Digital Transformation Reduces Costs of the Paints and Coatings Development Process

Abstract

1. Introduction

2. Materials and Methods

- The conventional practice of process execution—presented with the As-Is model,

- Process execution after the digital transformation—presented with the To-Be model.

- Licensing fees (“on-premises vs. cloud-hosted”), implementation costs, training costs, integration costs, development costs, support costs, and maintenance and upgrade costs [15];

- Labor costs, training costs, testing costs, re-engineered processes costs, change management costs, customization and integration costs, customer dissatisfaction costs, and ongoing support and maintenance costs [16].

- The salary of staff and management involved in the implementation and analysis,

- Labor costs that have been interrupted or delayed due to system implementation,

- The cost of the work environment’s adjustment—technical and ergonomic [19] adjustments,

- Cost and time spent on employee training.

- Licensing fees, which include: package software, licenses and upgrades costs, and operations costs;

- Implementation costs, which include: implementation, installation, configuration, management effort and dedication, employee motivation, employee time and strains on resources costs, and data communication;

- Maintenance costs, which include: maintenance of the system and maintenance of data;

- Training costs, which include: training (study time and course participation time) costs;

- Change management costs, such as project management, management time, communication, management/staff resources, overheads, software disposal, hardware disposal, business process re-engineering (BPR), organizational restructuring, staff-related costs (changes in salaries), and commissioning costs;

- Opportunity costs, which include: opportunity costs and risks, implementation risks (covert resistance), productivity loss, and personnel issues costs.

- The technical enabler is cloud-based information technology,

- The provider of technical enabler covers system maintenance costs,

- The provider performs web-based training.

- X—the number of newly developed products when digital transformation rentability threshold is reached,

- ΔCpd—the difference between the average cost of executing the process in a conventional manner and the average cost of executing the process after digital transformation,

- CDT—costs of digital transformation.

- Cpd1—the average cost of new product development in a conventional manner (before digital transformation),

- Cpd2—the average cost of new product development after digital transformation.

2.1. Product Development’s Costs (ΔCpd)

- A smaller number of laboratory tests,

- Lower material consumption,

- Less labor (due to shorter activities times).

- Pm—material costs,

- n—the number of ingredients in the formulation,

- mi—the mass of each ingredient in the formulation (rounded up to the packaging unit),

- pi—the price of each ingredient’s packaging unit.

- Less workload due to shorter development time,

- Faster ingredient purchase,

- The lower purchase price,

- Cheaper handover of ingredients.

2.2. Costs of Digital Transformation (CDT)

- CDT—costs of digital transformation,

- Cl—licensing costs,

- Ci—implementation costs,

- Cm—maintenance costs,

- Ct—training costs,

- Cc—change management costs,

- Co—opportunity costs (due to the elimination of existing tools).

- Manual data input (on new ingredients from safety data sheets)—by the provider,

- Manual data input (on new ingredients from safety data sheets)—by the user,

- Manual formulation input (by the provider),

- Manual formulation input (by the user),

- Automatic capture by the parsing of the safety data sheets (.pdf format) and manual correction of the data,

- Automatic data transfer from the ERP system.

- The preparative tasks of the trainer,

- The working time required to engage the trainer during the training,

- The working time needed for the active participation of the participants during the training,

- An e-learning platform.

3. Results

3.1. Costs Analysis of the Existing Paints and Coatings Development Process

- The conventional process of new product development without ICT support,

- New product development process with ICT support and the use of a local database.

- ci—the cost of a particular activity (€),

- ti—time of particular activity (h),

- pi—the price of work per hour for a particular activity (€/h),

- C—the total cost of product development (€).

3.2. The Paints and Coatings Development Process Redesign

3.3. Results of the Redesigned Process Costs Analysis

3.4. The Costs of Digital Transformation (Case Results)

3.4.1. Licensing Costs

- Five employees participated in the development process,

- Prepared and managed 500 SDS per month,

- Used 200 hazardous ingredients,

- Had up to 300 active ingredients in the database,

- Had up to 100 active formulations (products) in the database.

