Abstract

A large proportion of small and medium-sized enterprises are managed by their owners and founders. The goal of this research was to describe the diversity of management practices in owner-managed SMEs. Understanding this diversity will raise awareness of the challenges SMEs are facing and suggest possible solutions that will help improve their management and sustainability. In this study, 205 owner-managed SMEs with more than nine people employed were analyzed using a company self-assessment based on a tailor-made governance model. Data were analyzed using statistical analysis software in combination with a visual analysis. To group similar companies, the cluster analysis technique was used. The results showed a high diversity in how companies were managed and their performances. This research indicated that statistical analysis itself is not sufficient for exploring this diversity, and other approaches, such as visual analysis, must be used as well.

1. Introduction

Small and medium-sized enterprises (SMEs) represent up to 99% of all businesses in Europe, and provide two-thirds of the total employment in the private sector [1]. A large proportion of these enterprises are managed by their owners and founders.

Compared with larger organizations, SMEs have limited internal resources and internal knowledge, and must use external knowledge. However, the problem is that business literature, as well as training programs, often tend to use large enterprises and corporations as best-practice examples for establishing management practices, and often they are not appropriate for SMEs. In addition, management practices often used by professional managers cannot be used in the same way by owner-managers of SMEs, who mostly do not have a professional education in management. The adoption of open innovation by SMEs improves their overall innovation performance [2].

There is also a high diversity in the SME sector. These companies represent almost all business sectors, and have different operational patterns, different cultures, and different growth potentials, and no single classification could fit them all. In addition, open-innovation practices can be adopted by SMEs in diverse ways, such as the outside-in, inside-out, and coupled paradigms [3].

The goal of this research is to describe the diversity of management practices in owner-managed SMEs. This will highlight challenges SMEs are facing and provide possible solutions that will contribute to improving their management and sustainability.

Three enterprise categories are defined in Europe to distinguish SMEs by their size: microenterprises, small enterprises, and medium-sized enterprises. Enterprises with less than 10 employees are defined as microenterprises. Small enterprises have from 10 to 49 employees, and medium-sized enterprises are those that have from 50 to 249 employees. [4]. This research will focus on privately owned and owner-managed enterprises with more than nine people employed.

Jennings and Beaver formed a view on the management processes in small firms. They suggested that the management process in a small firm is unique and entirely different than the management process in larger enterprises. It shall not be assumed that small-firm management performs the same management process as performed in large companies by professional managers, only on a smaller scale [5].

A management system, according to Kaplan and Norton, is an integrated set of processes and tools that a company uses to develop its strategy, translate it into operational terms, and monitor and improve the effectiveness of both. Along with the definition, they suggested a concept, called the balanced scorecard, which integrated financial, market, process, and development dimensions of business and linked various financial and nonfinancial aspects of business by defined cause-and-effect relationships [6].

There is increasing controversial evidence of particular concepts having an impact on organizations and their performances and processes. According to Yusr, the arguments regarding the relationship between total quality management (TQM) and innovation are classified into two groups: the first group supports the positive relationship between TQM and innovation, whereas the second group claims that TQM does not support innovation in firms [7].

Accelerating environmental dynamics in today’s turbulent business environment requires speeding up the innovation process, and a suitable solution may be the use of agility, especially at the front end of innovation [8]. Agility attributes, capabilities, and practices also can be used to build an organizational agility model [9].

A large proportion of enterprises in the private sector are owned by individuals or families, and at the same time managed by their founders or owners. A preliminary typology consisting of 10 types of SME owner-managers as determined by their different ownership status and managerial authorities in companies was developed as result of research conducted by Millers and Gaile-Sarkane [10].

A study conducted in the UK found that SMEs were less likely to use formal management practices than larger firms. However, such practices appeared to have demonstrable benefits for those SMEs that used them, being positively associated with firm survival, growth, and productivity [11].

Open innovation has been defined as the use of purposive inflows and outflows of knowledge to accelerate internal innovation and expand the markets for external use of innovation [12]. Small and medium-sized enterprises have limited internal resources and internal knowledge, and must use external knowledge; however, diversity in the SME sector is high. Chesbrough et.al [13] identified several trends regarding how open innovation develops. One of the trends is that innovation is moving from large companies to SMEs; Another trend is that the industry is beginning to professionalize internal processes to manage open innovation more effectively and efficiently. Nevertheless, it is currently still more trial and error than a professionally managed process.

There is a deep relationship between open innovation, complex adaptive systems, and evolutionary change, and Yun et al. arranged them into conceptual model. According to Yun, the basic agent of open innovation is the firm. Open innovation at a firm goes through a complex adaptive system, which then leads to evolutionary change. However, in reality, a specific complex adaptive system can trigger open innovation through evolutionary properties at any given firm [14].

Svirina et al. [15] evaluated how closed- and open-innovation concepts are implemented by social enterprises in the emerging information economy. The inbound knowledge transfer for the development of open innovation can be used as an approach to business management [16].

Romero et al. identified 10 highly recognized authors on business models and business modelling who proposed formal meta-business models in publications between 2000 and 2010 [17], including Chesbrough, Hamel, and Osterwalder [12,18,19,20].

There are many ways to conduct an in-depth assessment of an organization’s performance regarding sustainability [21]. Company sustainability can be determined by a range of economic aspects, noneconomic aspects, and critical factors [22].

Management practices adopted in enterprise also can be influenced by the owner’s mentality [23], the age of the owner or CEO [24], management style, and personal preferences [25,26]. Assuming SMEs often are managed by persons who do not have a formal management education, an approach to analyze and develop their management practices must correspond with their management skills and understanding.

2. Materials and Methodology

In order to understand and explore the diversity of management practices in SMEs, a company self-assessment according to a tailor-made governance model was conducted. Research data were analyzed using statistical analysis software in combination with a visual analysis. The cluster analysis technique was used to group companies with similar management practices.

2.1. Development of the Governance Model for SME Self-Assessment

SMEs often are managed by owners and founders of the company who do not have a special management education. A governance model suitable for owner-managed SMEs was developed to collect data on how such companies are managed.

The model was based on the following principles:

- Systematic approach: the governance model was based on a systemic approach, and contained a definite and finite number of interrelated elements that provided a holistic view of the company;

- The principle of causes and effects: the model reflected the relationship between the approach established in the company and the outcome;

- Simplicity and transparency: the model should be simple and transparent enough to be understandable by and relevant to people without a special management education;

- Quantifiable evaluation: the governance model should be designed so that each element of the model can be quantified, regardless of the industry and the business specifics of particular enterprise.

The governance model created for this research consisted of nine elements that represented three logical levels: strategic level, organizational level, and management and control level. The model is presented in Table 1.

Table 1.

The owner-managed SME governance model.

