1. Introduction

There is great confidence in the future of financial technology (FinTech) investment worldwide in 2022, with many subsectors poised to keep expanding and new ones projected to emerge and thrive [

1]. According to Statista’s projections, the value of all transactions would increase at a compound annual growth rate (CAGR 2022–2027) of 12.31%, reaching USD 15.17 by the year 2027 [

2]. According to a recent report in 2021, the United States and China have the most FinTech startups and enterprises, whereas no companies in Saudi Arabia have been reported among the top 100 [

3].

To begin, a definition of “FinTech” is required; however, this is a difficult task since the term has come to signify many different things.

“New entrants that promised to quickly revolutionize how financial products were conceived, supplied, and consumed” is one way the World Economic Forum explains FinTech [

4]. Another complete definition of FinTech is

“Organizations that use new business models and technology to allow, improve and disrupt financial services.” In addition to startups and fresh entrants, this definition stresses that FinTech also covers scale-ups, mature businesses, and even non-financial-service organizations. FinTech firms include newcomers, and entrepreneurs are not the only ones benefiting from FinTech [

5].

Based on Saudi Arabia’s Vision 2030, the government has established a plan to reduce the country’s dependence on oil and diversify the economy [

6]. This plan will also help to expand sectors, such as healthcare, education, infrastructure, recreation, and tourism, that provide public services. Thus, economic and investment attempts will be boosted to achieve such goals. One of the main themes of Vision 2030 is a flourishing economy that provides for the future via investment. New emergent actors, such as FinTech businesses, are encouraged by the Financial Sector Development Program (FSDP) to stimulate innovation and competition by 2030, as per Vision 2030 on this topic [

7]. Another measure is the satisfaction index of FinTech enterprises in Saudi Arabia with the country’s FinTech ecosystem. Two more game-changing elements necessary for establishing FinTech-focused funds, accelerators, and incubators are the availability of venture capital/equity investment and the stimulation of an entrepreneurial environment [

8].

The National Digital Transformation Unit (NDU), managed by a high-level committee comprising six ministers and other relevant agencies, is another Saudi Vision 2030 program [

9]. A sustainable digital economy based on innovation and practical digital skills is the organization’s component’s cornerstone and purpose. It highlights the change to

“a digital society based on the building of digital platforms to increase participation and effective community involvement, eventually enriching the Kingdom’s inhabitants, residents, tourists, and investors’ experience” [

9], not to mention that the Saudi government’s e-government effort is often regarded as among the world’s finest. According to United Nations (UN) surveys, Saudi Arabia’s infrastructure is well-suited for FinTech ecosystems [

10].

Despite the Kingdom’s exserted efforts in this direction and the available ingredients for a successful FinTech adoption and implementation, it is crucial to identify and explore what enables FinTech innovation. This is important to guide a successful sustainable FinTech, expedite its implementation, and maximize its performance and desired benefits. Thus, this research study aims to identify and model essential enablers of Fintech innovation in Saudi Arabia. This is in an attempt to develop a model that draws the pathways and determines the priorities to achieve FinTech innovation. A literature review of previous FinTech research studies and extracted critical enablers in FinTech innovation, the materials and methods used to attain the objective, results, discussion, and conclusions are provided in the subsequent sections.

2. Literature Review

According to Romer’s theory, companies can avoid the restriction of decreasing marginal profits by increasing their capacity for technological innovation [

11]. FinTech, as the focus of this study, is one of the innovations that could help companies to avoid restrictions, reducing marginal profits. A new creative industry may be developed by a technical innovation that relies on science and technology while simultaneously increasing the production efficiency of enterprises through the enhancement of the issues connected to the labor force.

Science and technology have advanced tremendously in recent years all across the globe, and discoveries have been made in several essential fields. Major economies worldwide are speeding up the implementation of innovative development policies, increasing spending on innovation and R&D, and increasing their degree of innovation competitiveness [

12]. The rise in corporate innovation significantly impacts the national innovation system and the overall pace of technological growth. As a result, corporate innovation is a critical part of the overall innovation process. However, due to the virus’s global spread, there has been a negative impact on many firms’ operations, yet their overall corporate innovation, patents, and research expenditures continue to rise. Therefore, businesses have emerged as the primary source of innovation in the global economy [

13,

14]. Moreover, the COVID-19 pandemic resulted in impacts, challenges, and changes in policy priorities, underscoring the importance of FinTech, digital infrastructure investment, and digital financial education for driving economic recovery and sustainable development.

