A Swap-Integrated Procurement Model for Supply Chains: Coordinating with Long-Term Wholesale Contracts

Abstract

1. Introduction

- (1)

- Formulating the expected swap inflows and outflows under the swap-integrated strategy and embedding them into the expected profit function to derive optimal order quantities;

- (2)

- Comparing the performance of the proposed strategy with a baseline wholesale contract to assess the structural benefits of swap integration;

- (3)

- Conducting sensitivity analyses on key parameters—such as demand asymmetry and swap prices—to identify the conditions under which the proposed strategy yields its greatest performance benefits.

2. Literature Review

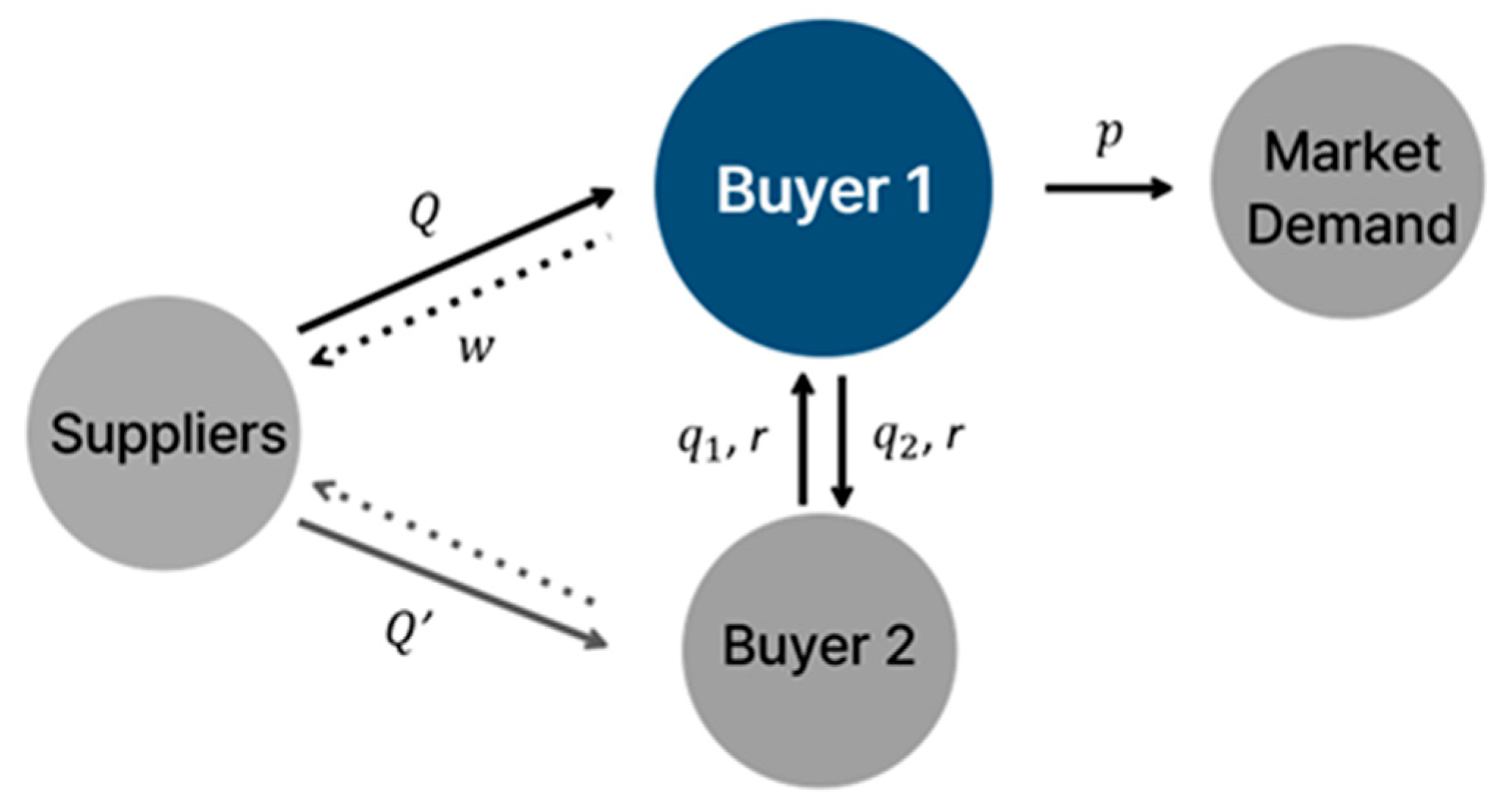

3. Model Description

3.1. Baseline Model: Long-Term Wholesale (WH) Procurement Model

3.2. Swap-Integrated (SW) Procurement Model

- (1)

- The two buyers are fully cooperative under the swap contract. If one buyer holds excess inventory and the other faces a shortage after demand is realized, the surplus is mandatorily transferred at the pre-agreed swap price, r.

