Determinants of Household-Level Coping Strategies and Recoveries from Riverine Flood Disasters: Empirical Evidence from the Right Bank of Teesta River, Bangladesh

Abstract

1. Introduction

2. Materials and Methods

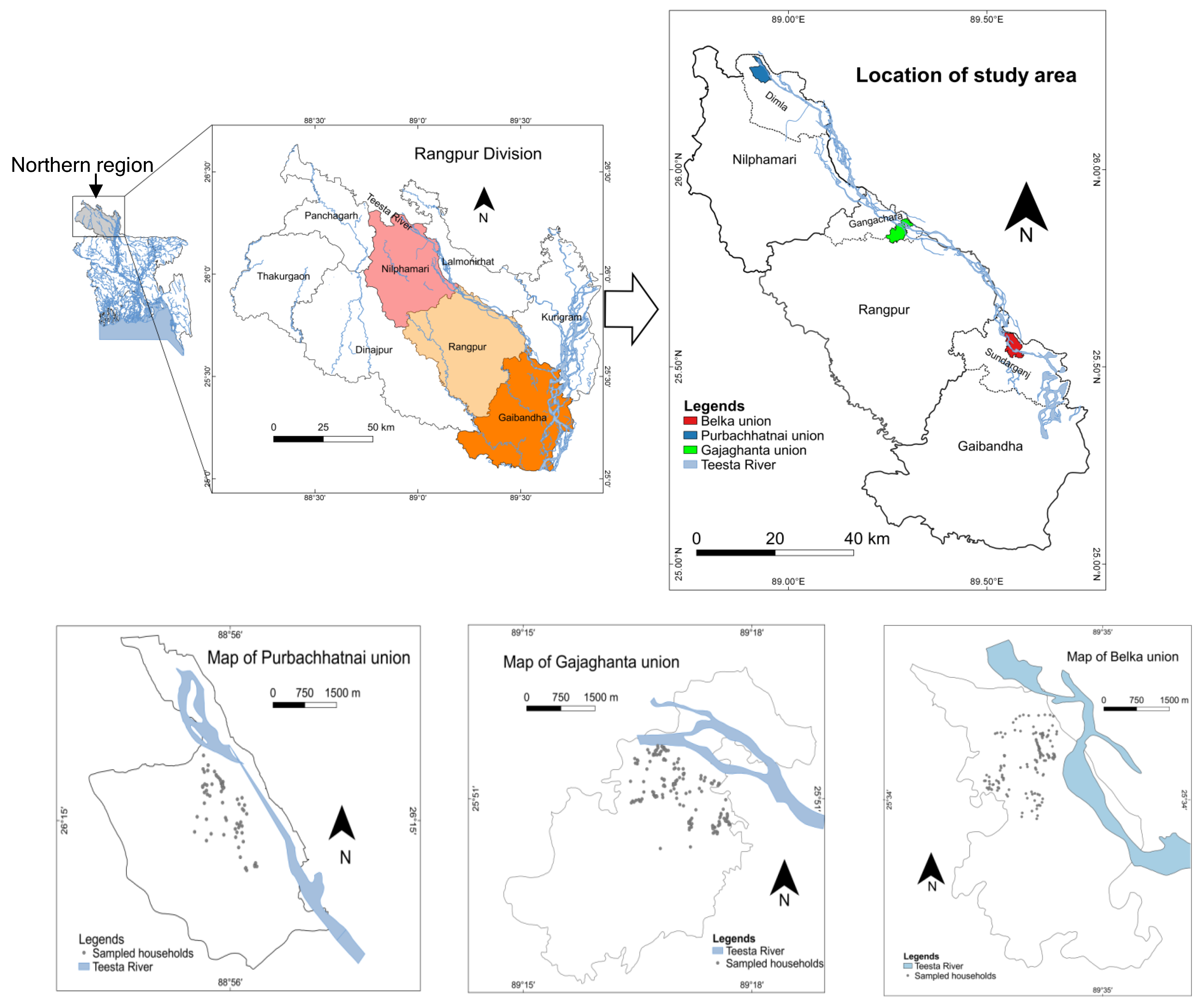

2.1. Study Area

2.2. Sampling and Data Collection

3. Variables Selection and Statistical Analysis

3.1. Dependent Variables

- ▪

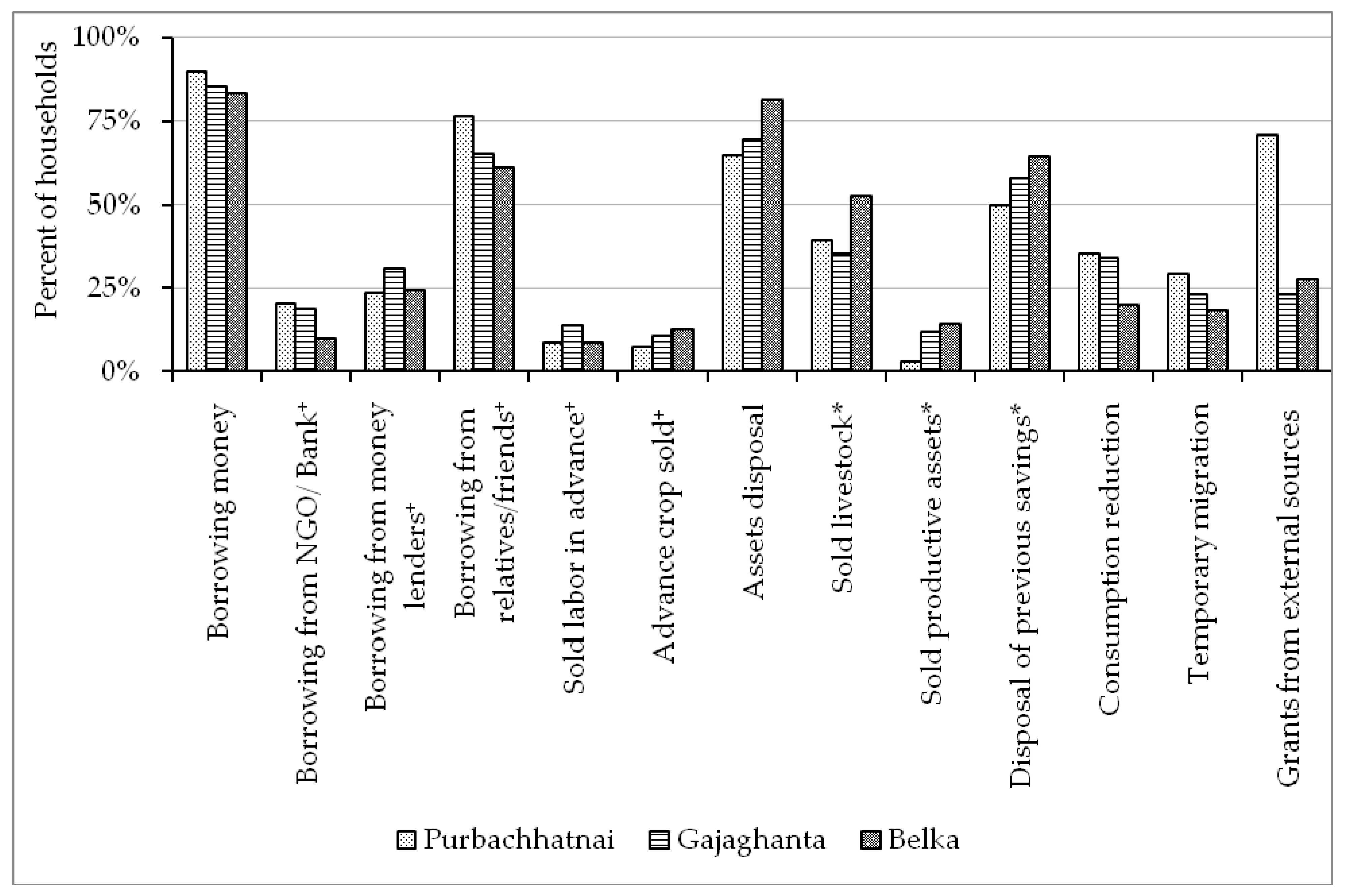

- Borrowing money: The term borrowing includes all kinds of strategies that a household employed to take loans from others. The formal sources include banks and non-governmental organizations (NGOs), whereas informal sources include local money lenders, friends, relatives, or neighbors. In extreme situations, some people borrow money by selling labor or field crops with an advance payment. Households that employed one or a combination of these strategies were grouped in this category.

- ▪

- Assets disposal: Disposable items include financial and physical assets. The physical disposable assets are comprised of livestock (poultry, cattle, goats), household utensils, jewelry, trees, crops, land. On the other hand, financial assets include household savings (deposits). If a household sold any physical assets or used up its savings in response to flood, it was classified in this category.

- ▪

- ▪ Consumption reduction: Food scarcity is common in disaster-affected areas. Households adopt numerous strategies to cope with shocks, including consumption smoothing, resorting to cheap foods, wild foods collection [16]. In this study, consumption reduction implies a household reducing their consumption in response to a flood disaster, in the form of meal skipping or starvation.

- ▪

- Temporary migration: Migration to cities or other flood-free areas is a common measure to compensate losses incurred from flood. If a family member from a household migrated outside of the flood prone area (study area) for income and then returned to their houses within six months, the household was labeled in this category.

- ▪

- Grants from external sources: Grants from external sources are vital for short-term survival. It helps flood disaster victims to compensate their losses [21]. Grants are distributed among flood victims by the local/national government, NGOs, local elites, or a host of other organizations. In this study, if a household received grants from external sources (e.g., government, NGOs, or local elites), it was classified in this category.

