The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review

Abstract

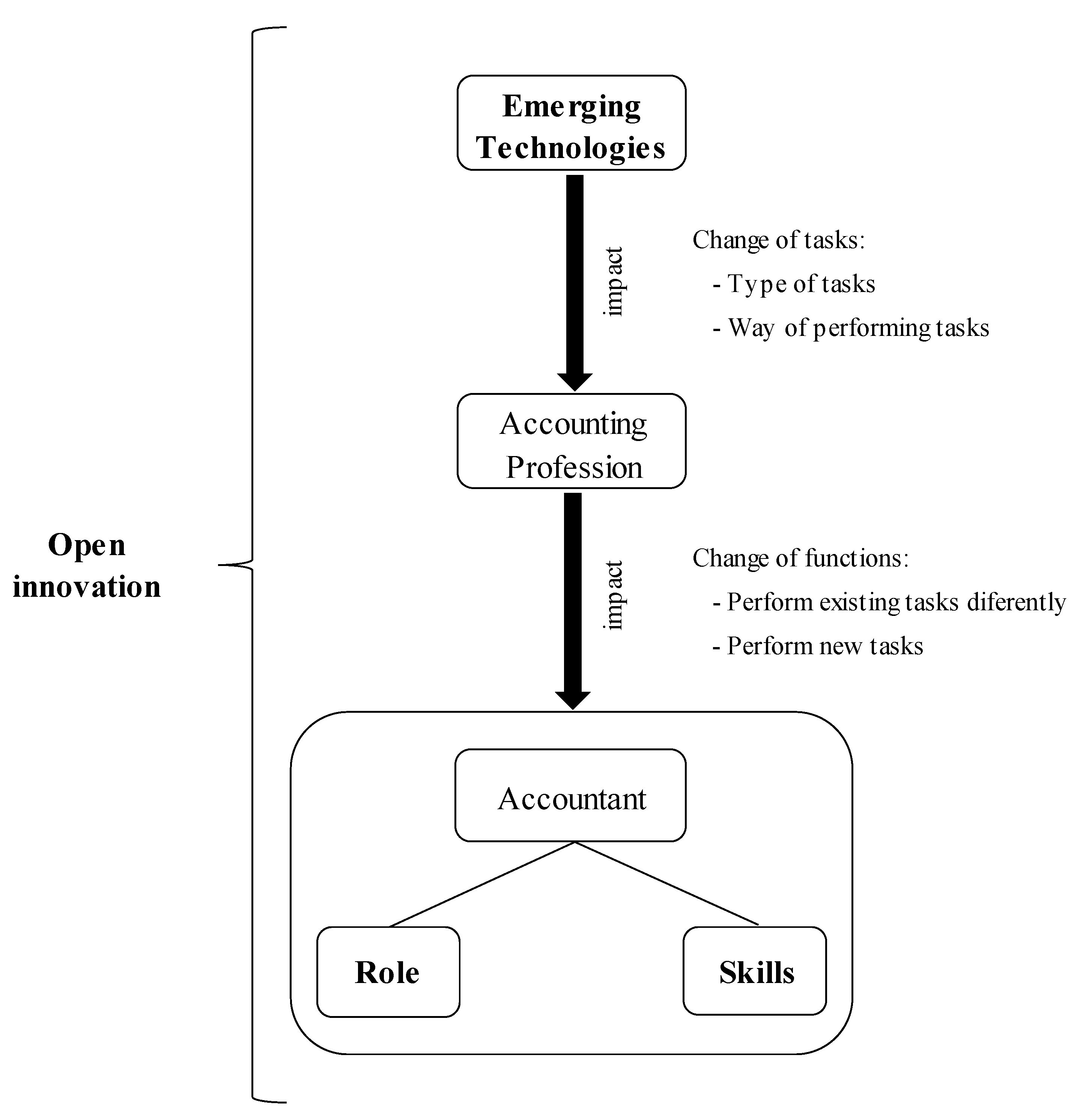

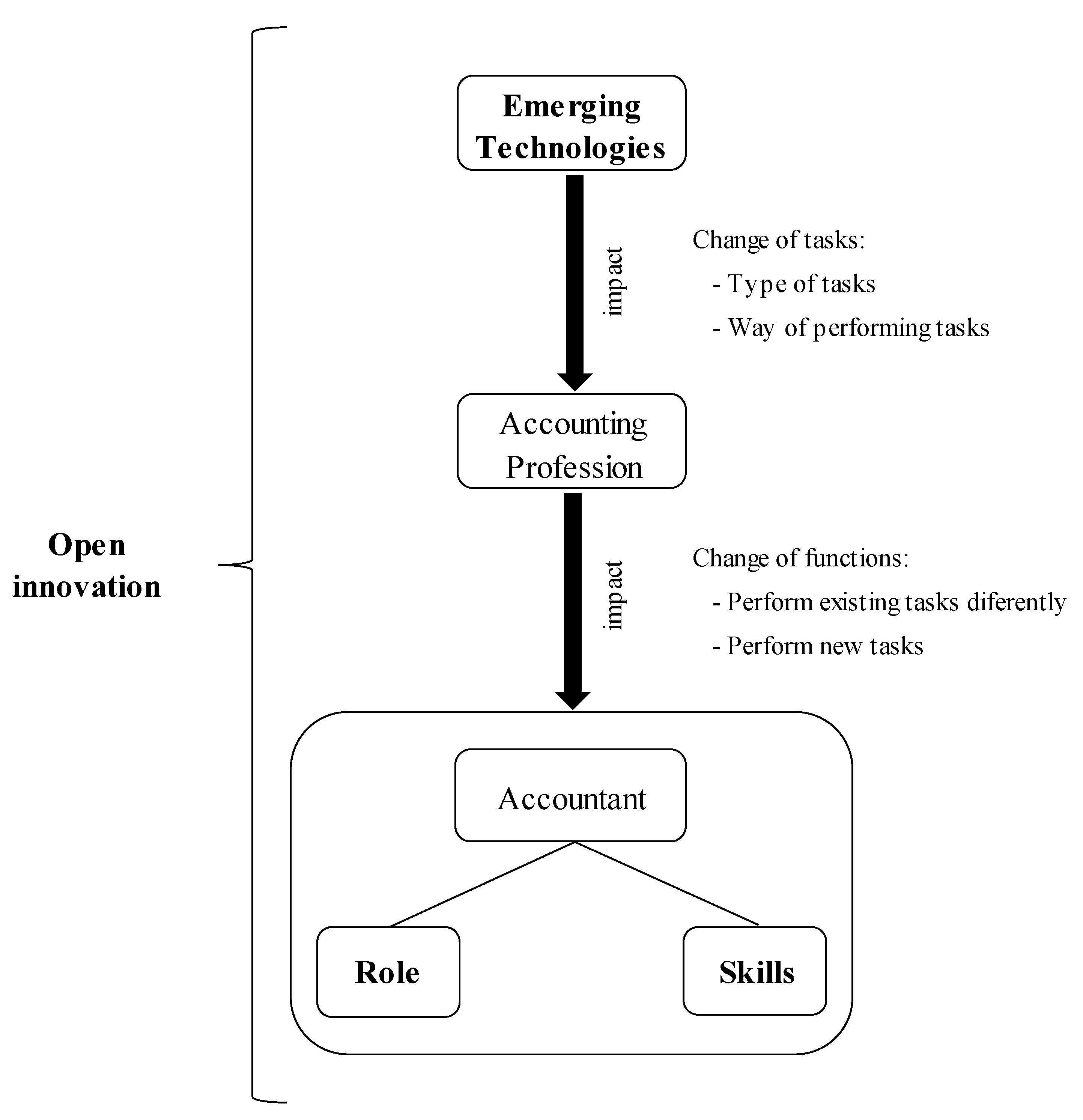

:1. Introduction

- Which emerging technology is most often studied concerning its impacts on accountants’ role and skills?

- What research strategies are being used to identify emerging technologies’ impacts on accountants’ role or skills?

- Is open innovation an influencing factor connecting emerging technologies and accountants’ role and skills?

- What are the most commonly identified impacts of emerging technologies on accountants’ role and skills?

