Three key clean energy technologies are examined—solar photovoltaics (PV) (focusing on thin-film cells using critical minerals tellurium, selenium and indium), wind power (with rare earth elements neodymium and dysprosium in magnets) and fuel cells (using, alternatively, platinum or yttrium oxide as key elements). These are not the full suite of available technologies, and they are not considered in concert but rather as individual demand drivers. Importantly, due to the wide coverage of technologies, efforts were made to utilize consistent, publically available data; hence, the minerals production figures from the United States Geological Survey (USGS) are utilized for all minerals, although this may produce some error in estimates where reporting is incomplete.

Following analysis of the scenarios, the discussion includes a consideration of key constraints in making energy urban ores or deep ocean resources feasible for exploitation.

3.1. Energy Scenarios

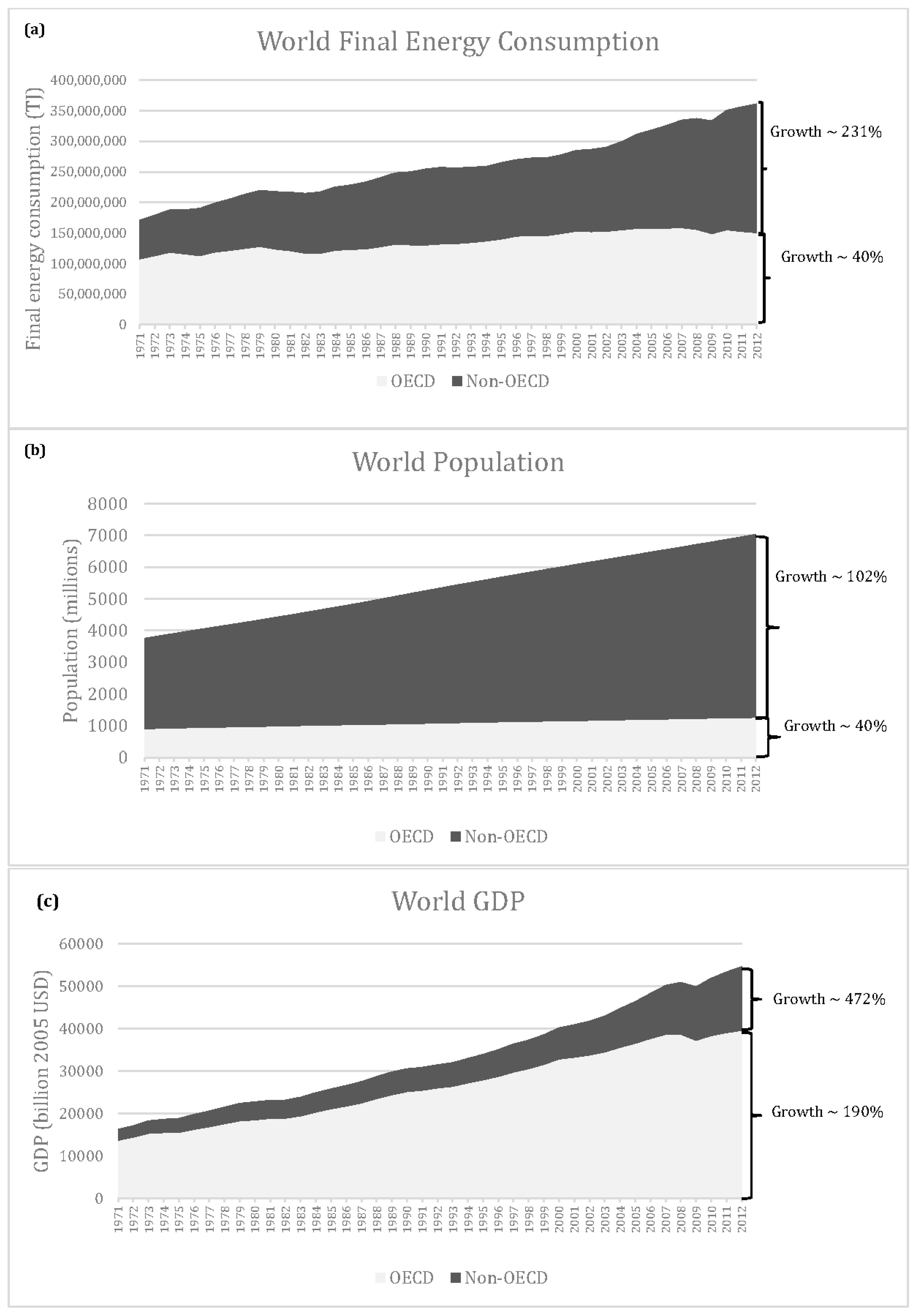

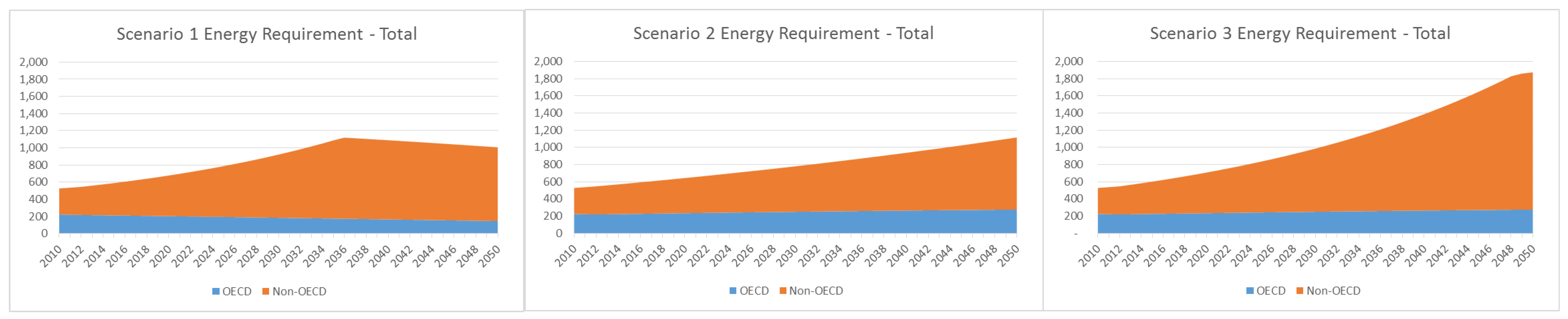

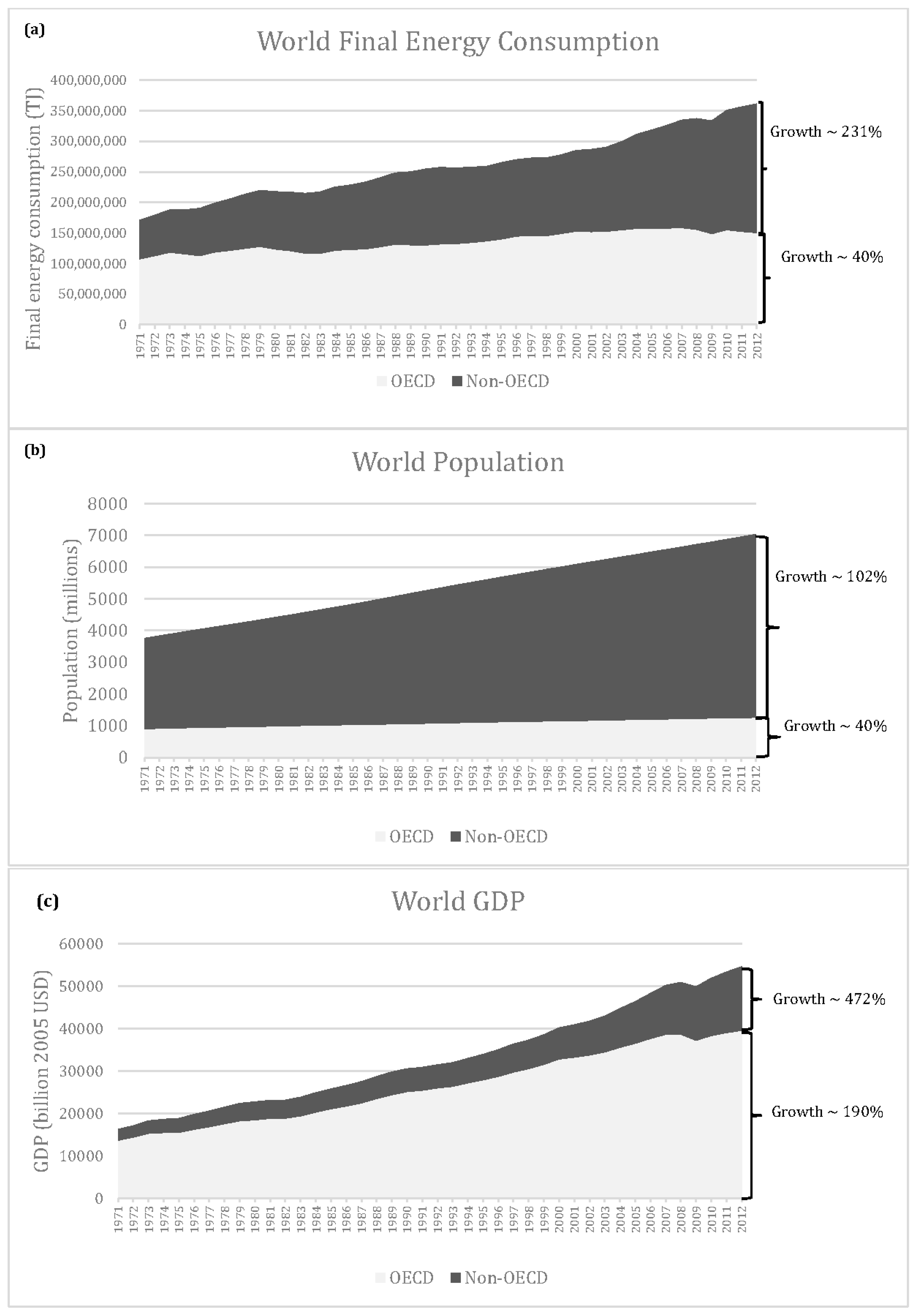

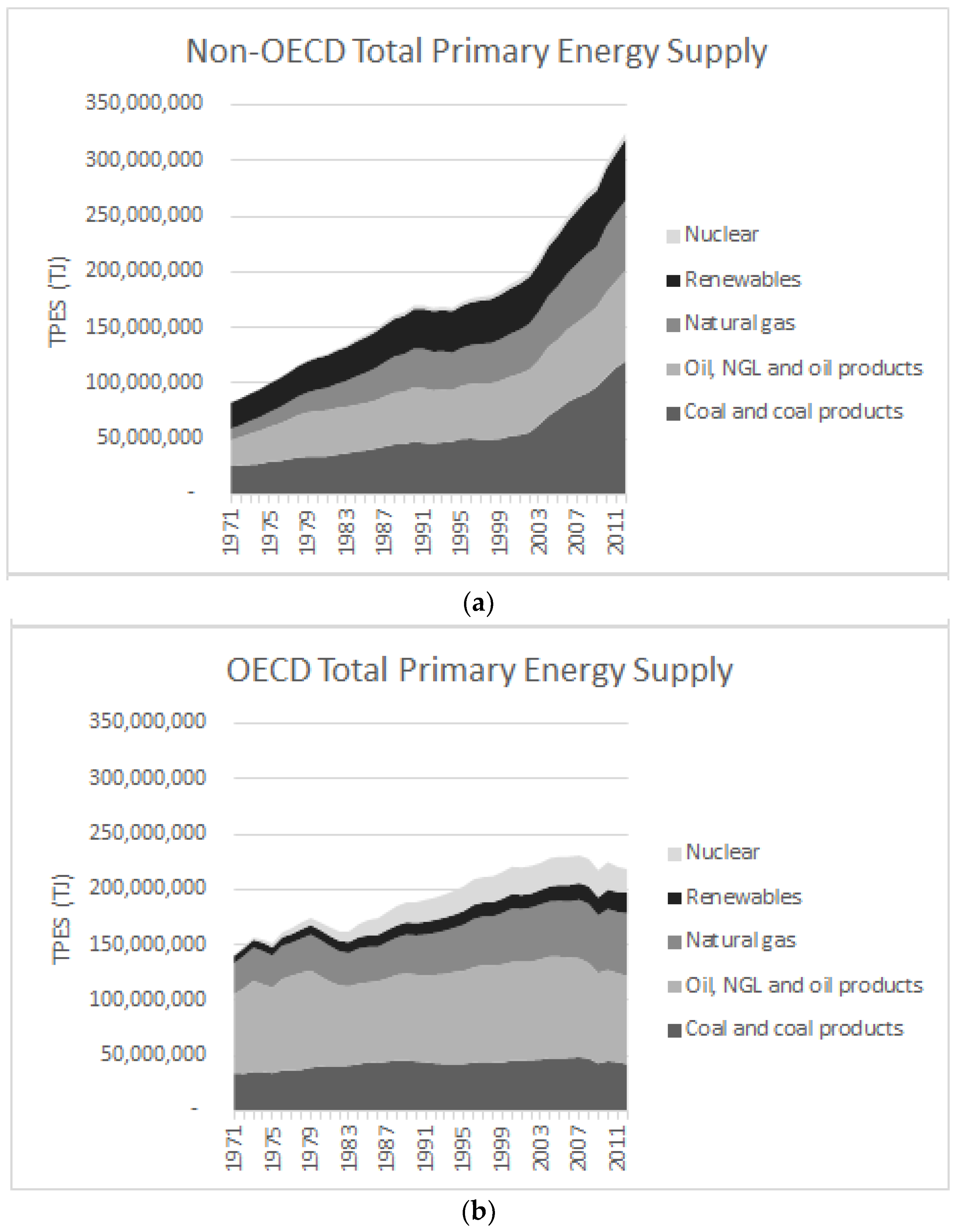

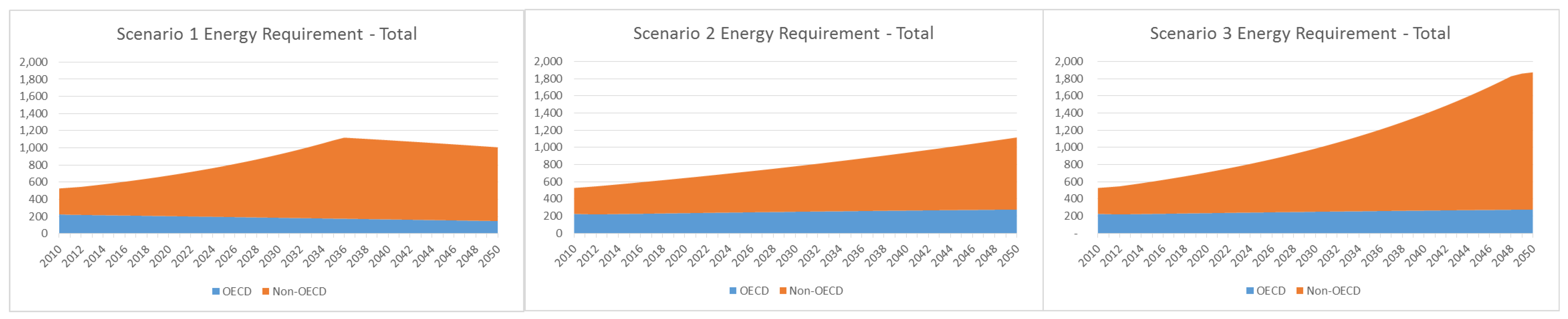

In order to develop a variety of potential future scenarios for critical minerals demand from energy technologies, IEA data was analyzed, and potential trends were extrapolated from 2010 to 2050. With regards to the overall energy demand, the calculations used the per capita energy intensity and projected population trends from the OECD statistics to calculate the total energy requirement, shown in

Figure 8. All scenarios assumed the same population trends, and in all scenarios it was assumed that the non-OECD per capita energy usage would eventually equal that of the OECD. In scenario 1, the recent trend of OECD countries of reducing energy intensity is considered to continue at a trend (year on year) decline, while non-OECD countries are assumed to rise to the recent peak of OECD energy intensity before starting to decline. In scenario 2, the longer-term trends of growth are assumed to continue, rather than the recent decline in the OECD. Scenario 3 uses the more recent rapid expansion of the non-OECD and the long-term expansion trends of the OECD in combination.