According to [

15,

16], modern scientific and technical advancements in financial services have been transformed into a new business model for the financial services sector, resulting in financial technology. Financial services companies, regulators, and customers all stand to gain financially due to this new approach [

17]. “Fintech,” or “financial + technology,” has emerged in recent years as a new business as advanced technologies, such as big data, cloud computing, and blockchain, are developed. This business has revolutionized corporate finance [

18]. Fintech crowdfunding and financial technology lending are two terminal application models that provide a wide variety of benefits, such as large funding channels, a comprehensive spectrum of financing, and excellent service quality [

19,

20,

21]. Some of the social concerns these terminal application models address, such as poverty and unemployment, are greatly improved by their use. For instance, new technologies may help banks find and screen firms more effectively, provide financial support to those with creative potential, eliminate financial mismatches, and boost efficiency with loan funds. In opposition to this, digital financial systems could provide investors with more information on current market circumstances and industry prospects of investment projects, reducing the costs of information identification and increasing investors’ willingness to participate in these initiatives [

16,

22]. However, advances in FinTech can help to ease access to banking for underserved communities.

With digital finance, micro-enterprises may have a secure and sustainable economic basis for technical innovation by breaking down informational enablers and providing customized goods. Digital finance, a new product born from the marriage of conventional finance and technological enablement, has the potential to cut financing costs, minimize business financial risk significantly, and provide a solid economic basis for the future [

23]. As a result of financial technology, small firms may gain enormous benefits from using digital finance. This is because digital finance is a new product generated by traditional finance using a technology-enabled method. This industry has begun to expand recently in the Saudi Arabian financial technology sector in recent years. Despite this, Saudi Arabia ranked seventh in the Middle East and North Africa area in terms of financial technology growth due to its rapid development.

The “2021 Global financial technology Index Report” [

24] states that Saudi Arabia ranks 126th in the world in total financial technology leading the charge. This is an improvement from Saudi Arabia’s ranking of 232nd in 2020. Riyadh, the capital of Saudi Arabia, has moved up 106 positions in the city index, making it the city with the highest rise. In addition, according to the survey, Saudi Arabia, the most populated and prosperous state in the Gulf area, is the third-best FinTech center in all Middle Eastern countries. Because of the enormous economic value that is up for grabs in the nation, FinTech companies can expand quickly and attract funding. The pandemic led to a spike in demand for its quick response (QR) codes and remote payment services in a nation with a very high consumption rate. The fact that the organization offers FinTech solutions that are compliant with the provisions of Islamic law is another selling point, which has the potential to be appealing to Muslims all over the globe.

With favorable market circumstances, a vibrant startup environment, and a burgeoning investment activity, Saudi Arabia’s FinTech industry has witnessed considerable developments in recent years. According to Fintech Saudi, the number of FinTech businesses operating in Saudi Arabia grew from 60 in 2020 to 82 in 2021, a 37% increase in only two years. There are already several big rounds completed by growth-stage FinTech businesses in 2022, which will be used to fund expansion [

25].