3.2. Explanatory Variables

3.3. Recovery from Flood Disasters

3.4. Data Analysis

4. Results and Discussion

4.1. Households’ Characteristics

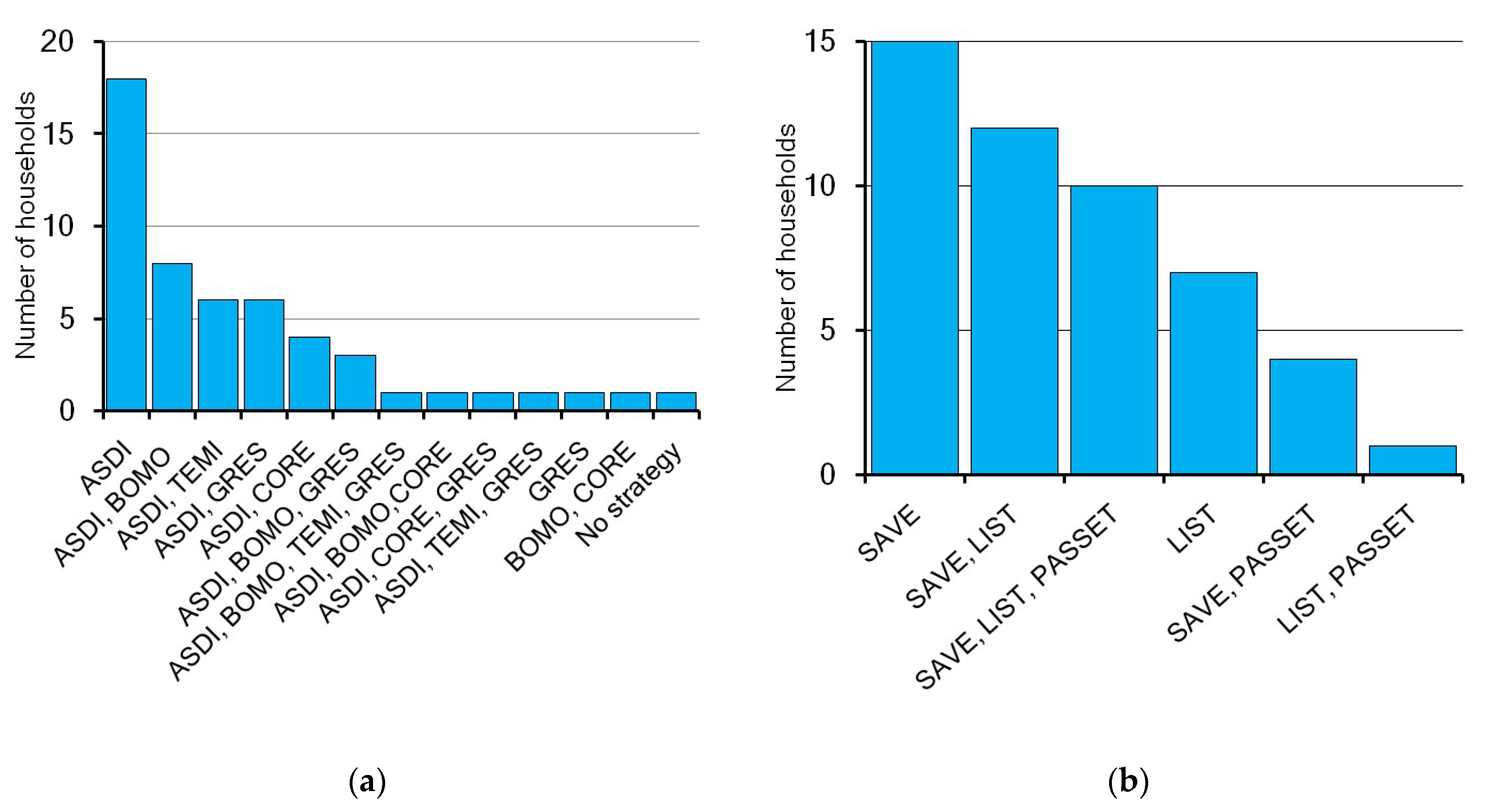

4.2. Household-Level Coping Strategies

4.3. Determinants of Coping Strategies

- ▪

- The Hazard Component

- ▪

- The Exposure Component

- ▪

- The Vulnerability Component

- ▪

- The Capacity Component

4.4. Association between Coping Strategies and Post-Disaster Recovery

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Groups | Measures |

|---|---|

| Borrowing money | Borrowed money from NGOs |

| Borrowed money from local money lenders | |

| Borrowed money from relatives | |

| Borrowed money from friends | |

| Borrowed money from banks | |

| Borrowed money by selling labor in advance | |

| Borrowed money by selling crops in advance | |

| Assets disposal | Sold poultry (livestock) |

| Sold cattle (livestock) | |

| Sold goats (livestock) | |

| Sold household’sgoods (household assets) | |

| Sold/leased out jewelry (household assets) | |

| Sold/leased out lands (household assets) | |

| Sold crops (household assets) | |

| Sold trees (household assets) | |

| Spent previous savings | |

| Consumption reduction | Starvation/meal skipping during flood |

| Temporary migration | Temporary migration for work |

| Grants from external sources | Received emergency support from NGOs |

| Received emergency support from government | |

| Received emergency support from local elites |

| Explanatory Variables | Dependent Variable: Borrowing Money | Dependent Variable: Assets Disposal | Dependent Variable: Consumption Reduction | Dependent Variable: Temporary Migration | Dependent Variable: Grants from External Sources | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| B a | Exp(B) b | B a | Exp(B) b | B a | Exp(B) b | B a | Exp(B) b | B a | Exp(B) b | |

| Floodwater depth | −0.97 (0.70) | 0.38 [0.10, 1.48] | −0.94 (0.55) | 0.39 [0.13, 1.15] | 2.25 *** (0.58) | 9.46 [3.05, 29.36] | −0.26 (0.57) | 0.77 [0.25, 2.35] | −0.48 (0.52) | 0.62 [0.23, 1.71] |

| Location of house | 1.09 *** (0.39) | 2.98 [1.40, 6.36] | −0.86 * (0.43) | 0.42 [0.18, 0.97] | 0.35 (0.41) | 1.42 [0.64, 3.17] | 0.0 6(0.37) | 1.06 [0.51, 2.21] | 0.85 * (0.39) | 2.34 [1.08, 5.07] |

| Affected by disease | 0.99 * (0.43) | 2.68 [1.16, 6.18] | −0.80 (0.46) | 0.45 [0.18, 1.11] | 0.77 (0.46) | 2.15 [0.87, 5.32] | 1.28 * (0.52) | 3.59 [1.31, 9.87] | 0.53 (0.38) | 1.71 [0.82, 3.56] |

| Age | −0.03 * (0.01) | 0.97 [0.95, 1.00] | 0.00 (0.01) | 1.00 [0.98, 1.02] | −0.01 (0.01) | 0.99 [0.97, 1.01] | −0.02 * (0.01) | 0.98 [0.96, 1.00] | 0.01 (0.01) | 1.01 [0.99, 1.02] |

| Female | −1.62 ** (0.59) | 0.20 [0.06, 0.64] | −0.24 (0.52) | 0.79 [0.28, 2.19] | 0.08 (0.55) | 1.08 [0.37, 3.20] | −0.37 (0.70) | 0.69 [0.18, 2.75] | −0.16 (0.57) | 0.85 [0.28, 2.57] |

