Comparative Study on Lower-Middle-, Upper-Middle-, and Higher-Income Economies of ASEAN for Fiscal and Current Account Deficits: A Panel Econometric Analysis

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

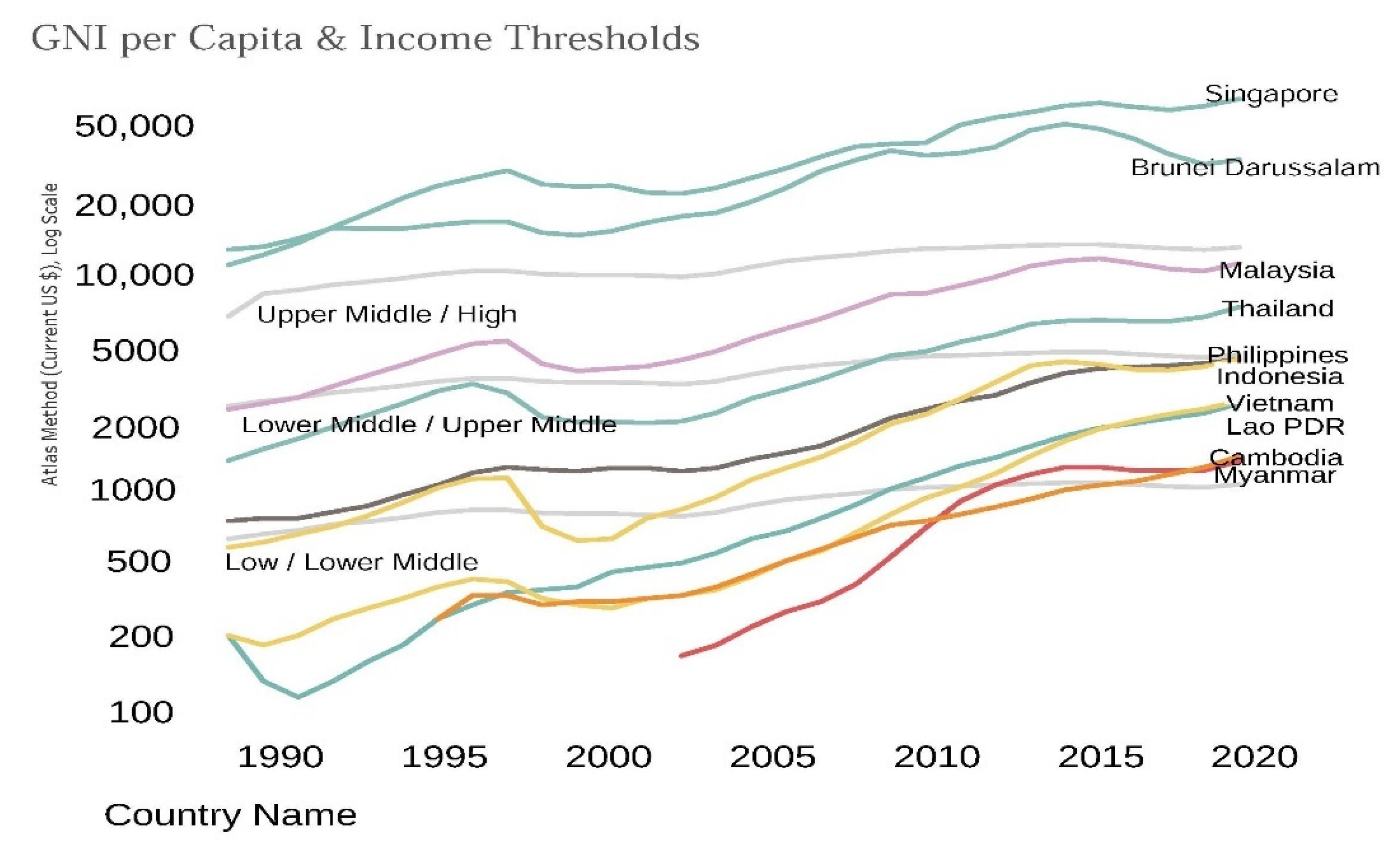

3.1. Data and Variables

3.2. Empirical Model

3.2.1. Panel Unit Root Test

3.2.2. Panel Cointegration Autoregressive Distributed Lag (ARDL)

3.2.3. Panel Cointegration Regression

3.2.4. Dumitrescu and Hurlin (DH) Granger Panel Causality Test

3.2.5. Diagnostic Checks

Endogeneity

Heteroscedasticity

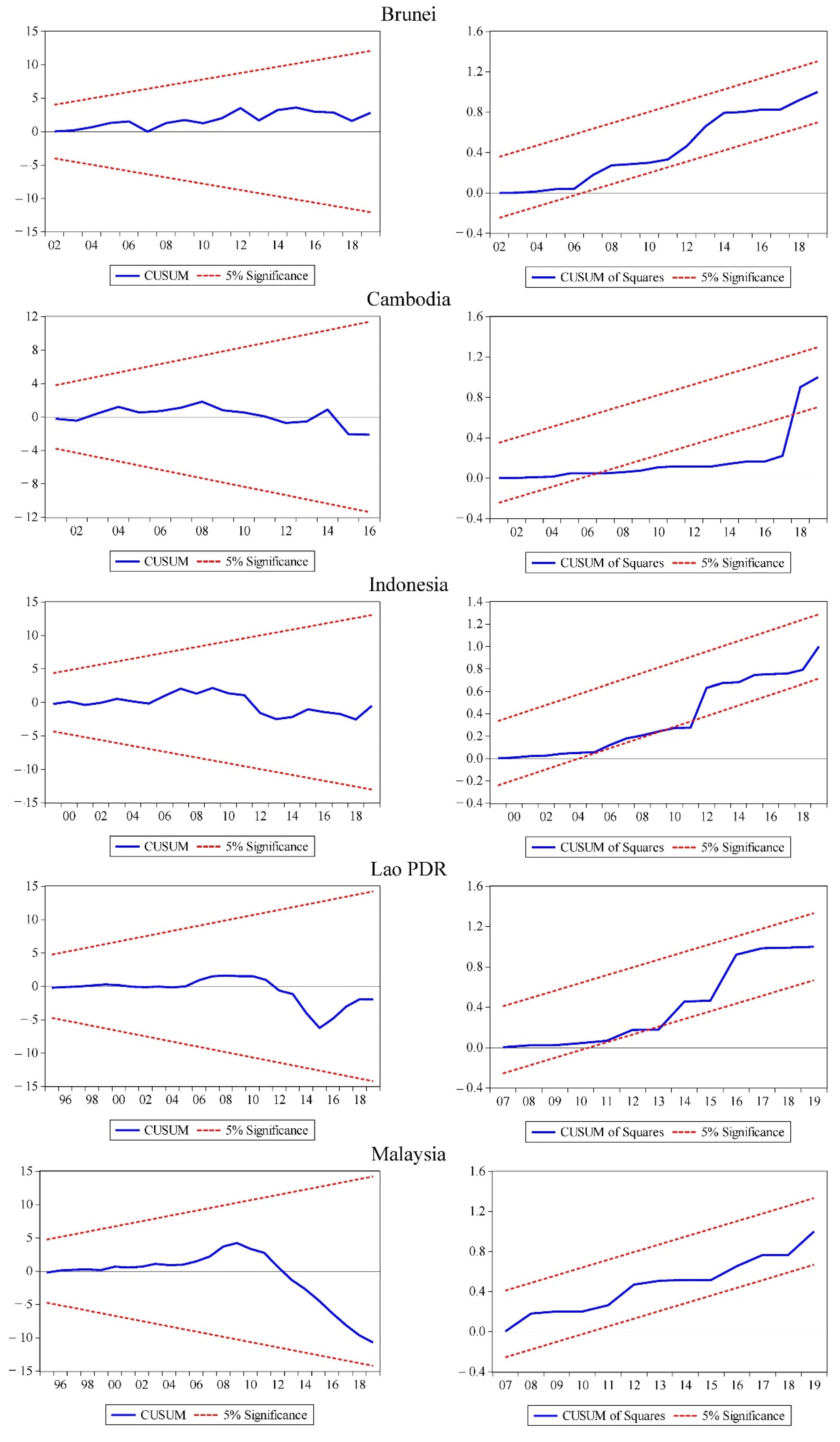

3.2.6. Stability Checks

4. Empirical Findings

4.1. Findings from Panel Unit Root Testing

4.2. Fixed/Random Effects for Panel Data

4.3. Findings of Panel ARDL for Three Sub-Groups

4.4. Findings of Panel Cointegration Regression

4.5. DH Granger Causality Analysis for ASEAN’s Income Groups

4.6. Diagnostic Checks

4.7. Findings of Stability Diagnostics

5. Discussion

6. Conclusions

7. Policy Implications

- In LMIE, policy practitioners can target the current account balance, as it monitors the trade competitiveness to evaluate the flow of net exports. A unidirectional relationship from CAD to FD indicates that the current account is initiating the fiscal deficit, and external imbalance is transmitted to national accounts via automatic stabilizers.

- The results for UMIE can illuminate to the policymakers that the fiscal deficit does not cause the trade balance in the context of the twin deficit hypothesis. However, the fiscal deficit can influence and has a consequence on the current account deficit in the long run. Hence, the fiscal deficit and the exchange rate can be the targeted factors for authorities.

