A Study on Early Warnings of Financial Crisis of Chinese Listed Companies Based on DEA–SVM Model

Abstract

:1. Introduction

2. Literature Review

3. Description of the Methodology

3.1. SBM Model

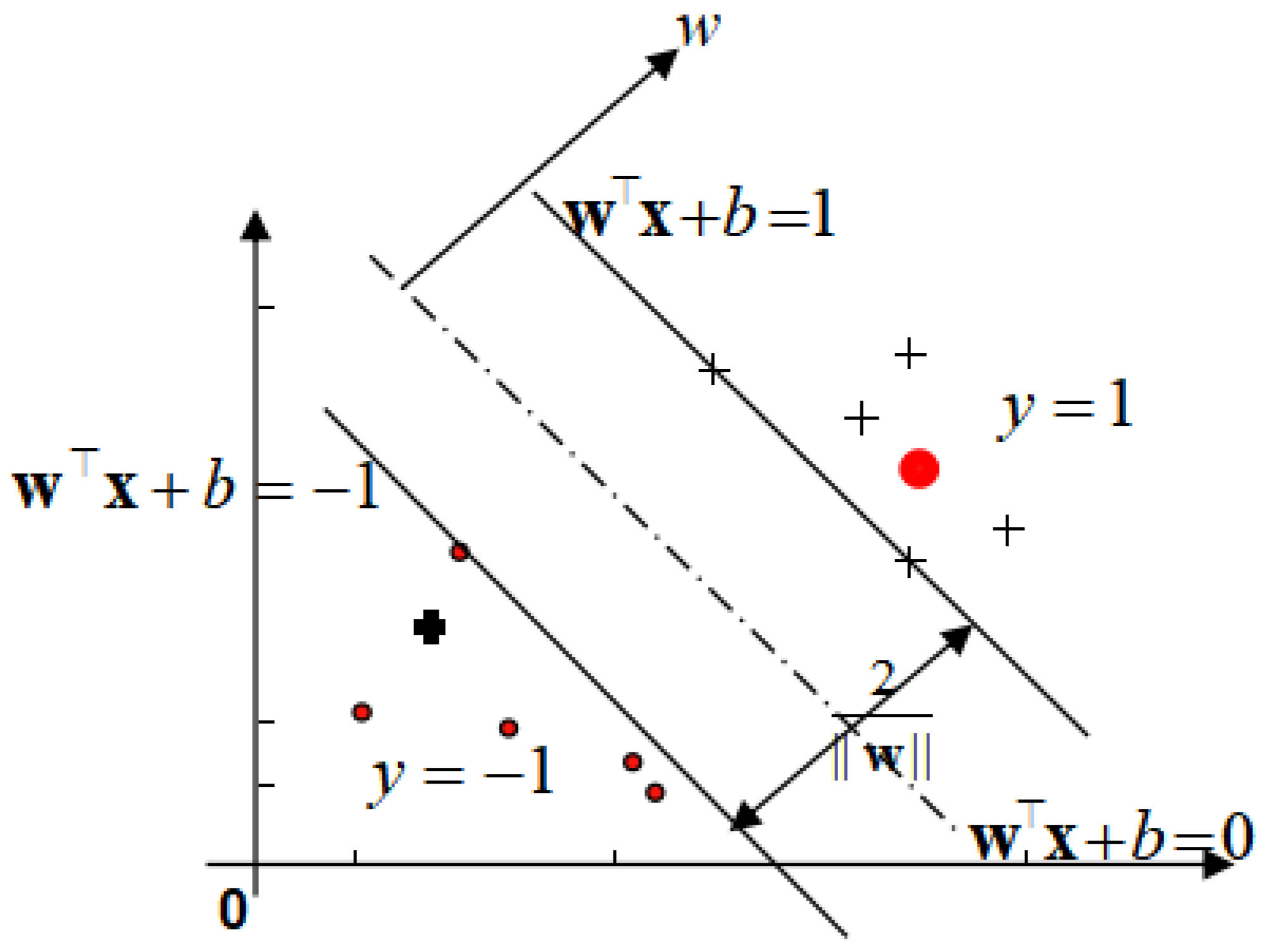

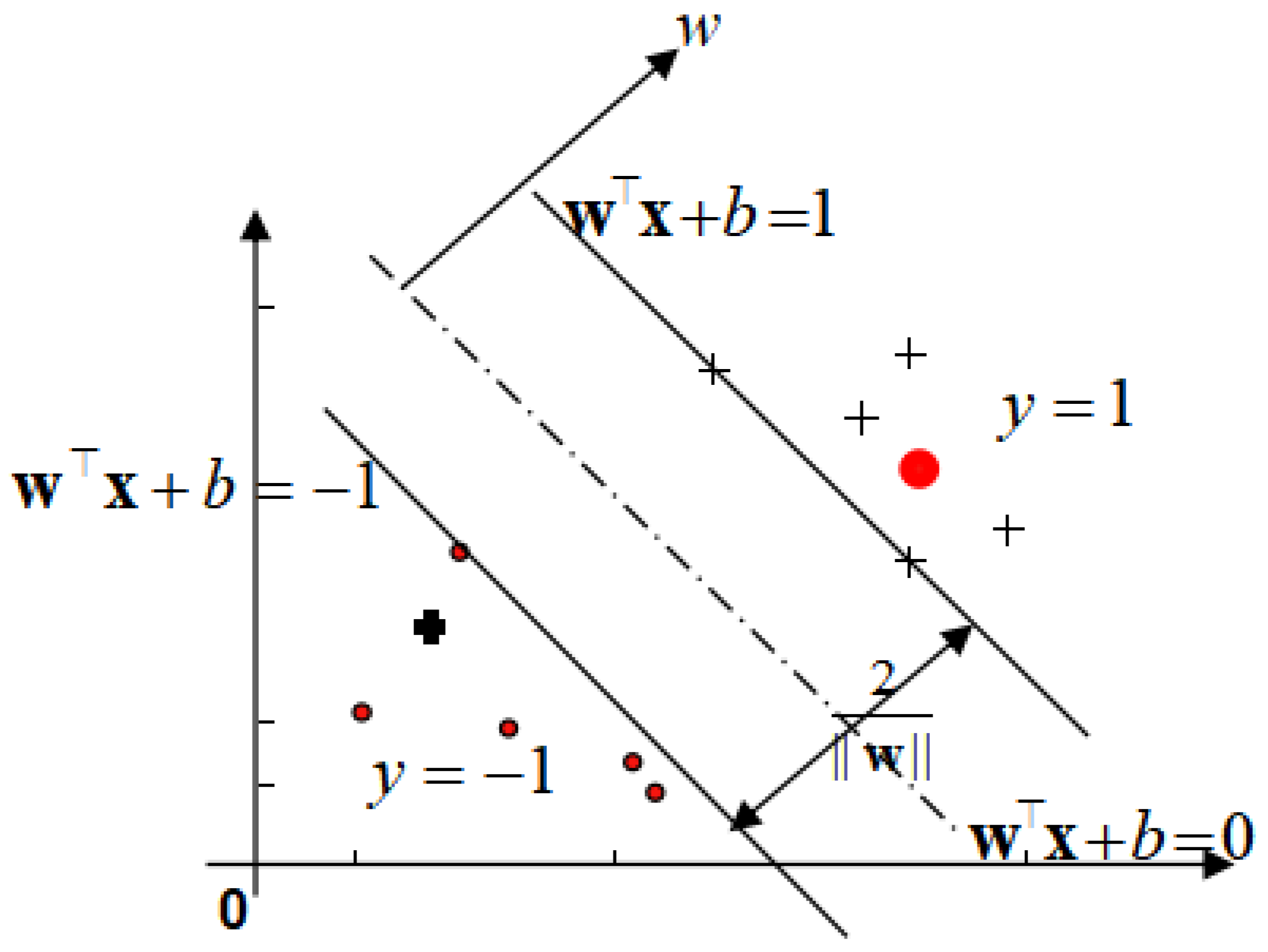

3.2. Support Vector Machine (SVM)

- The linear kernel function, whose expression is shown in Equation (11)where c represents an optional constant.

- The polynomial kernel function, whose expression is shown in Equation (12).where represents the slope, is a constant term, and d is a power of the polynomial.

- The radial basis kernel function, which is currently the most dominant kernel function, has the following expressions in Equation (13).where represents the open root sign of the sum of squares of the components after the vector is differenced, and is the parameter of the Gaussian kernel.

- Sigmoid function, whose expression is shown in Equation (14).where μ and r are the parameters of kernel function.