| Agricultural landless | 0.12 (0.34) | 1.13 [0.58, 2.22] | −1.12 *** (0.28) | 0.33 [0.19, 0.56] | 1.00 *** (0.29) | 2.71 [1.55, 4.75] | 0.95 *** (0.28) | 2.58 [1.49, 4.47] | −0.08 (0.25) | 0.93 [0.56, 1.53] |

| Crop save | −0.22 (0.37) | 0.80 [0.39, 1.66] | 0.48 (0.33) | 1.62 [0.84, 3.11] | −1.76 *** (0.42) | 0.17 [0.08, 0.39] | 0.84 *** (0.29) | 2.31 [1.31, 4.09] | −0.21 (0.28) | 0.81 [0.46, 1.41] |

| Mobile phone | 0.89 * (0.43) | 2.44 [1.06, 5.63] | 0.28 (0.34) | 1.32 [0.67, 2.59] | −0.02 (0.36) | 0.98 [0.49, 1.97] | 1.07 * (0.49) | 2.92 [1.11, 7.63] | −0.22 (0.36) | 0.80 [0.40, 1.62] |

| Mitigation measures | 0.08 (0.41) | 1.08 [0.49, 2.40] | 0.28 (0.31) | 1.33 [0.73, 2.42] | −0.80 ** (0.31) | 0.45 [0.25, 0.83] | 0.92 * (0.41) | 2.50 [1.13, 5.55] | 0.46 (0.32) | 1.58 [0.84, 2.97] |

| Nonfarm income | −1.06 *** (0.34) | 0.35 [0.18, 0.67] | 0.77 ** (0.31) | 2.16 [1.19, 3.94] | −0.47 (0.31) | 0.63 [0.34, 1.15] | −0.09 (0.29) | 0.91 [0.52, 1.61] | −0.20 (0.27) | 0.82 [0.49, 1.39] |

| Gajaghanta | −0.36 (0.57) | 0.70 [0.23, 2.12] | 0.34 (0.37) | 1.41 [0.68, 2.92] | −0.53 (0.40) | 0.59 [0.27, 1.28] | −0.34 (0.38) | 0.71 [0.34, 1.51] | −1.86 *** (0.36) | 0.16 [0.08, 0.31] |

| Belka | −1.05 (0.57) | 0.35 [0.12, 1.07] | 1.18 *** (0.40) | 3.25 [1.49, 7.08] | −1.53 *** (0.43) | 0.22 [0.09, 0.50] | −0.77 (0.40) | 0.47 [0.21, 1.01] | −1.67 *** (0.36) | 0.19 [0.09, 0.38] |

| Constant | 2.31 * (1.10) | 10.07 | 2.20 * (0.93) | 9.03 | −1.26 (0.93) | 0.28 | −3.28 *** (1.06) | 0.04 | −0.55 (0.88) | 0.58 |

| Log Likelihood | 266.31 | 317.096 | 345.51 | 354.186 | 421.07 | |||||

| Wald Chi Square | 46.981 | 65.077 | 105.767 | 48.252 | 60.689 | |||||

| Cox & Snell R Square | 0.117 | 0.159 | 0.245 | 0.120 | 0.149 | |||||

| Nagelkerke R Square | 0.208 | 0.231 | 0.350 | 0.183 | 0.206 | |||||

| a | b | c | d | e | f | g | h | i | j | k | l | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| a. Floodwater depth | 1 | −0.036 | 0.196 ** | −0.001 | 0.088 | 0.1 | −0.059 | −0.210 ** | −0.154 ** | −0.137 ** | 0.158 ** | 0.058 |

| b. Location of house | 1 | −0.067 | −0.036 | 0.068 | 0 | −0.071 | 0.005 | −0.031 | 0.022 | −0.115 * | −0.027 | |

| c. Affected by disease | 1 | 0.07 | 0.028 | 0.039 | 0.006 | −0.085 | 0.006 | −0.102 * | 0.003 | −0.043 | ||

| d. Age | 1 | 0.036 | −0.074 | 0.038 | −0.081 | 0.005 | 0.111 * | 0.136 ** | −0.164 ** | |||

| e. Female | 1 | 0.150 ** | −0.118 * | −0.230 ** | −0.088 | 0.058 | −0.033 | −0.121 * | ||||

| f. Agricultural landless | 1 | −0.170 ** | −0.229 ** | −0.189 ** | 0.013 | 0.062 | −0.031 | |||||

| g. Crop save | 1 | 0.174 ** | 0.157 ** | 0.138 ** | 0.015 | −0.035 | ||||||

| h. Mobile phone | 1 | 0.139 ** | 0.048 | −0.002 | 0.058 | |||||||

| i. Mitigation measures | 1 | 0.104 * | −0.056 | 0.033 | ||||||||

| j. Nonfarm income | 1 | 0.093 | −0.166 ** | |||||||||

| k. Gajaghanta | 1 | −0.694 ** | ||||||||||

| l. Belka | 1 |

References

- Gotham, K.F.; Campanella, R.; Lauve-Moon, K.; Powers, B. Hazard experience, geophysical vulnerability, and flood risk perceptions in a postdisaster city, the case of New Orleans. Risk Anal. 2018, 38, 345–356. [Google Scholar] [CrossRef] [PubMed]

- CRED; UNISDR. The Human Cost of Weather-Related Disasters 1995–2015; Centre for Research on the Epidemiology of Disasters (CRED): Brussels, Belgium; United Nations Office for Disaster Risk Reduction (UNISDR): Geneva, Switzerland, 2015. [Google Scholar]

- Centre for Research on the Epidemiology of Disasters. The Interantional Disaster Database (EM-DAT). Available online: http://emdat.be (accessed on 14 January 2020).

