A Blockwise Empirical Likelihood Test for Gaussianity in Stationary Autoregressive Processes

Abstract

1. Introduction

2. The Blockwise Empirical Likelihood Ratio Test Statistic

3. Monte Carlo Simulation Procedures

3.1. Block Size Selection

3.2. Finite Sample Performance

- Standard normal ,

- Standard log-normal (Log N),

- Student t with 10 degrees of freedom ,

- Chi-squared with 1 and 10 degrees of freedom ,

- Beta with parameters (2, 1) ,

- Uniform on [0, 1] .

4. Real Data Applications

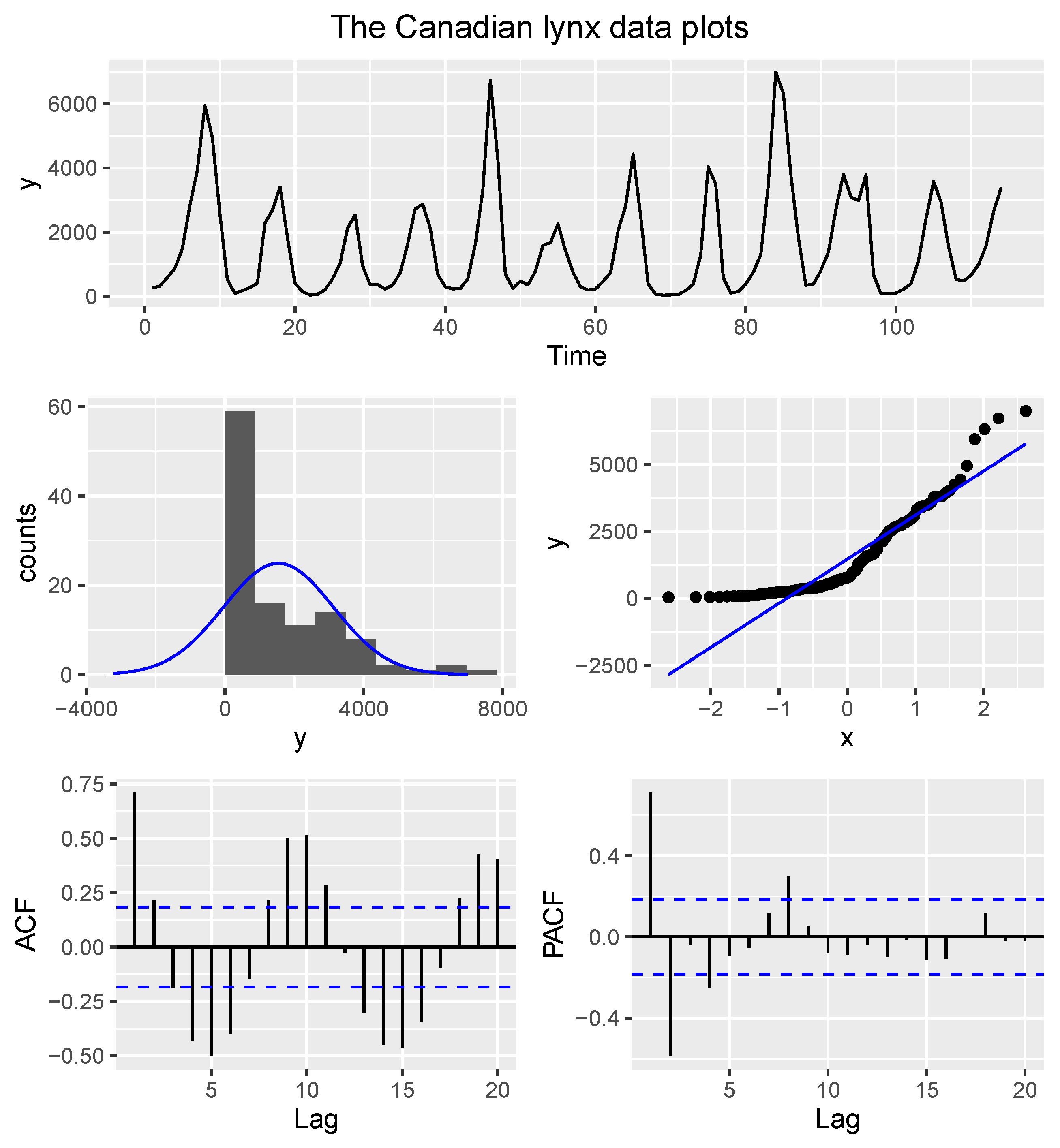

4.1. The Canadian Lynx Data

4.2. The Souvenir Data

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Epps, T.W. Testing that a stationary time series is Gaussian. Ann. Stat. 1987, 1683–1698. [Google Scholar] [CrossRef]

- Lobato, I.N.; Velasco, C. A simple test of normality for time series. Econom. Theory 2004, 20, 671–689. [Google Scholar] [CrossRef]

- Bai, J.; Ng, S. Tests for skewness, kurtosis, and normality for time series data. J. Bus. Econ. Stat. 2005, 23, 49–60. [Google Scholar] [CrossRef]

- Nieto-Reyes, A.; Cuesta-Albertos, J.A.; Gamboa, F. A random-projection based test of Gaussianity for stationary processes. Comput. Stat. Data Anal. 2014, 75, 124–141. [Google Scholar] [CrossRef]

- Psaradakis, Z.; Vávra, M. A distance test of normality for a wide class of stationary processes. Econom. Stat. 2017, 2, 50–60. [Google Scholar] [CrossRef]

- Moulines, E.; Choukri, K. Time-domain procedures for testing that a stationary time-series is Gaussian. IEEE Trans. Signal Process. 1996, 44, 2010–2025. [Google Scholar] [CrossRef]

- Bontemps, C.; Meddahi, N. Testing normality: A GMM approach. J. Econom. 2005, 124, 149–186. [Google Scholar] [CrossRef]

- Rao, T.S.; Gabr, M.M. A test for linearity of stationary time series. J. Time Ser. Anal. 1980, 1, 145–158. [Google Scholar] [CrossRef]

- Kitamura, Y. Empirical likelihood methods with weakly dependent processes. Ann. Stat. 1997, 25, 2084–2102. [Google Scholar] [CrossRef]

- Owen, A.B. Empirical likelihood ratio confidence intervals for a single functional. Biometrika 1988, 75, 237–249. [Google Scholar] [CrossRef]

