1. Introduction

The worldwide recovery from the COVID-19 pandemic is anticipated to continue throughout 2022 and 2023, driven by progress in global immunization efforts, the implementation of supportive macroeconomic policies in major economies, and favorable financial conditions. In response to the COVID-19 crisis, policymakers took significant legislative actions that involved providing substantial fiscal support to businesses and individuals, thereby preventing a deeper decline in employment, incomes, and productivity

Dörr et al. (

2022). The successful deployment of COVID-19 vaccines increased confidence among consumers and businesses, leading to a resumption of economic activities. This boost in economic confidence accelerated recovery, prompting central banks to revise growth projections upwards (

Oskam and Davis 2023). On the other hand, in advanced economies, central banks and monetary authorities have implemented substantial measures to ease monetary policy, aiming to bolster the economy and attain their inflation targets. These measures include lowering interest rates and augmenting their government bond holdings as part of their reserve assets (

Gertler and Karadi 2011).

The primary objective of this research is to analyze the effects of monetary policy measures on key economic indicators, such as GDP (Gross Domestic Product), inflation, and unemployment, during the COVID-19 pandemic period and in the post-pandemic period.

This study is motivated by inconsistent macroeconomic circumstances such as heightened levels of public debt, limited monetary policy flexibility, and the lasting effects on certain segments of the labor market. The most of OECD (Organisation for Economic Co-operation and Development) countries currently face an unparalleled economic situation in the wake of the profound aftermath of the COVID-19 pandemic. This predicament has been exacerbated by the surge in energy and food prices, driven by Russia’s invasion of Ukraine. Given these intricate circumstances, the necessity arises to meticulously identify both fiscal and monetary policy measures and their corresponding impacts.

Many researchers (

Deslatte et al. 2020;

Kritzinger et al. 2021;

Naudé and Cameron 2021) argue that governments and their economic policies have demonstrated a clear mishandling of the COVID-19 pandemic from the very start. This fact has become increasingly apparent over time. The concern lies in their current misinterpretation of the inflationary stage of the epidemic, which poses the significant risk of a recession. On the other hand, to mitigate demand, governments can consider reducing their own expenditures. Central banks have also taken measures to increase the cost of borrowing money, thereby curbing demand, as evidenced by the recent interest rate hikes in the U.S., Australia, and Europe (

Song and Zhou 2020). Hence, an examination of how governments responded through monetary policy measures to address economic growth, inflationary pressures, and unemployment during both the COVID-19 period and the subsequent post-pandemic period becomes essential.

Since this study is based on panel data analysis, employing a Panel ARDL (Autoregressive Distributed Lag) model for 33 OECD countries from 2020 to 2023, it is important to note that each country has different exchange rate policy regimes and interest rate policy decisions. This study does not account for these differences due to data availability and to avoid complexities. Therefore, it relaxes the conditions regarding exchange rate policy regimes and distinct interest rate rules for the monetary policies of each respective country.

A pandemic is defined as a widespread outbreak of a contagious disease, typically affecting a vast geographic area and leading to profound societal and economic disruptions. Accurate policy decisions made by a country are of paramount importance in shaping economic growth, controlling inflation, and managing employment levels, especially in the face of such significant economic shocks. Monetary policy stands out as a critical factor in this equation, given that economic effects and challenges often persist even after the immediate health crisis subsides. Surprisingly, there has been a dearth of substantial discussion and focus on the specific question of how monetary policy should be conducted during a pandemic and in the post-pandemic recovery phase. Considering the substantial economic ramifications of a pandemic and the pivotal role that monetary policy plays in maintaining economic stability, this lack of attention underscores the pressing need for further discussion on this critical topic. The novelty of this research lies in its comparative analysis of the effectiveness and sustainability of different monetary policy responses across various OECD countries. It provides valuable insights into the evolving role of central banks in crisis management and contributes to the broader understanding of how monetary policy can be adapted to unprecedented global challenges.

This paper is structured as follows:

Section 2 discusses the role of COVID-19 in the current economic problems and

Section 3 provides a literature review, while

Section 4 describes the methodology. In

Section 5, we examine the economic impact of the COVID-19 pandemic and the monetary policy responses, and we then discuss the deployment of fiscal policies during the COVID-19 crisis in OECD countries. Finally,

Section 6 concludes the study by summarizing the findings, presenting policy implications, acknowledging the limitations of the existing literature, and proposing avenues for future research.

2. The Global Economic Challenges during the COVID-19 Pandemic

The global economy has experienced a profound impact due to the COVID-19 pandemic, resulting in widespread disruptions to historical growth trends in countries across the globe. Nevertheless, as most COVID-19-related restrictions and health measures are being lifted, economic growth is now showing signs of recovering and aligning with longer-term patterns. However, it is crucial to acknowledge that the economic consequences of the pandemic were evident from the beginning, and it has taken a toll on public health and human lives. Therefore, this unprecedented global crisis is widely acknowledged as the most significant economic shock witnessed in decades.

The COVID-19 pandemic underscored the urgency of taking immediate action to mitigate its health-related and economic consequences, to safeguard vulnerable populations, and to establish a foundation for long-term recovery. It was crucial for all the countries, many of which confront formidable vulnerabilities, to enhance their public health systems, tackle the issues arising from informal sectors, and implement reforms that will foster robust and sustainable growth beyond the health crisis.