4. Financial Crisis Early Warning Indicator Design

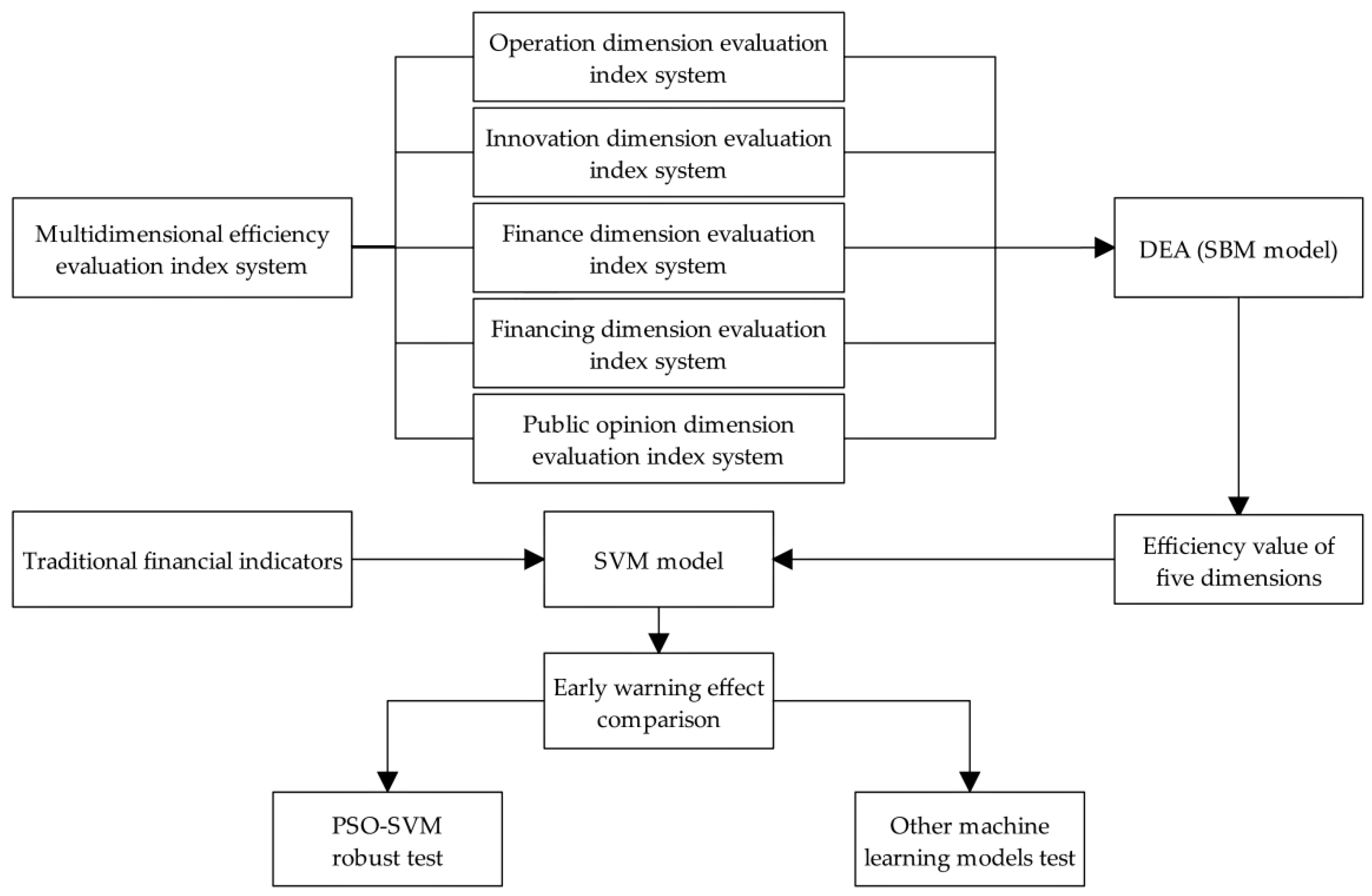

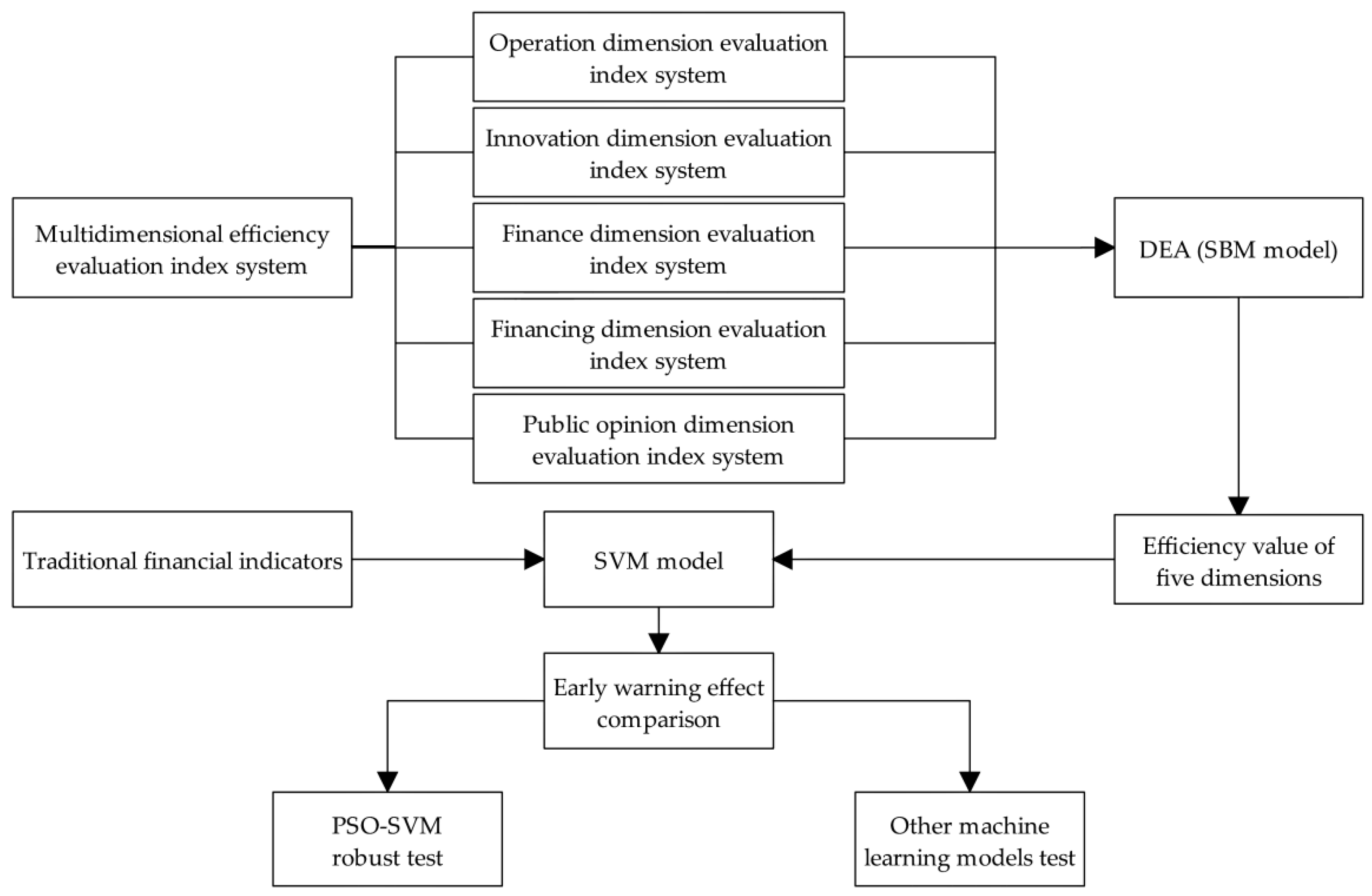

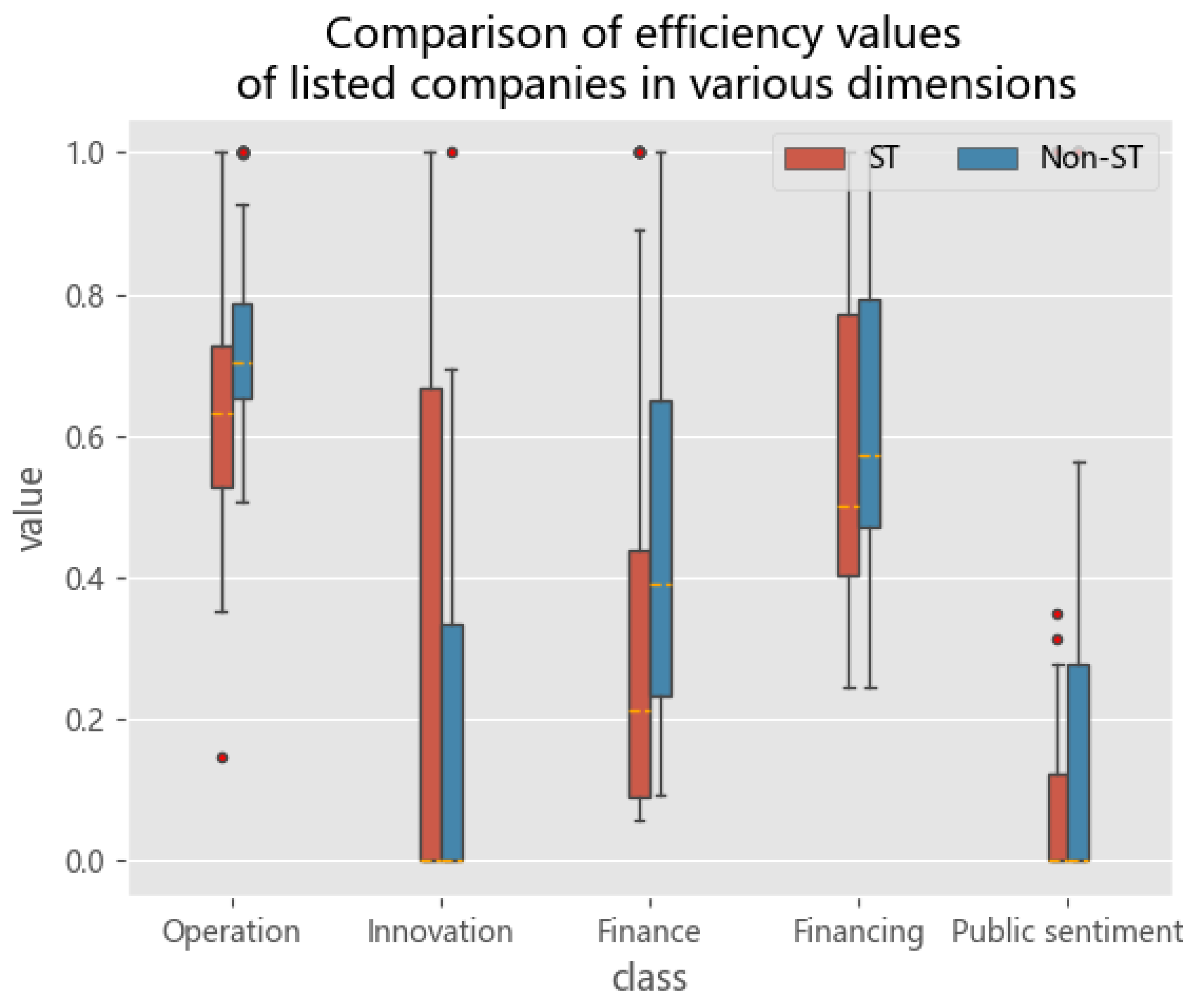

4.1. Multidimensional Efficiency Evaluation Index System Design

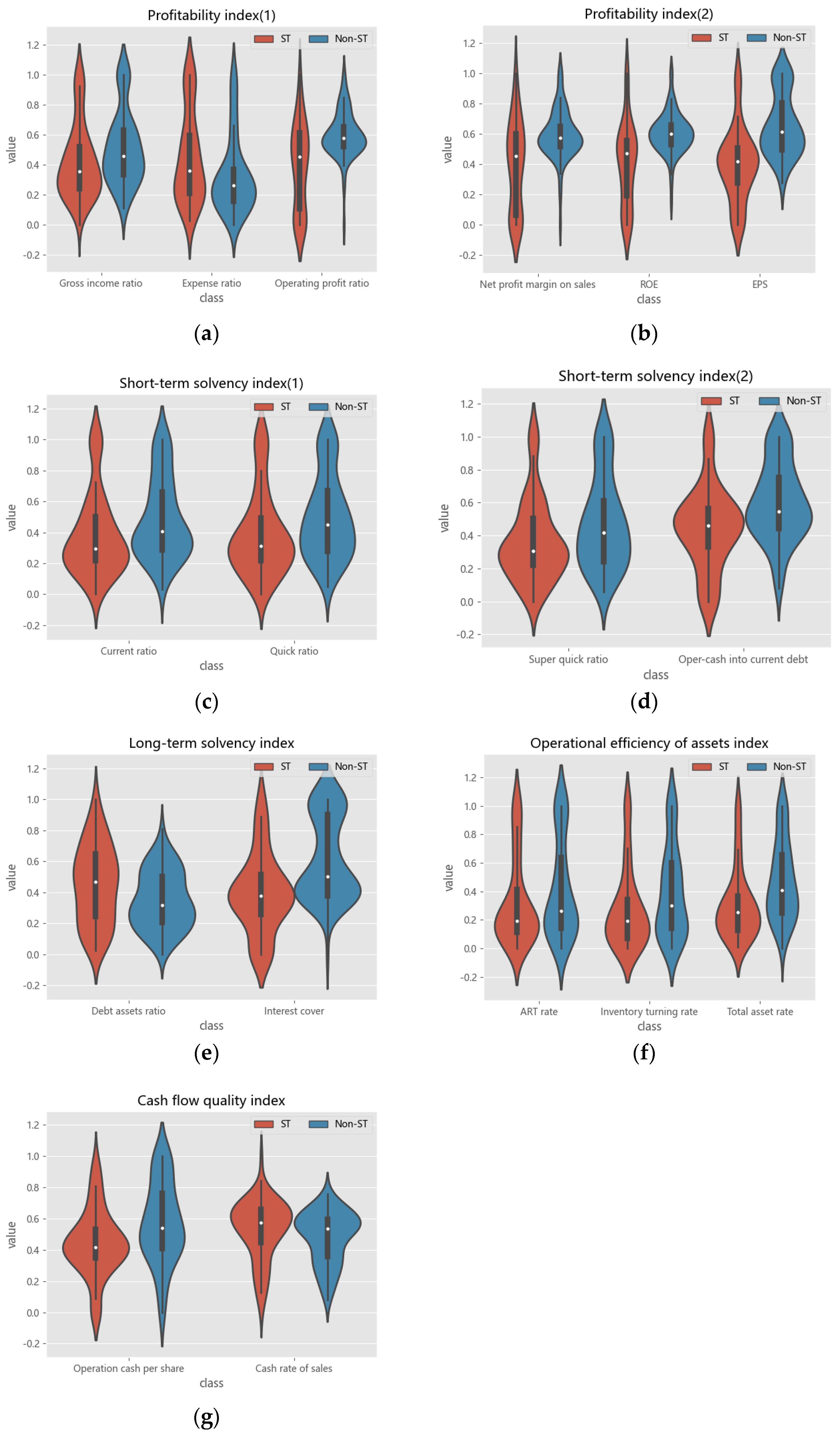

4.2. Principles of Selecting Traditional Financial Indicators and Calculation Caliber

5. Empirical Analysis

5.1. Design of DEA–SVM Financial Crisis Early Warning Method

5.2. Data Source and Sample

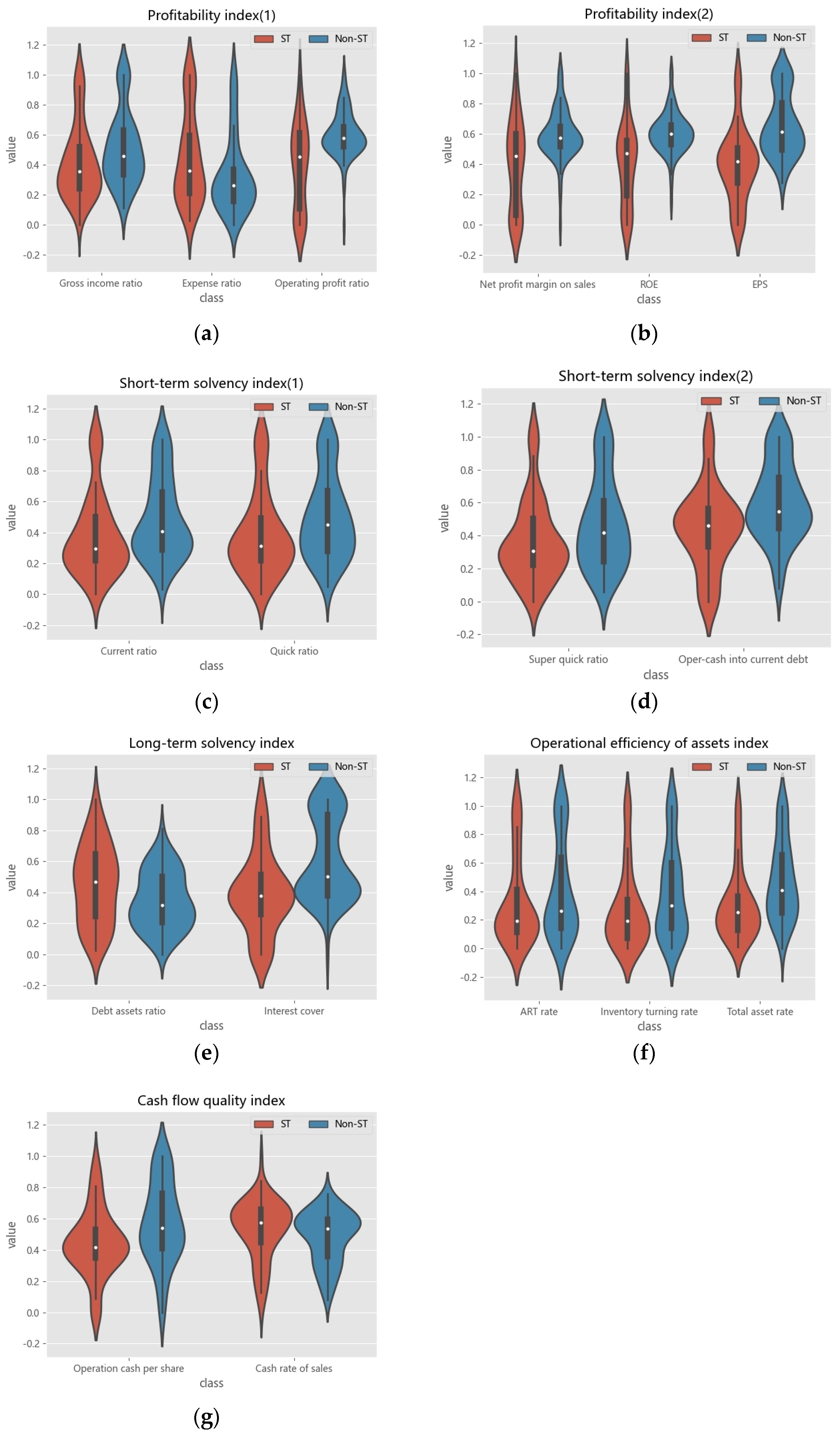

5.3. Data Processing

5.4. Efficiency Value Measurement Based on SBM Model

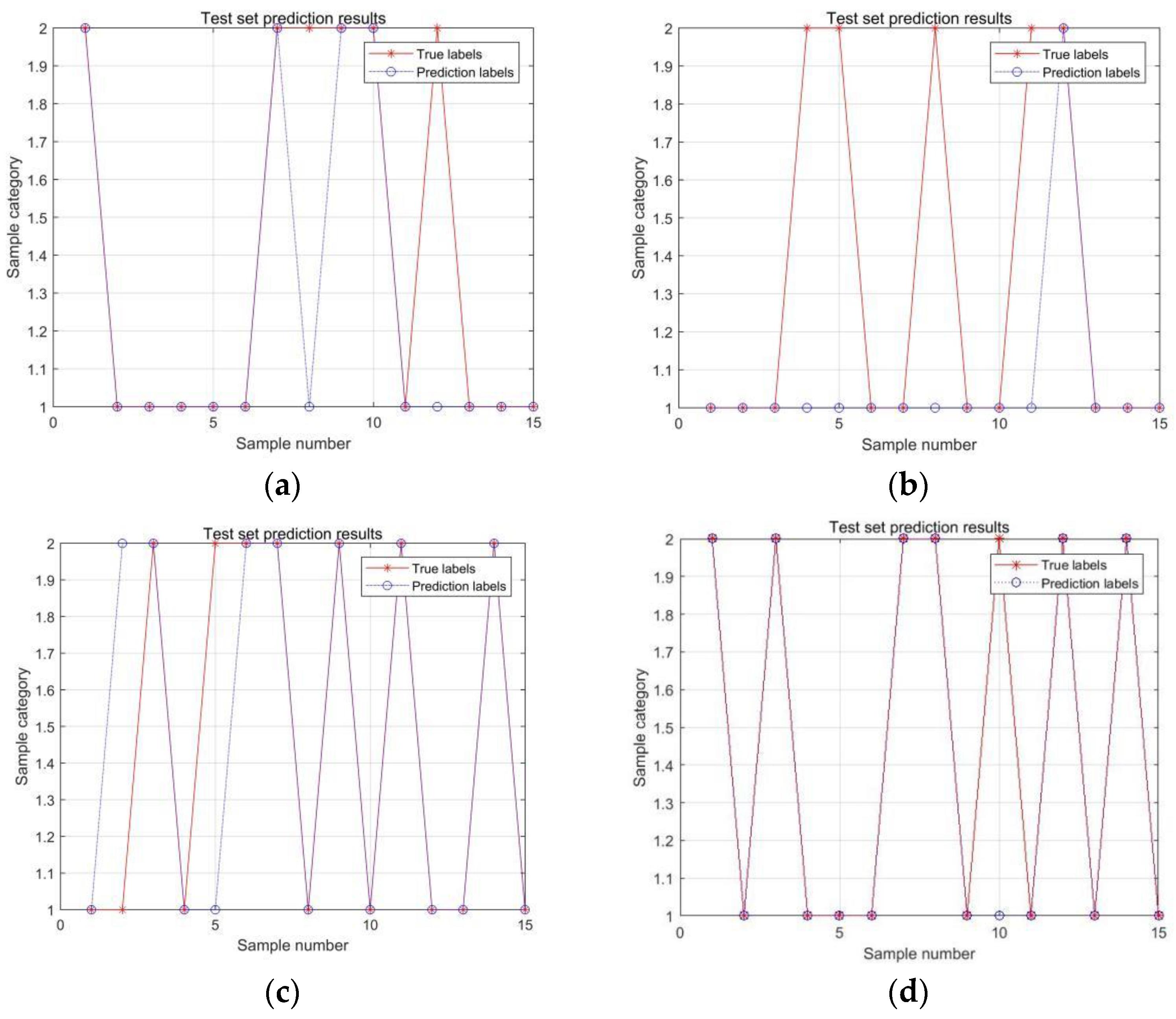

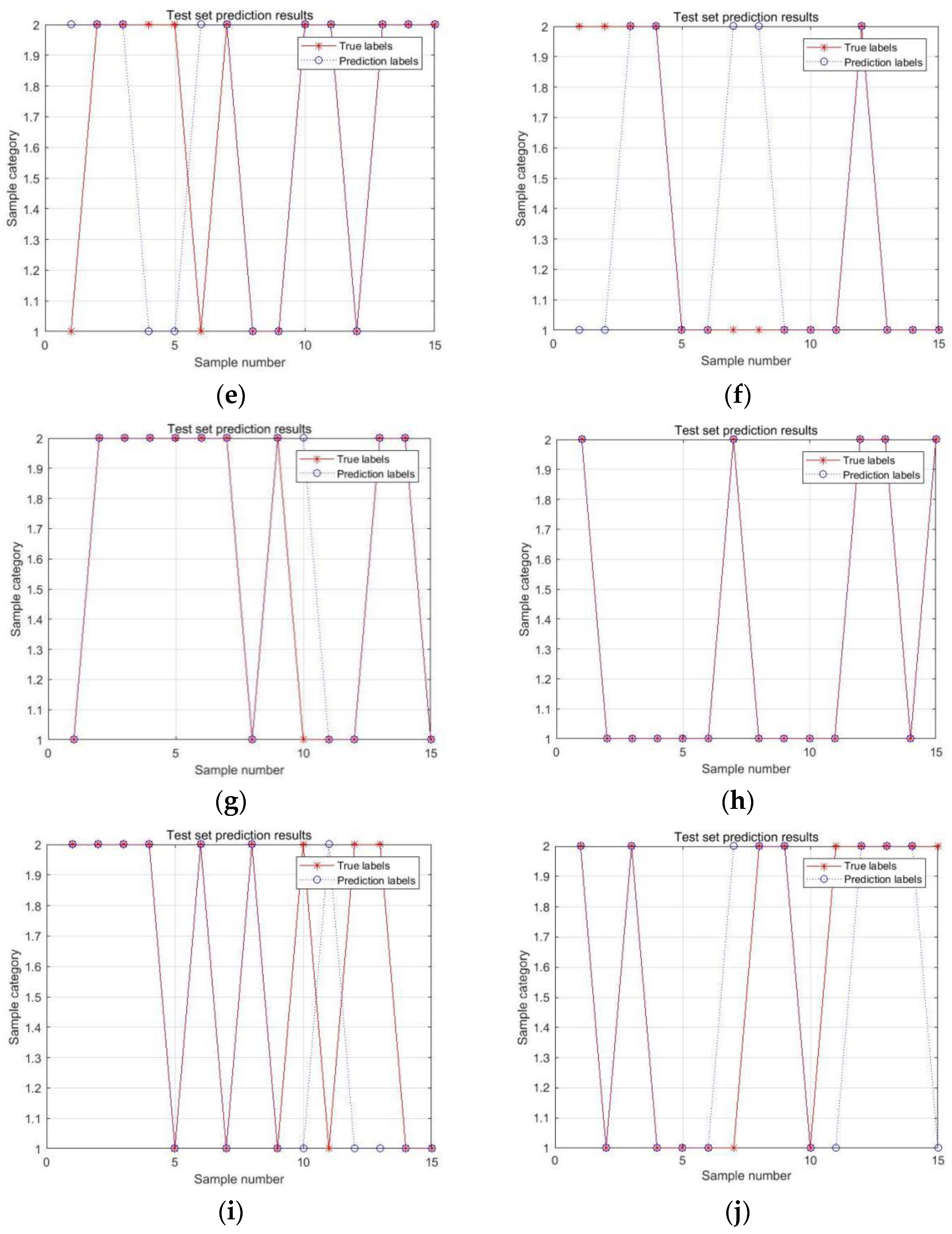

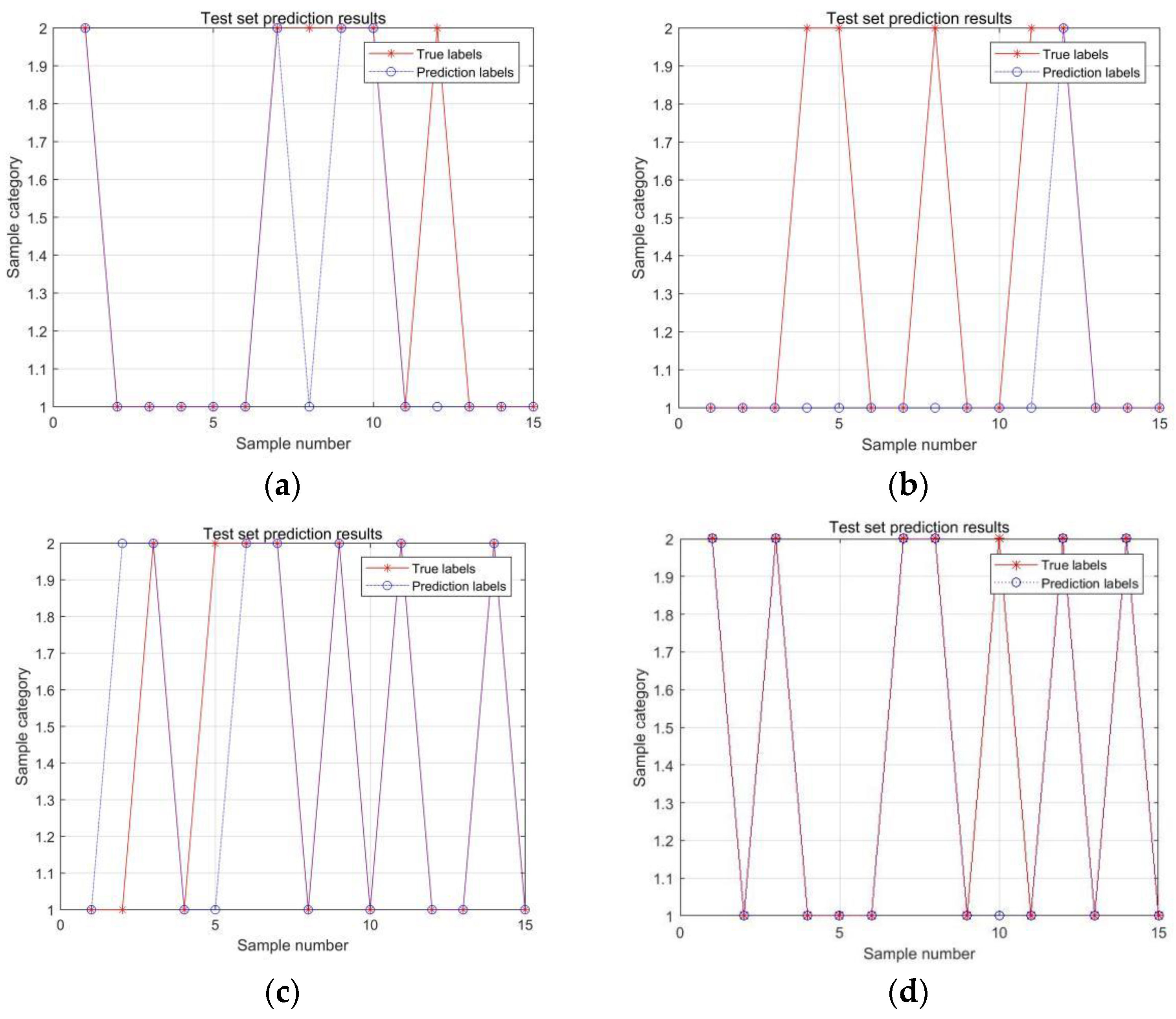

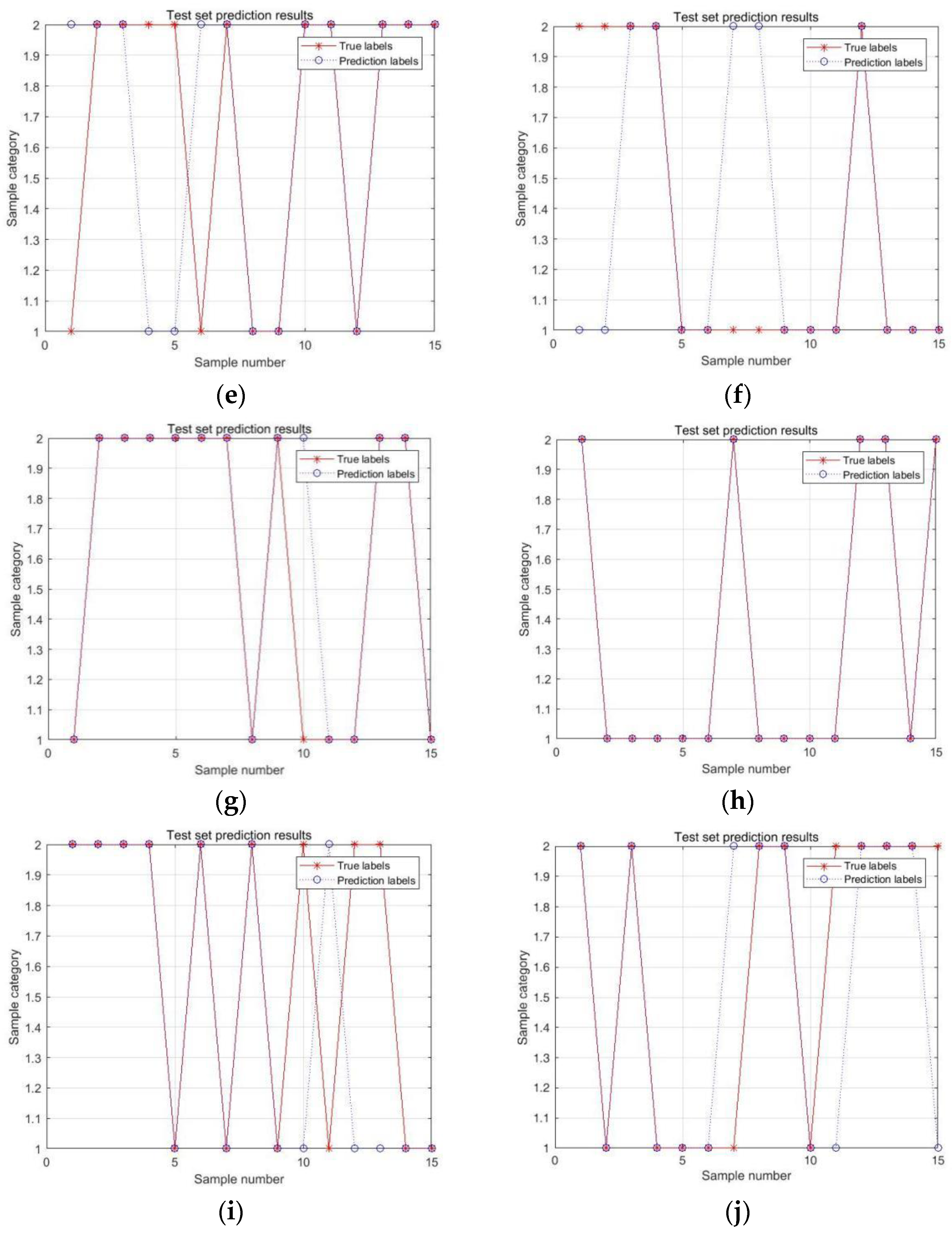

5.5. Development and Experimentation of a Support Vector Machine-Based Early Warning Model

5.6. Empirical Analysis Results

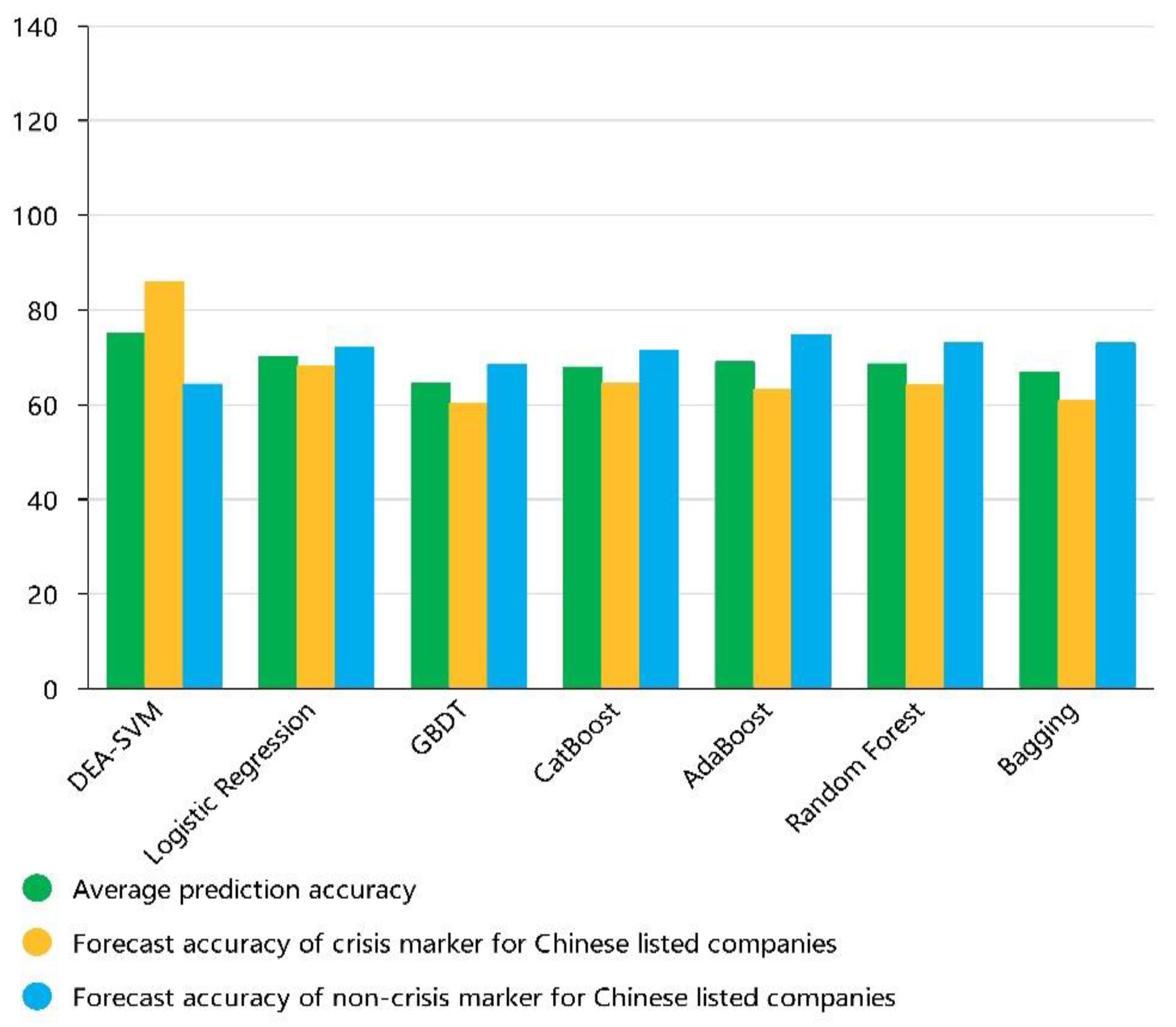

5.7. Empirical Results of DEA and Other Machine Learning Models

6. Conclusions

- In this paper, based on the principles of traditional financial indicators selection and based on the relevant literature, a total of 17 traditional financial indicators in four aspects of profitability, solvency, asset operating efficiency, and cash flow quality are screened based on the combination of modern financial management theory and the Interim