- Cl—licensing costs,

- Ccl—the costs of the selected license (€/month),

- CcSDS—the costs of the selected scope of SDS creation (€/month),

- CcRD—the costs of the selected scope of the regulatory dashboard (€/month).

3.4.2. Implementation Costs

- Ingredients input,

- Formulation input,

3.4.3. Maintenance Costs

3.4.4. Training Costs

- For the trainer,

- For five users (the average hourly rate according to education was taken into account),

3.4.5. Change Management Costs

3.5. The Eligibility of the Digital Process Transformation

4. Discussion and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References and Note

- Nurioglu, A.G.; Esteves, A.C.C.; De With, G. Non-toxic, non-biocide-release antifouling coatings based on molecular structure design for marine applications. J. Mater. Chem. B. 2015, 3, 6547–6570. [Google Scholar] [CrossRef] [PubMed]

- Akafuah, N.K.; Poozesh, S.; Salaimeh, A.; Patrick, G.; Lawler, K.; Saito, K. Evolution of the automotive body coating process—A review. Coatings 2016, 6, 24. [Google Scholar] [CrossRef]

- Kern, T.; Krhač, E.; Senegačnik, M.; Urh, B. Digitalizing the Paints and Coatings Development Process. Processes 2019, 7, 539. [Google Scholar] [CrossRef]

- Urh, B.; Senegačnik, M.; Kern, T.; Krhač, E. Reducing waste of laboratory tests in the coating development process. Pol. J. Environ. Stud. 2020, 29, 3841–3851. [Google Scholar] [CrossRef]

- Eurostat. Industry by Employment Size Class (NACE Rev 2, B-E) Manufacture of Paints, Varnishes and Similar Coatings, Printing Ink and Mastics. 2019. Available online: https://appsso.eurostat.ec.europa.eu/nui/submitViewTableAction.do (accessed on 7 November 2019).

- Partidário, P.J.; Verdragt, P.H.J. Shaping sustainable technology development in the coatings chain Defining boundaries, environmental problems and main players. J. Clean. Prod. 2000, 8, 201–214. [Google Scholar] [CrossRef]

- Staring, E.; Dias, A.A.; Van Benthem, R.A. New challenges for R&D in coating resins. Prog. Org. Coat. 2002, 45, 101–117. [Google Scholar] [CrossRef]

- Cole, I.S.; Hughes, A.E. Designing molecular protection: New paradigm for developing corrosion resistant materials uniting high throughput studies, multiscale modelling and self-repair. Corros. Eng. Sci. Technol. 2014, 49, 109–115. [Google Scholar] [CrossRef]

- Bohorquez, S.J.; Van den Berg, P.; Akkerman, J.; Mestach, D.; Van Loon, S.; Repp, J. High-throughput paint optimisation by use of a pigment-dispersing polymer. Surf. Coat. Int. 2015, 98, 85–89. [Google Scholar]

- Björklund, S.; Goel, S.; Joshi, S. Function-dependent coating architectures by hybrid powder suspension plasma spaying: Injector design, processing and concept validation. Mater. Des. 2018, 142, 56–65. [Google Scholar] [CrossRef]

- Coatingstech, Coatings Xperience: Accelerating Coatings Development with High Throughput Technology. Available online: https://www.paint.org/coatingstech-magazine/articles/accelerating-coatings-development-high-throughput-technology/ (accessed on 8 May 2020).

- Nameer, S.; Johansson, M. Fully bio-based aliphatic thermoset polyesters via self-catalyzed self-condensation of multifunctional epoxy monomers directly extracted from natural sources. J. Coat. Technol. Res. 2017, 14, 757–765. [Google Scholar] [CrossRef]

- Ben-Arieh, D.; Qian, L. Activity-based cost management for design and development stage. Int. J. Prod. Econ. 2003, 83, 169–183. [Google Scholar] [CrossRef]

- Nibusiness.Info.Co.UK [nd] Change Management—Cost of Change Management. Available online: https://www.nibusinessinfo.co.uk/content/cost-change-management (accessed on 19 June 2020).

