Granular Fuzzy Fractional Financial Systems Governed by Granular Caputo Fractional Derivative

Abstract

1. Introduction

1.1. Motivation and Contribution

1.2. Fundamental Difference Between Fuzzy and Stochastic Modeling

1.3. Model Formulation

2. Basic Concepts

Granular Laplace Transform for FVFs

3. The Existence and Uniqueness of the Fuzzy Solution to the GFFFS Under -CFD

- (HF − I)

- The functions and are measurable and continuous for each , respectively.

- (HF − II)

- There exists such that for every .

- (HF − III)

- There exists such that

- (HF − VI)

- There exists such that

- The supremum metric

- Step-1:

- The operator is onto itself. Indeed, for every and , we have

- Step-2:

- The operator is continuous. In fact, let be such that . Then,

- For each and employing hypotheses (, we haveBy applying Lebesgue’s dominated theorem, we obtainas , and hence is continuous on .

- Step-3:

- Next, we need to demonstrate that is a contraction mapping. To do this, let . It is sufficient to demonstrate the existence of a constant satisfying

- Infect, for every , it holds that:By dividing both sides by and taking the supremum over , we obtainIt is important to note that for sufficiently large , we have . This implies that is a contraction. Finally, employing the Banach contraction principle, we have the unique fixed point as the mild solution of the system (22). □