- Owen, A. Empirical likelihood ratio confidence regions. Ann. Stat. 1990, 18, 90–120. [Google Scholar] [CrossRef]

- Shan, G.; Vexler, A.; Wilding, G.E.; Hutson, A.D. Simple and exact empirical likelihood ratio tests for normality based on moment relations. Commun. Stat. Comput. 2010, 40, 129–146. [Google Scholar] [CrossRef]

- Marange, C.S.; Qin, Y. A simple empirical likelihood ratio test for normality based on the moment constraints of a half-Normal distribution. J. Probab. Stat. 2018, 2018, 8094146. [Google Scholar] [CrossRef]

- Marange, C.S.; Qin, Y. A new empirical likelihood ratio goodness of fit test for normality based on moment constraints. Commun. Stat. Simul. Comput. 2019, 50, 1561–1575. [Google Scholar] [CrossRef]

- Marange, C.S.; Qin, Y. An Empirical Likelihood Ratio-Based Omnibus Test for Normality with an Adjustment for Symmetric Alternatives. J. Probab. Stat. 2021, 2021, 6661985. [Google Scholar] [CrossRef]

- Zhao, Y.; Moss, A.; Yang, H.; Zhang, Y. Jackknife empirical likelihood for the skewness and kurtosis. Stat. Its Interface 2018, 11, 709–719. [Google Scholar] [CrossRef]

- Lin, L.; Zhang, R. Blockwise empirical Euclidean likelihood for weakly dependent processes. Stat. Probab. Lett. 2001, 53, 143–152. [Google Scholar] [CrossRef]

- Bravo, F. Blockwise empirical entropy tests for time series regressions. J. Time Ser. Anal. 2005, 26, 185–210. [Google Scholar] [CrossRef]

- Bravo, F. Blockwise generalized empirical likelihood inference for non-linear dynamic moment conditions models. Econom. J. 2009, 12, 208–231. [Google Scholar] [CrossRef]

- Nordman, D.J.; Sibbertsen, P.; Lahiri, S.N. Empirical likelihood confidence intervals for the mean of a long-range dependent process. J. Time Ser. Anal. 2007, 28, 576–599. [Google Scholar] [CrossRef]

- Nordman, D.J. Tapered empirical likelihood for time series data in time and frequency domains. Biometrika 2009, 96, 119–132. [Google Scholar] [CrossRef]

- Chen, S.X.; Wong, C.M. Smoothed block empirical likelihood for quantiles of weakly dependent processes. Stat. Sin. 2009, 71–81. [Google Scholar]

- Chen, Y.Y.; Zhang, L.X. Empirical Euclidean likelihood for general estimating equations under association dependence. Appl. Math. J. Chin. Univ. 2010, 25, 437–446. [Google Scholar] [CrossRef]

- Wu, R.; Cao, J. Blockwise empirical likelihood for time series of counts. J. Multivar. Anal. 2011, 102, 661–673. [Google Scholar] [CrossRef]

- Lei, Q.; Qin, Y. Empirical likelihood for quantiles under negatively associated samples. J. Stat. Plan. Inference 2011, 141, 1325–1332. [Google Scholar] [CrossRef]

- Nordman, D.J.; Bunzel, H.; Lahiri, S.N. A nonstandard empirical likelihood for time series. Ann. Stat. 2013, 3050–3073. [Google Scholar] [CrossRef]

- Nordman, D.J.; Lahiri, S.N. A review of empirical likelihood methods for time series. J. Stat. Plan. Inference 2014, 155, 1–18. [Google Scholar] [CrossRef]

- Nelson, C.R. Applied Time Series Analysis for Managerial Forecasting; Holden-Day Inc.: San Francisco, CA, USA, 1973. [Google Scholar]

- Wei, W. Time Series Analysis; Addison-Wisley Publishing Company Inc.: Reading, MA, USA, 1990. [Google Scholar]

- Box, G.E.; Jenkins, G.M.; Reinsel, G.C. Time Series Analysis: Forecasting and Control, 3rd ed.; Prentice Hall: Englewood Cliffs, NJ, USA, 1994. [Google Scholar]

- Kim, Y.M.; Lahiri, S.N.; Nordman, D.J. A progressive block empirical likelihood method for time series. J. Am. Stat. Assoc. 2013, 108, 1506–1516. [Google Scholar] [CrossRef]

- Ploberger, W.; Krämer, W. The CUSUM test with OLS residuals. Econom. J. Econom. Soc. 1992, 271–285. [Google Scholar] [CrossRef]

- Gombay, E.; Horvath, L. An application of the maximum likelihood test to the change-point problem. Stoch. Process. Their Appl. 1994, 50, 161–171. [Google Scholar] [CrossRef]

- Gurevich, G.; Vexler, A. Change point problems in the model of logistic regression. J. Stat. Plan. Inference 2005, 131, 313–331. [Google Scholar] [CrossRef]

- Vexler, A.; Wu, C. An optimal retrospective change point detection policy. Scand. J. Stat. 2009, 36, 542–558. [Google Scholar] [CrossRef]

- Vexler, A.; Liu, A.; Pollak, M. Transformation of Changepoint Detection Methods into a Shiryayev-Roberts Form; Department of Biostatistics, The New York State University at Buffalo: Buffalo, NY, USA, 2006. [Google Scholar]

- Wilks, S.S. The large-sample distribution of the likelihood ratio for testing composite hypotheses. Ann. Math. Stat. 1938, 9, 60–62. [Google Scholar] [CrossRef]

- Hall, P.; Horowitz, J.L.; Jing, B.Y. On blocking rules for the bootstrap with dependent data. Biometrika 1995, 82, 561–574. [Google Scholar] [CrossRef]

- Lahiri, S.N. Resampling Methods for Dependent Data; Springer: New York, NY, USA, 2003. [Google Scholar]

- Andrews, D.W. Heteroskedasticity and autocorrelation consistent covariance matrix estimation. Econom. J. Econom. Soc. 1991, 59, 817–858. [Google Scholar] [CrossRef]

- Monti, A.C. Empirical likelihood confidence regions in time series models. Biometrika 1997, 84, 395–405. [Google Scholar] [CrossRef]

- Qin, Y.; Lei, Q. Empirical Likelihood for Mixed Regressive, Spatial Autoregressive Model Based on GMM. Sankhya A 2021, 83, 353–378. [Google Scholar] [CrossRef]