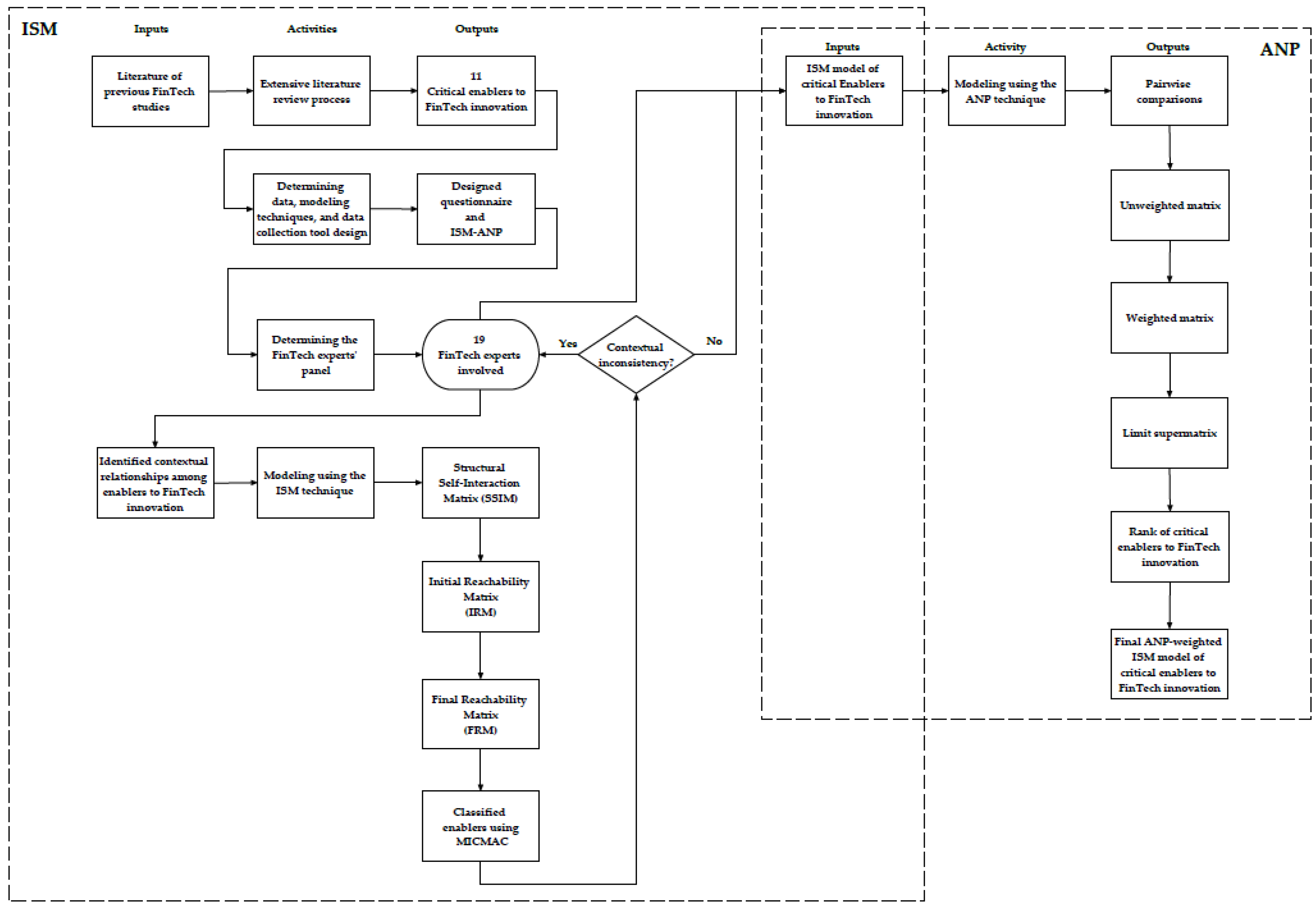

Therefore, in this stage, it is crucial to explore what enables FinTech innovation to facilitate its development, foster its potential benefits, and put Saudi Arabia in a higher position as a FinTech center in the Middle East and the world. Thus, this research study aims to identify and model the enablers of FinTech innovation by exploring contextual relationships among them and their priorities. Implications of the resulting model allow for a better understanding of the critical elements in an innovative FinTech and their associated essential components for its implementation. To achieve the objective,

Table 1 lists eleven FinTech innovation critical enablers and their essential components extracted from the literature of previous FinTech-related research studies. FinTech is a relatively recent emerging topic; thus, extracting the enablers necessitated a systematic search process using pertaining keywords in scientific databases and an extensive review of their essential components described in the literature. The extracted enablers are regulation and policy, regulators, financial ethics and literacy, personal data protection, customer protection, security, infrastructure, payment systems, technology, digital insurance, and framework and model. As can be observed from

Table 1, essential components of the eleven extracted enablers mostly revolve around rules and regulations, support, ethics and morals, security, protection and insurance, knowledge and awareness, framework and model, systems and technologies from the perspectives of the regulator, service provider, technology developer, consumer, and community. Subsequently, a hybrid approach is followed to model the extracted eleven enablers (