Measures for Integrated Performance Evaluation Management of Central Enterprises (2016) issued by the State-owned Assets Supervision and Administration Commission of China. This is a useful exploration of indicator selection and expands the related research.

- This paper makes a more comprehensive evaluation of the operation condition of listed companies through the DEA method, introduces the efficiency indicators obtained from the evaluation into the index system of early warning model, and proposes a prediction index system containing multidimensional efficiency indicators evaluated by DEA and traditional financial indicators.

- This paper considers the construction of a multidimensional efficiency evaluation index system from the input–output perspective and uses big data elements in the construction of the evaluation index system. Then, this paper introduces the public opinion dimension into the index system of the financial crisis early warning model by introducing the stockholders’ comments of the Easteconomy stock forum and Sina stock forum and by measuring the positive sentiment index based on the stockholders’ comments.

- This article constructs a DEA–SVM model together with the SVM model based on the advantages and characteristics of the DEA method and conducts a financial crisis early warning study on 156 listed companies in China. This article proves the effectiveness of the method through empirical research, improves the early warning accuracy of the model, and further optimizes the model using an intelligent optimization algorithm.

- The study is based on the Chinese stock market, and whether it can be extended to the global capital market to form a more universal early warning model is a direction for further research in this paper.

- This study used stock bar commentary texts to the model. This will be a direction for future exploration as to whether other texts, e.g., industry research reports, news media reports, etc., also have a role in identifying early warnings of financial crises.

- This paper uses the positive sentiment index in text analysis, but it is to be further explored whether word frequency, readability, and tense can improve the warning accuracy of the warning model.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Stock Codes | |||

|---|---|---|---|

| 002766.SZ | 002333.SZ | 002232.SZ | 002082.SZ |

| 002005.SZ | 600238.SH | 002745.SZ | 002646.SZ |

| 600702.SH | 300325.SZ | 000799.SZ | 000973.SZ |

| 002420.SZ | 601258.SH | 300475.SZ | 600297.SH |

| 002306.SZ | 002592.SZ | 000721.SZ | 603239.SH |

| 002336.SZ | 002684.SZ | 605188.SH | 603730.SH |

| 000572.SZ | 600698.SH | 601127.SH | 601689.SH |

| 600423.SH | 002700.SZ | 002556.SZ | 002911.SZ |

