Network Formation and Financial Inclusion in P2P Lending: A Computational Model

Abstract

1. Introduction

2. Materials and Methods

2.1. Literature Review

2.1.1. Platform Lending

2.1.2. Financial Inclusion and Platform Lending

2.2. Computational Model

SMEs Characteristics

3. Results

3.1. Number of Loans, Average Interest and Investment

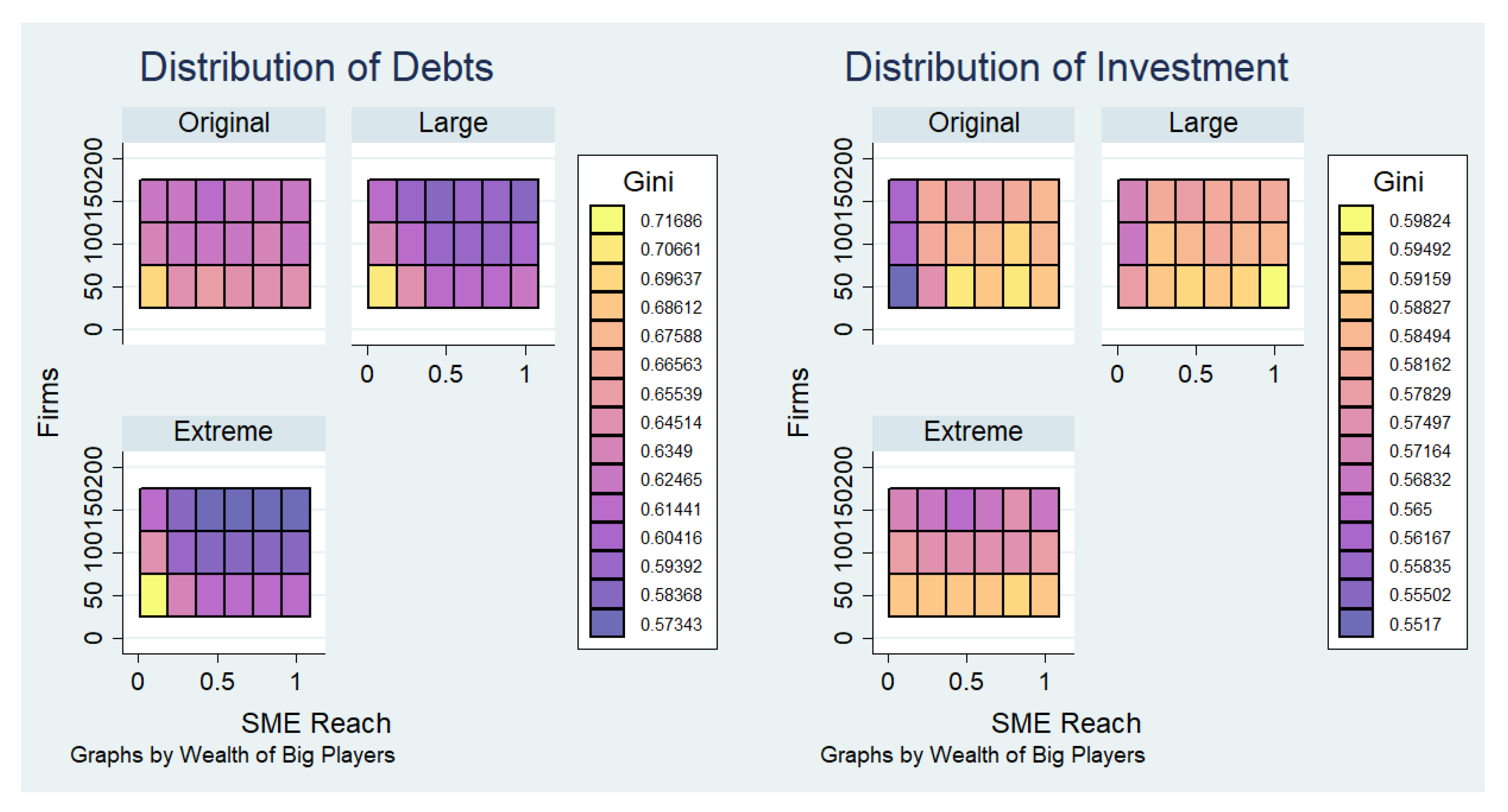

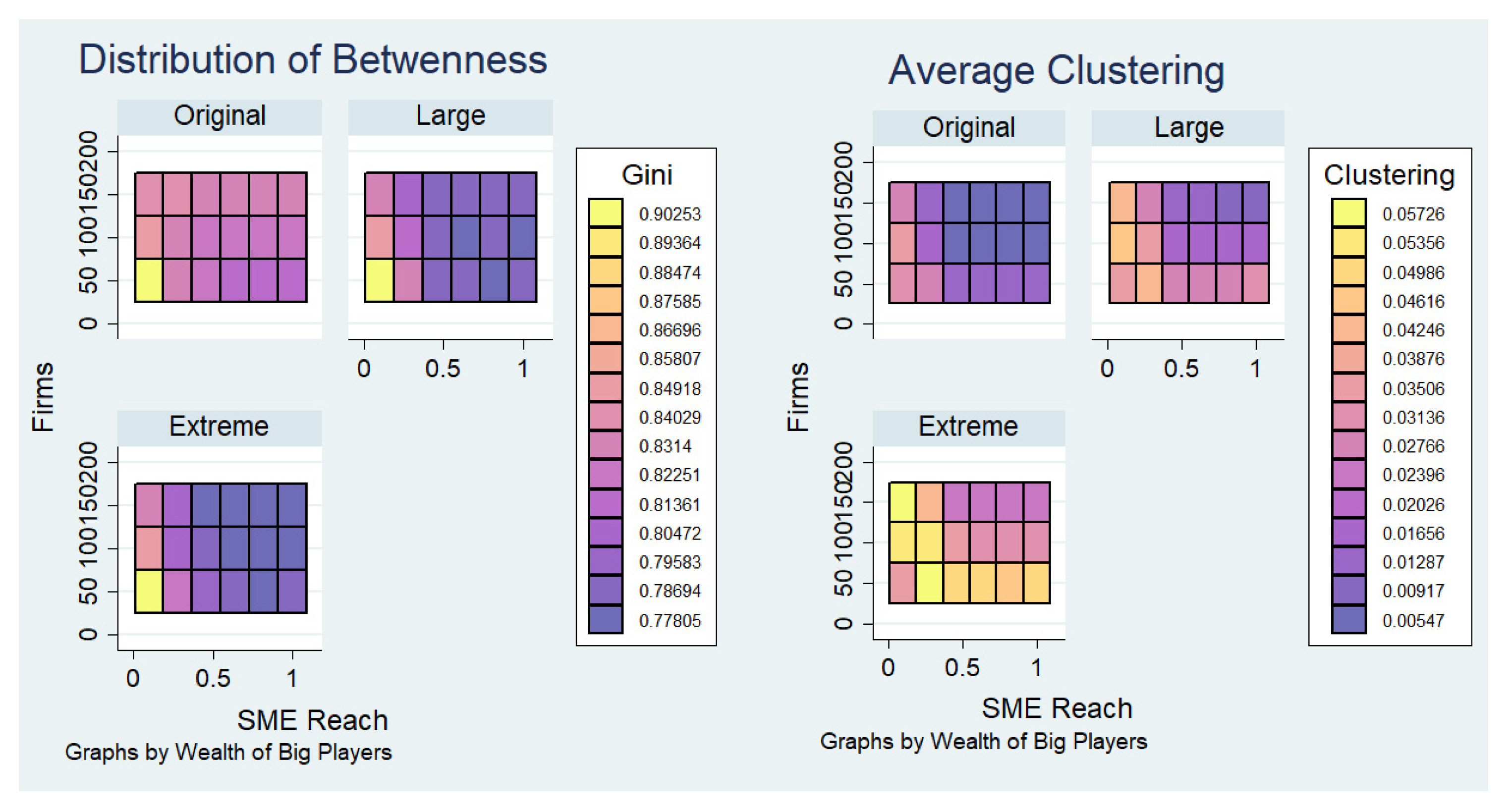

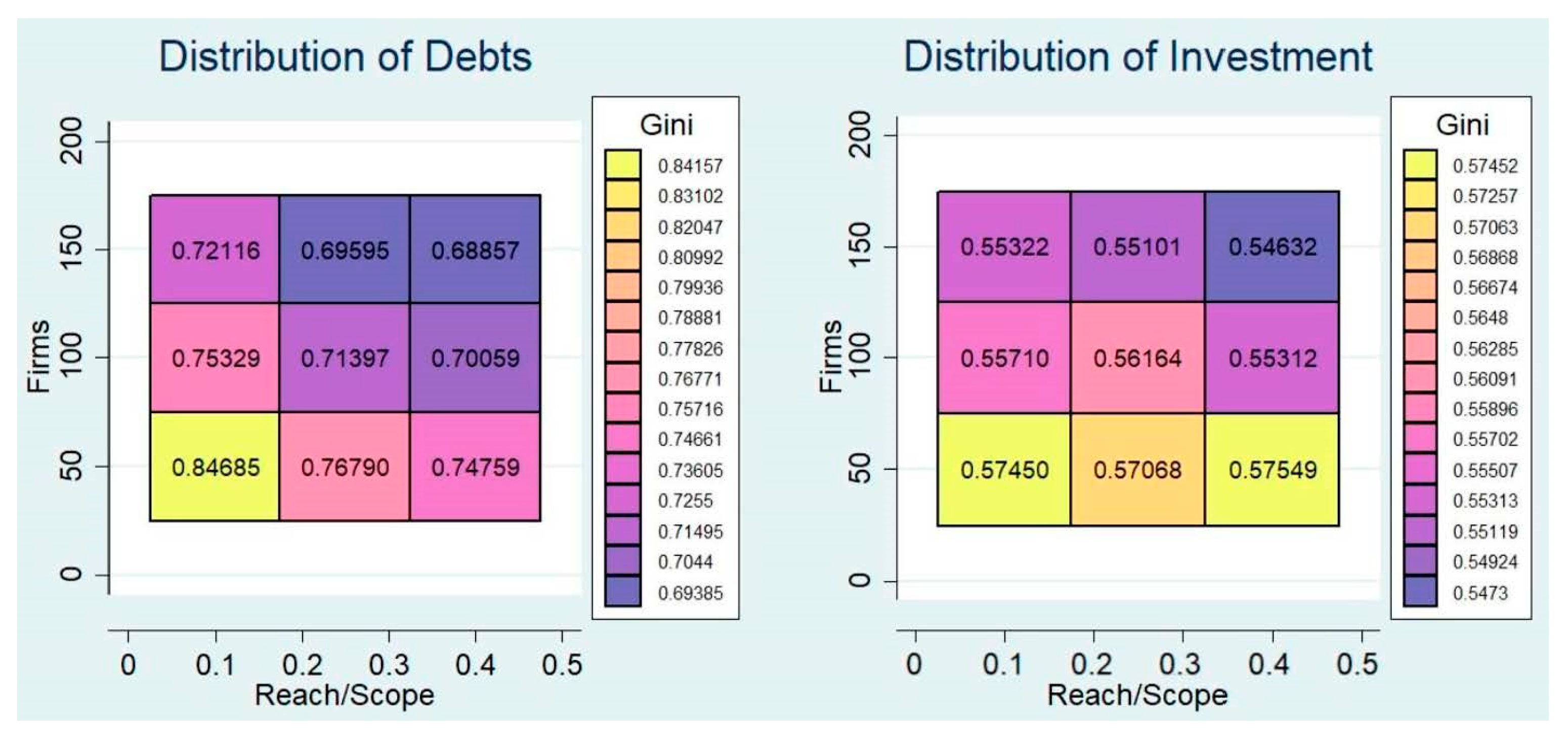

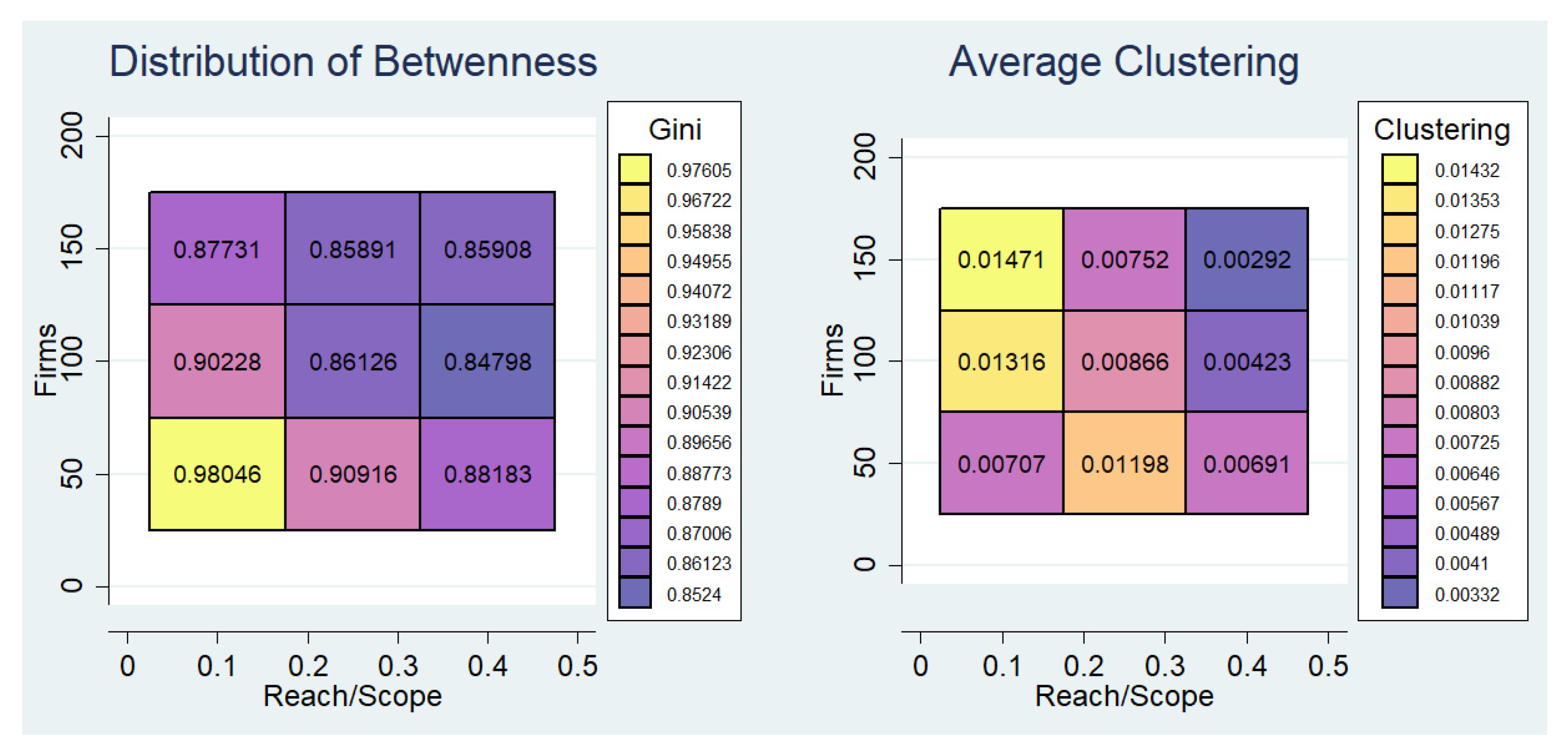

3.2. Financial Inclusion: Distribution of Debts and Investment and Network Characteristics

4. Discussion: Limitations and Future Steps

5. Conclusions

5.1. Research Contributions

5.2. Implications for Managers

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Additional Computational Experiments: Increasing the Number of Large Firms (LFs)