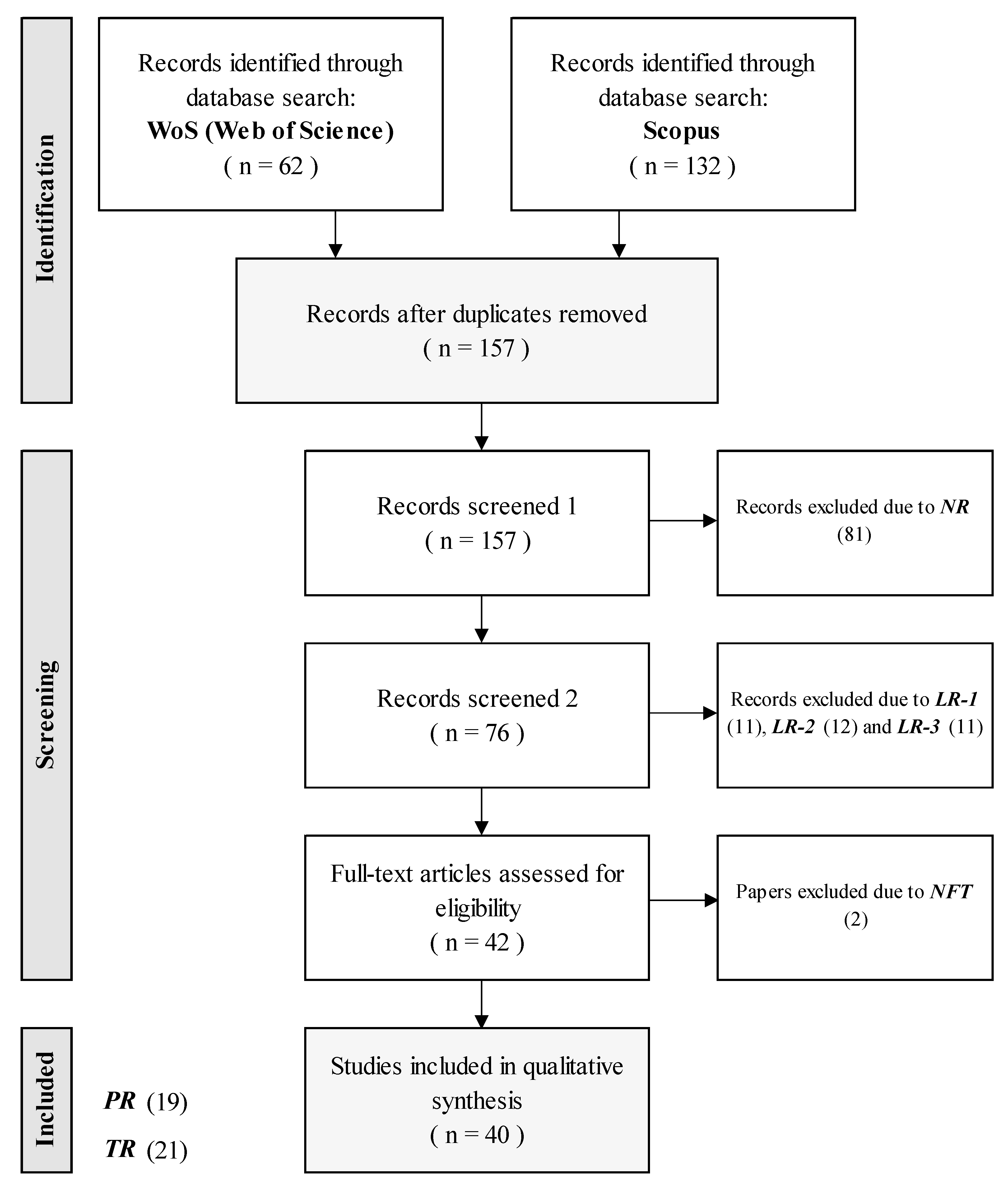

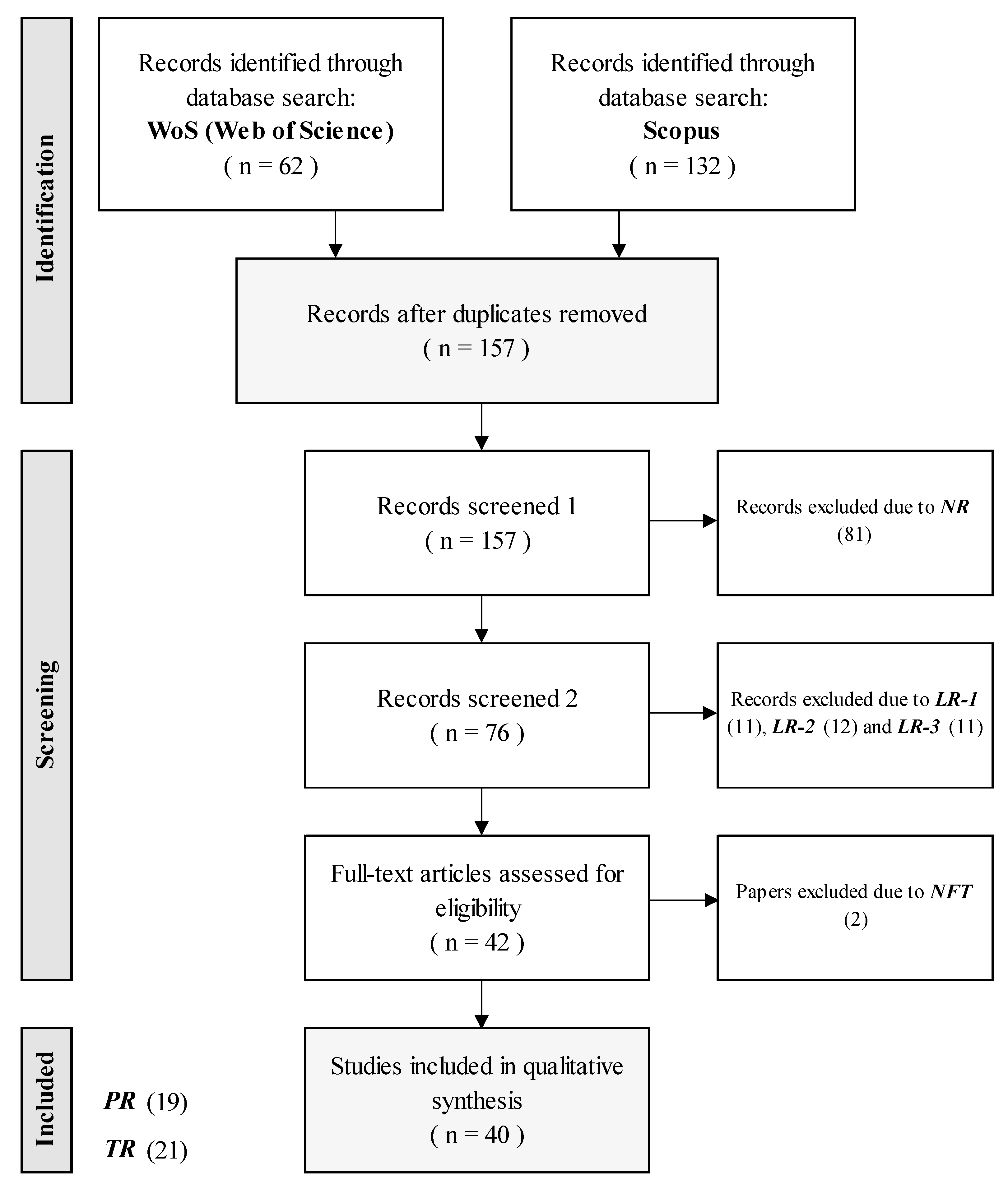

2. Methodology

2.1. Article Collection

2.2. Data Collection

- Archival, which presents a review related to impacts of emerging technologies on accountants’ role and skills as its main content (includes Literature Review);

- Behavioral, which uses experimental or observational methods to identify and analyze specific issues related to the impacts of emerging technologies on accountants’ role and skills (includes Case Study, Survey, Interviews, and Experimental);

- Conceptual, which offers a discussion of challenges, issues, or trends related to impacts of emerging technologies on accountants’ role and skills as its main content, adding something “new” to the research area.

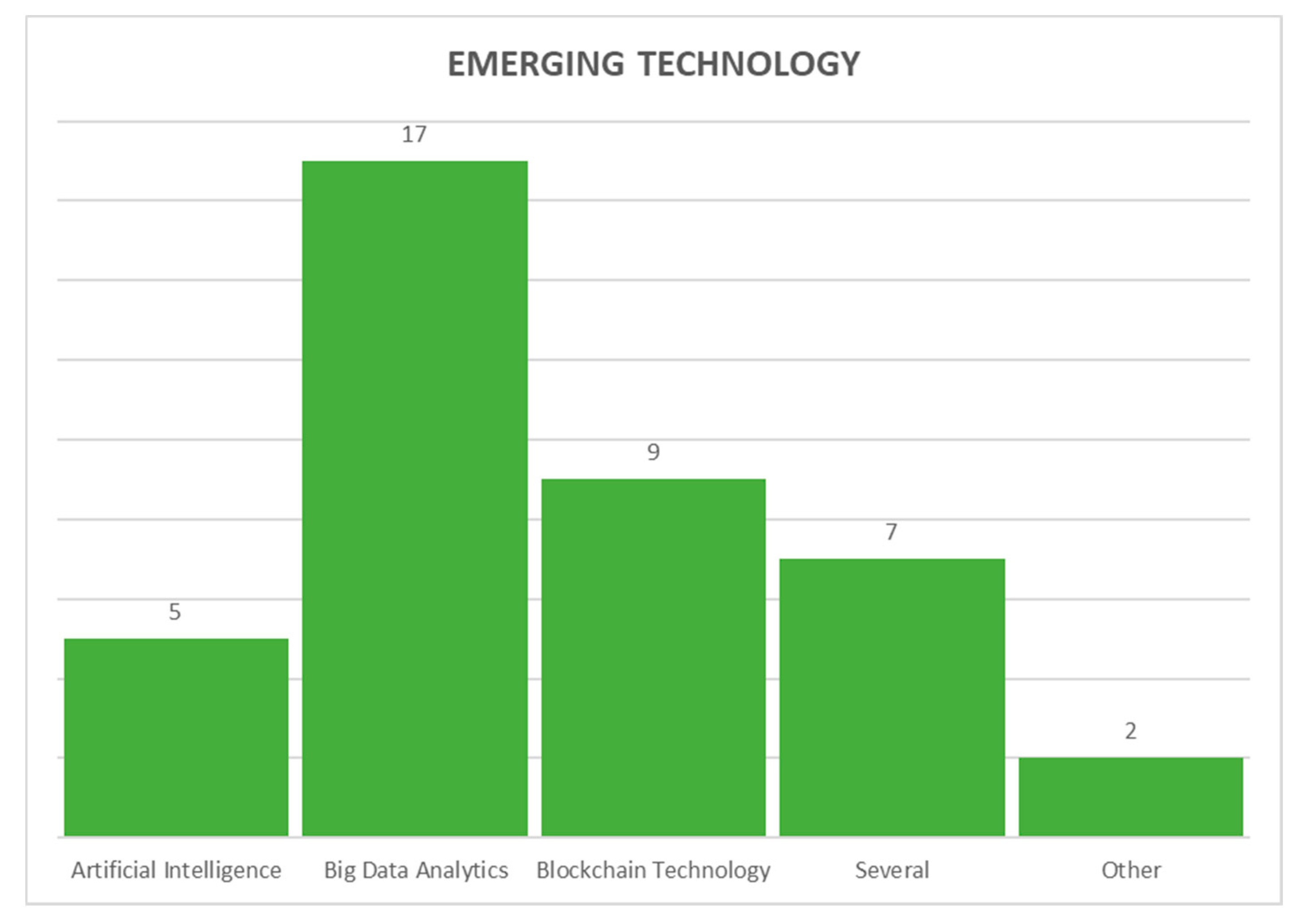

- Big data analytics; Blockchain technology; Artificial intelligence; Several (includes several or all the before mentioned technologies); Other;

- Accounting (general); Financial accounting; Management accounting; Auditing; Auditing and accounting; Management and financial accounting; Other.