For many economies, real GDP has reached or surpassed pre-pandemic levels observed in the fourth quarter of 2019. Nevertheless, there remains significant variation in economic progress across different countries (

Jackson et al. 2020). The

World Economic Situation and Prospects report underscores the continued repercussions of the COVID-19 pandemic, along with unattended macroeconomic structural challenges, which present substantial risks to the global economy. Projected for 2023, global GDP growth is anticipated to be 2.6%, marking the lowest annual rate since the global financial crisis, excluding the influence of the 2020 pandemic. However, there is a slight recovery expected in 2024, with growth predicted to improve to 2.9% (

Seitzer et al. 2023). The economic consequences of the COVID-19 crisis vary across different regions. The extent of the impact is influenced by regional economic specialization in sectors that are directly or indirectly affected by the crisis, as well as the level of involvement in global value chains (

Boyce et al. 2023).

In 2022, the global economy witnessed a significant surge in inflation, affecting both developed and emerging economies. This increase in inflation was driven by a combination of global factors that contributed to and amplified the ongoing worldwide inflationary trend. The recovery of demand following the COVID-19 crisis, coupled with various supply challenges, played a key role in exerting pricing pressures on the economy (

Hazakis 2022).

The COVID-19 pandemic has had a notable impact on elevating inflation rates in numerous countries. Sectors that experienced significant disruptions due to lockdown measures, including recreation, accommodation, and transportation, have been major contributors to the inflation surge in 2022. In the contest of OECD countries, the inflation rate in the OECD area experienced a notable and considerable increase in December 2021 when compared to the same 12-month period in 2020. This surge in inflation was partially driven by a significant rise in Turkey’s annual inflation (

OECD 2023). Within the OECD area, energy prices witnessed a substantial increase of 25 percent over the 12-month period leading up to December 2021. When excluding food and energy, OECD year-on-year inflation also rose sharply to 4.6% and made a significant contribution to headline inflation in several major economies. Looking at the entirety of 2022, the annual inflation rate in the OECD rose to 4.0%, a significant increase compared to the 1.4% recorded in 2021, marking the highest annual average rate since 2000. These statistics indicate that the global economy faces a myriad of challenges, including high inflation, tightening financial conditions across most regions, Russia’s invasion of Ukraine, and the COVID-19 pandemic. These factors are exerting significant pressure on economic prospects. The normalization of monetary and fiscal policies, which provided unprecedented support during the pandemic, is now dampening demand as policymakers aim to curb inflation and restore stability. Consequently, an increasing number of economies are witnessing a slowdown, and some even face contractionary growth. The future health of the global economy hinges critically on the precise calibration of monetary policy, the resolution of the Ukrainian conflict, and the potential for additional supply-side shocks stemming from the ongoing pandemic.