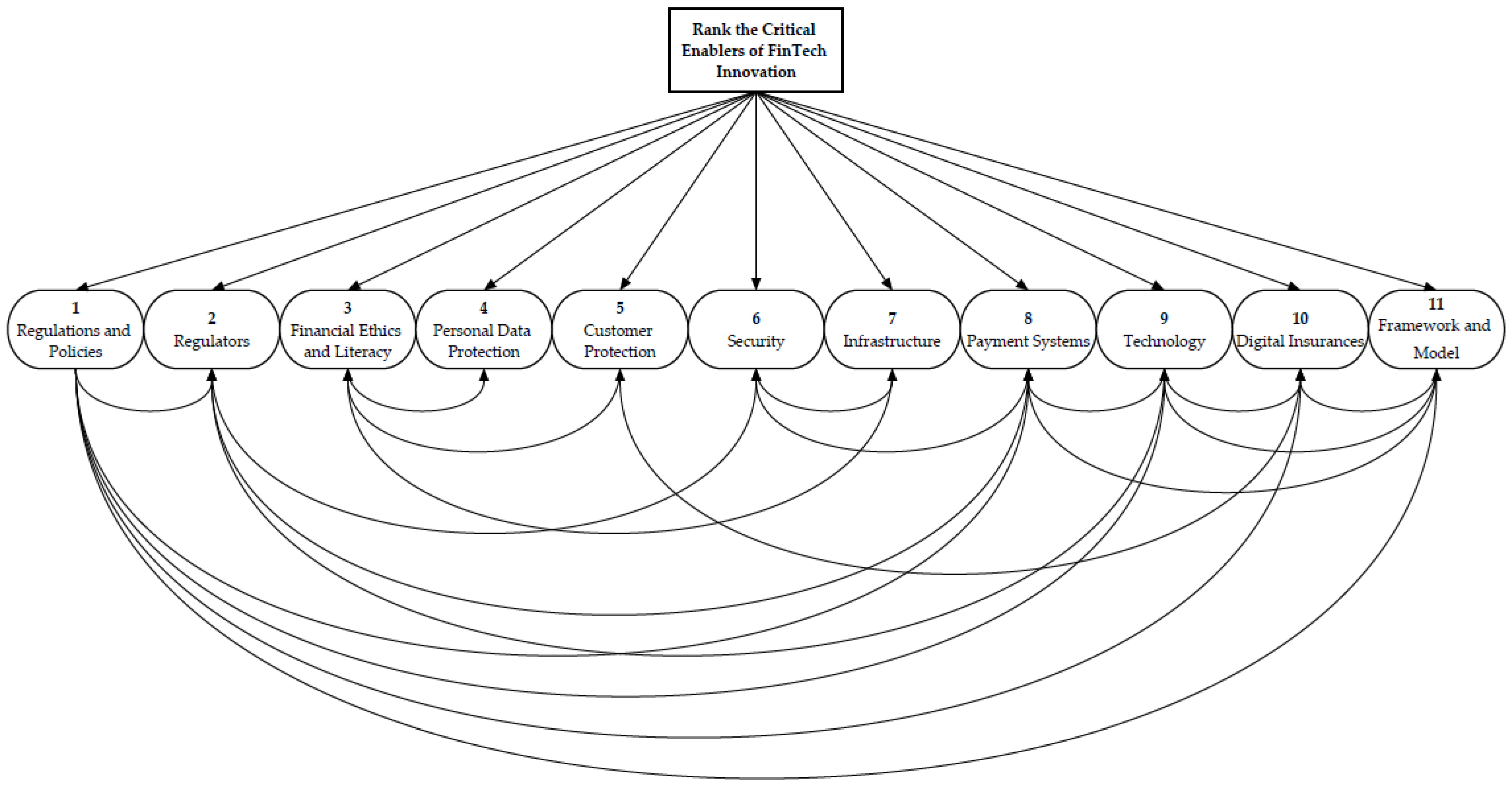

Table 1) using the Interpretive Structural Modeling (ISM), the Cross-Impact Matrix Multiplication Applied to Classification (MICMAC), and the Analytic Network Process (ANP) techniques to their modeling. Details on the materials and methods used to achieve the objective of this research study are provided in the subsequent sections of this article.

5. Discussion

This study demonstrated the usefulness of integrating the ISM and ANP methods to explore the critical enablers that foster the development of new FinTech products and innovation. The eleven critical enablers were chosen for this investigation after a systematic process of thoroughly reviewing the available literature and validation by subject matter experts. The ISM was used to reveal and model the interrelationships between the enablers, after which the ANP analysis was then used to rank them based on their relative importance.

Although there is a lot of overlap between the global and local FinTech ecosystems, it is important to keep them separate. Examining the ecology around FinTech innovation is essential for understanding its potential and limitations. For this research, we considered the fintech innovation ecosystem in Saudi Arabia. The FinTech sector’s development depends critically on maintaining a healthy, mutually beneficial environment [

85]. The FinTech ecosystem also includes government agencies and financial institutions [

86].

FinTech startups, technology developers, governments, financial clients, and traditional financial institutions are the five segments in the FinTech ecosystem [

16]. Innovation, economic growth, and a healthier level of financial sector competition are all fostered by the many forms of cooperation that make up the FinTech ecosystem. Startups in the financial sector will ultimately benefit from this.

Entrepreneurial and innovative FinTech startups are at the center of the FinTech revolution. They have lower operating expenses than their conventional equivalents and are pioneers in some sectors, such as payments, foreign transfers, lending, crowdfunding, capital markets, and insurance. Traditional financial institutions cannot compete with their ability to cater to specific markets and deliver individualized services. According to a previous study, one of the hallmarks of FinTech that is causing widespread disruption throughout the financial sector is that an ever-growing number of startups is rapidly unbundling the traditionally offered services by traditional financial institutions, resulting in new models of collaboration and a significant power shift [

65]. Examples of the many types of FinTech companies include asset management, exchange service, finance, insurance, loyalty program, payment, regulatory technology, and risk management [

34].

There is a need for new financial technology companies in places with more advanced economies and established conventional capital markets. This is to increase the country’s capacity to support cutting-edge technology, which, in turn, encourages the growth of FinTech companies that base their operations on advanced platforms. For a conventional financial institution, it is hypothesized that nations with weak financial systems are more likely to see a rise in FinTech firms. It is considered that FinTech is more prevalent in markets with more regulations and economies with larger labor markets. Thus, it is interesting to examine the roles of credit and labor markets and business regulations in the emergence of FinTech startups.

Technology companies should provide online resources and use social media, big data analytics, the cloud, AI, mobile devices, and more. Developers are making it easier for FinTech businesses to provide new services using cutting-edge technology. Cloud computing also allows resource-constrained FinTech firms to release web-based applications for a fraction of the cost of creating in-house infrastructure. Big data analytics may also be utilized to provide clients with one-of-a-kind, tailored services. Furthermore, Robo-advisor wealth management services, which are based on trading algorithms, may provide much cheaper costs than conventional asset management services. Crowdfunding and microlending communities are other solutions that may flourish with the help of social media. Businesses in the FinTech industry benefit from the low-cost infrastructure provided by mobile network carriers to develop new services, such as mobile payments and banking. For their part, these tech entrepreneurs generate income for the FinTech sector. Developers are in high demand, but supply is low, despite their critical importance to the FinTech industry.