The governance model for research was created by incorporating in one framework several key concepts and frameworks of strategy, quality management, and business modelling from Porter, Kaplan and Norton, Osterwalder and Pigneur, and the European Foundation for Quality Management [6,19,20,27,28].

The structure of the governance model, the number of elements and their titles, and the self-assessment criteria were discussed and approbated in a group of experts with consideration to the tools, methods, and language used in an academic environment, business literature, and management practice in small and medium-sized enterprises. The number of elements in the governance model was set to comply with the human limits of capacity to process information, defined by American psychologist G. A. Miller and recognized as “the magical number seven, plus or minus two” [29,30].

Each element in the self-assessment contained two questions—A and B, as described in Table 1. Question A regarded how developed and systematic the management approach was for companies for each element. Question B regarded results—specifically, what result was delivered for each element.

Altogether, there were 18 questions in the self-assessment, denoted by the relevant number of the element and the relevant letter (A for approach and B for results)—from 1A and 1B to 9A and 9B.

The scoring approach for self-assessment was based on a 5-point system. For questions on approach (the A question for each element), 1 point meant that there was no formal system in place, and the manager set all instructions and principles; and 5 points meant that a solid, advanced system was implemented. For results (the B question for each element), 1 point meant that there was evidence of weak results; and 5 points meant that the results were at the best-in-class level. Zero points meant that there was no evidence of any approach, or no results were known for the relevant element. The scoring criteria are described in Table 2.

Table 2.

Self-assessment criteria for Approach (A) and Results (B).

2.2. Self-Assessment Process

The self-assessment was usually performed as a part of management training session or knowledge-sharing events, and was guided by a facilitator who provided instructions and clarifications on assessment questions and principles.

Most of the respondents were owners, founders, and managers of the private SMEs. In several cases, the assessment was performed by a member of the management team or a management consultant involved in the SME’s organizational development activities.

Self-assessment data from 205 owner-managed SMEs with 10 or more people employed were collected through the electronic tool or in paper form. In several cases, participants completed the self-assessment together with their management team. Entrepreneurs who owned or managed several unrelated businesses could complete a self-assessment for each business separately. The research data from the electronic self-assessment tool and from the paper self-assessment questionnaires were summarized in an electronic table.

2.3. Data Analysis and Interpreation

For data analysis and representation of results, statistical software tools (SPSS and MS Excel) were used [31]. The cluster analysis technique was used to group companies with similar management practices. A dendrogram using the average linkage between groups (based on a rescaled distance cluster combine) was used to identify clusters of enterprises with similar management practices and performance levels.

Research data were analyzed using the statistical analysis software in combination with a visual analysis.

3. Results

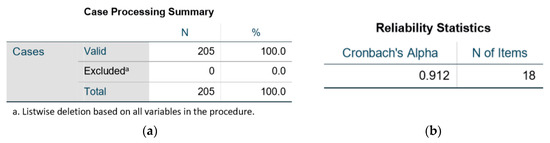

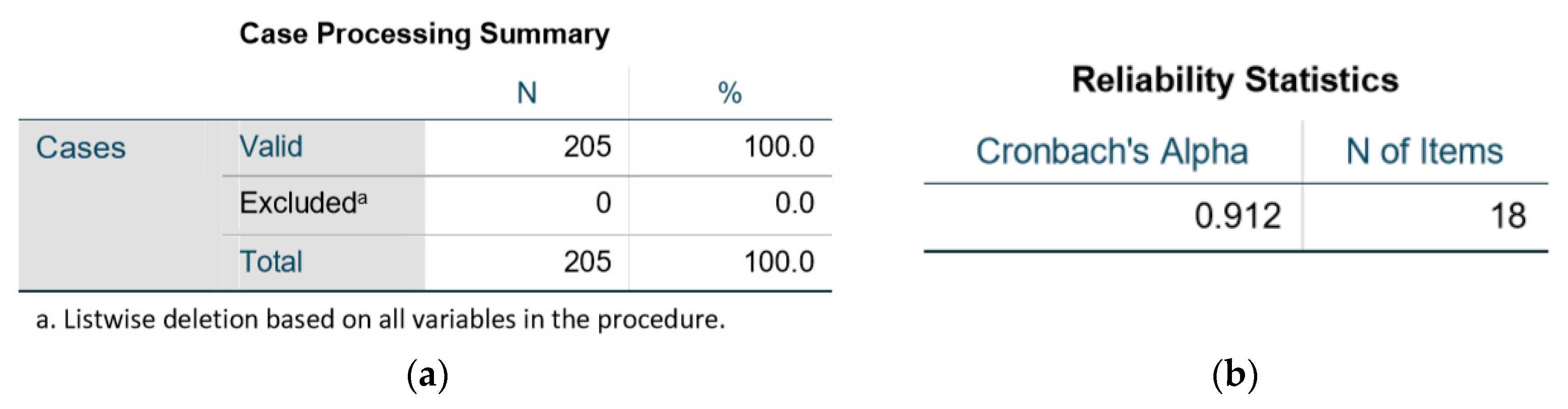

Questionnaires submitted by 205 respondents were considered valid for statistical data analysis. The general statistics are presented in Figure 1.

Figure 1.

General statistics: (a) case-processing summary; (b) reliability statistics.

The Cronbach’s alpha coefficient for the 18 items was 0.912, suggesting that the items had a relatively high internal consistency.

3.1. Distribution of Respondents by Company Size

In order to characterize the respondents according to the size of the company they represented, five categories of companies were defined, which in this study were denoted by the numbers 10, 25, 50, 100, and 200. In this case, the size of the company was defined as the sum of full- or part-time employees in the company, the number of permanently employed full-time or part-time external service providers (such as couriers, accountants, auxiliary workers, technical staff, etc.), and regularly engaged specialists or freelancers (designers, salespeople, experts, consultants, etc.). In cases where one business consisted of a group of several legal units or enterprises, the number of employees was the total number of employees in all these enterprises. Therefore, in the context of this study, the number of employed persons by a company could differ from the number of employees reported in the state registers. The number of survey respondents according to the company size is shown in Table 3.

Table 3.

The distribution of respondents by company size (n = 205).