- Fiscal policy tools can be utilized to achieve favorable current accounts in HIE. Practitioners can target the current account balance to minimize the fiscal deficit. The current account targeting hypothesis (CATH) leads to monitoring the trade balance.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Marimuthu, M.; Khan, H.; Bangash, R. Fiscal causal hypotheses and panel cointegration analysis for sustainable economic growth in ASEAN. J. Asian Financ. Econ. Bus. 2021, 8, 99–109. [Google Scholar]

- Salvatore, D. Twin Deficits in the G-7 Countries and Global Structural Imbalances. J. Policy Model. 2006, 28, 701–712. [Google Scholar] [CrossRef]

- Lau, W.-Y.; Yip, T.-M. The Nexus between Fiscal Deficits and Economic Growth in ASEAN. J. Southeast Asian Econ. 2019, 36, 25–36. [Google Scholar] [CrossRef]

- Khan, H.; Marimuthu, M.; Lai, F.-W. A Granger Causal Analysis of Tax-Spend Hypothesis: Evidence from Malaysia. In Proceedings of the SHS Web of Conferences, Virtual, Malaysia, 13–15 July 2021; p. 04002. [Google Scholar]

- Ridzuan, M.R.; Abd Rahman, N.A.S. The Deployment of Fiscal Policy In Five ASEAN Countries in Dampening The Impact of COVID-19. J. Emerg. Econ. Islam. Res. 2021, 9, 16–28. [Google Scholar]

- Wijaya, S. Determinant of Value Added Tax Revenue in ASEAN (the Association of Southeast Asian Nations) Countries. Int. J. Manag. 2020, 11, 1453–1463. [Google Scholar]

