1. Introduction

This paper provides an optimal and adaptive portfolio allocation strategy based on the technical analysis of a diversified investment portfolio. The investment portfolio often contains more than one risky asset to avert possible significant loss. Portfolio allocation is an important strategy for investors and traders, and they are interested in an optimal allocation when they have enough capital to invest in more than two assets. They might want to allocate the wealth not only between one risk-free asset and another risky asset but also among different risky assets. The common approach is to assign equal weights when allocating the wealth among the risky assets, which, however, is not always optimal. We believe that an allocation amount should be a function of the investor’s specified risk tolerance, and this consideration could lead to a more favorable investment outcome. We focus on finding optimal trading strategies based on technical analysis, such as moving averages for building a multiple-asset portfolio. We propose a multiasset generalized moving average crossover (MGMA) strategy. This strategy can allocate wealth not only between one risky asset and another risk-free asset but also among different risky assets, with the risk tolerance specified by the investor. It can also increase both the investor’s expected utility of wealth and the investor’s expected wealth.

Technical analysis is widely adopted by investors in practice. The empirical evidence, including the predicted performance of a stock return, demonstrates the usefulness of technical analysis (see [

1,

2,

3,

4]). Among all the technical analysis methods, the moving average strategy is the simplest and most popular trading rule. Ref. [

1] appeared to be the first article to provide strong evidence of profitability by using a moving average technique in analyzing daily Dow Jones Industrial Average (DJIA) data. The moving average strategy in technical analysis follows an all-or-nothing investment strategy: when a

buy signal is triggered by the moving average crossover (MA) strategy, the investor should allocate all of his/her wealth to the stocks of interest; when a

sell signal is triggered by MA, the investor should allocate none of the wealth into the stocks by selling all the current holdings. Thus, this simple moving average strategy suffers from a well-known drawback, since its allocation is always either 100% or 0%. Ref. [

2] provided further evidence based on different time series data obtained from financial markets. These studies have generated further research interest on moving average strategies. However, most of the studies have been focused on validating the strategy using different data sets. The conclusions are mixed and inconclusive (see [

5,

6,

7,

8,

9]). An increasing number of studies are focused on the predictive power of a moving average technique (see [

10,

11,

12,

13,

14,

15]). Ref. [

16] provided the first theoretical analysis for this simple moving average crossover strategy. Their study focuses on how technical analysis such as this moving average strategy can add value to commonly used allocation rules that invest fixed proportions of wealth in stocks. Ref. [

17] provided a general equilibrium model for the MA strategy and argued MA signals in their model are helpful for investors in pricing the asset. In addition, more studies focus on the applications of MA strategy. Ref. [

18] combined MA signals to create a factor to explain various term momentum. Ref. [

19] combined MA signals to estimate equity returns. Ref. [

20] suggested that the effectiveness of technical analysis depends on the level of PIN (probability of informed trading).

Most asset allocation studies focus on finding an optimal portfolio choice under different modeling processes (see [

21,

22,

23,

24,

25]). Refs. [

26,

27] incorporated technical indicators into the portfolio construction problem. However, they do not study the optimal allocation in the context of using technical analysis strategies for a multiasset portfolio. In addition, few studies reconciled the technical indicators with a portfolio selection policy that guides investment decisions in a multiasset setting. Ref. [

28] bridged the gap by devising a portfolio strategy in which optimal weights are directly parameterized as a function of multiple trend-following signals. However, there is no extension to a multiple-asset setting with an optimal allocation as the objective. Recently, an increasing number of studies are focused on using machine learning for portfolio allocation strategies. Ref. [

29] used machine learning to find the optimal portfolio weights between the market index and the risk-free asset and found that a portfolio allocation strategy employing machine learning to reward–risk time in the market gave significant improvements in investor utility and ratios. They use random forest and update the weights on only a monthly basis or over a relatively long period of time, while our methods are instantaneous and much less computationally intensive, since they do not require building a forest or any tree pruning. Ref. [

30] developed optimization algorithms with machine learning techniques and assessed the risk characteristics of a large commodity portfolio. Their objective is the prediction of risk measures instead of expected returns. Ref. [

31] proposed a novel two-stage method for well-diversified portfolio construction based on stock return prediction using machine learning. They use the mean-variance model for portfolio construction. The challenge of the mean-variance model is its well-known sensitivity to the change in mean return.

We derive the expected log-utilitity of wealth, which provides the mechanism for the optimal allocation estimates. This provides the theoretical foundations of our strategy. The algorithm using our MGMA strategy is also developed for the application of our methods. Furthermore, motivated by recent years’ studies on higher-frequency information on financial market forecasting (see [

32,

33]), we tested the proposed MGMA strategy using the daily second-level exchange-traded fund in the North American market. In general, the Sharpe index is appropriate for evaluating a trading strategy. We did not feel that this is the best measure for our method, since the expected return of our strategy is clearly not normally distributed, with the median much closer to the minimum than that from the maximum, as suggested in our simulation study. This suggested that there is a long tail on the right-hand side associated with the case of high profitability. The large variation above the median level suggested a desirable significant chance of making a great profit. If we use the standard deviation as the denominator, it will dilute the advantage of our method, since it is unduly penalized by the possibility of extreme profitability.

