Abstract

This study aims to explore the moderating role of corporate governance disclosures on the link between executive board gender diversity and financial performance. Governance disclosures were assessed based on executive managers’ information presented in the companies’ annual reports. The analysis was conducted on Romanian-listed companies from eight industries, covering a time range of ten years. Various robustness tests were used and examined the Blau index apart of the proportion of women managers, as well as different measures for financial performance. The endogeneity issue was solved by the Two-Stage Least Square method and the Generalized Method of Moments. The results revealed that a higher governance disclosure level on executive managers’ characteristics is reflected in increased financial performance. A positive influence was found for the composite financial performance indicator, return on assets, return on equity, and global solvency. Our findings led to the conclusion that the governance disclosure index moderates the relationship between board gender diversity and corporate business performance, and the effect of gender diversity on financial performance will be less positive with a higher level of disclosures on board characteristics. Therefore, managers can filter the quantity and quality of governance disclosure and can monitor the influence of the board’s composition on performance.

1. Introduction

Board gender diversity (BGD) has recently become a matter of significant interest in the business environment, and various studies have analyzed the relationship between the presence of women on boards and the financial performance (FP) of entities. This research falls within the field of corporate governance and has suggested that greater gender diversity on boards can have a positive influence on financial performance.

The concept of BGD and the involvement of women in board leadership began to gain more attention starting in the 1990s with the growing interest in diversity in organizations and its impact on performance. This period marks the beginning of the movement to promote gender equality within organizations, with various policies and regulations being implemented in certain countries (Finland, France, Denmark, etc.). Till 2003, the research on the topic was in its early stages, and empirical works have mainly examined the direct link between BGD and company performance [1,2,3,4]. In the next decade, the research gained momentum, attracting interest from both academics and the business community. Researchers delved into various aspects, including the influence of gender diversity on FP [5], the effects of laws and regulations on gender diversity [6], the way GD influenced corporate social responsibility, and the reputation of companies, and provided international perspectives [7].

After 2013, new streams of research developed, and some major themes emerged on GD influence on financial and non-financial performance, female leadership and leadership style, effects on organizational culture and corporate governance, and the reaction of financial markets to GD. Thus, studies continued to assess the women in board leadership influence on the financial and non-financial performance of companies, including measures like profitability, revenue growth, innovation, and corporate social responsibility. Simionescu et al. [8] demonstrated a positive impact of women on boards on return on assets (ROA) and price-earnings per share (EPS), while Khatri [9] discovered that greater female board representation positively influenced sustainability performance. Soare et al. [10] argued that displacing one male director with one woman director on average negatively affected several indicators. Aluchna et al. [11] showed that there is a tendency of examined Polish companies to choose women in executive boards only in the case of lower-performing companies, demonstrating that higher participation of women in the executive boards is correlated with a decrease in company value on long term, and also gender bias dominates the existing mentality in the capital market. Also, certain investigations explored women’s leadership styles and their influence on organizational decisions [12]. Education and age were also factors influencing management styles [13,14]. The education of entrepreneurs negatively influences the people-oriented leadership style, meaning highly educated women entrepreneurs are less inclined toward people-oriented leadership and prioritize human relations less [15]. However, the age of female entrepreneurs had a positive influence on people-focused leadership, indicating that work experience increased with age, and emphasized the importance of human relationships when leading an organization. García-Meca [16] focused on board diversity, emphasizing gender and nationality diversity, and found that banks’ BGD had a significant positive effect on corporate performance. In the meantime, other studies [17,18,19] explored how BGD influenced organizational culture and governance practices.

According to the European Institute for Gender Equality, in 2024, with a score of 57.5/100, Romania ranked last among EU member states in terms of gender equality [20]. The World Bank report [21] shows that Romania has the largest gender gap among EU states in terms of labor force participation rates. Businesswomen are underrepresented on the boards of large publicly traded companies and are also paid less than men. The situation is no different in the entrepreneurial sphere, where there is a 4% gap [21]. In Romanian culture, the idea that women’s primary role is to take care of the home and family (children and the elderly) is deeply rooted in the collective consciousness. Eight out of ten Romanians embrace this idea, which makes the process of eliminating gender inequality difficult. But things are evolving. The Romanian Government is making efforts to reduce these gaps. Some of the main objectives of the National Strategy for the Promotion of Equal Opportunities and Treatment between Women and Men 2018–2021, continued by the one for the period 2021–2027, are promoting work–life balance, as well as increasing women’s involvement in decision-making processes.

The statistics underlying this strategy show that although more women are reaching university studies, they mainly specialize in feminized fields such as Educational Sciences or Health, and too few are in Information and Communications Technology, and Engineering (approximately 30% in 2017). At the same time, their interest in doctoral studies is lower than in master’s studies, including in already-feminized fields. Gender imbalances existing in the Romanian educational system are subsequently reflected in the labor market. This also explains the lower remuneration of women, as they occupy jobs in lower-paid fields, according to their major. However, according to the study conducted by PwC [22], Romania has made important steps in reducing gender disparities in the labor market. However, the wage gap persists (21.6% in 2023), with the banking sector making the largest negative contribution (with a 30.5% wage gap in favor of men). The situation has also improved in terms of women’s representation in management positions. In total, 62% of companies listed on the Bucharest Stock Exchange had at least one woman on the board of directors in 2020 (20% more than in 2015), and 65% of companies had women on executive committees in 2020, compared to 53% in 2015, according to the Deloitte and PWNR report [23]. The same report concludes that it is important for women to be involved in advisory boards within large, growing, or IPO entrepreneurial businesses, thus contributing their expertise to support executive teams.

The present study falls into the mainstream that investigates different executive board characteristics, such as competence, education, innovation skills, heterogeneity, professional expertise, independence, diversity, cultural background, and their impact on corporate performance [24,25,26,27,28]. As Al Frijat et al. [29] highlighted, board-of-directors competence is an intangible capital that can stimulate the increase in the involvement degree of the company in CSR activities and also enable the increase in FP. In this respect, the present work aims to investigate the moderating function of board characteristics disclosure on the nexus between BGD and FP.

The current research wishes to add knowledge to the analysis of the moderating effects exerted by various factors seeking to reveal new governance strategies from the perspective of listed companies. Moreover, the purpose was to discuss to what extent the board executive characteristics-disclosure degree influences the intensity of the relationship between GD and financial indicators. The rest of the paper is organized as follows: the second section synthesizes the review conducted on scientific similar works and the research assumptions; the next sections contain the data and methodology, followed by empirical results, robustness test, and a discussion on the analysis of endogeneity; and rest of the paper covers the conclusions, implications, contributions, and also limits of the study.

2. Materials and Methods

2.1. Previous Studies Related to the Moderation and/or Mediator Impact on Gender Diversity and Corporate Performance Connection

The subject of this research falls within the scope of the implications of several theories, of which agency theory and resource dependence theory are considered to be the most relevant. Agency theory traces the relationship between the principal (the shareholders within a company) and the agent (the company manager or board of directors). Due to information asymmetry (management has more information about the company than shareholders), agents may act in their interest, which is not necessarily the interest of the principal. This theory seeks solutions to agency problems that arise from divergences in objectives and risk tolerances between the principal and the agent [30]. By strengthening governance mechanisms, the presence of women in director positions helps reduce agency conflicts between owners and managers, ensuring better oversight [31]. Resource-based theory, also known as the resource-based view, was initially launched by Birger Wernerfelt in 1984 [32] and later refined by Jay B. Barney [33]. According to this theory, a company achieves a lasting competitive advantage by relying on its unique resources and capabilities, as long as they are valuable, rare, difficult to copy, and indispensable. By intelligently exploiting these internal elements, the firm ensures a superior market position and offers added value to customers [34]. Directors of different categories provide the company with different categories of resources [35], with female directors contributing their relational skills and empathy to gain a competitive advantage for the company.

As interest in this research topic grew and became more sophisticated, subsequent studies began to explore moderating effects, bringing in-depth knowledge of the relationship between the board of directors’ gender diversity and corporate performance. Works on the moderator–mediator effect appeared in the literature in the early 1980s. A mediator variable is causally situated between one variable (A) and another (B) and is the channel through which A transmits its effect on B. A mediator can be almost anything that is instigated by A, but then causally influences B [36]. Moderating effect refers to a variable that can influence the direction or strength of the relationship between an independent variable and another dependent variable. Thus, moderation involves individual differences or circumstantial conditions that can change how two variables influence each other [37,38]. In a mediation process, the mediator clarifies the link between an independent and a dependent variable [39]. If a mediation analysis focuses on examining how an effect operates, moderation analysis is used when the interest is directed toward questions about when that effect occurs [36]. Under what circumstances does one variable, A, influence the other, B? As Hayes [39] pointed out, moderating variables are those circumstances or cases that influence the magnitude of a variable’s effect. According to Holbert and Park [40], moderation analysis is important and relevant in research because studying the moderating effect of a variable on a construct can provide insights into the relationship between two or more variables.