- Patnaik, U.; Narayanan, K. Are traditional coping mechanisms effective in managing the risk against extreme events? Evidences from flood-prone region in rural India. Water Policy 2015, 17, 724–741. [Google Scholar] [CrossRef]

- Mondal, M.S.H. The implications of population growth and climate change on sustainable development in Bangladesh. Jàmbá J. Disaster Risk Stud. 2019, 11, 1–10. [Google Scholar] [CrossRef] [PubMed]

- NDRCC. Daily Disaster Situation: 12 September 2017; The National Disaster Response Coordination Centre (NDRCC), Department of Disaster Management: Dhaka, Bangladesh, 2017. [Google Scholar]

- Philip, S.; Sparrow, S.; Kew, S.; Van Der Weil, K.; Wanders, N.; Singh, R.; Hassan, A.; Mohammed, K.; Javid, H.; Haustein, K.; et al. Attributing the 2017 Bangladesh floods from meteorological and hydrological perspectives. Hydrol. Earth Syst. Sci. 2019, 23, 1409–1429. [Google Scholar] [CrossRef]

- Gros, C.; Bailey, M.; Schwager, S.; Hassan, A.; Zingg, R.; Uddin, M.M.; Shahjahan, M.; Islam, H.; Lux, S.; Jaime, C.; et al. Household-level effects of providing forecast-based cash in anticipation of extreme weather events: Quasi-experimental evidence from humanitarian interventions in the 2017 floods in Bangladesh. Int. J. Disaster Risk Reduct. 2019, 41, 101275. [Google Scholar] [CrossRef]

- Smith, L.C.; Frankenberger, T.R. Does Resilience Capacity Reduce the Negative Impact of Shocks on Household Food Security? Evidence from the 2014 Floods in Northern Bangladesh. World Dev. 2018, 102, 358–376. [Google Scholar] [CrossRef]

- Kamal, A.S.M.M.; Shamsudduha, M.; Ahmed, B.; Hassan, S.M.K.; Islam, M.S.; Kelman, I.; Fordham, M. Resilience to flash floods in wetland communities of northeastern Bangladesh. Int. J. Disaster Risk Reduct. 2018, 31, 478–488. [Google Scholar] [CrossRef]

- Mondal, M.S.H.; Murayama, T.; Nishikizawa, S. Assessing the flood risk of riverine households: A case study from the right bank of the Teesta River, Bangladesh. Int. J. Disaster Risk Reduct. 2020, 51, 101758. [Google Scholar] [CrossRef]

- Sultana, P.; Thompson, P.M.; Wesselink, A. Coping and resilience in riverine Bangladesh. Environ. Hazards 2019, 19, 70–89. [Google Scholar] [CrossRef]

- Siegel, P.B.; Alwang, J. An Asset-Based Approach to Social Risk Management: A Conceptual Framework; The World Bank: Washington, DC, USA, 1999. [Google Scholar]

- Del Ninno, C.; Dorosh, P.A.; Smith, L.C. Public policy, markets and household coping strategies in Bangladesh: Avoiding a food security crisis following the 1998 floods. World Dev. 2003, 31, 1221–1238. [Google Scholar] [CrossRef]

- Paul, S.K.; Routray, J.K. Flood proneness and coping strategies: The experiences of two villages in Bangladesh. Disasters 2010, 34, 489–508. [Google Scholar] [CrossRef] [PubMed]

- Paul, S.K.; Routray, J.K. Household response to cyclone and induced surge in coastal Bangladesh: Coping strategies and explanatory variables. Nat. Hazards 2011, 57, 477–499. [Google Scholar] [CrossRef]

- Sultana, N.; Rayhan, M.I. Coping strategies with floods in Bangladesh: An empirical study. Nat. Hazards 2012, 64, 1209–1218. [Google Scholar] [CrossRef]

- Adams, A.M.; Cekan, J.; Sauerborn, R. Towards a conceptual framework of household coping: Reflections from rural West Africa. Africa 1998, 68, 263–283. [Google Scholar] [CrossRef]

- Frankenberger, T.R. Indicators and data collection methods for assessing household food security. In Household Food Security: Concepts, Indicators, Measurements: A Technical Review; Maxwell, S., Frankenberger, T.R., Eds.; UNICEF: New York, NY, USA; IFAD: Rome, Italy, 1992. [Google Scholar]

- Shoji, M. How do the poor cope with hardships when mutual assistance is unavailable? Econ. Bull. 2008, 15, 1–17. [Google Scholar]

- Mavhura, E.; Manyena, S.B.; Collins, A.E.; Manatsa, D. Indigenous knowledge, coping strategies and resilience to floods in Muzarabani, Zimbabwe. Int. J. Disaster Risk Reduct. 2013, 5, 38–48. [Google Scholar] [CrossRef]

- Balgah, R.A.; Bang, H.N.; Fondo, S.A. Drivers for coping with flood hazards: Beyond the analysis of single cases. Jàmbá J. Disaster Risk Stud. 2019, 11, 1–9. [Google Scholar] [CrossRef]

- Rayamajhee, V.; Bohara, A.K. Natural Disaster Damages and Their Link to Coping Strategy Choices: Field Survey Findings from Post-Earthquake Nepal. J. Int. Dev. 2019, 31, 336–343. [Google Scholar] [CrossRef]

- Rashid, D.A.; Langworthy, M.; Aradhyula, S. Livelihood Shocks and Coping Strategies An Empirical Study of Bangladesh Households. In Proceedings of the American Agricultural Economics Association Annual Meeting, Long Beach, CA, USA, 23–26 July 2006. [Google Scholar]