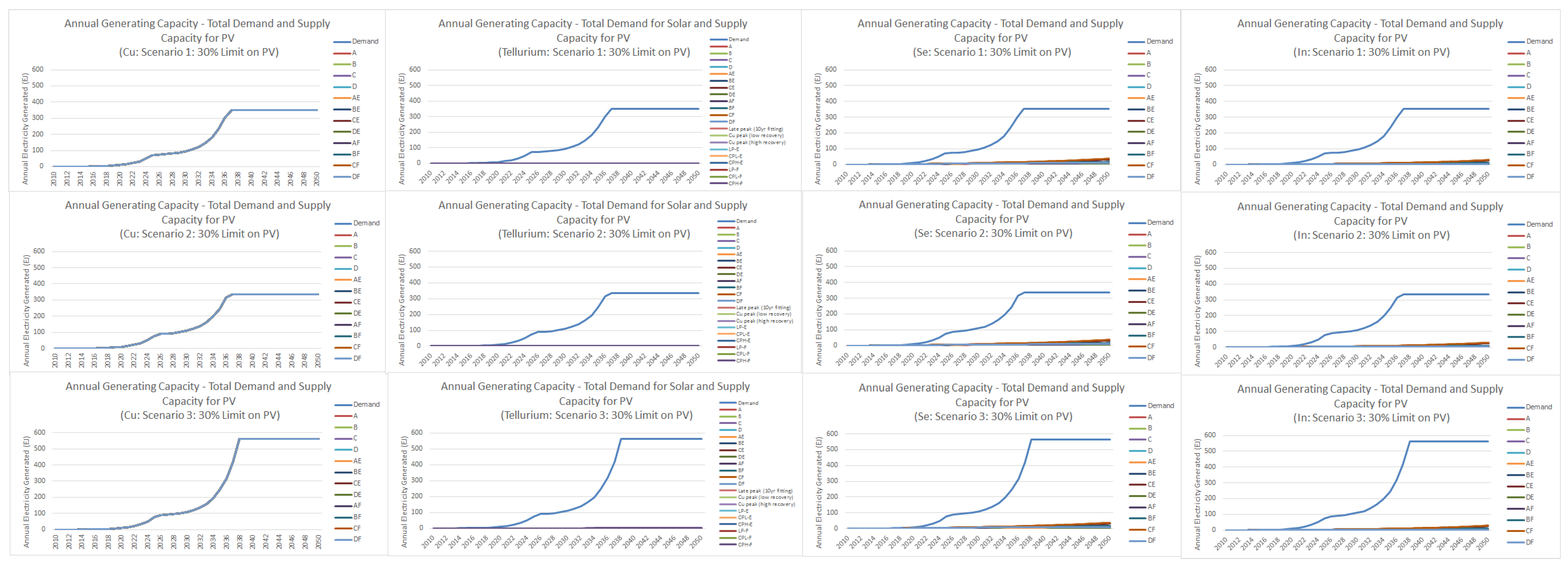

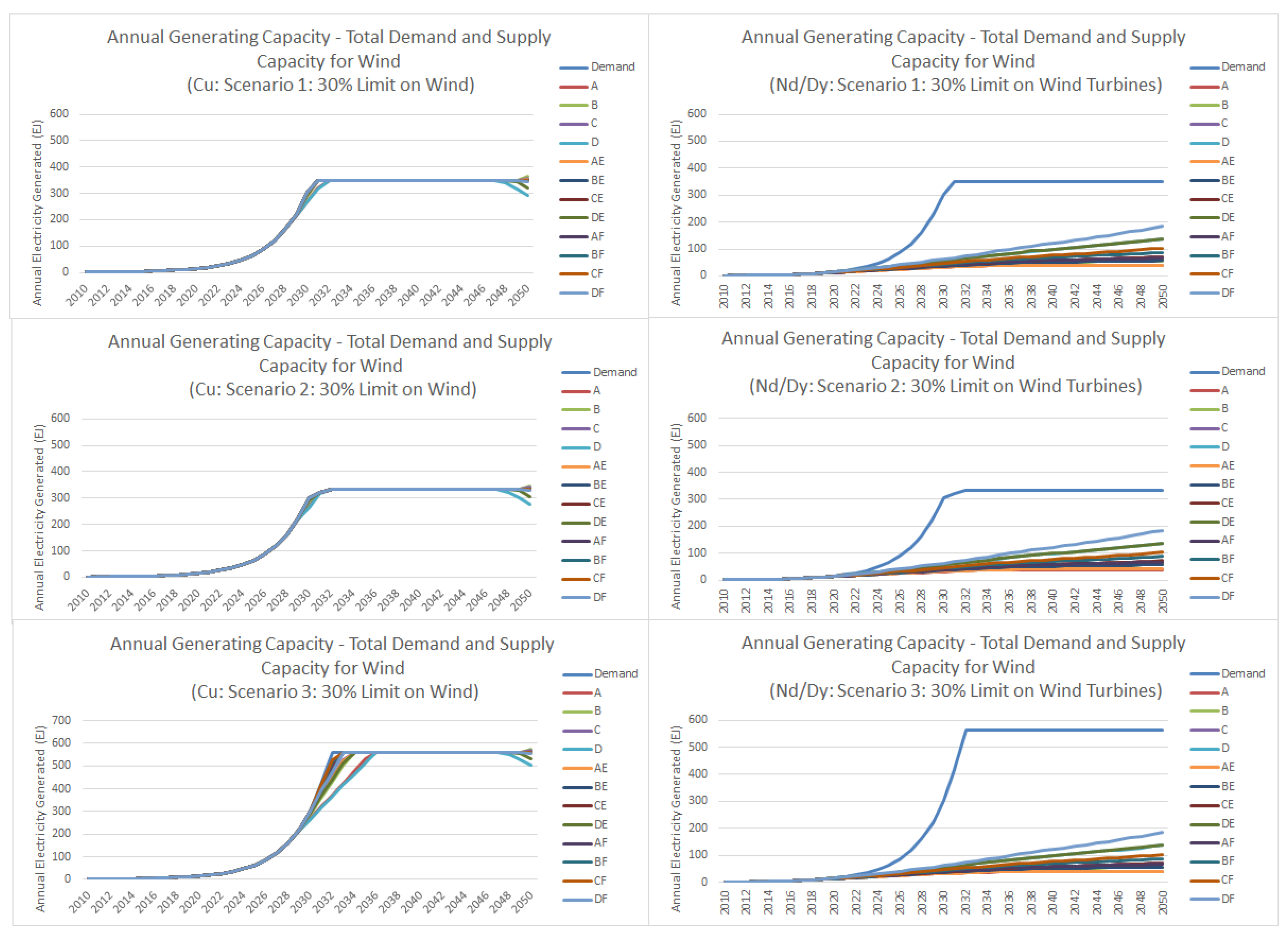

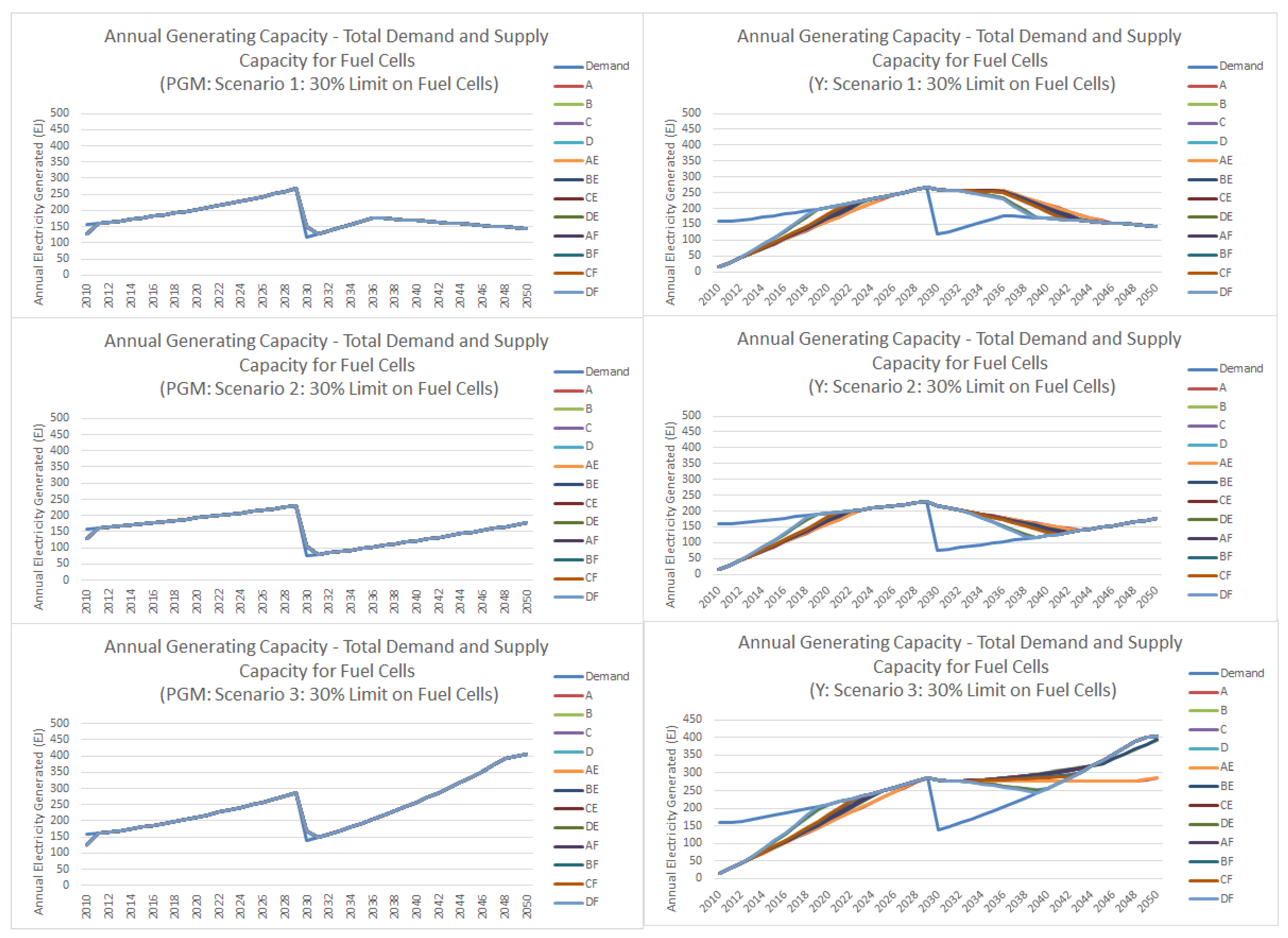

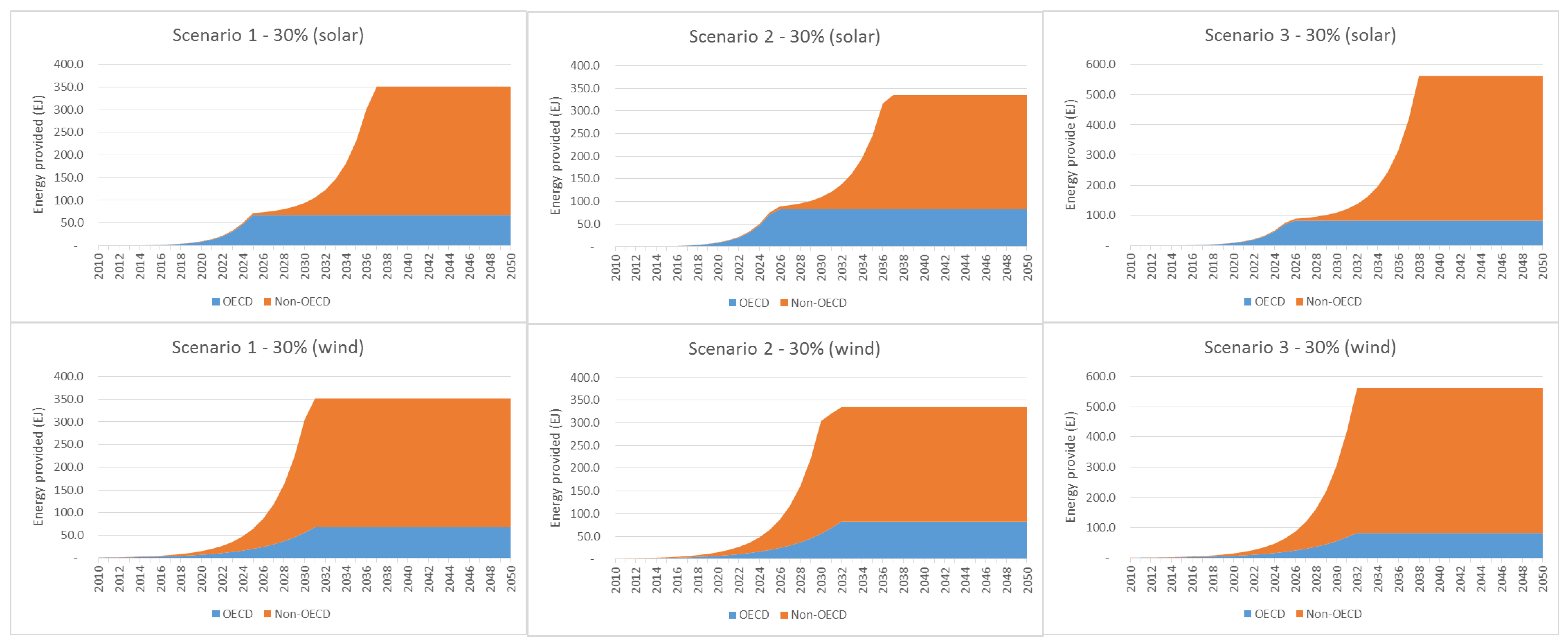

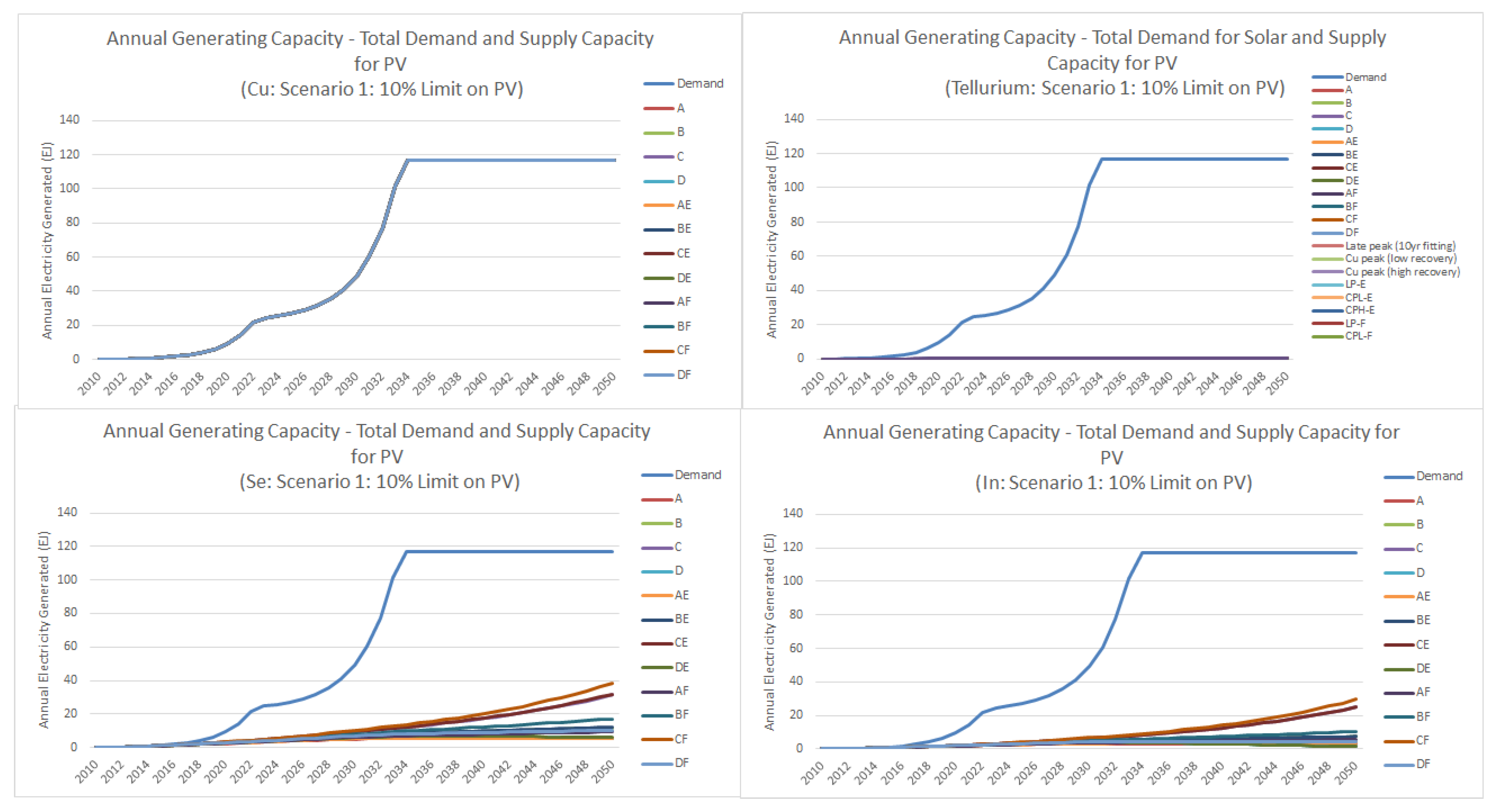

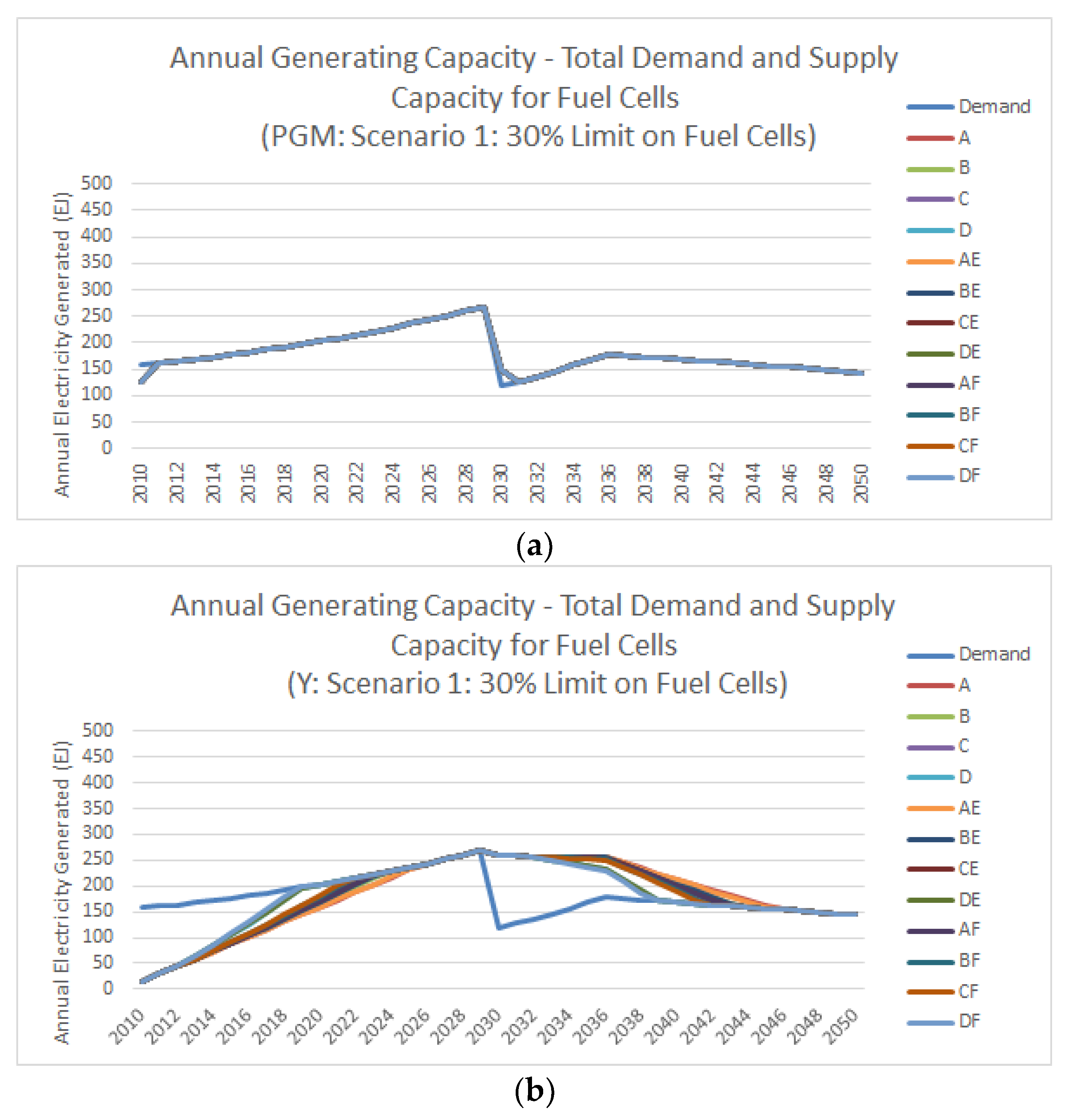

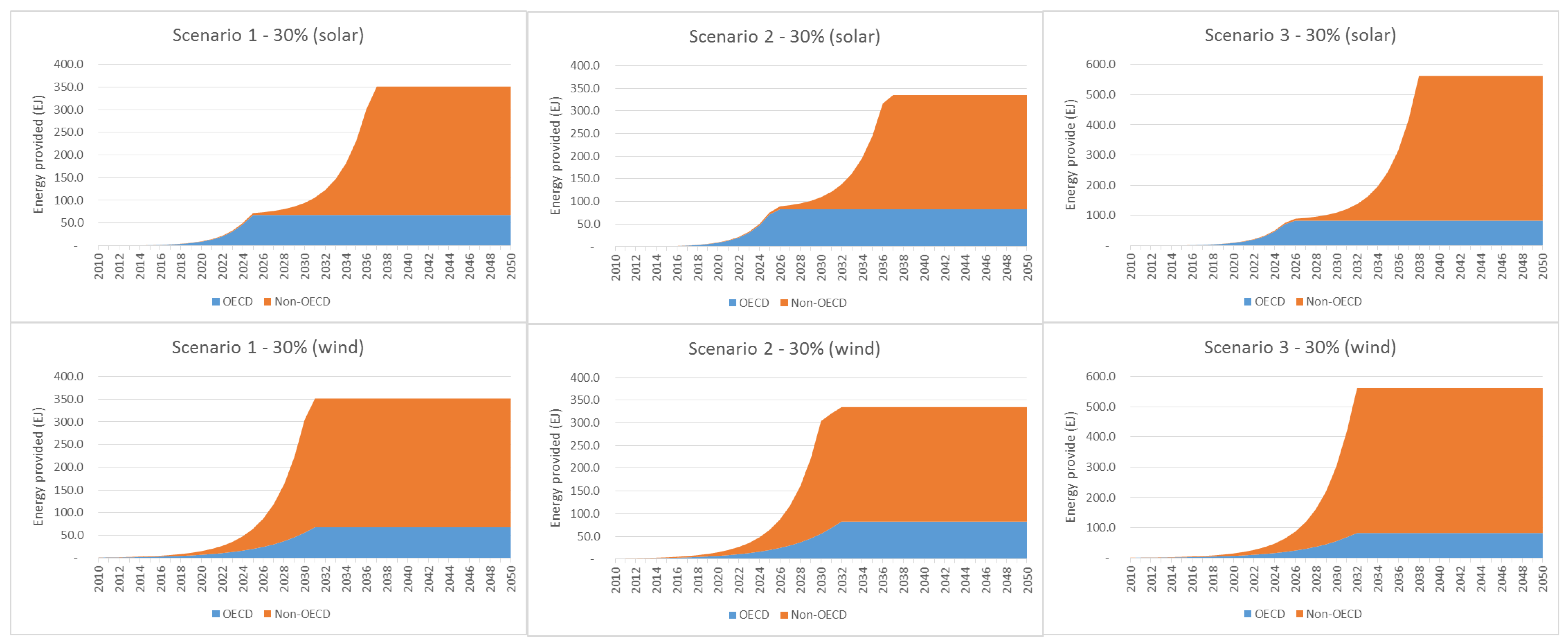

In addition to the scenarios for total energy demand, a number of scenarios were examined for the roll-out of solar photovoltaics, wind power and fuel cells. In the case of fuel cells, a simple percentage of total energy demand was attributed to fuel cell power systems, at levels of 10%, 20% and 30%. In the case of wind power and solar power, historical trends were used to extrapolate future take-up. In all cases, a limit was set on the maximum uptake of wind and solar power, set at 10%, 20% or 30% of the peak annual energy demand for the period out to 2050; once this was attained, it was assumed that this level would be maintained throughout the remainder of the period. The resulting energy demand from solar and wind in the three scenarios is shown in

Figure 9.

It should be noted that these levels of clean energy uptake are extremely high when compared with most conventional scenarios, but are based on the historic rates of expansion. Moreover, the uptake of solar power (for example) does not differentiate on the basis of technology, so the thin-film technologies considered here (which do not provide more than 10% of the current solar markets) are considered with respect to their potential to provide for the entire solar expansion, whereas they are realistically only one segment of the overall sector.

3.2. Materials Requirement and Recycling Scenarios

In order to estimate the demand for materials, the specific material requirement (kg/kW) was utilized from [

