1. Introduction

Modeling the term structure of interest rates is a long-standing topic in financial economics. Many stochastic interest rate models have been proposed in the past decades to provide a realistic and tractable method of describing the term structure; some early contributions include Vasicek [

1], Dothan [

2], Cox et al. [

3], and Hull-White [

4]. If the interest rate is determined by only one stochastic differential equation, the model is referred to as a one-factor model. Cox et al. [

3] assume that the evolution of the interest rate dynamics and the stochastic volatility is given by

where the constants

characterize the long time mean, the volatility, and the speed of adjustment, respectively. In the classical case,

is assumed to be the standard Brownian motion. The stochastic differential equation (SDE) defined by (

1) is said to be a CIR model. It is well known that the CIR model (

1) is nonnegative and has some empirically relevant properties. In this model, when

, the interest rate

has a light-tailed stationary distribution; when

, the interest rate

does not have a stationary distribution (see Shreve [

5]). Single-factor term structure models have been extended to multi-factor models in the literature, for example, by Longstaff–Schwartz [

6] and Duffie–Kan [

7]. According to the memory phenomena in the real market, an appropriate modification (see e.g., [

8,

9,

10,

11,

12,

13]) for the CIR model is to replace the standard Brownian motion by the fractional Brownian motion (fBm) with Hurst parameter

H. For example, Hong et al. [

8] investigated the first result on strong convergence rate for the numerical approximation of (

1) when

in which case (

1) is understood as a pathwise Riemann–Stieltjes integral equation.

As is known, interest rates usually undergo sudden changes; see [

14,

15,

16] and references therein. In the real world, we observe that asset price processes have jumps or spikes, and risk managers have to take them into consideration. Therefore, we consider the CIR model driven by pure jump noise,

where

Z is a function space and

is a compensated Poisson random measure on

Z with intensity measure

, and

and

are constants. However, Jin et al. [

15] dealt with the pure jump noise in an additive sense,

where

,

,

are constants and

is a pure jump Lévy process with its Lévy measure

concentrating on

and satisfying

where they proved the ergodicity under certain conditions. Compared to a classical CIR model (

1), we replace the standard Brownian motion by pure jump process to reflect sudden changes in the stock market, forward market, etc. Compared with Jin [

15], we consider the multiplicative noise rather than additive noise, which better reflects the influence of the classical CIR model itself. The main goal of this paper is to prove the well-posedness and ergodicity of the CIR model driven by pure jump noise, and construct the stationary solution of the CIR model (

2).

Compared to the standard Brownian setting, the main difficulty in studying equations driven by pure jump noise is that the trajectory is not continuous, which makes the Kolmogorov continuity criterion inapplicable in such situation. We will use the truncation method and Picard iteration to prove the existence and uniqueness of truncated equation, and estimate the lower bound of the solution to truncated equation and Equation (

2); thus, the well-posedness of Equation (

2) can be obtained by the convergence of solution. As for providing ergodicity, we perform some estimations to obtain the irreducibility; then, the ergodicity can be obtained with the Feller property. In addition, to the best of our knowledge, there are few papers about the CIR model driven by pure jump noise in a multiplicative sense.

The paper is organized as follows. In

Section 2, we introduce definitions and properties of Poisson jump process, the corresponding Poisson random measure, transition semigroup, transition probability, invariant measure, etc. In

Section 3, we show the well-posedness of the solution and estimate it. Subsequently, we obtain the ergodicity of CIR model driven by the pure jump process in

Section 4. Eventually, using the Skorohod embedding theorem, we construct the stationary solution to Equation (

2) from the invariant measure in

Section 5.

2. Preliminaries

Let be a filtered probability space, for each , and denoted by the -norm.

Assumption 1. Assume that

; there exists a positive constant , such that , and ; it permits that .

Lemma 1 ([17]). Assume that λ is a probability measure on S, where S is a separable and complete metric space. Then, for any small enough, there exists a compact set , such that .

Definition 1 ([17]). Denote by the value at time t of the solution to (

2),

starting at time s from x. Defineand for all , , and , We call the transition semigroup, and the corresponding transition function.

3. The Existence and Uniqueness of Solution

Considering the CIR equation driven by pure jump process, we denote

,

. As for the well-posedness of (

2), we have the following conclusion.

Theorem 1. If Assumption 1 holds and , then for any arbitrary fixed, there exists a unique solution to (

2)

with the formandwhere , In order to prove Theorem 1, we need following two lemmas.