- Brouwer, R.; Akter, S.; Brander, L.; Haque, E. Socioeconomic vulnerability and adaptation to environmental risk: A case study of climate change and flooding in Bangladesh. Risk Anal. Int. J. 2007, 27, 313–326. [Google Scholar] [CrossRef]

- Mondal, S.H.; Islam, S. Chronological trends in maximum and minimum water flows of the Teesta River, Bangladesh, and its implications. Jàmbá J. Disaster Risk Stud. 2017, 9, 1–11. [Google Scholar] [CrossRef]

- Ferdous, M.R.; Wesselink, A.; Brandimarte, L.; Slager, K.; Zwarteveen, M.; Di Baldassarre, G. The Costs of Living with Floods in the Jamuna Floodplain in Bangladesh. Water 2019, 11, 1238. [Google Scholar] [CrossRef]

- Ferdous, J.; Mallick, D. Norms, practices, and gendered vulnerabilities in the lower Teesta basin, Bangladesh. Environ. Dev. 2019, 31, 88–96. [Google Scholar] [CrossRef]

- Hutton, D.; Haque, C.E. Human Vulnerability, Dislocation and Resettlement: Adaptation Processes of River-bank Erosion-induced Displacees in Bangladesh. Disasters 2004, 28, 41–62. [Google Scholar] [PubMed]

- Jabeen, H.; Johnson, C.; Allen, A. Built-in resilience: Learning from grassroots coping strategies for climate variability. Environ. Urban. 2010, 22, 415–431. [Google Scholar] [CrossRef]

- Haque, A.N.; Dodman, D.; Hossain, M.M. Individual, communal and institutional responses to climate change by low-income households in Khulna, Bangladesh. Environ. Urban. 2014, 26, 112–129. [Google Scholar] [CrossRef]

- Mozumder, P.; Bohara, A.K.; Berrens, R.P.; Halim, N. Private transfers to cope with a natural disaster: Evidence from Bangladesh. Environ. Dev. Econ. 2009, 14, 187–210. [Google Scholar] [CrossRef]

- Alam, G.M.M.; Alam, K.; Mushtaq, S. Climate change perceptions and local adaptation strategies of hazard-prone rural households in Bangladesh. Clim. Risk Manag. 2017, 17, 52–63. [Google Scholar] [CrossRef]

- Sarker, M.N.I.; Wu, M.; Alam, G.M.M.; Shouse, R.C. Life in riverine islands in Bangladesh: Local adaptation strategies of climate vulnerable riverine island dwellers for livelihood resilience. Land Use Policy 2020, 94, 104574. [Google Scholar] [CrossRef]

- Alam, G.M.M.; Alam, K.; Mushtaq, S.; Sarker, M.N.I.; Hossain, M. Hazards, food insecurity and human displacement in rural riverine Bangladesh: Implications for policy. Int. J. Disaster Risk Reduct. 2020, 43, 101364. [Google Scholar] [CrossRef]

- Islam, M.R. Climate Change, Natural Disasters and Socioeconomic Livelihood Vulnerabilities: Migration Decision Among the Char Land People in Bangladesh. Soc. Indic. Res. 2018, 136, 575–593. [Google Scholar] [CrossRef]

- Alam, G.M.M.; Alam, K.; Mushtaq, S.; Clarke, M.L. Vulnerability to climatic change in riparian char and river-bank households in Bangladesh: Implication for policy, livelihoods and social development. Ecol. Indic. 2017, 72, 23–32. [Google Scholar] [CrossRef]

- Sarker, M.N.I.; Wu, M.; Alam, G.M.M.; Shouse, R.C. Livelihood Vulnerability of Riverine-Island Dwellers in the Face of Natural Disasters in Bangladesh. Sustainability 2019, 11, 1623. [Google Scholar] [CrossRef]

- Alam, G.M.M. Livelihood Cycle and Vulnerability of Rural Households to Climate Change and Hazards in Bangladesh. Environ. Manag. 2017, 59, 777–791. [Google Scholar] [CrossRef] [PubMed]

- Sarker, M.N.I.; Wu, M.; Alam, G.M.M.; Shouse, R.C. Livelihood diversification in rural Bangladesh: Patterns and determinants in disaster prone riverine islands. Land Use Policy 2020, 96, 104720. [Google Scholar] [CrossRef]

- Sarker, M.N.I.; Wu, M.; Alam, G.M.M.; Shouse, R.C. Livelihood resilience of riverine island dwellers in the face of natural disasters: Empirical evidence from Bangladesh. Land Use Policy 2020, 95, 104599. [Google Scholar] [CrossRef]

- Alam, G.M.M.; Alam, K.; Mushtaq, S.; Filho, W.L. How do climate change and associated hazards impact on the resilience of riparian rural communities in Bangladesh? Policy implications for livelihood development. Environ. Sci. Policy 2018, 84, 7–18. [Google Scholar] [CrossRef]

- Poussin, J.K.; Botzen, W.J.W.; Aerts, J.C.J.H. Factors of influence on flood damage mitigation behaviour by households. Environ. Sci. Policy 2014, 40, 69–77. [Google Scholar] [CrossRef]

- Abramson, D.M.; Stehling-Ariza, T.; Park, Y.S.; Walsh, L.; Culp, D. Measuring individual disaster recovery: A socioecological framework. Disaster Med. Public Health Prep. 2010, 4, S46–S54. [Google Scholar] [CrossRef]

- Chacowry, A.; McEwen, L.J.; Lynch, K. Recovery and resilience of communities in flood risk zones in a small island developing state: A case study from a suburban settlement of Port Louis, Mauritius. Int. J. Disaster Risk Reduct. 2018, 28, 826–838. [Google Scholar] [CrossRef]