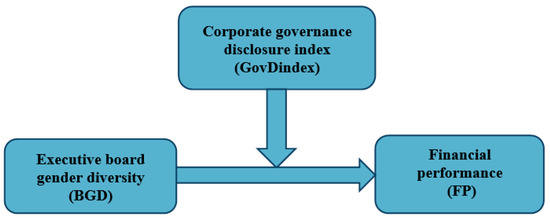

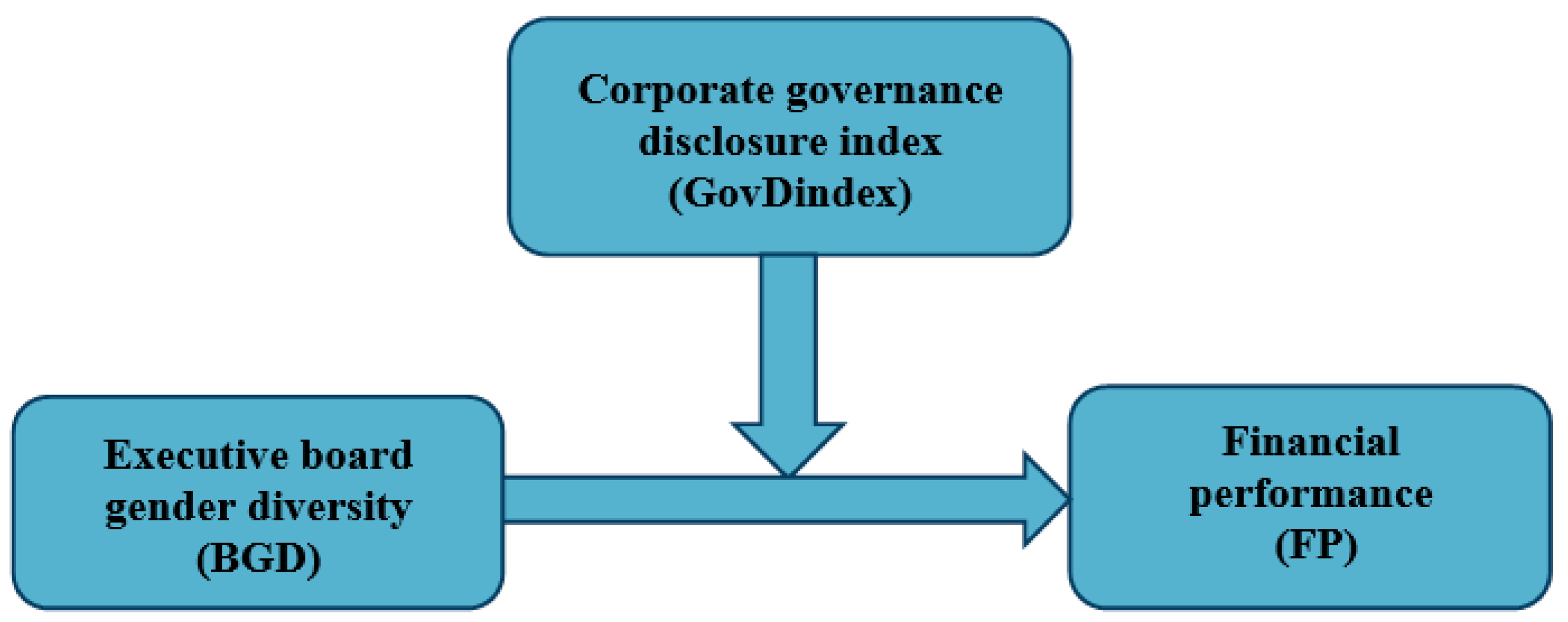

Recently, researchers have delved into these concepts to gain deeper insights into the intricate dynamics between variables and their influence on economic phenomena. For instance, García-Meca [16] examined how institutional factors, such as investor protection and banking regulations, could moderate the relationship between board diversity and bank performance. The specific characteristics of these institutional factors were found to shape the impact of diversity; for example, in countries with weaker regulations and lower investor protection, the influence of board diversity on bank performance might be diminished. Wang et al. [41] discovered a positive correlation between entrepreneurial growth strategies and unethical corporate behavior. Governance mechanisms such as management stock ownership and executive functional diversity were also found to moderate the relationship. The present study explored the moderator effect of governance (executive board characteristics) disclosures on the relationship between executive BGD and FP, illustrated in Figure 1.

Figure 1.

Conceptual research model.

Investigations on the moderating and/or mediating effect of board diversity on performance considered different aspects of diversity, such as age, experience, nationality, and education diversity of board members, and GD, providing relevant insights for improving corporate governance and making better decisions on board composition. Karajeh [42] found that both structural and demographic diversity significantly improve company performance, with ESG acting as a moderating and partially mediating factor. The mediating role of strategic R&D decisions in the relationship between top management team overseas’ experiences and innovation performance was highlighted by Yang et al. [43], while Dezső and Ross [44] argued that innovation intensity positively moderates the impact of female representation in top management on corporate performance, particularly in innovation-focused firms. Jing et al. [14] demonstrated how female leaders’ characteristics enhance knowledge sharing and employee innovative performance, offering insights into female leadership and innovation. Fan et al. [45] discovered that women on boards had a more significant impact on bank-earnings manipulation, especially those with higher education and significant board experience. Song et al. [46] studied internationalization’s impact on gender and age diversity in firm performance. They found that gender diversity positively affects performance, but age diversity does not. Al-Jaifi et al. [47] discovered that board independence moderates the relationship between seniority and GD and environmental performance, enhancing the independent board’s impact on environmental performance. Marquez-Cardenas et al. [48] explored the relationship between BGD and FP, from agency-theory and resource-dependence-theory perspectives, finding that board independence does not significantly affect the requirement for women on boards. CEO duality and sustainable performance were investigated by Zhu et al. [49]. Women in CEO roles positively impacted sustainability, while CEO duality had a negative effect. Alodat et al. [50] found that BGD positively affects performance, with sustainability disclosure mediating this relationship. In contrast, Shah and Ivascu [51] showed that an active board benefits performance, with environmental performance and ecological innovation enhancing this effect. Al-Jaifi et al. [47] emphasized the impact of age and GD, while Shakil [52] delved into ESG performance as a moderating factor in the relationship between diversity and financial risk. Albitar et al. [53] examined ESG diversity, observing its positive influence on corporate performance, analyzing ownership-concentration, gender-diversity, and board-size influence. Fayyaz et al. [54] examined board diversity’s role in European sustainable companies’ performance, highlighting its structural and demographic benefits, along with the ESG disclosure mediating function. Kahloul et al. [55] and Fatma and Chouaibi [56] investigated the BGD and FP connection, emphasizing the CSR’s moderating role, considering the influence of organizational culture and values. Also, Galbreath [57] emphasized that women on boards shape CSR behavior and enhance FP. Mohsni et al. [58] revealed that BGD negatively relates to operational and financial risk, but it positively connects to performance, and post-crisis, GD assumed a more prominent role in risk management.

2.2. Hypotheses

The board of directors exerts control and management over specific companies’ business procedures, as well as providing information to the market. All interested parties are interested in board composition and the role of its members because certain people have specific knowledge and can bring a great contribution to the entity [59,60,61,62]. Company FP is crucial for all stakeholders, but especially for shareholders. Müller [63] studied the factors that influence FP, focusing on the relationship between leadership ability, as well as board composition, and the business performance assessed by the ROA indicator. He argued that foreign members’ proportion and board independence exert a strong influence on performance. Inostroza et al. [64] analyzed the decision-making style’s effect on the FP of SMEs by gender and examined how decisions are made, in particular, identifying clear evidence of mutual influence between gender and decision-making ways, especially between gender and the dependent style. Le and Nguyen [65], using fixed-effects (FEM) and random-effects (REM) regression models with panel data, showed that ownership has a positive influence on financial performance; however, board size has a negative effect on financial performance, and supervisory board characteristics have a positive effect on financial performance of Vietnamese listed companies.