- Caner, M.; Kilian, L. Size distortions of tests of the null hypothesis of stationarity: Evidence and implications for the PPP debate. J. Int. Money Financ. 2001, 20, 639–657. [Google Scholar] [CrossRef]

- De Long, J.B.; Summers, L.H. Is Increased Price Flexibility Stabilizing? Natl. Bur. Econ. Res. 1986, 76, 1031–1044. [Google Scholar]

- Campbell, M.J.; Walker, A.M. A Survey of Statistical Work on the Mackenzie River Series of Annual Canadian Lynx Trappings for the Years 1821–1934 and a New Analysis. J. R. Stat. Soc. Ser. A 1977, 140, 411–431. [Google Scholar] [CrossRef]

- Tong, H. Some comments on the Canadian lynx data. J. R. Stat. Soc. Ser. A 1977, 140, 432–436. [Google Scholar] [CrossRef]

- Haggan, V.; Heravi, S.M.; Priestley, M.B. A study of the application of state-dependent models in non-linear time series analysis. J. Time Ser. Anal. 1984, 5, 69–102. [Google Scholar] [CrossRef]

- Makridakis, S.; Wheelwright, S.; Hyndman, R. Forecasting: Methods and Applications; John Willey & Sons: New York, NY, USA, 1998. [Google Scholar]

- Coghlan, A. A Little Book of R for Time Series; Release 0.2; Parasite Genomics Group, Wellcome Trust Sanger Institute: Cambridge, UK, 2017. [Google Scholar]

- Truong, P.; Novák, V. An Improved Forecasting and Detection of Structural Breaks in time Series Using Fuzzy Techniques; Contribution to Statistics; Springer: Cham, Switzerland, 2022. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| NOL Blocks | OL Blocks | |||||||