- Widiyanti, M.; Sadalia, I.; Nugraha, A.T. Integrating Fiscal Matters with Environmental Sustainability In ASEAN Countries: Role Of Fiscal Deficit, Interest Rate And Stock Exchange Index. J. Secur. Sustain. Issues 2020, 10, 349–359. [Google Scholar] [CrossRef]

- Ngo, M.N.; Nguyen, L.D. The Role of Economics, Politics and Institutions on Budget Deficit in ASEAN Countries. J. Asian Financ. Econ. Bus. 2020, 7, 251–261. [Google Scholar] [CrossRef]

- Fitriaini, R. Fiscal Policy Behaviour in ASEAN: Countercyclical or Procyclical? KnE Soc. Sci. 2020, 4, 170–178. [Google Scholar] [CrossRef]

- Alwan, F.; Hakim, L.; Saputro, N. The Pattern of Twin Deficits in ASEAN: Granger Casuality Approach. Issues Incl. Growth Dev. Ctries. 2020, 1, 01–12. [Google Scholar]

- Chen, L. ASEAN in the Digital Era: Enabling Cross-border E-commerce. In Developing the Digital Economy in ASEAN; Chen, L., Kimura, F., Eds.; Routledge: London, UK, 2019; pp. 259–275. [Google Scholar]

- Abdullah, H.; Yien, L.C.; Khan, M.A. The impact of fiscal policy on economic growth in ASEAN-5 countries. Int. J. Supply Chain. Manag. 2019, 8, 754. [Google Scholar]

- Thanh, S.D. Threshold effects of inflation on growth in the ASEAN-5 countries: A Panel Smooth Transition Regression approach. J. Econ. Financ. Adm. Sci. 2015, 20, 41–48. [Google Scholar] [CrossRef]

- Syadullah, M. Governance and tax revenue in ASEAN countries. J. Soc. Dev. Sci. 2015, 6, 76–88. [Google Scholar] [CrossRef]

- Magazzino, C. The twin deficits in the ASEAN countries. Evol. Inst. Econ. Rev. 2021, 18, 227–248. [Google Scholar] [CrossRef]

- Chugunov, I.; Makohon, V.; Krykun, T. Fiscal policy and institutional budget architectonics. Balt. J. Econ. Stud. 2019, 5, 197–203. [Google Scholar] [CrossRef]

- Shastri, S. Re-examining the Twin Deficit Hypothesis for Major South Asian Economies. Indian Growth Dev. Rev. 2019, 12, 265–287. [Google Scholar] [CrossRef]

- Shastri, S.; Giri, A.; Mohapatra, G. An empirical Investigation of the Twin Deficit Hypothesis: Panel Evidence from Selected Asian Economies. J. Econ. Res. 2017, 22, 1–22. [Google Scholar]

- Baharumshah, A.Z.; Ismail, H.; Lau, E. Twin Deficits Hypothesis and Capital Mobility: The ASEAN-5 Perspective. J. Pengur. 2009, 29, 15–32. [Google Scholar]

- Keynes, J.M. The general theory of employment. Q. J. Econ. 1937, 51, 209–223. [Google Scholar] [CrossRef]

- Mundell, R.A. Capital mobility and stabilization policy under fixed and flexible exchange rates. Can. J. Econ. Political Sci./Rev. Can. Econ. Sci. Polit. 1963, 29, 475–485. [Google Scholar] [CrossRef]

- Fleming, J.M. Domestic financial policies under fixed and under floating exchange rates. Staff Pap. 1962, 9, 369–380. [Google Scholar] [CrossRef]

- Buchanan, J.M. Barro on the Ricardian equivalence theorem. J. Political Econ. 1976, 84, 337–342. [Google Scholar] [CrossRef]

- Summers, L.H. Tax Policy and International Competitiveness. In International Aspects of Fiscal Policies; University of Chicago Press: Chicago, IL, USA, 1988; pp. 349–386. [Google Scholar]

- Kim, C.-H.; Kim, D. Does Korea have Twin Deficits? Appl. Econ. Lett. 2006, 13, 675–680. [Google Scholar] [CrossRef]

- Lau, E.; Mansor, S.A.; Puah, C.-H. Revival of the Twin Deficits in Asian Crisis-Affected Countries. Econ. Issues 2010, 15, 29–53. [Google Scholar]

- Maddala, G.S.; Wu, S. A Comparative Study of Unit Root Tests with Panel Data and a New Simple Test. Oxf. Bull. Econ. Stat. 1999, 61, 631–652. [Google Scholar] [CrossRef]

- Westerlund, J. Testing for panel cointegration with multiple structural breaks. Oxf. Bull. Econ. Stat. 2006, 68, 101–132. [Google Scholar] [CrossRef]

- Marimuthu, M.; Khan, H.; Bangash, R. Is the Fiscal Deficit of ASEAN Alarming? Evidence from Fiscal Deficit Consequences and Contribution towards Sustainable Economic Growth. Sustainability 2021, 13, 10045. [Google Scholar] [CrossRef]

- Marimuthu, M.; Khan, H.; Bangash, R. Reverse Causality between Fiscal and Current Account Deficits in ASEAN: Evidence from Panel Econometric Analysis. Mathematics 2021, 9, 1124. [Google Scholar] [CrossRef]

- Dumitrescu, E.-I.; Hurlin, C. Testing for Granger Non-causality in Heterogeneous Panels. Econ. Model. 2012, 29, 1450–1460. [Google Scholar] [CrossRef] [Green Version]