| 002427.SZ | 002770.SZ | 002998.SZ | 002946.SZ |

| 002650.SZ | 300367.SZ | 600305.SH | 300352.SZ |

| 601113.SH | 600654.SH | 002419.SZ | 600602.SH |

| 600696.SH | 000868.SZ | 600830.SH | 600686.SH |

| 002021.SZ | 000504.SZ | 600843.SH | 002693.SZ |

| 603188.SH | 600080.SH | 603980.SH | 000661.SZ |

| 300029.SZ | 600275.SH | 603628.SH | 600257.SH |

| 000972.SZ | 600399.SH | 600251.SH | 600507.SH |

| 002102.SZ | 002089.SZ | 300267.SZ | 600105.SH |

| 600421.SH | 600119.SH | 300838.SZ | 300240.SZ |

| 002290.SZ | 002289.SZ | 603519.SH | 688299.SH |

| 600408.SH | 600666.SH | 603113.SH | 002387.SZ |

| 600725.SH | 002692.SZ | 600792.SH | 002533.SZ |

| 600265.SH | 002473.SZ | 002679.SZ | 002959.SZ |

| 000422.SZ | 600721.SH | 002386.SZ | 688222.SH |

| 600091.SH | 600767.SH | 000510.SZ | 600763.SH |

| 600319.SH | 002872.SZ | 000635.SZ | 002462.SZ |

| 600301.SH | 600652.SH | 600753.SH | 002425.SZ |

| 600608.SH | 300038.SZ | 000151.SZ | 000607.SZ |

| 600870.SH | 002175.SZ | 600822.SH | 601599.SH |

| 600157.SH | 002629.SZ | 601088.SH | 300164.SZ |

| 300064.SZ | 002200.SZ | 600172.SH | 603316.SH |

| 002569.SZ | 600610.SH | 300840.SZ | 002374.SZ |

| 002656.SZ | 600112.SH | 002029.SZ | 300423.SZ |

| 600365.SH | 600518.SH | 000869.SZ | 600252.SH |

| 603779.SH | 601399.SH | 600543.SH | 600320.SH |

| 000611.SZ | 600193.SH | 600156.SH | 002713.SZ |

| 000737.SZ | 600209.SH | 002709.SZ | 603030.SH |