Lemma 2. For any fixed and , if is the solution to (

2),

then holds uniformly on . Proof. On the contrary, we assume that there exists a time

such that

, and

. Without generality, we assume that

; then, we have

. Considering the properties of Poisson process, for a small

, we assume there is no jump happened on

(otherwise there will be a time

,

). Therefore, on interval

, the Equation (

2) reduces to

which is an ODE and the trajectory of

is continuous on

. It often follows that there exists

, and

for

. However, on the interval

,

holds and

strictly increases, which is contrary to our assumption

. The proof is complete. □

Consequently, we use truncation methods with Equation (

2) and denote

if

,

, then

,

, and we have

. If

,

, then

,

, and we have

. If

, then

,

, and we have

. Then Equation (

2) after being truncated can be rewritten as

obviously, it is easy to verify that

f and

h satisfy the Lipschitz condition and linear growth, i.e., there exists a constant

such that

and

Thus, we can use Picard iteration to prove the existence and uniqueness of the solution, and give the estimation of the solution on with the bounded initial data.

Lemma 3 ([18]). There exists a unique solution of Equation (

4),

and is cádlág. Proof. Define a sequence of processes

,

, and for all

,

A simple inductive argument and use of Theorem 4.2.12 in [

18],

is cádlág. For each

, we have

We need to make some estimates, and for

, for each

, we have

Take the expectations and apply Doob’s martingale inequality; the following can be obtained:

With the linear growth of

f and

h, we can finally deduce that

where

and, moreover, for general,

. Similarly, we can obtain

Via Cauchy–Schwarz inequality, we can obtained

for all

. In addition, by It

’s isometry, the following can be obtained:

according to the Lipschitz condition, it can be easily found that

By induction based on (

5) and (

6), we can perform some iterations and integrals, and we deduce the key estimation:

for all

, where

,

.

One can easily find that

is convergent in

for each

. In fact, we can denote the

-norm by

; thus, for each

and for each

, the following can be obtained:

moreover, the right term converging implies that each

is Cauchy, and obviously convergent to some

. Through standard limiting argument, it yields a useful estimate

for each

, and

.

Frequently, the almost sure convergence of

needs to be established. Via the Chebyshev–Markov inequality given in (

7), it can be deduced that

from which we see that

through Borel’s lemma. Moreover,

is almost surely uniformly convergent to

on finite intervals

; thus, it follows that

is cádlág.

At present, we need to verify that

satisfies the Equation (

4). We can define a stochastic process

by

Hence, for each

,

According to (

8), for all

, the following can be obtained:

Hence, each

as required, and the existence has been proved. Let

and

be two distinct solutions to (

4). Hence, for each

,

Similar to the argument used in deducing (

6), it can be found that

thus, by Gronwall’s inequality,

therefore, the following can be obtained:

With the continuity of probability, we have

□

The rest of the proof is to assure that the solution of (

4) converges to the solution of (

2) as

, which implies

. Now, we will show the proof of Theorem 1.

Proof of Theorem 1. From Lemma 2, the solution to truncated Equation (

4) is

The key to prove

is to prove that there exists an integer

, for any

,

. Let us analyze it. If we go back to the truncation method

, obviously, if

,

, and if

,

. With Lemma 2, it is easy to find that there exists an integer

; for any

, we have

, which implies

. Therefore, the solution to Equation (

4) is in the form of

which satisfies Equation (

2). Hence, there is a unique solution to Equation (

2) with the form

In fact, with Lemma 2, it is easy to find that the global Lipschitz condition holds. Indeed, since

,

together with

, the Lipschitz constant

. Meanwhile, since

with Doob inequality, we obtain

with Gronwall inequality,

The proof is completed. □

4. Ergodicity

In this section, we are supposed to prove the existence and uniqueness of invariant measure by using Krylov–Bogoliubov theorem. Firstly, we introduce the most original Krylov–Bogoliubov theorem. E is denoted as a Polish space, is the -field of all Borel subsets of E, and is the set of all probability measures defined on .

Lemma 4 ([19]). Assume that is a Feller semigroup. If for some and some sequence , , and weakly as , then μ is the invariant measure for , where , , However, we usually prove the existence of invariant measures in a condition weaker than Lemma 4.

Lemma 5 ([20]). For , let , and . For the solution process , suppose that the transition probability function has the Feller property, and satisfies the following condition:

For some , there exists a sequence , strictly increasing to such thatuniformly in n. Then, there is an invariant measure μ on . In other words, once the Feller property and irreducibility of the transfer semigroup is proved, then the existence of the invariant measure can be obtained. Moreover, we will prove the uniqueness of the invariant measure for the Equation (

2), and use the invariant measure to construct stationary solutions in the next section.