3.2. Self-Assessment Results by Company Size

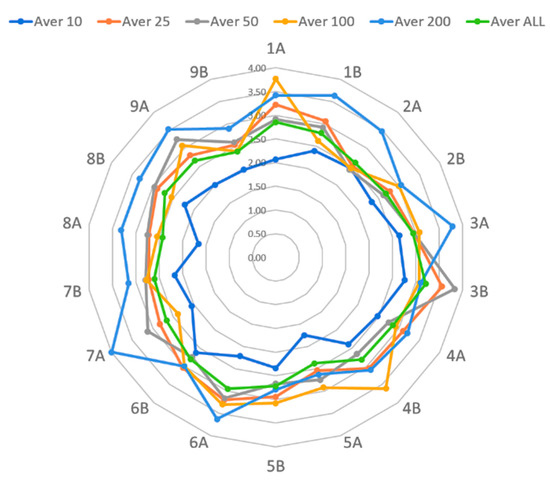

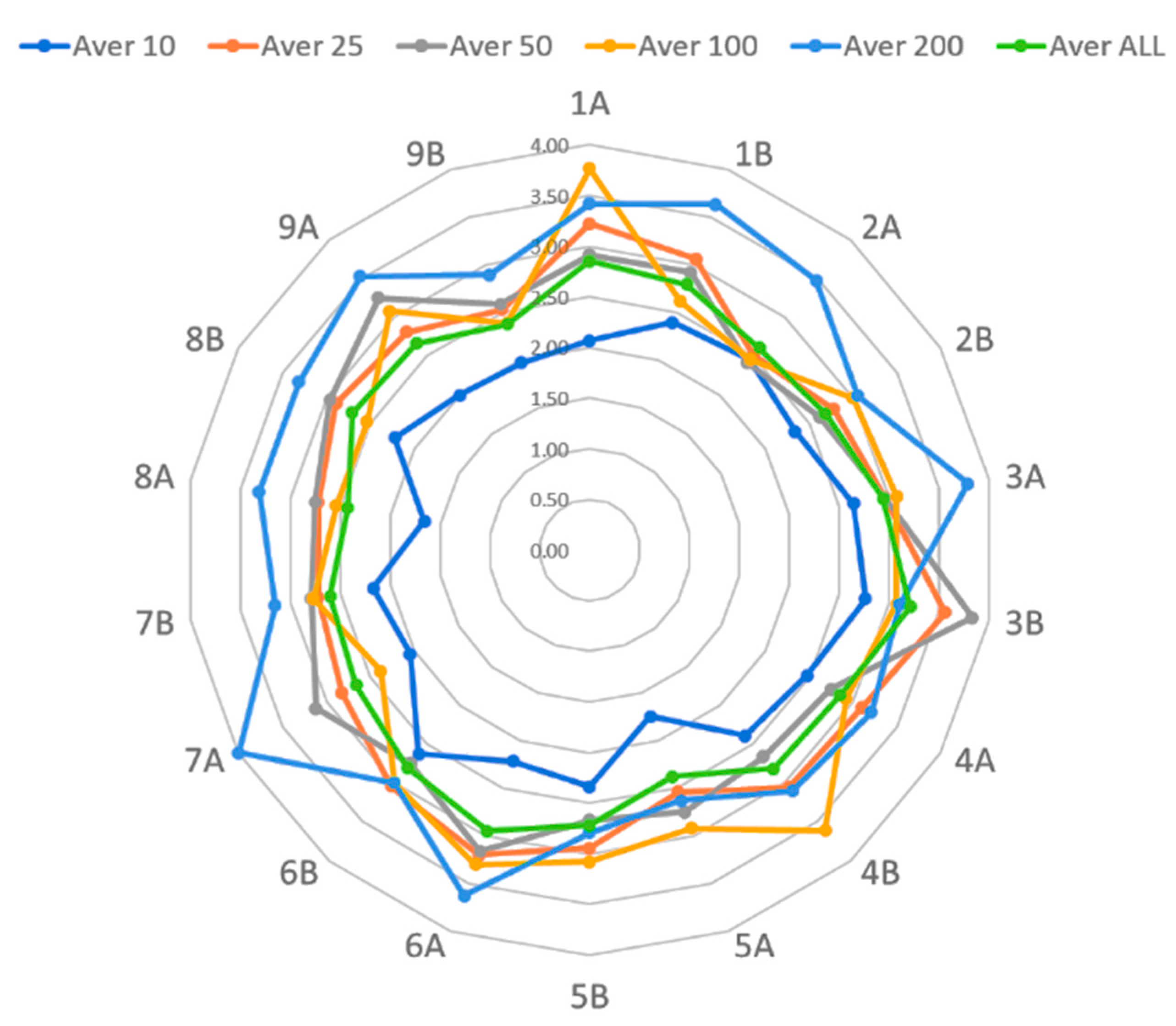

The average results of self-assessment for companies grouped by their size using a radar diagram format are shown in Figure 2.

Figure 2.

The average results for self-assessment in companies grouped by size.

The average self-assessment score of all groups (green line, “Aver ALL”) for most of the self-assessment questions was between 2.5 and 3.0 points. The result for self-assessment was slightly lower for question 5A (Approach—Process Management—2.38 points), but slightly higher for question 3B (Results—Customer Base and Loyalty—3.21 points).

In the group of companies with 10–20 people employed (dark blue line, “Aver 10”) the results of the self-assessment for almost all elements were slightly lower than for larger enterprises. On the other hand, for larger companies, the self-assessment results were slightly higher for questions, but for some questions, it was 1–1.5 points higher than for other companies. For example, among the largest companies—in the category “200” (see light blue line, “Aver 200” in Figure 2)—higher self-assessment results were returned for questions 3A—market and customer management approach, and 7A—management group organization. In turn, in the “100” category of companies (yellow line, “Aver 100” in Figure 2) the higher result was returned for questions 1A—Business Model (Approach) and 4B—Supply Competitiveness (Results).

The diagram shown in Figure 2 presents the averages of the groups of companies; however, the individual self-assessment results for each company could differ from the average results, as well as from other similar companies in their industry or group of companies. These results should be seen as statistical information, and without further analysis, would not yet be used as a basis for decisions on the company’s development.

It should also be noted that the results of the self-assessment for question 9B, as shown in Figure 2 visually appeared weaker than for other questions, which still meant that companies were working with a positive cash flow and showed a profit at least in the short term, and that was a sufficient result. The financial situation of a particular company should be assessed using the company’s financial statements, forecasts, and liabilities, as well as the comparative financial indicators of the industry.

3.3. Corelation between Approach and Results

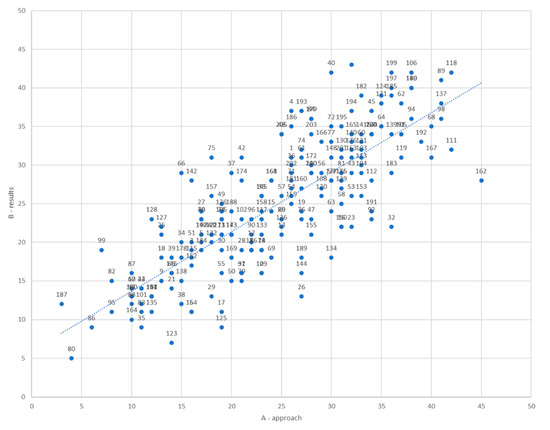

When analyzing the correlation between set A (sum of questions 1A to 9A), regarding the approach by the company in each of the self-assessment elements; and set B (sum of questions 1B to 9B, regarding the results for each of the self-assessment elements using Spearman’s correlation coefficient, a significant correlation (r = 0.808) was found (see Table 4).