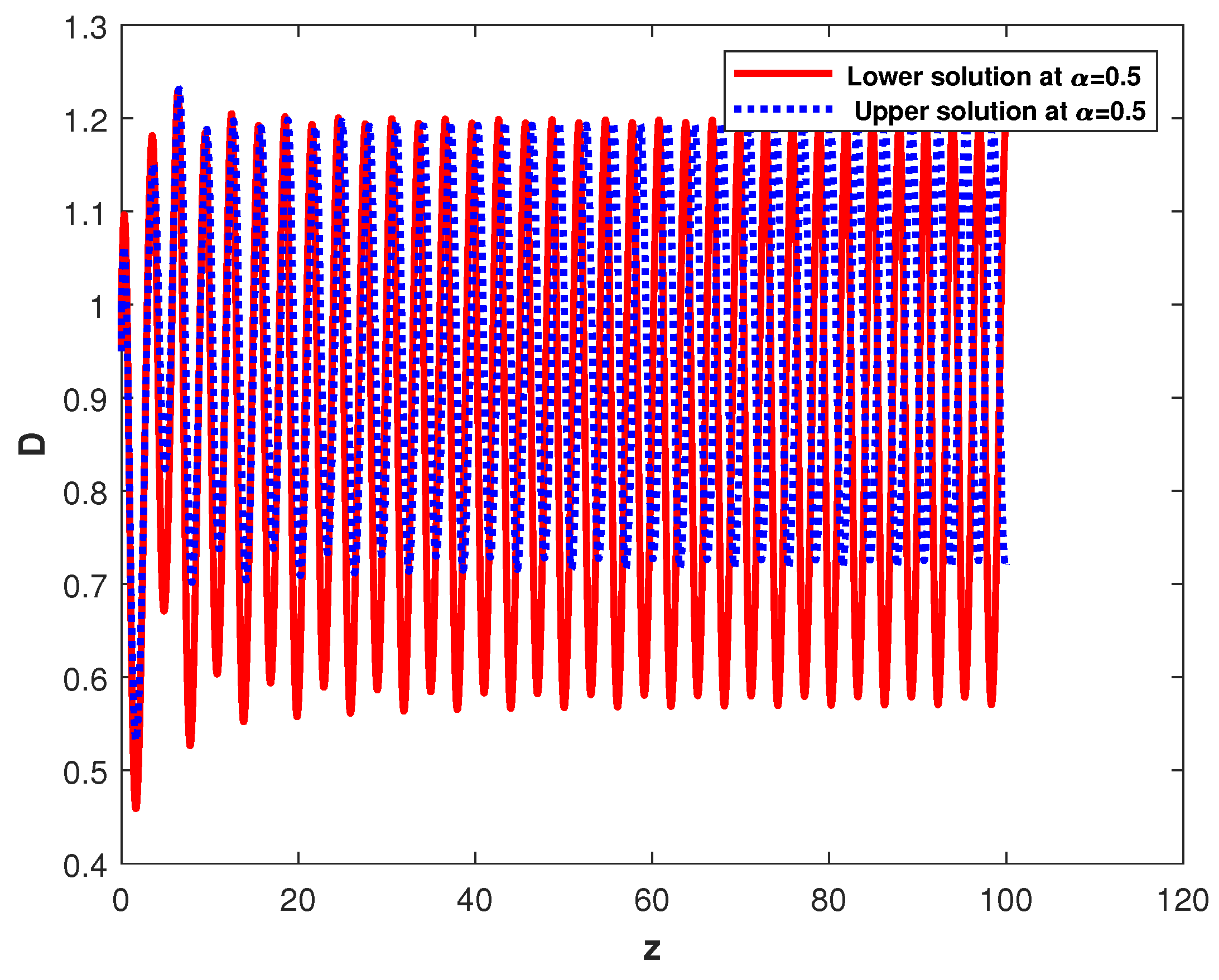

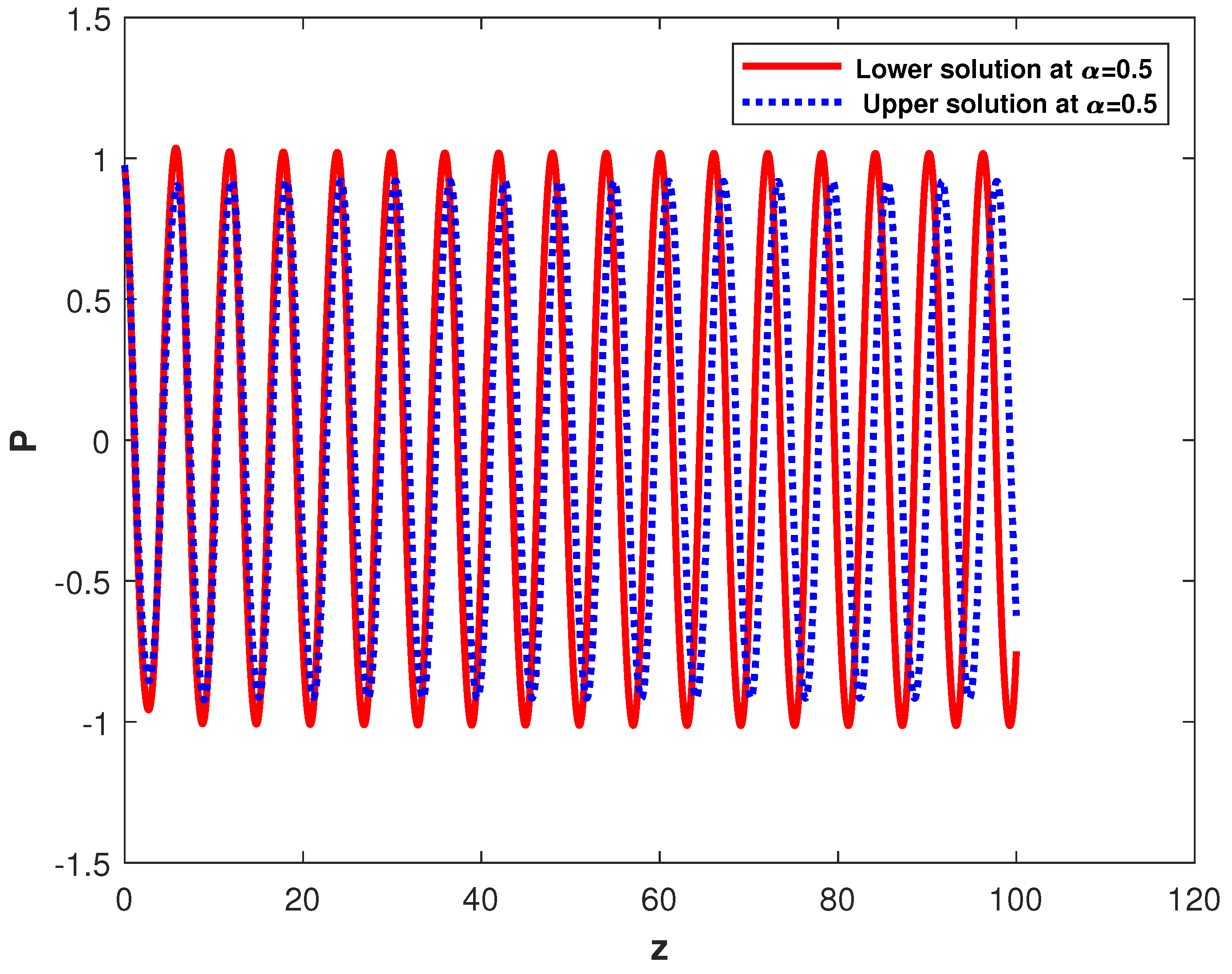

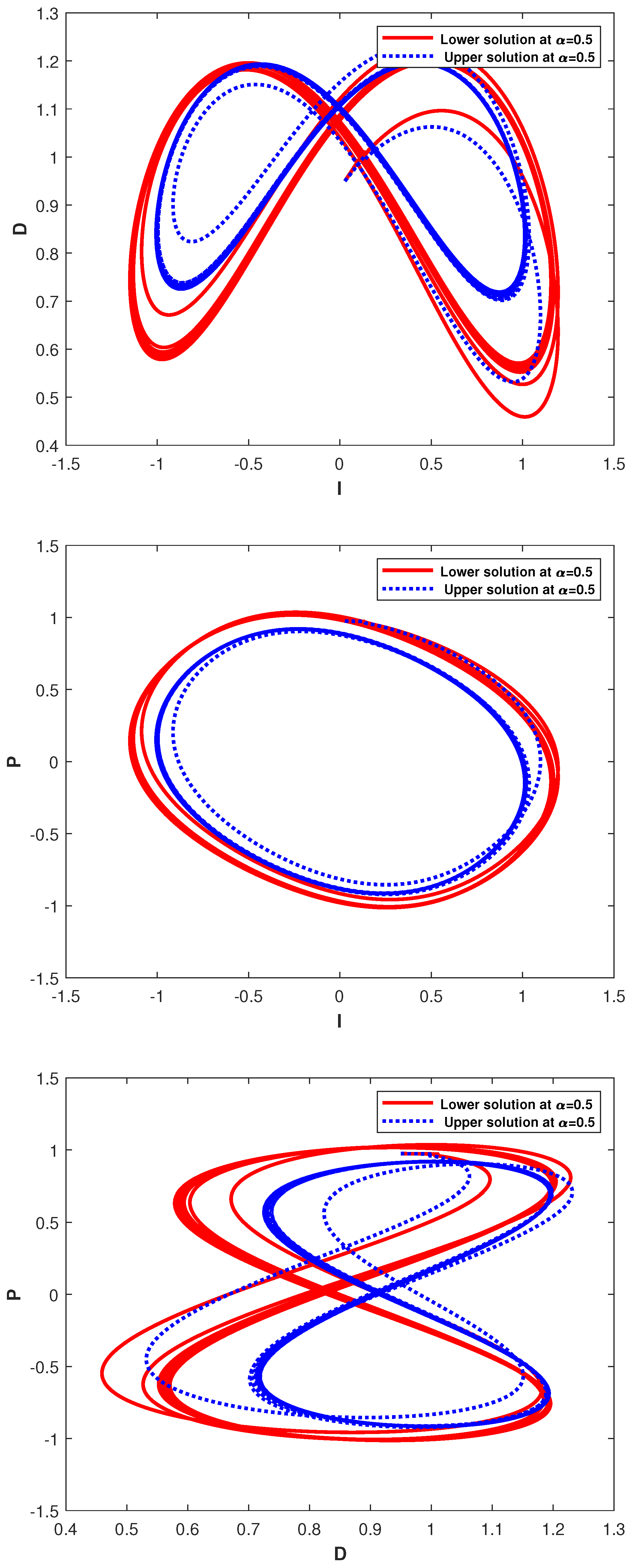

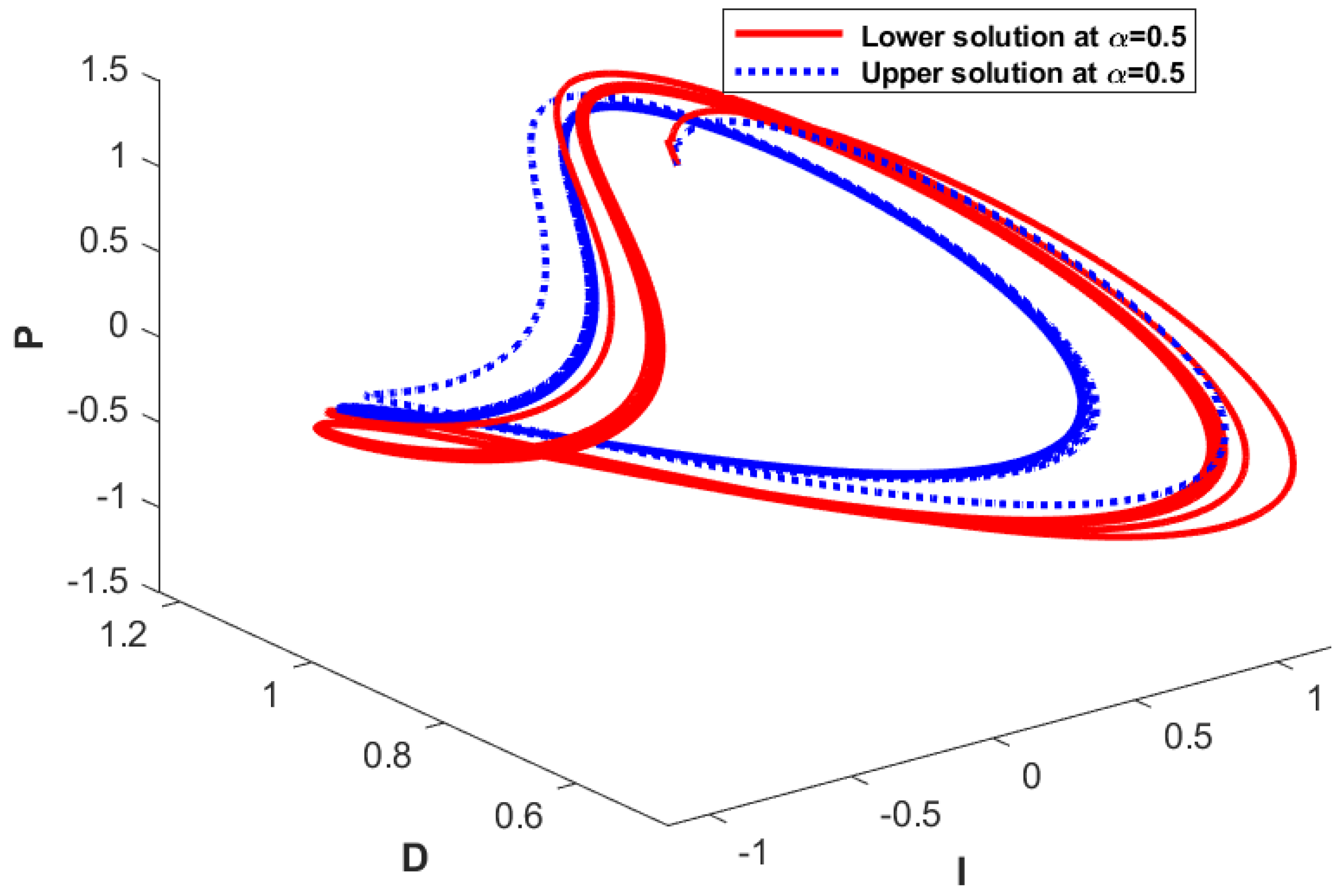

4. Numerical Solution of the GFFFS

4.1. Approximate Solution of FFFS (4) with FICs (5)

| Algorithm 1: Numerical algorithm |

| Input: The fractional-order , number of partitions N, model parameters, the initial and final time, and the fuzzy initial conditions |

| Output: The approximate solution of the GFFF (41) |

| Initialization; |

| ; ; // starting and ending point |

| ; // step size |

| ; ; ; // The solution vector |

| ; // Numerical solution of the system (41) |

| for do |

|

| ; // plot the numerical solution |

4.2. Error Estimation of the Proposed Numerical Technique

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Dubois, D.; Prade, H. Towards fuzzy differential calculus part 3: Differentiation. Fuzzy Sets Syst. 1982, 8, 225–233. [Google Scholar] [CrossRef]

