Emerging Technologies’ Contribution to the Digital Transformation in Accountancy Firms

Abstract

1. Introduction

2. Literature Review

3. Methodology

3.1. Research Questions Development

- What is the status of the academic literature in regard to the main technologies digitalizing the accounting profession? The aim of the first question (R.Q.1.) is to provide a critical and analytical analysis of the existing literature.

- How are the emerging technologies, separately or as part of an ecosystem, impacting the accountancy organizations? The second question (R.Q.2.) synthesizes the present implications for education, practice, policy, and/or regulation.

3.2. Data Collection

3.3. Data Sampling

3.4. Data Reliability

3.5. Data Coding and Interpretation

4. Results

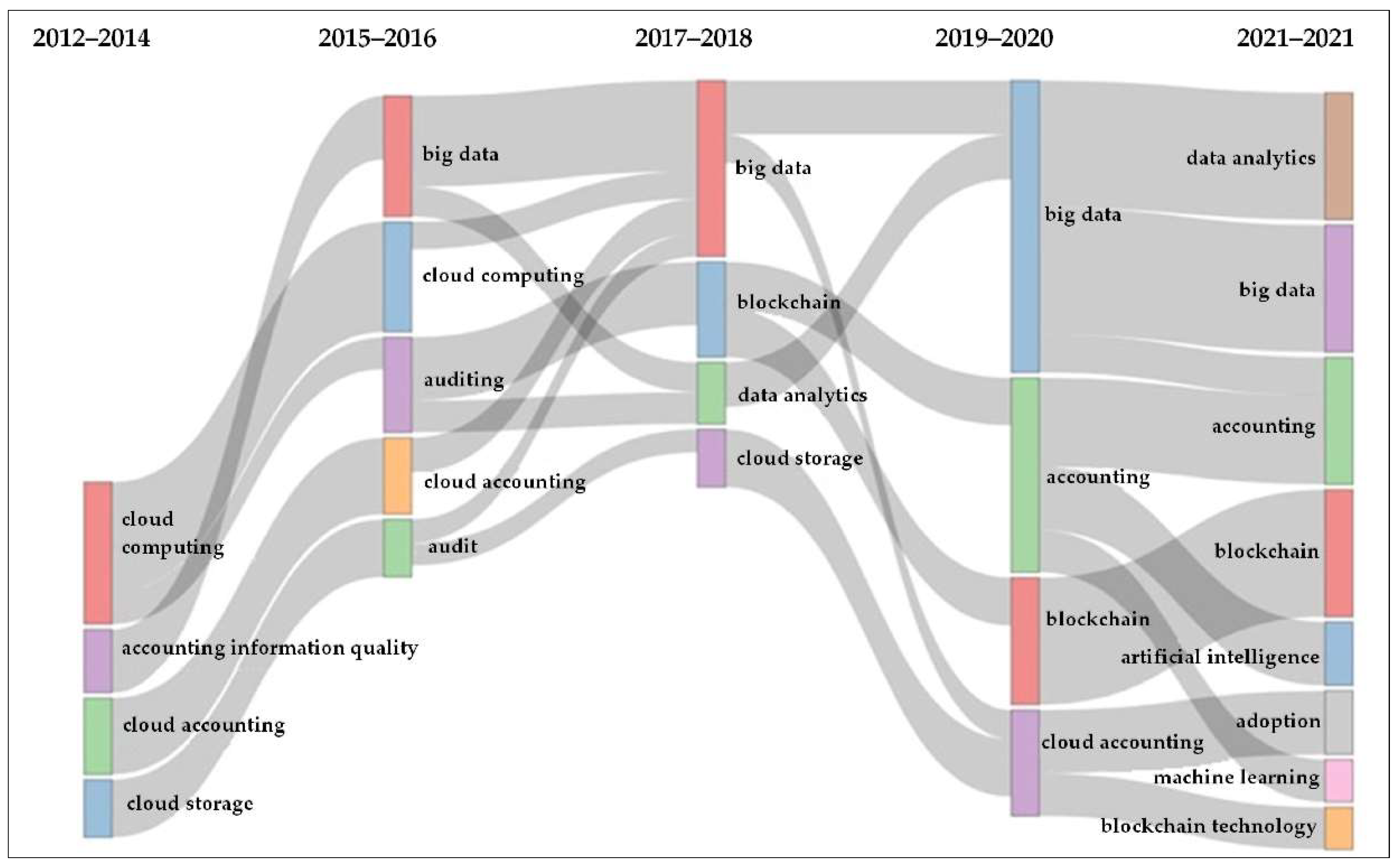

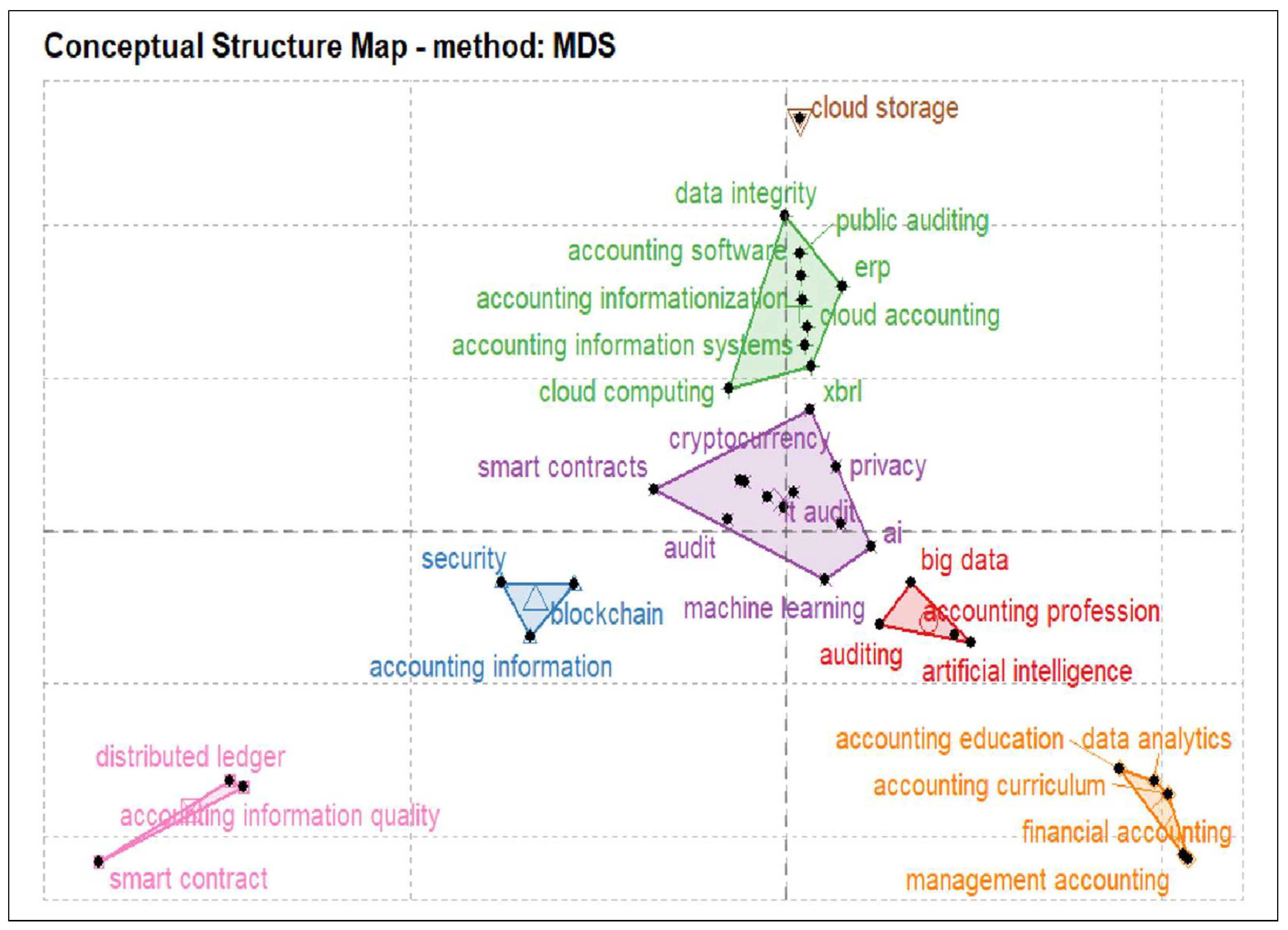

4.1. Quantitative Results—R.Q.1

4.2. Qualitative Results

4.2.1. Artificial Intelligence—AI

4.2.2. Blockchain Technology—BCT

4.2.3. Cloud

4.2.4. Big Data—Governance and Analytics

4.2.5. Cybersecurity

5. Discussions

- How regulators can respond in front of rapid technological development.

- How companies can face technological progress in a more effective way.

- How the daily activities of the firms will probably change.

- How the role and skills of the practitioners are expected to evolve.