The results of the study conducted by Müller et al. [66] on a sample of the largest listed European companies show a statistically significant relationship between the ROA indicator for the current year and several characteristics of the board composition (number of directors, board independence, proportion of foreign directors, average tenure of non-executive directors, CEO tenure, and proportion of women as directors), as well as the characteristics of the board remuneration (the basic fee of the non-executive director, additional remuneration for board committee members, and fees paid in shares). On the other hand, the results obtained by Suciu et al. [67] proved direct and significant impacts, both favorable and unfavorable, on the financial performance of the examined European companies, determined by human capital management on the topic of diversity and inclusion. Suciu et al. [67] argued that the empirical analysis highlighted the need to mitigate risks regarding the sustainability of financial performance by developing strong and efficient inclusion and diversity strategies.

Also, various studies developed by Iliev and Roth [68], Oh et al. [69], Hu et al. [70], Tang [71], and Dang et al. [72] examined the professional experience and other board characteristics and how they add value to the company. Therefore, a significant association between business governance factors and company performance was found. Moreover, as Raimo et al. [73] highlighted, several board characteristics (gender diversity, independence of directors, and meetings’ frequency) are positive drivers of integrated reporting disclosures. Based on five corporate governance characteristics, two profitability indicators (ROA and ROE), and one market indicator (Tobin Q), and by applying a regression analysis model on panel data, Nxumalo et al. [74] showed that corporate governance characteristics have a mixed influence on company profitability, with some indicating a negative or non-significant relationship, revealing the complexity of this association. The study by Nxumalo et al. [74] demonstrates that if a company chooses and implicitly discloses appropriate corporate governance characteristics, a firm’s profitability can be improved

Since in the last decades, disclosures of corporate governance information have significantly increased, we stated the first hypotheses.

H1:

Executive board characteristics disclosure positively affects financial performance.

H1a:

Executive board characteristics disclosure positively affects earnings per share (EPS) indicator.

H1b:

Executive board characteristics disclosure positively affects return on assets (ROA) indicator.

H1c:

Executive board characteristics disclosure positively affects return on equity (ROE) indicator.

H1d:

Executive board characteristics disclosure positively affects global solvency (SOL) indicator.

The study conducted by Hong and Kim [75] challenged us by the fact that its results showed the positive influence of female executives on business value; however, the impact weakens as the co-CEOs’ power gap becomes larger. Rubino et al. [76] noted that foreign and busy women directors negatively affect performance, while graduate women executives enhance the positive connection between female directors and business performance. In a recent investigation, Neuberger et al. [77] found that corporations that had more than three women on board also benefited from external recognition. Among the studies that analyze the influences of board characteristics on the disclosure practices is the one conducted by Chouaibi et al. [78] that applies multiple linear regression analyses, and the results demonstrate that board size and independence positively and significantly influence the disclosure degree of environmental information. Aly et al. [79], using the Generalized Method of Moments (GMM), show that board independence and board meeting frequency are significant determinants of environmental disclosure for British companies, and board independence and audit committee independence are significant determinants of environmental disclosure for American companies and support robust governance systems whose implementation can determine information asymmetry between companies and stakeholders.

Suherman et al. [80] focused on individual characteristics’ relevance to the process of appointing CEOs and emphasized that some of these determine the increase in company performance (number of women, seniority and experience, professional education, and foreign nationality), but some characteristics negatively influence performance, such as the age of the directors, the older they are, and the more conservative and inflexible they are to change. T.T.C. Nguyen and C.V. Nguyen [81] showed that the higher level of education of financial directors (master’s and PhD) does not affect the profitability of listed entities in the construction and real estate sectors, as the probability that these companies are more profitable than others is not verified. Zavertiaeva et al. [82] argue that committee independence positively influences company performance, but it also moderates the relationship between committee structure and performance. Thus, committee independence can amplify the positive influence of governance and female ownership on performance. In a recent study, Rahman et al. [83] found that ROA positively moderates the relationship between experience, business education, independent status, and experience associated with female CEOs, as well as their representation on the audit committee, with sustainable corporate practices. Also, ROA emphasizes the positive impact of female directors’ master’s degrees and other higher qualifications on sustainable practices more than bachelor’s or lower education [83].

Espinosa-Méndez and Inostroza Correa [84] examined the sociodemographic characteristics of the CEO and whether they are connected to performance or moderate the gender–performance relationship and found that CEO characteristics do not exert a statistically significant impact. However, Rahman and Zahid [85] argued that board monitoring significantly mediates the women directors and business performance connection. Following these studies that focused on the examination of governance variables and their moderating or mediating effect, we state the following hypotheses:

H2:

The board gender diversity and financial performance connection is moderated by executive board characteristics disclosure.

H2a:

The board gender diversity and EPS relationship is moderated by executive board characteristics disclosure.

H2b:

The board gender diversity and ROA relationship is moderated by executive board characteristics disclosure.

H2c:

Executive board characteristics disclosure moderates the board gender diversity and ROE relationship.

H2d:

Executive board characteristics disclosure moderate the board gender diversity and SOL relationship.

2.3. Data and Methodology

The current research looks to investigate the moderator function of the corporate governance characteristics disclosure index on the executive BGD and FP connection. In this respect, fifty-seven privately listed companies at the Bucharest Stock Exchange (BSE) from eight industries were analyzed for a time range of ten years. Following works conducted by Orlitzky et al. [86], Margolis et al. [87], Brahma et al. [88], Wang et al. [89], Arora [90], and Bogdan et al. [91] to measure FP, proxies such as ROA, ROE, SOL, and EPS were used, and also a composite metric was used as an aggregate variable, called financial performance composite index (FPindex). This composite FP index was designed by applying multivariate principal component analysis based on panel data. The corporate governance disclosure index was calculated based on the scoring (awarding grades) technique. Therefore, grades were assigned depending on the disclosure or presentation degree of information on executive managers’ characteristics. Thus, to quantify a detailed level of disclosure of information, score 2 was attributed while, for no information disclosed, 0 points were assigned. The used scale was [0; 1; 1.5; 2]. Relevant information counted for executive managers considered their education; professional qualifications; professional experience; training and other forms of continuous professional learning; management experience; various complementary professional abilities and competencies; personality traits; incentives; and various other bonuses received to increase professional performance. Executive BGD is calculated as the ratio of female executives divided by the number of female directors by the board size. As control variables, audit reports, corporate governance reports, and board size were introduced. In line with Wang et al. [89], a bigger size of the board can bring more flexibility and efficiency. Also, we inserted industry dummy variables for each industry, with one industry as a reference, and dummy variables for each year. The one-year dummy is considered as a reference to avoid the dummy variable trap. The robustness check is based on the use of an alternative measure of executive board-room gender diversity (the Blau index), in addition to the proportion of women executives, as well as different metrics of financial performance (composite index, ROA, ROE, EPS, and SOL); in addition, firm size (measured by the natural log of a firm’s total assets) and leverage (measured by total debt divided by total assets) were considered.

To capture the moderator effect of the governance characteristics disclosure index on the executive BGD and FP connection, following the main assumption of the study, the following model was developed:

where FP is financial performance; RWD is the ratio of female executives on the board; BS is the size of the board of directors; CV is control variables, including the availability of the audit and the corporate governance reports; ε represents the remaining perturbation term; Dindex_GOV is the disclosure index on executives’ characteristics information; is the interaction term; i = observation (firm); and t = year of observation.

A dynamic panel model was designed following studies of Brahma et al. [88] and Raheja [92] which analyzed a dynamic framework in which the present corporate governance characteristics disclosure and business performance are influenced by firms’ past performance:

where is the coefficient of moderating variable ().

Alternative measures of BGD and alternative measures for FP were used for the robustness check, and also the endogeneity problem was analyzed. Empirical works have identified potential endogeneity in the board composition–business performance relationship [93,94] caused by time-invariant heterogeneity. Endogeneity in regression models refers to the situation in which an explanatory parameter correlates with the error term [95]. If the non-correlation hypothesis is invalid, one or more regressors are considered endogenous. The endogeneity of the regressors makes the estimators inconsistent and reveals inappropriate inferences. As Barros et al. [96] pointed out, in corporate finance endogeneity, issues normally arise from missed variables, assessment errors of the model’s variables, and/or the simultaneity between the dependent and independent parameters. The assumption of strict exogeneity is necessarily violated when the model contains lags of the dependent parameter, a possible solution being the utilization of specific lags (and/or temporal differences) of the original regressors as instrumental variables, assuming zero association between the instruments and the model errors. The general solving of any endogeneity issue, whether it is generated by measurement errors, omitted variables, or simultaneity, is the utilization of valid instrumental parameters [96], implementing an estimation in two stages. Diverse estimation models that are adequate for short panels and use sequentially exogenous parameters as instruments are available. These can be grouped into estimators of instrumental parameters and estimators based on the Generalized Method of Moments (GMM) [96]. Among the different models elaborated for panels that can include instrumental variables, two are well known for their efficiency and flexibility in adjusting different patterns of variable behavior. The first one is a method designed by Nickell [97], and Arellano and Bond [98], and known as the Arellano–Bond estimator or first-differencing GMM (GMM-Dif). This method first converts the parameters of the model to eliminate the unobserved heterogeneity. The conversion normally applied implies computation of the difference between each parameter to its first lag.

