Identifying the Socio-Spatial Logics of Foreclosed Housing Accumulated by Large Private Landlords in Post-Crisis Catalan Cities

Abstract

1. Introduction

2. Materials and Methods

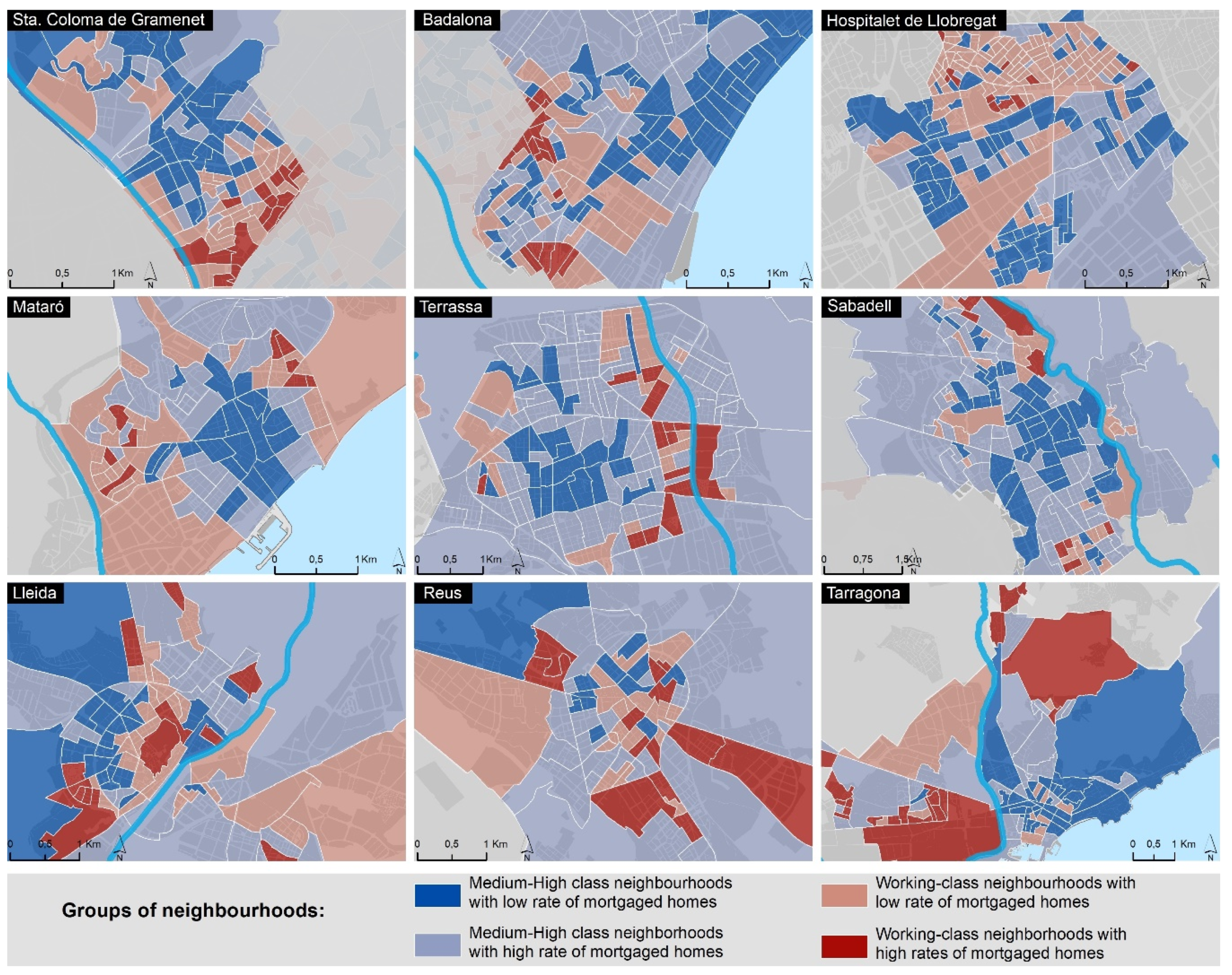

3. Results

4. Discussion and Conclusions

4.1. Implications of Our Findings and Main Contributions to the Field

4.2. Limitations

4.3. Future Research Lines

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Burriel, E. El estallido de la burbuja inmobiliaria y sus efectos en el territorio. In Geografía de la Crisis Econόmica en España; Albertos Puebla, J.M., Sánchez Hernández, J.L., Eds.; Universitat de València: Valencia, Spain, 2014; pp. 101–140. [Google Scholar]