Table 4.

Correlation between approach (the A questions) and results (the B questions).

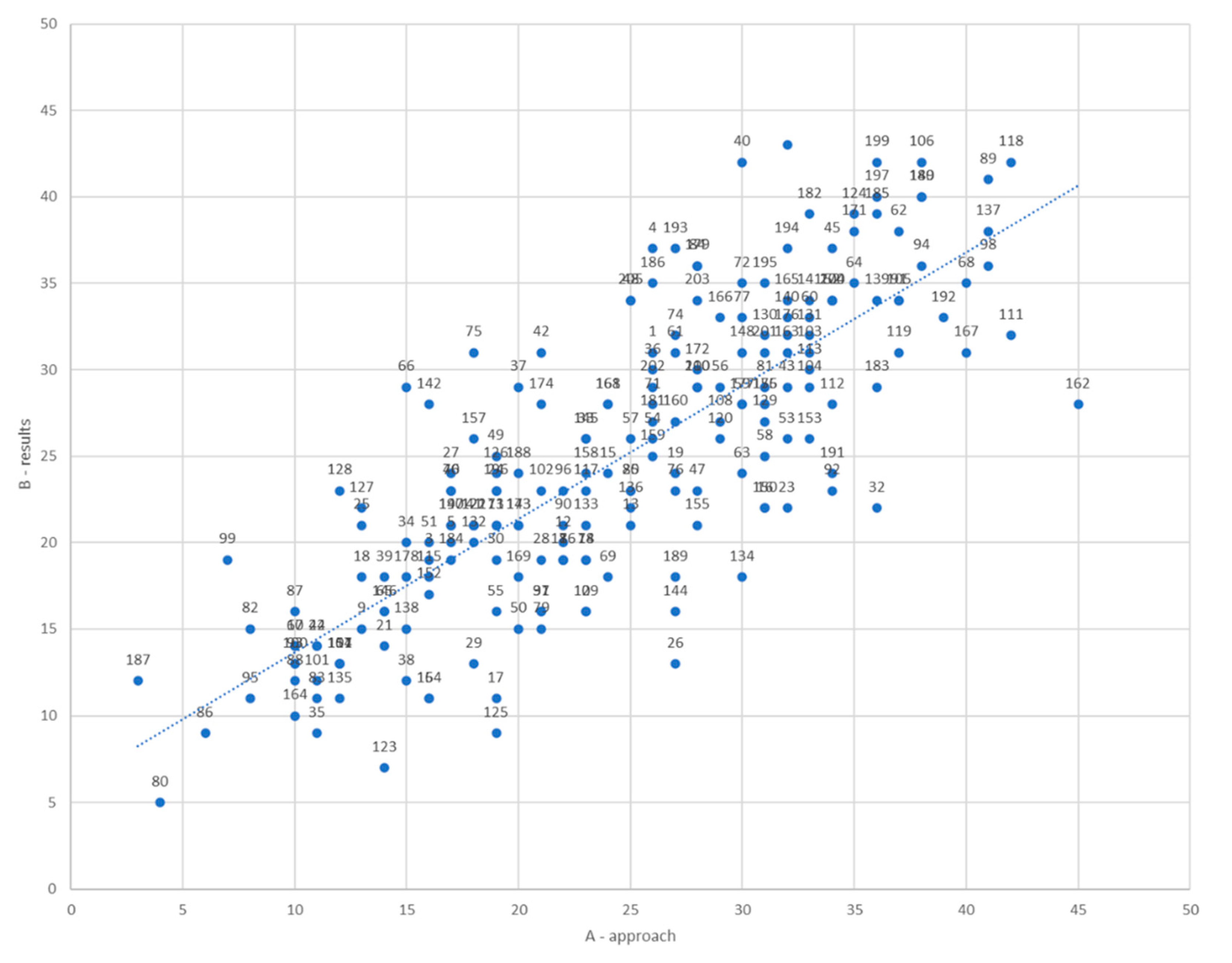

This showed that there was a correlation between the overall approach of a company and the company’s performance. The same relationship also was seen in the scatter diagram presented in Figure 3.

Figure 3.

A scatter diagram showing sums for Approach (A) and Results (B) (N = 205).

The scatter diagram (Figure 3) also shows that enterprises with a higher total score for the Approach questions (sum of A questions, on the horizontal x-axis) tended to also have higher scores for the Results questions (sum of B questions, on the vertical y-axis). However, there also were many respondents with total Results scores that were considerably higher or considerably lower than the total Approach scores.

3.4. Cluster Analysis by Enterprises

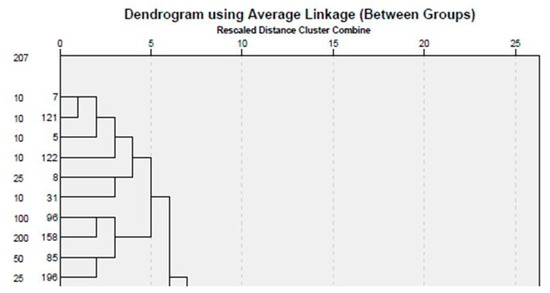

In order to search for companies with similar characteristics among respondents, a cluster analysis by company was performed. Cluster analyses are based on the mathematical calculation of the distance in the multidimensional space between the results of each company’s self-assessment.