- (2)

- The demand of Buyer 1 is represented by the random variable X, and Buyer 2’s demand is represented by Y, where Y follows the same distributional form as X but is scaled by a factor of c. For instance, if Buyer 1 represents the Korean market and Buyer 2 represents the Japanese market, c = 2.5 may reflect the population size ratio. The scaling factor, c, plays a central role in the sensitivity analysis conducted later in this study.

- (3)

- The swap price, r, is given exogenously. Sensitivity analyses with respect to varying values of r will be conducted in a following section.

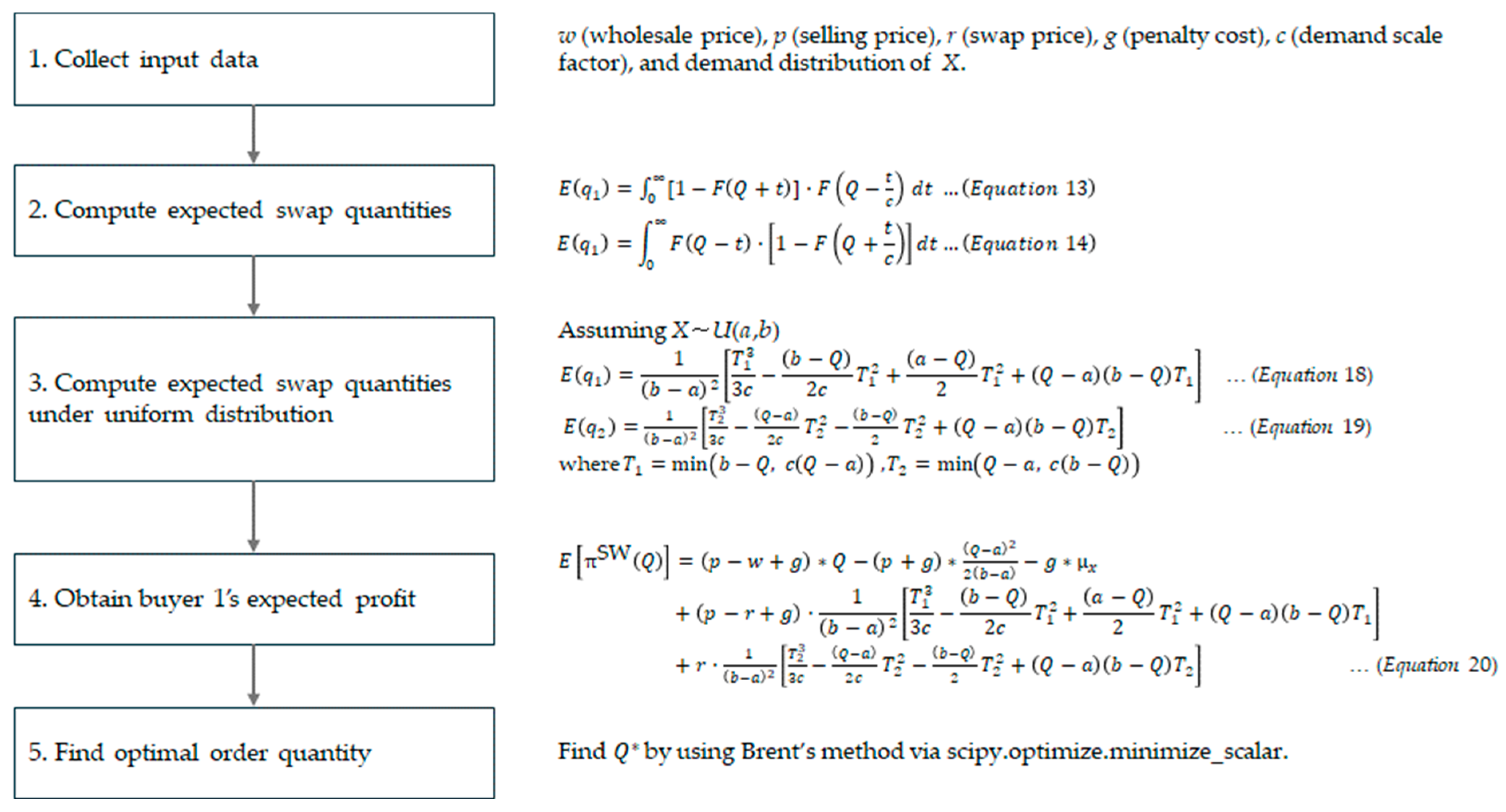

3.2.1. Expected Profit Model for the Swap-Integrated Procurement Strategy

3.2.2. Obtaining the Expected Swap Quantity

3.2.3. Optimal Order Quantity Model Under Uniform Distribution Conditions