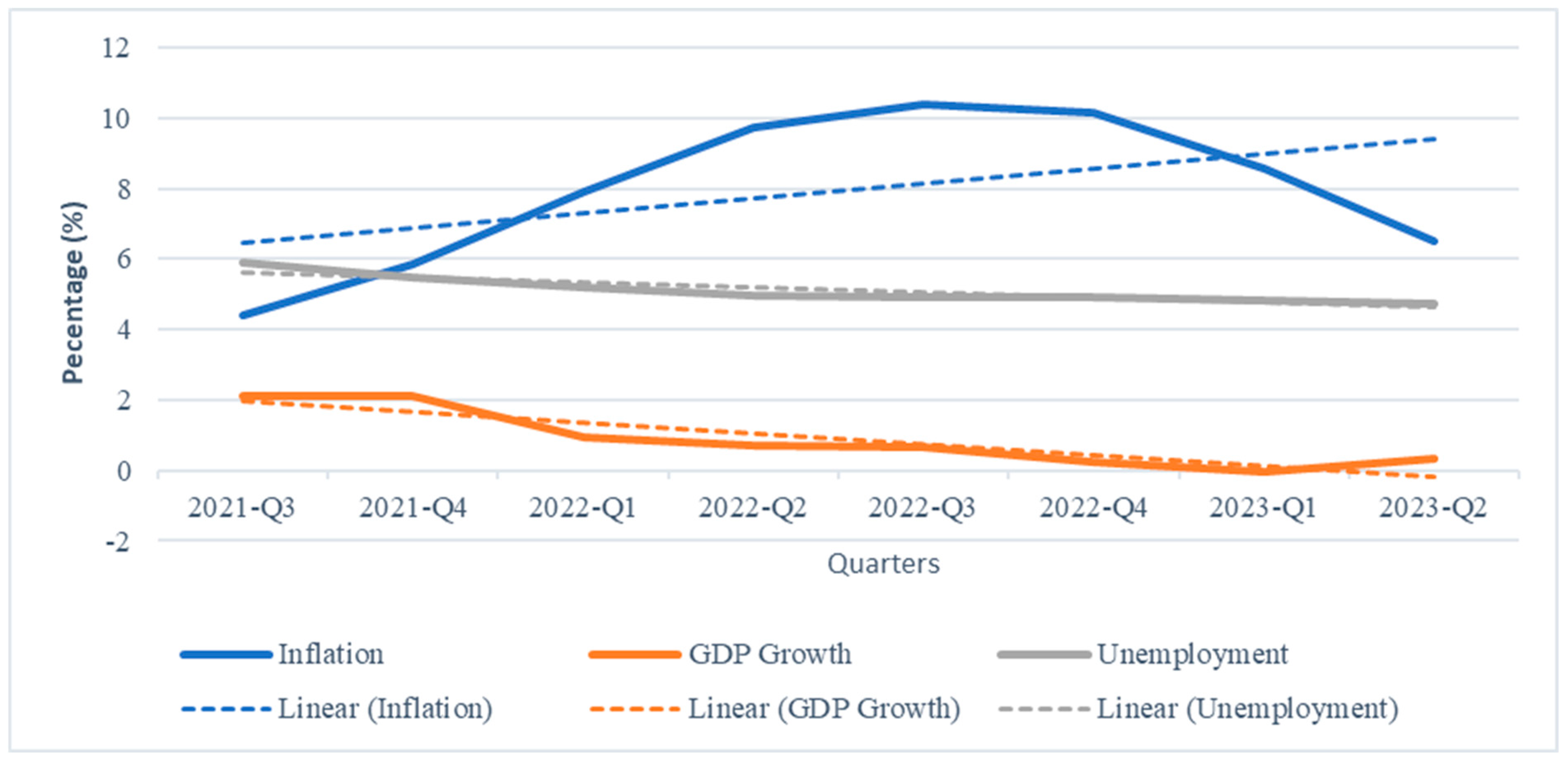

The economic shocks of 2022 are exacerbating the ongoing economic scarring from the pandemic (

Figure 1), particularly for all OECD economies. At the start of 2022, the pandemic’s severe impact on global GDP was already at a negative value of about −0.05 percent by Q1 2023. Inflation increased from 4.4 percent in Q3 2021 to 10.39 percent in Q3 2022, before declining to 8.56 percent in Q1 2023. Prices in the third quarter of 2023 declined at 6.1 percent lower than in the same quarter of 2022. Rising inflation with declining real wages and declining unemployment characterized the macroeconomic situation in 2021 in many economies. Therefore, the lasting reduction of inflation will depend significantly on the determination of monetary policymakers.

On the other hand, the tightening of labor markets coupled with reduced labor supply in contact-intensive industries due to health concerns, changing worker preferences, and limitations on cross-border movement, has likely added to the inflationary pressures. Moreover, numerous service sector businesses that are particularly vulnerable to these obstacles may face insurmountable challenges, leading to an escalation in the risk of job losses and bankruptcies. Consequently, this could adversely impact overall demand in the economy.

3. Literature Review

This paper contributes to the rapidly expanding literature on monetary policy reactions to the COVID-19 pandemic and the effectiveness of the policy measures in response. There are two main strands in the literature: the first investigates the theoretical background, while the second examines the impact of the COVID-19 shock on GDP growth, inflation rates, and unemployment due to monetary policy interactions and their effectiveness.

According to Keynesian economic theory, swift government actions are considered crucial for stimulating demand and facilitating economic recovery during crises, as highlighted in prior research (

van Aarle 2017). Keynes emphasized that a policy of government non-intervention would be a grave mistake, leading to a decline in economic output and prolonged suffering for millions of individuals (

Byrialsen et al. 2021;

Alozie et al. 2020). Consequently, both traditional and non-traditional economists seem to agree on the importance of combining short-term supply-side policies with traditional Keynesian expansionary measures to avert a recession and address price fluctuations during the current crisis (

Eichenbaum et al. 2021;

van Aarle 2017),

Godri Pollitt et al. (

2020).

Throughout history, health pandemics have inflicted significant shocks on the U.S. economy. Examples include the flu pandemics of 1957 and 1968, which were followed by economic downturns, as well as the highly disruptive impact of the 1918 Spanish flu on society as a whole. The unique nature of a pandemic leads to both a demand shock, as consumers curtail their activities, and a supply shock, as businesses either close or scale back their operations. Additionally, the sudden onset of these extreme shocks provides little to no advance warning for consumers, businesses, or governments, resulting in a swift and pronounced shift in overall economic conditions (

Wolf 2014).

The global financial market faced intensified challenges due to the COVID-19 outbreak, prompting central banks in developed countries to implement unconventional measures to alleviate the adverse effects. It is crucial, both from an academic and policy perspective, to comprehend the consequences of the pandemic shock and assess the effectiveness of the implemented policies aimed at mitigating its impact (

Karaman 2022). While some economists argue that nonconventional monetary tools may offset the effect of the lower bound and provide space for monetary policy (

Bernanke and Yellen 2020), others suggest that, due to the changing nature of macroeconomics, the ability of monetary policy to accomplish much when interest rates are at their lower bound is limited (

DeLong et al. 2012;

Eichenbaum 2019;

Corradin et al. 2021;

Ortmans and Tripier 2021).

Ortmans and Tripier (

2021) present evidence that fiscal and monetary policy measures effectively lowered bond yields for European economies. In contrast,

Lepetit and Fuentes-Albero (

2022) studied the effects of an unanticipated decline in interest rates, concluding that monetary policy is likely to be ineffective at the height of the pandemic but should aid in sustaining the recovery in economic activity once the virus begins to dissipate. Further, the high inflation following COVID-19 is not transitory but persistent. The recent economic recovery and the excessive supply of money from fiscal and monetary policies have increased the core inflation rate beyond a temporary phase (

Gharehgozli and Lee 2022;

Lepetit and Fuentes-Albero 2022).