3. Results

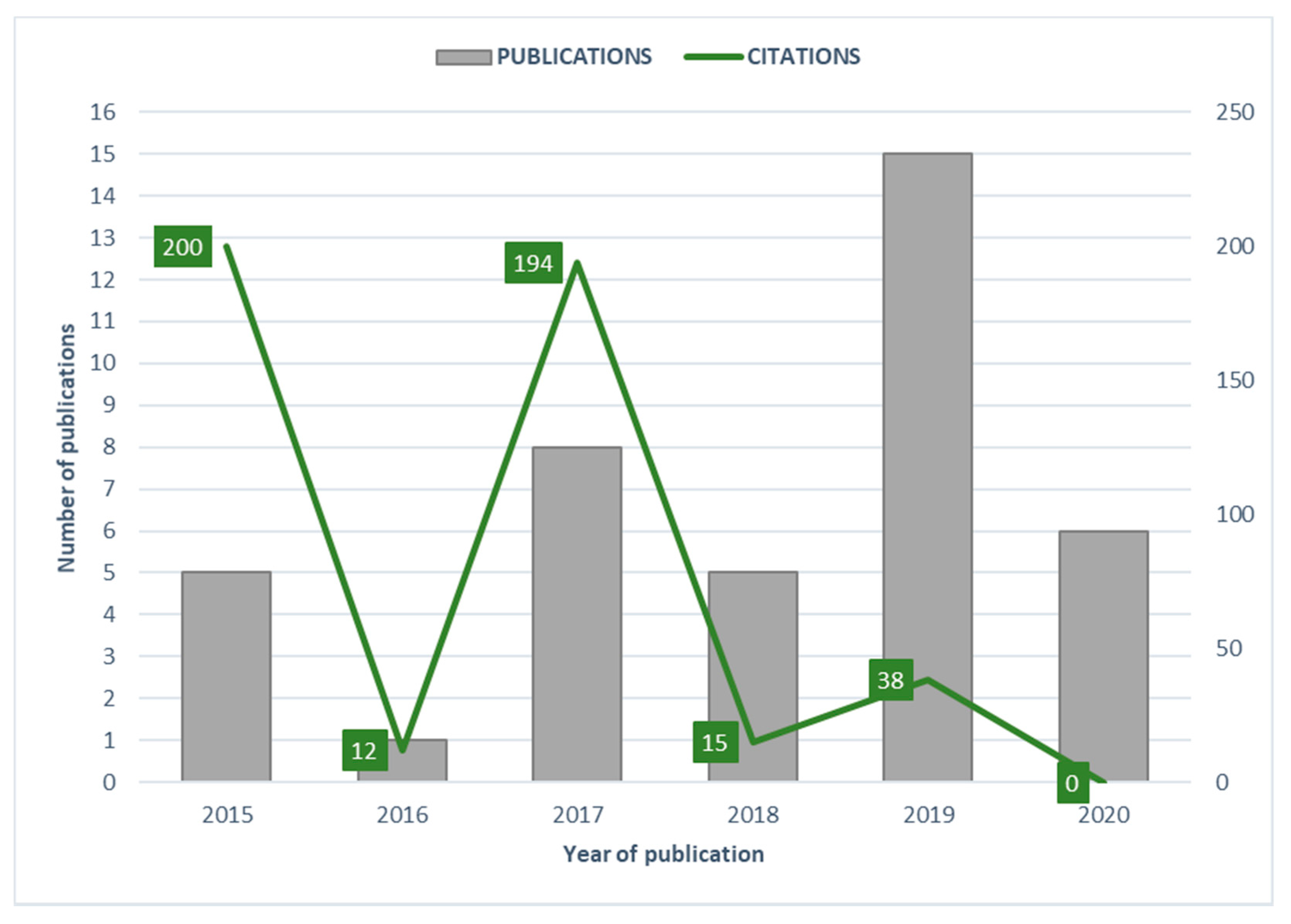

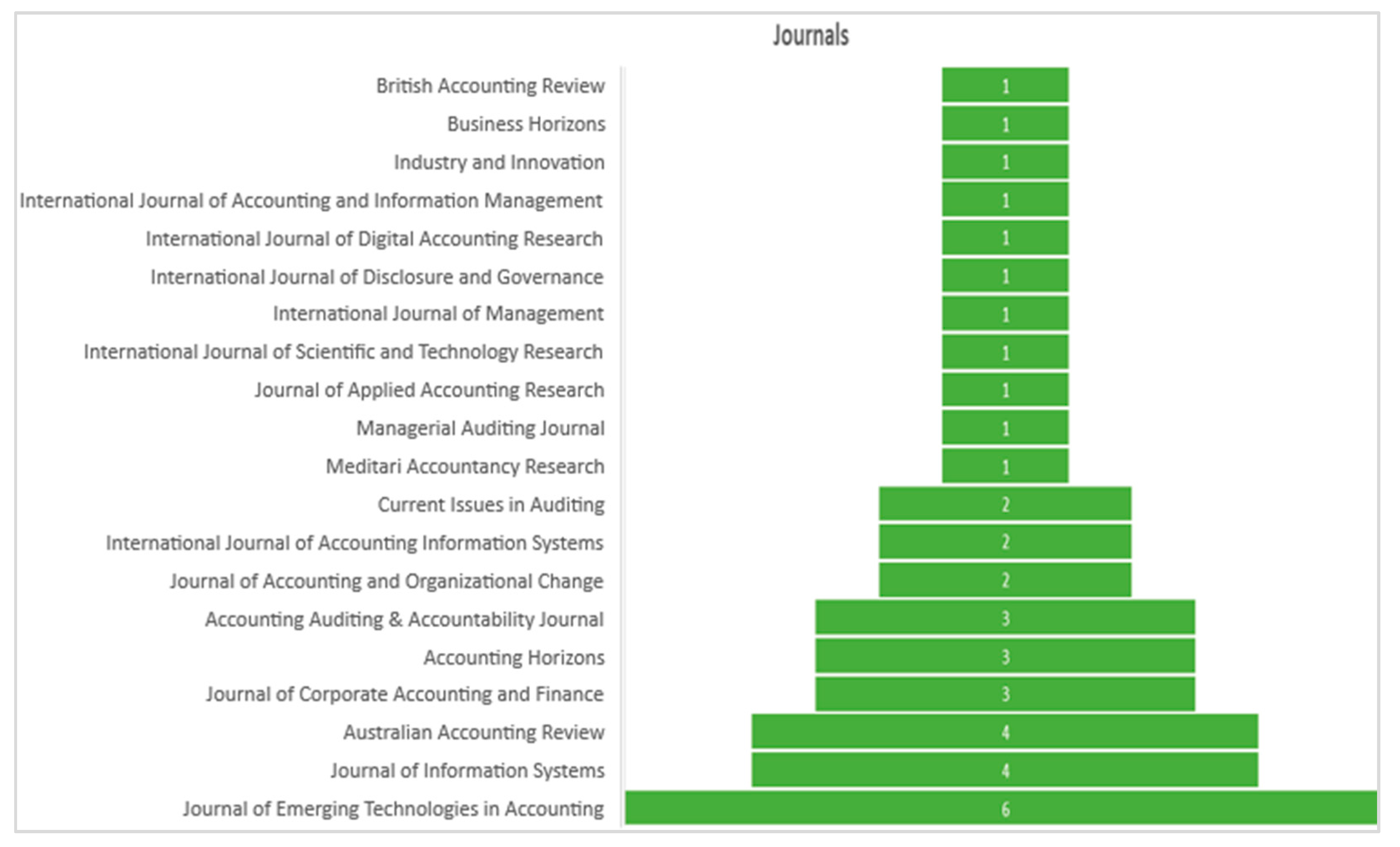

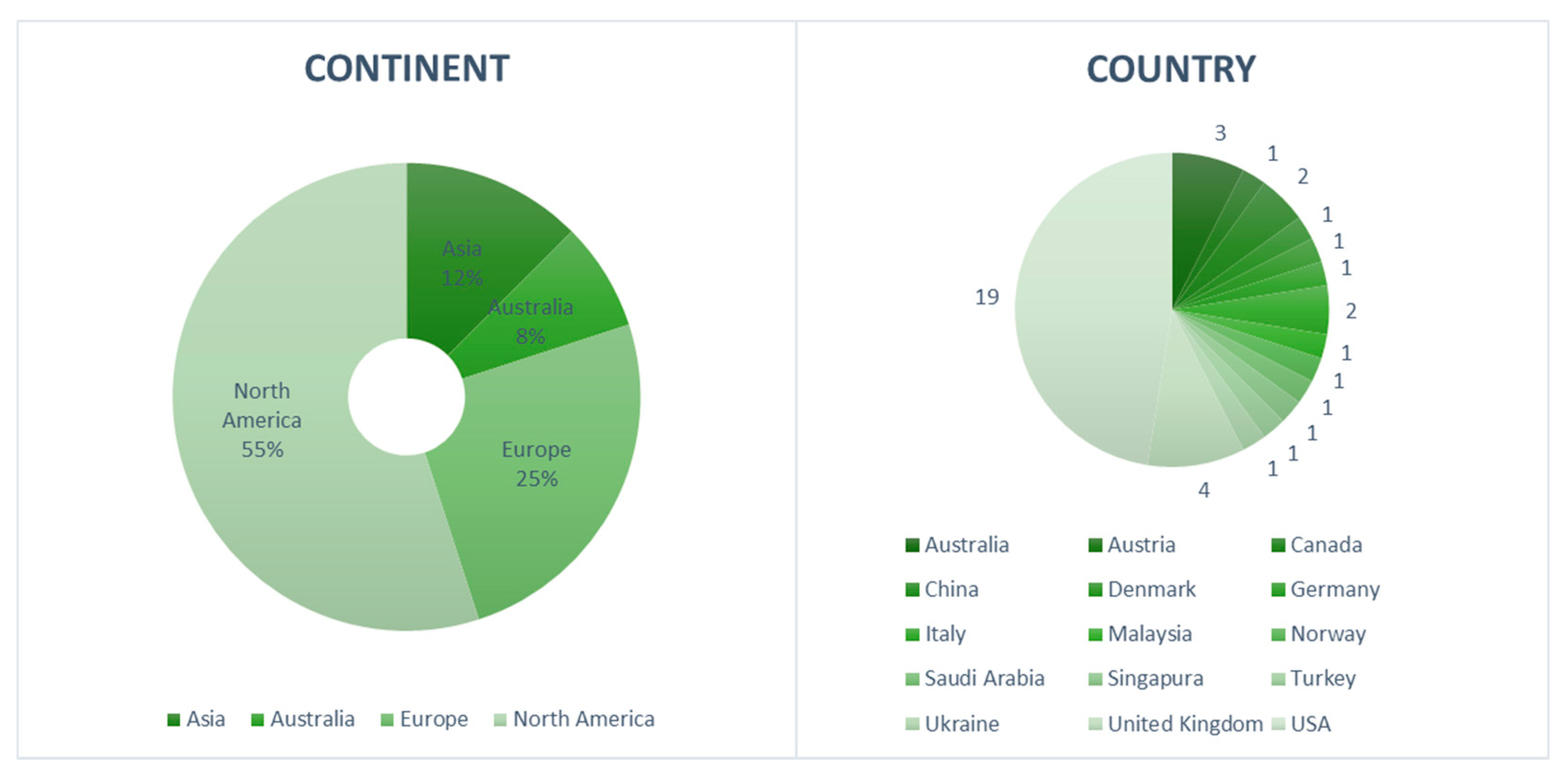

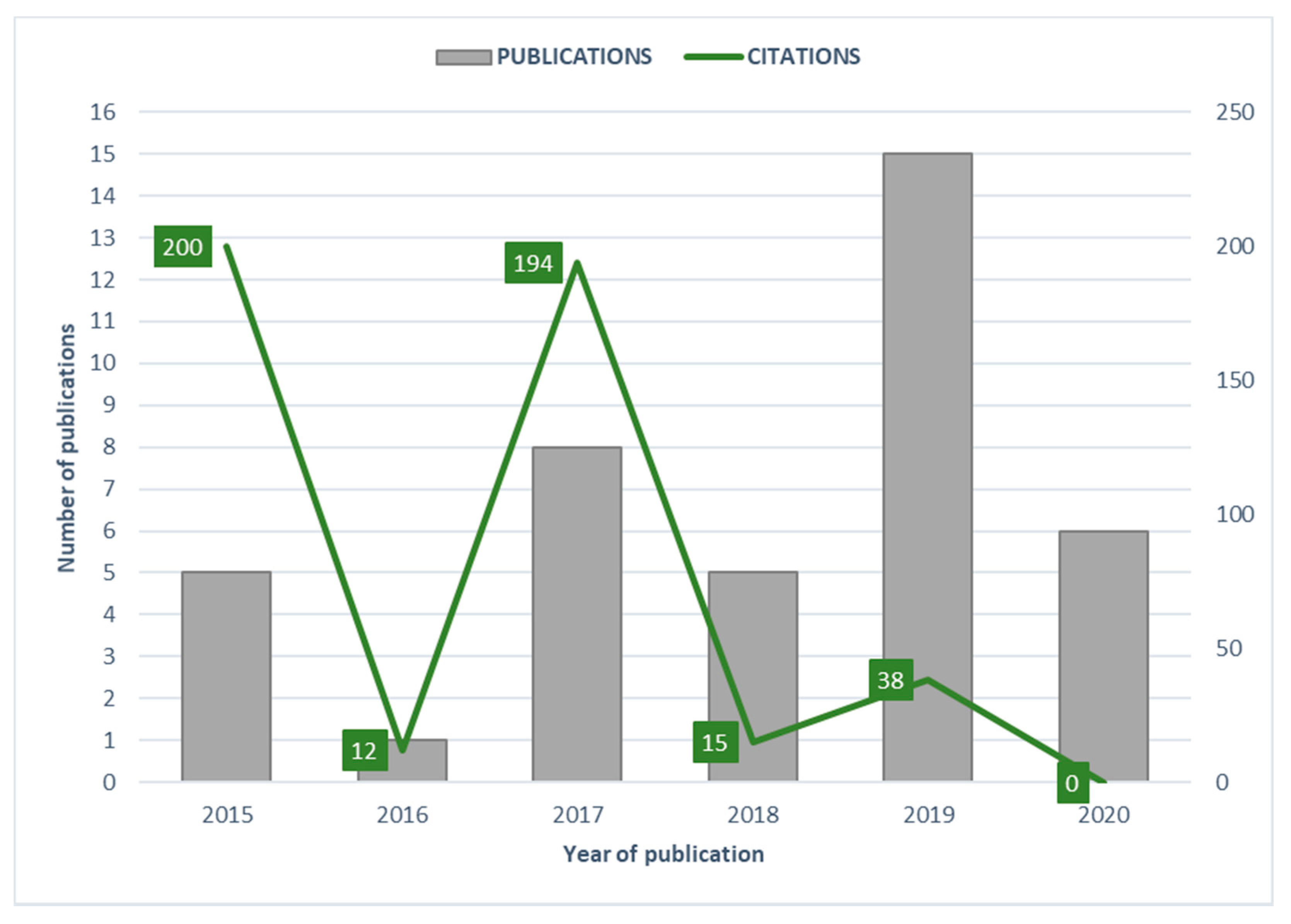

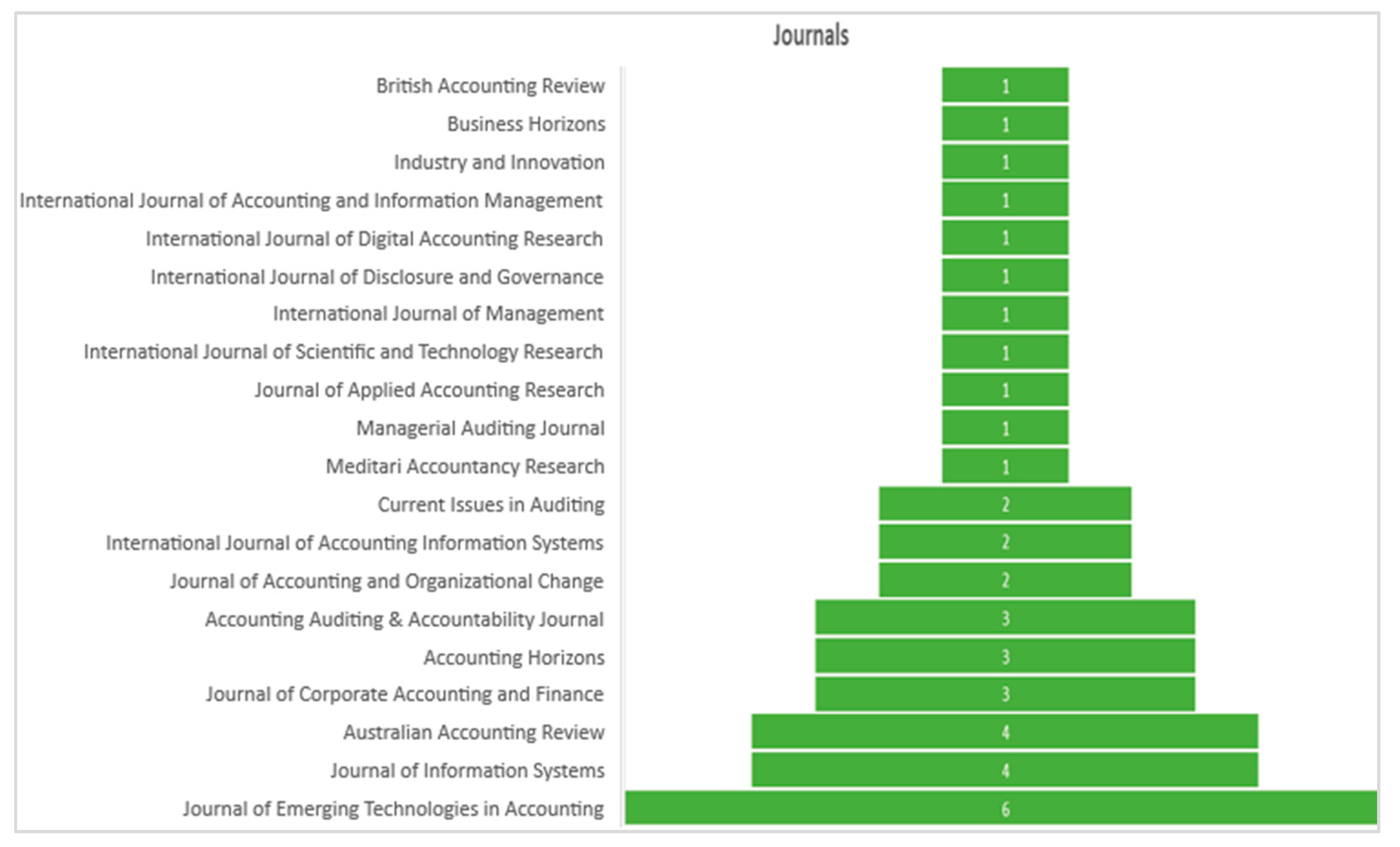

3.1. Descriptive Results

3.2. Content Analysis Results

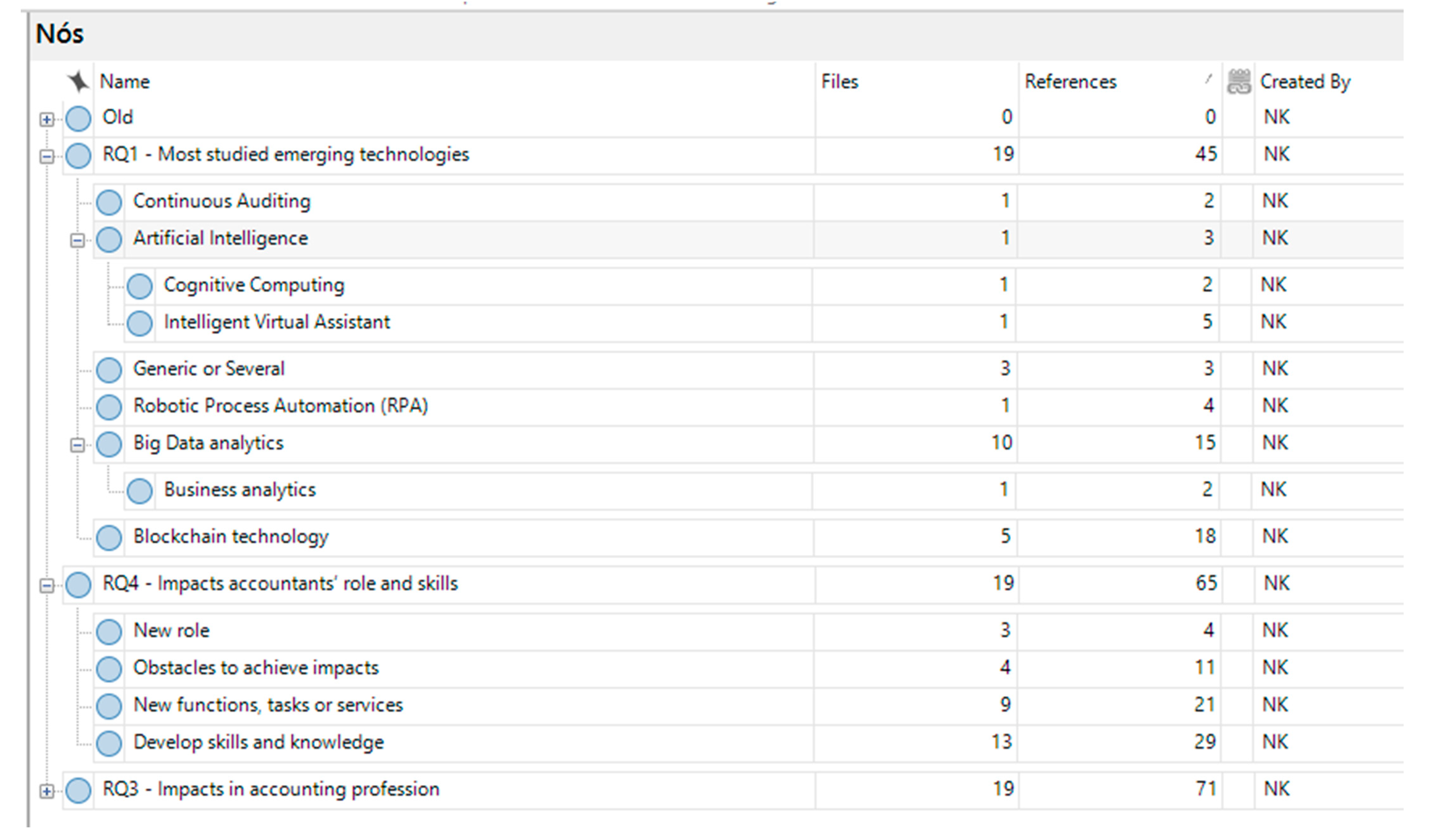

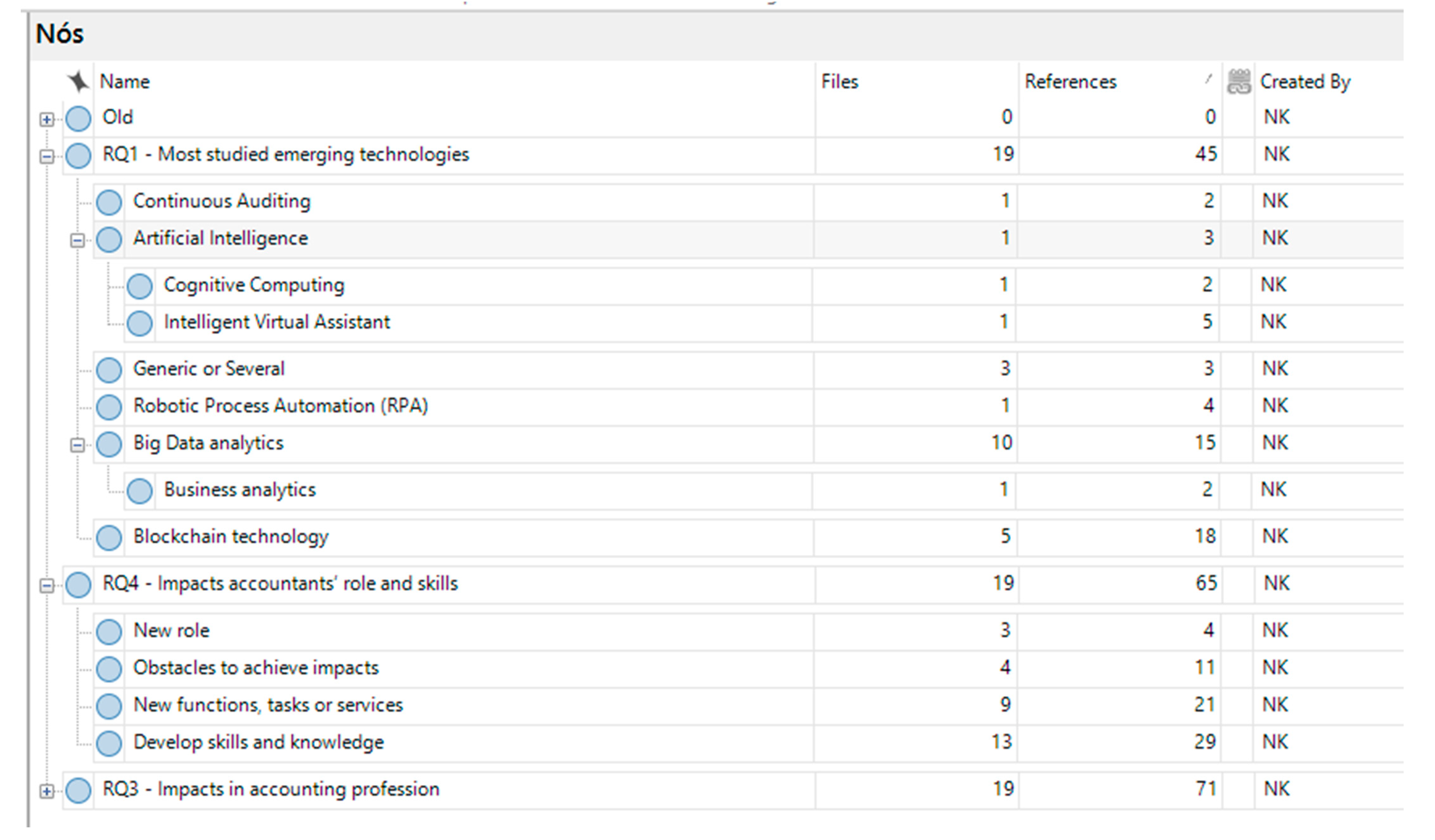

3.2.1. Which Emerging Technologies Are Most Studied Concerning Their Impacts on Accountants’ Role and Skills?

3.2.2. What Research Strategy Did the Papers Use to Identify the Impacts on Accountants’ Role or Skills?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Profession | Emerging Technology | Studies | Research Strategy |

|---|---|---|---|

| Accounting (general) | Artificial intelligence | [48] | Conceptual |

| [54] | Conceptual | ||

| Big data analytics | [47] | Case study | |

| [55] | Conceptual | ||

| [46] | Conceptual | ||

| [56] | Conceptual | ||

| [57] | Conceptual | ||

| [58] | Review | ||

| [59] | Survey | ||

| [60] | Conceptual | ||