5.1. Implications for Regulators

5.2. Implications for Firms

5.3. Implications for Daily Tasks

5.4. Implications for Practitioners

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Agrifoglio, R.; de Gennaro, D. New Ways of Working through Emerging Technologies: A Meta-Synthesis of the Adoption of Blockchain in the Accountancy Domain. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 836–850. [Google Scholar] [CrossRef]

- Bhimani, A.; Willcocks, L. Digitisation, ‘Big Data’ and the Transformation of Accounting Information. Account. Bus. Res. 2014, 44, 469–490. [Google Scholar] [CrossRef]

- Braccini, A.; Margherita, E. Exploring Organizational Sustainability of Industry 4.0 under the Triple Bottom Line: The Case of a Manufacturing Company. Sustainability 2018, 11, 36. [Google Scholar] [CrossRef]

- Schwab, K. The Fourth Industrial Revolution: What It Means, How to Respond; Crown Publishing Group: New York, NY, USA, 2017. [Google Scholar]

- Savastano, M.; Amendola, C.; Bellini, F.; D’Ascenzo, F. Contextual Impacts on Industrial Processes Brought by the Digital Transformation of Manufacturing: A Systematic Review. Sustainability 2019, 11, 891. [Google Scholar] [CrossRef]

- Pînzaru, F.; Dima, A.M.; Zbuchea, A.; Vereș, Z. Adopting Sustainability and Digital Transformation in Business in Romania: A Multifaceted Approach in the Context of the Just Transition. Amfiteatru Econ. 2022, 24, 28–45. [Google Scholar] [CrossRef]

- Tiron-Tudor, A.; Deliu, D. Big Data’s Disruptive Effect on Job Profiles: Management Accountants’ Case Study. J. Risk Financ. Manag. 2021, 14, 376. [Google Scholar] [CrossRef]

- Tiron-Tudor, A.; Deliu, D.; Farcane, N.; Dontu, A. Managing Change with and through Blockchain in Accountancy Organizations: A Systematic Literature Review. J. Organ. Chang. Manag. 2021, 34, 477–506. [Google Scholar] [CrossRef]

- Türegün, N. Impact of Technology in Financial Reporting: The Case of Amazon Go. J. Corp. Account. Financ. 2019, 30, 90–95. [Google Scholar] [CrossRef]

- Zhang, C. Intelligent Process Automation in Audit. J. Emerg. Technol. Account. 2019, 16, 69–88. [Google Scholar] [CrossRef]

- Leitner-Hanetseder, S.; Lehner, O.M.; Eisl, C.; Forstenlechner, C. A Profession in Transition: Actors, Tasks and Roles in AI-Based Accounting. J. Appl. Account. Res. 2021, 22, 539–556. [Google Scholar] [CrossRef]

- Cong, Y.; Du, H.; Vasarhelyi, M.A. Technological Disruption in Accounting and Auditing. J. Emerg. Technol. Account. 2018, 15, 1–10. [Google Scholar] [CrossRef]

- Qasim, A.; Kharbat, F.F. Blockchain Technology, Business Data Analytics, and Artificial Intelligence: Use in the Accounting Profession and Ideas for Inclusion into the Accounting Curriculum. J. Emerg. Technol. Account. 2020, 17, 107–117. [Google Scholar] [CrossRef]

- Zhang, C.; Dai, J.; Vasarhelyi, M.A. The Impact of Disruptive Technologies on Accounting and Auditing Education. How Should the Profession Adapt? CPA J. 2018, 88, 20–26. [Google Scholar]

- Damerji, H.; Salimi, A. Mediating Effect of Use Perceptions on Technology Readiness and Adoption of Artificial Intelligence in Accounting. Account. Educ. 2021, 30, 107–130. [Google Scholar] [CrossRef]

- Pimentel, E.; Boulianne, E. Blockchain in Accounting Research and Practice: Current Trends and Future Opportunities. Account. Perspect. 2020, 19, 325–361. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The Role of Internet-Related Technologies in Shaping the Work of Accountants: New Directions for Accounting Research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Kroon, N.; Alves, M.D.C.; Martins, I. The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. J. Open Innov. Technol. Mark. Complex. 2021, 7, 163. [Google Scholar] [CrossRef]

- Fereday, J.; Muir-Cochrane, E. Demonstrating Rigor Using Thematic Analysis: A Hybrid Approach of Inductive and Deductive Coding and Theme Development. Int. J. Qual. Methods 2006, 5, 80–92. [Google Scholar] [CrossRef]

- Kiger, M.E.; Varpio, L. Thematic Analysis of Qualitative Data: AMEE Guide No. 131. Med. Teach. 2020, 42, 846–854. [Google Scholar] [CrossRef]

- Thorne, S. Data Analysis in Qualitative Research. Evid. Based Nurs. 2000, 3, 68–70. [Google Scholar] [CrossRef]

- Tuckett, A.G. Applying Thematic Analysis Theory to Practice: A Researcher’s Experience. Contemp. Nurse 2005, 19, 75–87. [Google Scholar] [CrossRef] [PubMed]

- Bartolacci, F.; Caputo, A.; Soverchia, M. Sustainability and Financial Performance of Small and Medium Sized Enterprises: A Bibliometric and Systematic Literature Review. Bus. Strat. Environ. 2020, 29, 1297–1309. [Google Scholar] [CrossRef]

- Chawla, R.N.; Goyal, P. Emerging Trends in Digital Transformation: A Bibliometric Analysis. Benchmarking Int. J. 2022, 29, 1069–1112. [Google Scholar] [CrossRef]