The GMM estimator allows for endogeneity control between parameters and unobservable heterogeneity, which varies according to each company but is invariant over time. The dynamic panel model is easily recognized, as the fixed effects method is incompatible when the period is small [97], and the ordinary least squares estimator is entrenched on first differences. In these cases, GMM by Arellano and Bond [98] is broadly applied, and the GMM model will help the dominant feature of the results, which overcomes the weaknesses of prior studies [99,100]. Within these models based on GMM estimation, company size (measured by the natural log of total assets of a firm) and leverage (measured by total debt divided by total assets), as the additional control variables, were used. The lag of performance variables was used as one of the instruments in the estimation process. We considered that the utilization of random effect regression, complemented by 2SLS, and the system GMM would assure the robustness of the results. Several scholars argued that the GMM path generally delivers more efficient and accurate estimates compared to other estimators by ameliorating the finite sample bias [101,102]. Sial et al. [103] pointed out very clearly the advantages of using GMM models for panel data by applying Arellano and Bond’s [98] technique. Therefore, it is important to mention that the paper incorporated various robustness tests: from one perspective, the paper tested an alternative measure of executive BGD (the Blau index) apart from the proportion of women executives, as well as different metrics for the FP (the composite index, ROA, ROE, EPS, and global solvency); and from the other perspective, different methods of estimation were applied to tackle endogeneity issues.

3. Results

3.1. Corporate Governance Characteristics Disclosure Index Impact on Financial Performance

The governance characteristics disclosure index’s probable influence on FP was tested using five random effects models (Table 1), testing the main hypothesis, H1, along with its components, H1a, H1b, H1c, and H1d, using five proxies for FP.

Table 1.

The impact of the governance disclosure index on corporate performance applying panel-data analysis (random effects models).

The empirical results confirmed four of the five hypotheses, claiming that a higher disclosure level of executive managers’ characteristics information leads to an increase in the FP of the companies for financial indicators such as the synthetic measure of performance (FPindex), ROA, ROE, or global solvency, with only one exception of earnings per share (EPS). Therefore, H1 and its components H1b, H1c, and H1d are fully validated by the research. Among the control variables, board size was found to be positively correlated with most of the FP metrics (composite index, ROA, ROE, and EPS), implying that a larger board size leads to improved corporate performance. Regarding Big 4, we can report a statistically significant impact of the financial indicators ROA and EPS, revealing that if the company’s financial statements are audited by a Big 4 company, this will increase the FP. The detailed governance reports do not exhibit any impact on the FP of the company.

3.2. Corporate Governance Disclosure Index as a Moderator Between Executive Board Gender Diversity and Financial Performance

Table 2 presents a results overview of executive BGD and FP connection testing, moderated by the disclosure index on managers’ characteristics. In this part of the research, we have included a robustness check considering an alternative proxy for gender diversity (Blau index) and alternative measures of business performance (ROA, ROE, EPS, global solvency, or the aggregated index). The effect of BGD proxy by both the proportion of women executives and the Blau index on FP is positive and, in most cases, statistically significant, revealing that women directors can enhance a company’s FP. This is in alignment with other studies’ [88,90,104,105,106] results, proving that a women director has a positive influence on the firm FP. However, more significant results are given by the usage of the first proxy, the proportion of female managers being able to highlight the statistically significant impact in four of five FP indicators, in contrast to the Blau index, which revealed the statistical significance in only two of the cases (the composite index and ROA). The disclosure index pointed out a unanimous conclusion, revealing a positive effect on FP in all measures, with only the exception of EPS and for both measures of executive BGD.

Table 2.

The governance disclosure index’s moderating role on executive-board gender diversity and corporate financial performance.

The corporate governance disclosure index moderating function on BGD and FP has been captured through the interaction variables (disclosure index*proportion of women managers and disclosure index*Blau index). In the majority of the cases, the coefficients of both interaction variables are statistically significant at a 10% significance level, which means that the disclosure index acts as a moderating factor. This finding fully supports our second hypothesis for the proportion of women executives and only partially for the case of the Blau index, revealing a statistically significant impact only for the case of the synthetic measure, EPS, and global solvency (validating, as a consequence, H2 and its components, H2a and H2d).

For the empirical results related to moderation analysis, we can mention the negative sign of both interaction terms preserved in all the models, revealing that the effect of the combined action of BGD and governance disclosure index is less than the sum of the individual effects. As we know from the literature, a negative correlation coefficient means that the effect of mixed action of two predictors is less than the sum of each impact. If the association between A and B is negative reveals, the increase in A will decrease the significant influence of B; if the impact of B is negative, its influence will be less negative with increasing A; but if the impact of B is positive, its influence will be less positive with increasing A. Consequently, the negative correlation will not affect the sign or direction influence of a variable; it will only diminish the impact value. The same thing is true for the positive influence: it does not have any effect on the sign of both variables but will increase it in the same way. Positive relationships between the two variables and the outcome are weaker when the values of the other one are high. Therefore, as in our case, both BGD (for both proxies) and the governance disclosure index, taken individually, exert a positive influence on the company’s FP; the negative interaction term between both of them pointed out that the effect of executive BGD on the firm’s FP will be less positive with a higher level of disclosure on board characteristics. Overall, the control variables preserved a similar impact as they had previously. A larger board can assure more flexibility and efficiency, and it is associated with fewer administrative issues, validating the study of Wang et al. [89]. If company financial statements are audited by a Big4 audit company, this translates into improved FP, at least in the case of global solvency and EPS, findings which are confirmed also by the study of Jiang et al. [104].

4. Robustness

4.1. Endogeneity Testing of the Moderating Role of Corporate Governance Disclosure Index, Using Two-Stage Least Square (2SLS) Estimation

To solve the problem of endogeneity, we used two-stage least square (2SLS) regression models M6’–M15’ (Table 3).

Table 3.

Endogeneity testing of the moderator role of the governance disclosure index on the relation between board gender diversity and financial performance (2SLS estimation).

The analysis results proved that the governance disclosure index impact on the FP is significant partially, only in the case of the composite index of FP, as well as ROA and ROE for both proxies of executive BGD, thus validating H1, H1b, and H1c. Previous work conducted by Bogdan et al. [91] on the impact of BGD found that the assumption is validated for the FP composite index and ROE for the proportion of women executives, while the second proxy-Blau index remains insignificant at a 10% level. The moderator effect of the governance disclosure index on executive BGD and firm FP connection has been fully preserved for all proxies of FP in the case of the proportion of women executives, validating the H2, along with its components H2a to H2d. In the situation of the Blau index as the second proxy of BGD, the moderator effect of the governance disclosure index turned out to be statistically significant in the case of the composite index of FP, as well as ROA and EPS, validating H2, H2a, and H2b. The negative sign of the moderator effect is preserved in all models, revealing that the impact of the combined action of BGD and governance disclosure index is less than the total of each influence. Thus, even if both proxies of executive BGD, as well as the disclosure index, exhibited a positive impact on the FP, the negative sign of the interaction terms suggested that the effect of BGD on FP will be less positive with a higher level of governance disclosure on board characteristics. Regarding the significance of control variables, the board size exhibited a direct impact only partially on the FPindex, ROE, ROA, and EPS, validating the study of Wang et al. [89]. The Big4 variable capturing the status of the firm having the financial reports audited by a Big4 firm remains insignificant and exhibited only a slightly direct impact validated only for EPS.

4.2. Endogeneity Testing of the Moderating Role of Corporate Governance Disclosure Index on Executive Board Gender Diversity and Business Performance Using GMM Estimation

The results of the GMM estimate analysis, testing the relationship between the BGD and the FP in the presence of the governance disclosure index, are presented in Table 4, models M16–M25.

Table 4.

Endogeneity testing of the moderating role of governance disclosure index using dynamic panel-data estimation.