|---|---|---|---|---|---|---|---|---|

| −0.9 | 0.9998 | 0.9970 | 0.9522 | 0.9208 | 1.0000 | 0.9988 | 0.9810 | 0.9708 |

| −0.8 | 0.9976 | 0.9888 | 0.9374 | 0.9098 | 0.9992 | 0.9928 | 0.9716 | 0.9528 |

| −0.7 | 0.9938 | 0.9742 | 0.9266 | 0.8926 | 0.9960 | 0.9846 | 0.9588 | 0.9401 |

| −0.6 | 0.9850 | 0.9636 | 0.9230 | 0.8958 | 0.9914 | 0.9762 | 0.9512 | 0.9306 |

| −0.5 | 0.9778 | 0.9564 | 0.9116 | 0.8892 | 0.9846 | 0.9704 | 0.9436 | 0.9228 |

| −0.4 | 0.9706 | 0.9492 | 0.9076 | 0.8820 | 0.9784 | 0.9610 | 0.9384 | 0.9176 |

| −0.3 | 0.9630 | 0.9420 | 0.9072 | 0.8802 | 0.9688 | 0.9546 | 0.9322 | 0.9130 |

| −0.2 | 0.9562 | 0.9370 | 0.9026 | 0.8800 | 0.9600 | 0.9486 | 0.9272 | 0.9088 |

| −0.1 | 0.9504 | 0.9340 | 0.9000 | 0.8756 | 0.9530 | 0.9440 | 0.9224 | 0.9046 |

| 0 | 0.9402 | 0.9322 | 0.8924 | 0.8624 | 0.9444 | 0.9400 | 0.9258 | 0.8998 |

| 0.1 | 0.9300 | 0.9342 | 0.9054 | 0.8580 | 0.9266 | 0.9324 | 0.9088 | 0.8952 |

| 0.2 | 0.9180 | 0.9170 | 0.8948 | 0.8558 | 0.9254 | 0.9288 | 0.9064 | 0.8894 |

| 0.3 | 0.9010 | 0.9046 | 0.8896 | 0.8582 | 0.9122 | 0.9200 | 0.9026 | 0.8816 |

| 0.4 | 0.8852 | 0.8964 | 0.8848 | 0.8466 | 0.8880 | 0.9040 | 0.8996 | 0.8752 |

| 0.5 | 0.8578 | 0.8860 | 0.8794 | 0.8448 | 0.8570 | 0.8972 | 0.8868 | 0.8736 |

| 0.6 | 0.8254 | 0.8584 | 0.8634 | 0.8398 | 0.8134 | 0.8628 | 0.8748 | 0.8614 |

| 0.7 | 0.7514 | 0.8116 | 0.8274 | 0.8180 | 0.7620 | 0.8114 | 0.8478 | 0.8266 |

| 0.8 | 0.6526 | 0.7350 | 0.7824 | 0.7780 | 0.6482 | 0.7428 | 0.7896 | 0.7830 |

| 0.9 | 0.4538 | 0.5416 | 0.6438 | 0.6508 | 0.4716 | 0.5456 | 0.6474 | 0.6510 |

| Mean | 0.89 | 0.90 | 0.88 | 0.85 | 0.89 | 0.91 | 0.90 | 0.88 |

| MAD | 0.09 | 0.07 | 0.07 | 0.10 | 0.09 | 0.06 | 0.06 | 0.07 |

| −0.9 | 0.9870 | 0.9966 | 0.9792 | 0.9602 | 0.9924 | 0.9984 | 0.9906 | 0.9836 |

| −0.8 | 0.9832 | 0.9864 | 0.9608 | 0.9398 | 0.9890 | 0.9910 | 0.9772 | 0.9628 |

| −0.7 | 0.9768 | 0.9740 | 0.9490 | 0.9302 | 0.9848 | 0.9794 | 0.9678 | 0.9538 |

| −0.6 | 0.9744 | 0.9658 | 0.9398 | 0.9238 | 0.9804 | 0.9732 | 0.9630 | 0.9452 |

| −0.5 | 0.9708 | 0.9594 | 0.9372 | 0.9220 | 0.9768 | 0.9656 | 0.9592 | 0.9392 |

| −0.4 | 0.9668 | 0.9554 | 0.9338 | 0.9200 | 0.9696 | 0.9622 | 0.9552 | 0.9356 |

| −0.3 | 0.9628 | 0.9504 | 0.9326 | 0.9182 | 0.9644 | 0.9570 | 0.9524 | 0.9318 |

| −0.2 | 0.9586 | 0.9450 | 0.9310 | 0.9174 | 0.9592 | 0.9518 | 0.9502 | 0.9294 |

| −0.1 | 0.9532 | 0.9422 | 0.9282 | 0.9156 | 0.9538 | 0.9482 | 0.9474 | 0.9274 |

| 0 | 0.9424 | 0.9428 | 0.9298 | 0.9148 | 0.9534 | 0.9456 | 0.9344 | 0.9330 |

| 0.1 | 0.9422 | 0.9354 | 0.9246 | 0.9118 | 0.9402 | 0.9344 | 0.9322 | 0.9252 |

| 0.2 | 0.9258 | 0.9324 | 0.9224 | 0.9154 | 0.9374 | 0.9318 | 0.9304 | 0.9224 |

| 0.3 | 0.9158 | 0.9270 | 0.9130 | 0.9098 | 0.9260 | 0.9310 | 0.9308 | 0.9230 |

| 0.4 | 0.9142 | 0.9210 | 0.9228 | 0.9018 | 0.9012 | 0.9256 | 0.9296 | 0.9180 |

| 0.5 | 0.8880 | 0.9062 | 0.9126 | 0.9020 | 0.8922 | 0.9136 | 0.9158 | 0.9144 |

| 0.6 | 0.8594 | 0.8850 | 0.9088 | 0.8946 | 0.8654 | 0.9006 | 0.9050 | 0.9060 |

| 0.7 | 0.8182 | 0.8652 | 0.8918 | 0.8938 | 0.8094 | 0.8794 | 0.8968 | 0.9006 |

| 0.8 | 0.7348 | 0.7998 | 0.8558 | 0.8706 | 0.7350 | 0.8084 | 0.8692 | 0.8730 |

| 0.9 | 0.5880 | 0.6746 | 0.7578 | 0.7906 | 0.5614 | 0.6742 | 0.7664 | 0.8020 |

| Mean | 0.91 | 0.92 | 0.92 | 0.91 | 0.91 | 0.93 | 0.93 | 0.92 |

| MAD | 0.06 | 0.05 | 0.04 | 0.04 | 0.06 | 0.04 | 0.03 | 0.03 |

| NOL Blocks | OL Blocks | |||||||

|---|---|---|---|---|---|---|---|---|

| −0.9 | 0.9890 | 0.9886 | 0.9768 | 0.9610 | 0.9938 | 0.9884 | 0.9826 | 0.9780 |

| −0.8 | 0.9854 | 0.9800 | 0.9678 | 0.9492 | 0.9902 | 0.9821 | 0.9712 | 0.9668 |

| −0.7 | 0.9810 | 0.9764 | 0.9600 | 0.9428 | 0.9870 | 0.9764 | 0.9644 | 0.9594 |

| −0.6 | 0.9768 | 0.9704 | 0.9564 | 0.9398 | 0.9826 | 0.9707 | 0.9606 | 0.9556 |

| −0.5 | 0.9724 | 0.9652 | 0.9518 | 0.9388 | 0.9784 | 0.9664 | 0.9560 | 0.9522 |

| −0.4 | 0.9674 | 0.9630 | 0.9494 | 0.9360 | 0.9734 | 0.9631 | 0.9538 | 0.9506 |

| −0.3 | 0.9460 | 0.9592 | 0.9470 | 0.9334 | 0.9704 | 0.9602 | 0.9522 | 0.9480 |

| −0.2 | 0.9598 | 0.9566 | 0.9452 | 0.9316 | 0.9646 | 0.9564 | 0.9508 | 0.9462 |

| −0.1 | 0.9560 | 0.9528 | 0.9444 | 0.9314 | 0.9600 | 0.9544 | 0.9490 | 0.9440 |

| 0 | 0.9486 | 0.9496 | 0.9440 | 0.9212 | 0.9498 | 0.9540 | 0.9460 | 0.9346 |

| 0.1 | 0.9426 | 0.9440 | 0.9364 | 0.9302 | 0.9478 | 0.9458 | 0.9424 | 0.9356 |

| 0.2 | 0.9442 | 0.9384 | 0.9316 | 0.9224 | 0.9324 | 0.9426 | 0.9384 | 0.9306 |

| 0.3 | 0.9234 | 0.9280 | 0.9360 | 0.9216 | 0.9238 | 0.9384 | 0.9376 | 0.9344 |