The rest of the paper is organized as follows. We introduce the general model with the MGMA strategy in

Section 2. We present the main theoretical results in

Section 3. We provide an investment algorithm for the multiasset portfolio in

Section 4. We carry out simulation studies in

Section 5. We present the results of real data analysis in

Section 6. We conclude the article in

Section 7.

2. The Model and the MGMA Strategy

Suppose that there are assets in a financial market. For convenience, we assume that the first one is risk-free, e.g., a cash or money market account with a constant interest rate of r. The other n assets are risky ones, which, for example, can be stocks or indices representing the aggregate equity market. A multiasset portfolio contains n risky assets. The wealth can be allocated not only between the risk-free asset and one risky asset but also among risky assets.

We follow [

34] to define a general model for a multiasset portfolio with multiple predictive variables. Suppose that the price of the risk-free asset

at any time

t satisfies that

Moreover, suppose that there are

q predictive variables that can be accurately observed at continuous times. Then, the vector of

n risky asset prices

at any time

t satisfies that

and the dynamics of the vector of

q predictive variables

satisfies that

where

and

The vectors

and

and matrices

U,

,

, and

are all unknown. The vectors

and

are a multidimensional standard Brownian motion, such that

where

denotes an

identity matrix. Each predictive variable

is assumed to be a stationary process for

,

. In order to ensure

is a mean-reverting process,

is assumed to be symmetric negative definite, i.e.,

and

for any

.

We first recall the original MA strategy. We define some notations for the

kth stock (

) in the market. Let

be the real stock price at time

t and

be its log-transformed stock price, i.e.,

Denote a lag or lookback period by

. In view of [

16], a continuous time version of the moving average of this log-transformed stock price at any time

t is defined as

i.e., the average log-transformed stock price over time period

. Let

be the difference between

and

, where

is a short-term lookback period and

l is a long-term lookback period

, i.e.,

Denote the MA strategy for an

n-asset portfolio by

. Then,

for a single-asset portfolio, i.e.,

, is defined as

and the MA strategy

for a two-asset portfolio, i.e.,

, is defined in

Table 1. We follow the common approach to assign equal weights when there is more than one investment signal.

We now define the MGMA strategy. The key is to introduce an investor’s specific risk tolerance

into the moving average strategy. Define

as

Let

be the vector of

n stock prices,

be the vector of

n log-transformed stock prices, and

be the vector of

n differences between the moving averages, i.e.,

Let

and

,

. Define

as

Let

be the MGMA strategy for the

kth risky asset in a multiasset portfolio. Let

be the asset allocation parameter for the

kth risky asset in the multiasset portfolio. Suppose that

is the vector based on the MGMA strategy and

is the vector of the

n asset allocation parameters, i.e.,

Then, for

, we define the MGMA strategy

as

where

is an indicator function such that

To ensure is well-defined, for , we define as a constant vector , i.e., , where is a constant for and .

The MGMA strategy is a market-timing strategy that allocates wealth not only between one risk-free asset and one risky asset but also among risky assets, with the risk tolerance specified by the investor. Note that the MA strategy is a special case of the MGMA strategy. Theoretically speaking, the asset allocation parameter can be any number which is interpreted as a long portion of stocks if and a short portion of stocks if . Therefore, there are parameters for the MGMA strategy on a multiasset portfolio which contains n risky assets.

We give some examples of the MGMA strategy. The MGMA strategy

for a signal-asset portfolio

is defined as

where

and

. The MGMA strategy

for a two-asset portfolio

consists of 32 parameters, which is defined in

Table 2.

It is obvious that the MGMA strategy is very complex, even for a two-asset portfolio. In light of [

6], we consider no-borrowing and no-short-sale constrains, i.e.,

and

. We use these constrains to reduce parameters to five, i.e.,

, as in

Table 3, for implementation.

The MGMA strategy from an asset allocation perspective now becomes finding the optimal

that maximizes the investor’s expected log-utility of wealth

subject to a budget constraint

given an initial wealth

for a multiasset portfolio, a constant rate of interest

r, and an investment horizon

T, where

.

3. The Analytic Results

To focus on the framework and the MGMA strategy, we only present the main analytic results in this section. The lemmas used to derive the formulas are presented in

Appendix A.

In order to find an optimal

, we need to derive the investor’s expected log-utility of wealth

. To derive it, we need to find the joint distribution of

. Let

be the expectation of

,

be the expectation of

,

be the variance–covariance matrix of

,

be the variance–covariance of

, and

be the covariance matrix between

and

. Based on Lemmas A2, A4, A9 and A12 in

Appendix A, it is derived that

has a multivariate normal distribution, i.e.,

and

where

and

Note that the distribution of

does not depend on

t. From the multivariate normal distribution of

, we have

Denote

,

and

as

Thus, we have

where

and

is the correlation matrix for the vector

, i.e.,

Denote the probability density function of

by

. Let

be any hyper-rectangle. For a simple presentation, let

,

. We define

and

Similar to Equation (

9), we define

as

We also define

where

,

.

Given an initial wealth , a constant rate of interest r, and an investment horizon T, let be the investor-specified risk tolerance, be the vector of n asset allocation parameters, and be the vector-based multiasset generalized moving average crossover (MGMA) strategy. For the MGMA strategy, we have the following propositions.