4. Numerical Studies

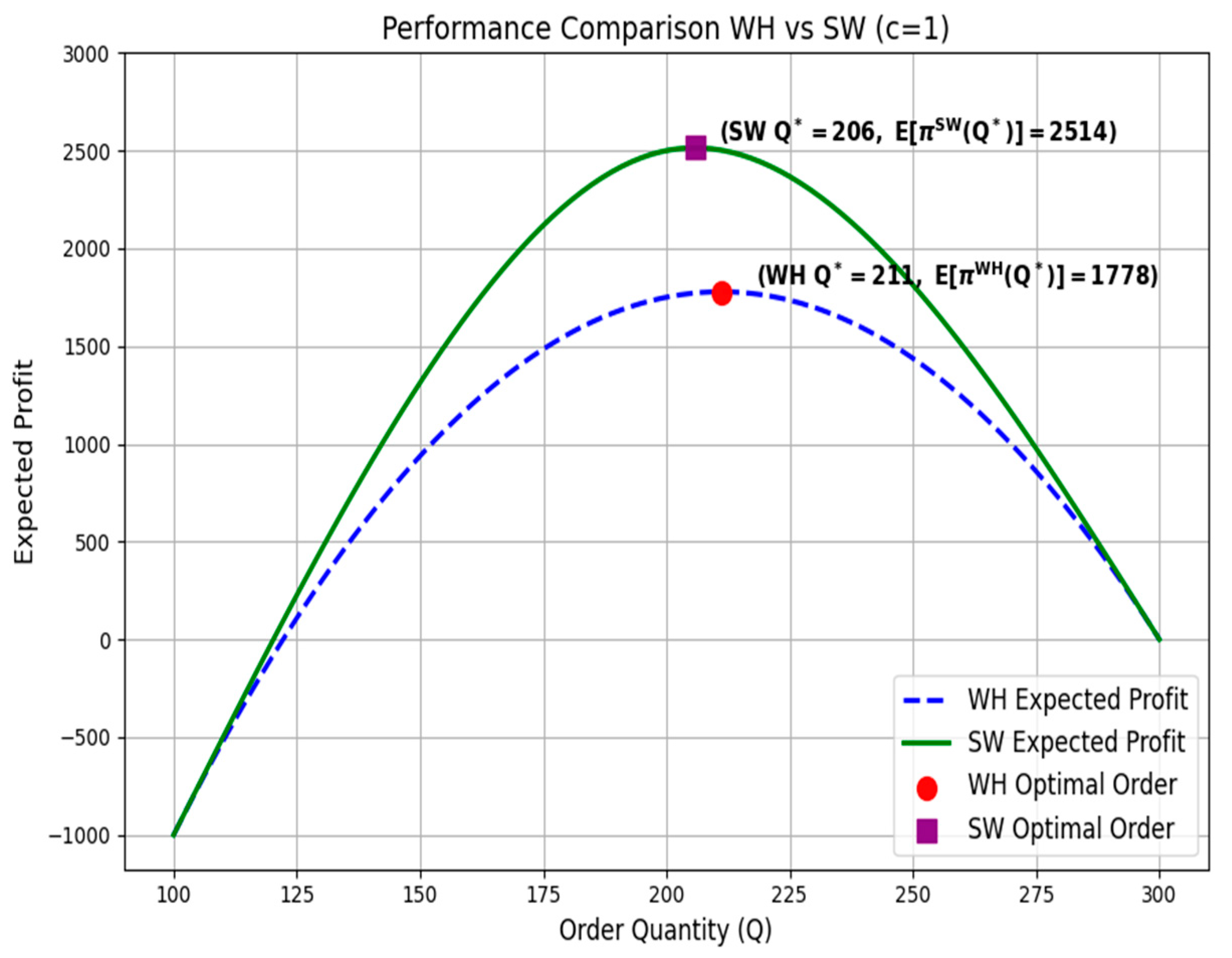

4.1. Performance Comparison: Wholesale-Based vs. Swap-Integrated Procurement Strategies

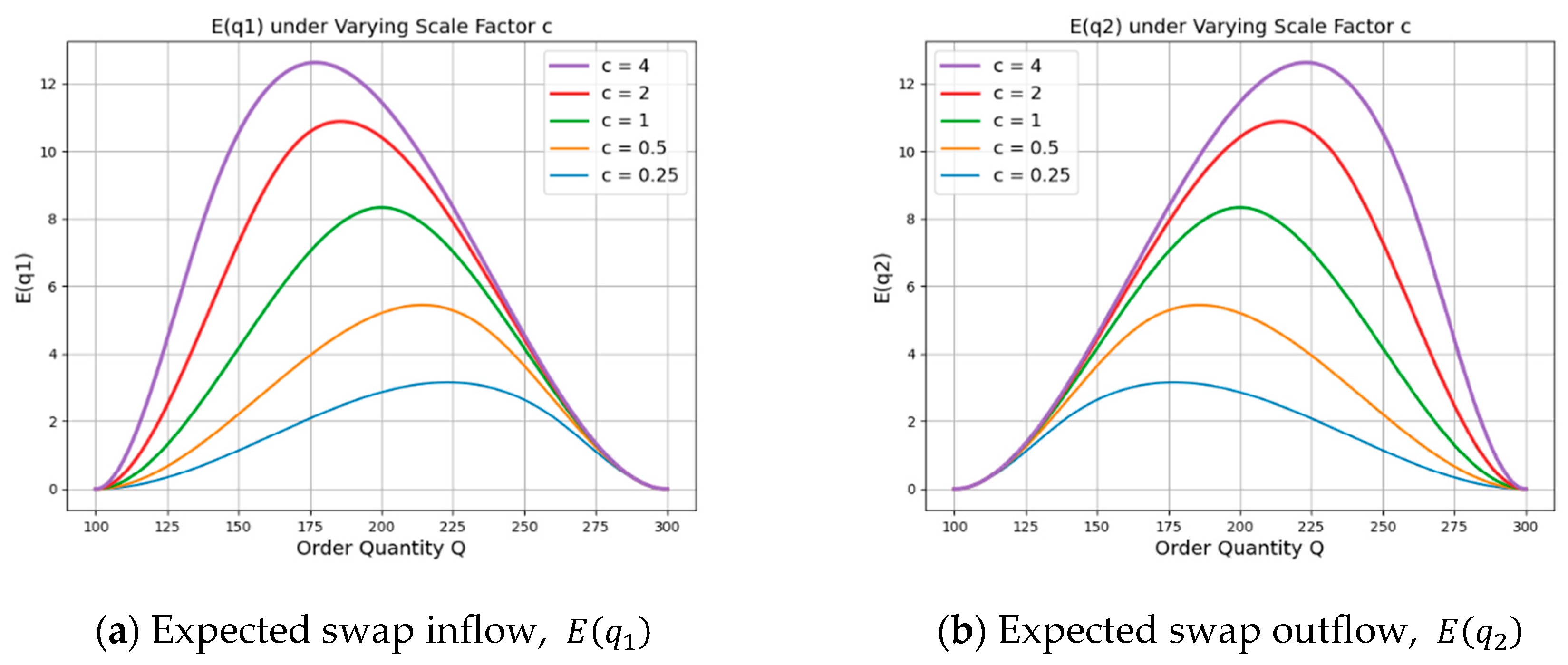

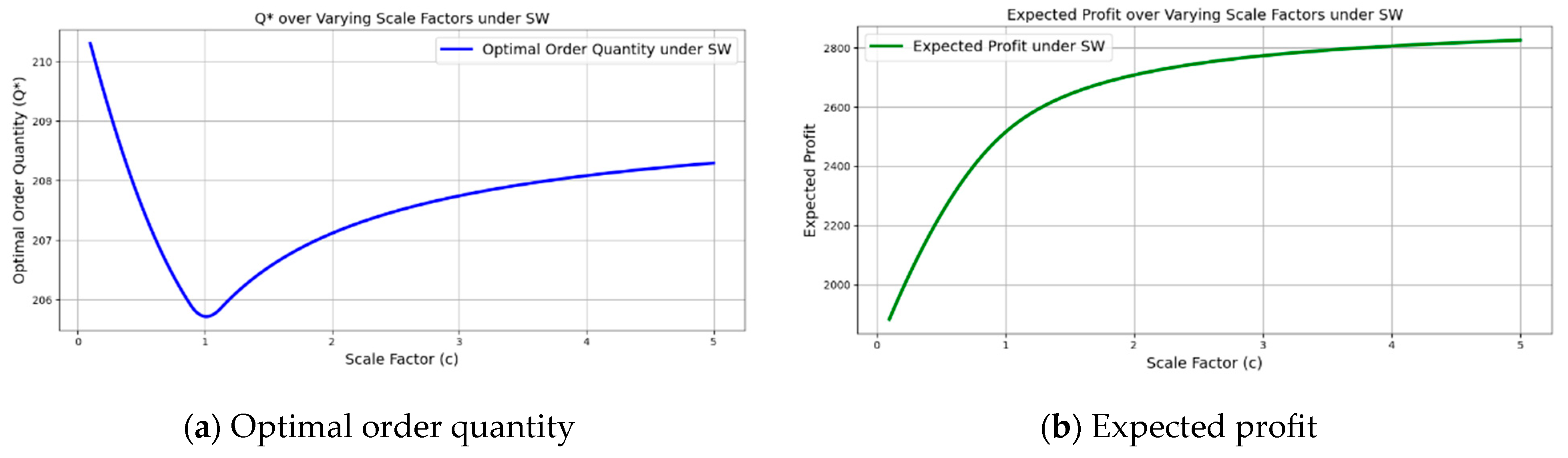

4.2. Effect of Demand Scaling Factor

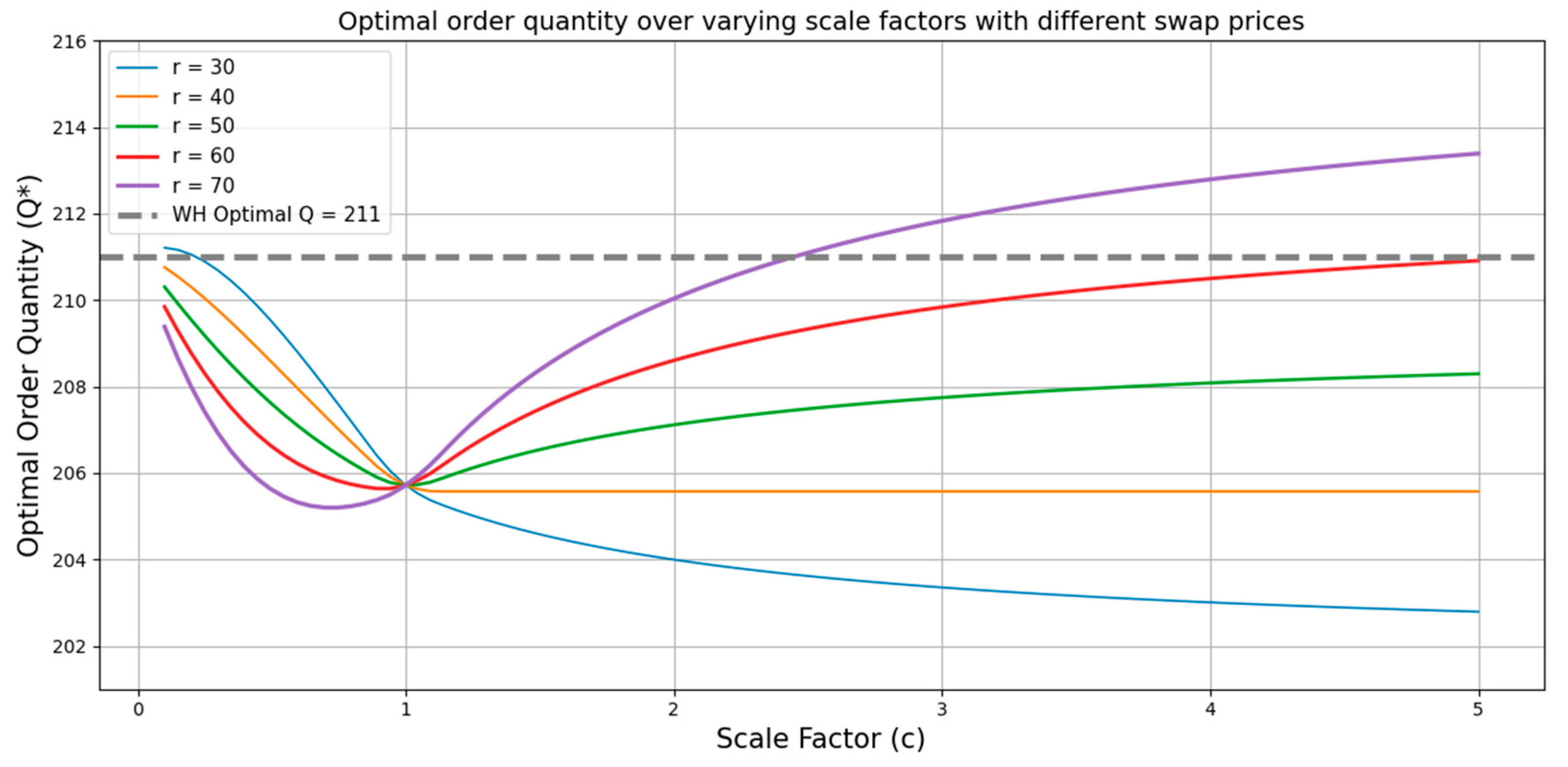

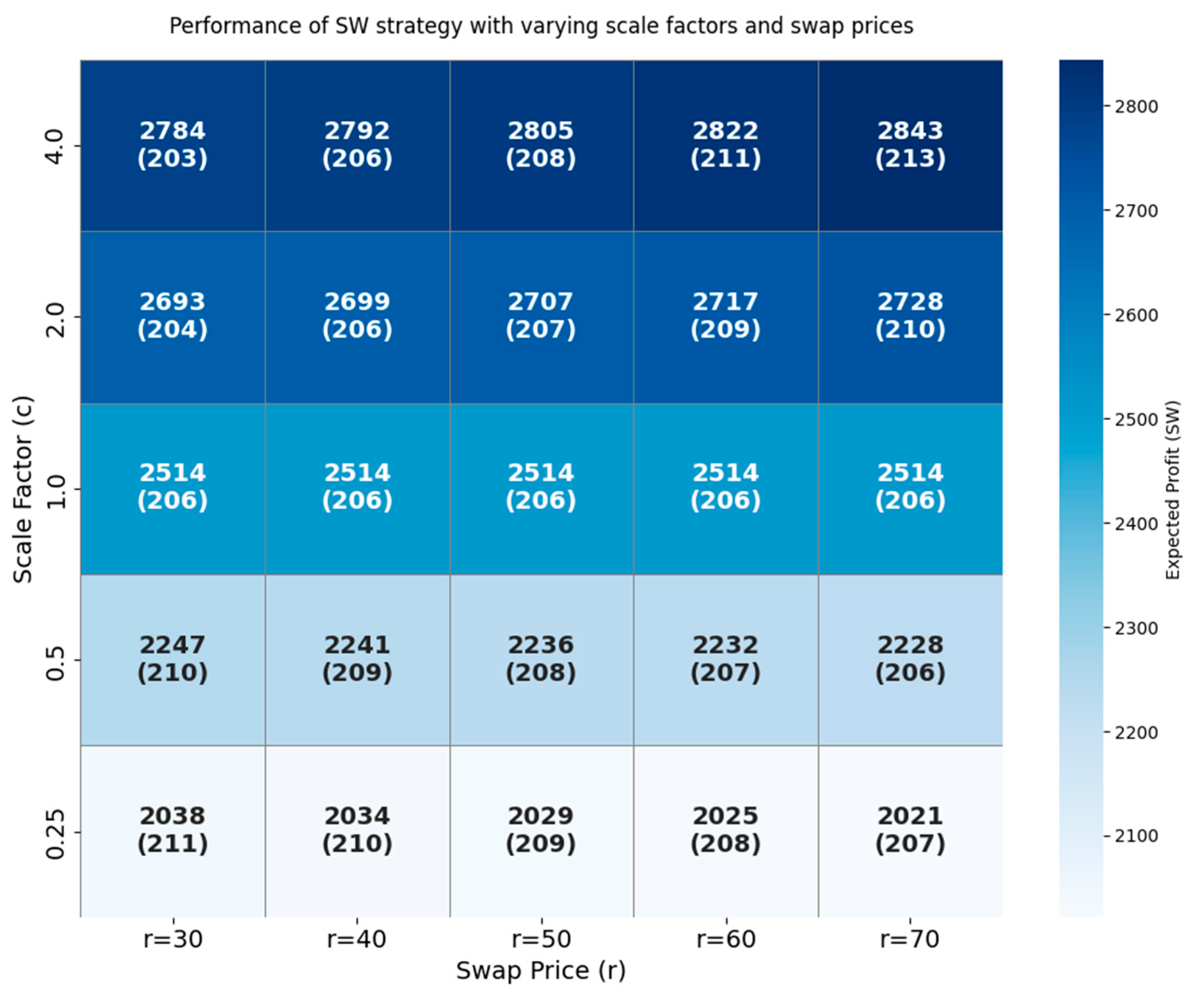

4.3. Effect of Swap Price

- (1)

- When c = 1, the focal and collaborating buyers have identical demand distributions, resulting in a symmetric setting. In this case, the probabilities of surplus and shortage are evenly balanced between the two parties, making the expected gains from swap transactions invariant to the swap price, r. As a result, the optimal order quantity under the SW strategy remains