Appendix B. Model Extension. External Market Interest Rate Is Endogenous

References

- Alt, R.; Zimmermann, H.-D. Electronic Markets on platform competition. Electron. Mark. 2019, 29, 143–149. [Google Scholar] [CrossRef]

- Parker, G.; Van Alstyne, M.; Choudary, S. Platform Revolution; W.W. Norton & Company: New York, NY, USA, 2016; ISBN 9780393249132. [Google Scholar]

- Cáamara, N.; Tuesta, D. Measuring Financial Inclusion: A Multidimensional Index; BBVA Research Working Paper; BBVA: Bilbao, Spain, 2014. [Google Scholar]

- Grow, A.; Van Bavel, J. Assortative mating and the reversal of gender inequality in education in Europe: An agent-based model. PLoS ONE 2015, 10, e0127806. [Google Scholar] [CrossRef] [PubMed]

- Cardaci, A.; Saraceno, F. Inequality, Financialisation and economic crises: An agent-based model. Work. Pap. 2015. [Google Scholar]

- Frost, J. The Economic Forces Driving Fintech Adoption across Countries; Bank for International Settlements (“BIS”): Basel, Switzerland, 2020. [Google Scholar]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. Special Issue: Financial Information Systems and the Fintech Revolution. J. Manag. Inf. Syst. 2018, 35, 12–18. [Google Scholar] [CrossRef]

- Jagtiani, J.; Lemieux, C. Fintech Lending: Financial Inclusion, Risk Pricing, and Alternative Information Federal Reserve Bank of Philadelphia; Working Paper; Federal Reserve Bank of Philadelphia: Philadelphia, PA, USA, 2017. [Google Scholar]

- Berg, T.; Fuster, A.; Puri, M. Fintech Lending; NBER Working Paper Series; NBER: Cambridge, MA, USA, 2021. [Google Scholar]

- Ribeiro-Navarrete, S.; Piñeiro-Chousa, J.; Ángeles López-Cabarcos, M.; Palacios-Marqués, D. Crowdlending: Mapping the core literature and research frontiers. Rev. Manag. Sci. 2021, 1–31. [Google Scholar] [CrossRef]

- Katsamakas, E.; Sun, H. Machine Learning Crowdfunding. Int. J. Knowl.-Based Organ. 2020, 10, 1–11. [Google Scholar] [CrossRef]

- Belleflamme, P.; Lambert, T.; Schwienbacher, A. Crowdfunding: Tapping the right crowd. J. Bus. Ventur. 2014, 29, 585–609. [Google Scholar] [CrossRef]

- Belleflamme, P.; Omrani, N.; Peitz, M. Understanding the Strategies of Crowdfunding Platforms; Leibniz-Institut für Wirtschaftsforschung an der Universität München: Munich, Germany, 2016; Volume 2. [Google Scholar]

- Zhao, H.; Ge, Y.; Liu, Q.; Wang, G.; Chen, E.; Zhang, H. P2P lending survey: Platforms, recent advances and prospects. ACM Trans. Intell. Syst. Technol. 2017, 8, 1–28. [Google Scholar] [CrossRef]

- Serrano-Cinca, C.; Gutiérrez-Nieto, B.; López-Palacios, L. Determinants of Default in P2P Lending. PLoS ONE 2015, 10, e0139427. [Google Scholar] [CrossRef]

- Chen, Y.-R.; Leu, J.-S.; Huang, S.-A.; Wang, J.-T.; Takada, J.-I. Predicting Default Risk on Peer-to-Peer Lending Imbalanced Datasets. IEEE Access 2021, 9, 73103–73109. [Google Scholar] [CrossRef]

- Zeng, X.; Liu, L.; Leung, S.; Du, J.; Wang, X.; Li, T. A decision support model for investment on P2P lending platform. PLoS ONE 2017, 12, e0184242. [Google Scholar] [CrossRef]

- Wang, C.; Han, D.; Liu, Q.; Luo, S. A Deep Learning Approach for Credit Scoring of Peer-to-Peer Lending Using Attention Mechanism LSTM. IEEE Access 2019, 7, 2161–2168. [Google Scholar] [CrossRef]

- Ariza-Garzón, M.J.; Camacho-Miñano, M.D.M.; Segovia-Vargas, M.J.; Arroyo, J. Risk-return modelling in the p2p lending market: Trends, gaps, recommendations and future directions. Electron. Commer. Res. Appl. 2021, 49, 101079. [Google Scholar] [CrossRef]

- Basha, S.A.; Elgammal, M.M.; Abuzayed, B.M. Online peer-to-peer lending: A review of the literature. Electron. Commer. Res. Appl. 2021, 48, 101069. [Google Scholar] [CrossRef]