When compared to traditional businesses, FinTech firms serve a highly specific niche. FinTech caters mainly to individual consumers, as opposed to the wide variety of clients served by more conventional banks. This clientele is crucial to the success of FinTech businesses since it represents the bulk of the industry’s income. It was previously shown that early FinTech adopters are often youthful and well-off [

87]. According to the 2019 Global FinTech Adoption Index (GFAI) [

88], consumer adoption of financial technologies throughout the world in 2019 hit 64 percent. Recently, it was found that among German families, 31% were open to the idea of switching to FinTech from more conventional banks [

89]. On the other hand, both our financial and non-financial consumers in Saudi Arabia have distinct personalities.

Saudi Arabia has a rigorous economy. The Saudi Central Bank reported that the macro-financial status in Saudi Arabia has remained steady [

90]. The government of Saudi Arabia has low debt relative to GDP and enough reserves, indicating that the country has room to finance its budget for the foreseeable future. Additionally, Saudi Arabia has a healthy financial system, as seen by its good credit rating. Historically, conventional banks have been unable to provide credit to small- and medium-sized businesses.

Due to the high cost of implementation, the government should provide financial assistance to FinTech businesses that have incorporated FinTech innovation into their operations. For the entrepreneur’s benefit, government backing in the form of rules and norms on FinTech is essential. A previous study [

27] argues that FinTech needs comprehensive regulations, which corroborates the results of this research.

