. [Google Scholar] [CrossRef]

- Shen, Y.; Meng, Q.; Shi, P. Maximum Principle for Mean-Field Jump-Diffusion Stochastic Delay Differential Equations and Its Application to Finance. Automatica 2014, 50, 1565–1579. [Google Scholar] [CrossRef]

- Meng, Q.; Shen, Y. Optimal Control of Mean-Field Jump-Diffusion Systems with Delay: A Stochastic Maximum Principle Approach. J. Comput. Appl. Math. 2015, 279, 13–30. [Google Scholar] [CrossRef]

- Tang, M.; Meng, Q. Linear-Quadratic Optimal Control Problems for Mean-Field Type Stochastic Differential Equations with Jumps. Asian J. Control 2019, 21, 809–823. [Google Scholar] [CrossRef]

- Barreiro-Gomez, J.; Duncan, T.E.; Tembine, H. Linear-Quadratic Mean-Field-Type Games: Jump-Diffusion Process With Regime Switching. IEEE Trans. Autom. Control 2019, 64, 4329–4336. [Google Scholar] [CrossRef]

- Zhang, X.; Sun, Z.; Xiong, J. A General Stochastic Maximum Principle for a Markov Regime Switching Jump-Diffusion Model of Mean-Field Type. SIAM J. Control Optim. 2018, 56, 2563–2592. [Google Scholar] [CrossRef]

- Benssousan, A.; Djehiche, B.; Tembine, H.; Yam, S.C.P. Mean-Field-Type Games with Jump and Regime Switching. Dyn. Games Appl. 2020, 10, 19–57. [Google Scholar] [CrossRef]

- Moon, J. Linear-quadratic mean field stochastic zero-sum differential games. Automatica 2020, 120. [Google Scholar] [CrossRef]

- Djehiche, B.; Tembine, H.; Tempone, R. A Stochastic Maximum Principle for Risk-Sensitive Mean-Field Type Control. IEEE Trans. Autom. Control 2015, 60, 2640–2649. [Google Scholar] [CrossRef]

- Lasry, J.M.; Lions, P.L. Mean Field Games. Jap. J. Math. 2007, 2, 229–260. [Google Scholar] [CrossRef]

- Tembine, H.; Zhu, Q.; Başar, T. Risk-sensitive Mean Field Games. IEEE Trans. Autom. Control 2014, 59, 835–850. [Google Scholar] [CrossRef]

- Moon, J.; Başar, T. Linear Quadratic Risk-sensitive and Robust Mean Field Games. IEEE Trans. Autom. Control 2017, 62, 1062–1077. [Google Scholar] [CrossRef]

- Duncan, T.E.; Tembine, H. Linear-Quadratic Mean-Field-Type Games: A Direct Method. Games 2018, 9, 7. [Google Scholar] [CrossRef]

- Applebaum, D. Lévy Processes and Stochastic Calculus, 2nd ed.; Cambridge University Press: Cambridge, UK, 2009. [Google Scholar]

- Oksendal, B.; Sulem, A. Applied Stochastic Control of Jump Diffusions, 2nd ed.; Springer: Berlin, Germany, 2006. [Google Scholar]

- Buckdahn, R.; Li, J. Stochastic Differential Games and Viscosity Solutions of Hamilton-Jabobi-Bellman-Isaacs Equations. SIAM J. Control Optim. 2008, 47, 444–475. [Google Scholar] [CrossRef]

- Yu, Z. An Optimal Feedback Control-Strategy Pair For Zero-Sum Linear-Quadratic Stochastic Differential Game: The Riccati Equation Approach. SIAM J. Control Optim. 2015, 53, 2141–2167. [Google Scholar] [CrossRef]

- Fleming, W.H.; Souganidis, P.E. On the Existence of Value Functions of Two-Player Zero-Sum Stochastic Differential Game. Indiana Univ. Math. J. 1989, 38, 293–314. [Google Scholar] [CrossRef]

- Başar, T.; Olsder, G.J. Dynamic Noncooperative Game Theory, 2nd ed.; SIAM: Philadelphia, PA, USA, 1999. [Google Scholar]

- Buckdahn, R.; Cardaliaguet, P.; Rainer, C. Nash Equilibrium Payoffs for Nonzero-Sum Stochastic Differential Games. SIAM J. Control Optim. 2004, 43, 624–642. [Google Scholar] [CrossRef]

- Horn, R.A.; Johnson, C.R. Matrix Analysis, 2nd ed.; Cambridge University Press: Cambridge, UK, 2013. [Google Scholar]

- Başar, T.; Bernhard, P. H∞ Optimal Control and Related Minimax Design Problems, 2nd ed.; Birkhäuser: Boston, MA, USA, 1995. [Google Scholar]

- Moon, J.; Kim, Y. Linear Exponential Quadratic Control for Mean Field Stochastic Systems. IEEE Trans. Autom. Control 2019, 64, 5094–5100. [Google Scholar] [CrossRef]

- Zhang, F.; Dong, Y.; Meng, Q. Backward Stochastic Riccati Equation with Jumps Associated with Stochastic Linear Quadratic Optimal Control with Jumps and Random Coefficients. SIAM J. Control Optim. 2020, 58, 393–424. [Google Scholar] [CrossRef]

- Abou-Kandil, H.; Freiling, G.; Ionescu, V.; Jank, G. Matrix Riccati Equations in Control and Systems Theory; Springer: Basel, Switzerland, 2003. [Google Scholar]

- Khalil, H.K. Nonlinear Systems, 3rd ed.; Prentice Hall: Upper Saddle River, NJ, USA, 2002. [Google Scholar]

- Boyd, S.; Ghaoui, E.; Feron, E.; Balakrishnan, B. Linear Matrix Inequalities in Systems and Control Theory; SIAM: Philadelphia, PA, USA, 1994. [Google Scholar]

- Shreve, S. Stochastic Calculus for Finance II: Continuous-Time Models; Springer: New York, NY, USA, 2004. [Google Scholar]

- Touzi, N. Optimal Stochastic Control, Stochastic Target Problems, and Backward SDE; Springer: New York, NY, USA, 2013. [Google Scholar]

- Zhou, X.Y.; Li, D. Continuous-Time Mean-Variance Portfolio Selection: A Stochastic LQ Framework. Appl. Math. Optim. 2000, 42, 19–33. [Google Scholar] [CrossRef]

- Kahaner, D.; Moler, C.; Nash, S. Numerical Methods and Software; Prentice Hall: Englewood Cliffs, NJ, USA, 1989. [Google Scholar]

- Hanson, F.B. Applied Stochastic Processes and Control for Jump-Diffusions; SIAM: Philadelphia, PA, USA, 2007. [Google Scholar]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).