Proposition 1. The expectation of is independent of time t and given by Proof. By Equations (

11), (

19), (

22) and (

23), we have

which concludes the proposition. □

Proposition 2. The expectation of is independent of time t and given by Proof. In light of Equations (

11), (

19), (

22) and (

23), we have

which concludes the proposition. □

Proposition 3. The expectation of is independent of time t and given by Proof. By (

18) and Proposition 1, we have

where

and based on Equations (

11) and (

19),

where

which implies that

□

Proposition 4. Let be a constant vector for MGMA strategy when , i.e., , where is a constant for and . Let be the investor-specified risk tolerance, then the investor’s expected log-utility of wealth at the end of investment period T iswhere and is a constant depending on l, i.e., By Propositions 1–3, Equation (24) can be rewritten as Proof. Based on Equations (

1) and (

2), the budget constraint for the multi-asset portfolio follows

Since

and

, where

and

is the identity matrix,

which implies that

By Equation (

11) with

,

which implies that

By Propositions 1–3, we note that

,

and

are all independent of time

t. Since

and

by Lemma A2 in

Appendix A, we derive

where

, and

is a constant depending on

l, i.e.,

then Equation (

24) is proved. □

Now, we can calculate optimal estimates of the asset allocation parameters for the MGMA strategy by maximizing

with respect to asset allocation parameters

. Suppose that the investor-specific risk tolerance

, then for

kth stock, we solve following equation for optimal estimates

, i.e.,

We also restrict

, which means there are no-borrowing and no-short-sale constrains; then, the optimal estimates of

are

Note that the optimal estimates are functions of the investor-specified risk tolerance . The results illustrate that the MGMA is a better investment strategy compared with the MA strategy for the multiasset portfolio, because it has a higher expected utility of wealth for the investor.

5. Simulation Studies

We present several numerical examples based on a simulated two-asset portfolio and a simulated three-asset portfolio. Motivated by recent research on higher-frequency information on financial market forecasting, we simulated a daily second-level two-asset portfolio and a daily second-level three-asset portfolio. The investment algorithm is tested and compared with the MA strategy as the benchmark.

5.1. Simulation Results for Two-Asset Portfolio

The simulated two-asset portfolio data are generated using the parameters below.

and

and

The simulation runs 1000 times. Each time series contains 97,500 observed points.

The simulation studies are performed under two scenarios (

vs.

). We set initial wealth

and interest rate

. Under each scenario, we test the MGMA strategy based on

and

and compare it with the MA strategy. The MGMA strategy performance results are provided in

Table 4 and

Table 5. We first report the theoretical expected log-utility of wealth

based on Equation (

25) with the percentage increase in the expected log-utility of wealth compared with the MA strategy. We then report numerical summaries to calculate from the simulation results, including the expected log-utility of wealth

, the expected wealth

, the expected return on asset ratio

, etc.

In the rest of this paper, , , , , and respectively stand for the estimates of , , , , and , and denotes the expected number of transactions.

Note that the MGMA strategy for a two-asset portfolio can increase the investor’s expected log-utility of wealth and also increase the investor’s expected wealth and the expected return on asset ratio from the simulation results. Under scenario 1, the expected log-utility of wealth increases in the range of to . The expected return ratio increases from benchmark return to , and , respectively. Under scenario 2, the expected log-utility of wealth increases in the range to . The expected return ratio increases from benchmark return to , and , respectively.

5.2. Simulation Results for Three-Asset Portfolio

The simulated three-asset portfolio time series data are generated using the parameters below.

and

and

The simulation runs 1000 times. Each time series contains 97,500 observed points.

The simulation studies are performed under two scenarios (

and

vs.

and

). We set initial wealth

and interest rate

. Under each scenario, we test the MGMA strategy based on

and

and compare it with the MA strategy. The MGMA strategy performance results are provided in

Table 6 and

Table 7. We first report the theoretical expected log-utility of wealth

based on Equation (

25) and the percentage increase in the expected log-utility of wealth compared with the MA strategy. We then report numerical summaries to calculate from the simulation results, including the expected log-utility of wealth

, the expected wealth

, the expected return on asset ratio

, the standard deviation of wealth

, the maximum of wealth

, the minimum of wealth

, the median of wealth

and the expected number of transactions

. By using no-borrowing and no-short-sale constraints, we can reduce the parameters of MGMA strategy for a three-asset portfolio from 192 to 37 for implementation. For easy illustration, we do not report the optimal asset allocation parameters in the simulation summary tables.

Note that the MGMA strategy for a three-asset portfolio can increase the investor’s expected log-utility of wealth and also increase the investor’s expected wealth and the expected return on asset ratio from the simulation results. Under scenario 1, the expected log-utility of wealth increases in the range to . The expected return ratio increases from a benchmark return of to and , respectively. Under scenario 2, the expected log-utility of wealth increases in the range of to . The expected return ratio increases from a benchmark return of to and , respectively.

6. Real Data Applications

We present several real data analyses based on high-frequency exchange-traded fund (ETF) data. The investment algorithm is tested and compared with the benchmark. The simplified MGMA strategy for a two-asset portfolio in

Table 3 is used. The MA strategy for a two-asset portfolio in

Table 1 is used as the benchmark strategy.