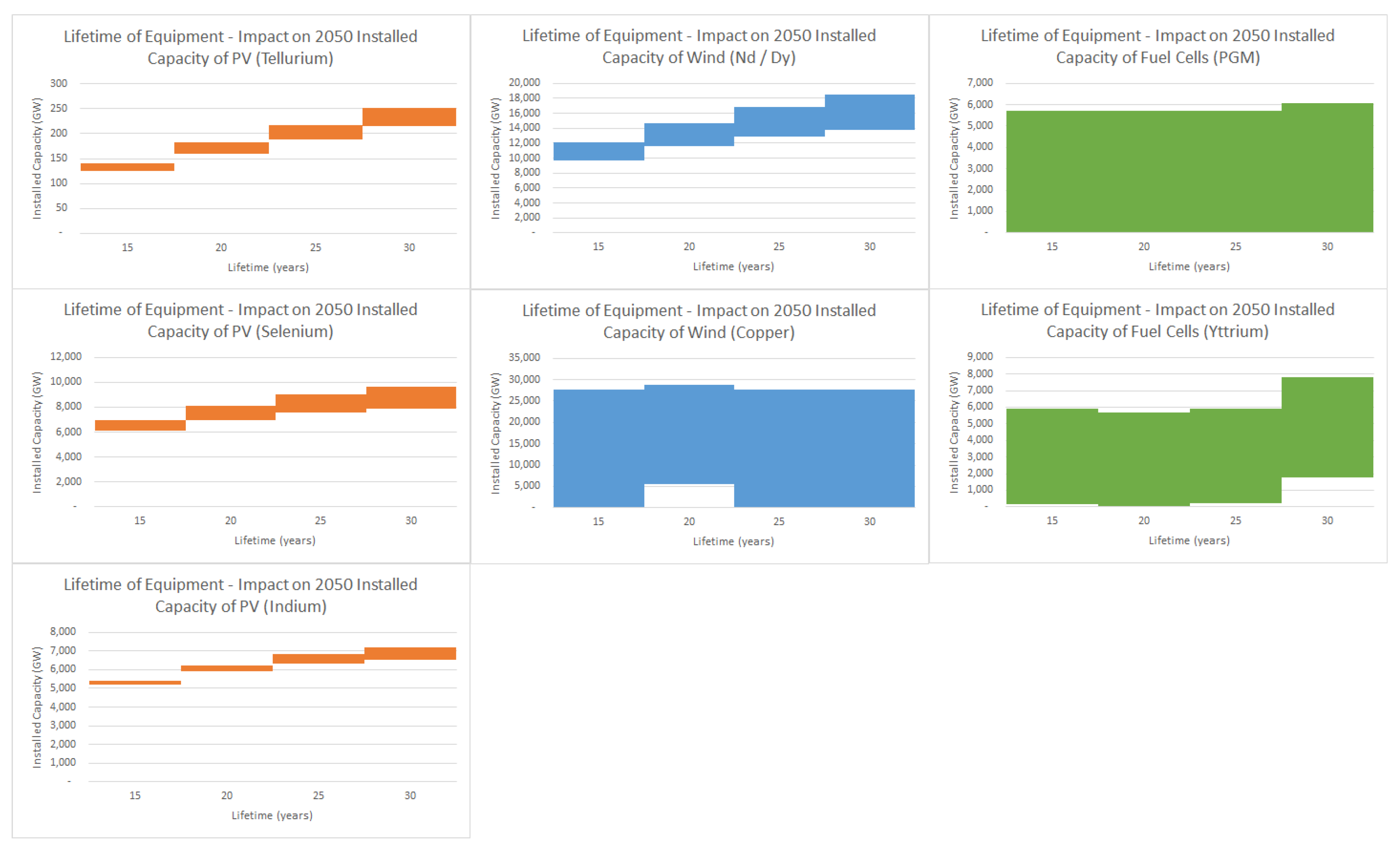

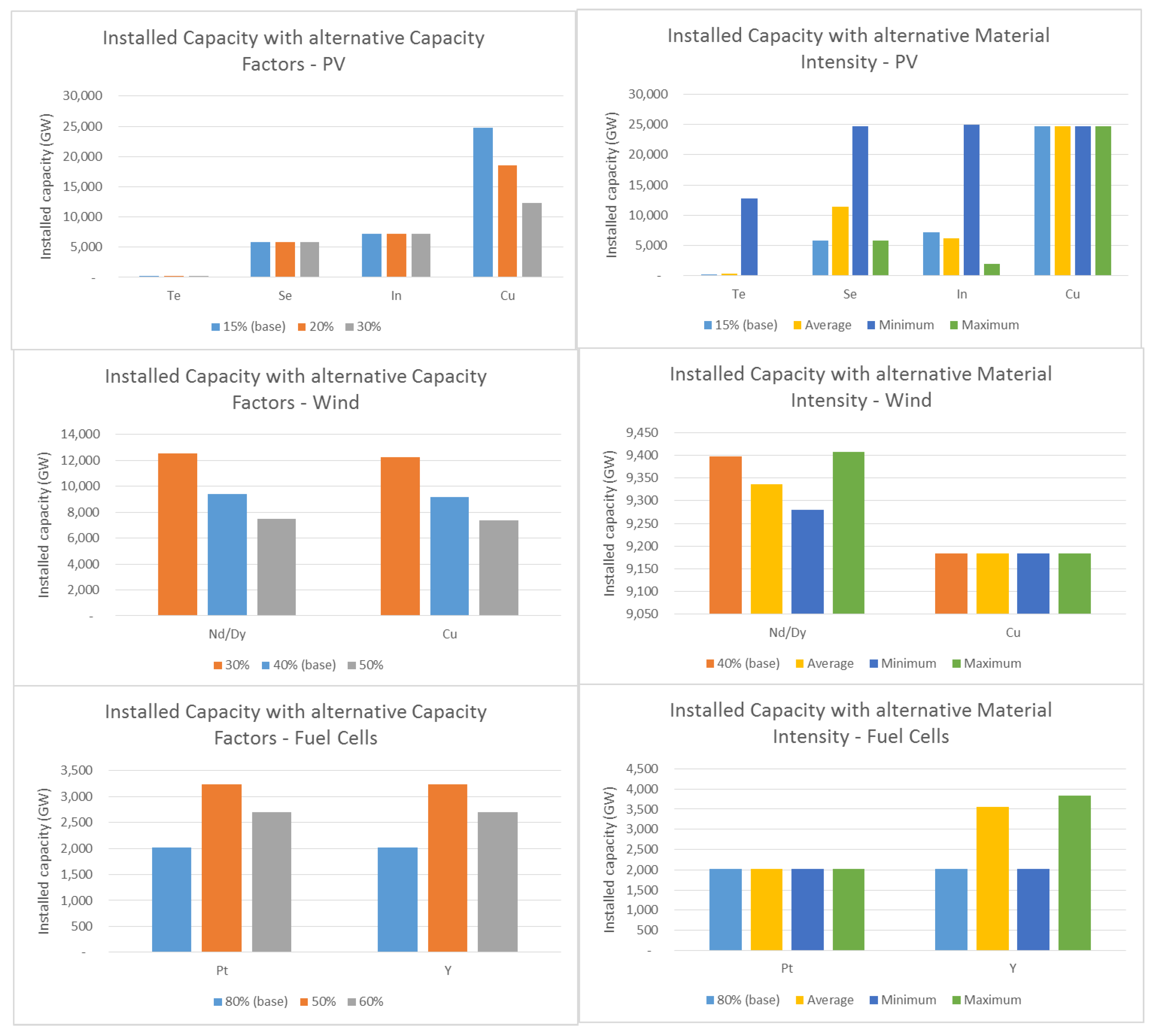

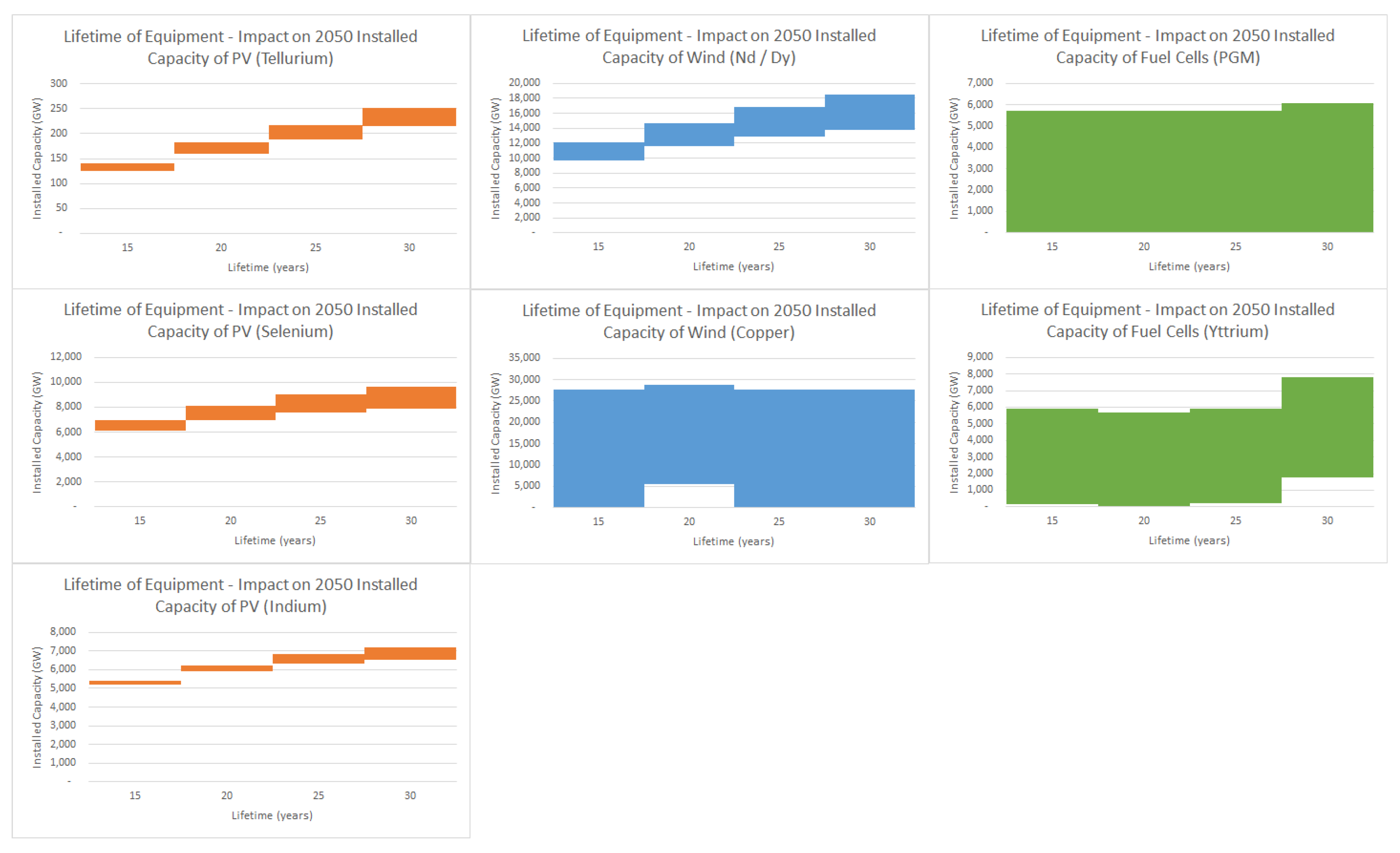

55]. The specific materials of interest were: indium, tellurium, selenium, copper, dysprosium/neodymium, yttrium and platinum. The specific material requirement was applied to each of the technologies, with an assumption of a capacity factor of 15% for solar and 40% for wind in order to obtain the energy output of each unit of installed capacity. In the initial assessment, no consideration was made for technology improvements to reduce materials usage. A lifetime of 20 years is applied to all of the technologies, requiring a replacement of an entire year’s added generation capacity in the 20th year following, in addition to any new capacity growth. While some applications may have longer lives than 20 years, this figure is considered to be reasonable in covering the three technology types considered here. These data were compared with materials supply scenarios to identify whether any shortages might be expected.

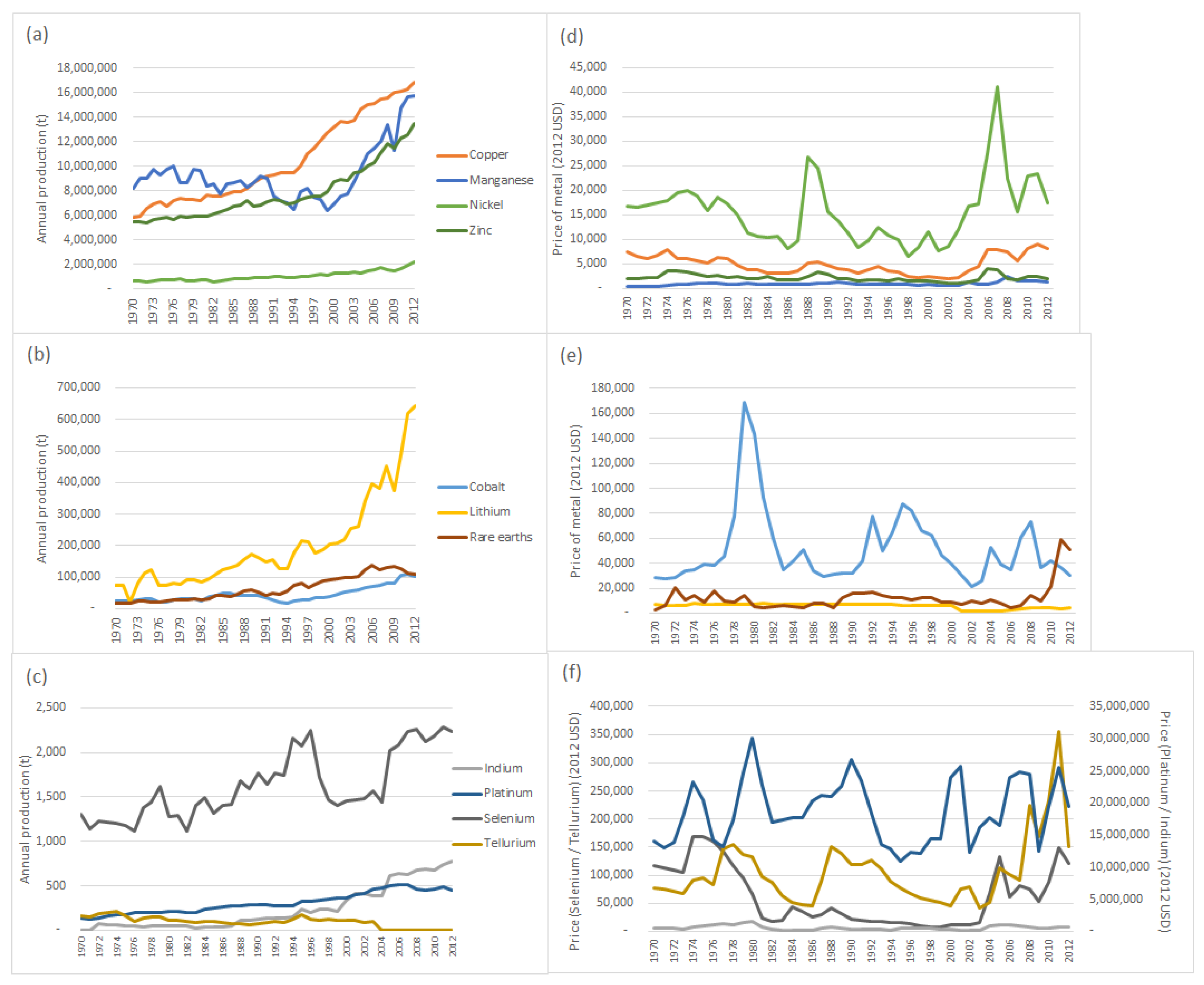

Historical data for supply were obtained from the USGS (various) [

48], and four alternative scenarios were developed for future supply. Recycling supplementation was then added to these four alternative scenarios so that there were ultimately 12 scenarios tested for each mineral. The characteristics of each of these material supply scenarios are given briefly in

Table 5.

The key criteria important to modeling and interpreting these supply trends are given in

Table 6. The estimation of future supply trends was based on existing historical data trends, not accounting for changes in ore grades or potential improvements in recovery. The recycling in the supply case is for all of the material supplied across all sectors, not just for the material supplied to the energy system (in contrast to the demand, which includes a lifetime of equipment that requires supplemented supply to meet with the redundancy rate of equipment).