- Romero, J.; Jimenez, F.; Villoria, M. (Un)Sustainable Territories: Causes of the Speculative Bubble in Spain (1996–2010) and its Territorial, Environmental, and Sociopolitical Consequences. Environ. Plan. C 2012, 30, 467–486. [Google Scholar] [CrossRef]

- Vinuesa, J. El Festín de la Vivienda. Auge y Caída del Negocio Inmobiliario en España; Diaz & Pons: Madrid, Spain, 2013. [Google Scholar]

- Domènech, A.; Gutiérrez, A. Paisatges Després de la Batalla. Geografies de la Crisi Inmobiliària; Institut d’Estudis Catalans: Barcelona, Spain, 2018. [Google Scholar]

- Méndez, R. La Telaraña Financiera. Una Geografía de la Financiarización y sus Crisis; IEUT-RIL Editores: Santiago de Chile, Chile, 2018. [Google Scholar]

- Gaja, F. Tras el tsunami inmobiliario. Salir del atolladero. In Paisajes Devastados. Después del Ciclo Inmobiliario: Impactos Regionales y Urbanos de la Crisis; Traficantes de Sueños: Madrid, Spain, 2013; pp. 313–354. [Google Scholar]

- Gutiérrez, A.; Delclòs, X. ¿Hipertrofia inmobiliaria? Análisis de las pautas territoriales del boom e implicaciones del estallido de la burbuja en Cataluña. Cuad. Geogr. 2015, 54, 283–306. [Google Scholar]

- Méndez, R. Ciudades en Venta: Estrategias Financieras y Nuevo Ciclo Inmobiliario en España; Universitat de València: Valencia, Spain, 2020. [Google Scholar]

- Madden, D.; Marcuse, P. In Defense of Housing: The Politics of Crisis; Verso: New York, NY, USA, 2016. [Google Scholar]

- Vives-Miró, S.; Rullan, O.; González-Pérez, J.M. Geografies de la Despossesió D’habitatge a Través de la Crisi: Els Desnonaments Marca Palma; Icaria: Barcelona, Spain, 2018. [Google Scholar]

- Gutiérrez, A.; Delclòs, X. Geografía de la crisis inmobiliaria en Cataluña: Una lectura a partir de los desahucios por ejecución hipotecaria. Scr. Nova 2017, 21, 7–33. [Google Scholar] [CrossRef]

- Gutiérrez, A.; Vives-Miró, S. Acumulación de viviendas por parte de los bancos a través de los desahucios: Geografía de la desposesión de vivienda en Cataluña. Eure 2018, 44, 5–26. [Google Scholar] [CrossRef]

- Alexandri, G.; Janoschka, M. Who Loses and Who Wins in a Housing Crisis? Lessons from Spain and Greece for a Nuanced Understanding of Dispossession. Hous. Policy Debate 2018, 28, 117–134. [Google Scholar] [CrossRef]

- Beswick, J.; Alexandri, G.; Byrne, M.; Vives-Miró, S.; Fields, D.; Hodkinson, S.; Janoschka, M. Speculating on London’s housing future. City 2016, 20, 321–341. [Google Scholar] [CrossRef]

- Gutiérrez, A.; Domènech, A. Spanish mortgage crisis and accumulation of foreclosed housing by SAREB: A geographical approach. J. Maps 2017, 13, 130–137. [Google Scholar] [CrossRef]

- Janoschka, M.; Alexandri, G.; Orozco Ramos, H.; Vives-Miró, S. Tracing the socio-spatial logics of transnational landlords’ real estate investment: Blackstone in Madrid. Eur. Urban Reg. Stud. 2019, 27, 125–141. [Google Scholar] [CrossRef]

- Doncel, L. Los fondos buitre reinan en España. El País. 21 May 2018. Available online: https://elpais.com/economia/2018/04/20/actualidad/1524234866_541409.html (accessed on 1 February 2020).