Lemma 6. If the conditions in Theorem 1 hold, for each , there exists a positive constant , such that Proof. For

, using Itô formula and Young inequality, we can obtain

where

; thus, it can be deduced that

Obviously, the left is uniformly bounded for all . □

Theorem 2. If Lemma 6 holds, there exists a unique invariant measure for Equation (

2).

Proof. Assume that

and

are solutions to Equation (

2) with initial data

and

, respectively; with inequality (

9), we obtain

thus, by Gronwall inequality,

For any

, it can be approximated pointwise by a sequence of functions in

. Therefore, it suffices to take a bounded Lipschitz-continuous function

to verify the Feller property. Thus, for

, and

,

where

is Lipschitz constant. Making use of (

10), the Feller property follows. Since the probability measure

of the solution

supported in

,

together Chebyshev inequality with (

9), it can be deduced that

which converges to zero as

uniformly in

. Hence by Lemma 4, there exists an invariant measure

. By the convergence, for

,

now, for any invariant measure

, it can be obtained that

which implies

is the unique invariant measure. □

6. Numerical Simulation

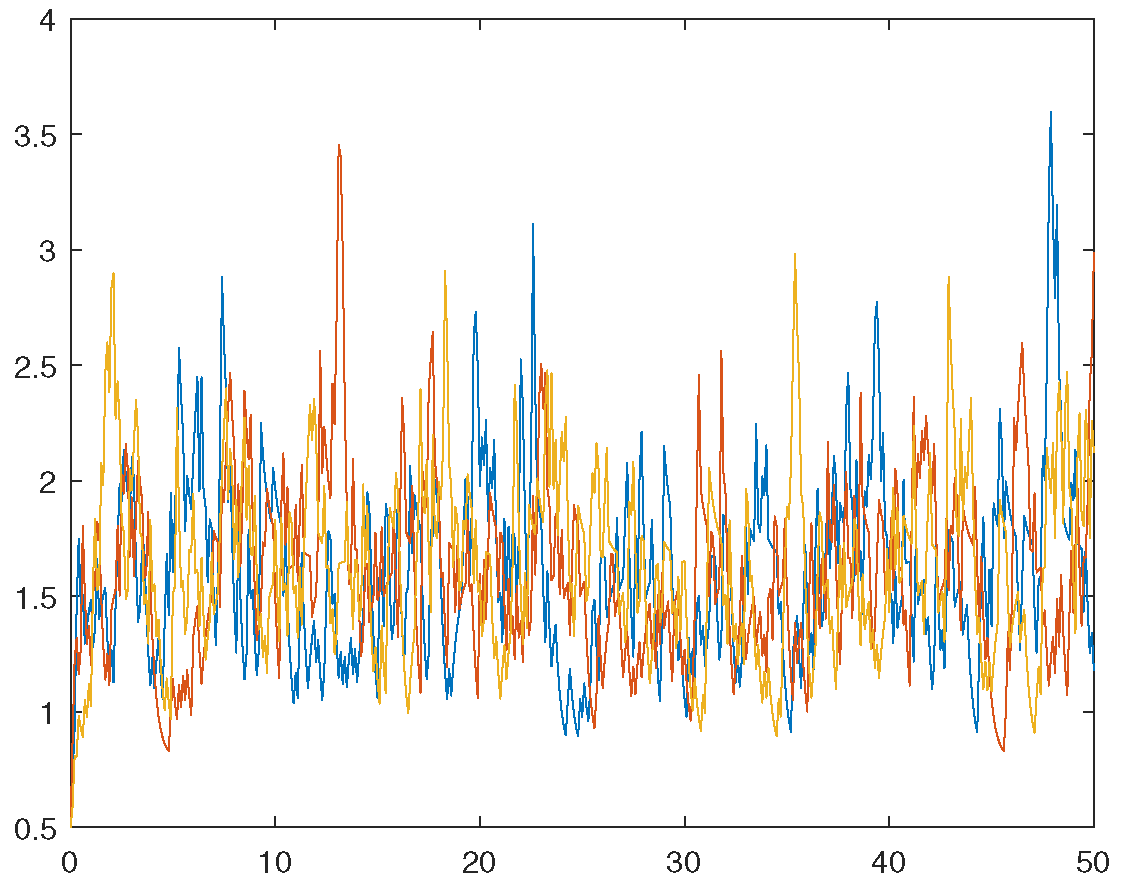

In this section, we will perform some numerical simulations to visualize and verify our theoretical results. For a concrete CIR model driven by pure jump process, we take Poisson parameter

, and as for the CIR model itself, we take

, and

. In order to verify the boundedness of

, we take different initial data

and

; then, we have explicit CIR as follows

We will use the Euler–Maruyama method to iteration [

22], in which the time interval

and step length

. Firstly, we present three sample paths of the solution

to verify the boundedness of

in time. Hence, we take the initial data

in

Figure 1 and

in

Figure 2, respectively.