- Moadad, S. The Hidden Costs of ERP Implementation. Medium. Available online: https://medium.com/@shadi.moadad/the-hidden-costs-of-erp-implementation-d4eb17b7d8a6 (accessed on 21 April 2020).

- Miller, H. 9 hidden ERP Costs that can Blow Your Implementation Budget. ERP FOCUS. Available online: https://www.erpfocus.com/hidden-erp-costs-1621.html (accessed on 16 July 2020).

- Barreau, D. The hidden costs of implementing and maintaining information systems. Bottom Line 2001, 14, 207–212. [Google Scholar] [CrossRef]

- Alter, S. Information Systems: A Management Perspective, 3rd ed.; Benjamin Cummings: Menlo Park, CA, USA, 1999. [Google Scholar]

- Balantič, Z.; Polajnar, A.; Jevšnik, S. Ergonomics in Theory and Practice; National Institute for Public Health: Ljubljana, Slovenia, 2016. [Google Scholar]

- Irani, Z.; Ghoneim, A.; Love, P.E.D. Evaluating cost taxonomies for information systems management. EJOR 2006, 73, 1103–1122. [Google Scholar] [CrossRef]

- DKE Deutsche Kommission Elektrotechnik Elektronik Informationstechnik in DIN und VDE, German Standardization Roadmap, Industrie 4.0. Available online: https://www.din.de/blob/65354/57218767bd6da1927b181b9f2a0d5b39/roadmap-i4-0-e-data.pdf (accessed on 9 May 2020).

- Gartner ®. The 2019 CIO Agenda: Securing a New Foundation for Digital Business. Available online: https://www.gartner.com/doc/3891665/cio-agenda-securing-new-foundation (accessed on 9 May 2020).

- Challener, C. The Paint and Coatings Industry in the Age of Digitalization. Available online: https://www.paint.org/coatingstech-magazine/articles/paint-coatings-industry-age-digitalization/ (accessed on 16 July 2020).

- ALLCHEMIST®. Digital Platform for Experts Working in the Paint Coatings Industry Who Want to Work Directly with Data Instead of Datasheets 2018. Available online: https://www.allchemist.net/ (accessed on 7 November 2019).

- Chamber of Commerce and Industry of Slovenia (Gospodarska Zbornica Slovenije): Plačni Kažipot—Podatki za Obračun Prejemkov (in Slovene). Available online: https://www.gzs.si/Portals/SN-Pravni-Portal/Vsebine/novice-priponke/PK_2019_1.pdf (accessed on 21 April 2020).

- Labour Costs, Slovenia. Republic of Slovenia Statistical Office, 2018. Available online: https://www.stat.si/StatWeb/News/Index/8443 (accessed on 21 April 2020).

- Pellinen, J. Costs Factors of Training—How to Calculate Your Training Budget (9.4. 2019). Available online: https://www.vuolearning.com/en/blog/training-budget (accessed on 21 April 2020).

- Saunders, P.; Ganly, D.; Torii, D. How to Develop Initial Cost Estimates for ERP Initiatives. Gartner®. Available online: https://www.gartner.com/document/3947229?ref=solrAll&refval=253149678 (accessed on 16 June 2020).

- ALLCHEMIST®. Pricing. Internal Document of the COMPANY—Allchemist Provider

- Spak, N.; Kuzmin, O.; Dvulit, Z.; Onysenko, T.; Sroka, W. Digitalization of the Marketing Activities of Enterprises: Case Study. Information 2020, 11, 109. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