- Milne, A.; Parboteeah, P. The Business Models and Economics of Peer-to-Peer Lending. SSRN Electron. J. 2016. [Google Scholar] [CrossRef]

- Bruton, G.; Khavul, S.; Siegel, D.; Wright, M. New financial alternatives in seeding entrepreneurship: Microfinance, crowdfunding, and peer-to-peer innovations. Entrep. Theory Pract. 2015, 39, 9–26. [Google Scholar] [CrossRef]

- Abbasi, K.; Alam, A.; Brohi, N.A.; Brohi, I.A.; Nasim, S. P2P lending Fintechs and SMEs’ access to finance. Econ. Lett. 2021, 204, 109890. [Google Scholar] [CrossRef]

- Nemoto, N.; Huang, B.; Storey, D.J. Optimal Regulation of P2P Lending for Small and Medium-Sized Enterprises. SSRN Electron. J. 2019. [Google Scholar] [CrossRef]

- Cumming, D.J.; Hornuf, L. Marketplace Lending of SMEs. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Au, C.H.; Sun, Y. The development of P2P lending platforms: Strategies and implications. In Proceedings of the 40th International Conference on Information Systems, ICIS 2019, Munich, Germany, 15–18 December 2019. [Google Scholar]

- Au, C.H.; Tan, B.; Sun, Y. Developing a P2P lending platform: Stages, strategies and platform configurations. Internet Res. 2020. ahead-of-print. [Google Scholar] [CrossRef]

- Lin, M.; Prabhala, N.R.; Viswanathan, S. Judging borrowers by the company they keep: Friendship networks and information asymmetry in online peer-to-peer lending. Manag. Sci. 2013, 59, 17–35. [Google Scholar] [CrossRef]

- Liu, D.; Brass, D.J.; Lu, Y.; Chen, D. Friendships in online peer-to-peer lending: Pipes, prisms, and relational herding. MIS Q. 2015, 39, 729–742. [Google Scholar] [CrossRef]

- Freedman, S.; Jin, G.Z. The information value of online social networks: Lessons from peer-to-peer lending. Int. J. Ind. Organ. 2017, 51, 185–222. [Google Scholar] [CrossRef]

- Lee, E.; Lee, B. Herding behavior in online P2P lending: An empirical investigation. Electron. Commer. Res. Appl. 2012, 11, 495–503. [Google Scholar] [CrossRef]

- Yum, H.; Lee, B.; Chae, M. From the wisdom of crowds to my own judgment in microfinance through online peer-to-peer lending platforms. Electron. Commer. Res. Appl. 2012, 11, 469–483. [Google Scholar] [CrossRef]

- Cai, S.; Lin, X.; Xu, D.; Fu, X. Judging online peer-to-peer lending behavior: A comparison of first-time and repeated borrowing requests. Inf. Manag. 2016, 53, 857–867. [Google Scholar] [CrossRef]

- Worldbank Financial Inclusion Overview. Available online: https://www.worldbank.org/en/topic/financialinclusion/overview (accessed on 16 August 2022).

- Ozili, P.K. Financial inclusion research around the world: A review. Forum Soc. Econ. 2021, 50, 457–479. [Google Scholar] [CrossRef]

- Gálvez-Sánchez, F.J.; Lara-Rubio, J.; Verdú-Jóver, A.J.; Meseguer-Sánchez, V. Research Advances on Financial Inclusion: A Bibliometric Analysis. Sustainability 2021, 13, 3156. [Google Scholar] [CrossRef]

- Tram, T.X.H.; Lai, T.D.; Nguyen, T.T.H. Constructing a composite financial inclusion index for developing economies. Q. Rev. Econ. Financ. 2021, in press. [Google Scholar] [CrossRef]

- Philippon, T. On Fintech and Financial Inclusion; NBER Working Paper Series; NBER: Cambridge, MA, USA, 2019. [Google Scholar]

- Arner, D.W.; Buckley, R.P.; Zetzsche, D.A.; Veidt, R. Sustainability, FinTech and Financial Inclusion. Eur. Bus. Organ. Law Rev. 2020, 21, 7–35. [Google Scholar] [CrossRef]

- Gabor, D.; Brooks, S. The digital revolution in financial inclusion: International development in the fintech era. New Polit. Econ. 2017, 22, 423–436. [Google Scholar] [CrossRef]

- Sahay, R.; von Allmen, U.E.; von Lahreche, A.; Khera, P.; Ogawa, S.; Bazarbash, M.; Beaton, K. The Promise of Fintech: Financial Inclusion in the Post COVID-19 Era; International Monetary Fund: Wasington, DC, USA, 2020. [Google Scholar]

- Demir, A.; Pesqué-Cela, V.; Altunbas, Y.; Murinde, V. Fintech, financial inclusion and income inequality: A quantile regression approach. Eur. J. Financ. 2020, 28, 86–107. [Google Scholar] [CrossRef]

- Kling, G.; Pesqué-Cela, V.; Tian, L.; Luo, D. A theory of financial inclusion and income inequality. Eur. J. Financ. 2022, 28, 137–157. [Google Scholar] [CrossRef]