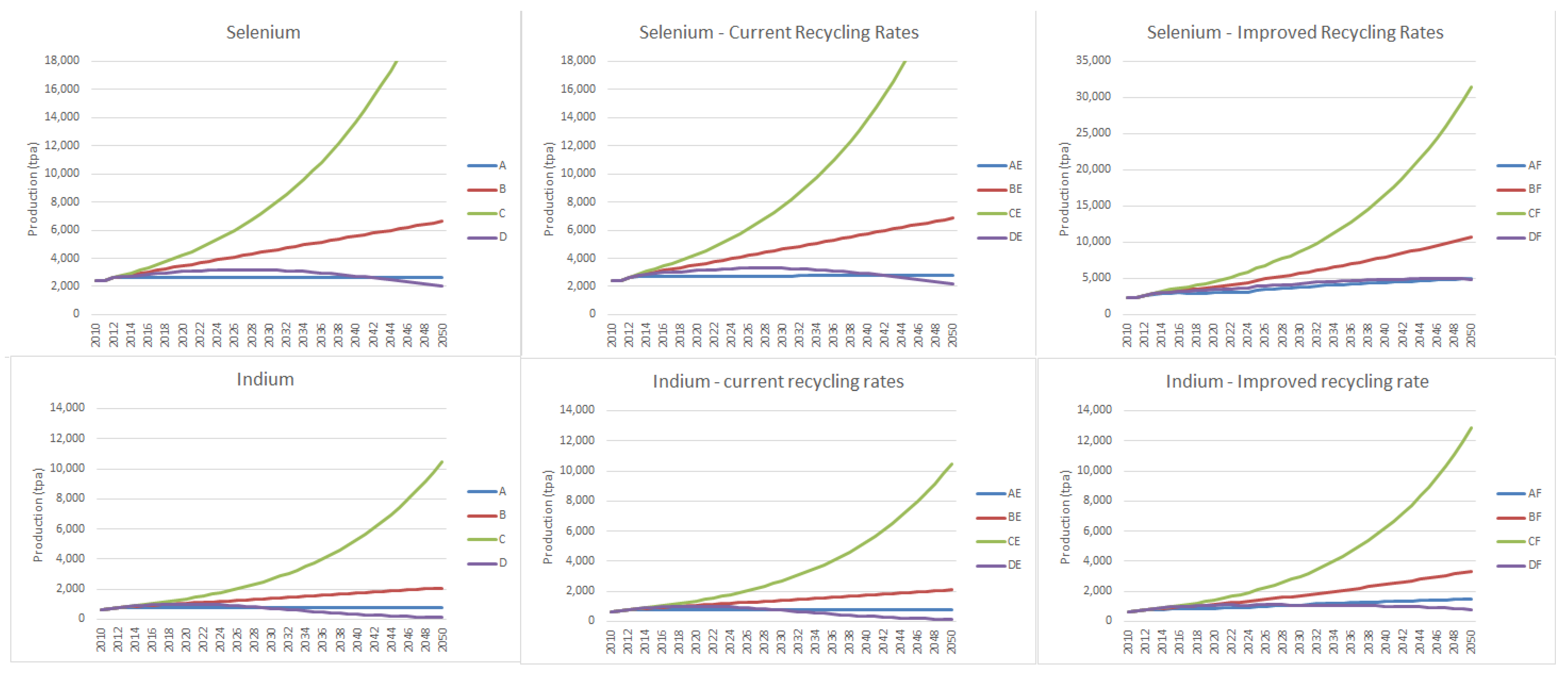

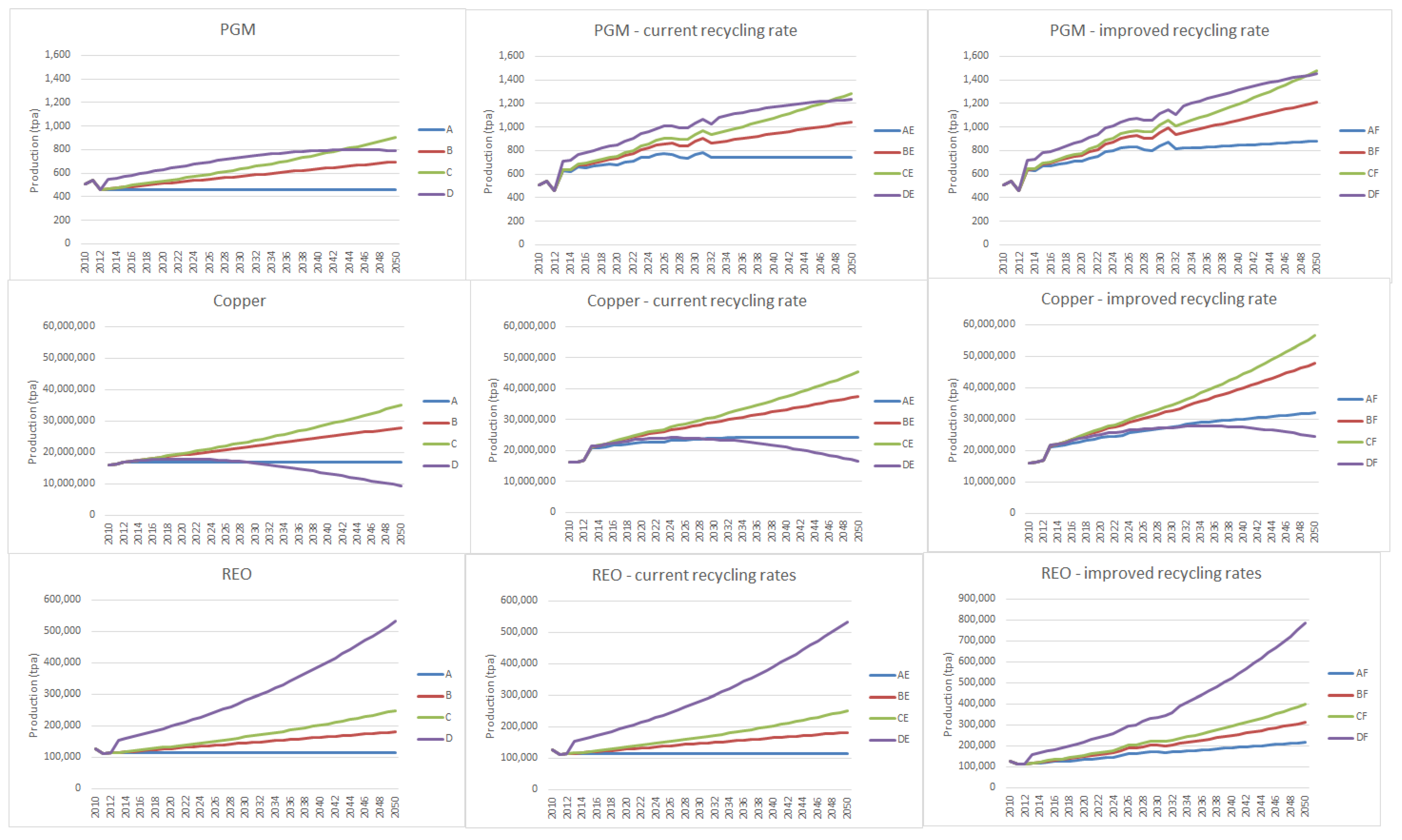

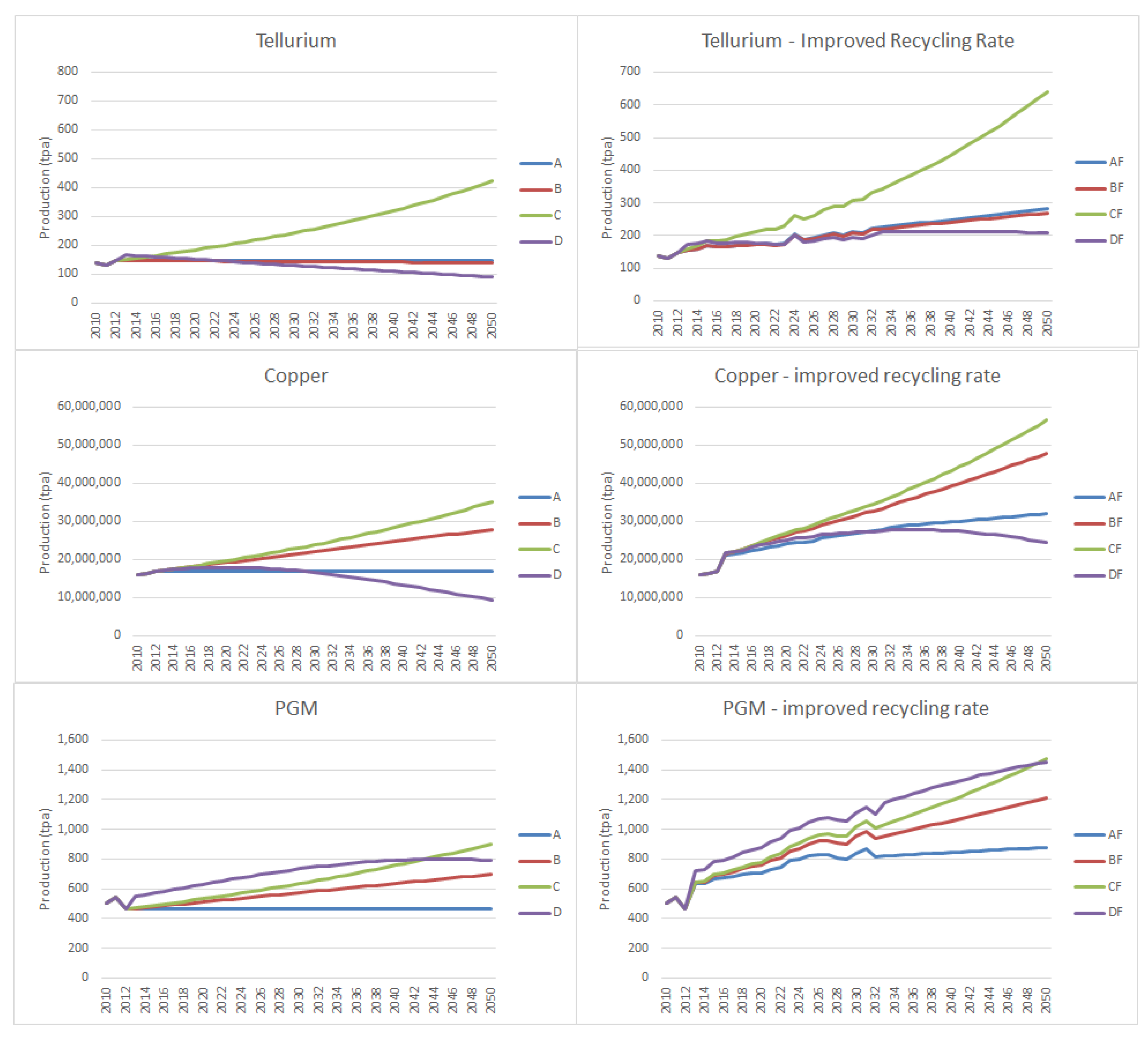

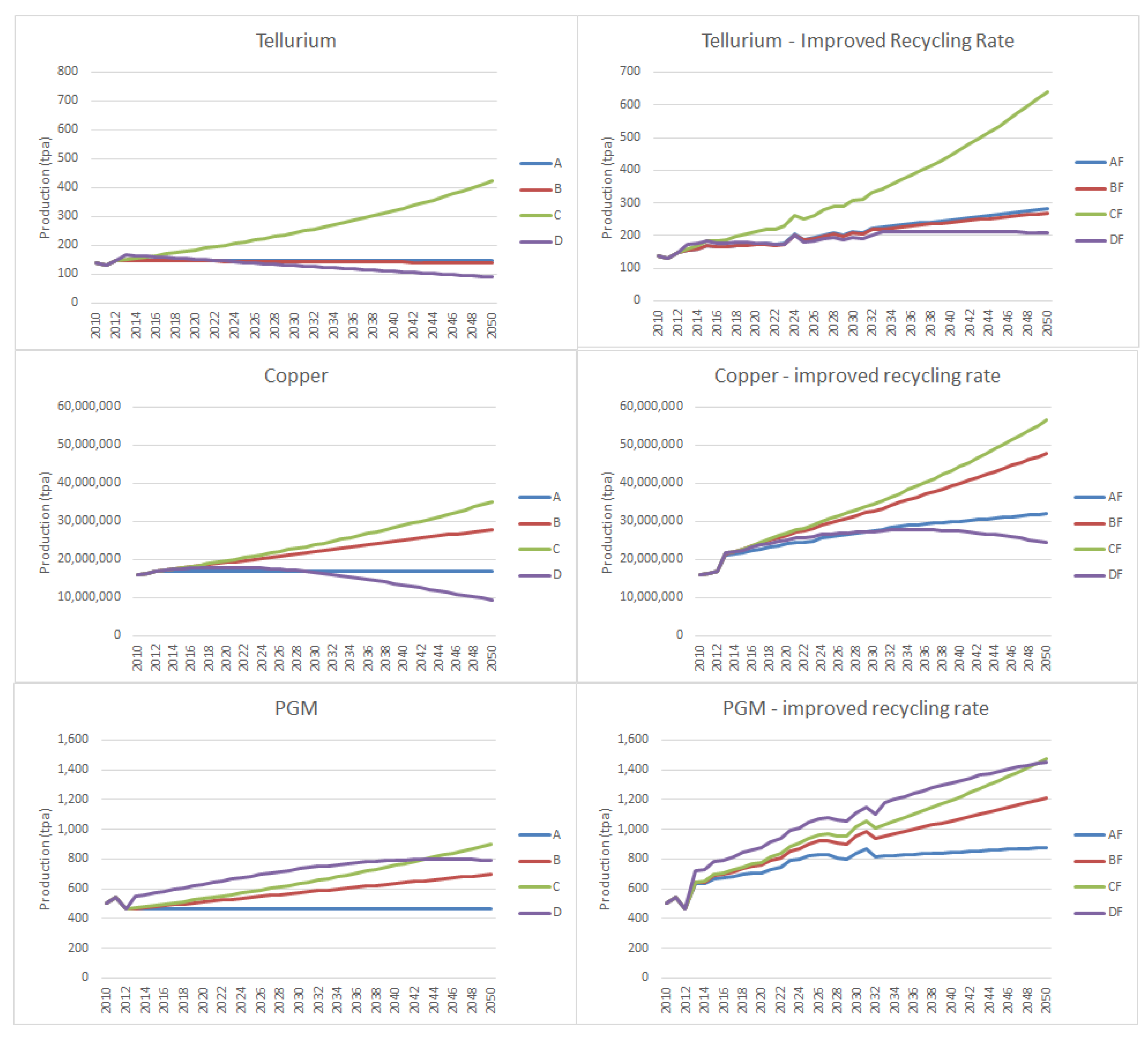

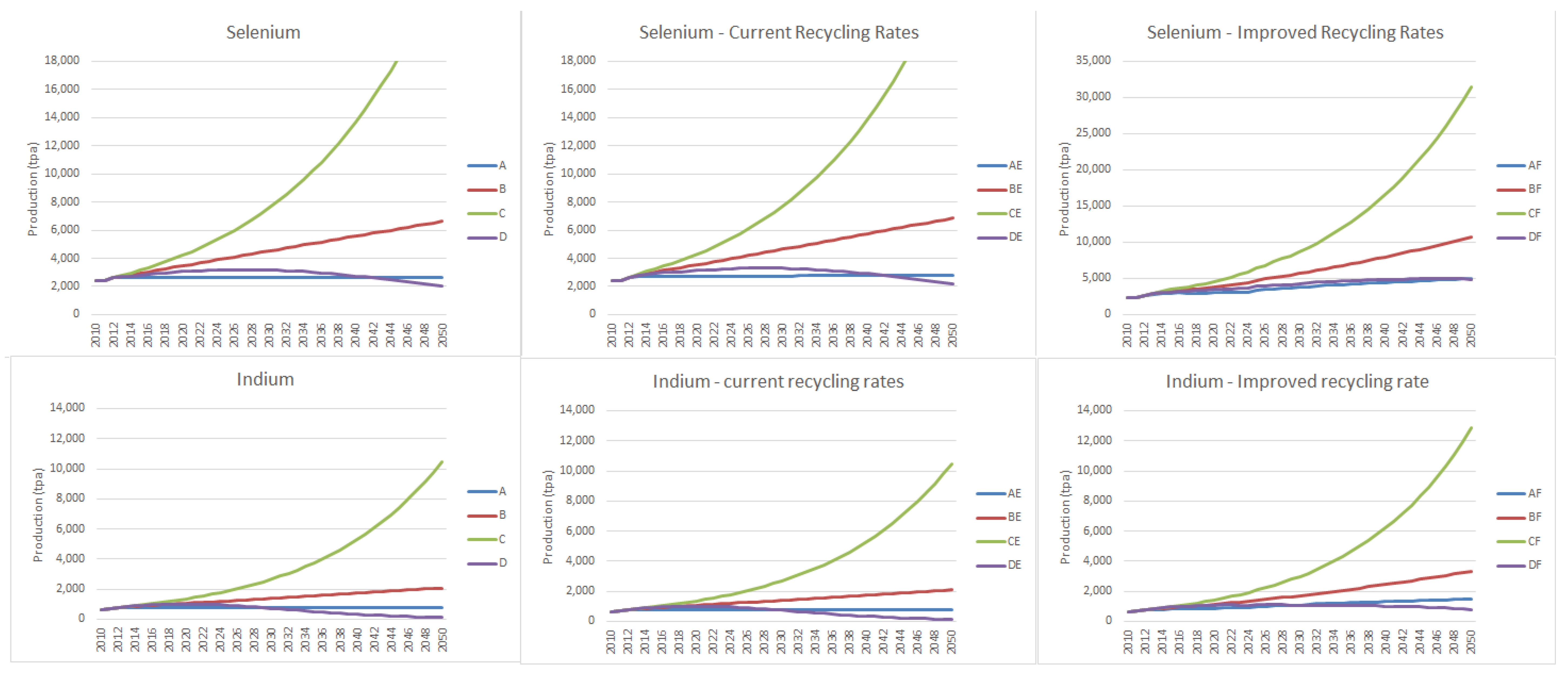

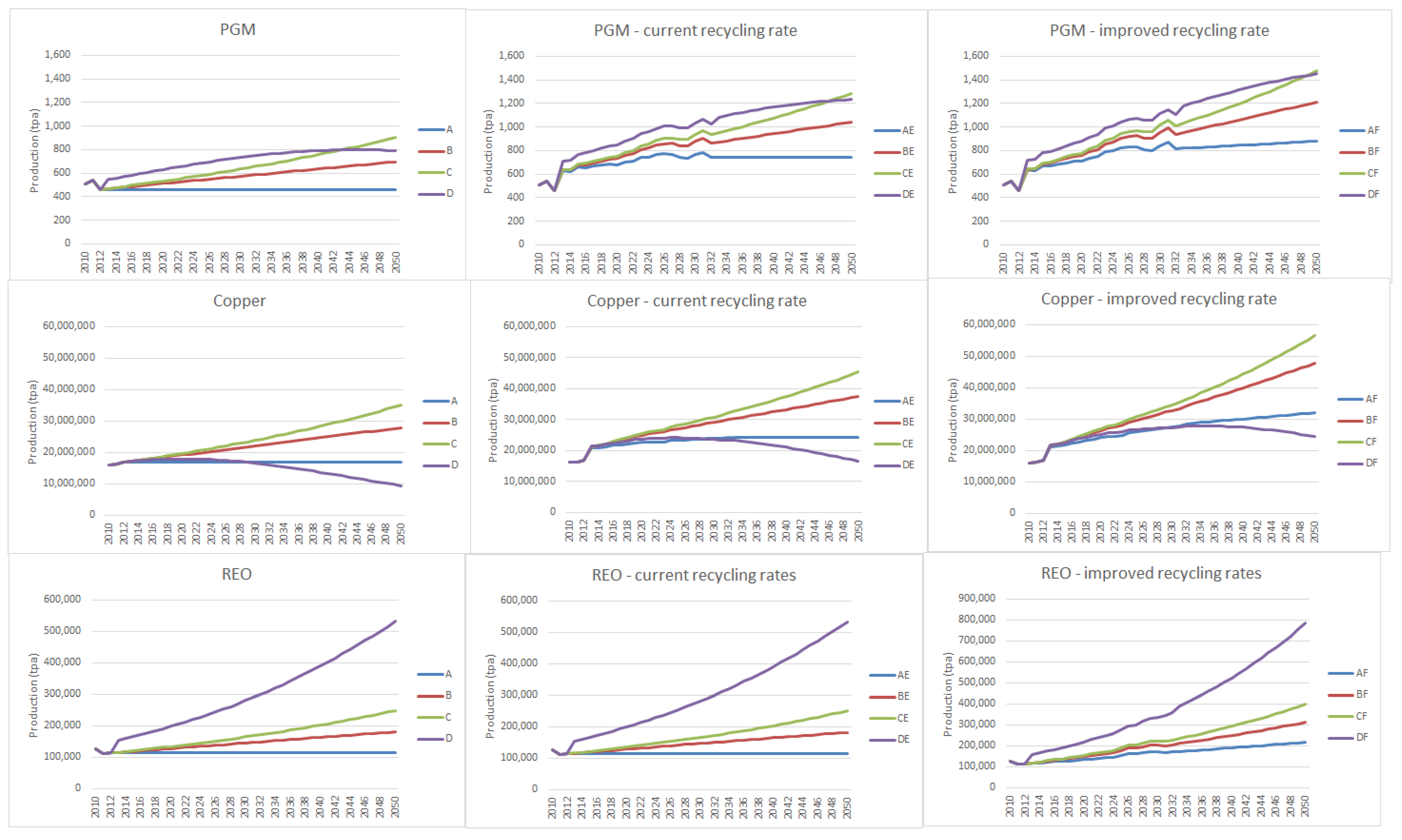

Selected material supply scenarios for the no-recycling and improved recycling conditions are shown in

Figure 10 (a full set is shown in the

appendix as

Figure A1 and

Figure A2). It is important to note that in the exponential and linear growth scenarios, no limitations were put on the growth of production, which is an unlikely reality in the long term, but is perhaps achievable in the short term. In the recycling scenarios, it is noted that the “bumpiness” of the production is attributable largely to the use of actual production data (with a 20-year lag that is the assumed infrastructure lifetime) to determine recycling quantities. The recycling rates used here were obtained from a United Nations Environment Programme (UNEP) report [

57], and there has been no differentiation made here between the end-uses of materials, which may or may not enable the higher rate of recycling (90%) proposed in the improvement scenarios. It may be of interest that, although the D scenarios involve a peak curve estimate, these are largely unpronounced in many of the scenarios; some due to the peak having already arrived, and some are due to it being beyond the 2050 time scale of the scenarios, although the assumed peak is apparent in

Figure 10 for PGM and copper.

Table 7 shows the change in annual production of each mineral from the beginning to the end of the period of interest for each of the scenarios. It is apparent that recycling is important in increasing the rate of production (or reducing the amount of the decrease). The effectiveness of recycling in increasing supply is highly influenced by three factors: the basis rate of recycling, the assumed rate of increase of the recycling rate to the final 90% (scenarios F) and the rate of change of production in the base case. Those metals starting from a low basis recycling rate do not see as great an increase in production as metals with a higher recycling rate, due to the compounding effects of recycling of materials after 20 years, which accumulate faster under the higher recycling rate.

Table 8 shows the cumulative production of metal across the period 2031–2050 (the final 20 years). This does not differentiate between primary and secondary resources, so taking the final 20 years should remove some of the effects of double-counting, as the period under consideration is equal to the assumed lifetime of the product or rate of recirculation.

