Asymptotically Normal Estimators of the Gerber-Shiu Function in Classical Insurance Risk Model

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Preliminaries

- , , .

- .

- denotes the Laplace transform of claim size density f,

- denotes the characteristic function of random vector , where t is a random vector in , .

- For , let be the scalar product and be -norm.

- For positive function , let be , where C is a positive constant.

- ⊤ means the transpose of matrix.

- is a zero vector.

- Let be convergence in probability and be convergence in distribution.

- means that for some constant C.

- Condition 1 The premium rate ;

- Condition 2 Suppose that

- Condition 3 For some , suppose that the penalty function

2.1. Laguerre Expansion of Gerber-Shiu Function

- form a complete orthogonal basis over . Then, when , it can be expanded by the Laguerre function:

- are uniformly bounded, i.e.

- , , and for .

2.2. Coefficient and

2.3. Statistical Inference

3. Asymptotically Normality

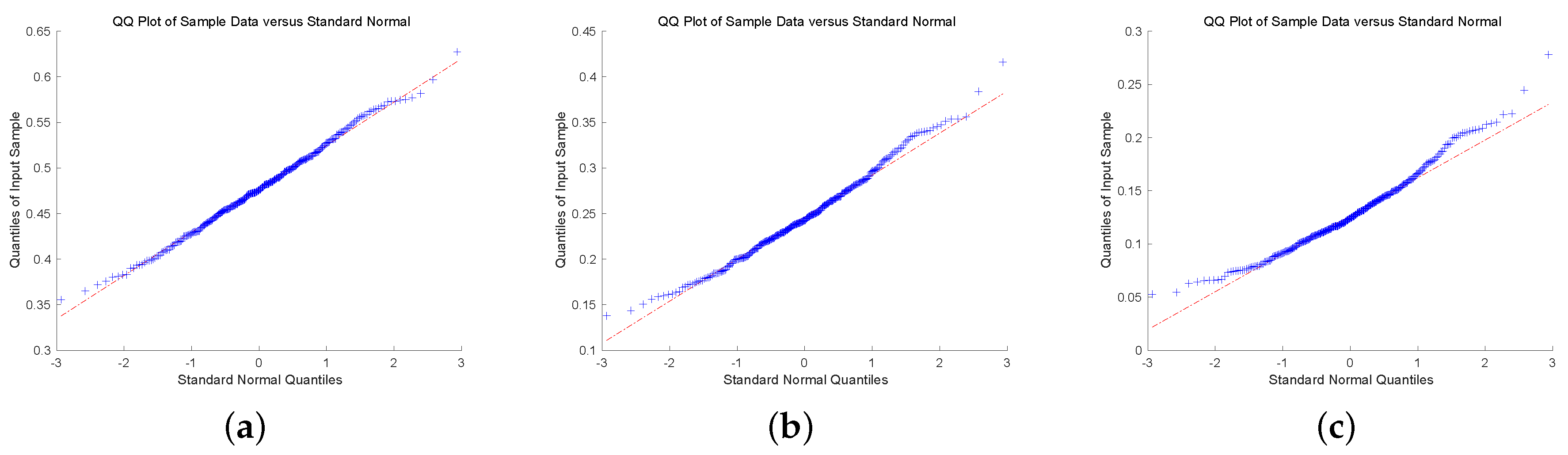

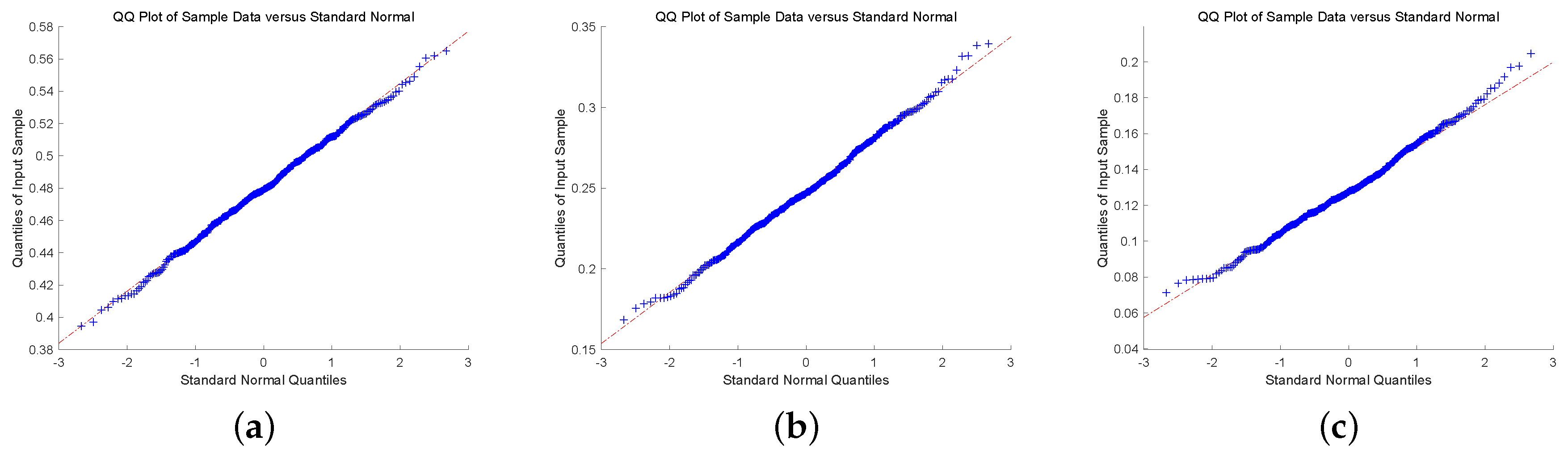