- Akbar, M.S.; Aldrich, D.P. Social capital’s role in recovery: Evidence from communities affected by the 2010 Pakistan floods. Disasters 2018, 42, 475–497. [Google Scholar] [CrossRef]

- Tran, V.Q. Household’s coping strategies and recoveries from shocks in Vietnam. Q. Rev. Econ. Financ. 2015, 56, 15–29. [Google Scholar] [CrossRef]

- Francisco, J.P. Determinants of property damage recovery time amongst households affected by an extreme flood event in Metro Manila, Philippines. Jàmbá J. Disaster Risk Stud. 2014, 6, 1–10. [Google Scholar] [CrossRef][Green Version]

- BBS. Population & Housing Census—2011: Community Report: Gaibandha/Nilphamari/Rangpur; Bangladesh Bureau of Statistics: Dhaka, Bangladesh, 2013. [Google Scholar]

- Davies, S. Are coping strategies a cop out? IDS Bull. 1993, 24, 60–72. [Google Scholar] [CrossRef]

- Merz, B.; Kreibich, H.; Schwarze, R.; Thieken, A. Assessment of economic flood damage. Nat. Hazards Earth Syst. Sci. 2010, 10, 1697–1724. [Google Scholar] [CrossRef]

- Yankson, P.W.K.; Owusu, A.B.; Owusu, G.; Boakye-Danquah, J.; Tetteh, J.D. Assessment of coastal communities’ vulnerability to floods using indicator-based approach: A case study of Greater Accra Metropolitan Area, Ghana. Nat. Hazards 2017, 89, 661–689. [Google Scholar] [CrossRef]

- Huong, N.T.L.; Yao, S.; Fahad, S. Assessing household livelihood vulnerability to climate change: The case of Northwest Vietnam. Hum. Ecol. Risk Assess. Int. J. 2018, 25, 1157–1175. [Google Scholar] [CrossRef]

- UNDRR. Terminology on Disaster Risk Reduction; United Nations Office for Disaster Risk Reduction: Geneva, Switzerland, 2017. [Google Scholar]

- Hahn, M.B.; Riederer, A.M.; Foster, S.O. The Livelihood Vulnerability Index: A pragmatic approach to assessing risks from climate variability and change—A case study in Mozambique. Glob. Environ. Chang. 2009, 19, 74–88. [Google Scholar] [CrossRef]

- Azen, R.; Walker, C.M. Categorical Data Analysis for the Behavioral and Social Sciences; Routledge: New York, NY, USA, 2011. [Google Scholar]

- Corbett, J. Famine and household coping strategies. World Dev. 1988, 16, 1099–1112. [Google Scholar] [CrossRef]

- Sakai, Y.; Estudillo, J.P.; Fuwa, N.; Higuchi, Y.; Sawada, Y. Do Natural Disasters Affect the Poor Disproportionately? Price Change and Welfare Impact in the Aftermath of Typhoon Milenyo in the Rural Philippines. World Dev. 2017, 94, 16–26. [Google Scholar] [CrossRef]

- Hyder, A.; Iqbal, N. Socio-Economic Losses of Flood and Household’s Coping Strategies: Evidence from Flood Prone District of Pakistan; Pakistan Instituteof Development Economics: Islamabad, Pakistan, 2016. [Google Scholar]

- Paul, B.K. Relief assistance to 1998 flood victims: A comparison of the performance of the government and NGOs. Geogr. J. 2003, 169, 75–89. [Google Scholar] [CrossRef]

- Mallick, B.; Rahaman, K.R.; Vogt, J. Coastal livelihood and physical infrastructure in Bangladesh after cyclone Aila. Mitig. Adapt. Strat. Glob. Chang. 2011, 16, 629–648. [Google Scholar] [CrossRef]

- Lawson, D.; Kasirye, I. How the Extreme Poor Cope with Crises: Understanding the Role of Assets and Consumption. J. Int. Dev. 2013, 25, 1129–1143. [Google Scholar] [CrossRef]

- Tomás, M.T.; Galán-Mercant, A.; Carnero, E.A.; Fernandes, B. Functional capacity and levels of physical activity in aging: A 3-year follow-up. Front. Med. 2018, 4, 244. [Google Scholar] [CrossRef] [PubMed]

- Bhattacharjee, K.; Behera, B. Determinants of household vulnerability and adaptation to floods: Empirical evidence from the Indian State of West Bengal. Int. J. Disaster Risk Reduct. 2018, 31, 758–769. [Google Scholar] [CrossRef]

- Boas, I. Social networking in a digital and mobile world: The case of environmentally-related migration in Bangladesh. J. Ethn. Migr. Stud. 2020, 46, 1330–1347. [Google Scholar] [CrossRef]

| District | Upazila | Union | Total Households | Sample Households |

|---|---|---|---|---|

| Nilphamari | Dimla | Purbachhatnai | 3435 | 68 |

| Rangpur | Gangachara | Gajaghanta | 7929 | 158 |

| Gaibandha | Sundarganj | Belka | 7608 | 151 |

| Total | 18,972 | 377 | ||

| Variables | Description | Mean | SD |

|---|---|---|---|

| Floodwater depth | Height of floodwater inside the home (continuous) | 2.12 | 1.03 |

| Location of house | Location of home within 1000 m from the riverbank: yes = 1, otherwise = 0 | 0.85 | 0.36 |

| Affected by disease | Family members infected by communicable disease in the last 5 years due to flood: yes = 1, otherwise = 0 | 0.86 | 0.35 |

| Age | Age of household head (in years) | 48.93 | 14.15 |

| Female | Female headed household: yes = 1, otherwise = 0 | 0.05 | 0.22 |

| Agricultural landless | Household does not have agricultural lands: yes = 1, otherwise = 0 | 0.48 | 0.50 |