| 0.4 | 0.9096 | 0.9312 | 0.9288 | 0.9198 | 0.9142 | 0.9330 | 0.9366 | 0.9272 |

| 0.5 | 0.8836 | 0.9262 | 0.9266 | 0.9182 | 0.8926 | 0.9240 | 0.9312 | 0.9290 |

| 0.6 | 0.8676 | 0.9092 | 0.9192 | 0.9160 | 0.8690 | 0.9118 | 0.9294 | 0.9336 |

| 0.7 | 0.8264 | 0.8778 | 0.9114 | 0.9140 | 0.8168 | 0.8914 | 0.9240 | 0.9274 |

| 0.8 | 0.7408 | 0.8304 | 0.8892 | 0.9018 | 0.7448 | 0.8498 | 0.9150 | 0.9076 |

| 0.9 | 0.5626 | 0.7070 | 0.8178 | 0.8372 | 0.5862 | 0.7280 | 0.8964 | 0.8548 |

| Mean | 0.91 | 0.93 | 0.93 | 0.92 | 0.91 | 0.93 | 0.94 | 0.94 |

| MAD | 0.06 | 0.04 | 0.02 | 0.03 | 0.06 | 0.03 | 0.02 | 0.02 |

| −0.9 | 0.9998 | 0.9860 | 0.9732 | 0.9638 | 1.0000 | 0.9868 | 0.9786 | 0.9720 |

| −0.8 | 0.9944 | 0.9776 | 0.9660 | 0.9504 | 0.9966 | 0.9792 | 0.9668 | 0.9586 |

| −0.7 | 0.9830 | 0.9720 | 0.9606 | 0.9470 | 0.9878 | 0.9732 | 0.9600 | 0.9524 |

| −0.6 | 0.9750 | 0.9664 | 0.9562 | 0.9430 | 0.9776 | 0.9690 | 0.9564 | 0.9500 |

| −0.5 | 0.9676 | 0.9616 | 0.9540 | 0.9416 | 0.9722 | 0.9642 | 0.9522 | 0.9482 |

| −0.4 | 0.9618 | 0.9598 | 0.9524 | 0.9402 | 0.9680 | 0.9604 | 0.9502 | 0.9454 |

| −0.3 | 0.9570 | 0.9568 | 0.9508 | 0.9386 | 0.9634 | 0.9572 | 0.9484 | 0.9450 |

| −0.2 | 0.9530 | 0.9552 | 0.9490 | 0.9380 | 0.9592 | 0.9550 | 0.9474 | 0.9440 |

| −0.1 | 0.9502 | 0.9524 | 0.9480 | 0.9374 | 0.9560 | 0.9534 | 0.9454 | 0.9418 |

| 0 | 0.9504 | 0.9488 | 0.9422 | 0.9404 | 0.9486 | 0.9570 | 0.9442 | 0.9414 |

| 0.1 | 0.9428 | 0.9442 | 0.9404 | 0.9406 | 0.9432 | 0.9494 | 0.9482 | 0.9442 |

| 0.2 | 0.9402 | 0.9450 | 0.9368 | 0.9396 | 0.9380 | 0.9472 | 0.9452 | 0.9464 |

| 0.3 | 0.9256 | 0.9354 | 0.9464 | 0.9348 | 0.9332 | 0.9428 | 0.9436 | 0.9372 |

| 0.4 | 0.9216 | 0.9360 | 0.9430 | 0.9318 | 0.9250 | 0.9334 | 0.9360 | 0.9414 |

| 0.5 | 0.9148 | 0.9324 | 0.9338 | 0.9368 | 0.9166 | 0.9296 | 0.9374 | 0.9402 |

| 0.6 | 0.8856 | 0.9246 | 0.9294 | 0.9284 | 0.8722 | 0.9194 | 0.9344 | 0.9360 |

| 0.7 | 0.8412 | 0.9064 | 0.9306 | 0.9288 | 0.8550 | 0.9012 | 0.9290 | 0.9264 |

| 0.8 | 0.7870 | 0.8696 | 0.9066 | 0.9186 | 0.7814 | 0.8652 | 0.9030 | 0.9124 |

| 0.9 | 0.6516 | 0.7660 | 0.8492 | 0.8882 | 0.6476 | 0.7626 | 0.8628 | 0.8842 |

| Mean | 0.92 | 0.94 | 0.94 | 0.94 | 0.92 | 0.94 | 0.94 | 0.94 |

| MAD | 0.05 | 0.03 | 0.02 | 0.02 | 0.05 | 0.03 | 0.02 | 0.01 |

| NOL Blocks | OL Blocks | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| b | Log N | Log N | |||||||

| −0.9 | 0.0636 | 0.0474 | 0.0670 | 0.0512 | 0.0240 | 0.0460 | 0.0470 | 0.0564 | |

| 0.0986 | 0.0502 | 0.0676 | 0.0468 | 0.0382 | 0.0486 | 0.0616 | 0.0652 | ||

| −0.5 | 0.9884 | 0.0632 | 0.5088 | 0.2832 | 0.9928 | 0.0620 | 0.5098 | 0.2908 | |

| 0.9806 | 0.0542 | 0.4582 | 0.2484 | 0.9846 | 0.0538 | 0.4578 | 0.2630 | ||

| 0 | 1.0000 | 0.0690 | 0.8842 | 0.9996 | 1.0000 | 0.0772 | 0.8730 | 0.9988 | |

| 1.0000 | 0.0518 | 0.8464 | 0.9948 | 1.0000 | 0.0586 | 0.8250 | 0.9938 | ||

| 0.5 | 0.9996 | 0.0544 | 0.4812 | 0.4612 | 1.0000 | 0.0532 | 0.4456 | 0.4244 | |

| 0.9984 | 0.0396 | 0.3624 | 0.4046 | 0.9954 | 0.0452 | 0.3272 | 0.3836 | ||

| 0.6 | 0.9964 | 0.0544 | 0.3000 | 0.2486 | 0.9948 | 0.0456 | 0.3064 | 0.2146 | |

| 0.9896 | 0.0314 | 0.2196 | 0.2328 | 0.9764 | 0.0470 | 0.2346 | 0.2208 | ||

| 0.7 | 0.9672 | 0.0470 | 0.1978 | 0.1198 | 0.9542 | 0.0506 | 0.1924 | 0.1218 | |

| 0.9226 | 0.0400 | 0.1204 | 0.1206 | 0.8884 | 0.0476 | 0.1282 | 0.1124 | ||

| 0.8 | 0.7766 | 0.0516 | 0.1048 | 0.0656 | 0.7674 | 0.0518 | 0.0998 | 0.0612 | |

| 0.6770 | 0.0260 | 0.0720 | 0.0760 | 0.6450 | 0.0420 | 0.0706 | 0.0728 | ||

| 0.9 | 0.3268 | 0.0562 | 0.0596 | 0.0858 | 0.3284 | 0.1012 | 0.0595 | 0.0828 | |

| 0.3118 | 0.0490 | 0.0558 | 0.0552 | 0.2928 | 0.0770 | 0.0520 | 0.0544 | ||

| −0.9 | 0.7696 | 0.0496 | 0.1158 | 0.0600 | 0.6694 | 0.0442 | 0.1060 | 0.0652 | |

| 0.7984 | 0.0490 | 0.1288 | 0.0550 | 0.6254 | 0.0462 | 0.1146 | 0.0562 | ||

| −0.5 | 1.0000 | 0.0974 | 0.9988 | 0.9186 | 1.0000 | 0.0974 | 0.9990 | 0.9282 | |

| 1.0000 | 0.0808 | 0.9986 | 0.8860 | 0.9994 | 0.0892 | 0.9992 | 0.8962 | ||

| 0 | 1.0000 | 0.4280 | 1.0000 | 1.0000 | 1.0000 | 0.4474 | 1.0000 | 1.0000 | |

| 1.0000 | 0.3596 | 1.0000 | 1.0000 | 1.0000 | 0.4050 | 1.0000 | 1.0000 | ||

| 0.5 | 1.0000 | 0.2174 | 0.9982 | 0.9906 | 1.0000 | 0.2280 | 0.9990 | 0.9914 | |

| 1.0000 | 0.1954 | 0.9972 | 0.9880 | 1.0000 | 0.1818 | 0.9960 | 0.9842 | ||

| 0.6 | 1.0000 | 0.1332 | 0.9778 | 0.7884 | 1.0000 | 0.1364 | 0.9730 | 0.7884 | |

| 1.0000 | 0.1090 | 0.9656 | 0.7754 | 1.0000 | 0.1156 | 0.9618 | 0.7704 | ||

| 0.7 | 1.0000 | 0.0802 | 0.8274 | 0.3436 | 1.0000 | 0.0802 | 0.8420 | 0.3524 | |