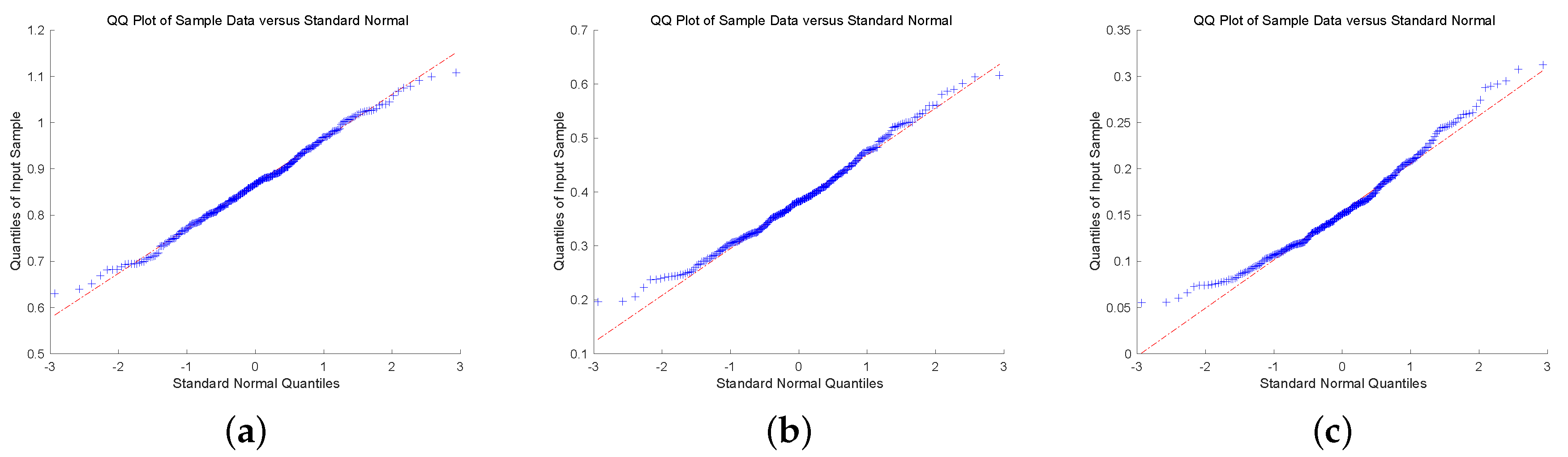

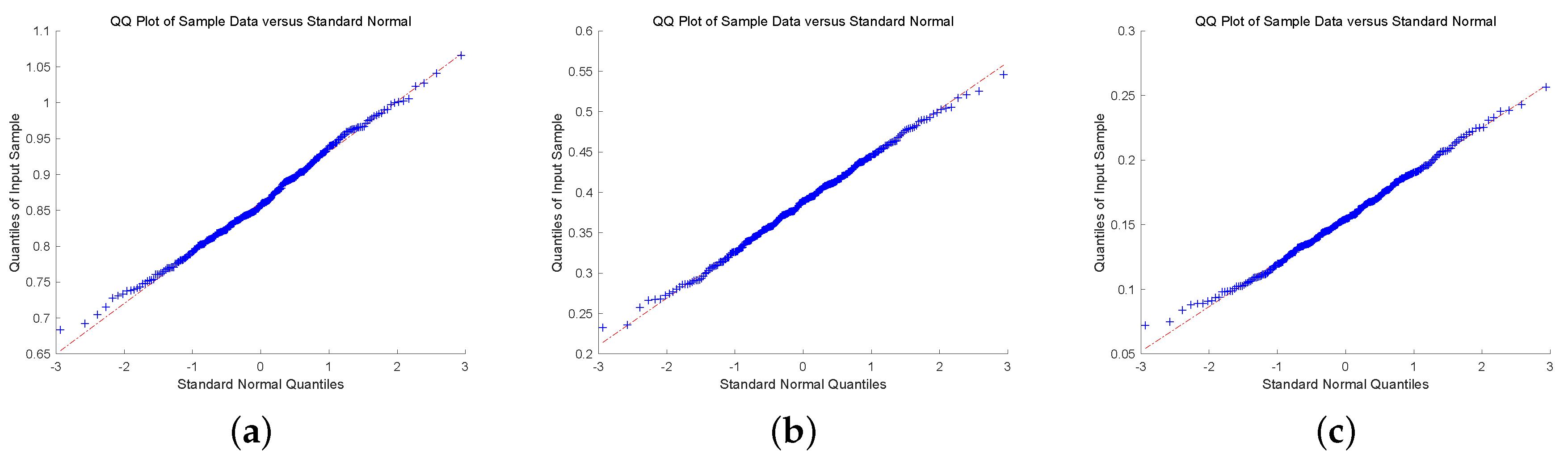

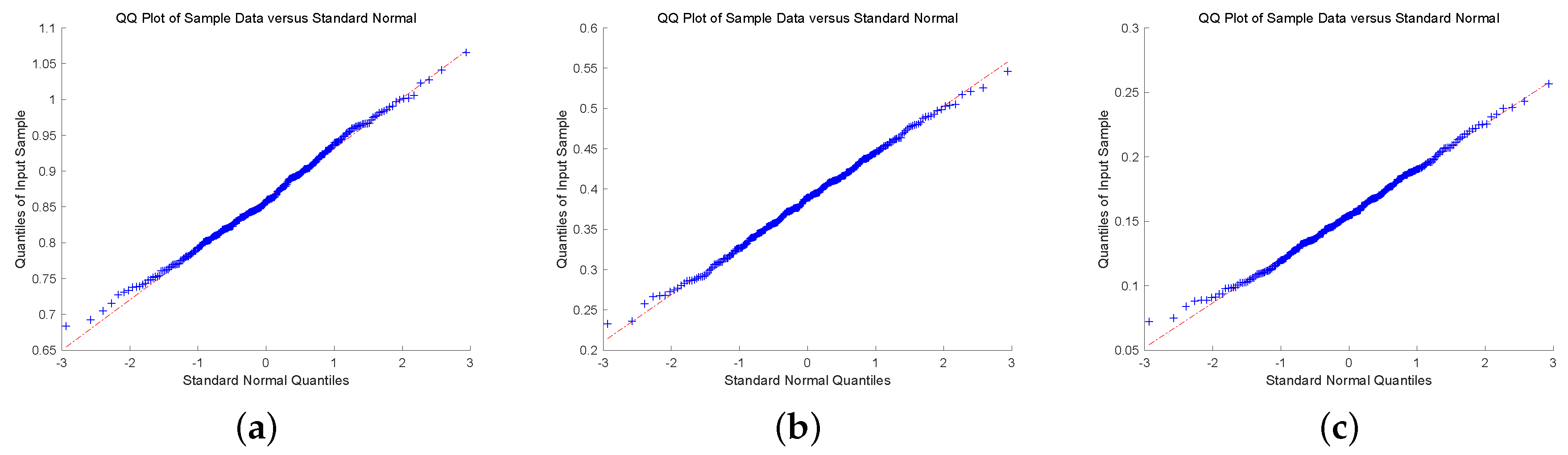

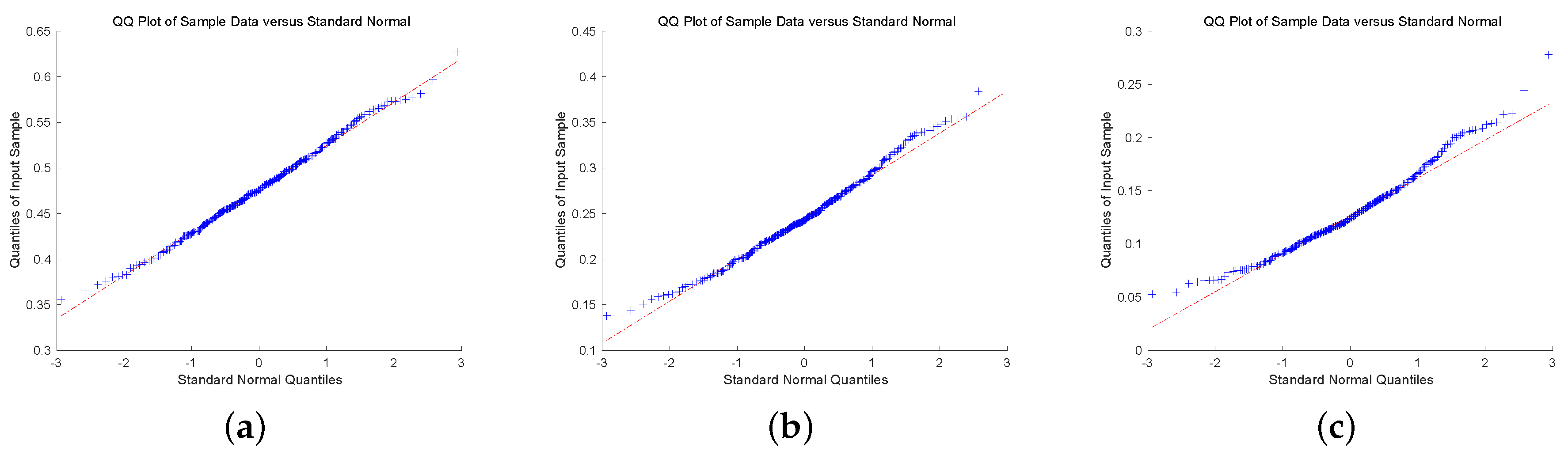

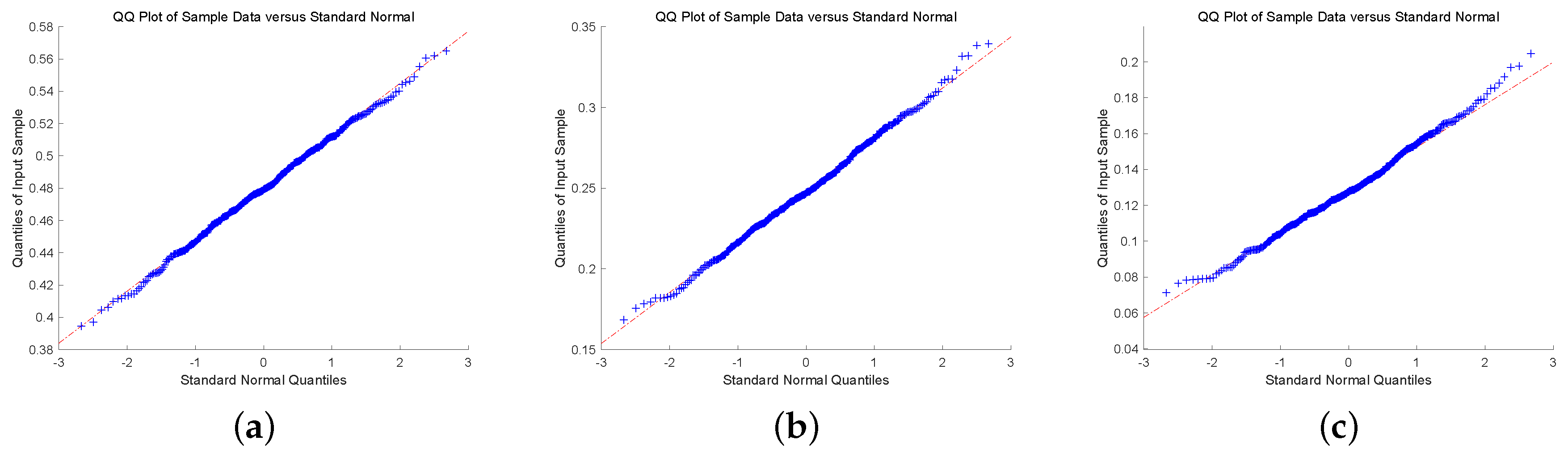

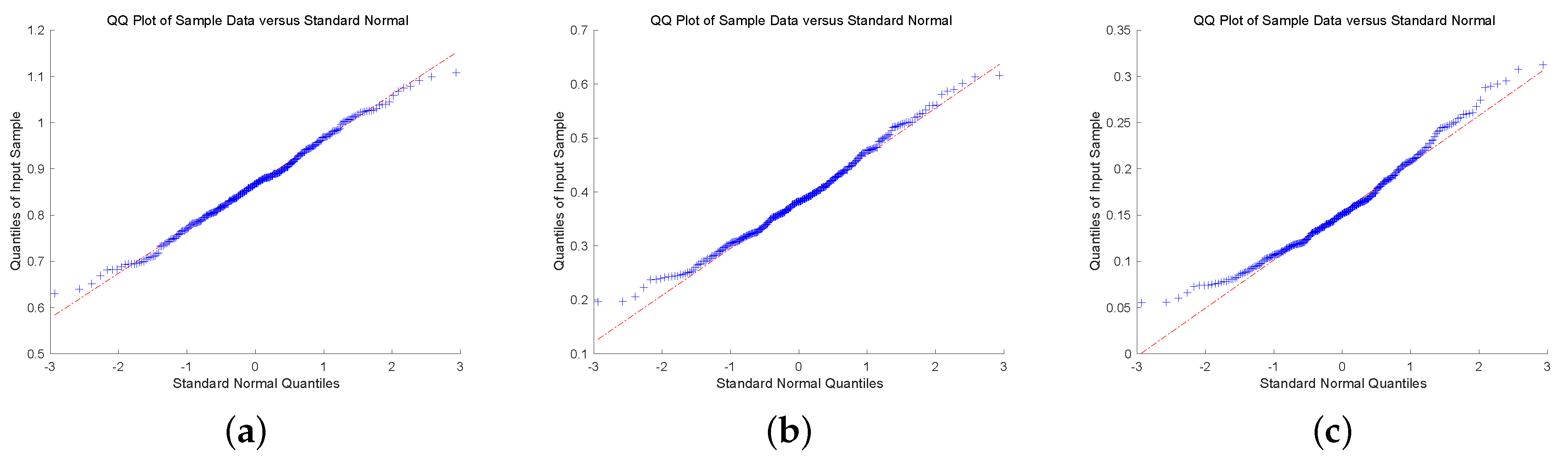