Furthermore, conventional monetary policy has a minimal impact on GDP during pandemics, whereas unconventional monetary policy measures have the potential to mitigate the overall decline in GDP (

Gertler and Karadi 2011).

Yilmazkuday (

2020) examines the effects of U.S. monetary policy, specifically policy rates, on exchange rates in 21 emerging-market countries during the pandemic period. The findings indicate that a negative shock in U.S. monetary policy resulted in currency depreciation in emerging markets.

Bhar and Malliaris (

2021) discover that the Federal Reserve’s unconventional monetary policies, implemented in response to the 2008 financial crisis, could effectively reduce longer-term interest rates. They suggest that these findings hold valuable insights for central banks in addressing the financial and economic repercussions of COVID-19 (

Bhar and Malliaris 2021;

Yilmazkuday 2020).

According to

Wei and Han (

2021), during the COVID-19 pandemic, neither conventional nor unconventional monetary policies had significant effects on all four financial markets: government bonds, stocks, exchange rates, and credit default swaps. However, unconventional monetary policies were slightly more effective than conventional policies, as they had some impact on the stock and exchange rate markets. On the other hand, the uncertainty effects of COVID-19 are much stronger, affecting aggregate demand, prices, the exchange rate, and the degree of trade openness, while complicating monetary policy interventions. In terms of regulating demand and curbing inflation, simulations conducted to assess monetary policy responses indicate that such policies are ineffective and would have no effect for at least 24 months (

Andryushin 2020).

Existing research on monetary policy primarily focuses on assessing its effectiveness by examining its impact on stock markets in various regions, including North America, Africa, Asia, and Europe. Therefore, there is a potential research gap in conducting a comparative analysis of the effectiveness of unconventional monetary policy measures across various regions or countries in mitigating the economic impact of pandemics, as well as examining the broader implications of different monetary policy strategies on key macroeconomic variables such as GDP growth, inflation rates, and unemployment rates during such crises. Moreover, none of these studies have addressed the influence of COVID-19-induced interest rate uncertainty on the transmission of monetary policy in OECD countries. (

Phan and Narayan 2020). Consequently, this study aims to bridge this gap by scrutinizing the impact of monetary policy measures undertaken by OECD countries on the macroeconomy during both the COVID-19 era and the subsequent post-COVID period. The insights garnered from this investigation are intended to serve as a guiding framework for effectively addressing future pandemics or economic shocks of a similar nature.

4. Data and Methodology

4.1. Data Collection

This empirical analysis relies on an extensive database at the country level that combines information on monetary policy measures and macroeconomic variables, as discussed in

Table 1. In particular, GDP growth rate serves as a proxy for economic growth, while the consumer price index is used as a proxy for inflation rate. In both equations, real GDP growth is computed by calculating the monthly year-on-year percentage growth rates. The inflation rate variable is derived from the year-on-year percentage change in the consumer price index (CPI). Data were extracted from various sources, including the International Monetary Fund’s (IMF) macroeconomic and financial data, the Organisation for Economic Co-operation and Development (OECD), and the WHO’s Coronavirus data.

4.2. Sample Selection

The Organisation for Economic Co-operation and Development, abbreviated as OECD, is an international organization of 38 countries committed to democracy and the market economy. We included all 33 countries based on the availability of data. The study included Australia, Austria, Belgium, Canada, the Czech Republic, Denmark, Finland, France, Greece, Hungary, Iceland, Ireland, Italy, Korea, Mexico, the Netherlands, New Zealand, Norway, Poland, Portugal, the Slovak Republic, Spain, Switzerland, Türkiye, the United Kingdom, United States, Argentina, Brazil, Chile, Indonesia, Israel, Slovenia and South Africa. These countries represent a diverse range of economic structures, levels of development, and policy frameworks, making them a valuable sample for analyzing macroeconomic trends and policy responses. By including data from a broad range of OECD countries, the study aims to capture diverse experiences and variations in policy responses to the COVID-19 pandemic across different regions and economic contexts. The study’s timeframe utilizes fortnightly data, derived from the OECD statistics database, spanning from January 2020 to December 2023. Quarterly data was converted to a fortnightly basis using EViews software.

4.3. Methodology

The empirical literature has primarily focused on three key aspects: the impact of interest rates on money markets though monetary policy, and their effects on macroeconomic variables such as GDP growth, inflation and unemployment.

This study employs a balanced panel dataset and a panel ARDL model to analyze the relationship between key macroeconomic policy targets. This model enables the differentiation between short-term and long-term effects. In other words, it makes it possible to examine how variables adjust toward short-term and long-term equilibrium conditions. The ARDL model allows intersection points, short-term coefficients, and error variances to change freely between groups but keeps the long-term coefficients the same. The PMG (Pooled Mean Group) estimator enables us to investigate long-term homogeneity without imposing homogeneity of parameters in the short term (

Pesaran et al. 1999).

The considered time period is sufficient to obtain meaningful results because the ARDL approach is suitable for generating both short-run and long-run elasticities from a small sample size (

Duasa 2007;

Narayan 2004).