- Akram, M.; Muhammad, G.; Allahviranloo, T.; Pedrycz, W. Solution of initial-value problem for linear third-order fuzzy differential equations. Comput. Appl. Math. 2022, 41, 398. [Google Scholar] [CrossRef]

- Muhammad, G.; Akram, M. Fuzzy fractional epidemiological model for Middle East respiratory syndrome coronavirus on complex heterogeneous network using Caputo derivative. Inf. Sci. 2024, 659, 120046. [Google Scholar] [CrossRef]

- Ahmad, S.; Ullah, A.; Ullah, A.; Hoa, N.V. Fuzzy natural transform method for solving fuzzy differential equations. Soft Comput. 2023, 27, 8611–8625. [Google Scholar] [CrossRef]

- Akram, M.; Muhammad, G.; Allahviranloo, T. Explicit analytical solutions of an incommensurate system of fractional differential equations in a fuzzy environment. Inf. Sci. 2023, 645, 119372. [Google Scholar] [CrossRef]

- Akram, M.; Muhammad, G.; Allahviranloo, T.; Pedrycz, W. Incommensurate non-homogeneous system of fuzzy linear fractional differential equations using the fuzzy bunch of real functions. Fuzzy Sets Syst. 2023, 473, 108725. [Google Scholar] [CrossRef]

- Allahviranloo, T.; Ahmadi, M.B. Fuzzy Laplace transforms. Soft Comput. 2010, 14, 235–243. [Google Scholar] [CrossRef]

- Effati, S.; Pakdaman, M. Artificial neural network approach for solving fuzzy differential equations. Inf. Sci. 2010, 180, 1434–1457. [Google Scholar] [CrossRef]

- Muhammad, G.; Akram, M. Fuzzy fractional generalized Bagley-Torvik equation with fuzzy Caputo gH-differentiability. Eng. Appl. Artif. Intell. 2024, 133, 108265. [Google Scholar] [CrossRef]

- Mazandarani, M.; Pan, J. The challenges of modeling using fuzzy standard interval arithmetic: A case study in electrical engineering. Inf. Sci. 2024, 653, 119774. [Google Scholar] [CrossRef]

- Mazandarani, M.; Pariz, N.; Kamyad, A.V. Granular differentiability of fuzzy-number-valued functions. IEEE Trans. Fuzzy Syst. 2017, 26, 310–323. [Google Scholar] [CrossRef]

- Chalco-Cano, Y.; Roman-Flores, H. On new solutions of fuzzy differential equations. Chaos Solitons Fractals 2008, 38, 112–119. [Google Scholar] [CrossRef]

- Nabulsi, R.A.E.; Anukool, W. Qualitative financial modelling in fractal dimensions. Financ. Innov. 2025, 11, 42. [Google Scholar] [CrossRef]

- Nikan, O.; Rashidinia, J.; Jafari, H. Numerically pricing American and European options using a time fractional Black–Scholes model in financial decision-making. Alex. Eng. J. 2025, 112, 235–245. [Google Scholar] [CrossRef]

- Ahmad, I.; Jan, R.; Razak, N.N.A.; Khan, A.; Abdeljawad, T. Exploring Fractional-Order Models in Computational Finance via an Efficient Hybrid Approach. Eur. J. Pure Appl. Math. 2025, 18, 5793. [Google Scholar] [CrossRef]

- Selvam, A.; Boulaaras, S.; Sabarinathan, S.; Radwan, T. Nonlinear fractional order financial system: Chaotic behavior and Ulam-Hyers stability. Fractals 2025, 33, 11–22. [Google Scholar] [CrossRef]

- Bozkurt, M.A.; Köse, Y.; Çelik, S. Analyzing the dynamic behavior and market efficiency of green energy investments: A geometric and fractional brownian motion approach. Energy Sources Part B Econ. Plan. Policy 2025, 20, 2457438. [Google Scholar] [CrossRef]

- Akgüller, Ö.; Balcı, M.A.; Batrancea, L.M.; Gaban, L. Fractional Transfer Entropy Networks: Short-and Long-Memory Perspectives on Global Stock Market Interactions. Fractal Fract. 2025, 9, 69. [Google Scholar] [CrossRef]