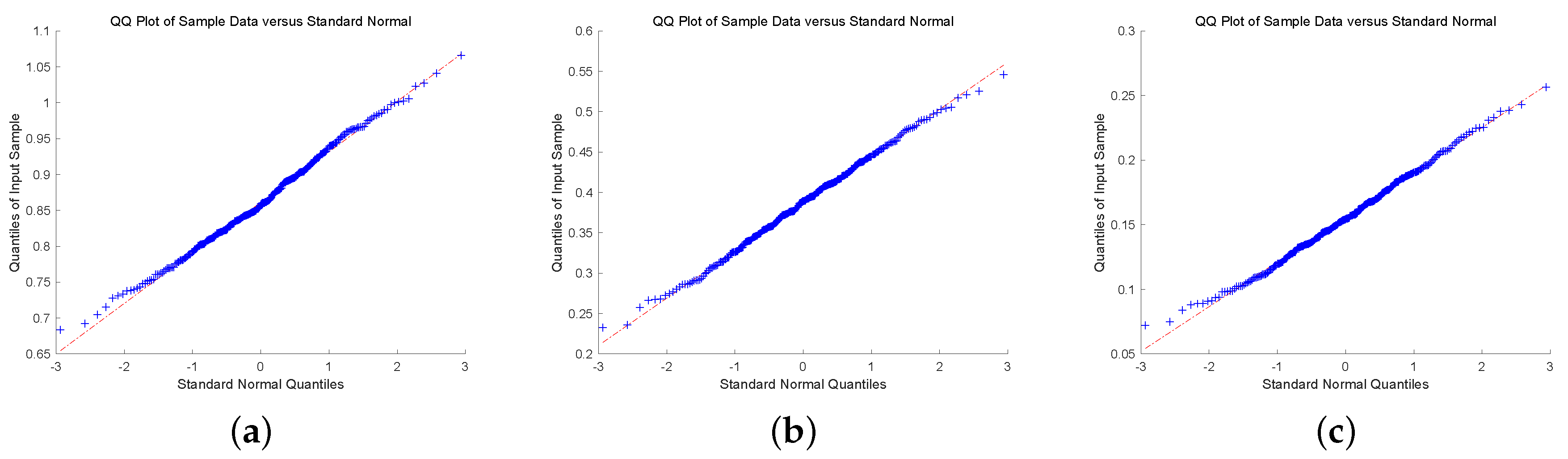

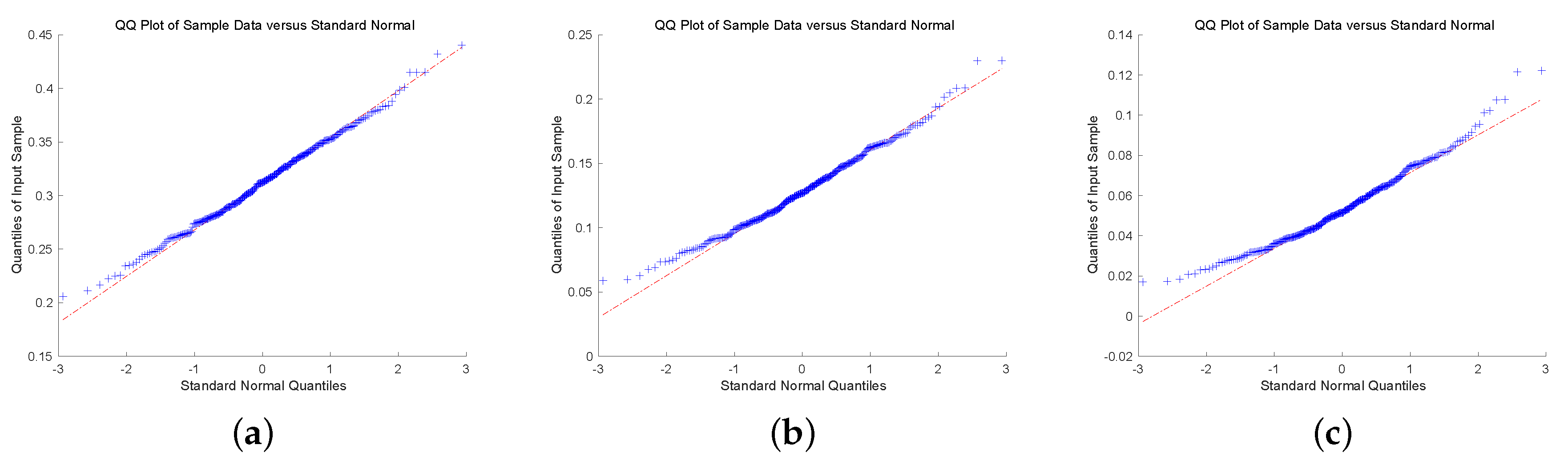

4. Simulation

- Exponential: ;

- Erlang(2): ;

- Combination-of-exponentials: .

- Ruin probability (RP);

- Expected claim size causing ruin (ECS);

- Expected deficit at ruin (ED).