6.1. An Algorithm to Estimate Model Parameters

In order to use the investment algorithm for a multiasset portfolio on real data, we need to estimate model parameters

,

,

U,

,

,

, and

. There is no such algorithm in the literature due to complex model settings. We propose an algorithm to fill the gap. Without loss generality, we describe the algorithm by using a general model for a two-asset portfolio. Based on Equation (

2),

and Equation (

3),

where

and

Let

; then, it is easy to check the log-likelihood function for

is

and let

, then the log-likelihood function for

is

Let

; it is also easy to verify that

Then, the algorithm contains the following steps:

- Step 1.

Given a , calculate , , and (for ) based on the historical time series.

- Step 2.

Use least square estimation method to estimate parameters

,

,

,

,

, and

by minimizing

- Step 3.

Let

, and use least square estimation method to estimate parameters

,

,

, and

by minimizing

- Step 4.

Calculate and from , , and , , , , , , , , , , , , and .

- Step 5.

Use maximum likelihood estimation method and set

to estimate

from

. Since

, we can estimate parameters

,

,

, and

.

- Step 6.

Use maximum likelihood estimation method and set

to estimate

,

,

,

and

from

.

- Step 7.

Calculate and from , , , and .

- Step 8.

Calculate from and . Then, the estimated parameter is .

6.2. Case 1: MGMA Strategy on High-Frequency Exchange-Traded Fund in North American Market

We use PowerShares QQQ Trust Series 1 (QQQ) and SPDR S&P 500 ETF Trust (SPY). These are exchange-traded funds incorporated in the USA. QQQ ETF tracks the performance of the Nasdaq 100 Index. It holds large-cap U.S. stocks and tends to focus on the technology and consumer sector. The holdings are weighted by market capitalization. As of 6 October 2017, there were 107 holding companies. The top three holding companies are Apple Inc., Austin, TX, USA (AAPL, 11.57%), Microsoft Corp., Redmond, WA, USA (MSFT, 8.44%), and Amazon.com, Inc., Seattle, WA, USA (AMZN, 6.86%). SPY ETF tracks the S&P 500 Index. The trust consists of a portfolio representing all 500 stocks in the S&P 500 Index. It holds predominantly large-cap U.S. stocks. It is structured as a unit investment trust and pays dividends on a quarterly basis. The holdings are weighted by market capitalization. As of 6 October 2017, the top three holding companies were Apple Inc., Austin, TX, USA (AAPL, 3.67%), Microsoft Corp., Redmond, WA, USA (MSFT, 2.68%), and Facebook Inc., Menlo Park, CA, USA) Class A (FB, 1.87%).

We collected daily second-level QQQ ETF, SPY ETF, MSFT, and AAPL price time series for this study. The QQQ ETF price time series and SPY ETF price time series are used as the vector-based ETF price

. The MSFT and AAPL stock price time series are used as the vector-based predictive variable

. The collection period is the daily trading time from 9:30 a.m. to 4:00 p.m. (Eastern Time) to ensure a high liquid market. We divided QQQ ETF and SPY ETF time series into two data sets: vector-based ETF price

training data (9:30 a.m. to 3:00 p.m., which contains 19,800 s) and vector-based ETF price

test data (3:00 p.m. to 4:00 p.m., which contains 3601 s). We use the MSFT and AAPL price time series as the vector-based predictive variables’

training data (9:30 a.m. to 3:00 p.m., which contains 19,800 s). We set initial wealth