Table 9 presents the assumptions or estimates of available reserves or resources used in previous studies compared with the URR (reserves plus historical cumulative production used here) of the present study, in order to contextualize some of the alternative estimates. Most studies utilize the data of the USGS for reserves and production, and this has also been used in this case. It is apparent that a few cases express much larger figures; specifically these are associated with the resource data, which has higher geological uncertainty and no guarantee of economic viability. In the present study, we have specifically utilized the reserves data, which provides greater certainty of economic and physical availability; however, this may be seen as a conservative estimate. Still, some of the extreme resource data, and unconventional resources, must be treated carefully in order to not provide over-optimistic estimates.

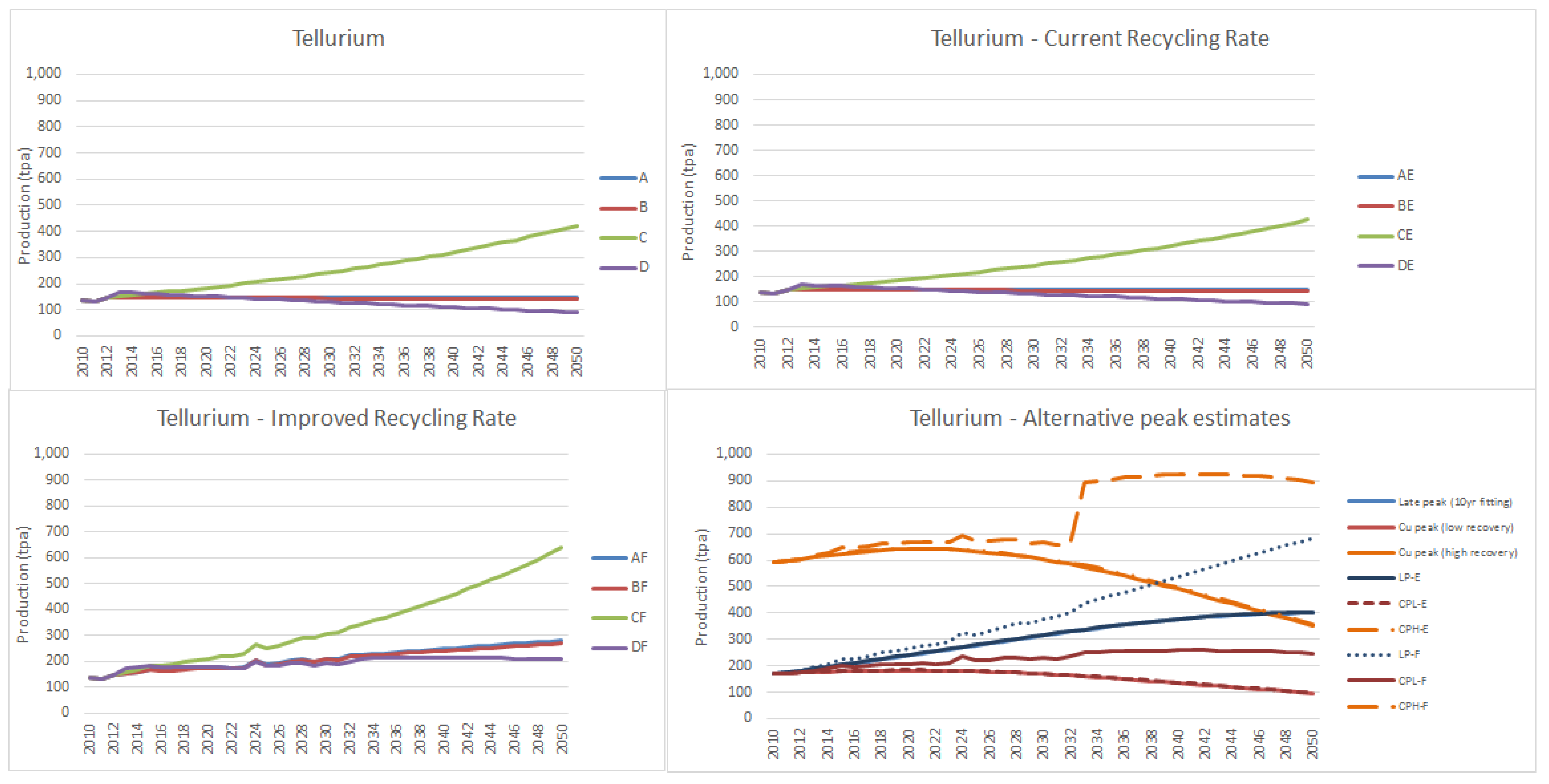

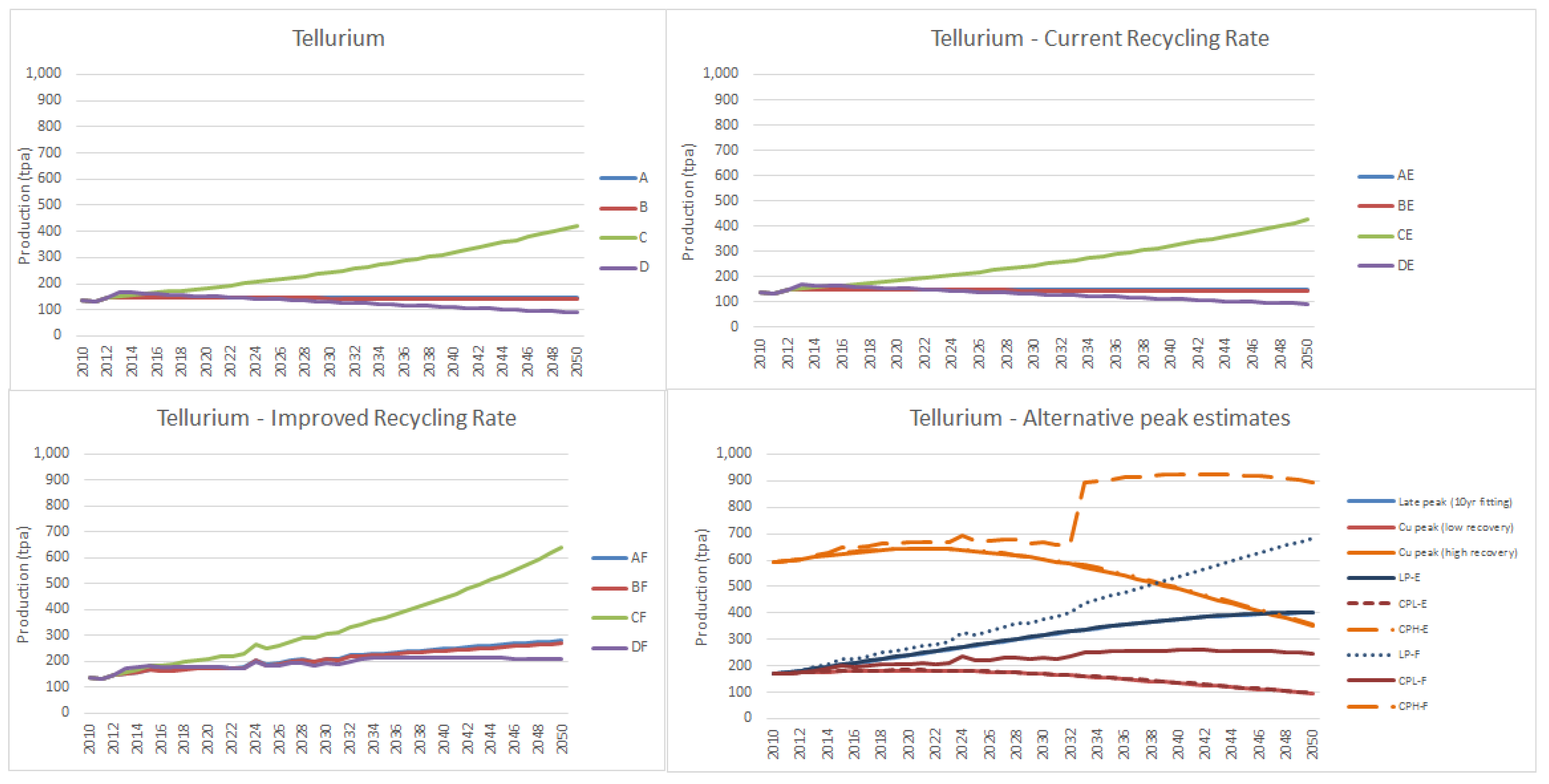

Some specific metals should be treated with particular care. The metals tellurium, selenium and indium are predominately produced as byproducts of copper, lead and zinc. Taking tellurium as an example, a wide variety of future production rates have been given by various authors, and are well reviewed by other authors [

37,

58]. Reviewed estimates of indium availability are 290–26,143 tpa annual production and 625–6000 t cumulative production (to 2020), while tellurium availability is 128–2000 tpa annual production and 5250–47,000 t cumulative production (to 2020) [

37]. These are not directly comparable with the current study (cumulative production shown in

Table 7) but indicate the wide variation of estimates based on different assumptions. As is pointed out very clearly by others [

59], it is also very important to consider the effects of changes in the ore and production techniques for various metals, particularly these byproduct materials. In the case of tellurium, the annual availability is based on the amount of electrolytic copper production, from whose anode slimes the majority of tellurium is currently extracted [

59]. The life of currently mined ore bodies which are processed using this technique is a key limitation on tellurium availability, which may call into question the higher estimates of some studies [

58]. It has been argued elsewhere that the market dynamics of increasing demand should drive price incentives and therefore the better supply-side recovery of such metals [

38]; however, the current study does not consider improved recovery or market forces explicitly, but uses the alternative supply-side models based on trend growth and peak estimations to provide the mineral supply curves. Tellurium is taken here as an example case for byproduct metals and the uncertainty of supply projections.

Figure A2 shows alternative supply curves for tellurium, with consideration that in the base case, the mineral peak is the best fit from the available data, showing a decline from 1975, whereas by fitting to the copper production curve (the mother ore for tellurium) the peak comes later (around 2020 in the current study). Additionally, byproduct recovery rates must be considered as key factors in the availability of these metals. In the extended analysis examining tellurium, we have considered two rates: one with the recent (10 years average) rate of recovery as defined by the ratio of copper to tellurium production, and one with a higher recovery of twice the current rate. Finally, we have included an alternative scenario that fits a peak curve to the most recent data (rather than the full set of data, which presents a dual peak), and this gives a peak primary mineral production of 400 tpa in 2050.