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Gerber, H.U.; Shiu, E.S.W. On the time value of ruin. N. Am. Actuar. J. 1998, 2, 48–78. [Google Scholar] [CrossRef]

- Asmussen, S.; Albrecher, H. Ruin Probabilities, 2nd ed.; World Scientific: Singapore, 2010. [Google Scholar]

- Gerber, H.U.; Landry, B. On the discounted penalty at ruin in a jump-diffusion and the perpetual put option. Insur. Math. Econ. 1998, 22, 263–276. [Google Scholar] [CrossRef]

- Tsai, C.C.L. On the discounted distribution functions of the surplus process perturbed by diffusion. Insur. Math. Econ. 2001, 28, 401–419. [Google Scholar] [CrossRef]

- Tsai, C.C.L. On the expectations of the present values of the time of ruin perturbed by diffusion. Insur. Math. Econ. 2003, 32, 413–429. [Google Scholar] [CrossRef]

- Yu, W.G. Some results on absolute ruin in the perturbed insurance risk model with investment and debit interests. Econ. Model. 2013, 31, 625–634. [Google Scholar] [CrossRef]

- Yu, W.G.; Huang, Y.J.; Cui, C.R. The absolute ruin insurance risk model with a threshold dividend strategy. Symmetry 2018, 10, 377. [Google Scholar] [CrossRef] [Green Version]

- Zhao, X.H.; Yin, C.C. The Gerber-Shiu expected discounted penalty function for Lévy insurance risk processes. Acta Math. Appl. Sin. 2010, 26, 575–586. [Google Scholar] [CrossRef]

- Xie, J.H.; Zou, W. On the expected discounted penalty function for the compound Poisson risk model with delayed claims. J. Comput. Appl. Math. 2011, 235, 2392–2404. [Google Scholar] [CrossRef]

- Zhu, H.M.; Huang, Y.; Yang, X.Q.; Zhou, J.M. On the expected discounted penalty function for the classical risk model with potentially delayed claims and random incomes. J. Appl. Math. 2014, 2014, 717269. [Google Scholar] [CrossRef] [Green Version]

- Yin, C.C.; Wang, C.W. The perturbed compound Poisson risk process with investment and debit Interest. Methodol. Comput. Appl. 2010, 12, 391–413. [Google Scholar] [CrossRef]

- Shen, Y.; Yin, C.C.; Yuen, K.C. Alternative approach to the optimality of the threshold strategy for spectrally negative Lévy processes. Acta Math. Appl. Sin. 2013, 29, 705–716. [Google Scholar] [CrossRef] [Green Version]

- Yin, C.C.; Yuen, K.C. Exact joint laws associated with spectrally negative Lévy processes and applications to insurance risk theory. Front. Math. China 2014, 9, 1453–1471. [Google Scholar] [CrossRef] [Green Version]

- Cai, C.; Chen, N.; You, H. Nonparametric estimation for a spectrally negative Lévy risk process based on low-frequency observation. J. Comput. Appl. Math. 2018, 328, 432–442. [Google Scholar] [CrossRef]

- Deng, Y.C.; Liu, J.; Huang, Y.; Li, M.; Zhou, J.M. On a discrete interaction risk model with delayed claims and stochastic incomes under random discount rates. Commun. Stat. Theory Methods 2018, 47, 5867–5883. [Google Scholar] [CrossRef]

- Dong, H.; Yin, C.C.; Dai, H.S. Spectrally negative Lévy risk model under Erlangized barrier strategy. J. Comput. Appl. Math. 2019, 351, 101–116. [Google Scholar] [CrossRef]

- Wang, W.Y.; Zhang, Z.M. Computing the Gerber-Shiu function by frame duality projection. Scand. Actuar. J. 2019, 2019, 291–307. [Google Scholar] [CrossRef]

- Yu, W.G.; Guo, P.; Wang, Q.; Guan, G.F.; Yang, Q.; Huang, Y.J.; Yu, X.L.; Jin, B.Y.; Cui, C.R. On a periodic capital injection and barrier dividend strategy in the compound Poisson risk model. Mathematics 2020, 8, 511. [Google Scholar] [CrossRef] [Green Version]