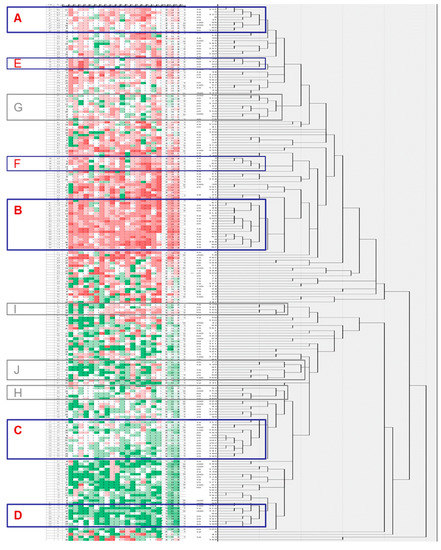

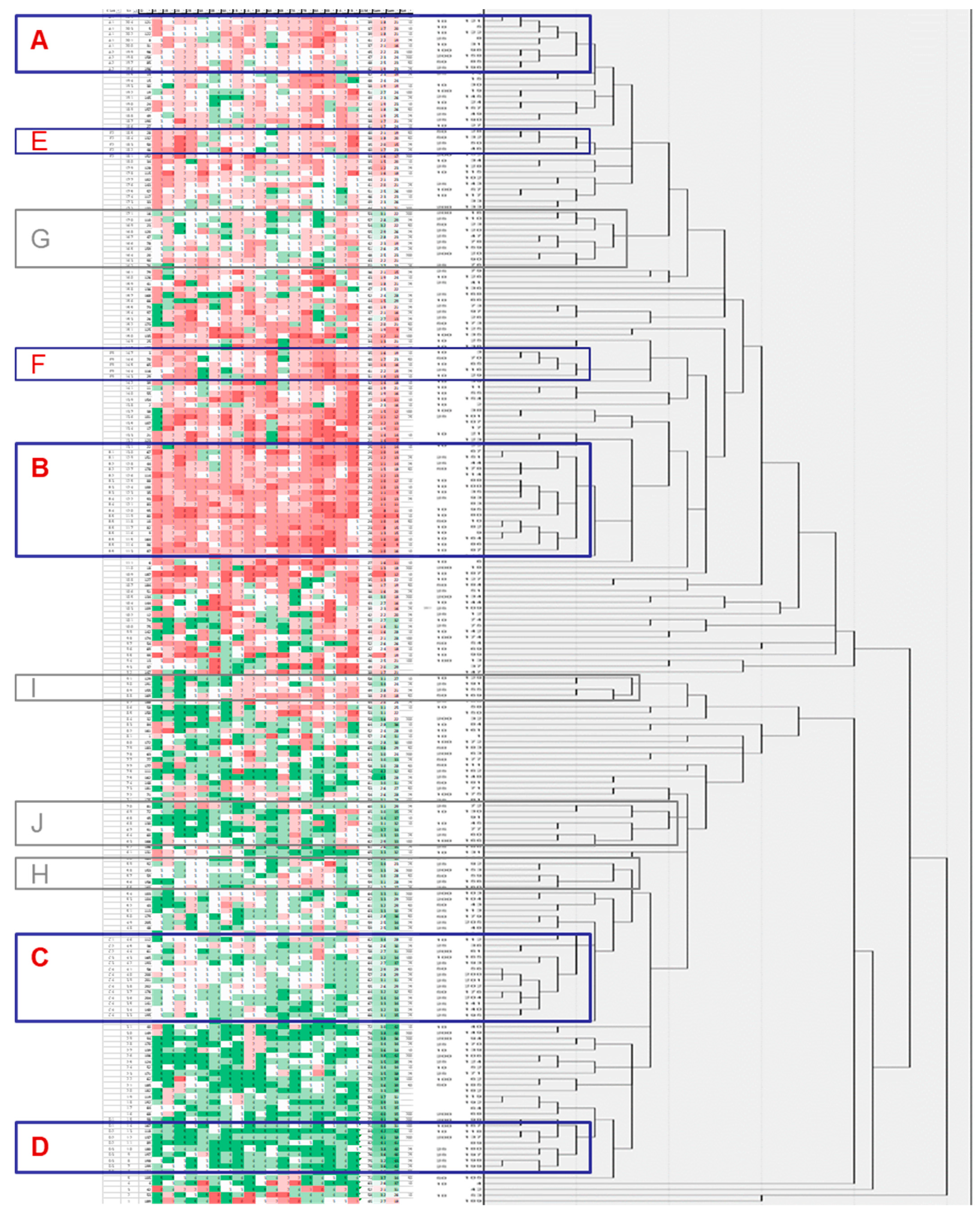

The result of the cluster analysis performed using SPSS software was visually represented by a dendrogram. To understand which companies were forming clusters, the dendrogram was realigned with the self-assessment results table for all 205 enterprises. To enable visual analysis of the results, all individual responses were highlighted using the red-to-green color code, which is explained in Figure 4.

Figure 4.

The red-to-green color code for the self-assessment scoring table.

The dendrogram of all 205 enterprises is presented on the right in Figure 5. The self-assessment results table for all 205 enterprises, rearranged according to the dendrogram and colored with the red-to-green color code, is presented on the left in Figure 5. Enlarged parts of this picture are presented further in this section—part of the dendrogram representing Cluster A is shown in Figure 6, and part of the table with the individual responses of Cluster A enterprises in shown in Table 5.

Figure 5.

Clusters illustrated by individual responses (left) combined with a dendrogram (right).