The lagged FP variable pointed out its statistical significance in almost all of the cases except for EPS, revealing that the FP of the companies from the previous year led to a direct impact on the current FP. The direct impact of BGD on the FP led to a growth in the financial performance of the companies for both proxies at a 1% significance level (Bogdan et al., 2022) [91]. The governance disclosure index preserved its impact mainly in the case of ROA and ROE for the executive BGD and all proxies of FP, when using the Blau index, supporting the idea that, in most of the cases, H1 and its components were confirmed. The moderator effect of the governance disclosure index was fully preserved for almost all proxies of FP in the case of the proportion of women executives, except EPS, validating the second hypothesis (H2), along with its components H2a, H2b, and H2d. By using the Blau index as the second proxy of BGD, the moderator effect of the governance disclosure index has been proven to be statistically significant for all proxies of FP, fully validating H2 and its components H2a to H2d. The negative sign of the moderator effect is preserved in all models, revealing that the effect of the combined action of BGD and governance disclosure index is less than the aggregated amount of each effect. Therefore, the negative sign of the interaction terms suggested that the effect of BGD on FP will be less positive, with an increased amount of board characteristics disclosure. In terms of control variables’ significance, the board size, Big4 status, company size, or leverage exerted, in most cases, a significant influence on corporate performance. Nevertheless, board size showed an inconclusive sign. The Big4 variable capturing the status of the firm having the financial reports audited by a Big4 firm remains statistically pointing out a slightly direct impact. The effect of firm size on FP mostly is negative and relevant for different metrics of performance. The outcomes revealed that financial leverage has a positive influence on corporate performance if the total amount of debts is not higher than the total amount of equity. The impact of the control variables, especially board size and Big4 auditor affiliation, demonstrate some inconsistency across models and performance measures. For example, board size is negatively associated with ROA and ROE in certain models, but neither the sign nor significance was consistent from specification to specification. The variability aligns with the theoretical conceptualization that Raheja [92] put forward in implying that the relationship between board size and firm performance may be non-linear; large boards may provide managers with an increased capacity to enhance the monitoring of firm resources, but may also increase the coordination costs or could introduce a different set of agency problems. In a similar relationship, the Big4 variable (a proxy for audit quality) is only statistically significant in some models; more specifically, those explaining ROA and EPS. While this is consistent with prior results (e.g., Francis et al. [60]) that demonstrate the positive impact of Big4 auditors on improving the quality of financial reporting, the lack of consistent significance across all performance metrics may result from a reduced degree of heterogeneity in terms of audit quality in our sample, most of which are publicly listed and regulated firms, relative to other performance metrics. These observations further substantiate the idea that governance-related controls should be interpreted within their respective institutional and firm contexts and provide an impetus for the exploration of the conditional nature of the effects in future research. Although the total number of observations appears to be the same in the presented GMM models (389), that is not the case; it is to some degree an unbalanced panel, as is indicated in the GMM estimation output “Total panel (unbalanced) observations: 389” “Cross-sections included: 57; Periods included: 7”. This comes from the fact that the original dataset consists of a balanced panel design (57 Romanian listed firms for 9 years, 2011–2019) and lost some data due to missing information on selected variables to meet the requirements of a GMM estimation (such as the Blau Index, an agency-type disclosure index, EPS, dummy for audit firm, and lagged dependent variables). Also, where there are lagged dependent variables in the GMM estimator in first differences, there will be a loss of data because differencing will remove the first period for each entity; lagged dependent variables will cause loss of data, as they require some form of a lag of ≥2 past periods to form a valid instrument, and as the GMM method uses listwise deletion for missing values in either the regressors or instruments. Thus, we ended up with a final estimation sample of 57 firms in an effective seven periods (389 usable firm-year observations, an ordinary structure for GMM methodology in corporate governance research). Additionally, while the sample is ultimately unbalanced, the firms included are representative of the heart of the Romanian listed market, or those that have complete-enough governance and financial disclosures to allow for dynamic panel modeling of this nature. Hence, the findings are generalizable to the most economically important and, perhaps, most regulated part of the market.

5. Conclusions

This study investigated the influence of governance disclosures of executive managers’ characteristics on corporate performance, focusing on the moderating function of governance-characteristics disclosure on the connection between board gender diversity and business financial performance. Therefore, the results of the random effects model proved the influence of the governance disclosure index on financial performance. The performed analysis revealed that a higher governance disclosure level for executive managers’ characteristics is reflected in increased corporate performance, expressed through financial ratios. In this case, a positive influence was found for the composite FPindex, ROA, ROE, and SOL, except for the EPS indicator. Also, board size and Big4 audit report were found to have a statistically significant impact in the case of ROA and EPS proxies. In terms of capturing the moderating role of the corporate governance disclosure index on the relationship BGD-FP, the interaction-variable analysis showed that both coefficients of interaction variables (disclosure index*proportion of women executives and disclosure index*Blau index) are statistically significant at a 10% significance level, which means that the governance disclosure index moderates the executive board gender diversity and financial performance link. Consequently, in the situation of the proportion of women directors, the assumption of the moderator role of governance disclosure was fully confirmed, but in the case of the Blau index, the validation was only partial, revealing a statistically significant impact only for FPindex, EPS, and SOL indicators. It is worth mentioning as a main finding that the negative sign of both interaction terms is preserved in all the models. Hence, the corporate governance disclosure index on board characteristics negatively moderates the relationship between board gender diversity and corporate financial performance. Analysis results proved that the impact of board gender diversity on corporate financial performance will be less positive with an increased level of governance disclosure on executives’ characteristics. To test endogeneity issues and to assure the model’s robustness, 2SLS and GMM estimations were used. Outcomes are in alignment with Song et al. [46], Alodat et al. [50], Rahman and Zahid [85], Espinosa-Méndez and Inostroza Correa [84], and Wang et al. [41], meaning that the moderating effects of ESG aspects are worthy of further investigation. Moreover, periods marked by uncertainty and risks, such as that of the COVID-19 pandemic or the crisis generated by war conflicts, require rethinking governance issues at the level of all businesses to adapt and adjust to the existing circumstances. Therefore, information on the board of executives’ characteristics, along with the effects of executive board size, composition, diversity, education, professional skills, demographic, and cultural dimensions, acquires greater importance in correlation with the achievement of financial performance goals. Although the number of studies investigating board diversity in correlation with financial performance is increasing, there is still a lack of scientific research works analyzing the influence of moderating variables.

The main outcomes of the empirical study add value to the present knowledge by emphasizing the importance of the moderating function of corporate governance variables. The analysis reveals that as the degree of executive managers’ characteristics disclosure increases, the effect of board gender diversity on financial performance is less favorable. Therefore, the study has theoretical implications for academia, demonstrated by the outcomes of the moderation analysis, but also practical value for companies’ management. Thus, managers taking note of the results can filter the governance information disclosed in reports, as well as their quantity and quality, and can monitor the impact of the board’s composition on financial performance. Meanwhile, new performance optimization and business management tools can be developed. Limits of the study can be found mainly in the selected variables and the size of the sampled companies. By extending the dataset, the results can be refined, providing support for further analyses and decisions.

Author Contributions

Conceptualization, V.B. and D.-N.P.; methodology, M.B.; software, M.B.; validation, D.-E.M., V.B. and D.-N.P.; formal analysis, D.-E.M.; investigation, D.-N.P.; resources, D.-E.M.; data curation, M.B.; writing—original draft preparation, V.B. and D.-E.M.; writing—review and editing, D.-N.P.; visualization, D.-E.M.; supervision, V.B.; project administration, V.B. and D.-N.P.; funding acquisition, D.-E.M. All authors have read and agreed to the published version of the manuscript.

Funding

The APC was funded by the University of Oradea.

Data Availability Statement

The data is available upon request.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Bilimoria, D.; Huse, M. A Qualitative Comparison of the Boardroom Experiences of U.S. and Norwegian Corporate Directors. Int. Rev. Women Leadersh. 1997, 3, 63–76. [Google Scholar]

- Daily, C.M.; Certo, S.T.; Dalton, D.R. A Decade of Corporate Women: Some Progress in the Boardroom, None in the Executive Suite. Strateg. Manag. J. 1999, 20, 93–100. [Google Scholar] [CrossRef]

- Adams, R.B.; Ferreira, D. Gender Diversity in the Board Room. In ECGI Working Paper Series in Finance 57; European Corporate Governance Institute: Brussels, Belgium, 2004. [Google Scholar] [CrossRef]

- Carter, D.A.; Simkins, B.J.; Simpson, W.G. Corporate Governance, Board Diversity, and Firm Value. Financ. Rev. 2003, 38, 33–53. [Google Scholar] [CrossRef]

- Eagly, A.H.; Johannesen-Schmidt, M.C.; van Engen, M.L. Transformational, Transactional, and Laissez-Faire Leadership Styles: A Meta-Analysis Comparing Women and Men. Psychol. Bull. 2003, 129, 569–591. [Google Scholar] [CrossRef] [PubMed]

- Barron, L.G.; Hebl, M. The Force of Law: The Effects of Sexual Orientation Antidiscrimination Legislation on Interpersonal Discrimination in Employment. Psychol. Public Policy Law 2013, 19, 191–205. [Google Scholar] [CrossRef]