| Blockchain technology | [38] | Conceptual | |

| [51] | Conceptual | ||

| [50] | Conceptual | ||

| [52] | Conceptual | ||

| Several | [61] | Conceptual | |

| [62] | Interviews | ||

| [53] | Interviews | ||

| [16] | Review | ||

| [15] | Review | ||

| Auditing | Artificial intelligence | [63] | Conceptual |

| [64] | Conceptual | ||

| Big data analytics | [37] | Conceptual | |

| [65] | Conceptual | ||

| [66] | Review | ||

| [67] | Survey | ||

| Blockchain technology | [68] | Conceptual | |

| [42] | Conceptual | ||

| [39] | Review | ||

| Other | [69] | Case study | |

| Several | [70] | Conceptual | |

| Auditing and Accounting | Artificial intelligence | [71] | Conceptual |

| Big data analytics | [72] | Conceptual | |

| Blockchain technology | [49] | Conceptual | |

| [11] | Review | ||

| Financial Accounting | Several | [73] | Case study |

| Management Accounting | Big data analytics | [74] | Conceptual |

| [75] | Experimental | ||

| [76] | Review | ||

| Other | [77] | Case study | |

| Other | Big data analytics | [78] | Survey |

| Accounting (general)—(47.5%) Financial accounting (2.5%) Management accounting (10%) Auditing (27.5%) Auditing and accounting (10%) Other (2.5%) | Big data analytics (42.5%) Blockchain technology (22.5%) Artificial intelligence (12.5%) Several (17.5%) Other (5%) | Conceptual (57.5%) Review (17.5%) Case study (10%) Experimental (2.5%) Survey (7.5%) Interviews (5%) |

3.2.3. Is Open Innovation an Influencing Factor in Connecting Emerging Technologies and Accountants’ Role and Skills?

3.2.4. What Are the Most Identified Impacts of Emerging Technologies on Accountants’ Role and Skills?

Impacts on General Accountants’ Role

- Work along with intelligent accounting machines, monitoring their performance and results and (eventually) improving their performance;

- Monitor the use of intelligent machines in audit processes and find out the need to adjust the automation tools (more, less, or different);

- Develop new tools or technologies based on AI in conjunction with accounting firms and software houses and support the existing ones.