- El Confidencial. Blackstone, el mayor comprador de ladrillo español, prepara una oleada de ventas masiva. El Confidencial. 27 March 2019. Available online: https://www.elconfidencial.com/empresas/2019-03-27/blackstone-oleada-ventas-fidere-popular_1905118/ (accessed on 1 February 2020).

- Europa Press. Blackstone, el mayor casero de España, fusiona la gestión de 20.000 pisos en alquiler. Público. 12 January 2020. Available online: https://www.publico.es/economia/blackstone-mayor-casero-espana-fusiona-gestion-20000-pisos-alquiler.html (accessed on 1 February 2020).

- Byrne, M. Generating rent and the financialization of housing: A comparative exploration of the growth of the private rental sector in Ireland, the UK and Spain. Hous. Stud. 2020, 35, 743–765. [Google Scholar] [CrossRef]

- Fields, D. Constructing a New Asset Class: Property-led Financial Accumulation after the Crisis. Econ. Geogr. 2018, 94, 118–140. [Google Scholar] [CrossRef]

- Gutiérrez, A.; Domènech, A. The mortgage crisis and evictions in Barcelona: Identifying the determinants of the spatial clustering of foreclosures. Eur. Plan. Stud. 2018, 26, 1939–1960. [Google Scholar] [CrossRef]

- Leonard, T.; Murdoch, J.C. The neighborhood effects of foreclosure. J. Geogr. Syst. 2009, 11, 317. [Google Scholar] [CrossRef]

- Libman, K.; Fields, D.; Saegert, S. Housing and Health: A Social Ecological Perspective on the US Foreclosure Crisis. Hous. Theory Soc. 2012, 29, 1–24. [Google Scholar] [CrossRef]

- Schuetz, J.; Been, V.; Gould Ellen, I. Neighborhood effects of concentrated mortgage foreclosures. J. Hous. Econ. 2008, 17, 306–319. [Google Scholar] [CrossRef]

- Rugh, J.S.; Massey, D.S. Racial Segregation and the American Foreclosure Crisis. Am. Sociol. Rev. 2010, 75, 629–651. [Google Scholar] [CrossRef]

- Immergluck, D.; Smith, G. The Impact of Single-family Mortgage Foreclosures on Neighborhood Crime. Hous. Stud. 2006, 21, 851–866. [Google Scholar] [CrossRef]

- Immergluck, D.; Smith, G. The External Costs of Foreclosure: The Impact of Single-Family Mortgage Foreclosures on Property Values. Hous. Policy Debate 2006, 17, 57–79. [Google Scholar] [CrossRef]

- Lin, Z.; Rosenblatt, E.; Yao, V.W. Spillover Effects of Foreclosures on Neighborhood Property Values. J. Real Estate Financ. 2009, 38, 387–407. [Google Scholar] [CrossRef]

- García-Hernández, J.S.; Díaz-Rodríguez, M.C.; García-Herrera, L.M. Auge y crisis inmobiliaria en Canarias: Desposesión de vivienda y resurgimiento inmobiliario. Investig. Geogr. 2018, 69, 23–39. [Google Scholar] [CrossRef]

- Méndez, R. De la Hipoteca al Desahucio: Ejecuciones Hipotecarias y Vulnerabilidad Territorial en España. Rev. Geogr. Norte Gd. 2017, 67, 9–31. [Google Scholar] [CrossRef]

- Jiménez Barrado, V.; Sánchez Martín, J.M. Banca privada y vivienda usada en la ciudad de Madrid. Investig. Geogr. 2016, 66, 43–58. [Google Scholar] [CrossRef]

- Parreño-Castellano, J.M.; Domínguez-Mujica, J.; Armengol-Martín, M.; Pérez García, T.; Boldú Hernández, J. Foreclosures and Evictions in Las Palmas de Gran Canaria during the Economic Crisis and Post-Crisis Period in Spain. Urban Sci. 2018, 2, 109. [Google Scholar] [CrossRef]