| 1.0000 | 0.0738 | 0.7862 | 0.3622 | 1.0000 | 0.0730 | 0.7890 | 0.3512 | ||

| 0.8 | 1.0000 | 0.0572 | 0.4684 | 0.1204 | 1.0000 | 0.0600 | 0.4742 | 0.1092 | |

| 1.0000 | 0.0516 | 0.4388 | 0.1310 | 0.9998 | 0.0506 | 0.4166 | 0.1248 | ||

| 0.9 | 0.9610 | 0.0576 | 0.1576 | 0.0558 | 0.9616 | 0.0518 | 0.1404 | 0.0490 | |

| 0.9508 | 0.0484 | 0.1242 | 0.0564 | 0.9466 | 0.0462 | 0.1254 | 0.0516 | ||

| −0.9 | 0.9832 | 0.0562 | 0.2254 | 0.0556 | 0.9836 | 0.0482 | 0.2190 | 0.0632 | |

| 0.9842 | 0.0520 | 0.2448 | 0.0526 | 0.9696 | 0.0502 | 0.2130 | 0.0482 | ||

| −0.5 | 1.0000 | 0.1926 | 1.0000 | 1.0000 | 1.0000 | 0.2130 | 1.0000 | 1.0000 | |

| 1.0000 | 0.1862 | 1.0000 | 0.9974 | 1.0000 | 0.1770 | 1.0000 | 0.9986 | ||

| 0 | 1.0000 | 0.8058 | 1.0000 | 1.0000 | 1.0000 | 0.8220 | 1.0000 | 1.0000 | |

| 1.0000 | 0.7844 | 1.0000 | 1.0000 | 1.0000 | 0.7946 | 1.0000 | 1.0000 | ||

| 0.5 | 1.0000 | 0.4934 | 1.0000 | 1.0000 | 1.0000 | 0.4788 | 1.0000 | 1.0000 | |

| 1.0000 | 0.4656 | 0.9998 | 0.9970 | 1.0000 | 0.4860 | 1.0000 | 1.0000 | ||

| 0.6 | 1.0000 | 0.2872 | 1.0000 | 0.9782 | 1.0000 | 0.3018 | 1.0000 | 0.9818 | |

| 1.0000 | 0.2710 | 0.9936 | 0.9768 | 1.0000 | 0.2882 | 0.9998 | 0.9754 | ||

| 0.7 | 1.0000 | 0.1354 | 0.9862 | 0.6346 | 1.0000 | 0.1422 | 0.9852 | 0.6174 | |

| 1.0000 | 0.1296 | 0.9790 | 0.6280 | 1.0000 | 0.1426 | 0.9846 | 0.6170 | ||

| 0.8 | 1.0000 | 0.0746 | 0.7962 | 0.1862 | 1.0000 | 0.0654 | 0.7786 | 0.1744 | |

| 1.0000 | 0.0720 | 0.7476 | 0.1912 | 1.0000 | 0.0652 | 0.7372 | 0.1840 | ||

| 0.9 | 0.9992 | 0.0474 | 0.2714 | 0.0610 | 0.9994 | 0.0530 | 0.2564 | 0.0658 | |