- Panos, G.A.; Wilson, J.O.S. Financial literacy and responsible finance in the FinTech era: Capabilities and challenges. Eur. J. Financ. 2020, 26, 297–301. [Google Scholar] [CrossRef]

- Schuetz, S.; Venkatesh, V. Blockchain, adoption, and financial inclusion in India: Research opportunities. Int. J. Inf. Manag. 2020, 52, 101936. [Google Scholar] [CrossRef]

- Makina, D. The Potential of FinTech in Enabling Financial Inclusion. In Extending Financial Inclusion in Africa; Academic Press: Cambridge, MA, USA, 2019; pp. 299–318. ISBN 9780128142035. [Google Scholar]

- Joia, L.A.; Cordeiro, J.P.V. Unlocking the potential of fintechs for financial inclusion: A delphi-based approach. Sustainability 2021, 13, 11675. [Google Scholar] [CrossRef]

- Kanungo, R.P.; Gupta, S. Financial inclusion through digitalisation of services for well-being. Technol. Forecast. Soc. Chang. 2021, 167, 120721. [Google Scholar] [CrossRef]

- Senyo, P.; Osabutey, E.L.C. Unearthing antecedents to financial inclusion through FinTech innovations. Technovation 2020, 98, 102155. [Google Scholar] [CrossRef]

- Ge, R.; Zheng, Z.; Tian, X.; Liao, L. Human-robot interaction: When investors adjust the usage of robo-advisors in peer-to-peer lending. Inf. Syst. Res. 2021, 32, 774–785. [Google Scholar] [CrossRef]

- Maskara, P.K.; Kuvvet, E.; Chen, G. The Role of P2P Platforms in Enhancing Financial Inclusion in US—An Analysis of Peer-to-Peer Lending Across the Rural-Urban Divide. Financ. Manag. 2020, 50, 747–774. [Google Scholar] [CrossRef]

- Ravishankar, M.N. Social innovations and the fight against poverty: An analysis of India’s first prosocial P2P lending platform. Inf. Syst. J. 2021, 31, 745–766. [Google Scholar] [CrossRef]

- Berentsen, A.; Markheim, M. Peer-to-Peer Lending and Financial Inclusion with Altruistic Investors. Int. Rev. Financ. 2021, 21, 1407–1418. [Google Scholar] [CrossRef]

- Deng, J. The crowding-out effect of formal finance on the P2P lending market: An explanation for the failure of China’s P2P lending industry. Financ. Res. Lett. 2022, 45, 102167. [Google Scholar] [CrossRef]

- Klein, G.; Shtudiner, Z.; Zwilling, M. Why do peer-to-peer (P2P) lending platforms fail? The gap between P2P lenders’ preferences and the platforms’ intentions. Electron. Commer. Res. 2021. [Google Scholar] [CrossRef]

- Burtch, G.; Ghose, A.; Wattal, S. Cultural Differences and Geography as Determinants of Online Prosocial Lending. MIS Q. 2014, 38, 773–794. [Google Scholar] [CrossRef]

- Lin, M.; Viswanathan, S. Home Bias in Online Investments: An Empirical Study of an Online Crowdfunding Market. Manag. Sci. 2015, 62, 1393–1414. [Google Scholar] [CrossRef]

- Singh, P.; Uparna, J.; Karampourniotis, P.; Horvat, E.-A.; Szymanski, B.; Korniss, G.; Bakdash, J.Z.; Uzzi, B. Peer-to-peer lending and bias in crowd decision-making. PLoS ONE 2018, 13, e0193007. [Google Scholar] [CrossRef] [PubMed]

- Fanta, A.B.; Makina, D. Unintended Consequences of Financial Inclusion. In Extending Financial Inclusion in Africa; Academic Press: Cambridge, MA, USA, 2019; pp. 231–256. ISBN 9780128142035. [Google Scholar]

- Igra, M.; Kenworthy, N.; Luchsinger, C.; Jung, J.K. Crowdfunding as a response to COVID-19: Increasing inequities at a time of crisis. Soc. Sci. Med. 2021, 282, 114105. [Google Scholar] [CrossRef] [PubMed]

- Kollenda, P. Financial returns or social impact? What motivates impact investors’ lending to firms in low-income countries. J. Bank. Financ. 2021, 136, 106224. [Google Scholar] [CrossRef]

- Haki, K.; Beese, J.; Aier, S.; Winter, R. The evolution of information systems architecture: An agent-based simulation model. MIS Q. Manag. Inf. Syst. 2020, 44, 155–184. [Google Scholar] [CrossRef]

- Zhang, M.; Chen, H.; Lyytinen, K. Validating the coevolutionary principles of business and IS alignment via agent-based modeling. Eur. J. Inf. Syst. 2020, 30, 496–511. [Google Scholar] [CrossRef]

- Fischbach, K.; Marx, J.; Weitzel, T. Agent-based modeling in social sciences. J. Bus. Econ. 2021, 91, 1263–1270. [Google Scholar] [CrossRef]

- Macal, C.M. Everything you need to know about agent-based modelling and simulation. J. Simul. 2016, 10, 144–156. [Google Scholar] [CrossRef]

- Rand, W.; Stummer, C. Agent-based modeling of new product market diffusion: An overview of strengths and criticisms. Ann. Oper. Res. 2021, 305, 425–447. [Google Scholar] [CrossRef]