As per the theory of the monetary policy transmission mechanism, multiple channels exist to elucidate the impact of monetary policy on real sectors or on overall economic progress (

Prabheesh and Kumar 2021). These channels encompass mechanisms that are perceived to operate via the influence exerted by central bank monetary policy instruments including, but not limited to, the interest rate, credit supply, exchange rate, and expectations (

Chundakkadan and Sasidharan 2020). Therefore, the model examines the impact of conventional monetary policy, demand and supply shocks, inflation, and short-term growth dynamics.

By separately accounting for the GDP growth, inflation and unemployment, the study disentangles these factors from pure supply and demand shocks, respectively. This separation allows for a more precise analysis of their individual effects within the structural theoretical framework.

where

Yit indicates a dependent variable, where it denotes gross domestic product growth, inflation, and the unemployment rate.

β0 is the intercept; t denotes time,

i denotes country and

εt stands for an error term. Likewise, “

r” denotes the interest rate, “

k” stands for uncertainty measured by a volatility index (it is implied volatility as measured by the VIX index can be interpreted as the market’s expectation of risk) and “exe” stands for exchange rate.

To capture monetary shocks by incorporating both the interest rate and inflation rate, the study employs the above model by replacing the dependent variable () with the inflation rate (Equation (2)).

Further, inflation is proxied by the consumer price index, interest rates are proxied by the lending rate and exchange rates denote the value of the country’s currency used for conversion to the US dollar. To comprehensively analyze the actual impact, the fundamental Equation (2) is augmented with two additional variables: cyclical unemployment (unp), denoting the disparity between unemployment and the natural rate, and expected inflation (Inf_Ex) as control variables.

Further, to identify short-term aggregate supply changes, the study uses a third equation by replacing the dependent variable with the cyclical unemployment rate. In order to accurately ascertain the real impact, the equation incorporates GDP growth and the inflation rate as control variables.

Examining the impact of COVID-19 uncertainty on monetary policy effectiveness was captured by the triple interaction term (r*k*COVID_Dum), where COVID_Dum stands for a dummy variable that takes the value of 1 for the COVID-19 pandemic period and 0 for other periods. All variables in the models are expressed in logarithmic form.

Firstly, the study examines cross-sectional dependency (CD) through the use of LM tests, namely those by

Pesaran et al. (

2004) and Breusch-Pagan test. These tests are performed to counteract panel data issues and ensure the robustness and consistency of the estimators (

Pesaran et al. 2004).

In addition, the study performs stationary tests for both dependent and independent variables using unit root tests. Generally, an augmented Dickey–Fuller test is conducted to identify non-stationarity in time series data. The panel unit root test makes it possible to investigate the mean reversion in the panel. It is essential to identify the level of integration among the variables, to pursue time series-based OLS regression and to avoid spurious regression models. Next, optimal lag selections using the unrestricted model and an information criterion were used to decide the choice of lags for each group per variables. Then, the panel cointegration test was used to determine the possibility of establishing a long-run equilibrium relationship between the variables. The deviation of the system from equilibrium at any given point is referred to as the equilibrium error. The Pedroni and Kao tests are based on

Engle and Granger’s (

1987) two-step (residual-based) cointegration tests. The

Engle and Granger (

1987) cointegration test is based on an examination of the residuals, to check whether a spurious regression is performed using I(1) variables. If the variables are cointegrated then the residuals should be I(0). On the other hand, if the variables are not cointegrated then the residuals will be I(1).

Pedroni (

1999,

2004) and

Kao (

1999) extended the Engle-Granger framework to test panel data. This paper employed the Pedroni (Engle–Granger-based) and Kao residual cointegration tests to assess the feasibility of producing a panel ARDL model. Finally, the study uses the Hausman test to indicate the null hypothesis of homogeneity based on the comparison between the mean group (MG), and the pooled mean group (PMG) estimators.

The testing of the ARDL approach consists of two steps. The first step is to check the existence of a long-run cointegration relationship among the variables. If cointegration is established, the second step is to estimate the long- and short-run coefficients. If the cointegration is rejected, the second step converges to the estimation of short-run coefficients only. Then, as ARDL assumes no serial correlation, an appropriate lag length (m) should be considered. The study estimates the ARDL model based on Akaike’s information criterion (AIC).

As a robustness test, this study uses the panel ARDL pooled mean group (PMG) method as it allows constant term, error variance, and short-run parameters to vary among panel countries. However, it assumes that the coefficients of the long-run relationship are constant across countries. The PMG estimator considers both pooling due to the homogeneity constraints on the long-run coefficients and averaging across countries to obtain the means of the estimated values of the error correction coefficients and short-run coefficients of the model.

Due to its incorporation of both pooling and averaging strategies, this model outperforms dynamic ordinary least squares and completely modified least squares methods. Further, this panel regression can be expressed using the ARDL (l and g) technique, according to

Pesaran et al. (

1999), where “l” is the lag of the dependent variable and “g” is the lag of the regressors. This can be expressed mathematically as follows: (

Pesaran et al. 1999, #159)

In the given context, where “i” represents the number of countries and “t” denotes the period, the vector “Yt” consists of dependent variables, including GDP growth rate, inflation rate, and unemployment rate, represented as a (k × 1) vector. Meanwhile, Xi is a matrix of explanatory variables, with an order of (T × k), encompassing variables such as interest rate, uncertainty rate, exchange rate, and an interaction term between interest rate and uncertainty index, and dummy variables. Additionally, the variable represents fixed effects accounting for country specific characteristics, while is an error term, capturing unexplained variations in the model.