and interest rate

. Suppose that the investor’s risk tolerance is

. We restrict

,

,

,

, and

in

,

s in

, and

l in

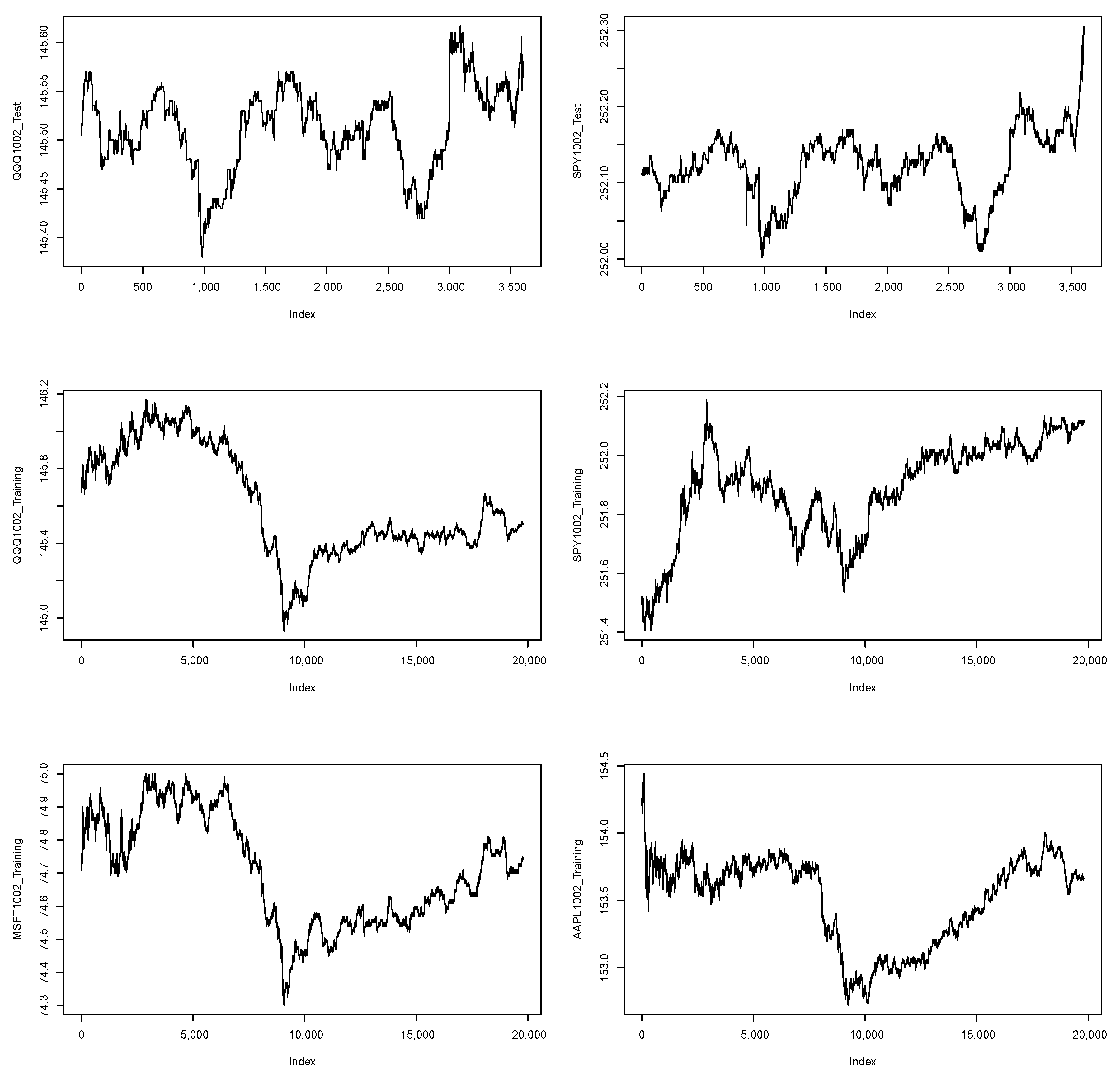

and 240. We use training data to choose model parameters with the highest return. We first report the MGMA strategy performance summary for QQQ ETF and SPY ETF on training data; then, we report the MGMA strategy evaluation summary for QQQ ETF and SPY ETF on test data. Our study spans five days from 10 February 2017 to 10 June 2017. We plot second-level QQQ ETF and SPY ETF price time series on day 1 (10 February 2017) in

Figure 1 as an example.

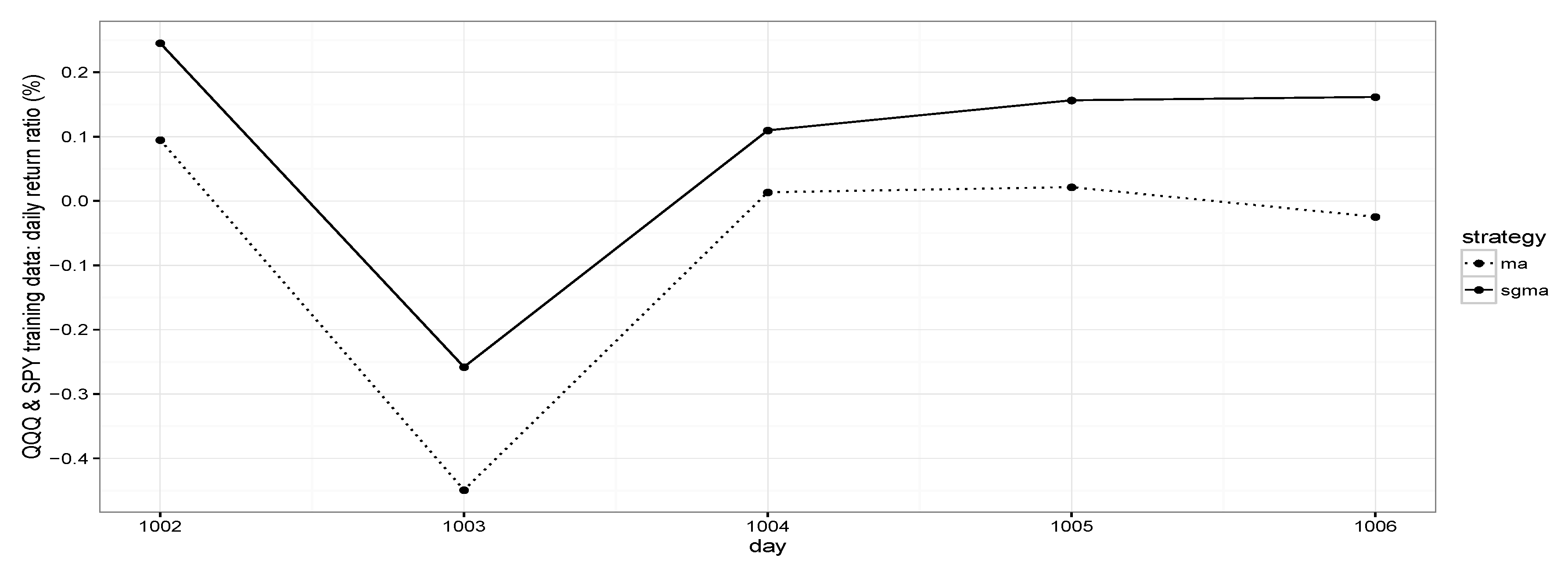

The MGMA strategy performance summary for QQQ ETF and SPY ETF on day 1 (10 February 2017) to day 5 (10 June 2017); training data are provided in