| 300446.SZ | 000409.SZ | 300847.SZ | 600784.SH |

| 600228.SH | 600149.SH | 002909.SZ | 000632.SZ |

| 600539.SH | 600234.SH | 603408.SH | 600051.SH |

References

- Wu, X.Z. Financial Crisis Early Warning Research: Problems and Framework Reconstruction. Account. Res. 2011, 2, 59–65. [Google Scholar]

- Zhang, Y.; Jiang, T.K. Hayek and Schumpeter—Introduction, comparison and evaluation of the two Austrian schools of economic cycle theory. Economist 2018, 7, 96–104. [Google Scholar]

- Ross, S.A. The Economic Theory of Agency: ThePrincipal’s Problem. Am. Econ. Rev. 1973, 63, 134–139. [Google Scholar]

- Wang, L.; Xing, H.B. A Review of Foreign Corporate Crisis Management Research. Yunnan Financ. Econ. Univ. J. Econ. Manag. 2011, 26, 49–53. [Google Scholar]

- Charnes, A.; Cooper, W.; Rhodes, E. Measuring the efficiency of decision-making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Zhang, M.; Li, L.; Cheng, Z. Research on carbon emission efficiency in the Chinese construction industry based on a three-stage DEA-Tobit model. Environ. Sci. Pollut. Res. 2021, 28, 51120–51136. [Google Scholar] [CrossRef]

- Zhong, K.; Li, C.; Wang, Q. Evaluation of Bank Innovation Efficiency with Data Envelopment Analysis: From the Perspective of Uncovering the Black Box between Input and Output. Mathematics 2021, 9, 3318. [Google Scholar] [CrossRef]