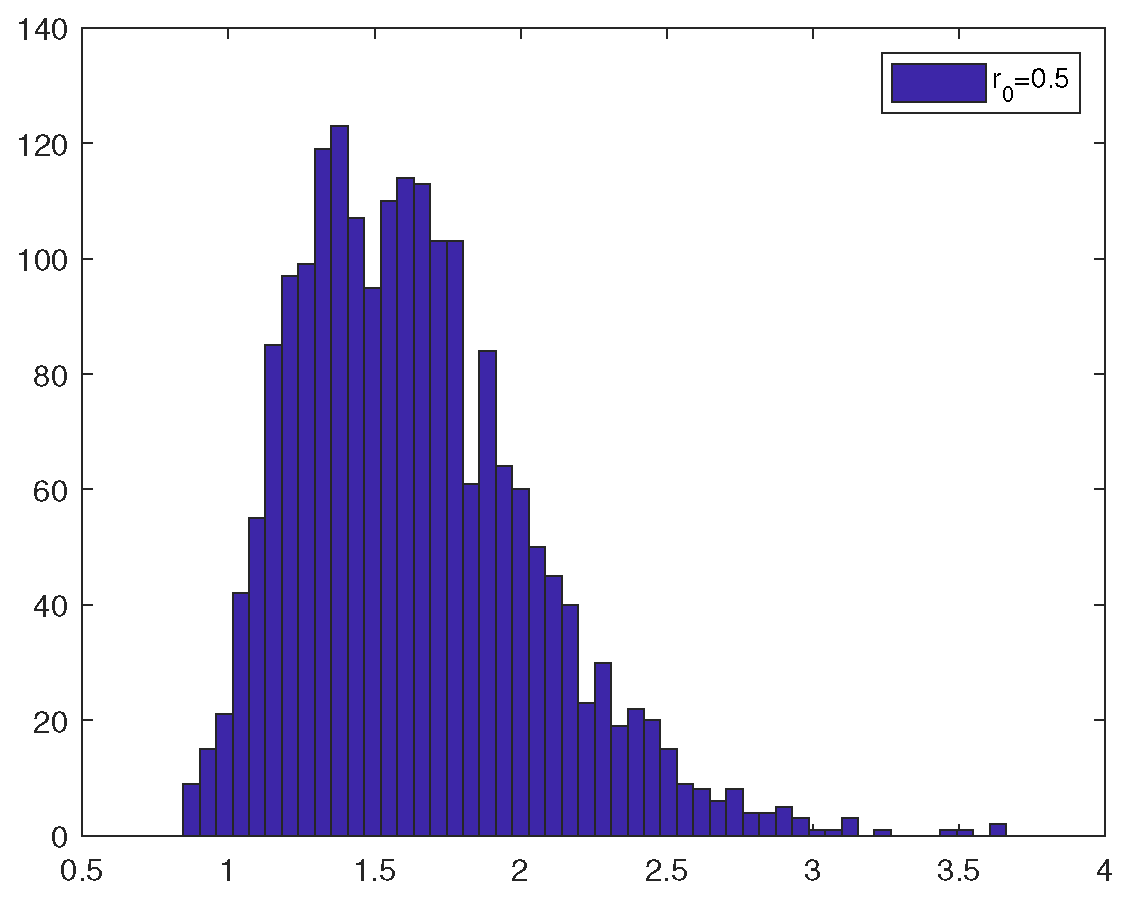

Remark 1. In Figure 1 and Figure 2, we show sample paths at random, and they undergo great ups and downs, which shows the influence of the Poisson process on the properties of the equation solution well. Meanwhile, the trend of the trajectory shows the effect of the item, , on the solution, which makes its distribution concentrated as is supposed. Furthermore, the phenomenon verifies our discussion about the boundedness of the solution quite well. In order to show the statistical characteristics to verify the ergodicity of (

13), similarly, we take two different initial data

and

and calculate and count the data of 1000 sample paths. Moreover, the statistical characteristics with different initial data are as follows. In

Figure 3 and

Figure 4, the values of the 1000 trajectories at the final moment show a tendency to concentrate, which explains the invariant measure numerically.

{kind=link}

{kind=link}

{kind=link}

{kind=link}