- Arthur, W.B. Foundations of complexity economics. Nat. Rev. Phys. 2021, 3, 136–145. [Google Scholar] [CrossRef]

- Axtell, R.L.; Farmer, J.D. Agent-Based Modeling in Economics and Finance: Past, Present, and Future; Working Paper GMU and SFI; Institute for New Economic Thinking at the Oxford Martin School, University of Oxford: Oxford, UK, 2018. [Google Scholar]

- Tesfatsion, L. Agent-based computational economics: Modeling economies as complex adaptive systems. Inf. Sci. 2003, 149, 263–269. [Google Scholar] [CrossRef]

- Wu, S.; Mu, P.; Shen, J.; Wang, W. An incentive mechanism model of credit behavior of SMEs based on the perspective of credit default swaps. Complexity 2020, 2020, 6639636. [Google Scholar] [CrossRef]

- Frick, W. Corporate Inequality Is the Defining Fact of Business Today. Available online: https://hbr.org/2016/05/corporate-inequality-is-the-defining-fact-of-business-today (accessed on 16 August 2022).

- Armstrong, M.; Vickers, J. Patterns of Competitive Interaction. Econometrica 2022, 90, 153–191. [Google Scholar] [CrossRef]

- Shang, Y. An agent based model for opinion dynamics with random confidence threshold. Commun. Nonlinear Sci. Numer. Simul. 2014, 19, 3766–3777. [Google Scholar] [CrossRef]

- Casner, B. Seller curation in platforms. Int. J. Ind. Organ. 2020, 72, 102659. [Google Scholar] [CrossRef]

- Dowling, M.; O’Gorman, C.; Puncheva, P.; Vanwalleghem, D. Trust and SME attitudes towards equity financing across Europe. J. World Bus. 2019, 54, 101003. [Google Scholar] [CrossRef]

- Farris, F.A. The Gini index and measures of inequality. Am. Math. Mon. 2010, 117, 851–864. [Google Scholar] [CrossRef]

- Shang, Y. A note on the H index in random networks. J. Math. Sociol. 2018, 42, 77–82. [Google Scholar] [CrossRef]

- Identity Review Top Six Decentralized Lending Platforms. Available online: https://identityreview.com/top-six-decentralized-lending-platforms/ (accessed on 17 March 2022).

- Veiga, A.; Weyl, E.G.; White, A. Multidimensional Platform Design. Am. Econ. Rev. 2017, 107, 191–195. [Google Scholar] [CrossRef]

- Teh, T.-H. Platform Governance. Am. Econ. J. Microecon. 2021, 14, 213–254. [Google Scholar] [CrossRef]

- Valletti, T.; Prat, A. Attention oligopoly. Am. Econ. J. Microecon. 2021, 14, 530–557. [Google Scholar]

- Yan, Y.; Lv, Z.; Hu, B. Building investor trust in the P2P lending platform with a focus on Chinese P2P lending platforms. Electron. Commer. Res. 2018, 18, 203–224. [Google Scholar] [CrossRef]

- Chen, D.; Lai, F.; Lin, Z. A trust model for online peer-to-peer lending: A lender’s perspective. Inf. Technol. Manag. 2014, 15, 239–254. [Google Scholar] [CrossRef]

- Dorfleitner, G.; Oswald, E.M.; Zhang, R. From Credit Risk to Social Impact: On the Funding Determinants in Interest-Free Peer-to-Peer Lending. J. Bus. Ethics 2019, 170, 375–400. [Google Scholar] [CrossRef]

- Lagna, A.; Ravishankar, M.N. Making the world a better place with fintech research. Inf. Syst. J. 2022, 32, 61–102. [Google Scholar] [CrossRef]

- Croxson, K.; Frost, J.; Gambacorta, L.; Valletti, T. Platform-Based Business Models and Financial Inclusion; BIS Working Papers; BIS: Basel, Switzerland, 2022. [Google Scholar]

- Katsamakas, E.; Miliaresis, K.; Pavlov, O. V Digital Platforms for the Common Good: Social Innovation for Active Citizenship and ESG. Sustainability 2022, 14, 639. [Google Scholar] [CrossRef]

- Bonina, C.; Koskinen, K.; Eaton, B.; Gawer, A. Digital platforms for development: Foundations and research agenda. Inf. Syst. J. 2021, 31, 869–902. [Google Scholar] [CrossRef]

- MacCrory, F.; Katsamakas, E. Competition of Multi-Platform Ecosystems in the IoT. SSRN Electron. J. 2021, 1–52. [Google Scholar] [CrossRef]

- Jacobides, M.G.; Cennamo, C.; Gawer, A. Towards a theory of ecosystems. Strateg. Manag. J. 2018, 39, 2255–2276. [Google Scholar] [CrossRef]

- Liu, J.; Dong, J. A multi-agent simulation of investment choice in the P2P lending market with bankruptcy risk. J. Simul. 2022, 16, 32–146. [Google Scholar] [CrossRef]

- Sanchez-Cartas, J.M.; Katsamakas, E. Artificial Intelligence, Algorithmic Competition and Market Structures. IEEE Access 2022, 10, 10575–10584. [Google Scholar] [CrossRef]