- Bai, Y.; Kehoe, P.J.; Lopez, P.; Perri, F. A Neoclassical Model of the World Financial Cycle; Technical report; National Bureau of Economic Research: Cambridge, MA, USA, 2025. [Google Scholar]

- Kumar, S.; ElKholy, M.; Liu, D.; Boulenger, A. Bridging the Gap: Efficient Cross-Lingual NER in Low-Resource Financial Domain. In Proceedings of the Joint Workshop of the 9th Financial Technology and Natural Language Processing, the 6th Financial Narrative Processing, and the 1st Workshop on Large Language Models for Finance and Legal, Abu Dhabi, United Arab Emirates, 19–20 January 2025; pp. 54–62. [Google Scholar]

- Shone, R. Economic Dynamics: Phase Diagrams and Their Economic Application; Cambridge University Press: Cambridge, UK, 2002. [Google Scholar]

- Chian, A.C.L.; Rempel, E.L.; Rogers, C. Complex economic dynamics: Chaotic saddle, crisis and intermittency. Chaos Solitons Fractals 2006, 29, 1194–1218. [Google Scholar] [CrossRef]

- Wang, Z.; Huang, X.; Shi, G. Analysis of nonlinear dynamics and chaos in a fractional order financial system with time delay. Comput. Math. Appl. 2011, 62, 1531–1539. [Google Scholar] [CrossRef]

- Elouahab, M.S.A.; Hamri, N.E.; Wang, J. Chaos control of a fractional-order financial system. Math. Probl. Eng. 2010, 18, 270646. [Google Scholar] [CrossRef]

- Johansyah, M.D.; Sambas, A.; Qureshi, S.; Zheng, S.; Elhameed, T.M.A.; Vaidyanathan, S.; Sulaiman, I.M. Investigation of the hyperchaos and control in the fractional order financial system with profit margin. Partial. Differ. Equ. Appl. Math. 2024, 9, 100612. [Google Scholar] [CrossRef]

- Olayiwola, M.O.; Alaje, A.I.; Yunus, A.O. A Caputo fractional order financial mathematical model analyzing the impact of an adaptive minimum interest rate and maximum investment demand. Results Control. Optim. 2024, 14, 100349. [Google Scholar] [CrossRef]

- Li, S.; Khan, S.; Riaz, M.; AlQahtani, S.; Alamri, A. Numerical simulation of a fractional stochastic delay differential equations using spectral scheme: A comprehensive stability analysis. Sci. Rep. 2024, 14, 6930. [Google Scholar] [CrossRef]

- Qayyum, M.; Ahmad, E.; Saeed, S.T.; Akgül, A.; Din, S.M.E. New solutions of fractional 4d chaotic financial model with optimal control via he-laplace algorithm. Ain Shams Eng. J. 2024, 15, 102503. [Google Scholar] [CrossRef]

- Pakhira, R.; Mondal, B.; Ghosh, U.; Sarkar, S. An EOQ model with fractional order rate of change of inventory level and time-varying holding cost. Soft Comput. 2024, 28, 3859–3877. [Google Scholar] [CrossRef]

- Liu, X.; Ye, G.; Liu, W.; Shi, F. Fuzzy discrete fractional granular calculus and its application to fractional cobweb models. Appl. Math. Comput. 2025, 489, 129176. [Google Scholar] [CrossRef]

- Xu, X.; Wang, L.; Du, Z.; Kao, Y. H∞ sampled-data control for uncertain fuzzy systems under Markovian jump and FBm. Appl. Math. Comput. 2023, 451, 128014. [Google Scholar] [CrossRef]

- Xu, K.; Wang, H.; Liu, P. Adaptive fuzzy finite-time tracking control of nonlinear systems with unmodeled dynamics. Appl. Math. Comput. 2023, 450, 127992. [Google Scholar] [CrossRef]

- Ali, M.; Narayanan, G.; Shekher, V.; Alsulami, H.; Saeed, T. Dynamic stability analysis of stochastic fractional-order memristor fuzzy BAM neural networks with delay and leakage terms. Appl. Math. Comput. 2020, 369, 124896. [Google Scholar]