5. Results and Discussion

Results

Stationary tests have been conducted, and the results (

Table 2) indicate that certain variables such as GDP growth, rate of uncertainty, gross capital formation, interest rate and inflation rate are stationary at levels. On the other hand, variables such as government expenditure, exchange rate, and unemployment are stationary at first difference, with a significant P-result of 0.0000. This indicates that the ARDL cointegration method is required when modeling with a mix of I(1) and I(0) regressors (the differed order of integration that is some variables are stationary at levels and some are at first difference).

In the cointegration analysis (

Table 3),

Pedroni (

2004), Jhohansen Fisher test and Kao residual panel cointegration tests are conducted for a robustness check. This paper employed the Kao residual cointegration test to assess the feasibility of producing a panel ARDL model. The Kao test specifies cross-section-specific intercepts and homogeneous coefficients for the first-stage regressors. The null and alternative hypotheses about the residual test are as follows, (

Pedroni 2004, #302).

According to the revealed results, the null hypothesis is rejected and the presence of cointegration confirmed, both in cases of deterministic trend and no trend.

Table 3 reveals that the Kao residual panel co-integration results revealed that Kao residual statistics significantly reject the null hypothesis of co-integration.

The Pesaran CD, Breusch–Pagan LM and Pesaran scaled LM test statistics for all three equations are within the upper tail and strongly reject the null hypothesis of no cross-section dependence in residuals.

The impact of cross-sectional dependence on estimates depends on several parameters including the extent of cross-sectional correlations and the nature of cross-sectional dependence. The findings presented in

Table 4 demonstrate that the null hypothesis of “no cross-sectional dependence” is rejected even at a 1 percent level of significance. Therefore, it is necessary for the study to proceed with tests and estimation techniques that can account for cross-sectional dependence. These findings call for the adoption of econometric methods that can produce reliable outcomes in the presence of dependencies. Additionally, the heterogeneity assumption was examined using the test displayed in the table.

Additionally, the observation of the variance inflation factor (VIF) for explanatory variables is crucial in statistical analysis. The VIF results indicate whether multicollinearity is present among the variables in the model. In this case, all three models show low VIF values, less than 5, indicating that multicollinearity is not a concern.

The results regarding the long-term effects of monetary policy measures and macroeconomic variables in OECD countries are presented in

Table 3. It is crucial to select an optimal lag length before employing the ARDL model. Various lag length criteria, such as the Akaike information criterion (AIC), the Hannan–Quinn (HQ) information criterion and Schwarz’s Bayesian criterion (SBC), can be employed to determine the optimal lag length. In this study, a lag length of 3 is chosen for our analysis based on the AIC.

The results of the panel ARDL analysis are shown in

Table 5. The selection of the most appropriate ARDL model was made by the EViews software, based on the Akaike information criterion and a maximum lag length of 3.

Table 5 summarizes the results of the long-run elasticity of GDP growth rate, inflation rate and unemployment rate concerning monetary policy measures and other control variables. The findings of this study suggest a significant negative effect of the interest rate (r) on economic growth and inflation during the pandemic period. These results indicate that a 1 percent increase in interest rates leads to a decrease of 0.08 percent in GDP growth and 0.26 percent in inflation within the economy during the COVID period. Conversely, a 1 percent rise in interest rates corresponds to a 0.22 percent increase in unemployment.

According to the findings of the study, a 1 percent increase in exchange rates reduces the GDP growth rate and inflation rate by 0.0008 percent and 0.0002 percent, respectively, during the COVID period. A higher exchange rate (currency appreciation) makes foreign goods and services cheaper compared with domestically produced goods. This leads to a decrease in exports and domestic production activities (

Ramasamy and Abar 2015). So, the effects of the exchange rate on economic growth and inflation are consistent. On the other hand, the 1 percent increase in exchange rate increases unemployment by 0.00002 percent. A stronger domestic currency makes exports more expensive for foreign buyers, reducing demand for domestic goods and services abroad. This can harm export-dependent industries like manufacturing and tourism, leading to lower revenues. To counter reduced income, some businesses may need to reduce their workforce, resulting in higher unemployment in these sectors.

A one percent increase in economic uncertainty reduces economic growth by 17.29 percent and increases both the inflation rate and unemployment by 1.7 and 3.05 percent, respectively, during the COVID period. During the COVID-19 pandemic, global economic uncertainty increased and that caused disruptions in supply, demand and productivity. These findings are theoretically consistent.

However, starting in 2022, all countries faced various economic shocks, notably the aftermath of the COVID-19 pandemic. As shown in

Table 4, models 2, 4 and 6 show monetary policy measures and their impacts on macroeconomic variables during the post-COVID-19 era. A 1 percent increase in interest rate result in 0.17 percent reduction in GDP growth and 1.1 percent reduction in inflation in the long run.

Consequently, a 1 percent increase in the exchange rate results in 0.002 percent of GDP growth, 0.009 percent inflation rate growth and a 0.0001 percent growth of the unemployment rate over the long term. The impact of economic uncertainty on GDP growth is negative but insignificant; the effects on inflation and unemployment are, respectively, negative and positive and the results were found to be significant and consistent. These outcomes echo the results of previous studies (

Lucian 2006;

Saymeh and Orabi 2013;

Carrera and Vergara 2012).