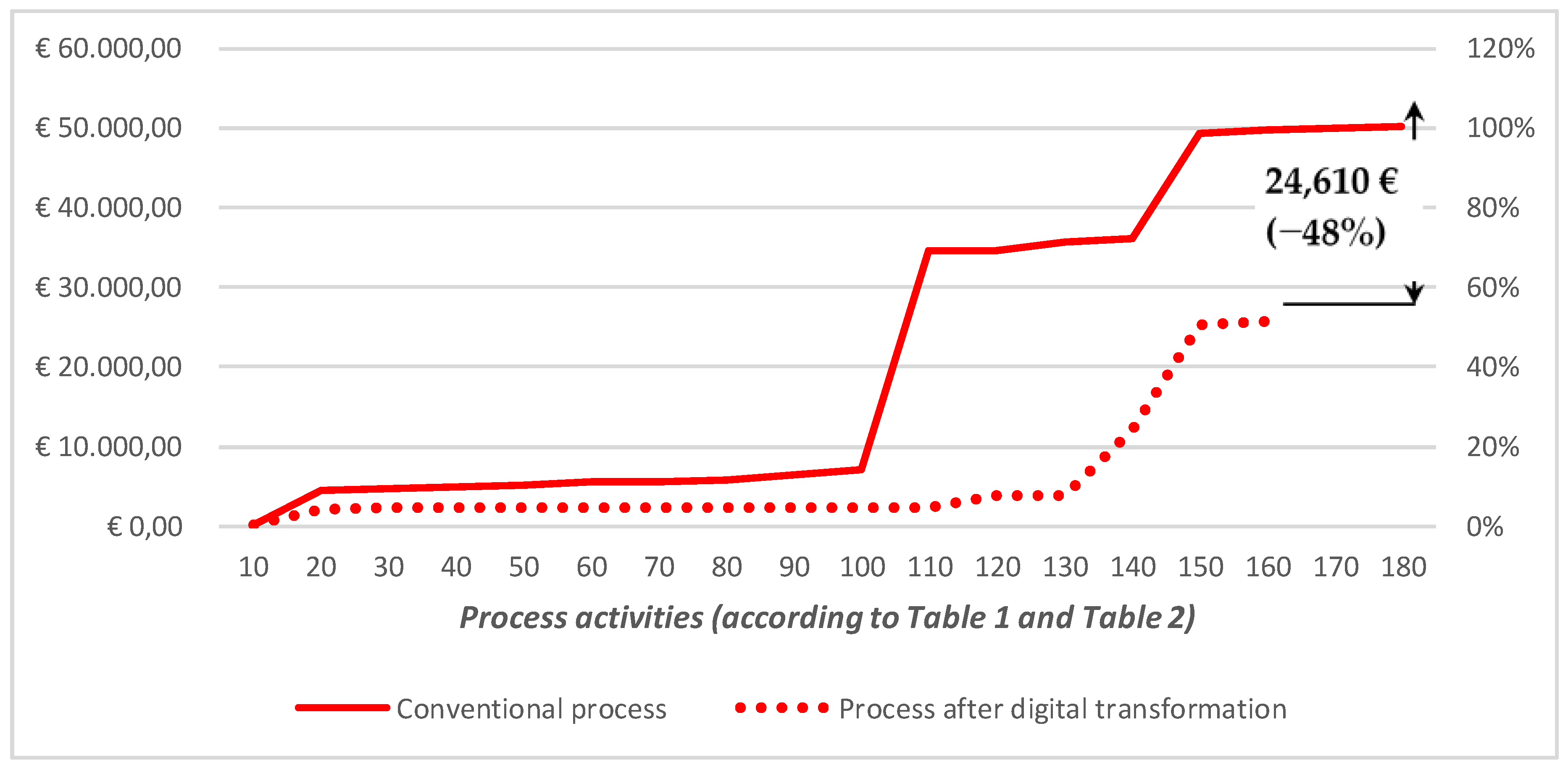

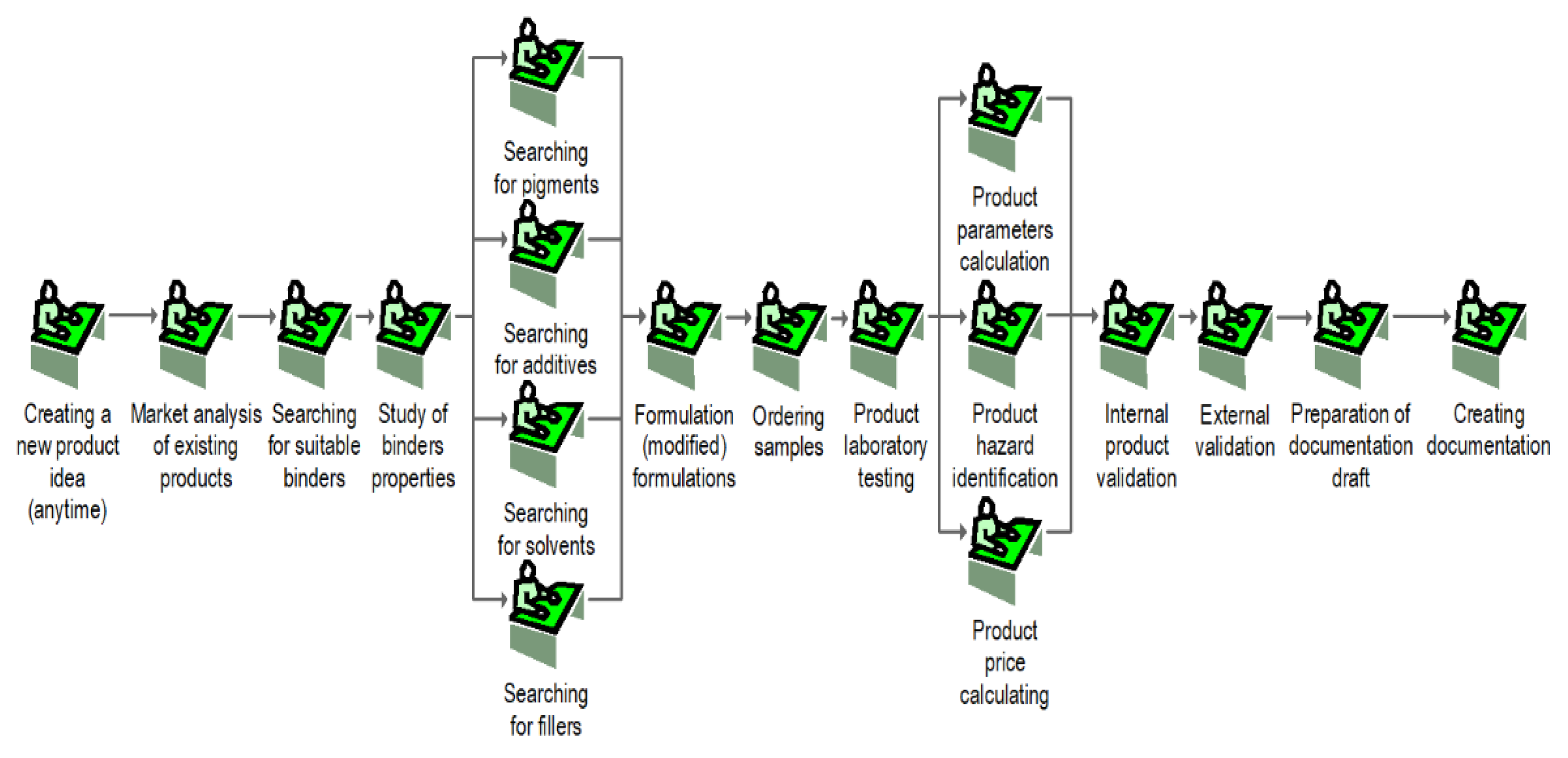

| The Conventional New Product Development Process | |||||

|---|---|---|---|---|---|

| ## | Process Activities | Probability 1 | Work for One Successful Product 2 (h) | The Cost of One Work’s Hour 3 (€) | The Cost of Activity Execution (€) |