- Perform tasks that AI-based computers cannot do, such as cultivating internal and external customers, interpreting results for top managers and boards of directors, and so forth;

- Perform accounting tasks that are infrequent and out of the ordinary, for which it is not economically viable to build automated solutions.

Impacts on Auditors’ Role

Impacts on Management Accountant’s Role

Impacts on General Accountants’ Skills

- Seek additional training in business strategy and business models to complement existing accounting knowledge.

- Develop business analytic capabilities.

- Learn to work with the (new) tools developed for big data/scaled for big data contexts, working with extensive structured and unstructured data.

- Understand the basics of programming so that accountants can more easily interact with data and computer scientists and at the same time develop the ability to learn about new technologies emerging in the future.

Impacts on Auditors’ Skills

Impacts on Management Accountants’ Skills

4. Discussion of Results and Implications

4.1. Opportunities, Challenges, and Risks

4.2. Suggestions for Future Research

5. Final Considerations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Author (s) | Year | Title | Journal | Citation |

|---|---|---|---|---|

| Al-Htaybat and von Alberti-Alhtaybat [47] | 2017 | Big Data and corporate reporting: impacts and paradoxes | Accounting Auditing & Accountability Journal | 21 |

| Alles [65] | 2015 | Drivers of the use and facilitators and obstacles of the evolution of big data by the audit profession | Accounting Horizons | 52 |

| Appelbaum, Kogan [74] | 2017 | Impact of business analytics and enterprise systems on managerial accounting | International Journal of Accounting Information Systems | 49 |

| Arnaboldi, Azzone [77] | 2017 | Governing social media: the emergence of hybridized boundary objects | Accounting Auditing & Accountability Journal | 6 |

| Arnaboldi, Busco [58] | 2017 | Accounting, accountability, social media and big data: revolution or hype? | Accounting Auditing & Accountability Journal | 35 |

| Bonyuet [39] | 2020 | Overview and impact of blockchain on auditing | International Journal of Digital Accounting Research | 0 |

| Burns and Igou [63] | 2019 | “Alexa, Write an Audit Opinion”: Adopting Intelligent Virtual Assistants in Accounting Workplaces | Journal of Emerging Technologies in Accounting | 1 |

| Coyne, Coyne [56] | 2018 | Big Data information governance by accountants | International Journal of Accounting and Information Management | 8 |

| Dzuranin and Mălăescu [70] | 2016 | The current state and future direction of IT audit: Challenges and opportunities | Journal of Information Systems | 12 |

| Earley [37] | 2015 | Data analytics in auditing: Opportunities and challenges | Business Horizons | 20 |

| Feung and Thiruchelvam [66] | 2020 | A framework model for continuous auditing in financial statement audits using big data analytics | International Journal of Scientific and Technology Research | 0 |

| Fuller and Markelevich [50] | 2020 | Should accountants care about blockchain? | Journal of Corporate Accounting and Finance | 0 |

| Gardner and Bryson [53] | 2020 | The dark side of the industrialization of accountancy: innovation, commoditization, colonization and competitiveness | Industry and Innovation | 0 |

| Huang and Vasarhelyi [69] | 2019 | Applying robotic process automation (RPA) in auditing: A framework | International Journal of Accounting Information Systems | 0 |

| Huerta and Jensen [55] | 2017 | An accounting information systems perspective on data analytics and big data | Journal of Information Systems | 13 |

| Izmailov, Pilevych [61] | 2020 | Information systems and technologies in accounting and taxation as a means of integration into the digital economy | International Journal of Management | 0 |

| Karajovic, Kim [52] | 2019 | Thinking Outside the Block: Projected Phases of Blockchain Integration in the Accounting Industry | Australian Accounting Review | 6 |

| Kend and Nguyen [62] | 2020 | Big Data Analytics and Other Emerging Technologies: The Impact on the Australian Audit and Assurance Profession | Australian Accounting Review | 0 |

| Kokina and Davenport [45] | 2017 | The emergence of artificial intelligence: How automation is changing auditing | Journal of Emerging Technologies in Accounting | 28 |

| Kokina, Mancha [51] | 2017 | Blockchain: Emergent industry adoption and implications for accounting | Journal of Emerging Technologies in Accounting | 26 |

| Krahel and Titera [72] | 2015 | Consequences of Big Data and Formalization on Accounting and Auditing Standards | Accounting Horizons | 53 |

| Liu, Wu [42] | 2019 | How Will Blockchain Technology Impact Auditing and Accounting: Permissionless versus Permissioned Blockchain | Current Issues in Auditing | 0 |

| Marrone and Hazelton [16] | 2019 | The disruptive and transformative potential of new technologies for accounting, accountants and accountability A review of current literature and call for further research | Meditari Accountancy Research | 0 |

| Marshall and Lambert [48] | 2018 | Cloud-Based Intelligent Accounting Applications: Accounting Task Automation Using I.B.M. Watson Cognitive Computing | Journal of Emerging Technologies in Accounting | 5 |

| Michael and Dixon [67] | 2019 | Audit data analytics of unregulated voluntary disclosures and auditing expectations gap | International Journal of Disclosure and Governance | 1 |

| Moll and Yigitbasioglu [15] | 2019 | The role of internet-related technologies in shaping the work of accountants: New directions for accounting research | British Accounting Review | 6 |

| Nielsen [76] | 2018 | Reflections on the applicability of business analytics for management accounting—and future perspectives for the accountant | Journal of Accounting and Organizational Change | 0 |

| Oesterreich and Teuteberg [75] | 2019 | The role of business analytics in the controllers and management accountants’ competence profiles. An exploratory study on individual-level data | Journal of Accounting and Organizational Change | 1 |

| Perkhofer, Hofer [59] | 2019 | Interactive visualization of big data in the field of accounting A survey of current practice and potential barriers for adoption | Journal of Applied Accounting Research | 5 |

| Pickard and Cokins [57] | 2015 | From bean counters to bean growers: Accountants as data analysts—a customer profitability example | Journal of Information Systems | 3 |

| Rezaee and Wang [78] | 2019 | Relevance of big data to forensic accounting practice and education | Managerial Auditing Journal | 4 |

| Richins, Stapleton [46] | 2017 | Big Data Analytics: Opportunity or Threat for the Accounting Profession? | Journal of Information Systems | 16 |

| Schmitz and Leoni [11] | 2019 | Accounting and Auditing at the Time of Blockchain Technology: A Research Agenda | Australian Accounting Review | 9 |

| Sheldon [68] | 2019 | A primer for information technology general control considerations on a private and permissioned blockchain audit | Current Issues in Auditing | 0 |

| Sutton, Arnold [54] | 2018 | How Much Automation Is Too Much? Keeping the Human Relevant in Knowledge Work | Journal of Emerging Technologies in Accounting | 1 |

| Tan and Low [38] | 2019 | Blockchain as the Database Engine in the Accounting System | Australian Accounting Review | 4 |

| Türegün [73] | 2019 | Impact of technology in financial reporting: The case of Amazon Go | Journal of Corporate Accounting and Finance | 0 |

| Warren, Moffitt [60] | 2015 | How Big Data Will Change Accounting | Accounting Horizons | 72 |

| Yu, Lin [49] | 2018 | Blockchain: The Introduction and Its Application in Financial Accounting | Journal of Corporate Accounting and Finance | 1 |

| Zhang [64] | 2019 | Intelligent process automation in audit | Journal of Emerging Technologies in Accounting | 1 |

Appendix B

References

- Olivier, H. Challenges facing the accountancy profession. Eur. Account. Rev. 2000, 9, 603–624. [Google Scholar] [CrossRef]

- Pazaitis, A. Breaking the Chains of Open Innovation: Post-Blockchain and the Case of Sensorica. Information 2020, 11, 104. [Google Scholar] [CrossRef] [Green Version]

- Chesbrough, H.W. Open Innovation: The New Imperative for Creating and Profiting from Technology; Harvard Business Review Press: Brighton, MA, USA, 2006; p. 272. [Google Scholar]

- Skordoulis, M.; Ntanos, S.; Kyriakopoulos, G.L.; Arabatzis, G.; Galatsidas, S.; Chalikias, M. Environmental Innovation, Open Innovation Dynamics and Competitive Advantage of Medium and Large-Sized Firms. J. Open Innov. Technol. Mark. Complex. 2020, 6, 195. [Google Scholar] [CrossRef]

- Fayyaz, A.; Chaudhry, B.N.; Fiaz, M. Upholding Knowledge Sharing for Organization Innovation Efficiency in Pakistan. J. Open Innov. Technol. Mark. Complex. 2020, 7, 4. [Google Scholar] [CrossRef]