- Sanchez-Cartas, J.M.; Katsamakas, E. Effects of Algorithmic Pricing on Platform Competition. SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Beese, J.; Haki, M.K.; Aier, S.; Winter, R. Simulation-Based Research in Information Systems: Epistemic Implications and a Review of the Status Quo. Bus. Inf. Syst. Eng. 2019, 61, 503–521. [Google Scholar] [CrossRef]

- Pavlov, O.V.; Katsamakas, E. Will colleges survive the storm of declining enrollments? A computational model. PLoS ONE 2020, 15, e0236872. [Google Scholar] [CrossRef]

- Georgantzas, N.C.; Katsamakas, E. Information systems research with system dynamics. Syst. Dyn. Rev. 2008, 24, 274–284. [Google Scholar] [CrossRef]

- Georgantzas, N.C.; Katsamakas, E.G. Performance effects of information systems integration: A system dynamics study in a media firm. Bus. Process Manag. J. 2010, 16, 822–846. [Google Scholar] [CrossRef]

- Rahmandad, H.; Sterman, J. Heterogeneity and Network Structure in the Dynamics of Diffusion: Comparing Agent-Based and Differential Equation Models. Manage. Sci. 2008, 54, 998–1014. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Platform Attributes | ||

|---|---|---|

| Platform Scale | N | Number of agents (SMEs) on the platform |

| SME Reach | R | % of other agents reachable by an SME |

| Maximum Risk Threshold | X | Maximum loan risk allowed on the platform |

| Insurance | The platform may offer an insurance product | |

| Loans | {Lij} | Set of all loans created on the platform (a loan is from agent i to agent j) |

| SME (agent i) attributes | ||

| Investment opportunity | An agent may come up with an investment idea during the simulation, and may need to borrow through the platform | |

| Liquidity | An agent may acquire liquidity during the simulation, which may be given to another agent as a loan that earns income | |

| Risk threshold | ri | Maximum risk the agent i is willing to accept as a lender |

| SME Risk Metric (Platform calculates and makes visible to all agents on the platform) | RMit | Riskiness of agent i as a borrower in period t (TotalAssetsit/TotalLiabilitiesit) |

| Risk Threshold (%) and SME Reach | Platform Scale (N) | ||

|---|---|---|---|

| 50 | 100 | 150 | |

| Risk Threshold: 0.5 | |||

| 0.1 | 37.90 (5.03) | 99.29 (9.08) | 160.62 (12.79) |

| 0.2 | 53.21 (7.68) | 113.69 (12.70) | 172.82 (15.72) |

| 0.4 | 56.66 (9.40) | 115.52 (13.70) | 173.78 (16.27) |

| 0.6 | 56.97 (9.54) | 115.58 (13.10) | 173.55 (16.46) |

| 0.8 | 57.12 (9.36) | 115.46 (13.82) | 173.78 (16.05) |

| 1 | 56.78 (9.27) | 115.84 (13.02) | 174.02 (16.67) |

| Risk Threshold: 0.7 | |||

| 0.1 | 39.83 (5.44) | 104.75 (9.99) | 170.87 (14.55) |

| 0.2 | 57.40 (8.76) | 122.61 (13.99) | 185.97 (18.12) |

| 0.4 | 61.20 (10.35) | 123.97 (14.93) | 186.92 (18.86) |

| 0.6 | 61.22 (10.78) | 124.63 (15.18) | 187.00 (18.55) |

| 0.8 | 60.88 (10.62) | 124.93 (15.90) | 187.11 (18.79) |

| 1 | 61.37 (10.75) | 124.00 (15.50) | 185.67 (18.46) |

| Risk Threshold: 1 | |||

| 0.1 | 40.84 (5.61) | 108.85 (10.49) | 178.80 (15.10) |

| 0.2 | 59.72 (9.18) | 129.09 (15.16) | 195.90 (20.00) |

| 0.4 | 64.73 (11.38) | 131.73 (16.35) | 197.66 (20.32) |

| 0.6 | 64.81 (11.79) | 131.81 (17.12) | 198.09 (20.36) |

| 0.8 | 64.57 (11.67) | 132.26 (16.70) | 197.35 (21.00) |

| 1 | 64.64 (11.73) | 132.36 (16.68) | 197.76 (21.16) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Katsamakas, E.; Sánchez-Cartas, J.M. Network Formation and Financial Inclusion in P2P Lending: A Computational Model. Systems 2022, 10, 155. https://doi.org/10.3390/systems10050155

Katsamakas E, Sánchez-Cartas JM. Network Formation and Financial Inclusion in P2P Lending: A Computational Model. Systems. 2022; 10(5):155. https://doi.org/10.3390/systems10050155

Chicago/Turabian StyleKatsamakas, Evangelos, and J. Manuel Sánchez-Cartas. 2022. "Network Formation and Financial Inclusion in P2P Lending: A Computational Model" Systems 10, no. 5: 155. https://doi.org/10.3390/systems10050155

APA StyleKatsamakas, E., & Sánchez-Cartas, J. M. (2022). Network Formation and Financial Inclusion in P2P Lending: A Computational Model. Systems, 10(5), 155. https://doi.org/10.3390/systems10050155