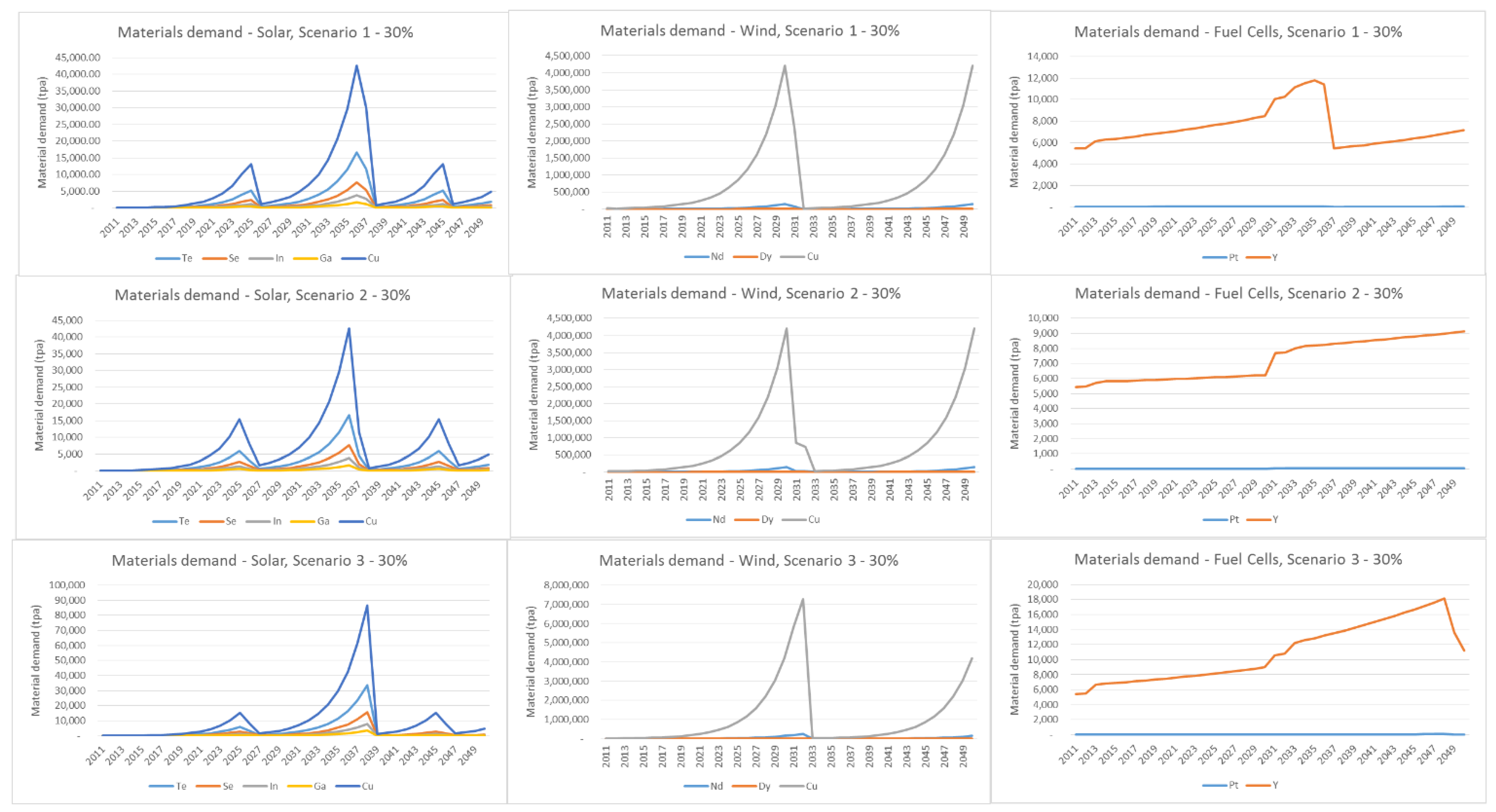

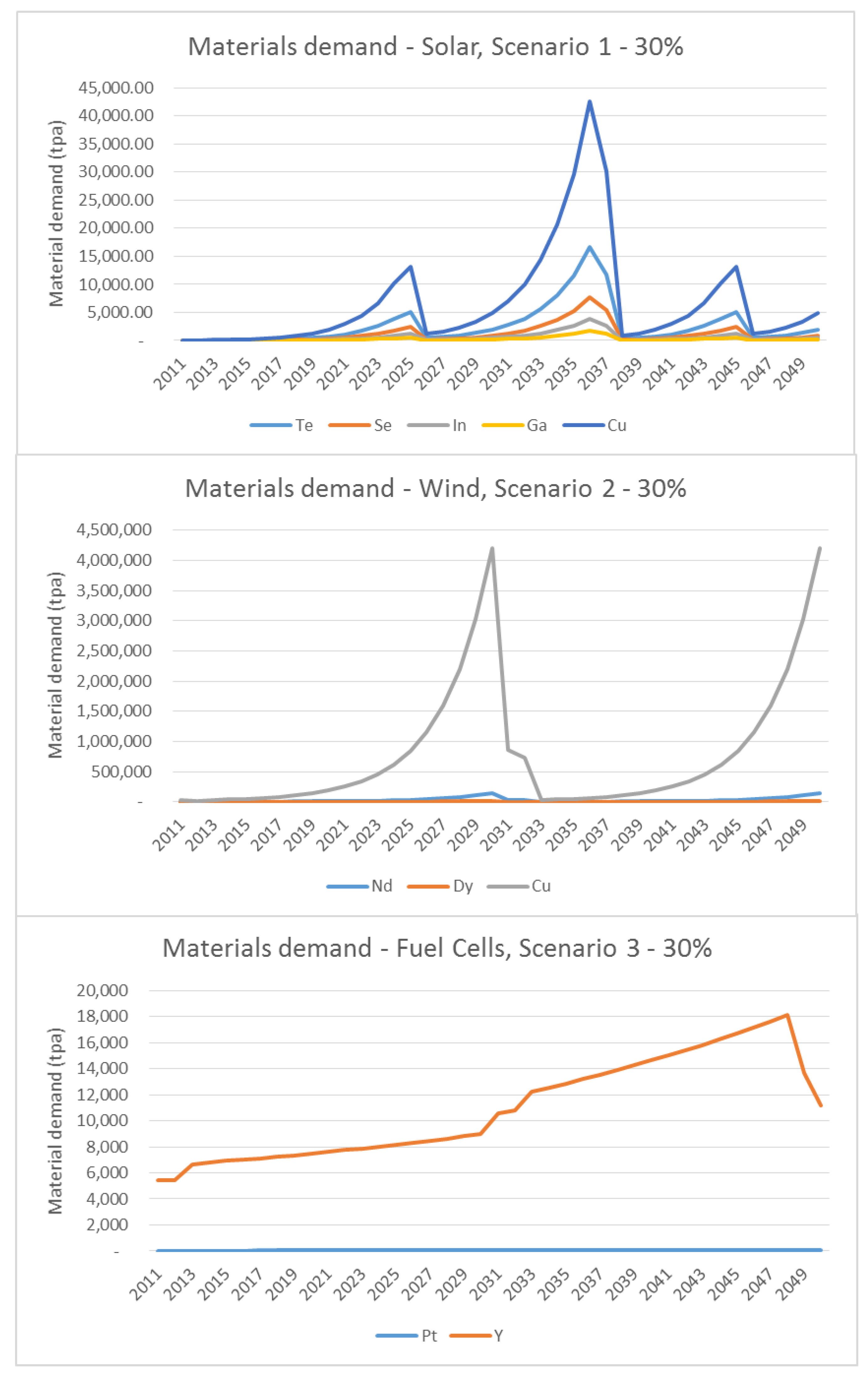

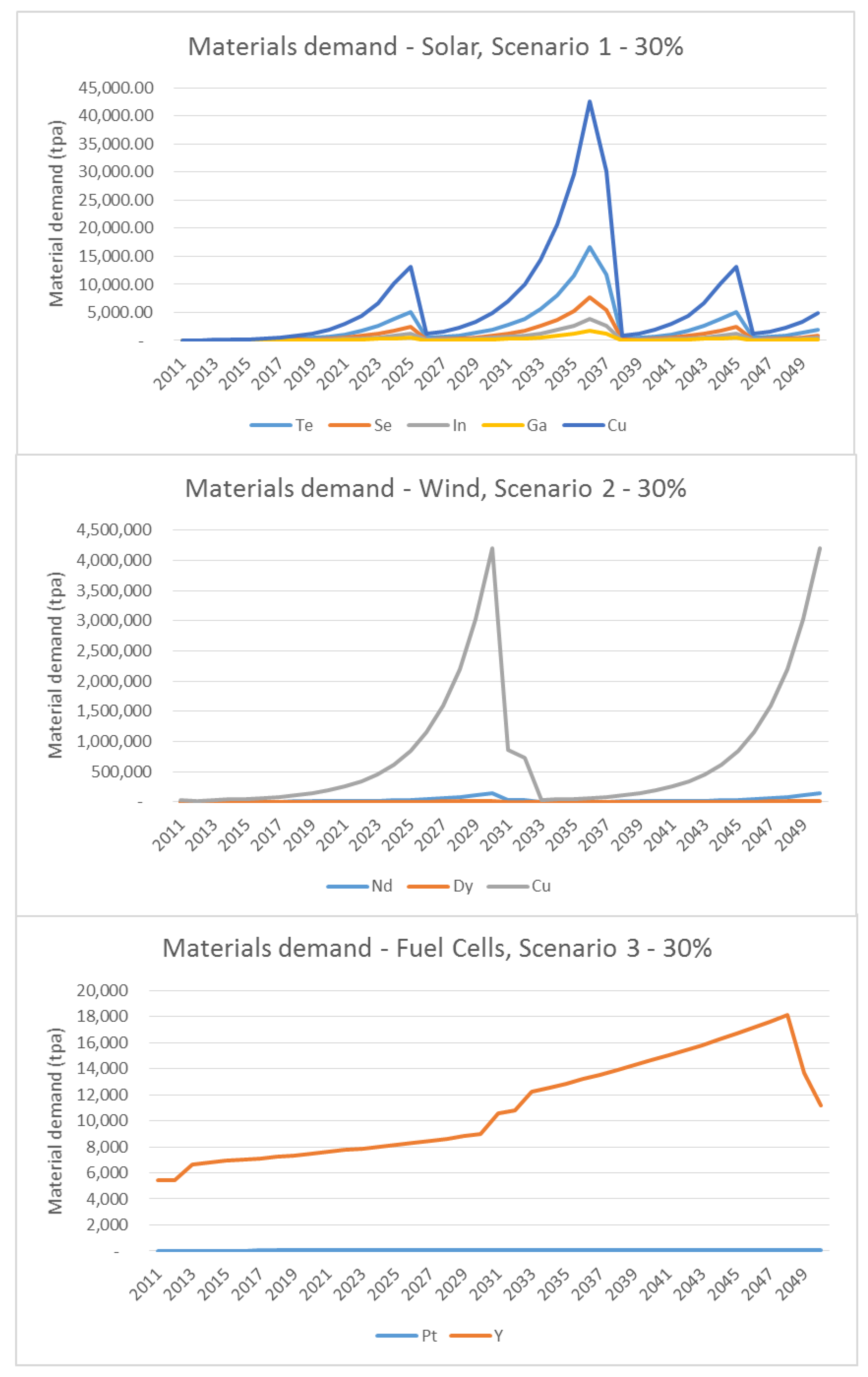

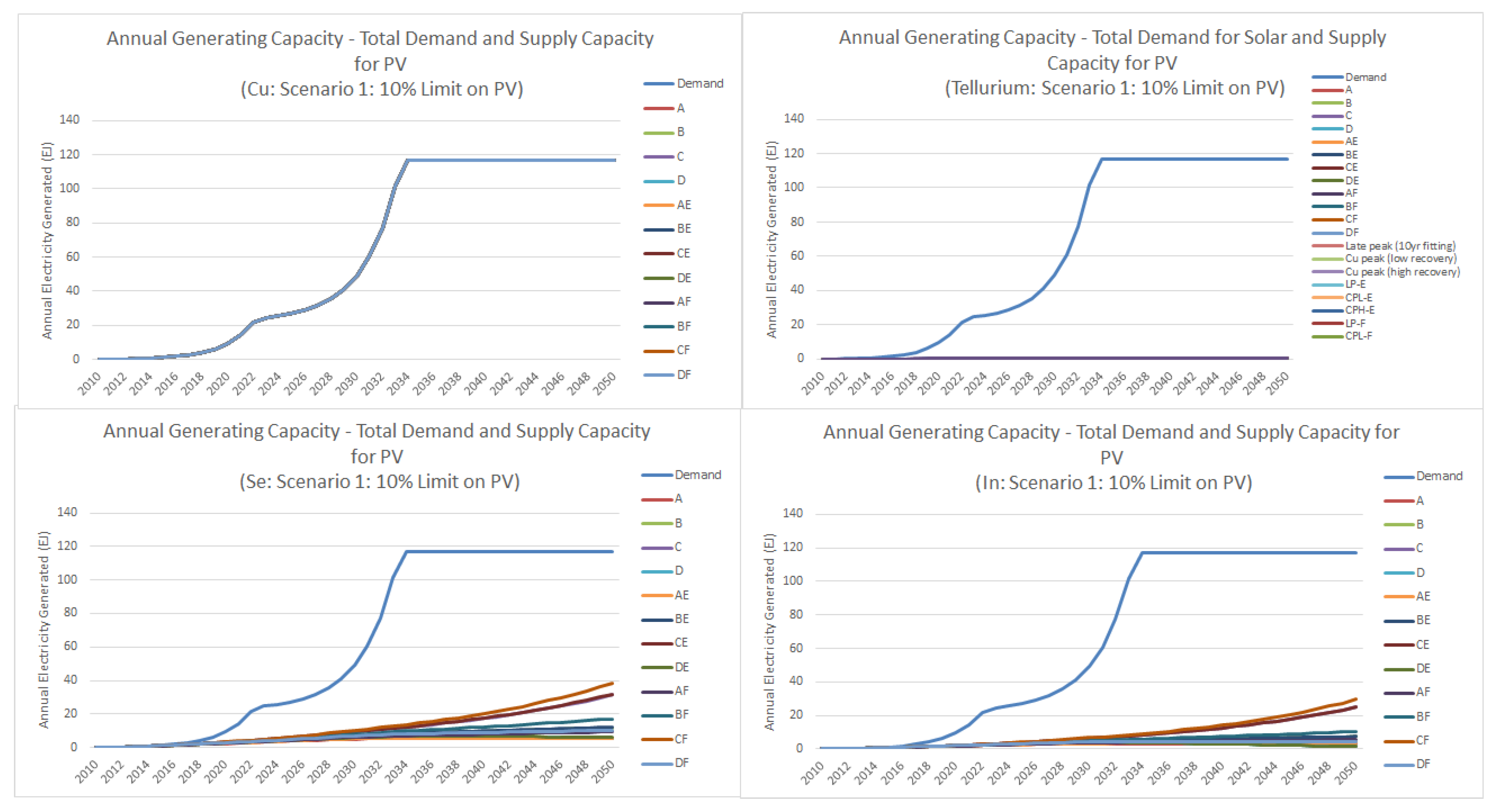

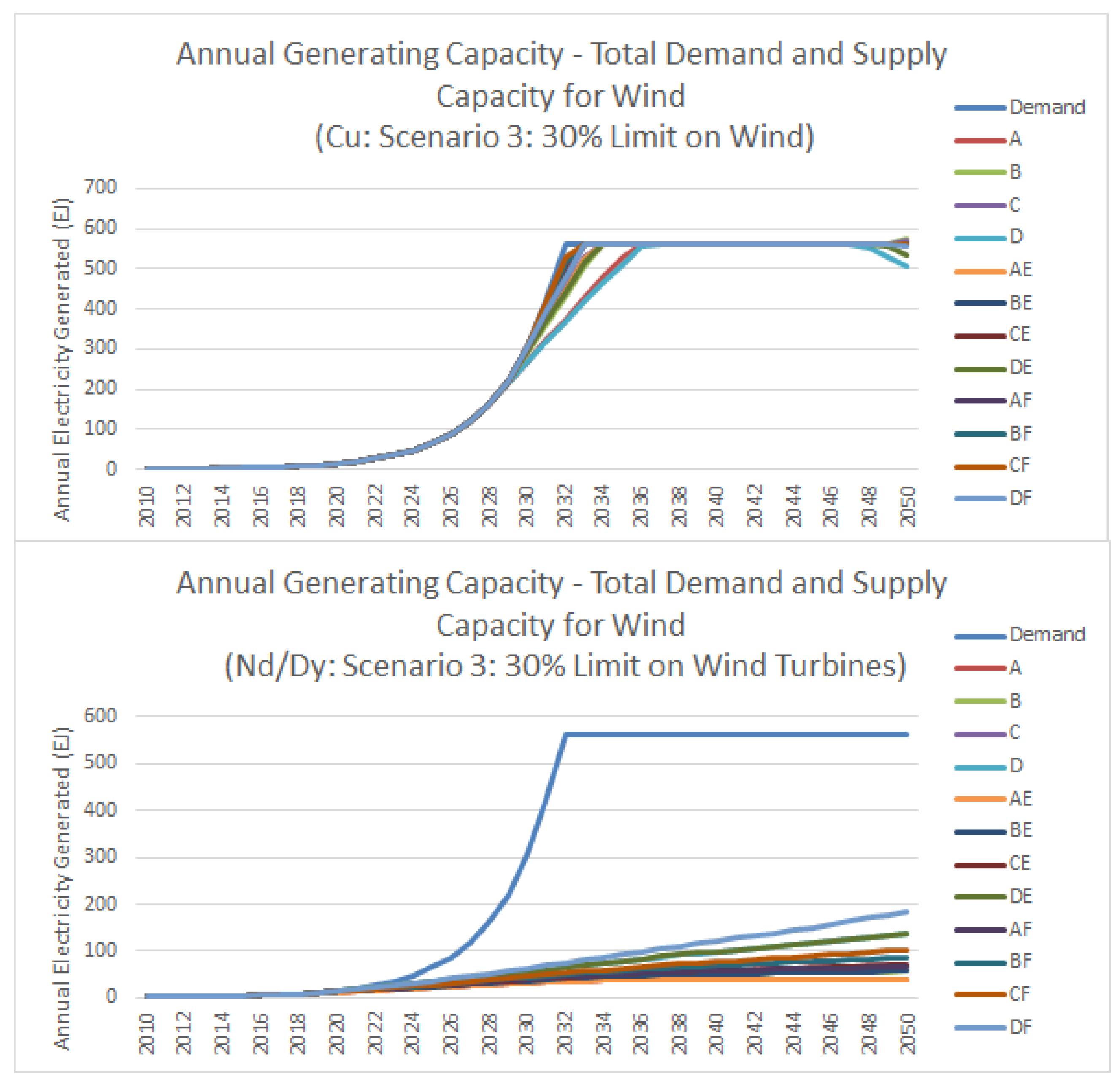

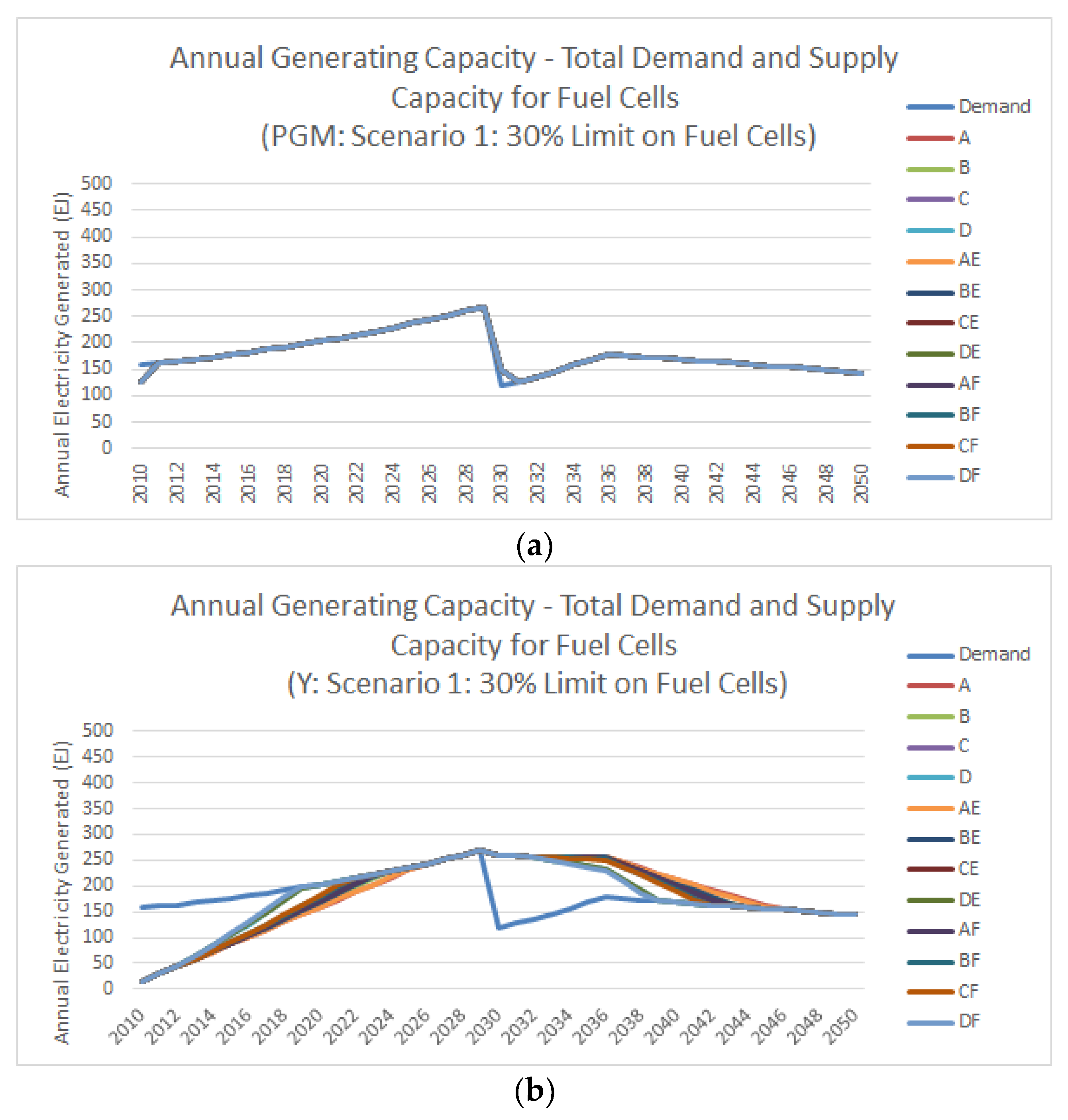

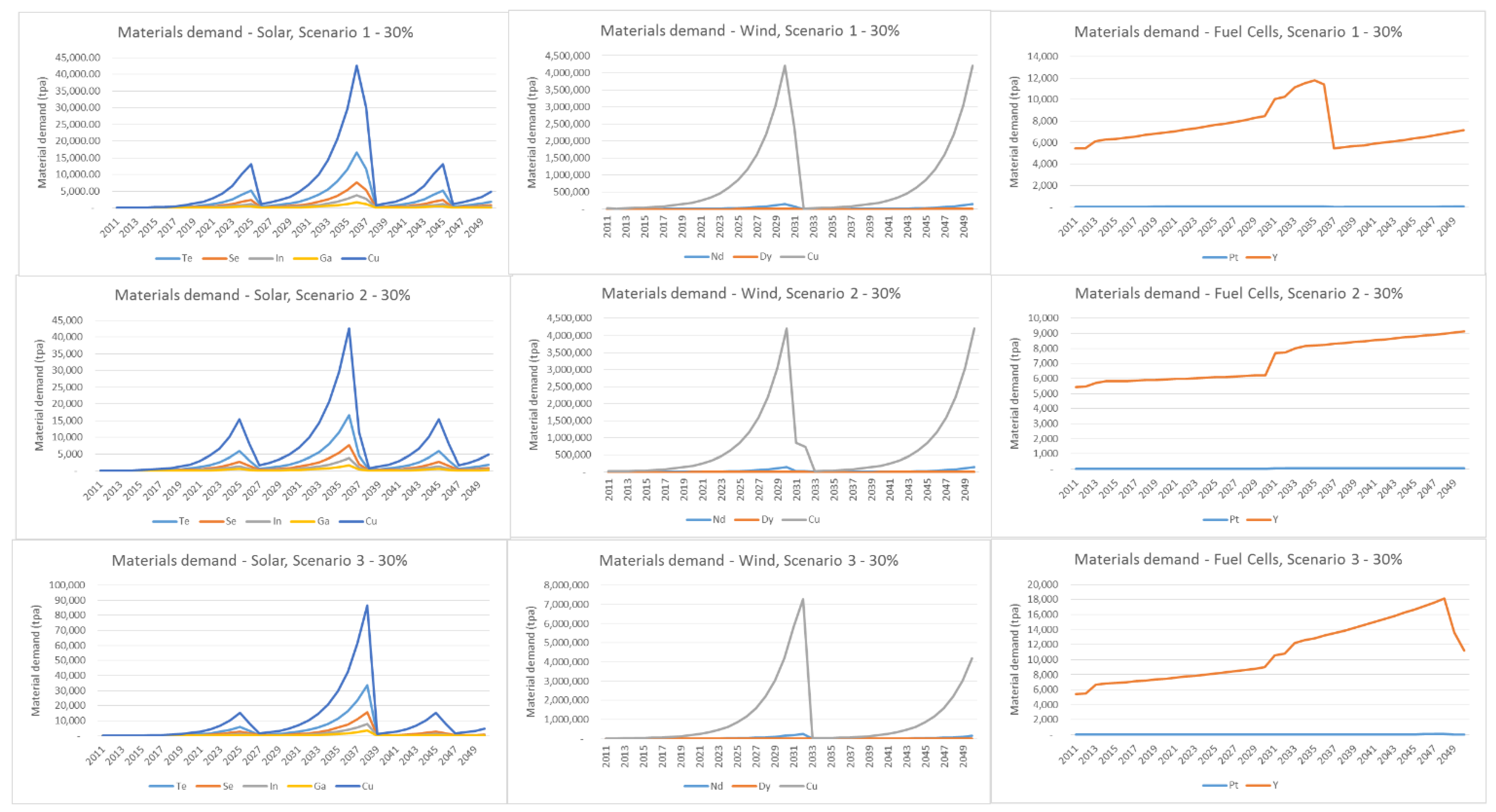

The material demand scenarios, shown in

Figure 11 (full set in

appendix Figure A3), have a series of alternative shapes according to the energy demand scenarios, with waves of demand according to the rate of growth of energy demand and the upper limitation accorded to the technologies in the scenario. In this study, no improvement in the material intensity has been considered, so the estimates are likely to be conservative.

Table 10 presents some of the major reviewed studies’ material intensities for various critical minerals in the selected technologies. As noted earlier, the figures for the current study were obtained during previous work that undertook an extensive review of lifecycle assessment (LCA) studies and other technical and academic literature regarding these technologies [

55]. It may be noted that the current study uses figures that are within the range of other studies, although differences arise in the kg/kW figure due to assumptions of efficiency as well as material per area or unit.