- Song, S.; Park, J.; Zhang, B.; Song, X. Adaptive hybrid fuzzy output feedback control for fractional-order nonlinear systems with time-varying delays and input saturation. Appl. Math. Comput. 2020, 364, 124662. [Google Scholar] [CrossRef]

- Xu, Z.; Sun, K.; Wang, H. Dynamics and function projection synchronization for the fractional-order financial risk system. Chaos Solitons Fractals 2024, 188, 115599. [Google Scholar] [CrossRef]

- Mesgarani, H.; Aghdam, Y.E.; Beiranvand, A.; Gómez-Aguilar, J. A novel approach to fuzzy based efficiency assessment of a financial system. Comput. Econ. 2024, 63, 1609–1626. [Google Scholar] [CrossRef]

- Qayyum, M.; Ahmad, E.; Sohail, M.; Sarhan, N.; Awwad, E.M.; Iqbal, A. Design and implementation of fuzzy-fractional Wu–Zhang system using He–Mohand algorithm. Fractals 2024, 32, 2440032. [Google Scholar] [CrossRef]

- Johansyah, M.D.; Hamidzadeh, S.M.; Benkouider, K.; Vaıdyanathan, S.; Sambas, A.; Mohamed, M.A.; Aziz, A.A. A Novel Hyperchaotic Financial System with Sinusoidal Hyperbolic Nonlinearity: From Theoretical Analysis to Adaptive Neural Fuzzy Controller Method. Chaos Theory Appl. 2024, 6, 26–40. [Google Scholar] [CrossRef]

- Qayyum, M.; Ahmad, E.; Akgül, A.; Din, S.M.E. Fuzzy-fractional modeling of Korteweg-de Vries equations in Gaussian-Caputo sense: New solutions via extended He-Mahgoub algorithm. Ain Shams Eng. J. 2024, 15, 102623. [Google Scholar] [CrossRef]

- Qayyum, M.; Ahmad, E.; Tahir, A.; Acharya, S. Modeling and analysis of the fuzzy-fractional chaotic financial system using the extended He–Mohand algorithm in a fuzzy-Caputo sense. Int. J. Intell. Syst. 2023, 2023, 3028824. [Google Scholar] [CrossRef]

- Aderyani, S.R.; Saadati, R.; Allahviranloo, T.; Abbasbandy, S.; Catak, M. Fuzzy approximation of a fractional Lorenz system and a fractional financial crisis. Iran. J. Fuzzy Syst. 2023, 20, 27–36. [Google Scholar]

- Bian, L.; Li, Z. Fuzzy simulation of European option pricing using sub-fractional Brownian motion. Chaos Solitons Fractals 2021, 153, 111442. [Google Scholar] [CrossRef]

- Rehman, Z.U.; Boulaaras, S.; Jan, R.; Ahmad, I.; Bahramand, S. Computational analysis of financial system through non-integer derivative. J. Comput. Sci. 2024, 75, 102204. [Google Scholar] [CrossRef]

- Alsenafi, A.; Alazemi, F.; Najafi, A. Geometric Asian power option pricing with transaction cost under the geometric fractional Brownian motion with w sources of risk in fuzzy environment. J. Comput. Appl. Math. 2025, 453, 116165. [Google Scholar] [CrossRef]

- Nand, A. Next-generation inventory optimization: Advanced inventory management harnessing demand variability integrating fuzzy logic and granular differentiability. RAIRO Oper. Res. 2025, 59, 335–353. [Google Scholar] [CrossRef]

- Brar, J.; Braun, J.; Hare, W.; Wang, D. A simulation analysis of returns-risk portfolio optimization models. Commun. Stat. Simul. Comput. 2025, 20, 1–28. [Google Scholar] [CrossRef]

- Xiong, T.; Liu, Z.; Zhang, M. Evaluating the efficacy of fuzzy Bayesian networks for financial risk assessment. Demonstr. Math. 2025, 58, 20240032. [Google Scholar] [CrossRef]

- Babakordi, F.; Allahviranloo, T.; Shahriari, M.R.; Catak, M. Fuzzy Laplace transform method for a fractional fuzzy economic model based on market equilibrium. Inf. Sci. 2024, 665, 120308. [Google Scholar] [CrossRef]