constant regardless of the value of r. Furthermore, this order quantity is consistently lower than that of the WH strategy, reflecting the risk-mitigating role of the swap mechanism. By enabling post-demand adjustments, the swap contract reduces the need for inventory buffers, thereby encouraging more conservative upfront procurement.

- (2)

- When c ≠ 1, the effect of the swap price, r, on the optimal ordering behavior diverges significantly depending on whether c < 1 or c > 1. This outcome is driven by the directional behavior of the expected swap quantities and their influence on the profit function. Recall that the r-dependent part of the expected profit in expression (5) is stated as −+ . Accordingly, the relative magnitude of and plays a critical role in shaping the impact of swap price changes. As shown in Figure 4, when c < 1, a lower order quantity, Q, tends to generate > , implying that an increase in r yields a net gain in the term −+ . Therefore, in this case, higher swap prices make lower Q values more desirable, leading to a decline in optimal order quantity as r increases. Conversely, applying a similar line of analysis reveals that when c > 1, the optimal order quantity tends to increase as the swap price, r, rises.

- (3)

- In most cases, the SW strategy yields a lower optimal order quantity than the WH strategy. However, when both c and r are sufficiently high, the SW strategy may induce a higher order quantity than the WH benchmark. For instance, when r = 70, the SW strategy begins to induce higher ordering quantities than the WH strategy for . This is because the incentive to dispose of excess inventory through swaps becomes stronger when the swap price is high. Also, a similar pattern emerges when and the swap price r is very low. In this case, even if surplus inventory occurs, it may be offloaded to the counterpart, which reduces the burden of holding excess stock. At the same time, the low swap price strengthens the collaborating buyer’s incentive to participate in swaps, thereby increasing the likelihood of successful transactions. As a result, it may be more profitable for the focal buyer to adopt a more aggressive ordering strategy. Accordingly, when the swap price is either sufficiently high or very low—depending on the demand structure—the SW strategy may actually lead to more aggressive ordering than the WH strategy.