- Shah, M.I. Current account deficit across South Asia: A Second Generation Methodological Adaptive Approach. J. Public Aff. 2020, 22, e2475. [Google Scholar] [CrossRef]

- Garg, B.; Prabheesh, K. Drivers of India’s current account deficits, with implications for ameliorating them. J. Asian Econ. 2017, 51, 23–32. [Google Scholar] [CrossRef]

- Khan, H.; Marimuthu, M.; Lai, F.-W. Fiscal Deficit and Its Less Inflationary Sources of Borrowing with the Moderating Role of Political Instability: Evidence from Malaysia. Sustainability 2020, 12, 366. [Google Scholar] [CrossRef]

- Levin, A.; Lin, C.-F.; Chu, C.-S.J. Unit root tests in panel data: Asymptotic and finite-sample properties. J. Econom. 2002, 108, 1–24. [Google Scholar] [CrossRef]

- Im, K.S.; Pesaran, M.H.; Shin, Y. Testing for unit roots in heterogeneous panels. J. Econom. 2003, 115, 53–74. [Google Scholar] [CrossRef]

- Baltagi, B.H. Econometric Analysis of Panel Data, 6th ed.; Springer Nature: Cham, Switzerland, 2021. [Google Scholar]

- Hall, S.G.; Asteriou, D. Applied Econometrics; Palgrave MacMillan: London, UK, 2016. [Google Scholar]

- Asteriou, D.; Hall, S.G. Applied Econometrics, 3rd ed.; Macmillan International Higher Education: Basingstoke, UK, 2015. [Google Scholar]

- Kao, C.; Chiang, M.-H. On the estimation and inference of a cointegrated regression in panel data. In Nonstationary Panels, Panel Cointegration, and Dynamic Panels; Baltagi, B.H., Fomby, T.B., Carter Hill, R., Eds.; Advances in Econometrics; Emerald Group Publishing Limited: Bentley, UK, 2001; Volume 15, pp. 179–222. [Google Scholar]

- Rahman, M.M.; Hosan, S.; Karmaker, S.C.; Chapman, A.J.; Saha, B.B. The effect of remittance on energy consumption: Panel cointegration and dynamic causality analysis for South Asian countries. Energy 2021, 220, 119684. [Google Scholar] [CrossRef]

- Arize, A.C.; Osang, T.; Slottje, D.J. Exchange-rate volatility and foreign trade: Evidence from thirteen LDC’s. J. Bus. Econ. Stat. 2000, 18, 10–17. [Google Scholar]

- Arize, A.C.; Malindretos, J.; Ghosh, D. Purchasing power parity-symmetry and proportionality: Evidence from 116 countries. Int. Rev. Econ. Financ. 2015, 37, 69–85. [Google Scholar] [CrossRef]

- Baltagi, B.H. Econometric Analysis of Panel Data, 3rd ed.; Wiley: New York, NY, USA, 2005. [Google Scholar]

- Antoch, J.; Hanousek, J.; Horváth, L.; Hušková, M.; Wang, S. Structural breaks in Panel Data: Large Number of Panels and Short Length Time Series. Econom. Rev. 2019, 38, 828–855. [Google Scholar] [CrossRef]

- Maciak, M.; Pešta, M.; Peštová, B. Changepoint in Dependent and Non-stationary Panels. Stat. Pap. 2020, 61, 1385–1407. [Google Scholar] [CrossRef]

- Pedroni, P. Panel cointegration: Asymptotic and finite sample properties of pooled time series tests with an application to the PPP hypothesis. Econom. Theory 2004, 20, 597–625. [Google Scholar] [CrossRef] [Green Version]

- Marques, A.C.; Fuinhas, J.A.; Pais, D.F. Economic growth, sustainable development and food consumption: Evidence across different income groups of countries. J. Clean. Prod. 2018, 196, 245–258. [Google Scholar] [CrossRef]

- Badaik, S.; Panda, P.K. Ricardian equivalence, Feldstein–Horioka puzzle and twin deficit hypothesis in Indian context: An empirical study. J. Public Aff. 2020, 22, e2346. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Item | January–May (2019) | January–May (2018) | Difference |

|---|---|---|---|

| Revenues | 105.4 | 92.7 | 12.7 |

| Operating expenditures | 106.5 | 109.9 | −3.3 |

| Current account balance | −1.1 | −17.1 | 16.0 |

| Development expenditures | 20.3 | 17.9 | 2.4 |

| Fiscal balance | −21.4 | −35.0 | 13.6 |

| S. No. | ASEAN-10 | Fiscal Deficit (% of GDP) | Expenditures to Support COVID-19 (% of GDP) |

|---|---|---|---|

| 1. | Brunei Darussalam | −17.94 | 7.4 |

| 2. | Cambodia | −6.5 | 2.3 |

| 3. | Indonesia | −6.6 | 12.3 |

| 4. | Lao PDR | −7.50 | 2.9 |

| 5. | Malaysia | −6.53 | 20.29 |

| 6. | Myanmar | −5.4 | 19 |

| 7. | Philippines | −7.5 | 5.83 |

| 8. | Singapore | −10.77 | 19.88 |

| 9. | Thailand | −5.21 | 11.5 |

| 10. | Vietnam | −6.02 | 14.6 |

| Author (Year) | Description |

|---|---|

| Keynesian absorption theory [20] | An increase in fiscal budget leads to an increase in aggregate demand, which puts upward pressure on imports and causes an increase in CAD. |