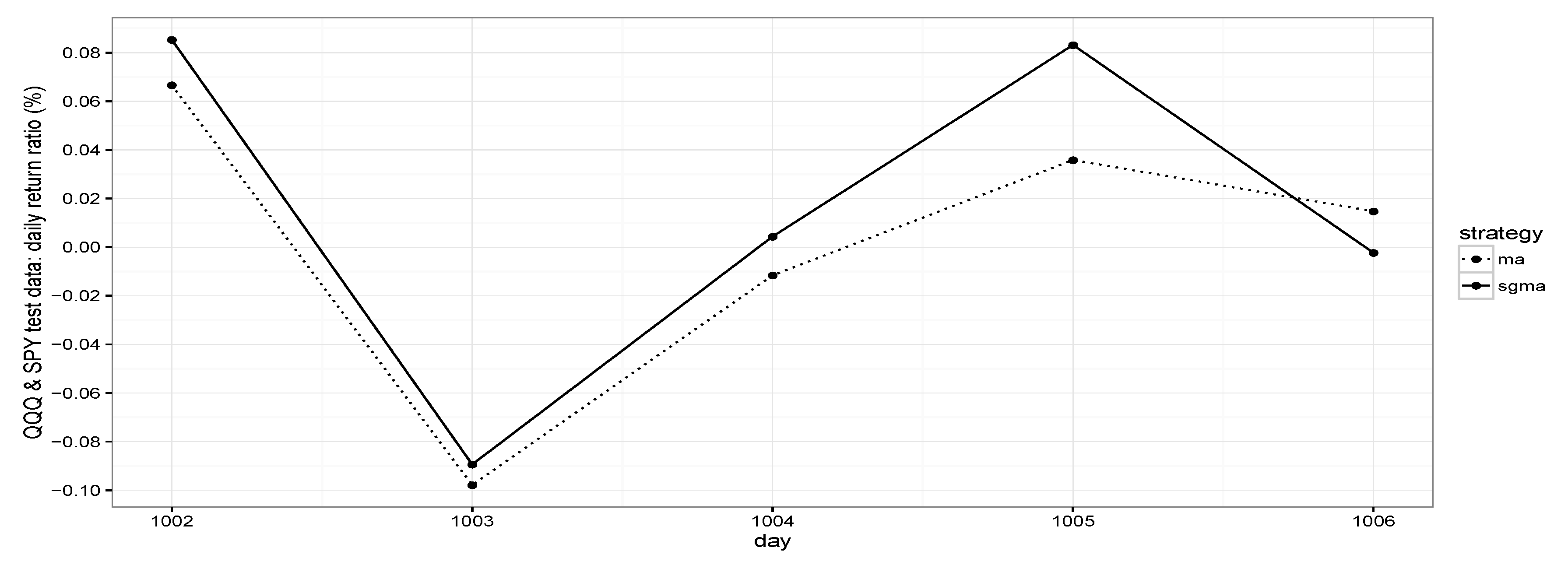

Table 8. The MGMA strategy evaluation summary for QQQ ETF and SPY ETF on day 1 (10 February 2017) to day 5 (10 June 2017) test data is provided in

Table 9.

Note that the MGMA strategy in general can outperform the MA strategy for both backward investments in training data and forward investments in test data. For example, for day 1 (10 February 2017), the MGMA strategy can increase the daily return ratio from to on training data, which equals an increase in annual return ratio of ; the MGMA strategy can increase the daily return ratio from to on test data, which equals an increase in annual return ratio of .

The MGMA strategy performance summary for QQQ ETF and SPY ETF on day 1 (10 February 2017) to day 5 (10 June 2017); training data are provided in

Figure 2. The MGMA strategy evaluation summary for QQQ ETF and SPY ETF on day 1 (10 February 2017) to day 5 (10 June 2017) test data is provided in

Figure 3.