- Belfo, F.P.; Trigo, A. Accounting Information Systems: Tradition and Future Directions. Procedia Technol. 2013, 9, 536–546. [Google Scholar] [CrossRef] [Green Version]

- Arnold, V. The changing technological environment and the future of behavioural research in accounting. Account. Financ. 2018, 58, 315–339. [Google Scholar] [CrossRef]

- Dos Santos, B.L.; Suave, R.; Ferreira, M.M.; Altoé, S.M.L. Profissão contábil em tempos de mudança: Implicações do avanço tecnológico nas atividades em um escritório de contabilidade. Rev. Contab. Control. 2020, 11. [Google Scholar] [CrossRef]

- Taipaleenmäki, J.; Ikäheimo, S. On the convergence of management accounting and financial accounting—the role of information technology in accounting change. Int. J. Account. Inf. Syst. 2013, 14, 321–348. [Google Scholar] [CrossRef]

- Schmitz, J.; Leoni, G. Accounting and Auditing at the Time of Blockchain Technology: A Research Agenda. Aust. Account. Rev. 2019, 29, 331–342. [Google Scholar] [CrossRef]

- Secinaro, S.; Calandra, D.; Biancone, P. Blockchain, trust, and trust accounting: Can blockchain technology substitute trust created by intermediaries in trust accounting? A theoretical examination. Int. J. Manag. Pract. 2021, 14, 129–145. [Google Scholar] [CrossRef]

- George, K.; Patatoukas, P.N. The Blockchain Evolution and Revolution of Accounting. 2020. Available online: https://ssrn.com/abstract=3681654 (accessed on 7 July 2020).

- Carlin, T. Blockchain and the Journey Beyond Double Entry. Aust. Account. Rev. 2019, 29, 305–311. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Marrone, M.; Hazelton, J. The disruptive and transformative potential of new technologies for accounting, accountants and accountability: A review of current literature and call for further research. Med. Account. Res. 2019, 27, 677–694. [Google Scholar] [CrossRef]

- International Federation of Accountants; Association of Accounting Tecnicians. An Illustrative Competency Framework for Accounting Technicians; International Federation of Accountants: New York, NY, USA; Association of Accounting Tecnicians: London, UK, 2019; pp. 1–92. [Google Scholar]

- Institute of Management Accounting. IMA Management Accounting Competency Framework; Institute of Management Accounting: Buffalo, NY, USA, 2019; pp. 1–48. [Google Scholar]

- Association of Chartered Certified Accountants. Future Ready: Accountancy Careers in the 2020s; Association of Chartered Certified Accountants: London, UK, 2020; pp. 1–72. [Google Scholar]

- Demirkan, S.; Demirkan, I.; McKee, A. Blockchain technology in the future of business cyber security and accounting. J. Manag. Anal. 2020, 7, 189–208. [Google Scholar] [CrossRef]

- The Association to Advance Collegiate Schools of Business-International. 2018 Eligibility Procedures and Accreditation Standards for Accounting Accreditation; The Association to Advance Collegiate Schools of Business: Tampa, FL, USA, 2018; pp. 1–35. [Google Scholar]

- Chiu, V.; Liu, Q.; Muehlmann, B.; Baldwin, A.A. A bibliometric analysis of accounting information systems journals and their emerging technologies contributions. Int. J. Account. Inf. Syst. 2019, 32, 24–43. [Google Scholar] [CrossRef]

- Fullana, O.; Ruiz, J. Accounting Information Systems in the Blockchain Era. 2020. Available online: https://ssrn.com/abstract=3517142 (accessed on 7 July 2020).

- Lombardi, R.; Secundo, G. The digital transformation of corporate reporting—A systematic literature review and avenues for future research. Med. Account. Res. 2020. [Google Scholar] [CrossRef]

- Lamboglia, R.; Lavorato, D.; Scornavacca, E.; Za, S. Exploring the relationship between audit and technology. A bibliometric analysis. Med. Account. Res. 2020. [Google Scholar] [CrossRef]

- Wolf, T.; Kuttner, M.; Feldbauer-Durstmüller, B.; Mitter, C. What we know about management accountants’ changing identities and roles—A systematic literature review. J. Account. Organ. Chang. 2020, 16, 311–347. [Google Scholar] [CrossRef]

- Saputro, V.S.; Ritchi, H.; Handoyo, S. Blockchain Disruption on Management Accountant’s Role: Systematic Literature Review. J. Account. Audit. Bus. 2021, 4, 1–13. [Google Scholar] [CrossRef]

- Denyer, D.; Tranfield, D. Producing a systematic review. In The Sage Handbook of Organizational Research Methods; Buchanan, D.A., Bryman, B.A., Eds.; Sage Publications Ltd.: Thousand Oaks, CA, USA, 2009; pp. 671–689. [Google Scholar]

- Coyne, J.G.; Summers, S.L.; Williams, B.; Wood, D.A. Accounting Program Research Rankings by Topical Area and Methodology. Issues Account. Educ. 2010, 25, 631–654. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.-D. Research Analysis on Emerging Technologies in Corporate Accounting. Mathematics 2020, 8, 1589. [Google Scholar] [CrossRef]

- Snyder, H. Literature review as a research methodology: An overview and guidelines. J. Bus. Res. 2019, 104, 333–339. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. Int. J. Surg. 2010, 8, 336–341. [Google Scholar] [CrossRef] [Green Version]

- Liberati, A.; Altman, D.G.; Tetzlaff, J.; Mulrow, C.; Gøtzsche, P.C.; Ioannidis, J.P.A.; Clarke, M.; Devereaux, P.J.; Kleijnen, J.; Moher, D. The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate health care interventions: Explanation and elaboration. PLoS Med. 2009, 6, e1000100. [Google Scholar] [CrossRef] [PubMed]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Shamseer, L.; Tetzlaff, J.M.; Akl, E.A.; Brennan, S.E.; et al. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 2021, 372, n71. [Google Scholar] [CrossRef] [PubMed]

- Gasparyan, A.Y.; Ayvazyan, L.; Kitas, G. Multidisciplinary Bibliographic Databases. J. Korean Med. Sci. 2013, 28, 1270–1275. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Chen, H.; Chiang, R.; Story, V. Business intelligence and analytics: From big data to big impact. MIS Q. 2012, 36, 1165–1188. [Google Scholar] [CrossRef]

- Gartner, I.T. Glossary: Big Data. 2020. Available online: https://www.gartner.com/en/information-technology/glossary/big-data (accessed on 15 March 2021).

- Earley, C. Data analytics in auditing: Opportunities and challenges. Bus. Horiz. 2015, 58, 493–500. [Google Scholar] [CrossRef]

- Tan, B.S.; Low, K.Y. Blockchain as the Database Engine in the Accounting System. Aust. Account. Rev. 2019, 29, 312–318. [Google Scholar] [CrossRef]

- Bonyuet, D. Overview and Impact of Blockchain on Auditing. Int. J. Digit. Account. Res. 2020, 20, 31–43. [Google Scholar] [CrossRef]

- Zheng, Z.; Xie, S.; Dai, H.-N.; Chen, X.; Wang, H. Blockchain challenges and opportunities: A survey. Int. J. Web Grid Serv. 2018, 14, 352–375. [Google Scholar] [CrossRef]

- Swan, M. Blockchain: Blueprints for a New Economie; O’Reilly Media: Newton, MA, USA, 2015; Volume 293, p. 129. [Google Scholar]

- Liu, M.; Wu, K.; Xu, J.J. How Will Blockchain Technology Impact Auditing and Accounting: Permissionless versus Permissioned Blockchain. Curr. Issues Audit. 2019, 13, A19–A29. [Google Scholar] [CrossRef] [Green Version]

- Schneider, G.; Dai, J.; Janvrin, D.J.; Ajayi, K.; Raschke, R.L. Infer, Predict, and Assure: Accounting Opportunities in Data Analytics. Account. Horiz. 2015, 29, 719–742. [Google Scholar] [CrossRef]

- Tschakert, N.; Kokina, J.; Kozlowski, S.; Vasarhelyi, M. The next frontier in data analytics. J. Account. 2016, 222, 58–63. [Google Scholar]

- Kokina, J.; Davenport, T.H. The Emergence of Artificial Intelligence: How Automation is Changing Auditing. J. Emerg. Technol. Account. 2017, 14, 115–122. [Google Scholar] [CrossRef]

- Richins, G.; Stapleton, A.; Stratopoulos, T.; Wong, C. Big Data Analytics: Opportunity or Threat for the Accounting Profession? J. Inf. Syst. 2017, 31, 63–79. [Google Scholar] [CrossRef]

- Al-Htaybat, K.; Von Alberti-Alhtaybat, L. Big Data and corporate reporting: Impacts and paradoxes. Account. Audit. Account. J. 2017, 30, 850–873. [Google Scholar] [CrossRef]

- Marshall, T.E.; Lambert, S.L. Cloud-Based Intelligent Accounting Applications: Accounting Task Automation Using IBM Watson Cognitive Computing. J. Emerg. Technol. Account. 2018, 15, 199–215. [Google Scholar] [CrossRef]

- Yu, T.; Lin, Z.; Tang, Q. Blockchain: The Introduction and Its Application in Financial Accounting. J. Corp. Account. Financ. 2018, 29, 37–47. [Google Scholar] [CrossRef]

- Fuller, S.H.; Markelevich, A. Should accountants care about blockchain? J. Corp. Account. Financ. 2020, 31, 34–46. [Google Scholar] [CrossRef]

- Kokina, J.; Mancha, R.; Pachamanova, D. Blockchain: Emergent Industry Adoption and Implications for Accounting. J. Emerg. Technol. Account. 2017, 14, 91–100. [Google Scholar] [CrossRef]