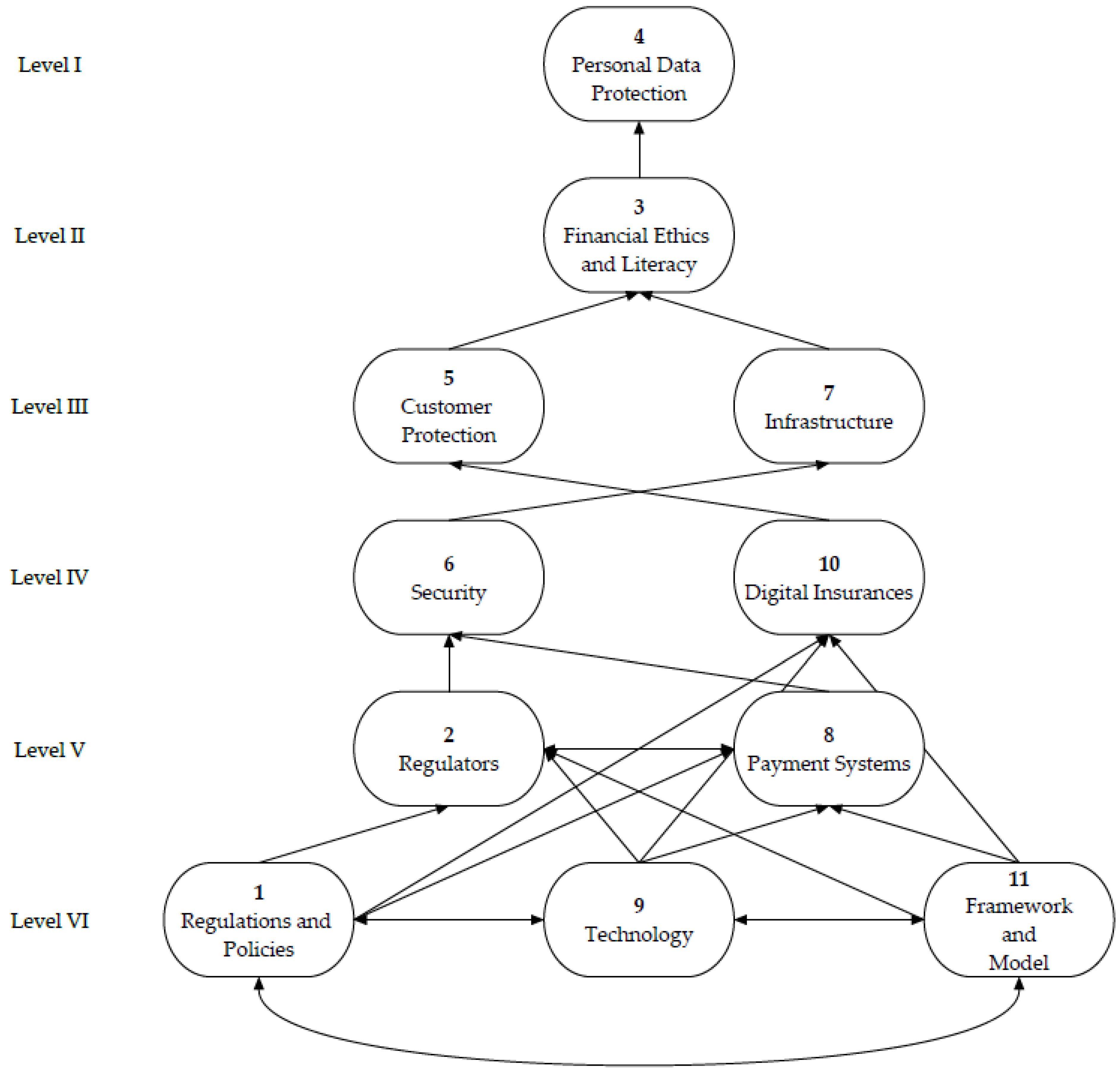

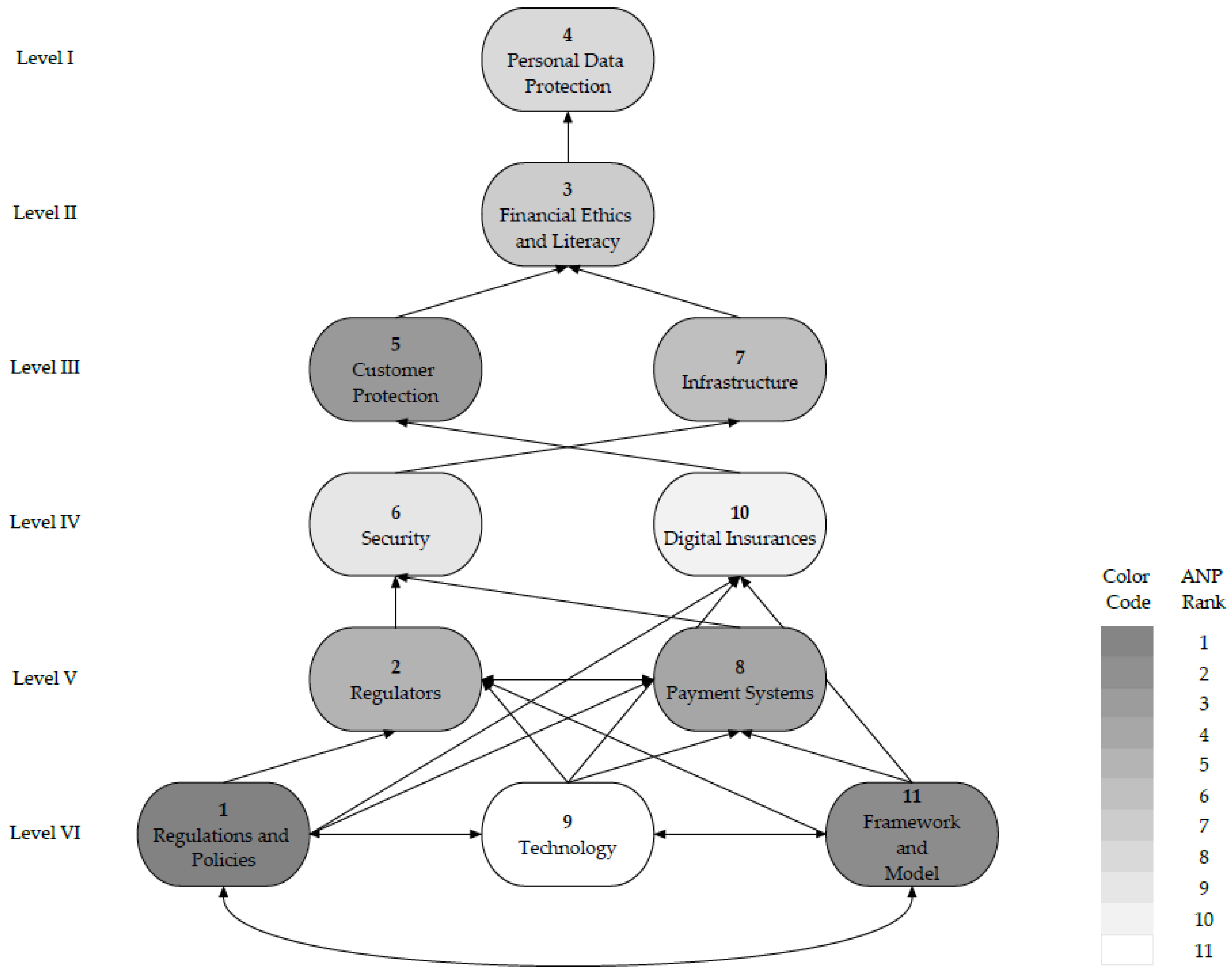

The results herein classified regulations, policies, frameworks, and models as fundamental enablers of FinTech innovation with the highest importance. Thus, considering the implementation of worldwide prudential norms enables addressing legal difficulties. The developed model in this study aids FinTech decision-makers, practitioners, and stakeholders in promptly developing strategies using the identified innovation enablers. The developed model revealed six levels of enablers that FinTech practitioners may use to design short-, medium-, and long-term strategies for successful FinTech innovation.