- Cricelli, L.; Strazzullo, S. The Economic Aspect of Digital Sustainability: A Systematic Review. Sustainability 2021, 13, 8241. [Google Scholar] [CrossRef]

- Pizzi, S.; Caputo, A.; Corvino, A.; Venturelli, A. Management Research and the UN Sustainable Development Goals (SDGs): A Bibliometric Investigation and Systematic Review. J. Clean. Prod. 2020, 276, 124033. [Google Scholar] [CrossRef]

- Aria, M.; Cuccurullo, C. Bibliometrix: An R-Tool for Comprehensive Science Mapping Analysis. J. Informetr. 2017, 11, 959–975. [Google Scholar] [CrossRef]

- Yigitbasioglu, O.M. External Auditors’ Perceptions of Cloud Computing Adoption in Australia. Int. J. Account. Inf. Syst. 2015, 18, 46–62. [Google Scholar] [CrossRef]

- Ahmad, F. A Systematic Review of the Role of Big Data Analytics in Reducing the Influence of Cognitive Errors on the Audit Judgement. Rev. Contab. 2019, 22, 187–202. [Google Scholar] [CrossRef]

- Gepp, A.; Linnenluecke, M.K.; O’Neill, T.J.; Smith, T. Big Data Techniques in Auditing Research and Practice: Current Trends and Future Opportunities. J. Account. Lit. 2018, 40, 102–115. [Google Scholar] [CrossRef]

- Brown-Liburd, H.; Issa, H.; Lombardi, D. Behavioral Implications of Big Data’s Impact on Audit Judgment and Decision Making and Future Research Directions. Account. Horiz. 2015, 29, 451–468. [Google Scholar] [CrossRef]

- Ferri, L.; Spanò, R.; Ginesti, G.; Theodosopoulos, G. Ascertaining Auditors’ Intentions to Use Blockchain Technology: Evidence from the Big 4 Accountancy Firms in Italy. Meditari Account. Res. 2020, 29, 1063–1087. [Google Scholar] [CrossRef]

- Cleary, P.; Quinn, M. Intellectual Capital and Business Performance: An Exploratory Study of the Impact of Cloud-Based Accounting and Finance Infrastructure. J. Intellect. Cap. 2016, 17, 255–278. [Google Scholar] [CrossRef]

- Munoko, I.; Brown-Liburd, H.L.; Vasarhelyi, M. The Ethical Implications of Using Artificial Intelligence in Auditing. J. Bus. Ethics 2020, 167, 209–234. [Google Scholar] [CrossRef]

- Islam, M.S.; Farah, N.; Stafford, T.F. Factors Associated with Security/Cybersecurity Audit by Internal Audit Function: An International Study. Manag. Audit. J. 2018, 33, 377–409. [Google Scholar] [CrossRef]

- Austin, A.A.; Carpenter, T.D.; Christ, M.H.; Nielson, C.S. The Data Analytics Journey: Interactions Among Auditors, Managers, Regulation, and Technology *. Contemp. Account. Res. 2021, 38, 1888–1924. [Google Scholar] [CrossRef]

- Yau-Yeung, D.; Yigitbasioglu, O.; Green, P. Cloud Accounting Risks and Mitigation Strategies: Evidence from Australia. Account. Forum 2020, 44, 421–446. [Google Scholar] [CrossRef]

- Issa, H.; Sun, T.; Vasarhelyi, M.A. Research Ideas for Artificial Intelligence in Auditing: The Formalization of Audit and Workforce Supplementation. J. Emerg. Technol. Account. 2016, 13, 1–20. [Google Scholar] [CrossRef]

- Lee, C.S.; Tajudeen, F.P. Usage and Impact of Artificial Intelligence on Accounting: 213 Evidence from Malaysian Organisations. Asian J. Bus. Account. 2020, 13, 213–240. [Google Scholar] [CrossRef]

- Avelar, E.A.; Jordão, R.V.D.; Ferreira, G.M.C.; da Silva, B.N.E.R. Artificial Intelligence to Support Management Accounting and Control Systems: An Analysis of App-Based Transportation Companies. SG J. 2021, 16, 59–64. [Google Scholar] [CrossRef]

- Losbichler, H.; Lehner, O.M. Limits of Artificial Intelligence in Controlling and the Ways Forward: A Call for Future Accounting Research. J. Appl. Account. Res. 2021, 22, 365–382. [Google Scholar] [CrossRef]

- Kokina, J.; Davenport, T.H. The Emergence of Artificial Intelligence: How Automation Is Changing Auditing. J. Emerg. Technol. Account. 2017, 14, 115–122. [Google Scholar] [CrossRef]

- Hu, K.-H.; Chen, F.-H.; Tzeng, G.-H. CPA Firm’s Cloud Auditing Provider for Performance Evaluation and Improvement: An Empirical Case of China. Technol. Econ. Dev. Econ. 2018, 24, 2338–2373. [Google Scholar] [CrossRef]

