1. Introduction

With the rapid development of the global economy and information technology, online credit loans have become a critical transaction channel in the market economy. The main job of financial institutions is to provide credit services to customers, as doing so can bring considerable profits [

1]. However, due to insufficient credit-scoring information, there may be market failures in the credit market, and credit risk can have a considerable impact on the financial industry. Especially after the subprime mortgage crisis in 2008, both developed and developing countries suffered long-term damage that made them realize the need for the accurate assessment of the creditworthiness of loan applicants and other financial investments [

2,

3,

4].

The rapid development of the credit industry has also brought many problems to banks. Customer credit defaults constantly appear, such as overdue loans, the inability of borrowers to repay, and malicious defaults, causing considerable losses to commercial banks [

5]. In the era of big data and financial technology, efficient and accurate credit-scoring models are very important for banks and financial institutions because an accurate credit-scoring system can make loan decisions faster, effectively reduce the occurrence of credit risks, and thus reduce cost [

6].

According to the Board of Governors of the Federal Reserve, as of February 2019, U.S. financial institutions had more than

$4 trillion in consumer loan balances, and this number is still growing at an annual rate of more than 4%. In addition, according to a report by the China Banking Regulatory Commission, China’s non-performing loan ratio reached about 1.67% in 2015, and it is still growing. Since lenders may default, financial institutions may face significant financial losses if they do not use credit-scoring models to assess lenders’ creditworthiness [

7].

Most credit-scoring models today use a sample of accepted loan applicants for analysis and exclude those who were rejected. However, credit models should be built based on complete information on all applicants. According to the Consumer Credit Access Expectations Survey conducted by the Federal Reserve Bank of New York (FRBNY), loan applicants are rejected three times as often as accepted. In Lending Club, one of the largest P2P (peer-to-peer) lending platforms in the world, more than 90% of loan applicants are rejected [

8]. If only a sample of accepted loan applicants is used to create a credit-scoring model, there may be a problem of sample bias, leading to selection bias. This sample bias not only leads to bias in parameter estimates but also affects the outcome of credit-scoring and thus lender equity [

9].

In recent years, many methods based on reject inference have emerged and been applied to the field of credit scoring. Common reject inference techniques include the Heckman model [

10] and reclassification [

11]. Among them, extrapolation and amplification [

12] are commonly used reject inference techniques. Amplification is assigning all rejected samples to bad or good lenders with a given score, and the extrapolation rule is to use only the model based on the accepted sample of loan applicants and then apply that model directly to predict the status of the rejected sample.

In a previous study, Bücker et al. [

13] showed that amplification impairs and does not improve the performance of credit-scoring models. Studies have also pointed out that extrapolation methods cannot improve the performance of credit-scoring models [

14]. In addition, there is an important issue with the use of loan data from the Lending Club credit lending platform. The problem is that the variables of the accepted and rejected datasets are not consistent. Another problem is that the sample size of rejected loan applicants is much larger than the sample size of accepted loan applicants. This study argues that acceptable applicants may be implied in the sample of rejected loan applicants and the outliers found in the sample of rejected loan applicants may represent those acceptable loan applicants. Furthermore, an accepted sample of loan applicants may imply applicants who should be rejected, while outliers found in the sample represent applicants who should be rejected. Therefore, if the sample of loan applicants is handled more properly, it is possible to increase the number of lenders, and increasing the number of lenders can increase the revenue of the lending platform. Therefore, finding potential qualified applicants in the rejected sample to increase the number of lenders and improve the credit-scoring model is the main purpose of this study.