The fundamental enablers in Levels VI and V, which generally concern people, processes, and tools, should prioritize by FinTech firms in their short-term strategic planning. Thus, government agencies should develop policies that encourage FinTech implementation by engaging stakeholders of the enterprises and understanding their needs.

The developed model also shows a close relationship between safety measures and digital insurance. This indicates the critical need for a standard set of global rules and frameworks businesses can use to create and maintain secure data management systems and ensure their safety. FinTech security standards should include cryptography, access control, clear screen, and data security. It is the role of governments to establish rules and legislation that encourage the development of new FinTech and the maintenance of sustainable business methods. Financial corporations should also consider consumers’ worries about their personal and financial data and reflect them in their business practices. This finding aligns with key findings of a survey exploring with whom consumers trust their data [

91].

Moreover, top management must consider consumer safety, infrastructure, ethics, knowledge, and money awareness while designing medium-term strategic plans. One of the tools to ensure that the payment system can meet consumer protection is the use of electronic signatures for agreements. It is recommended that FinTech firms conduct targeted awareness campaigns to educate their workers and their customers. Further, to raise serious data protection concerns, such initiatives can strengthen ties between businesses and their consumers and encourage employing big data and cutting-edge technological possibilities. This conclusion conforms with a recently published World Bank Group (WBG) policy research paper [

92].

Customer data protection is shown in the developed model as a result of implementing other enablers, indicating that it could be considered a long-term strategic objective for FinTech organizations. Despite being ranked lower than other enablers in the ANP results, it will have a lasting influence on the sustainability of FinTech adoption in the future.

The conclusions and suggestions of this research are consistent with those of two more recent studies in 2022 [

93,

94]. Adopting FinTech in Saudi Arabia could be facilitated using the developed model in this research study, opening the door to the country’s following socioeconomic and financial advantages.

This research study revealed and modeled the enablers of FinTech innovation and their essential components and properties to pave the way for new developments in the FinTech sector. The developed model in this study followed a hybrid approach using ISM and ANP, which helped obtain a holistic perspective on the interplay between FinTech and innovation and overcome the limitations of other methods, which was recommended in a recent study in 2022 [

95].

6. Conclusions

Since FinTech has emerged as a hot topic for financiers, predictions of the widespread upheaval it will wreak on consumers and companies are a constant source of speculation. As with any new trend, hopes are raised as FinTech firms are forming and business visions and long-term plans are designed to keep the movement in this direction alive. Therefore, exploring what enables FinTech innovation to facilitate its development and foster its potential benefits is crucial. This research study aimed to identify and model the critical enablers of FinTech innovation by exploring contextual relationships among them and their priorities. The goal is accomplished following a hybrid approach in two main phases using the ISM and ANP modeling techniques.