- Le Guyader, L.P. Artificial Intelligence in Accounting: GAAP’s “FAS133”. J. Corp. Account. Financ. 2020, 31, 185–189. [Google Scholar] [CrossRef]

- Schmitz, J.; Leoni, G. Accounting and Auditing at the Time of Blockchain Technology: A Research Agenda. Aust. Account. Rev. 2019, 29, 331–342. [Google Scholar] [CrossRef]

- White, B.S.; King, C.G.; Holladay, J. Blockchain Security Risk Assessment and the Auditor. J. Corp. Account. Financ. 2020, 31, 47–53. [Google Scholar] [CrossRef]

- O’Leary, D.E. Configuring Blockchain Architectures for Transaction Information in Blockchain Consortiums: The Case of Accounting and Supply Chain Systems. Intell. Syst. Account. Financ. Manag. 2017, 24, 138–147. [Google Scholar] [CrossRef]

- Vincent, N.E.; Skjellum, A.; Medury, S. Blockchain Architecture: A Design That Helps CPA Firms Leverage the Technology. Int. J. Account. Inf. Syst. 2020, 38, 100466. [Google Scholar] [CrossRef]

- Rîndaşu, S.-M. Blockchain in Accounting: Trick or Treat? Qual. Access Success 2019, 20, 143–147. [Google Scholar]

- Pedreño, E.P.; Gelashvili, V.; Nebreda, L.P. Blockchain and Its Application to Accounting. Intang. Cap. 2021, 17, 1–16. [Google Scholar] [CrossRef]

- Sinha, S. Blockchain—Opportunities and Challenges for Accounting Professionals. J. Corp. Account. Financ. 2020, 31, 65–67. [Google Scholar] [CrossRef]

- Bonsón, E.; Bednárová, M. Blockchain and Its Implications for Accounting and Auditing. Meditari Account. Res. 2019, 27, 725–740. [Google Scholar] [CrossRef]

- Yu, T.; Lin, Z.; Tang, Q. Blockchain: The Introduction and Its Application in Financial Accounting. J. Corp. Account. Financ. 2018, 29, 37–47. [Google Scholar] [CrossRef]

- Byström, H. Blockchains, Real-Time Accounting, and the Future of Credit Risk Modeling. Ledger 2019, 4, 40–47. [Google Scholar] [CrossRef]

- Carlin, T. Blockchain and the Journey Beyond Double Entry. Aust. Account. Rev. 2019, 29, 305–311. [Google Scholar] [CrossRef]

- Coyne, J.G.; McMickle, P.L. Can Blockchains Serve an Accounting Purpose? J. Emerg. Technol. Account. 2017, 14, 101–111. [Google Scholar] [CrossRef]

- Eldalabeeh, A.R.; Al-Shbail, M.O.; Almuiet, M.Z.; Bany Baker, M.; E’Leimat, D. Cloud-Based Accounting Adoption in Jordanian Financial Sector. J. Asian Financ. Econ. Bus. 2021, 8, 833–849. [Google Scholar] [CrossRef]

- Popivniak, Y. Cloud-Based Accounting Software: Choice Options in The Light of Modern International Tendencies. Balt. J. Econ. Stud. 2019, 5, 170–177. [Google Scholar] [CrossRef]

- Christauskas, C.; Miseviciene, R. Cloud–Computing Based Accounting for Small to Medium Sized Business. Eng. Econ. 2012, 23, 14–21. [Google Scholar] [CrossRef]

- Vasarhelyi, M.A.; Kogan, A.; Tuttle, B.M. Big Data in Accounting: An Overview. Account. Horiz. 2015, 29, 381–396. [Google Scholar] [CrossRef]

- Cao, M.; Chychyla, R.; Stewart, T. Big Data Analytics in Financial Statement Audits. Account. Horiz. 2015, 29, 423–429. [Google Scholar] [CrossRef]

- Eilifsen, A.; Kinserdal, F.; Messier, W.F., Jr.; McKee, T.E. An Exploratory Study into the Use of Audit Data Analytics on Audit Engagements. Account. Horiz. 2020, 34, 75–103. [Google Scholar] [CrossRef]

- Arnaboldi, M.; Busco, C.; Cuganesan, S. Accounting, Accountability, Social Media and Big Data: Revolution or Hype? Account. Audit. Account. J. 2017, 30, 762–776. [Google Scholar] [CrossRef]

- Richins, G.; Stapleton, A.; Stratopoulos, T.C.; Wong, C. Big Data Analytics: Opportunity or Threat for the Accounting Profession? J. Inf. Syst. 2017, 31, 63–79. [Google Scholar] [CrossRef]