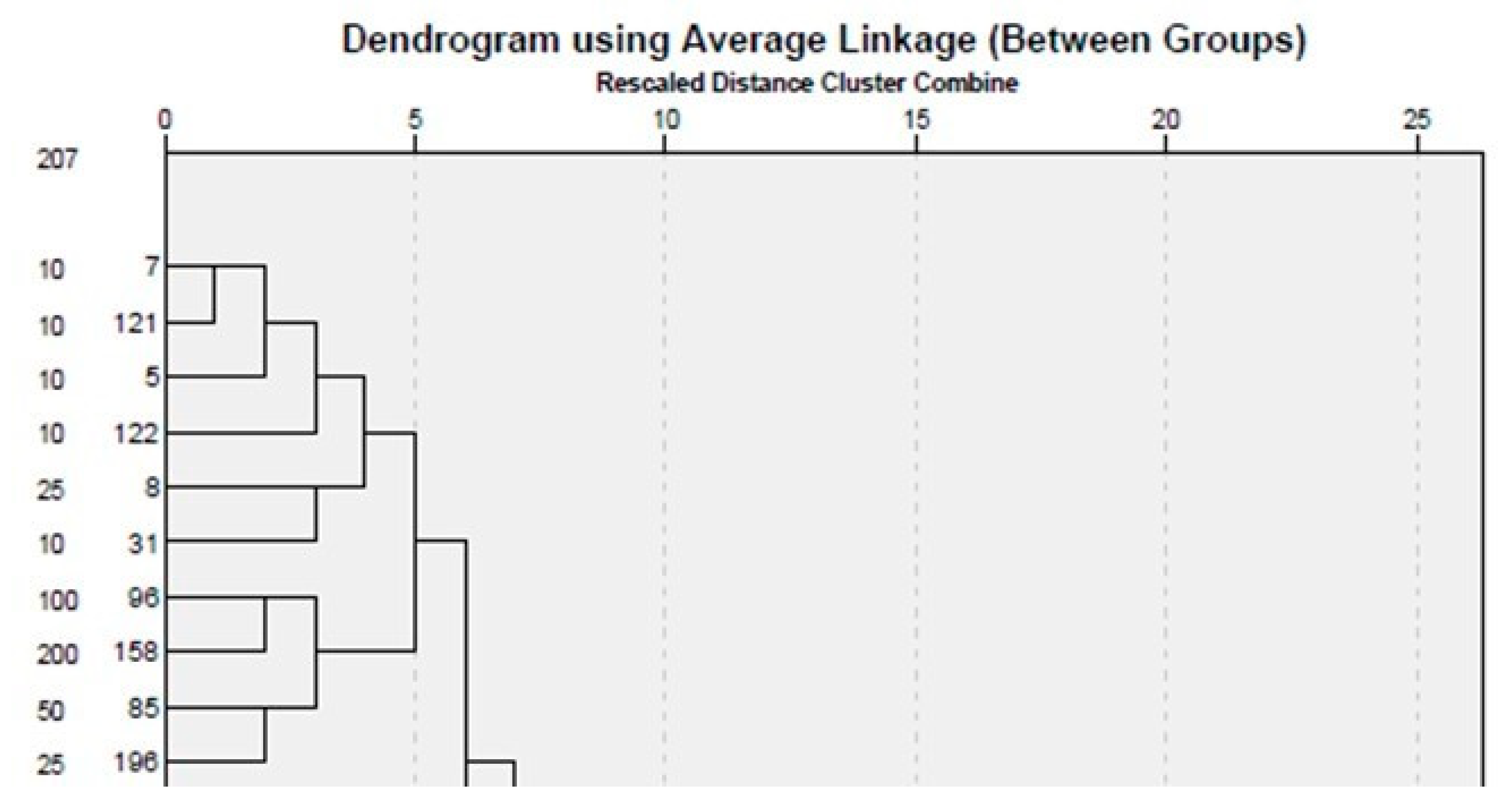

Figure 6.

The dendrogram fragment for cluster A.

Table 5.

The individual responses of respondents from cluster A.

The selection and formation of clusters must be performed based on two criteria. First, the cluster must be formed from enterprises with adequate similarity—respondents with a small enough distance from other respondents within the chosen cluster. Second, the cluster must have enough enterprises to form a sufficiently significant group.

For the first round of formation of cluster distance, five units were selected, and the target size of the cluster was 5% from the total number of respondents (in our case—10 enterprises from a total number of 205 participants in this research).

By choosing a distance value of 5 (five units) for cluster formation, four distinctly larger enterprise clusters with at least 10 or more respondents each appeared in the dendrogram for this study (Clusters A, B, C, and D in Figure 5).

With a chosen distance of five units, there were two more clusters in this dendrogram, with four or five respondents in each (Clusters E and F), and another 16 microclusters with two or three respondents each also could be found. For other respondents, the “distance” to the next-nearest respondent was greater than five units.

The first cluster (referred to as cluster “A”) consisted of 10 companies, which were numbered in the study data table as companies #7, #121, #5, #122, #8, #31, #96, #158, #85, and #196 (see also Figure 6 and Table 5).

The companies included in cluster A can be described as companies with a medium-developed approach and medium-good performance. The total self-assessment results for these companies ranged from 37 to 48 points, which was assessed as quite good. For some self-assessment questions, respondents in this cluster could also have a higher score (3 or 4 points), but for some questions, the performance was marked as weak (with 1 or even 0 points). The companies in this cluster were characterized by positive trends in the development of their customer bases, as well as good financial results (almost all companies had an assessment score of 3 points for question 9B (Financial Results); and for question 3B (Customer Base), 3 or even 4 points).

Although mathematically, all 10 companies were relatively divided into one group, there were two subgroups in this cluster, which will be referred to as A1 and A2, and there were already differences between these subgroups. The individual responses of the companies included in subgroups A1 and A2 are shown in Table 5.

In subgroup (subcluster) A1, which had six companies (#7, #121, #5, #122, #8, and #31), similar self-assessment results were expressed in questions 5B—Efficiency (2 points for all answers), 3A (Setting Goals and Strategy), and 3B (Achieving Goals)—all answers were at the level of 3 or 4 points; and showed good financial results (3-point answer to question 9B—Financial Results). This subgroup consisted mainly of companies from the group of smaller companies with 10 or 25 employees.

The second subgroup, A2, which included companies #96, #158, #85 and #196, had stronger management team practices with higher scores (3 points) for question 7B (Leadership). All enterprises in subgroup A2 were companies with 25–200 employees.

A similar analysis was performed with other clusters. The second cluster (referred to here as cluster “B”), consisted of 18 companies. In addition, this cluster could be split into several smaller subgroups, with differences specific to each. Subgroup B1 and subgroup B2 showed a higher performance for questions 3A and 3B (Target Market and Customer Base) than other companies in this cluster, while companies in subgroup B5 had better financial results (question 9B) than other companies in cluster B, and reached a level of 3 points, similar to companies in cluster A.

Companies in cluster C (15 enterprises) were characterized by good self-assessment results in terms of both Approach and Results, and the total self-assessment results were from 55 to 68 points. Cluster C companies also could be split into three more specific subsegments.