- (4)

- When the swap price, r, is low, increasing the scale factor, c, does not lead to a higher order quantity under the SW strategy; instead, the focal buyer tends to adopt a more conservative ordering approach. This outcome reflects the interplay of two reinforcing factors. First, a low swap price provides the focal buyer with a cost-effective means of addressing potential shortages, as inventory can be secured post hoc at a price lower than the wholesale cost, w. This reduces the incentive for large initial orders. Second, the financial benefit from offloading surplus inventory through swaps is diminished at lower r values, limiting the upside of over-ordering. Together, these effects weaken the buyer’s motivation to place aggressive orders in advance and instead encourage strategic reliance on the swap mechanism as a flexible, lower-cost buffer against demand uncertainty.

5. Conclusions

- (1)

- This study presents a novel application of swap mechanisms, traditionally used in financial sectors, to the context of buyer-to-buyer inventory reallocation. By modeling swaps as contractual exchanges of surplus and shortage inventory between buyers, this research reconceptualizes swaps as a post-demand coordination mechanism in supply chain operations.

- (2)

- A model is proposed to estimate the expected swap inflows and outflows resulting from swap transactions.

- (3)

- An analytical model is presented for the expected profit in a system that adopts a swap-integrated procurement policy.

- (4)

- Under the assumption that demand is uniformly distributed, a closed-form expression for the expected profit is derived, and a method for determining the optimal order quantity is presented.

- (5)

- Experimental analyses are conducted to quantify the strategic benefits of swap integration by comparing it to traditional wholesale-based procurement. The results highlight the influence of key parameters, such as demand asymmetry and swap price, on the strategy’s effectiveness.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| WH | Long-term wholesale-based procurement strategy |

| SW | Swap-integrated procurement strategy |

References

- Alkhatib, S.F.; Momani, R.A. Supply Chain Resilience and Operational Performance: The Role of Digital Technologies in Jordanian Manufacturing Firms. Adm. Sci. 2023, 13, 40. [Google Scholar] [CrossRef]

- Choi, T.-M.; Li, D.; Yan, H. Mean–variance analysis of a single supplier and retailer supply chain under a returns policy. Eur. J. Oper. Res. 2008, 184, 356–376. [Google Scholar] [CrossRef]

- Cachon, G.P.; Lariviere, M.A. Supply Chain Coordination with Revenue-Sharing Contracts: Strengths and Limitations. Manag. Sci. 2005, 51, 30–44. [Google Scholar] [CrossRef]

- Zhao, Y.; Choi, T.-M.; Cheng, T.C.E.; Wang, S. Supply option contracts with spot market and demand information updating. Eur. J. Oper. Res. 2018, 266, 1062–1071. [Google Scholar] [CrossRef]

- The Bank of Korea. The Bank of Korea and the Bank of Japan Announce an Increase in the Size of the Won-Yen Swap Arrangement, 2008, Press Release. Available online: https://www.bok.or.kr/eng/bbs/E0000634/view.do?menuNo=400423&nttId=146770 (accessed on 15 July 2025).

- Australian Government Department of Health and Aged Care. COVID-19 Vaccine Rollout Update: International Dose Swap Arrangements. 2024. Available online: https://www.health.gov.au/our-work/covid-19-vaccines/about-rollout/vaccine-agreements (accessed on 26 June 2025).

- Reuters. India’s GAIL Issues Swap Tender for 12 LNG Cargoes. Available online: https://www.reuters.com/business/energy/indias-gail-issues-swap-tender-12-lng-cargoes-sources-say-2025-02-04/ (accessed on 26 June 2025).

- Ekren, B.Y.; Arslan, M.C. Simulation-based lateral transshipment policy optimization for s, S inventory control problem in a single-echelon supply chain network. Int. J. Optim. Control. Theor. Appl. 2020, 10, 9–16. [Google Scholar] [CrossRef]

- Al Husain, R.; Assavapokee, T.; Khumawala, B. Modelling the supply chain swap problem in the petroleum industry. Int. J. Appl. Decis. Sci. 2008, 1, 261. [Google Scholar] [CrossRef]

- Bidyarthi, H.M.J.; Deshmukh, L.B. Swap in downstream petroleum supply chain: An effective inventory handling tool. In Driving the Economy Through Innovation and Entrepreneurship; Mukhopadhyay, C., Akhilesh, K.B., Srinivasan, R., Gurtoo, A., Ramachandran, P., Eds.; Springer: Berlin/Heidelberg, Germany, 2013; pp. 363–370. [Google Scholar] [CrossRef]

- Al-Husain, R.; Khorramshahgol, R. A comprehensive analysis of the determinants of swap problem in the supply chain of the petroleum industry. Int. J. Stat. Probab. 2016, 5, 97–108. [Google Scholar] [CrossRef]

- Farahani, M.; Rahmani, D. Production and distribution planning in petroleum supply chains regarding the impacts of gas injection and swap. Energy 2017, 141, 991–1003. [Google Scholar] [CrossRef]