- Cockcroft, S.; Russell, M. Big Data Opportunities for Accounting and Finance Practice and Research: Big Data in Accounting and Finance. Aust. Account. Rev. 2018, 28, 323–333. [Google Scholar] [CrossRef]

- Pickard, M.D.; Cokins, G. From Bean Counters to Bean Growers: Accountants as Data Analysts—A Customer Profitability Example. J. Inf. Syst. 2015, 29, 151–164. [Google Scholar] [CrossRef]

- Yoon, K.; Hoogduin, L.; Zhang, L. Big Data as Complementary Audit Evidence. Account. Horiz. 2015, 29, 431–438. [Google Scholar] [CrossRef]

- Appelbaum, D.; Kogan, A.; Vasarhelyi, M.A. Big Data and Analytics in the Modern Audit Engagement: Research Needs. Audit. J. Pract. Theory 2017, 36, 1–27. [Google Scholar] [CrossRef]

- Kend, M.; Nguyen, L.A. Big Data Analytics and Other Emerging Technologies: The Impact on the Australian Audit and Assurance Profession. Aust. Account. Rev. 2020, 30, 269–282. [Google Scholar] [CrossRef]

- Salijeni, G.; Samsonova-Taddei, A.; Turley, S. Big Data and Changes in Audit Technology: Contemplating a Research Agenda. Account. Bus. Res. 2019, 49, 95–119. [Google Scholar] [CrossRef]

- Kahyaoglu, S.B.; Caliyurt, K. Cyber Security Assurance Process from the Internal Audit Perspective. Manag. Audit. J. 2018, 33, 360–376. [Google Scholar] [CrossRef]

- Zadorozhnyi, Z.-M.; Muravskyi, V.V.; Shevchuk, O.; Muravskyi, V. The Accounting System as The Basis for Organising Enterprise Cybersecurity. Financ. Credit Act. Probl. Theory Pract. 2020, 3, 149–157. [Google Scholar] [CrossRef]

- Eaton, T.V.; Grenier, J.H.; Layman, D. Accounting and Cybersecurity Risk Management. Curr. Issues Audit. 2019, 13, C1–C9. [Google Scholar] [CrossRef]

- Haapamäki, E.; Sihvonen, J. Cybersecurity in Accounting Research. Manag. Audit. J. 2019, 34, 808–834. [Google Scholar] [CrossRef]

- Alles, M.G. Drivers of the Use and Facilitators and Obstacles of the Evolution of Big Data by the Audit Profession. Account. Horiz. 2015, 29, 439–449. [Google Scholar] [CrossRef]

- Alles, M.; Gray, G.L. Incorporating Big Data in Audits: Identifying Inhibitors and a Research Agenda to Address Those Inhibitors. Int. J. Account. Inf. Syst. 2016, 22, 44–59. [Google Scholar] [CrossRef]

- Dagilienė, L.; Klovienė, L. Motivation to Use Big Data and Big Data Analytics in External Auditing. Manag. Audit. J. 2019, 34, 750–782. [Google Scholar] [CrossRef]

- Dyball, M.C.; Seethamraju, R. The Impact of Client Use of Blockchain Technology on Audit Risk and Audit Approach—An Exploratory Study. Int. J. Audit. 2021, 25, 602–615. [Google Scholar] [CrossRef]

- Rezaee, Z.; Wang, J. Relevance of Big Data to Forensic Accounting Practice and Education. Manag. Audit. J. 2019, 34, 268–288. [Google Scholar] [CrossRef]

- Kokina, J.; Mancha, R.; Pachamanova, D. Blockchain: Emergent Industry Adoption and Implications for Accounting. J. Emerg. Technol. Account. 2017, 14, 91–100. [Google Scholar] [CrossRef]

- Rooney, H.; Aiken, B.; Rooney, M. Q&A. Is Internal Audit Ready for Blockchain? Technol. Innov. Manag. Rev. 2017, 7, 41–44. [Google Scholar] [CrossRef]

- Gauthier, M.P.; Brender, N. How Do the Current Auditing Standards Fit the Emergent Use of Blockchain? Manag. Audit. J. 2021, 36, 365–385. [Google Scholar] [CrossRef]

- Karajovic, M.; Kim, H.M.; Laskowski, M. Thinking Outside the Block: Projected Phases of Blockchain Integration in the Accounting Industry. Aust. Account. Rev. 2019, 29, 319–330. [Google Scholar] [CrossRef]

- Borthick, A.F.; Pennington, R.R. When Data Become Ubiquitous, What Becomes of Accounting and Assurance? J. Inf. Syst. 2017, 31, 1–4. [Google Scholar] [CrossRef]

- Dai, J.; Vasarhelyi, M.A. Toward Blockchain-Based Accounting and Assurance. J. Inf. Syst. 2017, 31, 5–21. [Google Scholar] [CrossRef]

- Calderón, J.; Stratopoulos, T.C. What Accountants Need to Know about Blockchain *. Account. Perspect. 2020, 19, 303–323. [Google Scholar] [CrossRef]