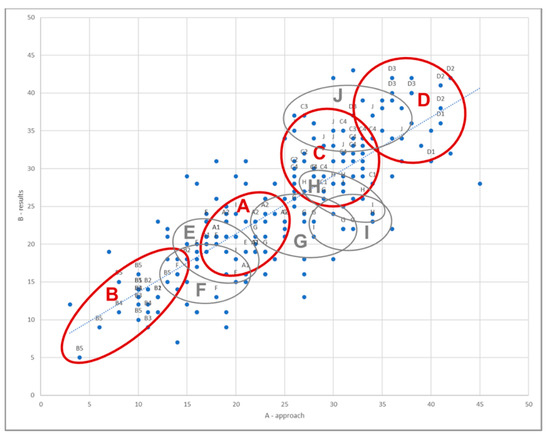

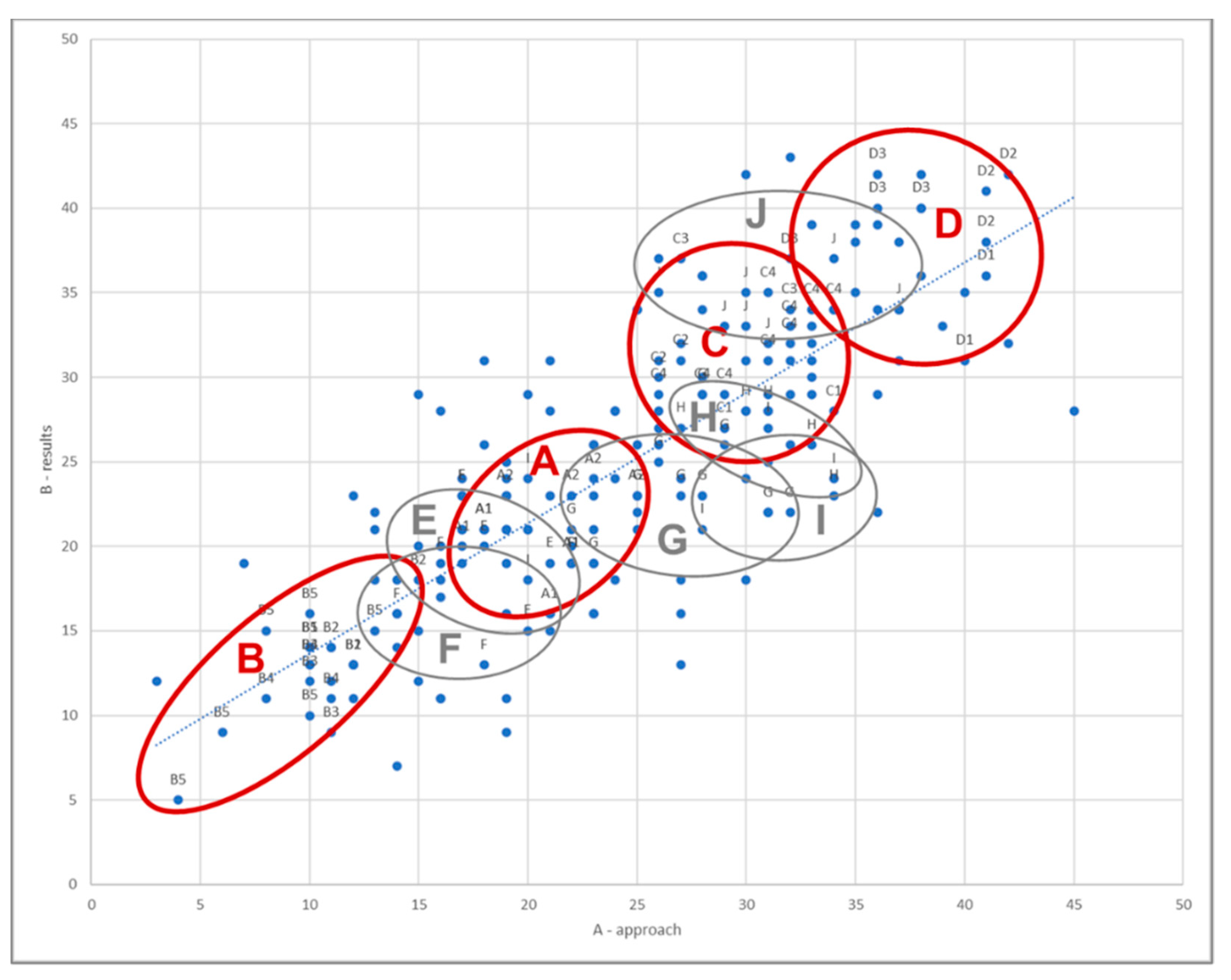

The locations of enterprises from clusters A, B, C, and D on the overall scatter diagram are presented in Figure 7, circled in red.

Figure 7.

The scatter diagram showing clusters A, B, C, and D; and E, F, G, H, I, and J.

Comparing the cluster framework of individual subgroup C, it was observed that the companies in subgroup C1 had weaker financial results (in question 9B) than other companies in this cluster, but for companies in subgroup C2, Product Portfolio (question 4B) had the highest possible rating—5 points. Subsegment C3 companies were characterized by strong financial management practices (high score for question 9A), as well as good financial results (score of 3 or 4 points for question 9B).

The D cluster was formed by 10 companies that were characterized by high scores for most self-evaluation questions—4 or 5 points; as well as a high total self-evaluation result—69–84 points. The planning approach was particularly highly valued (question 8A). Most companies in this cluster also had high financial results (5 points in question 9B).

The locations of enterprises from clusters E, F, G, H, I, and J on the overall scatter diagram are presented in Figure 7, circled in grey.

It was noted that together there were 53 enterprises in the four clusters A, B, C and D, and this represented only 26% of all respondents. All other enterprises were part of other smaller clusters.

An attempt to form clusters using a distance larger than 5 can lead to an unusable outcome. For example, clusters G and J (as shown in Figure 5) consisted of enterprises with very different approaches and different results in many self-evaluation elements. Clusters I and H consisted of very small number of enterprises, which represented just 2–3% of the total number of respondents.

If the distance for formation clusters was selected as 3 or 4 units, then the cluster map would result in 35 small specific clusters. Such a number was too high for formation of an easy-to-use and easy-to-communicate cluster map. Setting a lower distance for formation of clusters still left a significant proportion of enterprises (up to 30%) outside any defined cluster, as seen in the dendrogram in Figure 5 and also in the scatter diagram in Figure 7.

4. Discussion

The number of clusters and their structure in this study showed that there was a great diversity and variety among owner-managed small and medium-sized enterprises—how companies are managed and what their performance is.

The data from this study showed a strong correlation between the development level of management practices and approaches (represented by the A questions of the governance model) and company performance (represented by the B questions of the governance model).

However, evidence also showed that there were enterprises with well-developed management practices and weak performance at the same time, and vice versa—companies that could achieve higher performance levels with less developed management practices.

As could be expected, smaller enterprises (with 10–20 people employed) tended to have a less structured and systematic approach than larger SMEs. However, the size of enterprise did not lead automatically to higher results.

It shall be noted that only a small proportion of enterprises (53 enterprises in this research or 26% from all respondents) created several typical situations that are described in this research as clusters A, B, C, and D. Most enterprises created multiple unique situations that cannot be described by a relatively small number of typical and representative governance patterns (clusters).

The fact that the results of self-assessment of companies could be grouped into a finite number of small clusters (such as 35 clusters with 2-5-8 respondents in each cluster) suggested that a situation specific to one company may be similar to some other or several other companies, so it cannot be assumed that the situation of each company was unique and unrepeatable.

Increasing of cluster accuracy by reducing relative distance for formation clusters to 3 or 4 units, would result in a large number of clusters (35 small specific clusters, each representing 1–2% of the total number of respondent). A cluster map with such a large number of clusters is not easy to use and simple to communicate.

5. Conclusions

5.1. Implications

Mathematical analysis of company data makes it possible to identify typical company situations and find other companies with similar circumstances. Understanding of management practices and performance of enterprises belonging to the same cluster can give general indications on potential strength, weaknesses, or potential risks for enterprise.

However, such information does not yet provide sufficient grounds to draw any specific conclusions about the current organization and proposals for improvement of approaches and management practices in a specific enterprise.

Decisions about development efforts in a specific enterprise shall be made based on analysis management practices and performance in this particular enterprise, analysis of external environment, customers, and competition.

Visual interpretation of data—both individual and consolidated results—helps to see and understand information better, especially if this concerns owner-managers of SMEs, who often do not have formal education in management field.

5.2. Limits and Future Research Topics

This research was conducted in Latvia and included owner-managers of 205 SMEs with 10 and more people employed. The results of this research shall not be generalized to other markets and other enterprises without additional research.

The approach and methods used in this research, if adapted accordingly, can be used to analyze management practices in enterprises of different size or ownership.

In order to better interpret the results of the self-assessment, a visual analysis of individual self-assessment results can be used. To draw conclusions about the current situation and development opportunities of a particular company, it is necessary to look also on company internal and external situation, customers, competitions, and stakeholders. Self-assessment model used in this research can be used to help owners and management of the private SMEs make better decisions on their organization development.