- Waldron, R. The “unrevealed casualties” of the Irish mortgage crisis: Analysing the broader impacts of mortgage market financialisation. Geoforum 2016, 69, 53–66. [Google Scholar] [CrossRef]

- Gutiérrez, A.; Arauzo-Carod, J.M. Spatial Analysis of Clustering of Foreclosures in the Poorest-Quality Housing Urban Areas: Evidence from Catalan Cities. ISPRS Int. J. Geo-Inf. 2018, 7, 23. [Google Scholar] [CrossRef]

- García-Hernández, J.; Ginés de la Nuez, C. Geografías de la desposesión en la ciudad neoliberal: Ejecuciones hipotecarias y vulnerabilidad social en Santa Cruz de Tenerife (Canarias-España). Eure 2020, 46, 215–234. [Google Scholar]

- González-Pérez, J.M.; Vives-Miró, S.; Rullan, O. Evictions for unpaid rent in the judicial district of Palma (Majorca, Spain): A metropolitan perspective. Cities 2020, 97, 102466. [Google Scholar] [CrossRef]

- Anselin, L. Local indicators of spatial association—LISA. Geogr. Anal. 1995, 27, 93–115. [Google Scholar] [CrossRef]

- Anselin, L.; Syabri, I.; Kho, Y. GeoDa: An introduction to spatial data analysis. Geogr. Anal. 2006, 38, 5–22. [Google Scholar] [CrossRef]

- Celemín, J.P. Autocorrelación espacial e indicadores locales de asociación espacial. Importancia, estructura y aplicación. Rev. Univ. Geogr. 2009, 18, 11–31. [Google Scholar]

- IBM. SPSS—Missing Values 25. 2017. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=2ahUKEwig2OC2s5_pAhUjzIUKHZI2D-0QFjAAegQIARAB&url=ftp%3A%2F%2Fpublic.dhe.ibm.com%2Fsoftware%2Fanalytics%2Fspss%2Fdocumentation%2Fstatistics%2F25.0%2Fen%2Fclient%2FManuals%2FIBM_SPSS_Missing_Values.pdf&usg=AOvVaw1ks8Ok3xu6w70O64ff2S4i (accessed on 1 February 2020).

- Chatterjee, S.; Hadi, A.S. Regression Analysis by Example, 5th ed.; Wiley: Hoboken, NJ, USA, 2012. [Google Scholar]

- Esteban, M.; Altuzarra, A. Local Political Power and Housing Bubble in Spain. J. Reg. Res. 2016, 35, 107–127. [Google Scholar]

- Anselin, L. Exploring Spatial Data with GeoDa: A Workbook; Spatial Analysis Lab, University of Illinois: Urbana-Champaign, IL, USA, 2005; Available online: http://www.csiss.org/clearinghouse/GeoDa/geodaworkbook.pdf (accessed on 1 February 2020).

- Salas-Olmedo, M.H.; Moya-Gómez, B.; García-Palomares, J.C.; Gutiérrez, J. Tourists’ digital footprint in cities: Comparing Big Data sources. Tour. Manag. 2019, 66, 13–25. [Google Scholar] [CrossRef]

- Ministerio de Fomento. Atlas de la Vulnerabilidad Urbana; Ministerio de Fomento: Madrid, Spain, 2011. Available online: http://atlasvulnerabilidadurbana.vivienda.es/ (accessed on 1 February 2020).

- Hermosilla, T.; Palomar-Vázquez, J.; Balaguer-Bese, Á.; Balsa-Barreiro, J.; Ruiz, L.A. Using street based metrics to characterize urban typologies. Comput. Environ. Urban Syst. 2014, 44, 68–79. [Google Scholar] [CrossRef]

- Gutiérrez, A.; Delclòs, X. The uneven distribution of evictions as new evidence of urban inequality: A spatial analysis approach in two Catalan cities. Cities 2016, 56, 101–108. [Google Scholar] [CrossRef]