| 10 | Creating a new product idea | 0.06 | 10.31 | 21.95 | 226.36 |

| 20 | Market analysis of existing products | 1.00 | 165.00 | 25.35 | 4181.93 |

| 30 | Searching for suitable binders | 0.92 | 9.74 | 25.35 | 246.85 |

| 40 | Study of binders properties | 1.00 | 10.63 | 25.35 | 269.29 |

| 50 | Searching for pigments | 0.19 | 10.63 | 25.35 | 269.29 |

| 60 | Searching for additives | 13.13 | 25.35 | 332.65 | |

| 70 | Searching for solvents | 3.33 | 25.35 | 84.48 | |

| 80 | Searching for fillers | 3.33 | 25.35 | 84.48 | |

| 90 | Formulation (modified) formulations | 1.00 | 28.89 | 25.35 | 732.19 |

| 100 | Ordering samples | 1.00 | 32.22 | 21.95 | 707.28 |

| 110 | Product laboratory testing | 0.50 | 1248.89 | 21.95 | 27,413.11 |

| 120 | Product parameters measurement | 0.40 | 5.44 | 25.35 | 137.99 |

| 130 | Product hazard identification | 39.44 | 25.35 | 999.72 | |

| 140 | Product price calculating | 16.11 | 25.35 | 408.34 | |

| 150 | Internal validation | 0.50 | 600.89 | 21.95 | 13,189.51 |

| 160 | External validation | 0.75 | 23.47 | 21.95 | 515.09 |

| 170 | Preparation of documentation draft | 1.00 | 5.37 | 21.95 | 117.80 |

| 180 | Creating documentation | 1.00 | 18.70 | 21.95 | 410.47 |

| Total product development costs: | 2245.52 | 50,326.83 | |||

- Labor costs for the employer 2019, engineer, chemistry = 16.75 €/h × 1.203 = 20.15 €/h

- Labor costs for the employer 2019, MSc, chemistry = 16.75 €/h × 1.481= 23.75 €/h

- Labor costs for the employer 2019, Ph.D, chemistry = 16.75 €/h × 1.716 = 28.74 €/h.

| New Product Development Process after Digital Transformation | |||||

|---|---|---|---|---|---|

| ## | Process Activities | Probability 1 | Work for One Successful Product 2 (h) | The Cost of One Work’s Hour 3 (€) | The Cost of Activity Execution (€) |