- Karajovic, M.; Kim, H.M.; Laskowski, M. Thinking Outside the Block: Projected Phases of Blockchain Integration in the Accounting Industry. Aust. Account. Rev. 2019, 29, 319–330. [Google Scholar] [CrossRef]

- Gardner, E.C.; Bryson, J.R. The dark side of the industrialisation of accountancy: Innovation, commoditization, colonization and competitiveness. Ind. Innov. 2021, 28, 42–57. [Google Scholar] [CrossRef]

- Sutton, S.G.; Arnold, V.; Holt, M. How Much Automation Is Too Much? Keeping the Human Relevant in Knowledge Work. J. Emerg. Technol. Account. 2018, 15, 15–25. [Google Scholar] [CrossRef]

- Huerta, E.; Jensen, S. An Accounting Information Systems Perspective on Data Analytics and Big Data. J. Inf. Syst. 2017, 31, 101–114. [Google Scholar] [CrossRef]

- Coyne, E.M.; Coyne, J.G.; Walker, K.B. Big Data information governance by accountants. Int. J. Account. Inf. Manag. 2018, 26, 153–170. [Google Scholar] [CrossRef] [Green Version]

- Pickard, M.D.; Cokins, G. From Bean Counters to Bean Growers: Accountants as Data Analysts—A Customer Profitability Example. J. Inf. Syst. 2015, 29, 151–164. [Google Scholar] [CrossRef]

- Arnaboldi, M.; Busco, C.; Cuganesan, S. Accounting, accountability, social media and big data: Revolution or hype? Account. Audit. Account. J. 2017, 30, 762–776. [Google Scholar] [CrossRef] [Green Version]

- Perkhofer, L.M.; Hofer, P.; Walchshofer, C.; Plank, T.; Jetter, H.-C. Interactive visualization of big data in the field of accounting. J. Appl. Account. Res. 2019, 20, 497–525. [Google Scholar] [CrossRef]

- Warren, J.D.; Moffitt, K.C.; Byrnes, P. How Big Data Will Change Accounting. Account. Horiz. 2015, 29, 397–407. [Google Scholar] [CrossRef]

- Izmailov, Y.; Pilevych, D.; Shevtsiv, L.; Petlenko, Y.; Driha, O.; Lagun, A. Information systems and technologies in accounting and taxation as a means of integration into the digital economy. Int. J. Manag. 2020, 11, 122–131. [Google Scholar] [CrossRef]

- Kend, M.; Nguyen, L.A. Big Data Analytics and Other Emerging Technologies: The Impact on the Australian Audit and Assurance Profession. Aust. Account. Rev. 2020, 30, 269–282. [Google Scholar] [CrossRef]

- Burns, M.B.; Igou, A. “Alexa, Write an Audit Opinion”: Adopting Intelligent Virtual Assistants in Accounting Workplaces. J. Emerg. Technol. Account. 2019, 16, 81–92. [Google Scholar] [CrossRef]

- Zhang, C. Intelligent Process Automation in Audit. J. Emerg. Technol. Account. 2019, 16, 69–88. [Google Scholar] [CrossRef]

- Alles, M.G. Drivers of the Use and Facilitators and Obstacles of the Evolution of Big Data by the Audit Profession. Account. Horiz. 2015, 29, 439–449. [Google Scholar] [CrossRef]

- Feung, J.L.C.; Thiruchelvam, I.V. A framework model for continuous auditing in financial statement audits using big data analytics. Int. J. Sci. Technol. Res. 2020, 9, 3416–3434. [Google Scholar]

- Michael, A.; Dixon, R. Audit data analytics of unregulated voluntary disclosures and auditing expectations gap. Int. J. Discl. Gov. 2019, 16, 188–205. [Google Scholar] [CrossRef]

- Sheldon, M.D. A Primer for Information Technology General Control Considerations on a Private and Permissioned Blockchain Audit. Curr. Issues Audit. 2019, 13, A15–A29. [Google Scholar] [CrossRef] [Green Version]

- Huang, F.; Vasarhelyi, M.A. Applying robotic process automation (RPA) in auditing: A framework. Int. J. Account. Inf. Syst. 2019, 35, 100433. [Google Scholar] [CrossRef]

- Dzuranin, A.C.; Mălăescu, I. The Current State and Future Direction of IT Audit: Challenges and Opportunities. J. Inf. Syst. 2015, 30, 7–20. [Google Scholar] [CrossRef]

- Kokina, J.; Pachamanova, D.; Corbett, A. The role of data visualization and analytics in performance management: Guiding entrepreneurial growth decisions. J. Account. Educ. 2017, 38, 50–62. [Google Scholar] [CrossRef]

- Krahel, J.P.; Titera, W.R. Consequences of Big Data and Formalization on Accounting and Auditing Standards. Account. Horiz. 2015, 29, 409–422. [Google Scholar] [CrossRef]

- Türegün, N. Impact of technology in financial reporting: The case of Amazon Go. J. Corp. Account. Finance 2019, 30, 90–95. [Google Scholar] [CrossRef]

- Appelbaum, D.; Kogan, A.; Vasarhelyi, M.; Yan, Z. Impact of business analytics and enterprise systems on managerial accounting. Int. J. Account. Inf. Syst. 2017, 25, 29–44. [Google Scholar] [CrossRef]

- Oesterreich, T.D.; Teuteberg, F. The role of business analytics in the controllers and management accountants’ competence profiles: An exploratory study on individual-level data. J. Account. Organ. Chang. 2019, 15, 330–356. [Google Scholar] [CrossRef]

- Nielsen, S. Reflections on the applicability of business analytics for management accounting—And future perspectives for the accountant. J. Account. Organ. Chang. 2018, 14, 167–187. [Google Scholar] [CrossRef]

- Arnaboldi, M.; Azzone, G.; Sidorova, Y. Governing social media: The emergence of hybridised boundary objects. Account. Audit. Account. J. 2017, 30, 821–849. [Google Scholar] [CrossRef]

- Rezaee, Z.; Wang, J. Relevance of big data to forensic accounting practice and education. Manag. Audit. J. 2019, 34, 268–288. [Google Scholar] [CrossRef]

- Crawford, A. What Is DevOps? 2021. Available online: https://www.ibm.com/cloud/learn/devops-a-complete-guide (accessed on 4 June 2021).

- Foundation, T.L. Hyperledger Members. 2021. Available online: https://www.hyperledger.org/ (accessed on 4 June 2021).

- Enterprise Ethereum Alliance. Enterprise Ethereum Alliance. 2021. Available online: https://entethalliance.org/enterprise-ethereum-alliance-launches/ (accessed on 4 June 2021).

| I/E Criteria | Reason for Inclusion/Exclusion | |

|---|---|---|

| Exclusion criteria: | ||

| No full text | NFT | No full text. |

| Not related | NR | The article does not deal with the accounting profession, accountants’ role or skills, and emerging technologies. |

| Loosely related | LR-1 | The article addresses the accountants’ role or skills from a student’s or educator’s perspective. |

| LR-2 | The article addresses the accountant’s role or skills or the accounting profession without making a connection with emerging technologies. | |

| LR-3 | The article addresses emerging technologies without making a connection with the accountants’ role or skills or with the accounting profession. | |

| Inclusion criteria: | ||

| Partially related | PR | The article focuses on the impacts of emerging technologies on accounting. |

| Totally related | TR | The article focuses on the impacts of emerging technologies on accountants’ role and skills. |

| Technology | Innovation | Partnerships, Collaboration, and Alliances | Total |

|---|---|---|---|

| Artificial intelligence | 1 | 2 | 3 |

| Big data analytics | 3 | 3 | 6 |

| Blockchain technology | 2 | 4 | 6 |

| Other | 1 | 1 | |

| Several | 4 | 4 | |

| 11 | 9 | 20 |

| Role | Studies | |

|---|---|---|

| Emphasis on judgment | 4 | [37,38,49,62] |

| Advisory functions | 3 | [11,16,42] |

| Use data analytics | 3 | [37,39,76] |

| Blockchain implementation | 2 | [11,42] |

| Modify audit procedures | 1 | [39] |

| Information governance | 1 | [56] |

| Policy setter/validator | 1 | [38] |

| Role | Studies | |

|---|---|---|

| Analytical skills | 7 | [37,46,47,55,57,75,76] |

| Basic knowledge of ET | 4 | [11,46,53,75] |

| Creativity and openness | 3 | [47,55,76] |

| Communication skills | 3 | [47,55,76] |

| Teamwork skills | 2 | [56,76] |

| Systemic thinking | 1 | [39] |

| Accounting Area | Future Research Suggestions |

|---|---|

| I—Accounting (General) | |

| Artificial Intelligence |

|

| Big Data Analytics |

|

| Blockchain Technology |

|

| Several |

|

| II—Auditing | |

| Artificial Intelligence |

|

| Big Data Analytics |

|

| Blockchain Technology |

|

| III—Auditing and Accounting | |

| Artificial Intelligence |

|

| Blockchain Technology |

|

| Several |

|

| IV—Management Accounting | |

| Big Data Analytics |

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kroon, N.; Alves, M.d.C.; Martins, I. The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. J. Open Innov. Technol. Mark. Complex. 2021, 7, 163. https://doi.org/10.3390/joitmc7030163

Kroon N, Alves MdC, Martins I. The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(3):163. https://doi.org/10.3390/joitmc7030163

Chicago/Turabian StyleKroon, Nanja, Maria do Céu Alves, and Isabel Martins. 2021. "The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 3: 163. https://doi.org/10.3390/joitmc7030163

APA StyleKroon, N., Alves, M. d. C., & Martins, I. (2021). The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. Journal of Open Innovation: Technology, Market, and Complexity, 7(3), 163. https://doi.org/10.3390/joitmc7030163