| 0.9966 | 0.0472 | 0.2330 | 0.0608 | 0.9992 | 0.0500 | 0.2388 | 0.0606 | ||

| Rejection Rates for | ||||||||

|---|---|---|---|---|---|---|---|---|

| Test | Log N | (2,1) | ||||||

| −0.9 | BELT | 0.0474 | 0.0226 | 0.0478 | 0.0280 | 0.0684 | 0.0514 | 0.0574 |

| EPPS | 0.1268 | 0.0534 | 0.1216 | 0.0728 | 0.1226 | 0.1438 | 0.1574 | |

| LV | 0.0284 | 0.1454 | 0.0316 | 0.0892 | 0.0400 | 0.0224 | 0.0234 | |

| PV | 0.0628 | 0.2972 | 0.0640 | 0.1642 | 0.0880 | 0.0824 | 0.0302 | |

| −0.5 | BELT | 0.0530 | 0.9950 | 0.0610 | 0.9966 | 0.4956 | 0.4862 | 0.2932 |

| EPPS | 0.0712 | 0.6810 | 0.0532 | 0.8528 | 0.2044 | 0.4840 | 0.5538 | |

| LV | 0.0456 | 0.9994 | 0.1896 | 0.9988 | 0.4794 | 0.1698 | 0.0096 | |

| PV | 0.0482 | 0.9984 | 0.1286 | 0.9980 | 0.3584 | 0.3780 | 0.2664 | |

| 0 | BELT | 0.0468 | 1.0000 | 0.0552 | 1.0000 | 0.8868 | 0.9576 | 0.9978 |

| EPPS | 0.0632 | 0.9672 | 0.0858 | 0.9960 | 0.5426 | 0.9706 | 0.9948 | |

| LV | 0.0428 | 1.0000 | 0.2950 | 1.0000 | 0.7820 | 0.7460 | 0.5446 | |

| PV | 0.0484 | 1.0000 | 0.1568 | 1.0000 | 0.8048 | 0.9820 | 0.9602 | |

| 0.5 | BELT | 0.0510 | 0.9998 | 0.0532 | 0.9996 | 0.4534 | 0.3762 | 0.4248 |

| EPPS | 0.0732 | 0.8566 | 0.0646 | 0.9598 | 0.2658 | 0.5590 | 0.5668 | |

| LV | 0.0342 | 0.9978 | 0.1578 | 0.9984 | 0.4160 | 0.1030 | 0.0002 | |

| PV | 0.0384 | 0.9998 | 0.0862 | 0.9992 | 0.4040 | 0.4242 | 0.1100 | |

| 0.6 | BELT | 0.0554 | 0.9960 | 0.0520 | 0.9962 | 0.3084 | 0.2122 | 0.2214 |

| EPPS | 0.0750 | 0.6182 | 0.0610 | 0.8188 | 0.1990 | 0.3596 | 0.3392 | |

| LV | 0.0332 | 0.9872 | 0.1204 | 0.9738 | 0.2848 | 0.0676 | 0.0020 | |

| PV | 0.0660 | 0.9932 | 0.0826 | 0.9864 | 0.2932 | 0.2108 | 0.0510 | |

| 0.7 | BELT | 0.0524 | 0.9624 | 0.0500 | 0.9494 | 0.1986 | 0.1540 | 0.1064 |

| EPPS | 0.0798 | 0.3232 | 0.0664 | 0.4846 | 0.1462 | 0.2170 | 0.2158 | |

| LV | 0.0324 | 0.9050 | 0.0832 | 0.8292 | 0.1646 | 0.0382 | 0.0028 | |

| PV | 0.0600 | 0.9340 | 0.0868 | 0.8900 | 0.1520 | 0.0846 | 0.0326 | |

| 0.8 | BELT | 0.0482 | 0.7980 | 0.0488 | 0.7238 | 0.0952 | 0.0986 | 0.0606 |

| EPPS | 0.1104 | 0.1464 | 0.0972 | 0.2038 | 0.1308 | 0.1576 | 0.1636 | |

| LV | 0.0154 | 0.6246 | 0.0408 | 0.4400 | 0.0658 | 0.0240 | 0.0050 | |

| PV | 0.0648 | 0.6964 | 0.0684 | 0.5388 | 0.0920 | 0.0692 | 0.0546 | |

| 0.9 | BELT | 0.0522 | 0.4330 | 0.0502 | 0.2026 | 0.0576 | 0.1026 | 0.0874 |

| EPPS | 0.1708 | 0.1304 | 0.1474 | 0.1390 | 0.1516 | 0.1832 | 0.1844 | |

| LV | 0.0092 | 0.1750 | 0.0142 | 0.0836 | 0.0184 | 0.0048 | 0.0002 | |

| PV | 0.0782 | 0.3020 | 0.0744 | 0.1830 | 0.0840 | 0.0642 | 0.0324 | |

| Rejection Rates for | ||||||||

|---|---|---|---|---|---|---|---|---|

| Test | Log N | (2,1) | ||||||

| −0.9 | BELT | 0.0490 | 0.6774 | 0.0478 | 0.4806 | 0.1046 | 0.0904 | 0.0538 |

| EPPS | 0.0760 | 0.3736 | 0.0594 | 0.2214 | 0.0694 | 0.0896 | 0.0986 | |

| LV | 0.0692 | 0.8852 | 0.0866 | 0.6136 | 0.1222 | 0.0728 | 0.0562 | |

| PV | 0.0460 | 0.7134 | 0.0780 | 0.3820 | 0.0630 | 0.0660 | 0.0492 | |

| −0.5 | BELT | 0.0466 | 1.0000 | 0.0888 | 1.0000 | 0.9986 | 0.9992 | 0.9248 |

| EPPS | 0.0604 | 0.9998 | 0.1372 | 1.0000 | 0.7692 | 0.9900 | 0.9928 | |

| LV | 0.0422 | 1.0000 | 0.4564 | 1.0000 | 0.9942 | 0.9968 | 0.9638 | |

| PV | 0.0558 | 1.0000 | 0.2216 | 1.0000 | 0.9680 | 0.9954 | 0.9570 | |

| 0 | BELT | 0.0560 | 1.0000 | 0.3856 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| EPPS | 0.0554 | 1.0000 | 0.3266 | 1.0000 | 0.9976 | 1.0000 | 1.0000 | |

| LV | 0.0452 | 1.0000 | 0.7436 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| PV | 0.0452 | 1.0000 | 0.4938 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| 0.5 | BELT | 0.0520 | 1.0000 | 0.1900 | 1.0000 | 0.9958 | 0.9982 | 0.9888 |

| EPPS | 0.0610 | 1.0000 | 0.1494 | 1.0000 | 0.8748 | 0.9972 | 0.9948 | |

| LV | 0.0430 | 1.0000 | 0.4528 | 1.0000 | 0.9938 | 0.9960 | 0.9708 | |

| PV | 0.0384 | 1.0000 | 0.2072 | 1.0000 | 0.9930 | 0.9980 | 0.9196 | |

| 0.6 | BELT | 0.0542 | 1.0000 | 0.1218 | 1.0000 | 0.9766 | 0.9226 | 0.7842 |

| EPPS | 0.0596 | 0.9994 | 0.1040 | 1.0000 | 0.7276 | 0.9060 | 0.8186 | |

| LV | 0.0482 | 1.0000 | 0.3238 | 1.0000 | 0.9558 | 0.8890 | 0.4742 | |

| PV | 0.0420 | 1.0000 | 0.1386 | 0.9990 | 0.9274 | 0.9172 | 0.4590 | |

| 0.7 | BELT | 0.0534 | 1.0000 | 0.0856 | 1.0000 | 0.8334 | 0.6234 | 0.3440 |

| EPPS | 0.0634 | 0.9998 | 0.0824 | 1.0000 | 0.4724 | 0.5792 | 0.4224 | |

| LV | 0.0414 | 1.0000 | 0.2088 | 1.0000 | 0.7392 | 0.4152 | 0.0690 | |

| PV | 0.0480 | 0.9970 | 0.1074 | 0.9968 | 0.7186 | 0.5494 | 0.0842 | |

| 0.8 | BELT | 0.0512 | 1.0000 | 0.0742 | 1.0000 | 0.4812 | 0.2648 | 0.1168 |

| EPPS | 0.0850 | 0.9812 | 0.0728 | 0.9622 | 0.2554 | 0.2584 | 0.1844 | |

| LV | 0.0410 | 1.0000 | 0.1174 | 0.9988 | 0.3758 | 0.1288 | 0.0166 | |

| PV | 0.0514 | 0.9896 | 0.0752 | 0.9920 | 0.3744 | 0.2070 | 0.0308 | |

| 0.9 | BELT | 0.0450 | 0.9582 | 0.0422 | 0.8414 | 0.1450 | 0.0878 | 0.0584 |

| EPPS | 0.1174 | 0.5838 | 0.0962 | 0.4574 | 0.1516 | 0.1580 | 0.1430 | |

| LV | 0.0176 | 0.8318 | 0.0384 | 0.5552 | 0.0688 | 0.0218 | 0.0100 | |

| PV | 0.0452 | 0.5176 | 0.0720 | 0.3350 | 0.0212 | 0.0104 | 0.0072 | |

| Rejection Rates for | ||||||||

|---|---|---|---|---|---|---|---|---|

| Test | Log N | (2,1) | ||||||

| −0.9 | BELT | 0.0510 | 0.9816 | 0.0474 | 0.9098 | 0.2172 | 0.1236 | 0.0646 |

| EPPS | 0.0688 | 0.7914 | 0.0542 | 0.4806 | 0.0822 | 0.0786 | 0.0990 | |

| LV | 0.0910 | 0.9920 | 0.1182 | 0.8958 | 0.2408 | 0.1294 | 0.0684 | |

| PV | 0.0590 | 0.9240 | 0.0520 | 0.6160 | 0.0840 | 0.0450 | 0.0520 | |

| −0.5 | BELT | 0.0480 | 1.0000 | 0.2096 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| EPPS | 0.0544 | 1.0000 | 0.2508 | 1.0000 | 0.9784 | 1.0000 | 1.0000 | |