- Singh, V.; Terjesen, S.; Vinnicombe, S. Newly Appointed Directors in the Boardroom: How Do Women and Men Differ? Eur. Manag. J. 2008, 26, 48–58. [Google Scholar] [CrossRef]

- Simionescu, L.N.; Gherghina, Ş.C.; Tawil, H.; Sheikha, Z. Does Board Gender Diversity Affect Firm Performance? Empirical Evidence from Standard & Poor’s 500 Information Technology Sector. Financ. Innov. 2021, 7, 52. [Google Scholar] [CrossRef]

- Khatri, I. Board Gender Diversity and Sustainability Performance: Nordic Evidence. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 1495–1507. [Google Scholar] [CrossRef]

- Soare, T.-M.; Detilleux, C.; Deschacht, N. The Impact of the Gender Composition of Company Boards on Firm Performance. Int. J. Product. Perform. Manag. 2021, 71, 1611–1624. [Google Scholar] [CrossRef]

- Aluchna, M.; Honig, B.; Kamiński, B. Glass Ceiling or Glass Cliff: An Examination of the Role of Female Board Members on Market Performance in Poland. Post-Communist Econ. 2023, 35, 926–950. [Google Scholar] [CrossRef]

- Gipson, A.N.; Pfaff, D.L.; Mendelsohn, D.B.; Catenacci, L.T.; Burke, W.W. Women and Leadership: Selection, Development, Leadership Style, and Performance. J. Appl. Behav. Sci. 2017, 53, 32–65. [Google Scholar] [CrossRef]

- Rehman, U.U.; Iqbal, A. Nexus of Knowledge-Oriented Leadership, Knowledge Management, Innovation and Organizational Performance in Higher Education. Bus. Process Manag. J. 2020, 26, 1731–1758. [Google Scholar] [CrossRef]

- Jing, Z.; Hou, Q.; Zhang, Y.; Zhao, Y. The Relationship between Female Leadership Traits and Employee Innovation Performance—The Mediating Role of Knowledge Sharing. Sustainability 2022, 14, 6739. [Google Scholar] [CrossRef]

- Al-Shammari Abdullah, S.; Rehman, A.U.; Abdullah Alreshoodi, S.; Abdul Rab, M. How Entrepreneurial Competencies Influence the Leadership Style: A Study of Saudi Female Entrepreneurs. Cogent Bus. Manag. 2023, 10, 2202025. [Google Scholar] [CrossRef]

- García-Meca, E.; García-Sánchez, I.-M.; Martínez-Ferrero, J. Board Diversity and Its Effects on Bank Performance: An International Analysis. J. Bank. Financ. 2015, 53, 202–214. [Google Scholar] [CrossRef]

- Melón-Izco, Á.; Ruiz-Cabestre, F.J.; Ruiz-Olalla, M.C. Diversity in the Board of Directors and Good Governance Practices. Econ. Bus. Lett. 2020, 9, 97–105. [Google Scholar] [CrossRef]

- Orazalin, N.; Baydauletov, M. Corporate Social Responsibility Strategy and Corporate Environmental and Social Performance: The Moderating Role of Board Gender Diversity. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1664–1676. [Google Scholar] [CrossRef]

- Valls Martínez, M.d.C.; Santos-Jaén, J.M.; Soriano Román, R.; Martín-Cervantes, P.A. Are Gender and Cultural Diversities on Board Related to Corporate CO2 Emissions? J. Clean. Prod. 2022, 363, 132638. [Google Scholar] [CrossRef]

- EIGE. Gender Equality Index 2024: Sustaining Momentum on a Fragile Path; Publications Office of the European Union: Luxembourg, 2024.

- Robayo-Abril, M.; Chilera, C.P.; Rude, B.; Costache, I. Gender Equality in Romania: Where Do We Stand?—Romania Gender Assessment; World Bank: Washington, DC, USA, 2023; Available online: http://hdl.handle.net/10986/40666 (accessed on 24 May 2025).

- PwC. Gender Pay Gap Report; PwC Romania: Bucharest, Romania, 2024; Available online: https://hrleadersportal.pwc.com/media/1408/pwc-romania-gender-pay-gap-report-2024.pdf (accessed on 24 May 2025).

- Deloitte; PWNR. Women on Boards in Romania; Deloitte Romania & Professional Women’s Network Romania: Bucharest, Romania, 2022; Available online: https://www.amcham.ro/business-intelligence/deloitte-pwnr-report-romania-reports-progress-in-leadership-gender-balance.-62-of-the-companies-listed-on-the-bucharest-stock-exchange-have-women-on-boards-and-65-of-them-in-the-executive-committees (accessed on 24 May 2025).

- Noja, G.G.; Thalassinos, E.; Cristea, M.; Grecu, I.M. The Interplay between Board Characteristics, Financial Performance, and Risk Management Disclosure in the Financial Services Sector: New Empirical Evidence from Europe. J. Risk Financ. Manag. 2021, 14, 79. [Google Scholar] [CrossRef]

- Marashdeh, Z.; Alomari, M.W.; Aleqab, M.M.; Alqatamin, R.M. Board Characteristics and Firm Performance: The Case of Jordanian Non-Financial Institutions. J. Gov. Regul. 2021, 10, 150. [Google Scholar] [CrossRef]

- Al Amosh, H.; Khatib, S.F.A. Corporate Governance and Voluntary Disclosure of Sustainability Performance: The Case of Jordan. SN Bus. Econ. 2021, 1, 165. [Google Scholar] [CrossRef]

- Nguyen, T.H.; Nguyen, Q.T.; Nguyen, D.M.; Le, T. The Effect of Corporate Governance Elements on Corporate Social Responsibility Reporting of Listed Companies in Vietnam. Cogent Bus. Manag. 2023, 10, 2170522. [Google Scholar] [CrossRef]

- Kamukama, N.; Kyomuhangi, D.S.; Akisimire, R.; Orobia, L.A. Competitive Advantage: Mediator of Managerial Competence and Financial Performance of Commercial Banks in Uganda. Afr. J. Econ. Manag. Stud. 2017, 8, 221–234. [Google Scholar] [CrossRef]

- Al Frijat, Y.S.; Albawwat, I.E.; Elamer, A.A. Exploring the Mediating Role of Corporate Social Responsibility in the Connection between Board Competence and Corporate Financial Performance amidst Global Uncertainties. Corp. Soc. Responsib. Environ. Manag. 2023, 31, 1079–1095. [Google Scholar] [CrossRef]

- Fiorini, P.d.C.; Seles, B.M.R.P.; Jabbour, C.J.C.; Mariano, E.B.; Jabbour, A.B.L. de S. Management Theory and Big Data Literature: From a Review to a Research Agenda. Int. J. Inf. Manag. 2018, 43, 112–129. [Google Scholar] [CrossRef]

- Amin, A.; Rehman, R.U.; Ali, R.; Ntim, C.G. Does Gender Diversity on the Board Reduce Agency Cost? Evidence from Pakistan. Gend. Manag. Int. J. 2021, 37, 164–181. [Google Scholar] [CrossRef]

- Wernerfelt, B. A Resource-Based View of the Firm. Strateg. Manag. J. 1984, 5, 171–180. [Google Scholar] [CrossRef]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Mailani, D.; Hulu, M.Z.T.; Simamora, M.R.; Kesuma, S.A. Resource-Based View Theory to Achieve a Sustainable Competitive Advantage of the Firm: Systematic Literature Review. Int. J. Entrep. Sustain. Stud. 2024, 4, 1–15. [Google Scholar] [CrossRef]

- Hillman, A.J.; Cannella, A.A.; Paetzold, R.L. The Resource Dependence Role of Corporate Directors: Strategic Adaptation of Board Composition in Response to Environmental Change. J. Manag. Stud. 2000, 37, 235–256. [Google Scholar] [CrossRef]

- Igartua, J.-J.; Hayes, A.F. Mediation, Moderation, and Conditional Process Analysis: Concepts, Computations, and Some Common Confusions. Span. J. Psychol. 2021, 24, e49. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The Moderator–Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- Hernández, C.; Rivera Ottenberger, D.; Moessner, M.; Crosby, R.D.; Ditzen, B. Depressed and Swiping My Problems for Later: The Moderation Effect between Procrastination and Depressive Symptomatology on Internet Addiction. Comput. Hum. Behav. 2019, 97, 1–9. [Google Scholar] [CrossRef]

- Hayes, A.F. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach, 3rd ed.; The Guilford Press: New York, NY, USA, 2022; ISBN 978-1-4625-4903-0. [Google Scholar]