- Vives-Miró, S.; Rullan, O.; González-Pérez, J.M. Cartografías de los desplazamientos por desposesión de vivienda. Desahucios y ejecuciones hipotecarias en Palma a través de su geohistoria. Scr. Nova 2018, 22. [Google Scholar] [CrossRef]

- Immergluck, D. The Local Wreckage of Global Capital: The Subprime Crisis, Federal Policy and High-Foreclosure Neighborhoods in the US. Int. J. Urban Reg. Res. 2011, 35, 130–146. [Google Scholar] [CrossRef]

- Barreiro, J.B.; Landsperger, S. Pérdida de capital humano y desarrollo insostenible: Un círculo vicioso. Cuides 2013, 10, 55–84. [Google Scholar]

- Pawson, H.; Martin, C. Rental property investment in disadvantaged areas: The means and motivations of Western Sydney’s new landlords. Hous. Stud. 2020, 1–23. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Typology | Description | Source |

|---|---|---|

| Housing |

| Catalan Housing Agency |

| Origin |

| Spanish Census (2011) |

| Education level |

| Spanish Census (2011) |

| Economic |

| Spanish Census (2011) INE experimental 2 |

| Financial |

| Spanish Census (2011) |

| [a] | [b] | [c] | [d] | [e] | [f] | [g] | [h] | [i] | |

|---|---|---|---|---|---|---|---|---|---|

| [a] Housing units owned by banks | 1 | ||||||||

| [b] Foreign population (%) | 0.372 ** | 1 | |||||||

| [c] Employed population (%) | −0.276 ** | −0.348 ** | 1 | ||||||

| [d] Unemployed population (%) | 0.316 ** | 0.349 | −0.446 ** | 1 | |||||

| [e] Population (%) without studies | 0.172 ** | 0.083 | −0.433 ** | 0.239 ** | 1 | ||||

| [f] Population (%) with higher education | −0.289 ** | −0.284 ** | 0.493 ** | −0.462 ** | −0.545 ** | 1 | |||

| [g] Population (%) with income < 40% of the national median | 0.615 ** | 0.489 ** | −0.455 ** | 0.422 ** | 0.363 ** | −0.464 ** | 1 | ||

| [h] Average household income (€) | −0.441 ** | −0.383 ** | 0.470 ** | −0.487 ** | −0.522 ** | 0.758 ** | −0.717 | 1 | |

| [i] (%) Mortgages homes (%) | 0.116 ** | −0.182 ** | 0.270 ** | −0.042 | −0.244 ** | 0.069 * | −0.155 | 0.100 ** | 1 |

| Sta. Coloma Gramanet | 0.547 | Mataró | 0.407 | Lleida | 0.362 |

| Badalona | 0.422 | Terrassa | 0.264 | Reus | 0.202 |

| l’Hospitalet de Llobregat | 0.499 | Sabadell | 0.180 | Tarragona | 0.533 |

| Overall OLS | Badalona spatial error | Hospitalet de Llobregat spatial lag | Lleida spatial lag | Mataró spatial lag | |

|---|---|---|---|---|---|

| Foreign population (%)—2011 | 0.086 (0.020) *** | - | - | 0.170 (0.074) ** | - |

| Unemployed population (%)—2011 | 0.087 (0.048) *** | - | 0.239 (0.068) *** | - | - |

| Population with income < 40% median—2015 | 0.855 (0.042) *** | 1.399 (0.091) *** | 0.386 (0.060) *** | 0.525 (0.144) *** | 0.507 (0.085) *** |

| Mortgaged housing units (%)—2011 | 0.137 (0.016) *** | - | 0.072 (0.023) ** | 0.086 (0.053) * | 0.064 (0.035) * |

| Constant | −7.886 (0.929) *** | −7.081 (1.318) *** | −6.496 (1.319) *** | −5.761 (3.041) * | −4.047 (1.596) * |

| Spatial lag/error effects | - | 0.167 (0.125) + | 0.493 (0.068) *** | 0.520 (0.114) *** | 0.291 (0.134) * |

| Measure of fit: Adjusted R2 | 0.428 | 0.662 | 0.537 | 0.504 | 0.538 |

| Spatial dependence: Moran’s I for residuals | - | 0.001 | −0.033 | −0.032 | −0.034 |