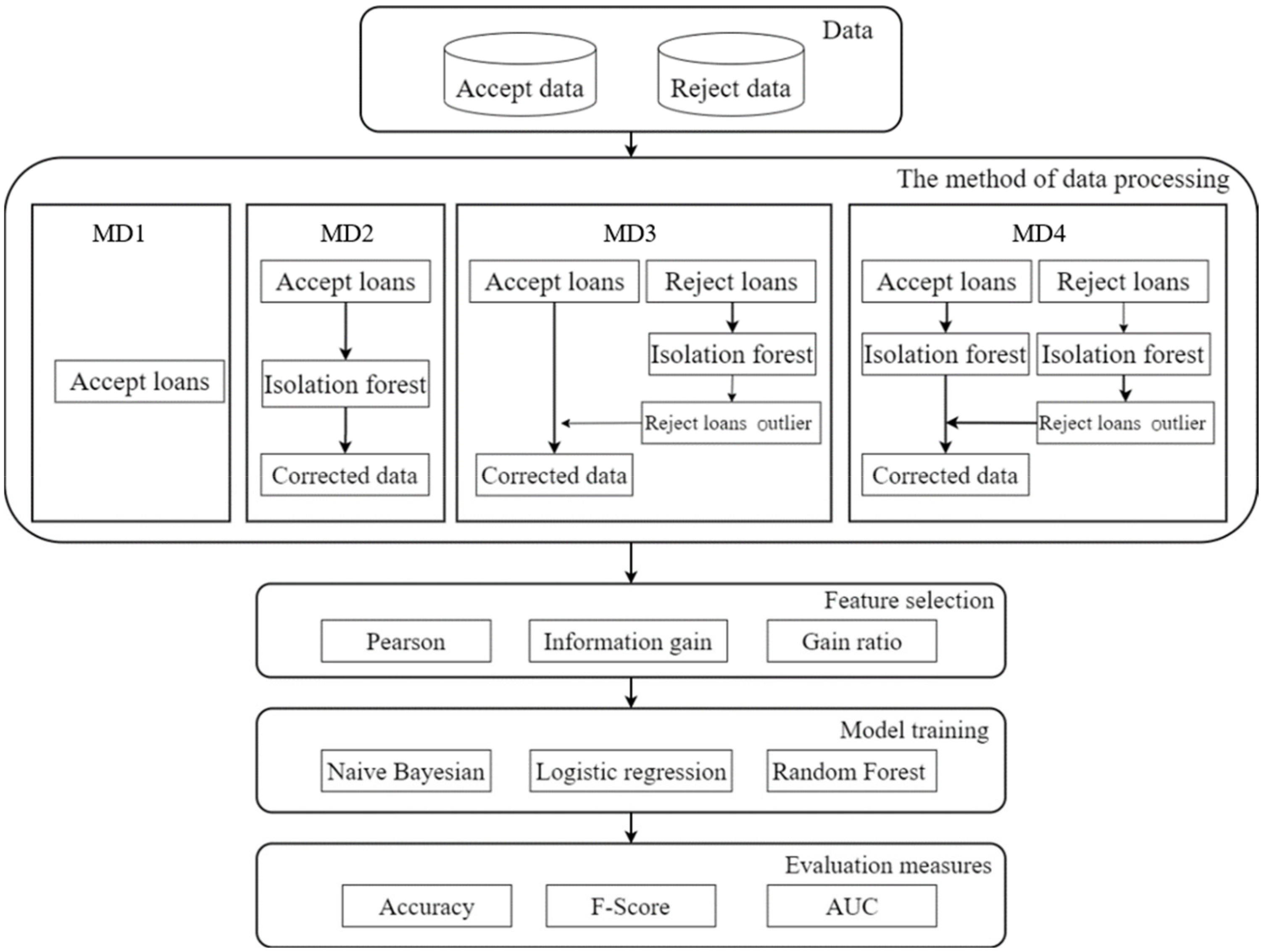

To address the above problems, this study proposes a global credit-scoring model framework that combines multiple feature-selection methods and classifiers to better evaluate the model after adding rejected samples. In addition, this study uses outlier detection methods to explore the internal relationships of all samples, which can delete outlier applicants in accepted samples or increase outlier applicants in rejected samples. At the same time, the credit-scoring model cannot reduce its performance by adding these potentially qualified applicants since the performance is essential for all stakeholders interested in the company’s direction [

15,

16]. Finally, this study uses four different samples and reject inference to evaluate their credit-scoring models.

This study hopes to experimentally demonstrate that it is feasible to exclude potentially unrepayable lenders from the accepted samples and select eligible applicants from the rejected samples.