- Peng, X.H.; Su, W.; Zhang, Z.M. On a perturbed compound Poisson risk model under a periodic threshold-type dividend strategy. J. Ind. Manag. Optim. 2020, 16, 1967–1986. [Google Scholar] [CrossRef]

- Shimizu, Y. Nonparametric estimation of the Gerber-Shiu function for the Winer-Poisson risk model. Scand. Actuar. J. 2012, 1, 56–69. [Google Scholar] [CrossRef]

- Zhang, Z.M.; Yang, H.L. Nonparametric estimate of the ruin probability in a pure-jump Lévy risk model. Insur. Math. Econ. 2013, 53, 24–35. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Z.M.; Yang, H.L. Nonparametric estimation for the ruin probability in a Lévy risk model under low-frequency observation. Insur. Math. Econ. 2014, 59, 168–177. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Z.M. Estimating the Gerber-Shiu function by Fourier-Sinc series expansion. Scand. Actuar. J. 2017, 10, 898–919. [Google Scholar] [CrossRef]

- Zhang, Z.M. Nonparametric estimation of the finite time ruin probability in the classical risk model. Scand. Actuar. J. 2017, 5, 452–469. [Google Scholar] [CrossRef]

- Zhang, Z.M.; Su, W. A new efficient method for estimating the Gerber-Shiu function in the classical risk model. Scand. Actuar. J. 2018, 5, 426–449. [Google Scholar] [CrossRef]

- Shimizu, Y.; Zhang, Z.M. Asymptotically normal estimators of the ruin probability for Lévy insurance surplus from discrete samples. Risks 2019, 7, 37. [Google Scholar] [CrossRef] [Green Version]

- Yu, W.G.; Wang, F.; Huang, Y.J.; Liu, H.D. Social optimal mean field control problem for population growth model. Asian J. Control 2019, 1–8. [Google Scholar] [CrossRef]

- Peng, J.Y.; Wang, D.C. Uniform asymptotics for ruin probabilities in a dependent renewal risk model with stochastic return on investments. Stochastics 2018, 90, 432–471. [Google Scholar] [CrossRef]

- Yu, W.G.; Yong, Y.D.; Guan, G.F.; Huang, Y.J.; Su, W.; Cui, C.R. Valuing guaranteed minimum death benefits by cosine series expansion. Mathematics 2019, 7, 835. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Z.M.; Yong, Y.D.; Yu, W.G. Valuing equity-linked death benefits in general exponential Lévy models. J. Comput. Appl. Math. 2020. [Google Scholar] [CrossRef]

- Abramowitz, M.; Stegun, I.A. Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables; National Bureau of Standards Applied Mathematics Series; US Government Printing Office: Washington, DC, USA, 1964.

- Cinlar, E. Probability and Stochastics; Springer: New York, NY, USA, 2015. [Google Scholar]

- Van Der Vaart, A.W. Asymptotic Statistics; Cambridge University Press: Cambridge, UK, 1998. [Google Scholar]

- Bongioanni, B.; Torrea, J.L. What is a Sobolev space for the Laguerre function system? Studia Math. 2009, 192, 147–172. [Google Scholar] [CrossRef] [Green Version]

- Dickson, D.C.M. Insurance Risk and Ruin; Cambridge University Press: Cambridge, UK, 2006. [Google Scholar]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Su, W.; Yu, W. Asymptotically Normal Estimators of the Gerber-Shiu Function in Classical Insurance Risk Model. Mathematics 2020, 8, 1638. https://doi.org/10.3390/math8101638

Su W, Yu W. Asymptotically Normal Estimators of the Gerber-Shiu Function in Classical Insurance Risk Model. Mathematics. 2020; 8(10):1638. https://doi.org/10.3390/math8101638

Chicago/Turabian StyleSu, Wen, and Wenguang Yu. 2020. "Asymptotically Normal Estimators of the Gerber-Shiu Function in Classical Insurance Risk Model" Mathematics 8, no. 10: 1638. https://doi.org/10.3390/math8101638

APA StyleSu, W., & Yu, W. (2020). Asymptotically Normal Estimators of the Gerber-Shiu Function in Classical Insurance Risk Model. Mathematics, 8(10), 1638. https://doi.org/10.3390/math8101638