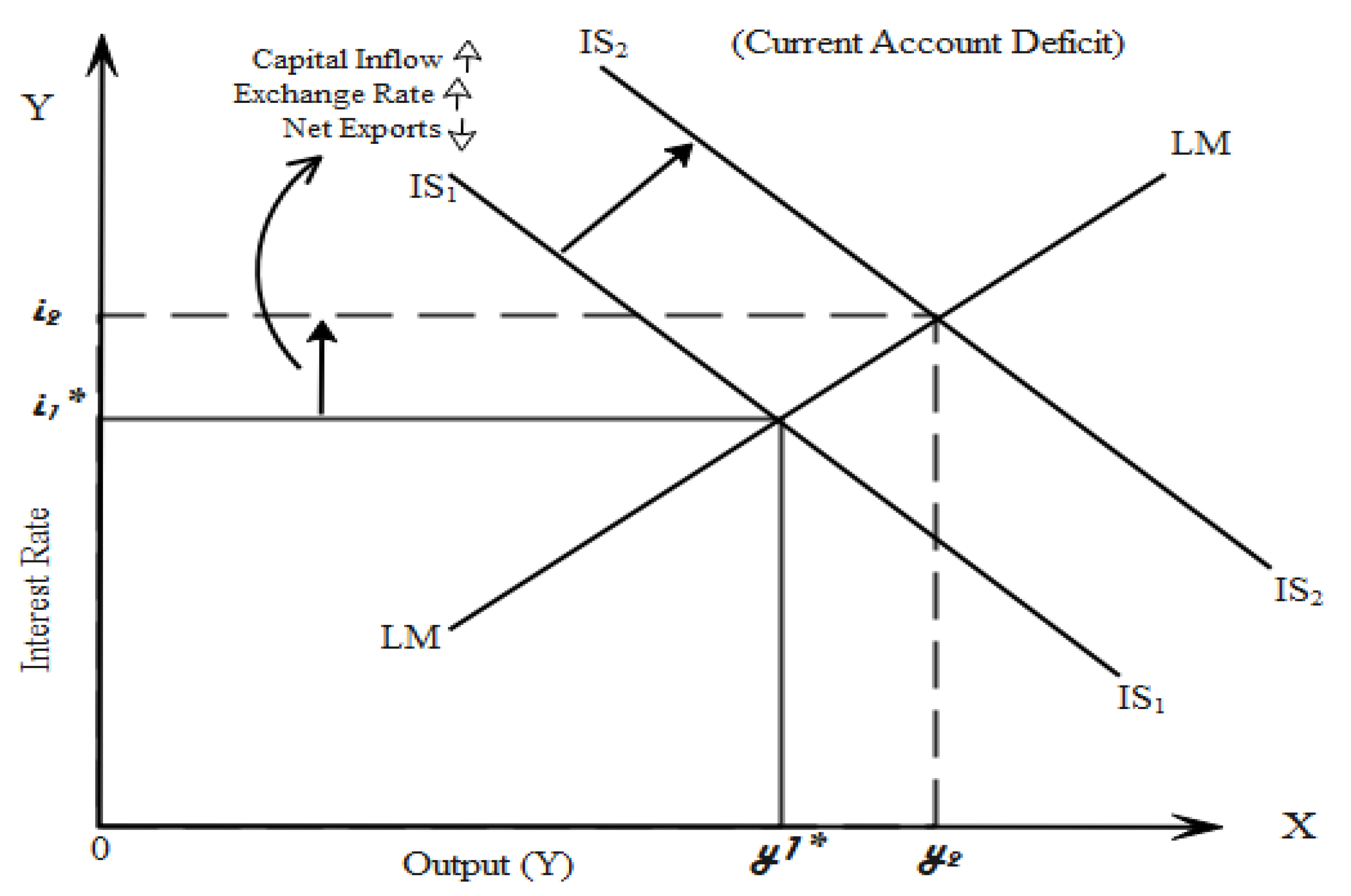

| Mundell and Fleming’s theory (1960s) [21,22] | An increase in fiscal deficit puts upward pressure on the interest rate, increasing capital inflow and appreciation in the exchange rate. This channel ultimately exacerbates the trade balance. Therefore, the first possibility indicates that causality runs from FD to CAD. |

| Ricardian equivalence (RE) theory [23] | An increase in tax rate can contract the fiscal deficit but may not change the trade balance. The RE theory suggests that an increase in the fiscal deficit will not alter the capital inflows and level of aggregate demand. The second possibility refers to no causality between CAD and FD. |

| Neo-classical theory [24] | The fiscal deficit can be used as an instrument to achieve the current account balance. The government uses its fiscal policy to regulate the external balance. This case refers to reverse causality, in which causality runs from current account deficit to fiscal deficit. This is known as the current account targeting hypothesis (CATH), where unidirectional causality runs from CAD to FD. |

| Kim and Kim [25] | Causality from CAD to FD refers to external adjustments through fiscal policy, while causality from FD to CAD may result from significant feedback. Therefore, in this way, bidirectional causality may occur between FD and CAD. |

| Gross Domestic Product | World Bank Data Bank 2020 | Million Dollars |

|---|---|---|

| Fiscal deficit | Asian Development Bank 2020 | In percentages |

| Current account deficit | Asian Development Bank 2020 | Million dollars |

| Official exchange rate | World Bank, Databank 2020 | Rate variable |

| Real interest rate | World Bank, Databank 2020 | Rate variable |

| Im, Pesaran, and Shin (Individual Root) | Levin, Lin, and Chu (Common Unit Root Process) | |||||

|---|---|---|---|---|---|---|

| Variable | At Level | At First Difference | At Level | At First Difference | ||