| LV | 0.0464 | 1.0000 | 0.6976 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| PV | 0.0520 | 1.0000 | 0.4010 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| 0 | BELT | 0.0496 | 1.0000 | 0.8112 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| EPPS | 0.0572 | 1.0000 | 0.5934 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| LV | 0.0488 | 1.0000 | 0.9422 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| PV | 0.0480 | 1.0000 | 0.7910 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| 0.5 | BELT | 0.0560 | 1.0000 | 0.4866 | 1.0000 | 1.0000 | 1.0000 | 1.0000 |

| EPPS | 0.0560 | 1.0000 | 0.2586 | 1.0000 | 0.9940 | 1.0000 | 1.0000 | |

| LV | 0.0488 | 1.0000 | 0.6720 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| PV | 0.0490 | 1.0000 | 0.3960 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | |

| 0.6 | BELT | 0.0442 | 1.0000 | 0.3028 | 1.0000 | 1.0000 | 1.0000 | 0.9798 |

| EPPS | 0.0572 | 1.0000 | 0.1738 | 1.0000 | 0.9592 | 0.9972 | 0.9826 | |

| LV | 0.0438 | 1.0000 | 0.4970 | 1.0000 | 0.9996 | 1.0000 | 0.9722 | |

| PV | 0.0590 | 0.9994 | 0.2300 | 1.0000 | 0.9998 | 0.9992 | 0.8800 | |

| 0.7 | BELT | 0.0552 | 1.0000 | 0.1394 | 1.0000 | 0.9888 | 0.9202 | 0.6256 |

| EPPS | 0.0618 | 0.9998 | 0.1016 | 1.0000 | 0.7678 | 0.8564 | 0.6302 | |

| LV | 0.0470 | 1.0000 | 0.3144 | 1.0000 | 0.9774 | 0.8898 | 0.3628 | |

| PV | 0.0490 | 1.0000 | 0.1404 | 0.9990 | 0.9580 | 0.9072 | 0.2490 | |

| 0.8 | BELT | 0.0468 | 1.0000 | 0.0690 | 1.0000 | 0.7744 | 0.4996 | 0.1740 |

| EPPS | 0.0744 | 1.0000 | 0.0754 | 0.9996 | 0.4172 | 0.4036 | 0.2364 | |

| LV | 0.0510 | 1.0000 | 0.1512 | 1.0000 | 0.6782 | 0.3184 | 0.0408 | |

| PV | 0.0622 | 0.9930 | 0.0880 | 0.9924 | 0.6550 | 0.3826 | 0.0430 | |

| 0.9 | BELT | 0.0496 | 1.0000 | 0.0536 | 0.9886 | 0.2578 | 0.1454 | 0.0652 |

| EPPS | 0.0902 | 0.9200 | 0.0882 | 0.7720 | 0.1780 | 0.1624 | 0.1220 | |

| LV | 0.0362 | 0.9924 | 0.0538 | 0.9008 | 0.1550 | 0.0624 | 0.0120 | |

| PV | 0.0514 | 0.5760 | 0.0560 | 0.4746 | 0.0008 | 0.0006 | 0.0002 | |

| Power Rankings | |||||||

|---|---|---|---|---|---|---|---|

| n | Ranking | Log N | (2,1) | ||||

| 100 | 1 | BELT, PV | LV | BELT | BELT | EPPS | EPPS |

| 2 | LV | EPPS, PV | PV | LV, PV | BELT, PV | BELT | |

| 3 | EPPS | BELT | LV | EPPS | LV | PV | |

| 4 | EPPS | LV | |||||

| 500 | 1 | BELT, LV | LV | BELT | BELT | BELT, EPPS | EPPS |

| 2 | PV | PV | LV | LV | PV, LV | BELT | |

| 3 | EPPS | BELT | PV, EPPS | PV | PV, LV | ||

| 4 | EPPS | EPPS | |||||

| 1000 | 1 | BELT, LV | LV | BELT | BELT | BELT | EPPS |

| 2 | PV, EPPS | PV, BELT | LV | LV | EPPS | BELT | |

| 3 | EPPS | EPPS, PV | PV | LV, PV | LV | ||

| 4 | EPPS | PV | |||||

| Test | Replications | Elapsed | Relative | User.self | Sys.self |

|---|---|---|---|---|---|

| BELT | 1000 | 13.91 | 5.434 | 13.31 | 0.59 |

| EPPS | 1000 | 8.09 | 3.160 | 7.40 | 0.66 |

| LV | 1000 | 2.56 | 1.000 | 2.47 | 0.09 |

| PV | 1000 | 1394.86 | 544.867 | 1381.02 | 13.16 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Marange, C.S.; Qin, Y.; Chiruka, R.T.; Batidzirai, J.M. A Blockwise Empirical Likelihood Test for Gaussianity in Stationary Autoregressive Processes. Mathematics 2023, 11, 1041. https://doi.org/10.3390/math11041041

Marange CS, Qin Y, Chiruka RT, Batidzirai JM. A Blockwise Empirical Likelihood Test for Gaussianity in Stationary Autoregressive Processes. Mathematics. 2023; 11(4):1041. https://doi.org/10.3390/math11041041

Chicago/Turabian StyleMarange, Chioneso S., Yongsong Qin, Raymond T. Chiruka, and Jesca M. Batidzirai. 2023. "A Blockwise Empirical Likelihood Test for Gaussianity in Stationary Autoregressive Processes" Mathematics 11, no. 4: 1041. https://doi.org/10.3390/math11041041

APA StyleMarange, C. S., Qin, Y., Chiruka, R. T., & Batidzirai, J. M. (2023). A Blockwise Empirical Likelihood Test for Gaussianity in Stationary Autoregressive Processes. Mathematics, 11(4), 1041. https://doi.org/10.3390/math11041041