| n censal tracts | 1075 | 149 | 226 | 81 | 77 |

| Reus spatial lag | Sabadell spatial error | Sta. Coloma de Gramenet spatial lag | Tarragona spatial lag | Terrassa spatial lag | |

| Foreign population (%)—2011 | - | 0.204 (0.049) *** | - | 0.158 (0.086) ** | 0.116 (0.061) * |

| Unemployed population (%)—2011 | - | - | 0.225 (0.095) * | - | - |

| Population with income < 40% median—2015 | 1.004 (0.176) *** | 1.020 (0.098) *** | 0.708 (0.105) *** | 0.493 (0.086) ** | 0.311 (0.118) ** |

| Mortgaged housing units (%)—2011 | 0.177 (0.081) * | - | 0.097 (0.037) ** | 0.115 (0.057) ** | - |

| Constant | −8.848 (4.331) + | −4.213 (1.165) *** | −9.569 (1.900) *** | −6.005 (2.846) ** | 2.041 (1.648) |

| Spatial lag/error effects | 0.219 (0.162) * | 0.195 (0.127) + | 0.199 (0.107) * | 0.387 (0.122) ** | 0.407 (0.105) ** |

| Measure of fit: Adjusted R2 | 0.422 | 0.602 | 0.660 | 0.507 | 0.263 |

| Spatial dependence: Moran’s I for residuals | 0.021 | 0.002 | −0.088 | −0.064 | −0.036 |

| n census tracts | 65 | 148 | 99 | 87 | 143 |

| Medium-High Class Neighbourhoods | Working-Class Neighbourhoods | ||||

|---|---|---|---|---|---|

| Overall Statistics (n = 1075) | [1] with Low Rate Mortgaged Homes (n = 326) | [2] with High Rate Mortgaged Homes (n = 345) | [3] with Low Rate Mortgaged Homes (n = 290) | [4] with High Rate Mortgaged Homes (n = 114) | |

| Foreign population (%)—2011 | 16.1 (15.1) | 9.1 (8.8) | 7.9 (7.3) | 26.4 (13.9) | 34.2 (18.3) |

| Unemployed population (%)—2011 | 15.5 (5.9) | 11.9 (4.4) | 14.2 (4.5) | 18.9 (5.0) | 21.5 (6.7) |

| Population with income < 40% median—2015 | 12.4 (7.2) | 8.1 (3.5) | 9.1 (4.1) | 16.2 (5.6) | 24.6 (7.6) |

| Mortgaged housing units (%)—2011 | 33.3 (16.3) | 23.3 (9.7) | 48.6 (11.2) | 24.4 (12.1) | 38.6 (16.6) |

| HOB | 10.0 (11.0) | 3.8 (4.0) | 8.0 (6.6) | 10.5 (6.1) | 32.3 (15.8) |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gutiérrez, A.; Domènech, A. Identifying the Socio-Spatial Logics of Foreclosed Housing Accumulated by Large Private Landlords in Post-Crisis Catalan Cities. ISPRS Int. J. Geo-Inf. 2020, 9, 313. https://doi.org/10.3390/ijgi9050313

Gutiérrez A, Domènech A. Identifying the Socio-Spatial Logics of Foreclosed Housing Accumulated by Large Private Landlords in Post-Crisis Catalan Cities. ISPRS International Journal of Geo-Information. 2020; 9(5):313. https://doi.org/10.3390/ijgi9050313

Chicago/Turabian StyleGutiérrez, Aaron, and Antoni Domènech. 2020. "Identifying the Socio-Spatial Logics of Foreclosed Housing Accumulated by Large Private Landlords in Post-Crisis Catalan Cities" ISPRS International Journal of Geo-Information 9, no. 5: 313. https://doi.org/10.3390/ijgi9050313

APA StyleGutiérrez, A., & Domènech, A. (2020). Identifying the Socio-Spatial Logics of Foreclosed Housing Accumulated by Large Private Landlords in Post-Crisis Catalan Cities. ISPRS International Journal of Geo-Information, 9(5), 313. https://doi.org/10.3390/ijgi9050313