| Gross domestic product (GDP) | 1.26 (0.897) | −3.56 (0.000) *** | (At none) | 3.14 (0.99) | −5.83 (0.001) *** | (At individual intercept) |

| Fiscal deficit (FD) | −0.89 (0.185) | −4.33 (0.001) *** | (At individual intercept) | 0.05 (0.52) | −4.64 (0.000) *** | (At individual intercept and trend) |

| Real interest rate (RIR) | −2.40 (0.008) | - | (At none) | −3.29 (0.00) | - | (At individual intercept and trend) |

| Current account deficit (CAD) | 3.68 (0.999) | −2.99 (0.001) *** | (At individual intercept) | 2.89 (0.99) | −5.69 (0.002) *** | (At individual intercept) |

| Exchange rate (EXC) | 1.58 (0.943) | −6.19 (0.001) *** | (At none) | −0.72 (0.23) | −3.98 (0.000) *** | (At individual intercept) |

| Im, Pesaran, and Shin (Individual Root) | Levin, Lin, and Chu (Common Unit Root Process) | |||||

|---|---|---|---|---|---|---|

| Variables | At Level | At First Difference | At Level | At First Difference | ||

| Gross domestic product (GDP) | 0.20 (0.580) | −2.88 (0.001) *** | (At individual intercept) | 1.93 (0.970) | −3.69 (0.000) *** | (At individual intercept) |

| Fiscal deficit (FD) | −0.25 (0.400) | −4.79 (0.001) *** | (At individual intercept) | −1.14 (0.120) | −6.58 (0.001) *** | (At individual intercept) |

| Real interest rate (RIR) | −2.81 (0.002) *** | - | (At individual intercept) | −2.50 (0.006) *** | - | (At individual intercept) |

| Current account deficit (CAD) | −3.52 (0.000) *** | - | (At individual intercept) | −3.99 (0.001) *** | - | (At individual intercept) |

| Exchange rate (EXC) | −0.41 (0.340) | −6.25 (0.002) *** | (At individual intercept and trend) | −0.05 (0.472) | −4.46 (0.001) *** | (At individual intercept) |

| Im, Pesaran, and Shin (Individual Root) | Levin, Lin, and Chu (Common Unit Root Process) | |||||

|---|---|---|---|---|---|---|

| Variable | At Level | At First Difference | At Level | At First Difference | ||

| Gross domestic product (GDP) | 0.40 (0.65) | −1.76 (0.03) ** | (At individual intercept) | 1.28 (0.90) | −2.16 (0.01) ** | (At individual intercept) |

| Fiscal deficit (FD) | 0.52 (0.29) | −3.81 (0.00) | (At individual intercept) | 0.98 (0.16) | 5.07 (0.00) *** | (At individual intercept) |

| Real interest rate (RIR) | −2.79 (0.00) *** | - | (At individual intercept) | −2.41 (0.00) *** | - | (At individual intercept) |

| Current account deficit (CAD) | 0.57 (0.71) | −6.12 (0.00) *** | (At none) | −0.07 (0.47) | −4.20 (0.00) | (At individual intercept) |

| Exchange rate (EXC) | −0.46 (0.32) | −2.83 (0.00) *** | (At individual intercept and trend) | −0.40 (0.34) | −2.19 (0.01) ** | (At individual intercept) |

| Lower-Middle-Income Economies | Chow Test | Lagrange Multiplier Test | Hausman Test |

|---|---|---|---|

| H0: Common Effect H1: Fixed Effects | H0: Common Effects H1: Random Effects | H0: Random Effects H1: Fixed Effects | |

| Decision: select CE (accept H0) | Decision: select RE (reject H0) | Decision: random effects (accept H0) | |

| Cross-section dependence test | Pesaran CD: 0.58 Prob. = 0.41 | N < T (cross-sections are independent) | |

| Upper-middle-income economies | H0: common effect H1: fixed effects | H0: common effects H1: random effects | H0: random effects H1: fixed effects |

| Decision: select CE (accept H0) | Decision: select RE (reject H0) | Decision: random effects (accept H0) | |

| Cross-section dependence test | Pesaran CD: 0.75 Prob. = 0.29 | N < T (cross-sections are independent) | |

| Higher-income economies | H0: common effect H1: fixed effects | H0: common effects H1: random effects | H0: random effects H1: fixed effects |

| Decision: select CE (accept H0) | Decision: select RE (reject H0) | Decision: random effects (accept H0) | |

| Cross-section dependence test | Pesaran CD: 0.44 Prob. = 0.41 | N < T (cross-sections are independent) |