3. Results

This study uses the accepted and rejected data from the Lending Club loan dataset, with outlier processing, and divides the dataset into 4 sample groups, namely MD1, MD2, MD3, and MD4; the study then uses three feature-extraction methods and three classification methods to build 4 credit-scoring models. The accuracy test results are shown in

Table 6. Among the feature-extraction methods, Pearson with RF classification results is the best.

Due to the better accuracy of using Pearson for feature extraction and the random forest to build the credit-scoring models, we further applied it to all 4 sample groups. The evaluation results are in

Table 7. As can be seen from

Table 7, the study results of the MD4 sample are the best, followed by the MD3 sample. This means that the accuracy of the credit-scoring model will increase if the outlier sample in the loan rejection sample is added to the loan acceptance sample. Therefore, the accuracy of the credit-scoring model is better if the outlier samples are removed from the loan acceptance sample, which is encouraging.

4. Discussion

It has been shown in previous studies that if a financial institution builds a credit-scoring model using only the accepted sample data of loan applicants, the model cannot be representative of all applicants, and this is where reject inference is proposed. Reject inference is inferring whether a loan applicant who has been denied was a good or bad loan applicant. However, it is necessary to combine the loan applicant’s rejection status with the loan applicant’s acceptance status [

22]. In a past study, Tian et al. [

23] removed outliers from rejected data and modeled them with accepted data. In addition, some scholars extract the outliers of the rejected data, add them to the accepted data, and then add the outliers in the rejected data to the accepted data. Both rejection and acceptance data are modeled [

24]. Liu [

25] applied reject inference to credit scoring to solve the problem of information asymmetry in credit-scoring models, combining loan acceptance data and rejection data as a credit-scoring model. However, this study argues that acceptable applicants may be implicit in the sample of rejected loan applicants, and the outliers found in the sample of rejected loan applicants represent those acceptable loan applicants. Furthermore, an accepted sample of loan applicants may also imply applicants who should be rejected, while outliers found in the sample represent applicants who should be rejected. Therefore, if the loan applicant sample is handled correctly, it may be possible to increase the number of loan applicants, and the increase in the number of loaners can increase the income of the loan platform. Therefore, according to this hypothesis, this study performed outlier detection and reorganization on all loan applicants, who were divided into 4 sample groups (MD1, MD2, MD3, MD4). A comparison of the practice of this study with other studies is shown in

Table 7 and includes a comparison of sample sizes.

Table 8 presents the number of accepted and rejected samples for each study, illustrating the number of variables for each study and the outlier handling of the data. In

Table 8, after adding the outliers in the rejected data into MD3 and MD4, the amount of accepted data is much greater than that without outliers added before. Using the accepted data without removing outliers, the number of data records is 928,112, and when adding outliers to the rejected data, the number of data records is 285,301. When outliers are removed from the accepted data, the number of data records is 75,871, and when adding outliers to the rejected data, the number of data records is 268,361. Adding outliers to rejected data adds a total of 1,924,901 data records, which is more than the accepted data record counts in previous studies. An increase in accepted data for lenders means an increase in the number of loan applicants being accepted, and an increase in the number of lenders means an increase in the loan income of the loan platform.

This study describes a credit-scoring model established based on the work of previous scholars through the Lending Club dataset in

Table 8. Xia [

24] added the outliers in the rejected data to the accepted data and modeled the accepted and rejected data. Tian et al. [

23] modeled the accepted and rejected data after removing outliers in the rejected data. Liu et al. [

25] classified the accepted and rejected data and then selected a small part of the accepted and rejected samples for modeling. The authors of [

23] extracted features through a single feature selection technique, but other studies use the features of rejected data for modeling. This study processed the accepted and rejected data by outlier detection: MD2 deletes the outliers in the accepted data, MD3 is the outlier that adds the accepted data to the rejected data, and MD4 deletes the outliers in the accepted data and adds the outliers in the rejected data. Different feature selection techniques were used to extract features for each model, and adopting Li et al. [

8], the data set was divided into 70% training set and 30% testing set. It is hoped that the combination of outlier detection, feature selection, and machine learning can improve the effectiveness of the current credit-scoring model.