- Zhong, K.Y.; Wang, Y.F.; Pei, J.M.; Tang, S.M.; Han, Z.L. Super efficiency SBM-DEA and neural network for performance evaluation. Inf. Process. Manag. 2021, 58, 102728. [Google Scholar] [CrossRef]

- Vapnik, V.N. The nature of statistical learning theory. Nat. Stat. Learn. Theory 1995, 20, 273–297. [Google Scholar]

- Vapnik, V.N. Statistical learning theory. Encycl. Sci. Learn. 1998, 41, 3185. [Google Scholar]

- Vapnik, V.N. An overview of statistical learning theory. IEEE Trans. Neural Netw. 1999, 10, 988–999. [Google Scholar] [CrossRef] [Green Version]

- Fitzpatrick, F. A comparison of ratios of successful industrial enterprises with those of failed firm. Certif. Public Account. 1932, 10, 598–605. [Google Scholar]

- Altman, E.I. Financial Ratios, Discriminant Analysis and the Prediction of Corporate Bankruptcy. J. Financ. 1968, 23, 589–609. [Google Scholar] [CrossRef]

- Altman, E.I.; Haldeman, R.G.; Narayanan, P. Zetatm analysis a new model to identify bankruptcy risk of corporations. J. Bank. Financ. 1977, 1, 29–54. [Google Scholar] [CrossRef]

- Ohlson, J.A. Financial ratios and the probabilistic prediction of bankruptcy. J. Account. Res. 1980, 3, 109–131. [Google Scholar] [CrossRef] [Green Version]

- Fan, A.; Palaniswami, M. Support vector machines symposium proceedings. In Proceedings of the IEEE Computer Society, Washington, DC, USA, 4–6 November 2002. [Google Scholar]

- Min, J.H.; Lee, Y.C. Bankruptcy prediction using support vector machine with optimal choice of kernel function parameters. Expert Syst. Appl. 2005, 28, 603–614. [Google Scholar] [CrossRef]

- Yan, J.J.; Liu, J.H. Support vector machine early warning model for financial crisis of listed companies. Stat. Decis. 2006, 12, 158–159. [Google Scholar]

- Song, J. An Empirical Study on Early Warning of Financial Crisis of Listed Companies Based on Support Vector Machine. Mark. Mod. 2007, 25, 391–392. [Google Scholar]

- Boyacioglua, M.A.; Kara, Y.; Baykan, K. Predicting bank financial failures using neural networks, support vector machines and multivariate statistical methods: A comparative analysis in the sample of savings deposit insurance fund (SDIF) transferred banks in Turkey. Expert Syst. Appl. 2009, 36, 3355–3366. [Google Scholar] [CrossRef]

- Beaver, W.H. Financial rations as predictors of failures. J. Account. Res. 1966, 4, 71–111. [Google Scholar] [CrossRef]

- Wu, S.N.; Lu, X.Y. A study on the prediction model of financial distress of listed companies in China. Econ. Res. J. 2001, 6, 46–55+96. [Google Scholar]

- Wang, J.T.; Sun, T.T. Research on financial early warning of energy-consuming enterprises based on genetic BP neural network. J. Harbin Univ. Commer. 2012, 5, 110–116. [Google Scholar]

- Barboza, F.; Kimura, H.; Altman, E. Machine learning models and bankruptcy prediction. Expert Syst. Appl. 2017, 83, 405–417. [Google Scholar] [CrossRef]

- Xiao, Y.; Xiong, K.L.; Zhang, X. Research on early warning model of enterprise financial risk based on TEI@I methodology. Manag. Rev. 2020, 32, 226–235. [Google Scholar]

- Ran, M.S.; Zhou, S.; Huang, L.Y. Application of SVM model based on DEA indicators in financial warning. Stat. Decis. 2009, 20, 143–145. [Google Scholar]

- Xu, X.; Wang, Y. Financial failure prediction using efficiency as a predictor. Expert Syst. Appl. 2009, 36, 366–373. [Google Scholar] [CrossRef]

- Li, Z.; Crook, J.N.; Andreeva, G. Dynamic prediction of financial distress using malmquist DEA. Soc. Sci. Electron. Publ. 2017, 80, 94–106. [Google Scholar] [CrossRef] [Green Version]

- Tone, K. A slacks-based measure of efficiency in data envelopment analysis. Eur. J. Oper. Res. 2001, 130, 498–509. [Google Scholar] [CrossRef] [Green Version]

- Cherkassky, V.; Ma, Y. Practical selection of SVM parameters and noise estimation for SVM regression. Neural Netw. 2004, 17, 113–126. [Google Scholar] [CrossRef] [Green Version]

- Sun, H.W.; Yu, Z.X. Extension of Mercer’s theorem. J. Univ. Jinan 2004, 3, 280–282. [Google Scholar]

- Xie, D.R.; Lin, L. Can the tone of management predict the future performance of the company?—A textual analysis based on annual earnings presentations of listed companies in China. Account. Res. 2015, 2, 20–27. [Google Scholar]

- Billio, M.; Casarin, R.; Costola, M.; Pasqualini, A. An entropy-based early warning indicator for systemic risk. J. Int. Financ. Mark. Inst. Money 2016, 45, 42–59. [Google Scholar] [CrossRef] [Green Version]

- Ma, Y.; Chen, Y. Financial imbalance index as a new early warning indicator: Methods and applications in the Chinese economy. China World Econ. 2014, 22, 64–86. [Google Scholar] [CrossRef]

- Zhang, Y.L.; You, X.L.; Qiang, W. LASSO-based early warning of corporate financial crisis and selection of key indicators. J. Henan Norm. Univ. 2016, 44, 160–165. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- China State-owned Assets Supervision and Administration Commission. Notice on the Issuance of the Implementation Rules for the Comprehensive Performance Evaluation of Central Enterprises. Announc. State Own. Assets Superv. Adm. Comm. State Counc. China 2006, 9, 5–16. [Google Scholar]

- Zhao, X.J.; Zhao, X.F.; Shao, L.J. Box plotting based on a new formula for calculating quartiles. J. Tangshan Norm. Univ. 2020, 42, 13–15. [Google Scholar]

- Shen, J.J.; Long, W. Treatment of negative output in DEA models-based on the use of software DEAP. In Proceedings of the Annual China Management Conference, Hefei, China, 6–8 December 2015. [Google Scholar]

- Kerstens, K.; Van, D. Negative data in DEA: A simple proportional distance function approach. J. Oper. Res. Soc. 2011, 62, 1413–1419. [Google Scholar] [CrossRef]

| Dimensions | Input Indicators | Output Indicators |

|---|---|---|

| Operation dimension | Operating costs Total expense | Revenue Total profit |

| Dimensions | Input Indicators | Output Indicators |

|---|---|---|

| Innovation dimension | R&D Number of R&D personnel Government subsidy | ROE Rate of return on total assets |

| Dimensions | Input Indicators | Output Indicators |

|---|---|---|

| Finance dimension | Oper-cash into current debt Debt assets ratio Total asset rate Current assets turnover | ROE Ratio of profits to cost Return on assets |

| Dimensions | Input Indicators | Output Indicators |

|---|---|---|

| Financing dimension | Cash flow from financing activities Total liabilities Total asset Operating costs | Total asset rate ROE Revenue |

| Dimensions | Input Indicators | Output Indicators |

|---|---|---|

| Public opinion dimension | Number of events announced by listed companies in China | Shareholder comments positive sentiment index |

| Indicators | Algorithms |

|---|---|

| Gross income ratio (%) | (Operating income-Operating costs)/Operating income × 100% |

| Expense ratio (%) | Selling expenses as a percentage + management expenses as a percentage + financial expenses as a percentage + R&D expenses as a percentage (all calculated as XX expenses/operating income × 100%) |

| Operating profit ratio (%) | Operating profit/Operating revenue × 100% |

| Net profit margin on sales (%) | (Net income attributable to shareholders of the parent company + minority interests)/operating income × 100% |

| ROE (%) | Net income/average net assets × 100% |

| EPS (Yuan) | Net income (also known as profits or earnings) divided by available shares. |

| Indicators | Algorithms |

|---|---|

| Current ratio(times) | Current assets/current liabilities |

| Quick ratio (times) | (Current Assets-Inventories-Prepaid Expenses)/Current Liabilities |

| Super quick ratio (times) | Super quick assets divide by the current liabilities of a business (super quick assets = cash + trading financial asset + notes receivable + accounts receivable + other receivables) |

| Oper-cash into current debt (%) | Cash flow from operating activities/current liabilities × 100% |

| Indicators | Algorithms |

|---|---|

| Debt assets ratio (%) | Total liabilities/total assets × 100% |

| Interest cover (times) | EBIT/interest expense (EBIT = net income + interest expense + income tax expense, the numerator “interest expense” is taken from the interest expense of financial expenses in the income statement, the denominator “interest expense” is taken from the interest expense of financial expenses in the income statement + capitalized interest included in the balance sheet fixed assets and other costs) |