6. Discussion

The findings of this study reveal a significant negative relationship between declining interest rates and increasing economic growth during the COVID-19 period. Notably, most countries aggressively lowered their interest rates during this time. A decrease in interest rates can have several economic effects. It can reduce the cost of borrowing, thereby encouraging consumer spending, business investment, and housing purchases. Lower interest rates may also discourage foreign capital, resulting in a depreciation of the domestic currency, which, in turn, can boost exports. Consequently, many OECD governments proactively supported their local economies during the crisis by providing assistance to households, businesses, and affected service sectors by reducing their interest rates.

It is important to recognize that the relationship between interest rates and GDP growth is a simplification of the complex and dynamic economic system, especially during the COVID-19 period when all economic sectors were affected due to lockdowns and social restrictions. Despite conventional economic IS-LM theory predicting that a slowdown in economic activity should increase interest rates, an intriguing deviation from this theory occurred, with savings rates continuing to rise. This phenomenon raises questions about the underlying factors driving this behavior. Moreover, despite the presence of conflicting economic forces, such as rising public debt and unprecedented savings, interest rates actually decreased during the pandemic. Local governments in many OECD countries played a pivotal role in providing comprehensive support, including financial aid, non-repayable grants, concessional loans at low or zero interest rates, liquidity loans, and facilitating access to external financing through guarantees. Additionally, they deferred loan installments as part of their support measures (

OECD 2020).

Persistently low interest rates during the pandemic can raise concerns about potential inflation, as central banks may worry about overheating the economy. To counteract this, they may consider tightening monetary policy in the future, raising interest rates to control inflation. The concept of a negative relationship between interest rates and inflation is grounded in economic theory. When interest rates are lowered, borrowing becomes more affordable, and consumer and business spending may increase. This higher demand can put upward pressure on prices, potentially leading to an increase in the inflation rate.

Despite initially high values, interest rates experienced a gradual decrease by the end of 2020. An unintended consequence of this policy was an increase in unemployment rates. However, the slowdown in economic activity and reduced production output prompted companies to curtail their hiring efforts, affecting unemployment rates during the pandemic.

Furthermore, a country’s monetary policy is closely related to its exchange rate policy. In a trade economy that engages with other countries, monetary policy can affect real output through the exchange rate channel, especially when nominal wages and prices remain relatively stable (

Krylova 2002). A higher exchange rate can also reduce inflation, as cheaper imports become available in domestic currencies. This could lead to currency appreciation, making imports more affordable while reducing the competitiveness of exports, resulting in a drop in domestic demand. As a result, local companies may reduce costs and cut jobs, causing unemployment to rise. These findings align with those of

Purfield and Rosenberg (

2010) during the global financial crisis of 2008–2009.

High levels of economic uncertainty can lead to decreased business and consumer confidence, which may result in reduced investments in capital, technology, and innovation. This, in turn, can slow down economic growth (

Bahmani-Oskooee and Mohammadian 2021). On the other hand, when people are uncertain about their economic future, especially in a pandemic period, they may save more and spend less or delay non-essential consumption, which can reduce overall economic activity. This situation aligns with the findings of the

Hepburn et al. (

2020).

On the other hand, a noteworthy development in the post-COVID-19 era is the increase in interest rates, coupled with a high inflationary environment in OECD countries. These findings suggest that the impact of elevated interest rates on financial markets and economic activity may be more significant than initially anticipated. This strategic policy shift aims to stimulate economic growth and counter the economic slowdown in the post-COVID-19 era. As the economy recovers and inflationary pressures mount, some central banks may contemplate a gradual increase in interest rates, aligning with the broader process of policy normalization (

Binici et al. 2022). An essential factor shaping interest rate policy in the post-pandemic era is the level of inflation. Should inflation persist at high levels, central banks may find it necessary to raise interest rates to control it, even as the economy rebounds.

Additionally, there is a positive relationship between exchange rates and GDP growth rate, indicating that a weaker currency can enhance a country’s competitiveness in foreign markets, potentially boosting export-related industries and overall economic growth (

Attah-Obeng et al. 2013). Moreover, exchange rates have the potential to impact a country’s trade balance, with a depreciating currency potentially improving the trade balance, thereby contributing positively to economic growth (

Razzaque et al. 2017). Nevertheless, it is crucial to acknowledge the volatility in exchange rate movements, making it challenging to predict their precise influence on economic growth during the post-COVID-19 era. Governments and central banks must diligently oversee and manage exchange rate dynamics to ensure they bolster, rather than hinder, their economic recovery endeavors.

Exchange rates play a significant role in determining the prices of imported goods and services. A depreciating domestic currency raises the cost of imports. Furthermore, exchange rate fluctuations can influence inflation expectations among consumers and businesses (

Auboin and Ruta 2013). If individuals anticipate a significant future depreciation of their currency, they may engage in behavior that accelerates inflation, such as hoarding goods. Additionally, inflation dynamics are influenced by various other domestic and global factors. Therefore, central banks and policymakers must carefully consider the interplay between exchange rates and inflation when making monetary policy decisions during the post-COVID-19 era.