In order to verify the effectiveness of the method proposed in this study, we compare the results from past studies, as shown in

Table 9. In terms of accuracy, the results for MD4 in this study are better than those proposed in previous studies. In addition, in terms of AUC, the results for MD3 of this study are also very good. Therefore, it can be seen that it is helpful to model the selection of the outlier applicants in the rejected samples and include them in the accepted applicants. This approach can increase the number of lenders and bring more benefits to the lending platform, while the accuracy of the credit-scoring model is still maintained.

Researchers using the Lending Club dataset want to build credit-scoring models by processing rejected samples, and they mostly use machine learning for learning and classification and evaluate credit-scoring models based on accuracy and AUC [

23,

24,

25]. Xia [

24] also believed that if a fixed dataset is used all the time, the generalizability of the model will be lost. Therefore, this study hopes to adjust the samples through outlier detection to improve the generalizability of future credit-scoring models. Past studies have tried removing outliers from the accepted data or adding rejected outliers. The aim of this study was to identify the combination that gave the best result, and machine learning was used to verify.

Table 10 is a consolidated comparison of the results of this study and previous studies. This study is compared with three previous studies on credit-scoring models; the data in the study are all from the Lending Club loan platform, and the study period is four years (2009 to 2012). This study uses outlier detection to add outliers in rejected data to accepted data (as in MD3), and there may be loan applicants who were rejected in the accepted data, so the accepted data also use the outlier detection method to remove outliers (as in MD4). The outliers in the accepted data and the rejected data represent the numbers of people who can increase the loans, and the loan amount will increase accordingly, thereby improving the platform’s revenue.

5. Conclusions

Credit loan transactions have become an important pipeline in the market economy, and most companies are starting to develop better strategies with the help of credit-scoring models. Most of the previous studies only use the method of accepted data or reject inference to build credit-scoring models. However, there should be useful data in both data sets, and lenders should not use just one; doing so can make the established credit model inaccurate and lead to sample bias, which hinders model performance. Indeed, in P2P network lending, many borrowers’ applications are rejected. A company building a credit-scoring model must combine these data to fully assess a loan’s potential risk. Researchers using the Lending Club dataset want to build credit-scoring models by processing rejected samples, with their models built only on accepted samples to directly predict the status of rejected samples. However, the distribution of accepted samples in online P2P lending is different from the distribution of rejected samples, and the credit-scoring model on the original accepted sample may no longer apply.

In this study, outlier detection is used with the real loan data on the loan platform to remove outliers in accepted data and add outliers in rejected data. This approach filters out loan applicants who have a chance of being bad loan applicants and includes loan applicants who may be good loan applicants. In addition, this study uses three feature-extraction methods, three classifier methods, and three evaluation metrics to build credit-scoring models and find out the best combination of accepted samples and rejected samples in the machine learning approach. Properly adding or deleting outliers can improve the model’s generalizability, avoid the use of fixed data sets, and improve the adaptability of future models. The experimental results show that the credit-scoring model combining Pearson and random forest proposed in this study has significantly better accuracy and AUCs than the models of other scholars. Compared with previous studies, using outlier detection to remove outliers in loan accept applicants and identify potentially creditworthy loan applicants from loan rejection samples is a good strategy. Furthermore, this study not only improves the accuracy of the credit-scoring model but also increases the number of lenders, which in turn increases the profitability of the lending platform.

In terms of practical implications, this study brings several advantages. First, because outlier detection and classifiers can be changed freely, the framework of this study is relatively flexible. Second, the size of the adjusted dataset becomes larger, which also represents the potential of this framework to handle large data sets. From a cost-benefit perspective, improving the performance of credit-scoring models from the perspective of outlier detection may bring more revenue to the company in the context of low loan approval rates.

Among the credit-scoring models in this study, only the isolated forest outlier detection method is used. Therefore, it is suggested that future studies can refer to the research of Zhang et al. [

26] and use various other outlier detection methods to find common outliers. In addition, the use of deep learning methods to establish a credit-scoring model may be considered, which may make research in this area more complete.

{kind=link}