| Dependent Variable CAD | Coefficient | t-Statistic | p-Value |

|---|---|---|---|

| Lower-middle-income economies | |||

| Exchange rate (EXC) | −0.28 | −1.27 | 0.21 |

| Real interest rate (RIR) | 0.06 | 8.57 | 0.00 *** |

| Fiscal deficit (FD) | 0.008 | 0.81 | 0.40 |

| Upper-middle-income economies | |||

| Exchange rate (EXC) | −0.53 | −2.05 | 0.04 ** |

| Real interest rate (RIR) | 0.02 | 2.077 | 0.03 ** |

| Fiscal deficit (FD) | 0.04 | 1.54 | 0.13 |

| Higher-income economies | |||

| Exchange rate (EXC) | 0.08 | 1.49 | 0.13 |

| Real interest rate (RIR) | 0.12 | 2.62 | 0.01 ** |

| Fiscal deficit (FD) | 0.01 | 1.33 | 0.19 |

| Dependent Variable CAD | Coefficient | Std. Error | t-Statistic | p-Value |

|---|---|---|---|---|

| Long-run equation | ||||

| Exchange rate (EXC) | −0.14 | 0.22 | −1.85 | 0.04 ** |

| Real interest rate (RIR) | 0.04 | 0.009 | 4.95 | 0.00 *** |

| Fiscal deficit (FD) | 0.003 | 0.008 | 0.46 | 0.64 |

| Short-run equation | ||||

| COINTEQ01 | −0.78 | 0.14 | −5.21 | 0.00 *** |

| Δ (CAD(−1)) | 0.04 | 0.05 | 0.81 | 0.42 |

| Δ (EXC) | 1.41 | 2.13 | 0.66 | 0.50 |

| Δ (EXC(−1)) | 0.80 | 1.18 | 0.67 | 0.50 |

| Δ (RIR) | 0.01 | 0.03 | 0.39 | 0.69 |

| Δ (RIR(−1)) | −0.014 | 0.01 | −1.23 | 0.22 |

| Δ (FD) | −0.01 | 0.06 | −0.23 | 0.81 |

| Δ (FD(−1)) | −0.02 | 0.02 | −0.75 | 0.45 |

| Gross domestic product (GDP) | 0.93 | 0.22 | 4.11 | 4.11 |

| Constant (C) | −1.79 | 1.48 | −1.21 | 0.22 |

| Dependent Variable CAD | Coefficient | Std. Error | t-Statistic | p-Value |

|---|---|---|---|---|

| Long-run equation | ||||

| Exchange rate (EXC) | 0.19 | 0.35 | 0.54 | 0.58 |

| Real interest rate (RIR) | 0.04 | 0.02 | 2.13 | 0.03 ** |

| Fiscal deficit (FD) | 0.08 | 0.07 | 1.01 | 0.32 |

| Short-run equation | ||||

| COINTEQ01 | −0.69 | 0.32 | −2.11 | 0.03 ** |

| Δ (EXC) | 1.18 | 0.81 | 1.45 | 0.15 |

| Δ (EXC(−1)) | 1.63 | 0.55 | 2.94 | 0.004 *** |

| Δ (RIR) | −0.01 | 0.01 | −1.64 | 0.10 |

| Δ (RIR(−1)) | −0.01 | 0.02 | −0.69 | 0.49 |

| Δ (FD) | 0.06 | 0.06 | 1.06 | 0.28 |

| Δ (FD(−1)) | 0.05 | 0.02 | 1.98 | 0.05 ** |

| Gross domestic product (GDP) | 0.71 | 0.45 | 1.58 | 0.11 |

| Constant (C) | −2.04 | 3.23 | −0.63 | 0.52 |

| Dependent Variable CAD | Coefficient | Std. Error | t-Statistic | p-Value |

|---|---|---|---|---|

| Long-run equation | ||||

| Exchange rate (EXC) | 0.46 | 0.56 | 0.82 | 0.41 |

| Real interest rate (RIR) | 0.006 | 0.003 | 2.24 | 0.03 ** |

| Fiscal deficit (FD) | 0.02 | 0.001 | 14.4 | 0.00 *** |

| Short-run equation | ||||

| COINTEQ01 | −0.98 | 0.08 | −11.77 | 0.00 *** |

| Δ (EXC) | 3.03 | 1.81 | 1.67 | 0.10 |

| Δ (EXC(−1)) | −3.62 | 2.24 | −1.61 | 0.11 |

| Δ (RIR) | −0.02 | 0.01 | −1.91 | 0.06 * |

| Δ (RIR(−1)) | −0.0008 | 0.006 | −0.11 | 0.90 |

| Δ (FD) | 0.002 | 0.02 | 0.09 | 0.92 |

| Δ (FD(-1)) | −0.01 | 0.001 | −6.91 | 0.00 *** |

| Gross domestic product (GDP) | 0.38 | 0.30 | 1.26 | 0.21 |

| Constant (C) | 4.87 | 4.23 | 1.15 | 0.25 |

| Variables | FMOLS | DOLS | ||

|---|---|---|---|---|

| Dependent Variable CAD | Coefficient | t-Statistics (p-Value) | Coefficient | t-Statistics (p-Value) |

| RIR | 0.05 | 2.33 (0.030) ** | 0.03 | 1.91 (0.041) ** |

| EXC | 0.07 | 1.93 (0.040) ** | 0.28 | 1.60 (0.110) |

| FD | −0.02 | −1.30 (0.191) | 0.005 | 0.892 |

| GDP | 0.98 | 7.94 (0.000) *** | 1.35 | 5.88 (0.000) *** |

| R2 | 0.70 | 0.88 | ||

| Variables | FMOLS | DOLS | ||

|---|---|---|---|---|

| Dependent Variable CAD | Coefficient | t-Statistics (p-Value) | Coefficient | t-Statistics (p-Value) |

| RIR | 0.008 | 0.81 (0.411) | 0.008 | 0.76 (0.440) |

| EXC | −0.12 | −2.47 (0.010) ** | −0.09 | −1.85 (0.060) * |

| FD | 0.07 | 1.95 (0.050) ** | 0.07 | 1.91 (0.050) ** |

| GDP | 0.87 | 53.61 (0.000) *** | 0.86 | 49.76 (0.000) *** |

| R2 | 0.72 | 0.82 | ||

| Variables | FMOLS | DOLS | ||

|---|---|---|---|---|

| Dependent Variable CAD | Coefficient | t-Statistics (p-Value) | Coefficient | t-Statistics (p-Value) |