- Dizbay, I.E.; Ozturkoglu, O. Product swapping and transfer sales between suppliers in a balanced network. In Proceedings of the 2013 Federated Conference on Computer Science and Information Systems, Krakow, Poland, 8–11 September 2013; pp. 1191–1194. [Google Scholar]

- Wang, Y.; Meng, Q.; Tan, Z. Short-term liner shipping bunker procurement with swap contracts. Marit. Policy Manag. 2017, 45, 211–238. [Google Scholar] [CrossRef]

- Park, S.J. Swapping inventory between competing firms. Int. J. Prod. Econ. 2018, 199, 26–46. [Google Scholar] [CrossRef]

- Kemper, A.; Schmeck, M.D.; Balci, A.K. The market price of risk for delivery periods: Pricing swaps and options in electricity markets. Energy Econ. 2022, 113, 106221. [Google Scholar] [CrossRef]

- Zhang, L.; Thomspon, R.G. Optimising product swaps in an urban retail network with uncertainty. Transp. Res. Procedia 2024, 79, 210–217. [Google Scholar] [CrossRef]

- Diks, E.B.; de Kok, A.G. Controlling a divergent two-echelon network with transshipments using linear programming. Eur. J. Oper. Res. 1996, 45, 369–379. [Google Scholar] [CrossRef]

- Paterson, C.; Kiesmüller, G.; Teunter, R.; Glazebrook, K. Inventory models with lateral transshipments: A review. Eur. J. Oper. Res. 2011, 210, 125–136. [Google Scholar] [CrossRef]

- Kumari, A.G.; Wijayanayake, A.; Niwunhella, H. Lateral Transshipment Inventory Models: A Systematic Literature Review of Models and Solution Approaches. Proc. Int. Conf. Bus. Manag. 2022, 18, 54–80. [Google Scholar] [CrossRef]

- Aggarwal, P.; Ganeshan, R. Using risk-management tools on B2Bs: An exploratory investigation. Int. J. Prod. Econ. 2007, 108, 2–7. [Google Scholar] [CrossRef]

- Zhang, Z. An Improvement to the Brent’s Method. Int. J. Exp. Algorithms 2011, 2, 21–26. [Google Scholar]

- Koo, P.-H. Exploring the relationship between buyback and revenue sharing contracts in channel coordination. J. Korean Inst. Ind. Eng. 2024, 50, 211–221. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Supply Swap in Prior Studies | Lateral Transshipment | Swap-Integrated Strategy | |

|---|---|---|---|

| Cooperation Entities | Competing suppliers | Logistics facilities within a firm facilities within a firm | Independent buyers |

| Decisions | Swap quantity and routing | Initial order quantity by location and point-to-point transshipment quantity | Long-term order quantity |

| Objective | Reduce transportation costs, improve delivery and logistics | Balance inventory levels, minimize transportation costs | Mitigate procurement risk and maximize profit |

| References | [9,10,11,12,13,14,15,16,17] | [8,18,19,20] | This study |

| Notations | Descriptions |

|---|---|

| w | per-unit wholesale price |

| p | per-unit retail price at the buyer |

| r | per-unit swap price |

| g | per-unit penalty cost per unit of unmet demand |

| c | demand scale factor of buyer 2 |

| X | market demand of buyer 1, with pdf f(x), and cdf F(x) and average |

| Y | market demand of buyer 2, with pdf fy(y) and cdf Fy(y) |

| Q | order quantity in a long-term wholesale contract (decision variable) |

| swap-inflow quantity from the collaborating buyer | |

| swap-outflow quantity to the collaborating buyer | |

| π | buyer’s profit under a wholesale contract |

| S(Q) | expected sales volume, given Q under a wholesale-only contract |

| L(Q) | expected shortage, given Q under a wholesale-only contract |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ryu, M.-Y.; Koo, P.-H. A Swap-Integrated Procurement Model for Supply Chains: Coordinating with Long-Term Wholesale Contracts. Mathematics 2025, 13, 2495. https://doi.org/10.3390/math13152495

Ryu M-Y, Koo P-H. A Swap-Integrated Procurement Model for Supply Chains: Coordinating with Long-Term Wholesale Contracts. Mathematics. 2025; 13(15):2495. https://doi.org/10.3390/math13152495

Chicago/Turabian StyleRyu, Min-Yeong, and Pyung-Hoi Koo. 2025. "A Swap-Integrated Procurement Model for Supply Chains: Coordinating with Long-Term Wholesale Contracts" Mathematics 13, no. 15: 2495. https://doi.org/10.3390/math13152495

APA StyleRyu, M.-Y., & Koo, P.-H. (2025). A Swap-Integrated Procurement Model for Supply Chains: Coordinating with Long-Term Wholesale Contracts. Mathematics, 13(15), 2495. https://doi.org/10.3390/math13152495