Conversely, an appreciating domestic currency can erode the competitiveness of exports, potentially reducing the demand for domestically produced goods and services in global markets, with potential negative repercussions for employment in export-oriented sectors. Moreover, an appreciating domestic currency can make imports more affordable, potentially intensifying competition for domestically produced goods. This can affect industries facing substantial competition from foreign imports, potentially leading to job losses.

Furthermore, economic uncertainty can result in cautious investment decisions by businesses and reduced consumer spending (

Hepburn et al. 2020). Uncertainty regarding the future can lead to businesses postponing capital expenditures and hiring, potentially decelerating economic growth. In the post-COVID-19 era, government policies aimed at reducing economic uncertainty and supporting recovery can significantly impact GDP growth. For instance, fiscal stimulus packages and supportive monetary policies can mitigate the adverse effects of uncertainty and stimulate economic activity. Central banks often respond to inflationary pressures by tightening monetary policy. Nevertheless, in the post-COVID-19 era, central banks may carefully balance the need to control inflation with the objective of supporting economic recovery, potentially adopting a more patient approach to interest rate increases to avoid stifling growth. Elevated economic uncertainty can prompt businesses to exercise caution when hiring new employees and, in some cases, initiate layoffs, contributing to higher unemployment rates.

There is a negative relationship between inflation rates and unemployment rates during and post COVID-19 period. The relationship between inflation and unemployment is often described by the Phillips curve, which suggests an inverse relationship between the two: as inflation increases, unemployment decreases, and vice versa. This relationship is known as the short-run Phillips curve. Especially during a pandemic, when demand is depressed, the long-term Phillips curve relationship is not so straightforward (

Lawler and Pavlenko 2020). Policymakers need to consider a range of factors, including the nature and duration of the crisis, the effectiveness of policy responses, and long-term expectations, when addressing unemployment and inflation during a pandemic.

7. Conclusions

Given the profound uncertainty brought about by the COVID-19 pandemic, this study closely examines the influence of monetary policy measures on GDP growth, inflation, and unemployment within 33 OECD countries that were significantly affected by the pandemic during the COVID-19 period and the subsequent post-pandemic era spanning from 2020 to 2023 using the panel ARDL approach. The study’s findings suggest that during the COVID-19 pandemic period, monetary policy measures exhibited a low level of interest rates, as the majority of the OECD economies reduced the cash rate and interest rates on exchange settlement balances. This was primarily due to the fiscal policy of most OECD countries, which provided substantial support to their economies, creating a shift that posed a challenge for countries with low budget deficits and minimal public debt.

In contrast, the post-COVID-19 era witnessed the implementation of high interest rates by countries, aimed at fostering economic growth and concurrently curbing unemployment. Introducing relaxed monetary policy measures carries some risks, such as public investment becoming an adjustment variable. Higher interest rates reduced the availability of credit, subsequently reducing consumer spending and thereby a reduction of economic growth.

These findings underscore the importance of swiftly transitioning patterns of monetary policy measures in response to economic shocks like pandemics. However, governments must manage inflationary pressures, a notable drawback of expansionary monetary policy. In the meantime, governments should announce significant recovery plans focusing on public investments, such as strengthening healthcare systems during a pandemic and accelerating the production process immediately after immunization against the virus. Therefore, monetary policies must remain adaptive and responsive to evolving economic conditions. Central banks should maintain a balance between controlling inflation and supporting economic activity through interest rate adjustments and quantitative easing.

On the other hand, occupations in the industrial and services sector must be adaptable to remote working based on the nature of the work. The adaptability of occupations to remote working depends significantly on the industry’s technological readiness and the nature of the job tasks. Employers may need to invest in training and technology to facilitate this transition, ensuring that employees have the tools and skills necessary to work effectively from remote locations.

Recognizing that the COVID-19 pandemic may not be the last epidemic and anticipating future economic shocks, this study offers potential policy insights that can be applied in similar circumstances moving forward. Well-calibrated policy measures are required to mitigate the impact of the recent sequence of negative shocks to the global economy, restore economic stability, and strengthen prospects for strong, inclusive, and sustainable improvements in living standards. The successful implementation of these policy implications requires a coordinated effort between governments, healthcare providers, the private sector, and communities. By addressing both the health and economic aspects of the COVID-19 pandemic, these policies can help mitigate the impacts of the virus, promote recovery, and build more resilient and equitable societies for the future. Simultaneously, it is essential to launch comprehensive public health campaigns to educate the population about the benefits of vaccination and dispel myths and misinformation; utilize multiple platforms, including social media, traditional media, and community outreach; and enhance the efficiency of vaccine distribution systems by investing in infrastructure improvements, such as cold chain logistics, storage facilities, and transportation networks.

This study encounters several limitations primarily stemming from time constraints. Given that the study’s scope is confined to a relatively short period, the long-term ramifications may differ. Furthermore, the study could not incorporate changes in energy prices in the fundamental models due to data limitations. Therefore, future research endeavors would be valuable, particularly through single-country analyses. Additionally, it would be beneficial to study how households and businesses in OECD countries responded to changes in interest rates, liquidity provisions, and other monetary measures during the COVID-19 pandemic. Analyzing the impact of these monetary policies on financial markets, including stock markets, bond markets, and housing markets in OECD countries, is also crucial.

{kind=link}