- Sukono; Sambas, A.; He, S.; Liu, H.; Vaidyanathan, S.; Hidayat, Y.; Saputra, J. Dynamical analysis and adaptive fuzzy control for the fractional-order financial risk chaotic system. Adv. Differ. Equ. 2020, 2020, 674. [Google Scholar] [CrossRef]

- Hashemi, H.; Ezzati, R.; Mikaeilvand, N.; Nazari, M. Study on fuzzy fractional European option pricing model with Mittag-Leffler kernel. J. Intell. Fuzzy Syst. 2023, 45, 8567–8582. [Google Scholar] [CrossRef]

- Rahaman, M.; Mondal, S.P.; Chatterjee, B.; Alam, S.; Shaikh, A.A. Generalization of classical fuzzy economic order quantity model based on memory dependency via fuzzy fractional differential equation approach. J. Uncertain Syst. 2022, 15, 2250003. [Google Scholar] [CrossRef]

- Bede, B.; Stefanini, L. Generalized differentiability of fuzzy-valued functions. Fuzzy Sets Syst. 2013, 230, 119–141. [Google Scholar] [CrossRef]

- Piegat, A.; Landowski, M. Horizontal membership function and examples of its applications. Int. J. Fuzzy Syst. 2015, 17, 22–30. [Google Scholar] [CrossRef]

- Son, N.T.K.; Long, H.V.; Dong, N.P. Fuzzy delay differential equations under granular differentiability with applications. Comput. Appl. Math. 2019, 38, 107. [Google Scholar] [CrossRef]

- Dong, N.P.; Long, H.V.; Khastan, A. Optimal control of a fractional order model for granular SEIR epidemic with uncertainty. Commun. Nonlinear Sci. Numer. Simul. 2020, 88, 105312. [Google Scholar] [CrossRef] [PubMed]

- Najariyan, M.; Zhao, Y. Fuzzy fractional quadratic regulator problem under granular fuzzy fractional derivatives. IEEE Trans. Fuzzy Syst. 2017, 26, 2273–2288. [Google Scholar] [CrossRef]

- Long, H.V.; Dong, N.P. An extension of Krasnoselskii’s fixed point theorem and its application to nonlocal problems for implicit fractional differential systems with uncertainty. J. Fixed Point Theory Appl. 2018, 20, 37. [Google Scholar] [CrossRef]

- Long, H.V.; Son, N.T.K.; Tam, H.T.T.; Yao, J.C. Ulam stability for fractional partial integro-differential equation with uncertainty. Acta Math. Vietnam. 2017, 42, 675–700. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter Type | Symbol | Values | Description |

|---|---|---|---|

| System parameters | |||

| Savings amount | Uncertain savings range | ||

| Cost of investment | Uncertain cost range | ||

| Demand elasticity | Uncertain sensitivity | ||

| Initial conditions | |||

| Interest rate | Uncertain initial interest rate | ||

| Demand for investment | Uncertain initial investment demand | ||

| Price index | Uncertain initial price variability | ||

| Numerical parameters | |||

| Fractional order | Memory strength | ||

| Time horizon | T | Simulation duration | |

| Step size | h | Discretization step | |

| -cut level | Fuzzy set’s confidence level | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aladsani, F.A.; Muhammad, G.; Elagan, S.K. Granular Fuzzy Fractional Financial Systems Governed by Granular Caputo Fractional Derivative. Mathematics 2025, 13, 1240. https://doi.org/10.3390/math13081240

Aladsani FA, Muhammad G, Elagan SK. Granular Fuzzy Fractional Financial Systems Governed by Granular Caputo Fractional Derivative. Mathematics. 2025; 13(8):1240. https://doi.org/10.3390/math13081240

Chicago/Turabian StyleAladsani, Feryal Abdullah, Ghulam Muhammad, and Sayed K. Elagan. 2025. "Granular Fuzzy Fractional Financial Systems Governed by Granular Caputo Fractional Derivative" Mathematics 13, no. 8: 1240. https://doi.org/10.3390/math13081240

APA StyleAladsani, F. A., Muhammad, G., & Elagan, S. K. (2025). Granular Fuzzy Fractional Financial Systems Governed by Granular Caputo Fractional Derivative. Mathematics, 13(8), 1240. https://doi.org/10.3390/math13081240