- Moffitt, K.C.; Rozario, A.M.; Vasarhelyi, M.A. Robotic Process Automation for Auditing. J. Emerg. Technol. Account. 2018, 15, 1–10. [Google Scholar] [CrossRef]

- Aman, A.; Mohamed, N. The Implementation of Cloud Accounting in Public Sector. Asian J. Account. Gov. 2017, 8, 1–6. [Google Scholar] [CrossRef]

- Ma, D.; Fisher, R.; Nesbit, T. Cloud-Based Client Accounting and Small and Medium Accounting Practices: Adoption and Impact. Int. J. Account. Inf. Syst. 2021, 41, 100513. [Google Scholar] [CrossRef]

- Saha, T.; Das, S.K.; Rahman, M.M.; Siddique, F.K.; Uddin, M.G. Prospects and Challenges of Implementing Cloud Accounting in Bangladesh. J. Asian Financ. Econ. Bus. 2020, 7, 275–282. [Google Scholar] [CrossRef]

- Omoteso, K. The Application of Artificial Intelligence in Auditing: Looking Back to the Future. Expert Syst. Appl. 2012, 39, 8490–8495. [Google Scholar] [CrossRef]

- Horák, J.; Bokšová, J. Influence of Big Data on Financial Accounting. Int. Adv. Econ. Res. 2018, 24, 205–206. [Google Scholar] [CrossRef]

- Perkhofer, L.M.; Hofer, P.; Walchshofer, C.; Plank, T.; Jetter, H.-C. Interactive Visualization of Big Data in the Field of Accounting: A Survey of Current Practice and Potential Barriers for Adoption. J. Appl. Account. Res. 2019, 20, 497–525. [Google Scholar] [CrossRef]

- Desplebin, O.; Lux, G.; Petit, N. To Be or Not to Be: Blockchain and the Future of Accounting and Auditing. Account. Perspect. 2021, 20, 743–769. [Google Scholar] [CrossRef]

- Fuller, S.H.; Markelevich, A. Should Accountants Care about Blockchain? J. Corp. Account. Financ. 2020, 31, 34–46. [Google Scholar] [CrossRef]

- Kokina, J.; Blanchette, S. Early Evidence of Digital Labor in Accounting: Innovation with Robotic Process Automation. Int. J. Account. Inf. Syst. 2019, 35, 100431. [Google Scholar] [CrossRef]

- Smith, S.S. Implications of Next Step Blockchain Applications for Accounting and Legal Practitioners: A Case Study. Australas. Account. Bus. Financ. J. 2018, 12, 77–90. [Google Scholar] [CrossRef]

- Fernandez, D.; Aman, A. Impacts of Robotic Process Automation on Global Accounting Services. Asian J. Account. Gov. 2018, 9, 123–132. [Google Scholar] [CrossRef]

- Heinzelmann, R. Occupational Identities of Management Accountants: The Role of the IT System. J. Appl. Account. Res. 2018, 19, 465–482. [Google Scholar] [CrossRef]

- Schmidt, P.J.; Riley, J.; Swanson Church, K. Investigating Accountants’ Resistance to Move beyond Excel and Adopt New Data Analytics Technology. Account. Horiz. 2020, 34, 165–180. [Google Scholar] [CrossRef]

- Sheldon, M.D. Using Blockchain to Aggregate and Share Misconduct Issues across the Accounting Profession. Curr. Issues Audit. 2018, 12, A27–A35. [Google Scholar] [CrossRef]

- Tan, B.S.; Low, K.Y. Blockchain as the Database Engine in the Accounting System. Aust. Account. Rev. 2019, 29, 312–318. [Google Scholar] [CrossRef]

- Asatiani, A.; Apte, U.; Penttinen, E.; Rönkkö, M.; Saarinen, T. Impact of Accounting Process Characteristics on Accounting Outsourcing—Comparison of Users and Non-Users of Cloud-Based Accounting Information Systems. Int. J. Account. Inf. Syst. 2019, 34, 100419. [Google Scholar] [CrossRef]

- Cai, C.W. Triple-entry Accounting with Blockchain: How Far Have We Come? Account. Financ. 2021, 61, 71–93. [Google Scholar] [CrossRef]

- Liu, M.; Wu, K.; Xu, J. How Will Blockchain Technology Impact Auditing and Accounting: Permissionless vs. Permissioned Blockchain. Curr. Issues Audit. 2019, 13, A19–A29. [Google Scholar] [CrossRef]

- McCallig, J.; Robb, A.; Rohde, F. Establishing the Representational Faithfulness of Financial Accounting Information Using Multiparty Security, Network Analysis and a Blockchain. Int. J. Account. Inf. Syst. 2019, 33, 47–58. [Google Scholar] [CrossRef]