| Crop save | Household has precautionary crop savings: yes = 1, otherwise = 0 | 0.27 | 0.45 |

| Mobile phone | Household has informational device at home: yes = 1, otherwise = 0 | 0.85 | 0.36 |

| Mitigation measures | Household has taken at least one structural mitigation measure to prevent a flood disaster: yes = 1, otherwise = 0 | 0.80 | 0.40 |

| Nonfarm income | Household has a non-farm income source: yes = 1, otherwise = 0 | 0.33 | 0.47 |

| Gajaghanta | Household lived in Gajaghanta: yes = 1, otherwise = 0 | 0.42 | 0.49 |

| Belka | Household lived in Belka: yes = 1, otherwise = 0 | 0.40 | 0.49 |

| Coping Strategies | Number of Coping Strategies | % of Households | |||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 0 | ||||||||||||||||||||||

| BOMO | ✓ | ⊙ | ⊙ | ⊙ | ⊙ | 🟂 | 🟂 | 🟂 | 🟂 | 🟂 | 🟂 | ✦ | ✦ | ✦ | ✦ | ✯ | 85% | ||||||||||

| ASDI | ✓ | ⊙ | ⊙ | ⊙ | ⊙ | 🟂 | 🟂 | 🟂 | 🟂 | 🟂 | ✦ | ✦ | ✦ | ✯ | 73% | ||||||||||||

| CORE | ✓ | ⊙ | ⊙ | ⊙ | 🟂 | 🟂 | 🟂 | 🟂 | ✦ | ✦ | ✦ | ✯ | 29% | ||||||||||||||

| TEMI | ⊙ | ⊙ | 🟂 | 🟂 | 🟂 | 🟂 | ✦ | ✦ | ✯ | 23% | |||||||||||||||||

| GRES | ✓ | ⊙ | ⊙ | ⊙ | 🟂 | 🟂 | 🟂 | 🟂 | 🟂 | ✦ | ✦ | ✦ | ✦ | ✯ | 34% | ||||||||||||

| Number of households | 15 | 22 | 4 | 2 | 98 | 23 | 9 | 11 | 4 | 7 | 7 | 3 | 9 | 49 | 12 | 8 | 28 | 2 | 1 | 24 | 12 | 9 | 1 | 5 | 9 | 3 | |

| Explanatory Variables | Dependent Variable | ||||

|---|---|---|---|---|---|

| Borrowing Money | Assets Disposal | Consumption Reduction | Temporary Migration | Grants from External Sources | |

| Floodwater depth | n.s | n.s | (2.25) *** | n.s | n.s |

| Location of house | (1.09) *** | (−0.86) * | n.s | n.s | (0.85) * |

| Affected by disease | (0.99) * | n.s | n.s | (1.28) * | n.s |

| Age | (−0.03) * | n.s | n.s | (−0.02) * | n.s |

| Female | (−1.62) ** | n.s | n.s | n.s | n.s |

| Agricultural landless | n.s | (−1.12) *** | (1.00) *** | (0.95) *** | n.s |

| Crop save | n.s | n.s | (−1.76) *** | (0.84) *** | n.s |

| Mobile phone | (0.89) * | n.s | n.s | (1.07) * | n.s |

| Mitigation measures | n.s | n.s | (−0.80) ** | (0.92) * | n.s |

| Nonfarm income | (−1.06) *** | (0.77) ** | n.s | n.s | n.s |

| Gajaghanta | n.s | n.s | n.s | n.s | (−1.86) *** |

| Belka | n.s | (1.18) *** | (−1.53) *** | n.s | (−1.67) *** |

| Constant | (2.31) * | (2.20) * | (−1.26) | (−3.28) *** | (−0.55) |

| Coping Strategies Variables | Recovered from Last Flood Disaster | ||

|---|---|---|---|

| Yes (N = 52) | No (N = 325) | OR [CI] (N = 3377) | |

| % of households borrowed money | 26.9 | 94.8 | 0.02 * [0.01–0.05] |

| % of households disposed assets | 94.2 | 70.2 | 6.95 * [2.12–22.84] |

| % of households reduced consumption | 13.5 | 31.1 | 0.35 * [0.15–0.79] |

| % of households migrated temporarily | 15.4 | 23.7 | 0.60 [0.26–1.30] |

| % of households received grants from external sources | 25.0 | 35.1 | 0.62 [0.32–1.20] |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mondal, M.S.H.; Murayama, T.; Nishikizawa, S. Determinants of Household-Level Coping Strategies and Recoveries from Riverine Flood Disasters: Empirical Evidence from the Right Bank of Teesta River, Bangladesh. Climate 2021, 9, 4. https://doi.org/10.3390/cli9010004

Mondal MSH, Murayama T, Nishikizawa S. Determinants of Household-Level Coping Strategies and Recoveries from Riverine Flood Disasters: Empirical Evidence from the Right Bank of Teesta River, Bangladesh. Climate. 2021; 9(1):4. https://doi.org/10.3390/cli9010004

Chicago/Turabian StyleMondal, Md. Sanaul Haque, Takehiko Murayama, and Shigeo Nishikizawa. 2021. "Determinants of Household-Level Coping Strategies and Recoveries from Riverine Flood Disasters: Empirical Evidence from the Right Bank of Teesta River, Bangladesh" Climate 9, no. 1: 4. https://doi.org/10.3390/cli9010004

APA StyleMondal, M. S. H., Murayama, T., & Nishikizawa, S. (2021). Determinants of Household-Level Coping Strategies and Recoveries from Riverine Flood Disasters: Empirical Evidence from the Right Bank of Teesta River, Bangladesh. Climate, 9(1), 4. https://doi.org/10.3390/cli9010004