| Indicators | Algorithms |

|---|---|

| ART rate (frequency) | Operating income/notes and accounts receivable (using operating income as the numerator here would overestimate the turnover rate of accounts receivable, and it is more reasonable to use credit sales, as credit sales data are not available; thus, operating income is used. In addition, there are seasonal factors affecting notes and accounts receivable; thus, it is more reasonable to take the average of multiple time points) |

| Inventory turning rate (frequency) | Operating costs/inventory (the assessment here is the performance of inventory management, not short-term solvency analysis; thus, operating costs are chosen and inventory is still using the average of the beginning and end of the year) |

| Total asset rate (frequency) | Operating income/total assets (where total assets are averaged at the beginning of the year-end) |

| Indicators | Algorithms |

|---|---|

| Operation cash per share (Yuan) | Cash flow from operating activities/Total common share capital at the end of the year |

| Cash rate of sales (times) | Cash received from sales of goods and services/operating income |

| Experimental Group | Average Prediction Accuracy | Forecast Accuracy of Crisis Marker for Chinese-Listed Companies | Forecast Accuracy of non-Crisis Marker for Chinese-Listed Companies |

|---|---|---|---|

| Contains multi-dimensional efficiency metrics | 75.09% | 85.89% | 64.29% |

| Without multidimensional efficiency indicators | 71.34% | 83.39% | 59.29% |

| Experimental Group | Average Prediction Accuracy | Forecast Accuracy of Crisis Marker for Chinese-Listed Companies | Forecast Accuracy of Non-Crisis Marker for Chinese-Listed Companies |

|---|---|---|---|

| Contains multi-dimensional efficiency metrics | 83.83% | 89.74% | 77.92% |

| Without multidimensional efficiency indicators | 74.02% | 87.01% | 61.03% |

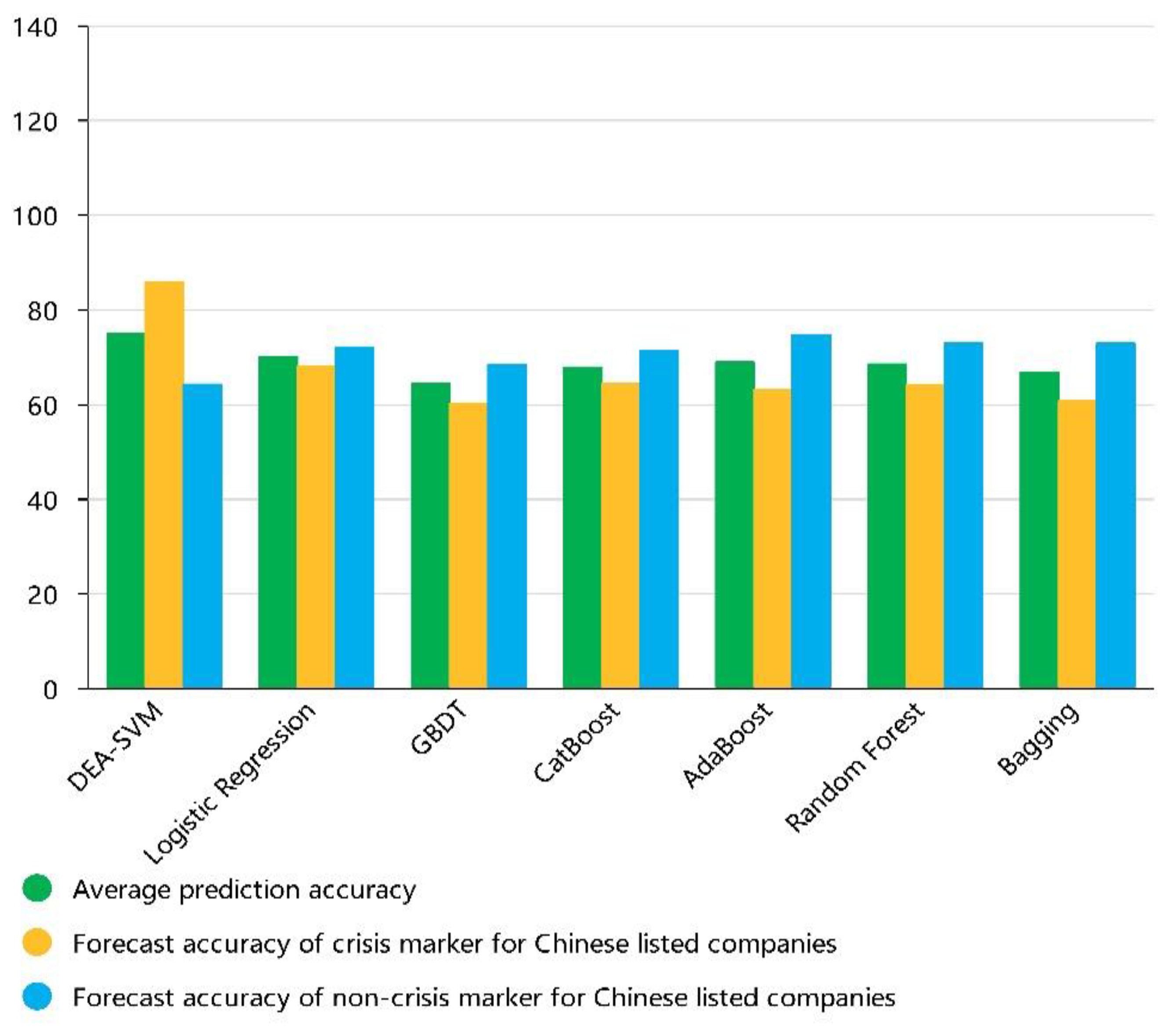

| Experimental Group | Average Prediction Accuracy | Forecast Accuracy of Crisis Marker for Chinese-Listed Companies | Forecast Accuracy of non-Crisis Marker for Chinese-Listed Companies | |

|---|---|---|---|---|

| Logistic Regression | Contains multi-dimensional efficiency metrics | 70.12% | 68.06% | 72.18% |

| Without multidimensional efficiency indicators | 66.20% | 64.77% | 67.63% | |

| Predicted improvement after incorporating multidimensional efficiency indicators | 3.92% | 3.29% | 4.55% | |

| GBDT | Contains multi-dimensional efficiency metrics | 64.38% | 60.34% | 68.42% |

| Without multidimensional efficiency indicators | 61.08% | 57.73% | 64.42% | |

| Predicted improvement after incorporating multidimensional efficiency indicators | 3.30% | 2.61% | 4.00% | |

| CatBoost | Contains multi-dimensional efficiency metrics | 67.88% | 64.41% | 71.35% |

| Without multidimensional efficiency indicators | 63.92% | 56.66% | 71.17% | |

| Predicted improvement after incorporating multidimensional efficiency indicators | 3.96% | 7.75% | 0.18% | |

| AdaBoost | Contains multi-dimensional efficiency metrics | 68.97% | 63.20% | 74.74% |

| Without multidimensional efficiency indicators | 65.26% | 57.02% | 73.49% | |

| Predicted improvement after incorporating multidimensional efficiency indicators | 3.71% | 6.18% | 1.25% | |

| Random Forest | Contains multi-dimensional efficiency metrics | 68.60% | 64.27% | 72.92% |

| Without multidimensional efficiency indicators | 65.13% | 60.41% | 69.85% | |

| Predicted improvement after incorporating multidimensional efficiency indicators | 3.46% | 3.86% | 3.07% | |

| Bagging | Contains multi-dimensional efficiency metrics | 66.85% | 60.77% | 72.92% |

| Without multidimensional efficiency indicators | 65.72% | 59.34% | 72.10% | |

| Predicted improvement after incorporating multidimensional efficiency indicators | 1.13% | 1.43% | 0.82% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Z.; Xiao, Y.; Fu, Z.; Zhong, K.; Niu, H. A Study on Early Warnings of Financial Crisis of Chinese Listed Companies Based on DEA–SVM Model. Mathematics 2022, 10, 2142. https://doi.org/10.3390/math10122142

Zhang Z, Xiao Y, Fu Z, Zhong K, Niu H. A Study on Early Warnings of Financial Crisis of Chinese Listed Companies Based on DEA–SVM Model. Mathematics. 2022; 10(12):2142. https://doi.org/10.3390/math10122142

Chicago/Turabian StyleZhang, Zhishuo, Yao Xiao, Zitian Fu, Kaiyang Zhong, and Huayong Niu. 2022. "A Study on Early Warnings of Financial Crisis of Chinese Listed Companies Based on DEA–SVM Model" Mathematics 10, no. 12: 2142. https://doi.org/10.3390/math10122142

APA StyleZhang, Z., Xiao, Y., Fu, Z., Zhong, K., & Niu, H. (2022). A Study on Early Warnings of Financial Crisis of Chinese Listed Companies Based on DEA–SVM Model. Mathematics, 10(12), 2142. https://doi.org/10.3390/math10122142