The energy technologies are all allocated a lifetime of 20 years and the need for replacement of existing infrastructure from the beginning of the period, as well as infrastructure installed from 2010–2050, is considered, with the existing infrastructure replacement averaged out over the first 20 years of the scenarios. The total material supply (not just for energy applications) is assumed to become available for potential recycling after 20 years, and is recycled according to the estimated rate (either the current rate or the improved rate, depending on the scenario).

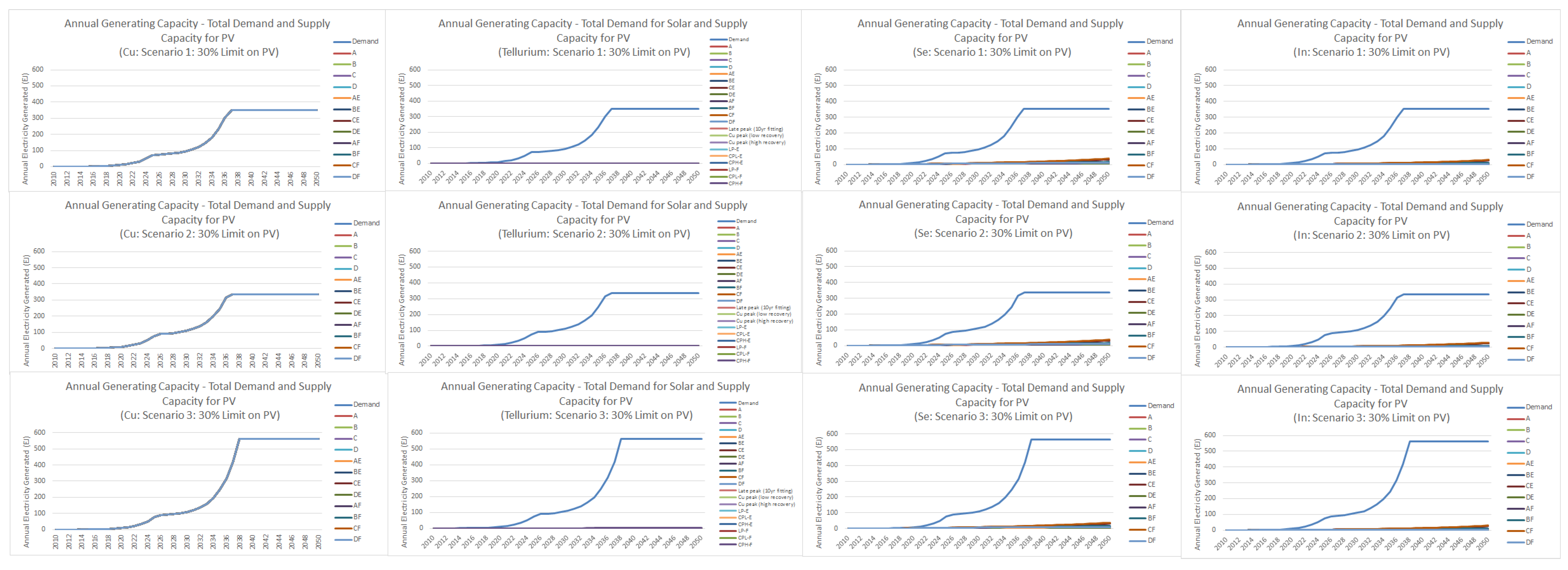

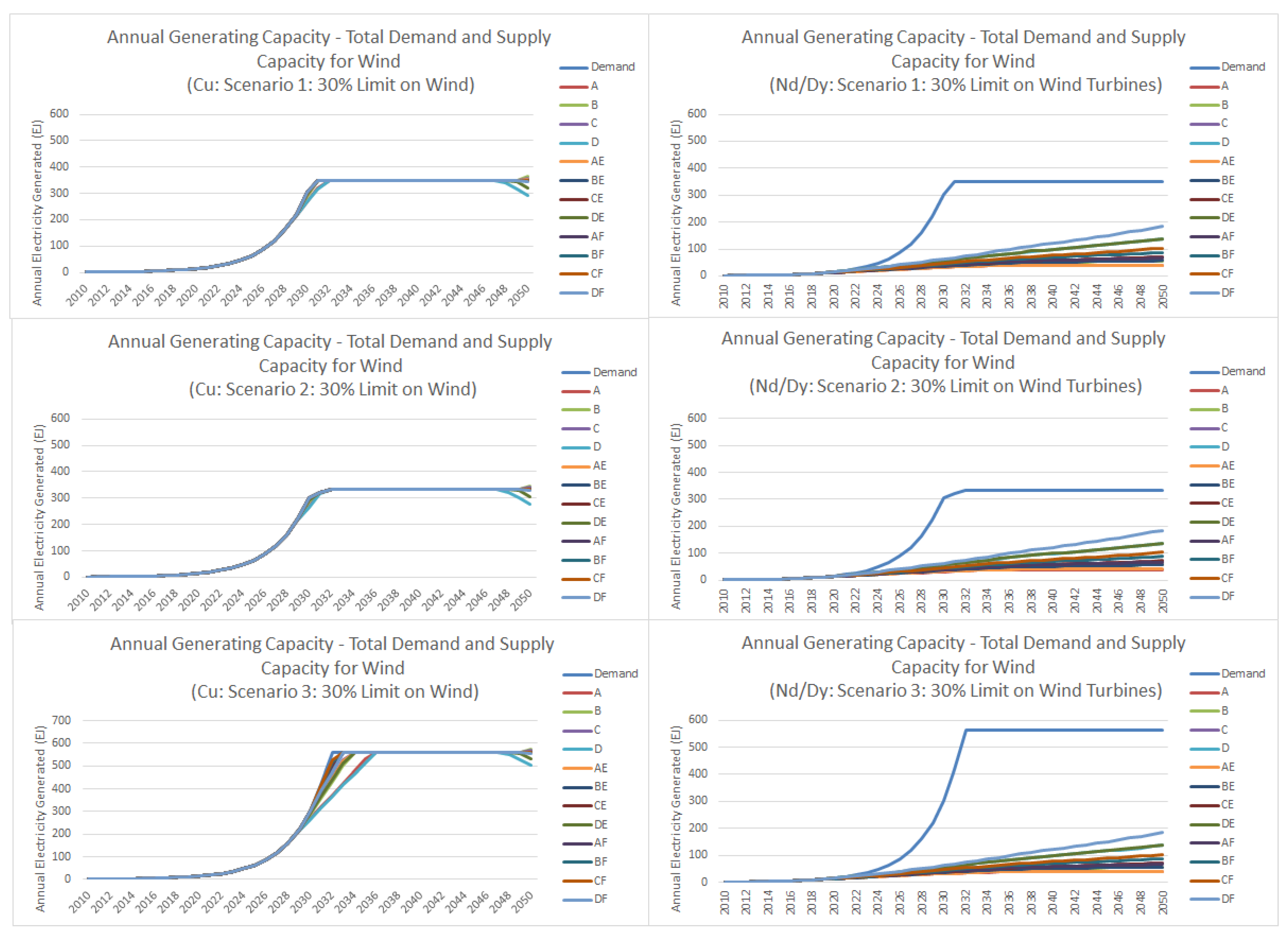

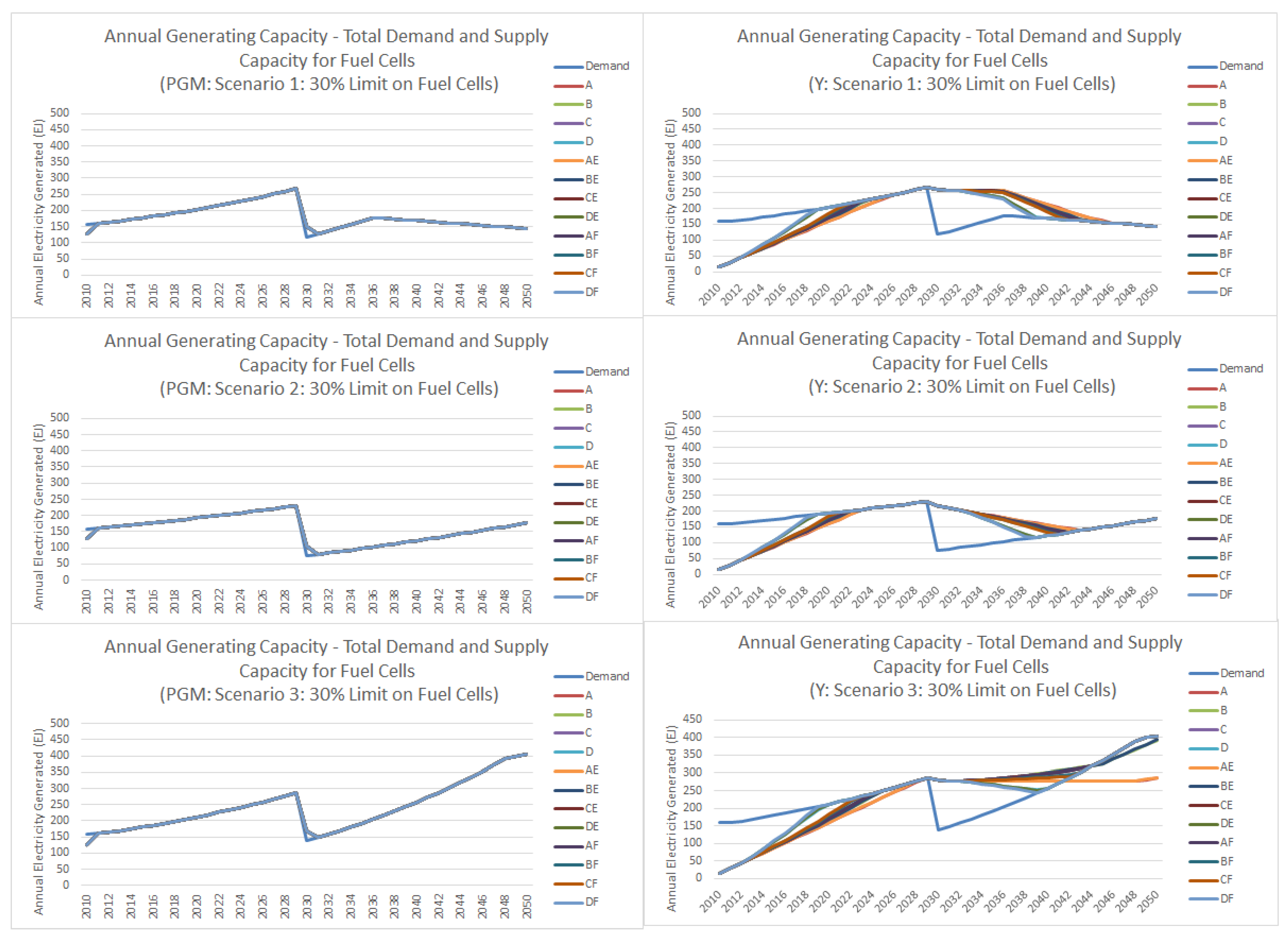

The results of the two scenario processes, supply and demand, were combined in order to determine whether shortfalls in critical minerals could be expected in the future. The combination of the supply and demand scenarios is used to provide a series of potential energy supply paths for each technology. In the case of no limitations, these supply paths under each mineral supply scenario will mirror the theoretical demand. In the case where demand exceeds supply, all of the supply of the mineral for the year will be used to produce the energy technology, and the limit in added capacity will become the real added capacity under that mineral supply scenario. Supply cannot exceed demand, except in cases where the theoretical energy demand declines over time, and the dynamics of the model mean that the decommissioning process will occur only at the end of the technology lifetime (20 years).

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}