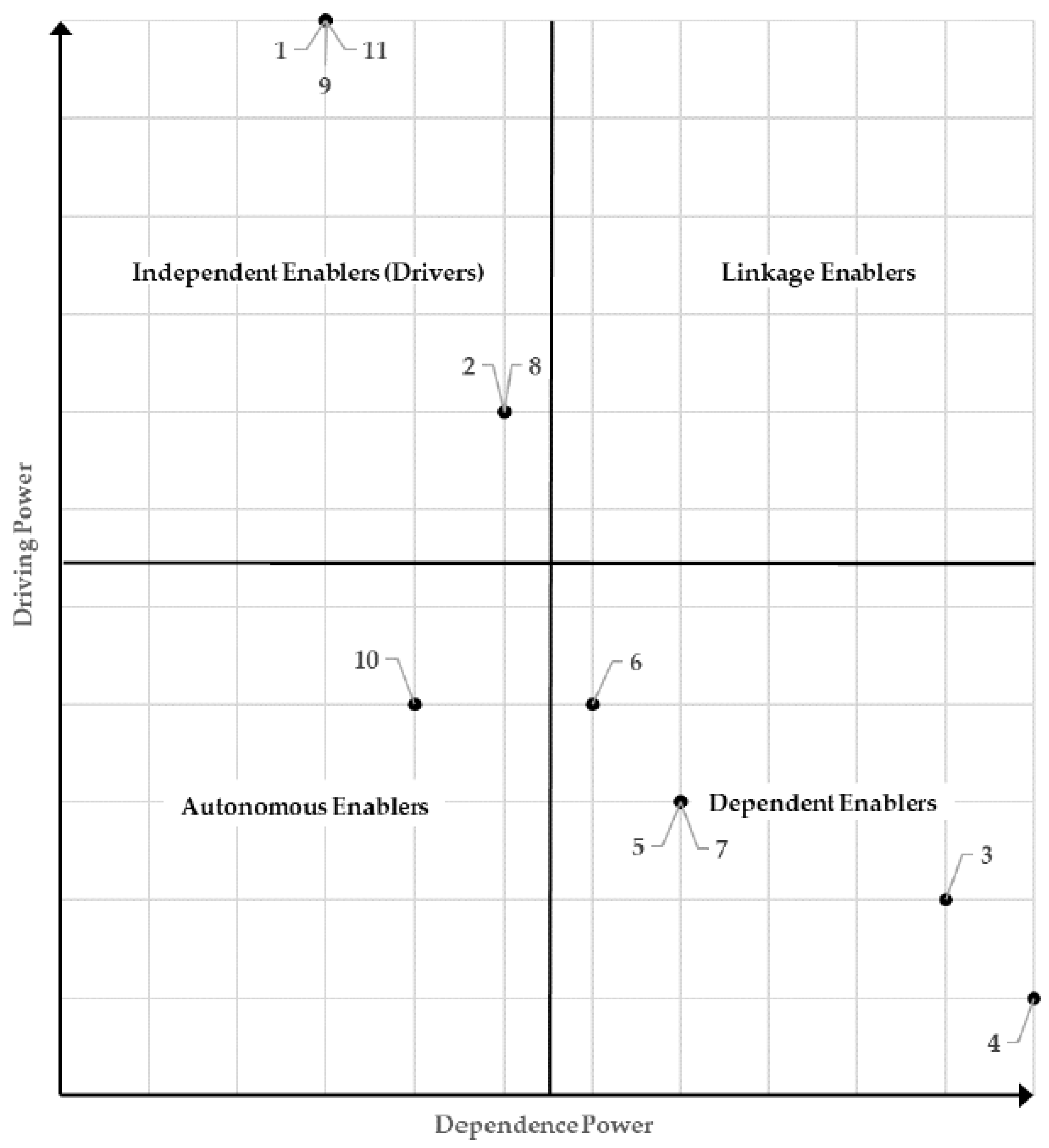

Results of the first phase revealed eleven critical enablers of FinTech innovation extracted from the literature and confirmed by experts’ opinions. An interpretive structural model based on interrelationships between them was developed. The study revealed that suitable regulation, policy, technology, framework, and model are foundational to FinTech innovation. Once ensured, regulators and payment systems should be the following points of focus. Then, security issues could be debugged to achieve customer protection, and digital insurance should be in place to develop the necessary financing infrastructure. Once achieved, financial ethics and literacy issues should be tackled to achieve personal data protection. In this sequence, all the enablers are required in FinTech innovation. Furthermore, the enablers were classified into four categories, each representing different degrees of dependency and driving powers. It was discovered that enablers that affect FinTech innovation, including financial ethics and literacy, personal data protection, customer protection, security, and infrastructure, classify as dependent enablers on other enablers, such as regulations and policies, regulators, payment systems, technology, and framework and model, with digital insurance being an autonomous enabler.

Results of the second phase revealed the enablers’ importance weights and their priority ranks using ANP. It was found that regulations and policies are relatively the most critical enabler of FinTech innovation, followed by framework and model, customer protection, payment systems, regulators, infrastructure, financial ethics and literacy, personal data protection, security, digital insurance, and technology being relatively the least important. This indicates that the technology by itself is an enabler of FinTech innovation, yet what is more important is the regulations and policies governing it, accounting for the security and protection of its users. These priority ranks were then incorporated into the developed ISM model in the first phase to establish the final ANP-weighted ISM model of critical enablers of FinTech innovation.

The developed model in this research study puts forward a holistic perspective on the interplay between FinTech and innovation and assists decision-makers, regulators, policy designers, practitioners, and technology developers in creating effective ways to safeguard the FinTech industry’s growth. The model provides a more profound understanding by answering questions about what critically enables FinTech innovation, how these enablers are interconnected, and their priorities. This is to facilitate the development of FinTech innovation, foster its potential benefits, and potentially put Saudi Arabia in a higher position as a FinTech center in the Middle East and the world. The scientific implication of this research study lies in following the hybrid approach using ISM and ANP, which could be used in future research directions studying similar complex problems comprising several interconnected elements.

Limitations of the study include that the developed model can only be extrapolated to the banking and finance industries. The enablers or barriers must be rethought and reshaped to be used in other fields or industries. Moreover, although the use of the ISM and ANP techniques in this study overcame the limitations of different methods and despite the reliability of the engaged experts and the utilized opinions data due to their experiences and close relation to the field of FinTech, the analysis heavily relies on their views, which may or may not align with the views of another group of experts. This is due to differences in backgrounds, perspectives, and bias; there will always be disagreements amongst those who are tasked with making important decisions, especially on emerging technologies. Furthermore, since all the experts chosen were Saudi nationals, the findings of this research study are expected to hold true for businesses in Saudi Arabia and may also be applicable in other emerging nations but may or may not be in developed countries. As a future research direction, further statistical modeling and sensitivity analysis might be applied to a more extensive data set, which would help eliminate the bias of numerical techniques and analyses based on data from a relatively small group of experts. Moreover, extending the existing study with a dynamic system approach allows for identifying the causal connection between the used enablers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}