| RIR | −0.001 | −0.35 (0.720) | −0.01 | −0.94 (0.350) |

| EXC | −3.53 | −3.06 (0.003) ** | −4.67 | −2.63 (0.010) ** |

| FD | 0.01 | 3.80 (0.000) *** | 0.02 | 2.74 (0.010) ** |

| GDP | 0.80 | 15.36 (0.000) *** | 0.72 | 13.21(0.020) ** |

| R2 | 0.40 | 0.78 |

| Null Hypothesis | W-Stat | Zbar-Stat | p-Value |

|---|---|---|---|

| Lower-middle-income economies (LMIE) | |||

| CA↛FD FD↛CAD | 4.68 1.81 | 2.28 −0.35 | 0.021 ** 0.722 |

| RIR↛CAD CAD↛RIR | 2.38 1.08 | 0.41 −1.02 | 0.680 0.300 |

| FD↛EXC EXC↛FD | 0.90 0.63 | −1.18 −1.43 | 0.230 0.150 |

| FD↛IR RIR↛FD | 0.28 1.20 | −1.76 −0.91 | 0.070 * 0.362 |

| EXC↛RIR RIR↛EXC | 6.10 3.79 | 3.58 1.46 | 0.000 *** 0.141 |

| EXC↛CAD CAD↛EXC | 2.38 0.71 | 0.17 −1.36 | 0.862 0.173 |

| Upper-middle-income economies (UMIE) | |||

| CA↛FD FD↛CAD | 0.33 0.78 | −1.32 −1.007 | 0.182 0.311 |

| RIR↛CAD CAD↛RIR | 2.59 0.24 | 0.28 −1.39 | 0.777 0.166 |

| FD↛EXC EXC↛FD | 1.34 0.82 | −0.60 −0.97 | 0.544 0.322 |

| FD↛RIR RIR↛FD | 5.31 1.92 | 2.21 −0.19 | 0.020 ** 0.840 |

| EXC↛RIR RIR↛EXC | 3.00 5.97 | 0.57 2.68 | 0.560 0.007 *** |

| EXC↛CAD CAD↛EXC | 0.78 1.89 | −1.00 −0.22 | 0.311 0.822 |

| Higher-income economies (HIE) | |||

| CA↛FD FD↛CAD | 11.95 0.94 | 5.67 −0.73 | 0.000 *** 0.460 |

| RIR↛CAD CAD↛RIR | 1.43 1.65 | −0.44 −0.31 | 0.650 0.752 |

| FD↛EXC EXC↛FD | 1.41 0.72 | −0.45 −0.85 | 0.643 0.396 |

| FD↛RIR RIR↛FD | 0.60 1.09 | −0.93 −0.64 | 0.355 0.522 |

| EXC↛RIR RIR↛EXC | 5.89 2.52 | 2.14 0.19 | 0.033 ** 0.840 |

| EXC↛CAD CAD↛EXC | 2.94 2.10 | 0.43 −0.05 | 0.666 0.955 |

| Lower-Middle-Income Economies (LMIE) | |||

|---|---|---|---|

| Model | Omitted Variable Test | Specification Test | Heteroscedasticity |

| TEST | Likelihood ratio | Hausman test | Breusch–Pagan |

| Hypotheses | Ho: omitted variable is irrelevant | Ho: no omitted variable | Ho: constant variance |

| Equation (2) | 0.41 (p-value) | 0.31 (p-value) | 0.07 * |

| Upper-middle-income economies (UMIE) | |||

| Equation (2) | 0.22 (p-value) | 0.16 (p-value) | 0.09 * |

| Higher-income economies (HIE) | |||

| Equation (2) | 0.35 (p-value) | 0.19 (p-value) | 0.11 |

| Lower-Middle-Income Economies (LMIE) | Upper-Middle-Income Economies (UMIE) | Higher-Income-Economies (HIE) | |

|---|---|---|---|

| Current Account Deficit | CATH (unidirectional causality) | No causality (CAD and FD are independent) | CATH (unidirectional causality) |

| RIR | Significant | Insignificant | Insignificant |

| EXC | Significant | Significant | Significant |

| FD | Insignificant | Significant | Significant |

| RIR is less sensitive/elastic to CAD | EXC and FD are less sensitive/elastic to CAD | EXC is more sensitive/elastic to CAD |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Marimuthu, M.; Khan, H.; Bangash, R. Comparative Study on Lower-Middle-, Upper-Middle-, and Higher-Income Economies of ASEAN for Fiscal and Current Account Deficits: A Panel Econometric Analysis. Mathematics 2022, 10, 3259. https://doi.org/10.3390/math10183259

Marimuthu M, Khan H, Bangash R. Comparative Study on Lower-Middle-, Upper-Middle-, and Higher-Income Economies of ASEAN for Fiscal and Current Account Deficits: A Panel Econometric Analysis. Mathematics. 2022; 10(18):3259. https://doi.org/10.3390/math10183259

Chicago/Turabian StyleMarimuthu, Maran, Hanana Khan, and Romana Bangash. 2022. "Comparative Study on Lower-Middle-, Upper-Middle-, and Higher-Income Economies of ASEAN for Fiscal and Current Account Deficits: A Panel Econometric Analysis" Mathematics 10, no. 18: 3259. https://doi.org/10.3390/math10183259

APA StyleMarimuthu, M., Khan, H., & Bangash, R. (2022). Comparative Study on Lower-Middle-, Upper-Middle-, and Higher-Income Economies of ASEAN for Fiscal and Current Account Deficits: A Panel Econometric Analysis. Mathematics, 10(18), 3259. https://doi.org/10.3390/math10183259