Methods and conclusions from this research can be used in education process in entrepreneurship programs in universities and also in management training.

Author Contributions

Conceptualization, M.M.; methodology, M.M.; supervision, E.G.-S.; formal analysis, M.M.; writing—original draft preparation, M.M.; review and editing, E.G.-S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- European Commission. Annual Report on European SMEs 2018/2019. Annual Report. 2019. Available online: https://op.europa.eu/en/publication-detail/-/publication/cadb8188-35b4-11ea-ba6e-01aa75ed71a1/language-en (accessed on 4 March 2021).

- Hossain, M.; Kauranen, I. Open innovation in SMEs: A systematic literature review. J. Strategy Manag. 2016, 9, 58–73. [Google Scholar] [CrossRef]

- Almeida, F. Open-innovation practices: Diversity in portuguese smes. J. Open Innov. Technol. Mark. Complex. 2021, 7, 169. [Google Scholar] [CrossRef]

- European Commission. User Guide to the SME Definition; Publications Office of the European Union: Luxemburg, 2020; pp. 1–60. Available online: https://op.europa.eu/en/publication-detail/-/publication/756d9260-ee54-11ea-991b-01aa75ed71a1 (accessed on 10 September 2020).

- Jennings, P.L.; Beaver, G. The managerial dimension of small business failure. Strateg. Chang. 1995, 4, 185–200. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Mastering the management system. Harv. Bus. Rev. 2008, 86, 62–77. [Google Scholar]

- Yusr, M.M. Innovation capability and its role in enhancing the relationship between TQM practices and innovation performance. J. Open Innov. Technol. Mark. Complex. 2016, 2, 6. [Google Scholar] [CrossRef] [Green Version]

- Brand, M.; Tiberius, V.; Bican, P.M.; Brem, A. Agility as an innovation driver: Towards an agile front end of innovation framework. Rev. Manag. Sci. 2021, 15, 157–187. [Google Scholar] [CrossRef]

- Žitkienė, R.; Deksnys, M. Organizational agility conceptual model. Montenegrin J. Econ. 2018, 14, 115–129. [Google Scholar] [CrossRef]

- Millers, M.; Gaile-Sarkane, E. Towards new typology of the owners-managers of the small and medium enterprises. In Proceedings of the International Scientific Conference Contemporary Issues in Business, Management and Economics Engineering, Vilnius, Lithuania, 11–12 May 2021. [Google Scholar] [CrossRef]

- Forth, J.; Bryson, A. Management practices and SME performance. Scott. J. Political Econ. 2019, 66, 527–558. [Google Scholar] [CrossRef]

- Chesbrough, H.W. Open Business Models: How to Thrive in the New Innovation Landscape. Res. Technol. Manag. 2006, 50, 256. [Google Scholar] [CrossRef]

- Gassmann, O.; Enkel, E.; Chesbrough, H. The future of open innovation. R D Manag. 2010, 40, 213–221. [Google Scholar] [CrossRef]

- Yun, J.J.; Won, D.; Park, K. Dynamics from open innovation to evolutionary change. J. Open Innov. Technol. Mark. Complex. 2016, 2, 7. [Google Scholar] [CrossRef] [Green Version]

- Svirina, A.; Zabbarova, A.; Oganisjana, K. Implementing open innovation concept in social business. J. Open Innov. 2016, 2, 20. [Google Scholar] [CrossRef] [Green Version]

- Dubickis, M.; Gaile-Sarkane, E. Transfer of know-how based on learning outcomes for development of open innovation. J. Open Innov. Technol. Mark. Complex. 2017, 3, 4. [Google Scholar] [CrossRef] [Green Version]

- Romero, M.C.; Lara, P.; Villalobos, J. Evolution of the Business Model: Arriving at Open Business Model Dynamics. J. Open Innov. Technol. Mark. Complex. 2021, 7, 86. [Google Scholar] [CrossRef]

- Hamel, G. Leading the Revolution: How to Thrive in Turbulent Times by Making Innovation a Way of Life; Plume/Penguin: New York, NY, USA, 2002. [Google Scholar]

- Osterwalder, A.; Pigneur, Y.; Tucci, C. Clarifying Business Models: Origins, Present, and Future of the Concept. Commun. Assoc. Inf. Syst. 2005, 16, 1. [Google Scholar] [CrossRef] [Green Version]

- Osterwalder, A.; Pigneur, Y. Business Model Generation—A Handbook for Visionaries, Game Changers and Challengers; John Wiley and Sons, Inc.: Hoboken, NJ, USA, 2010. [Google Scholar]

- Medne, A.; Lapiņa, I. Sustainability and Continuous Improvement of Organization: Review of Process-Oriented Performance Indicators. J. Open Innov. Technol. Mark. Complex. 2019, 5, 49. [Google Scholar] [CrossRef] [Green Version]

- Herrera, J.; de las Heras-Rosas, C. Economic, non-economic and critical factors for the sustainability of family firms. J. Open Innov. Technol. Mark. Complex. 2020, 6, 119. [Google Scholar] [CrossRef]

- Wijewardena, H.; Nanayakkara, G.; De Zoysa, A.D. The owner/manager’s mentality and the financial performance of SMEs. J. Small Bus. Enterp. Dev. 2008, 15, 150–161. [Google Scholar] [CrossRef]

- Belenzon, S.; Shamshur, A.; Zarutskie, R. CEO’s age and the performance of closely held firms. Strateg. Manag. J. 2019, 40, 917–944. [Google Scholar] [CrossRef]

- Jaouen, A.; Lasch, F. A new typology of micro-firm owner-managers. Int. Small Bus. J. 2015, 33, 397–421. [Google Scholar] [CrossRef]

- Wang, Y.; Poutziouris, P. Leadership Styles, Management Systems and Growth: Empirical Evidence from UK Owner-Managed SMEs. J. Enterp. Cult. 2010, 18, 331–354. [Google Scholar] [CrossRef]

- Porter, M.E. What is Strategy? Harv. Bus. Rev. 1996, 74, 61–78. [Google Scholar] [CrossRef] [Green Version]

- European Foundation for Quality Management. The EFQM Model. 2021. Available online: https://www.efqm.org/efqm-model (accessed on 7 June 2021).

- Miller, G.A. The magical number seven, plus or minus two: Some limits on our capacity for processing information. Psychol. Rev. 1956, 63, 81–97. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Baddeley, A. The Magical Number Seven: Still Magic After All These Years? Psychol. Rev. 1994, 101, 353–356. [Google Scholar] [CrossRef]

- Stehlik-Barry, K.; Babinec, A.J. Data analysis with IBM SPSS Statistics: Implementing data modeling, descriptive statistics and ANOVA. In Data Analysis with International Business Machines Statistical Package for the Social Sciences Statistics; Pact Publishing: Birmingham, UK, 2017. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).