6.3. Case 2: MGMA Strategy on High-Frequency Exchange-Traded Fund in Asian Market

We use the China 50 ETF (HuaXia) and Huatai-Pinebridge CSI 300 ETF (HuaTai). These are exchange-traded funds incorporated in China. The China 50 ETF (HuaXia) tracks the performance of the Shanghai Stock Exchange 50 Index (the SSE 50 Index). The holdings are weighted by market capitalization. As of 22 March 2018, the top five holding companies are PingAn Insurance Group, Shenzhen, China (PingAn, 12.30%), China Merchants Bank Co Ltd., Shenzhen, China (CMB, 5.65%), Kweichow Moutai Co Ltd., Zunyi China (600519, 5.41%), Industrial Bank Co Ltd., Fuzhou, China(IndBank, 4.81%), and China Minsheng Banking Corp Ltd., Beijing, China (CMAKY, 4.45%). The Huatai-Pinebridge CSI 300 ETF (HuaTai) is a capitalization-weighted stock market index designed to replicate the performance of the top 300 stocks traded in the Shanghai and Shenzhen stock exchange. As of 22 March 2018, the top three holding companies are PingAn Insurance Group, Shenzhen, China (PingAn, 4.17%), China Merchants Bank Co Ltd., Shenzhen, China (CMB, 2.34%), and Industrial Bank Co Ltd., Fuzhou, China (IndBank, 2.34%).

We collected daily second-level HuaXia ETF, HuaTai ETF, PingAn and IndBank price time series for this study. The HuaXia ETF price time series and HuaTai ETF price time series are used as the vector-based ETF price

. The PingAn and IndBank stock price time series are used as the vector-based predictive variable

. The collection period is the daily trading time from 8:30 p.m. to 2:00 a.m. (Eastern Time) to ensure a highly liquid market. Note that there is a break time from 10:30 p.m. to 0:00 a.m. (Eastern Time) for the Asian Market. We divide the HuaXia ETF and HuaTai ETF time series into two data sets: vector-based ETF price

training data (8:30 p.m. to 10:30 p.m. and 0:00 a.m. to 1:00 a.m., which contains 10,800 s) and vector-based ETF price

test data (1:00 a.m. to 2:00 a.m., which contains 3601 s). We use the PingAn and IndBank price time series as vector-based predictive variable

training data (8:30 p.m. to 10:30 p.m. and 0:00 a.m. to 1:00 a.m., which contains 10,800 s). We set initial wealth