- Cristea, L.M. Romanian Auditors’ Perception Concerning the IT Impact in the Big Data Era. Pénzü. Szle. Public Financ. Q. 2021, 66, 68–82. [Google Scholar] [CrossRef]

- Korhonen, T.; Selos, E.; Laine, T.; Suomala, P. Exploring the Programmability of Management Accounting Work for Increasing Automation: An Interventionist Case Study. Account. Audit. Account. J. 2020, 34, 253–280. [Google Scholar] [CrossRef]

- Zhyvets, A. Evolution of Professional Competencies of Accountants of Small Enterprises in The Digital Economy of Ukraine. Balt. J. Econ. Stud. 2019, 4, 87–89. [Google Scholar] [CrossRef]

- Stein Smith, S. Audit Implications of AI & Blockchain. In Blockchain, Artificial Intelligence and Financial Services; Springer International Publishing: Cham, Switzerland, 2020; pp. 165–173. ISBN 978-3-030-29760-2. [Google Scholar]

- Earley, C.E. Data Analytics in Auditing: Opportunities and Challenges. Bus. Horiz. 2015, 58, 493–500. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Applied Research Formula | |

|---|---|

| I | (“audit*” OR “account*”) AND (“RPA” OR “Robot Process Automation”) |

| 586 results generated; 15 results selected. | |

| II | (“audit*” OR “account*”) AND (“Cloud”) |

| 14,007 results generated; 81 results selected. | |

| III | (“audit*” OR “account*”) AND (“AI” OR “Artificial Intelligence”) |

| 4900 results generated; 73 results selected. | |

| IV | (“audit*” OR “account*”) AND (“Big Data” OR “Data Analysis”) |

| 13,516 results generated; 92 results selected. | |

| V | (“audit*” OR “account*”) AND (“Blockchain” OR “Distributed Ledger”) |

| 1451 results generated; 49 results selected. | |

| VI | (“audit*” OR “account*”) AND (“Cybersecurity” OR “Security Information”) |

| 465 results generated; 13 results selected. | |

| Authors | Publication Year | Total Citations |

|---|---|---|

| Moll and Yigitbasioglu [17] | 2019 | 161 |

| Yigitbasioglu [28] | 2015 | 139 |

| Ahmad [29] | 2019 | 139 |

| Pimentel and Boulianne [16] | 2020 | 132 |

| Gepp et al. [30] | 2018 | 127 |

| Brown-Liburd et al. [31] | 2015 | 118 |

| Ferri et al. [32] | 2020 | 114 |

| Cleary and Quinn [33] | 2016 | 112 |

| Munoko et al. [34] | 2020 | 108 |

| Islam et al. [35] | 2018 | 107 |

| Austin et al. [36] | 2021 | 107 |

| Yau-Yeung et al. [37] | 2020 | 104 |

| Issa et al. [38] | 2016 | 100 |

| Total citations 31 December 2021 | 2015–2021 | 1568 |

| Accounting Areas | No. of Studies | % | Main Research Method | No. of Studies | % |

|---|---|---|---|---|---|

| MA/FA | 37 | 32.46 | Literature Review | 26 | 22.81 |

| F. Audit/I. Audit | 28 | 24.56 | Exploratory | 20 | 17.54 |

| MA/FA/F. Audit/I. Audit | 15 | 13.16 | Commentary | 17 | 14.91 |

| FA | 12 | 10.53 | Interviews | 15 | 13.16 |

| F. Audit | 9 | 7.89 | Analytical | 9 | 7.89 |

| MA | 8 | 7.02 | Questionnaires | 9 | 7.89 |

| I. Audit | 4 | 3.51 | Conceptual | 9 | 7.89 |

| FA/F. Audit | 1 | 0.88 | Case Study | 9 | 7.89 |

| Total | 114 | 100% | Total | 114 | 100% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tiron-Tudor, A.; Donțu, A.N.; Bresfelean, V.P. Emerging Technologies’ Contribution to the Digital Transformation in Accountancy Firms. Electronics 2022, 11, 3818. https://doi.org/10.3390/electronics11223818

Tiron-Tudor A, Donțu AN, Bresfelean VP. Emerging Technologies’ Contribution to the Digital Transformation in Accountancy Firms. Electronics. 2022; 11(22):3818. https://doi.org/10.3390/electronics11223818

Chicago/Turabian StyleTiron-Tudor, Adriana, Adelina Nicoleta Donțu, and Vasile Paul Bresfelean. 2022. "Emerging Technologies’ Contribution to the Digital Transformation in Accountancy Firms" Electronics 11, no. 22: 3818. https://doi.org/10.3390/electronics11223818

APA StyleTiron-Tudor, A., Donțu, A. N., & Bresfelean, V. P. (2022). Emerging Technologies’ Contribution to the Digital Transformation in Accountancy Firms. Electronics, 11(22), 3818. https://doi.org/10.3390/electronics11223818