- Holbert, R.L.; Park, E. Conceptualizing, Organizing, and Positing Moderation in Communication Research. Commun. Theory 2020, 30, 227–246. [Google Scholar] [CrossRef]

- Wang, J.; Xing, Z.; Zhang, R. Exploring the Linkages between Firm Misconduct and Entrepreneurial Growth in China. J. Small Bus. Enterp. Dev. 2023, 30, 1503–1520. [Google Scholar] [CrossRef]

- Karajeh, A.I. The Moderating Role of Board Diversity in the Nexus between the Quality of Financial Disclosure and Dividends in Jordanian-Listed Banks. Asia-Pac. J. Bus. Adm. 2022, 15, 553–571. [Google Scholar] [CrossRef]

- Yang, L.; Xu, C.; Wan, G. Exploring the Impact of TMTs’ Overseas Experiences on Innovation Performance of Chinese Enterprises: The Mediating Effects of R&D Strategic Decision-Making. Chin. Manag. Stud. 2019, 13, 1044–1085. [Google Scholar] [CrossRef]

- Dezső, C.L.; Ross, D.G. Does Female Representation in Top Management Improve Firm Performance? A Panel Data Investigation. Strateg. Manag. J. 2012, 33, 1072–1089. [Google Scholar] [CrossRef]

- Fan, Y.; Jiang, Y.; Zhang, X.; Zhou, Y. Women on Boards and Bank Earnings Management: From Zero to Hero. J. Bank. Financ. 2019, 107, 105607. [Google Scholar] [CrossRef]

- Song, H.J.; Yoon, Y.N.; Kang, K.H. The Relationship between Board Diversity and Firm Performance in the Lodging Industry: The Moderating Role of Internationalization. Int. J. Hosp. Manag. 2020, 86, 102461. [Google Scholar] [CrossRef]

- Al-Jaifi, H.A.; Al-Qadasi, A.A.; Al-Rassas, A.H. Board Diversity Effects on Environmental Performance and the Moderating Effect of Board Independence: Evidence from the Asia-Pacific Region. Cogent Bus. Manag. 2023, 10, 2210349. [Google Scholar] [CrossRef]

- Marquez-Cardenas, V.; Gonzalez-Ruiz, J.D.; Duque-Grisales, E. Board Gender Diversity and Firm Performance: Evidence from Latin America. J. Sustain. Financ. Investig. 2022, 12, 785–808. [Google Scholar] [CrossRef]

- Zhu, C.; Husnain, M.; Ullah, S.; Khan, M.T.; Ali, W. Gender Diversity and Firms’ Sustainable Performance: Moderating Role of CEO Duality in Emerging Equity Market. Sustainability 2022, 14, 7177. [Google Scholar] [CrossRef]

- Alodat, A.Y.; Salleh, Z.; Nobanee, H.; Hashim, H.A. Board Gender Diversity and Firm Performance: The Mediating Role of Sustainability Disclosure. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 2053–2065. [Google Scholar] [CrossRef]

- Shah, S.G.M.; Ivascu, L. Accentuating the Moderating Influence of Green Innovation, Environmental Disclosure, Environmental Performance, and Innovation Output between Vigorous Board and Romanian Manufacturing Firms’ Performance. Environ. Dev. Sustain. 2024, 26, 10569–10589. [Google Scholar] [CrossRef]

- Shakil, M.H. Environmental, Social and Governance Performance and Financial Risk: Moderating Role of ESG Controversies and Board Gender Diversity. Resour. Policy 2021, 72, 102144. [Google Scholar] [CrossRef]

- Albitar, K.; Hussainey, K.; Kolade, N.; Gerged, A.M. ESG Disclosure and Firm Performance before and after IR: The Moderating Role of Governance Mechanisms. Int. J. Account. Inf. Manag. 2020, 28, 429–444. [Google Scholar] [CrossRef]

- Fayyaz, U.-E.-R.; Jalal, R.N.-U.-D.; Venditti, M.; Minguez-Vera, A. Diverse Boards and Firm Performance: The Role of Environmental, Social and Governance Disclosure. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 1457–1472. [Google Scholar] [CrossRef]

- Kahloul, I.; Sbai, H.; Grira, J. Does Corporate Social Responsibility Reporting Improve Financial Performance? The Moderating Role of Board Diversity and Gender Composition. Q. Rev. Econ. Financ. 2022, 84, 305–314. [Google Scholar] [CrossRef]

- Fatma, H.B.; Chouaibi, J. Gender Diversity, Financial Performance, and the Moderating Effect of CSR: Empirical Evidence from UK Financial Institutions. Corp. Gov. Int. J. Bus. Soc. 2023, 23, 1506–1525. [Google Scholar] [CrossRef]

- Galbreath, J. Is Board Gender Diversity Linked to Financial Performance? The Mediating Mechanism of CSR. Bus. Soc. 2018, 57, 863–889. [Google Scholar] [CrossRef]

- Mohsni, S.; Otchere, I.; Shahriar, S. Board Gender Diversity, Firm Performance and Risk-Taking in Developing Countries: The Moderating Effect of Culture. J. Int. Financ. Mark. Inst. Money 2021, 73, 101360. [Google Scholar] [CrossRef]

- Huang, H.; Lee, E.; Lyu, C.; Zhu, Z. The Effect of Accounting Academics in the Boardroom on the Value Relevance of Financial Reporting Information. Int. Rev. Financ. Anal. 2016, 45, 18–30. [Google Scholar] [CrossRef]

- Francis, B.; Hasan, I.; Wu, Q. Professors in the Boardroom and Their Impact on Corporate Governance and Firm Performance. Financ. Manag. 2015, 44, 547–581. [Google Scholar] [CrossRef]

- Kampouris, I.; Mertzanis, C.; Samitas, A. Foreign Ownership and the Financing Constraints of Firms Operating in a Multinational Environment. Int. Rev. Financ. Anal. 2022, 83, 102328. [Google Scholar] [CrossRef]

- Barroso-Castro, C.; Pérez-Calero, L.; Vecino-Gravel, J.D.; Villegas-Periñán, M.d.M. The Challenge of Board Composition: Effects of Board Resource Variety and Faultlines on the Degree of a Firm’s International Activity. Long Range Plan. 2022, 55, 102047. [Google Scholar] [CrossRef]

- Müller, V.-O. Do Corporate Board Compensation Characteristics Influence the Financial Performance of Listed Companies? Procedia Soc. Behav. Sci. 2014, 109, 983–988. [Google Scholar] [CrossRef]

- Inostroza, M.A.; Velásquez, J.S.; Ortúzar, S. Gender and Decision-Making Styles in Male and Female Managers of Chilean SMEs. Acad. Rev. Latinoam. Adm. 2023, 36, 289–334. [Google Scholar] [CrossRef]

- Le, H.P.; Nguyen, B.H. The Impact of Board Size, Ownership Structure and Characteristics of the Supervisory Board on the Financial Performance of Listed Companies in Vietnam. Tech. Bus. Manag. 2024, 8, 122–142. [Google Scholar] [CrossRef]

- Müller, V.-O.; Ienciu, I.; Bonaci, C.; Filip, C. Board Characteristics Best Practices and Financial Performance. Evidence from the European Capital Market. Amfiteatru Econ. 2014, 16, 672–683. [Google Scholar]

- Suciu, M.-C.; Noja, G.G.; Cristea, M. Diversity, Social Inclusion and Human Capital Development as Fundamentals of Financial Performance and Risk Mitigation. Amfiteatru Econ. 2020, 22, 742. [Google Scholar] [CrossRef]

- Iliev, P.; Roth, L. Learning from Directors’ Foreign Board Experiences. J. Corp. Financ. 2018, 51, 1–19. [Google Scholar] [CrossRef]

- Oh, S.; Ding, K.; Park, H. Cross-Listing, Foreign Independent Directors and Firm Value. J. Bus. Res. 2021, 136, 695–708. [Google Scholar] [CrossRef]

- Hu, T.; Guo, R.; Ning, L. Intangible Assets and Foreign Ownership in International Joint Ventures: The Moderating Role of Related and Unrelated Industrial Agglomeration. Res. Int. Bus. Financ. 2022, 61, 101654. [Google Scholar] [CrossRef]

- Tang, R.W. Institutional Unpredictability and Foreign Exit−reentry Dynamics: The Moderating Role of Foreign Ownership. J. World Bus. 2023, 58, 101389. [Google Scholar] [CrossRef]

- Dang, T.L.; Vo, T.T.A.; Vo, X.V.; Thi My Nguyen, L. Does Foreign Institutional Ownership Matter for Stock Price Synchronicity? International Evidence. J. Multinatl. Financ. Manag. 2023, 67, 100783. [Google Scholar] [CrossRef]