and interest rate

. Suppose that the investor’s risk tolerance is

. We restrict

,

,

,

, and

in

,

s in

, and

l in

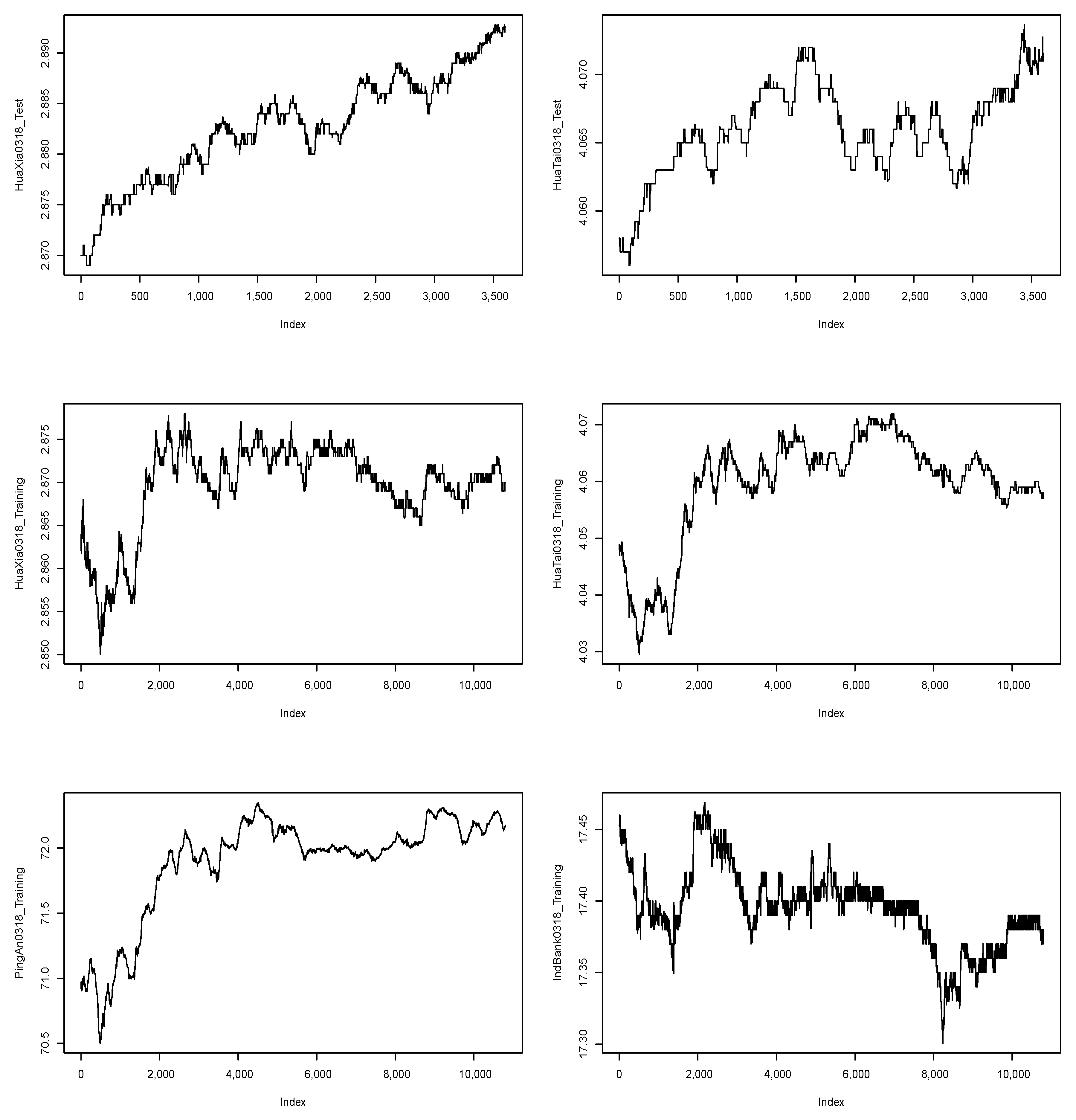

and 240. We use training data to choose model parameters with the highest return. We first report the MGMA strategy performance summary for HuaXia ETF and HuaTai ETF on training data; then, we report the MGMA strategy evaluation summary for HuaXia ETF and HuaTai ETF on test data. Our study spans five days from 18 March 2018 to 22 March 2018. We plot the second-level HuaTai ETF and HuaXia ETF price time series on day 1 (18 March 2018) in

Figure 4 as an example.

The MGMA strategy performance summary for HuaXia ETF and HuaTai ETF on day 1 (18 March 2018) to day 5 (22 March 2018) training data is provided in

Table 10. The MGMA strategy evaluation summary for HuaXia ETF and Huatai ETF on day 1 (18 March 2018) to day 5 (22 March 2018) test data is provided in

Table 11.

Note that the MGMA strategy in general can outperform the MA strategy for both backward investments on training data and forward investment on test data. Note that the optimal short-lag s, long-lag l, and allocation parameters to are all the same for 5 days, which might suggest that it is possible to use fixed parameters for MGMA strategy in reality.

The MGMA strategy performance summary for HuaXia ETF and HuaTai ETF on day 1 (18 March 2018) to day 5 (22 March 2018) training data is provided in

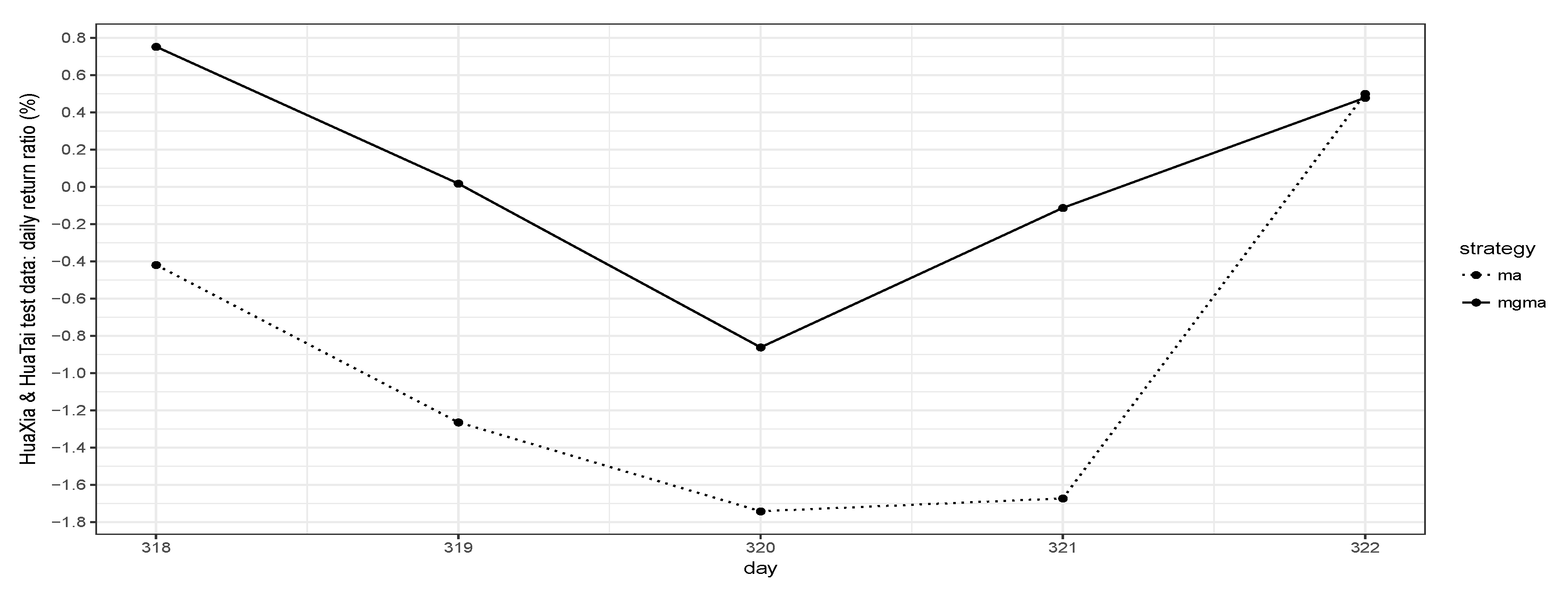

Figure 5. The MGMA strategy evaluation summary for HuaXia ETF and HuaTai ETF on day 1 (18 March 2018) to day 5 (22 March 2018) test data is provided in

Figure 6.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}