- Raimo, N.; NIcolò, G.; Polcini, P.T.; Vitolla, F. Corporate Governance and Risk Disclosure: Evidence from Integrated Reporting Adopters. Corp. Gov. Int. J. Bus. Soc. 2022, 22, 1462–1490. [Google Scholar] [CrossRef]

- Nxumalo, L.; Dlungwane, S.; Nomlala, B.C. The Relationship between Corporate Governance and Firm Profitability among JSE-Listed Basic Materials Sector Firms. Int. J. Res. Bus. Soc. Sci. 2025, 14, 231–241. [Google Scholar] [CrossRef]

- Hong, J.; Kim, S.-I. Female Executives and Firm Value: The Moderating Effect of Co-CEO Power Gaps. Gend. Manag. Int. J. 2022, 37, 933–949. [Google Scholar] [CrossRef]

- Rubino, F.E.; Tenuta, P.; Cambrea, D.R. Five Shades of Women: Evidence from Italian Listed Firms. Meditari Account. Res. 2021, 29, 54–74. [Google Scholar] [CrossRef]

- Neuberger, M.N.; Bernardi, R.A.; Bosco, S.M.; Landry, E.E. Does the Presence of Three or More Female Directors Associate with Corporate Recognition? Gend. Manag. Int. J. 2022, 38, 111–132. [Google Scholar] [CrossRef]

- Chouaibi, J.; Miladi, E.; Elouni, N. Exploring the Relationship between Board Characteristics and Environmental Disclosure: Empirical Evidence for European Firms. J. Account. Manag. Inf. Syst. 2022, 21, 51–76. [Google Scholar] [CrossRef]

- Aly, D.A.R.M.; Hasan, A.; Obioru, B.; Nakpodia, F. Corporate Governance and Environmental Disclosure: A Comparative Analysis. Corp. Gov. Int. J. Bus. Soc. 2024, 24, 210–236. [Google Scholar] [CrossRef]

- Suherman, S.; Mahfirah, T.F.; Usman, B.; Kurniawati, H.; Kurnianti, D. CEO Characteristics and Firm Performance: Evidence from a Southeast Asian Country. Corp. Gov. Int. J. Bus. Soc. 2023, 23, 1526–1563. [Google Scholar] [CrossRef]

- Nguyen, T.T.C.; Nguyen, C.V. Does the Education Level of the CEO and CFO Affect the Profitability of Real Estate and Construction Companies? Evidence from Vietnam. Heliyon 2024, 10, E28376. [Google Scholar] [CrossRef]

- Zavertiaeva, M.; Shenkman, E.; Kazarina, E. Does Independence of Board Committees Enhance Corporate Performance? The Case of Russia. Emerg. Mark. Financ. Trade 2023, 60, 1316–1332. [Google Scholar] [CrossRef]

- Rahman, H.U.; Zahid, M.; Al-Faryan, M.A.S. Does Firm Better Financial Performance Amplify the Role of Women Directors and Their Certain Characteristics in Promoting Corporate Sustainability Practices? Corp. Gov. Int. J. Bus. Soc. 2025. ahead-of-print. [Google Scholar] [CrossRef]

- Espinosa-Méndez, C.; Correa, A.I. Gender and Financial Performance in SMEs in Emerging Economies. Gend. Manag. Int. J. 2022, 37, 603–618. [Google Scholar] [CrossRef]

- Rahman, H.U.; Zahid, M. Women Directors and Corporate Performance: Firm Size and Board Monitoring as the Least Focused Factors. Gend. Manag. Int. J. 2021, 36, 605–621. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does It Pay to Be Good … And Does It Matter? A Meta-Analysis of the Relationship between Corporate Social and Financial Performance. SSRN Electron. J. 2009, 1–68. [Google Scholar] [CrossRef]

- Brahma, S.; Nwafor, C.; Boateng, A. Board Gender Diversity and Firm Performance: The UK Evidence. Int. J. Financ. Econ. 2021, 26, 5704–5719. [Google Scholar] [CrossRef]

- Wang, C.; Deng, X.; Álvarez-Otero, S.; Sial, M.S.; Comite, U.; Cherian, J.; Oláh, J. Impact of Women and Independent Directors on Corporate Social Responsibility and Financial Performance: Empirical Evidence from an Emerging Economy. Sustainability 2021, 13, 6053. [Google Scholar] [CrossRef]

- Arora, A. Gender Diversity in Boardroom and Its Impact on Firm Performance. J. Manag. Gov. 2022, 26, 735–755. [Google Scholar] [CrossRef]

- Bogdan, V.; Popa, D.-N.; Beleneşi, M. The Complexity of Interaction between Executive Board Gender Diversity and Financial Performance: A Panel Analysis Approach Based on Random Effects. Complexity 2022, 2022, 9559342. [Google Scholar] [CrossRef]

- Raheja, C.G. Determinants of Board Size and Composition: A Theory of Corporate Boards. J. Financ. Quant. Anal. 2005, 40, 283–306. [Google Scholar] [CrossRef]

- Adams, R.B.; Ferreira, D. Women in the Boardroom and Their Impact on Governance and Performance. J. Financ. Econ. 2009, 94, 291–309. [Google Scholar] [CrossRef]

- Wintoki, M.B.; Linck, J.S.; Netter, J.M. Endogeneity and the Dynamics of Internal Corporate Governance. J. Financ. Econ. 2012, 105, 581–606. [Google Scholar] [CrossRef]

- Ullah, S.; Akhtar, P.; Zaefarian, G. Dealing with Endogeneity Bias: The Generalized Method of Moments (GMM) for Panel Data. Ind. Mark. Manag. 2018, 71, 69–78. [Google Scholar] [CrossRef]

- Barros, L.A.B.C.; Castro, F.H.; Silveira, A.D.M.d.; Bergmann, D.R. Endogeneity in Panel Data Regressions: Methodological Guidance for Corporate Finance Researchers. Rev. Bus. Manag. 2020, 22, 437–461. [Google Scholar] [CrossRef]

- Nickell, S. Biases in Dynamic Models with Fixed Effects. Econometrica 1981, 49, 1417–1426. [Google Scholar] [CrossRef]

- Arellano, M.; Bond, S. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef]

- Cheng, S.; Lin, K.Z.; Wong, W. Corporate Social Responsibility Reporting and Firm Performance: Evidence from China. J. Manag. Gov. 2016, 20, 503–523. [Google Scholar] [CrossRef]

- Zhu, Y.; Sun, L.-Y.; Leung, A.S.M. Corporate Social Responsibility, Firm Reputation, and Firm Performance: The Role of Ethical Leadership. Asia Pac. J. Manag. 2014, 31, 925–947. [Google Scholar] [CrossRef]

- Baltagi, B.H. Econometric Analysis of Panel Data; Springer Texts in Business and Economics; Springer International Publishing: Cham, Switzerland, 2021; ISBN 978-3-030-53952-8. [Google Scholar]

- Blundell, R.; Bond, S.; Windmeijer, F. Estimation in Dynamic Panel Data Models: Improving on the Performance of the Standard GMM Estimator. In Nonstationary Panels, Panel Cointegration, and Dynamic Panels; Emerald Group Publishing Limited: Bingley, UK, 2001; Volume 15, pp. 53–91. ISBN 978-0-7623-0688-6. [Google Scholar]

- Sial, M.S.; Chunmei, Z.; Khan, T.; Nguyen, V.K. Corporate Social Responsibility, Firm Performance and the Moderating Effect of Earnings Management in Chinese Firms. Asia-Pac. J. Bus. Adm. 2018, 10, 184–199. [Google Scholar] [CrossRef]

- Jiang, L.; Cherian, J.; Sial, M.S.; Wan, P.; Filipe, J.A.; Mata, M.N.; Chen, X. The Moderating Role of CSR in Board Gender Diversity and Firm Financial Performance: Empirical Evidence from an Emerging Economy. Econ. Res.-Ekon. Istraživanja 2021, 34, 2354–2373. [Google Scholar] [CrossRef]

- Yang, W.; Yang, J.; Gao, Z. Do Female Board Directors Promote Corporate Social Responsibility? An Empirical Study Based on the Critical Mass Theory. Emerg. Mark. Financ. Trade 2019, 55, 3452–3471. [Google Scholar] [CrossRef]

- Chijoke-Mgbame, A.M.; Boateng, A.; Mgbame, C.O. Board Gender Diversity, Audit Committee and Financial Performance: Evidence from Nigeria. Account. Forum 2020, 44, 262–286. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).