| 10 | Creating a new product idea | 0.06 | 4.64 | 21.95 | 101.86 |

| 20 | Market analysis of existing products | 0.92 | 82.50 | 25.35 | 2090.96 |

| 30 | Searching for suitable binders | 0.19 | 0.53 | 25.35 | 13.46 |

| 40 | Searching for pigments | 0.53 | 25.35 | 13.46 | |

| 50 | Searching for additives | 0.66 | 25.35 | 16.63 | |

| 60 | Searching for solvents | 0.17 | 25.35 | 4.22 | |

| 70 | Searching for fillers | 0.17 | 25.35 | 4.22 | |

| 80 | Formulation (modified) formulations | 1.00 | 1.44 | 25.35 | 36.61 |

| 90 | Product parameters calculation | 0.80 | 0.00 | 25.35 | 0.00 |

| 100 | Product hazard identification | 0.00 | 25.35 | 0.00 | |

| 110 | Product price calculating | 3.22 | 25.35 | 81.67 | |

| 120 | Creating documentation | 62.33 | 21.95 | 1368.22 | |

| 130 | Ordering samples | 1.00 | 2.58 | 21.95 | 56.58 |

| 140 | Product laboratory testing | 0.50 | 374.67 | 21.95 | 8223.93 |

| 150 | Internal validation | 0.50 | 600.89 | 21.95 | 13,189.51 |

| 160 | External validation | 0.75 | 23.47 | 21.95 | 515.09 |

| Total product development costs: | 1157.79 | 25,716.45 | |||

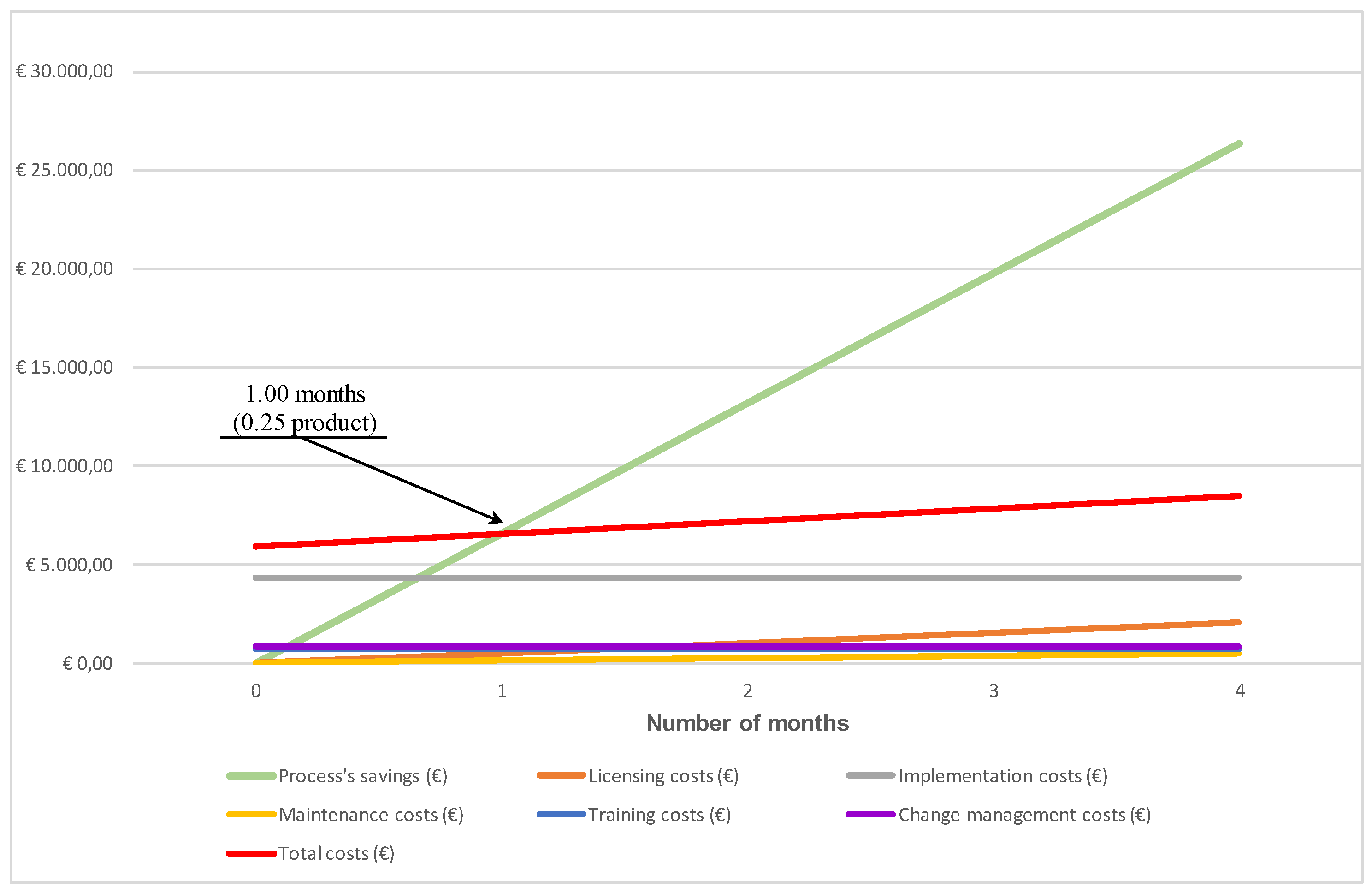

| The Cost Structure | At the Beginning | After 1 Month | After 2 Month | After 3 Month | After 4 Month |

|---|---|---|---|---|---|

| Licensing costs (€) | 0.00 | 514.00 | 1028.00 | 1542.00 | 2056.00 |

| Implementation costs (€) | 4343.51 | 4343.51 | 4343.51 | 4343.51 | 4343.51 |

| Maintenance costs (€) | 0.00 | 129.24 | 258.47 | 387.71 | 516.95 |

| Training costs (€) | 726.40 | 726.40 | 726.40 | 726.40 | 726.40 |

| Change management costs (€) | 856.74 | 856.74 | 856.74 | 856.74 | 856.74 |

| Total costs (€) | 5926.65 | 6569.88 | 7213.12 | 7856.36 | 8499.59 |

| Process’s savings (€) | 0.00 | 6584.35 | 13,168.70 | 19,753.05 | 26,337.41 |

| Input Parameters for Calculator | Value |

|---|---|

| The number of annually developed products (#): | 3 |

| The average labor cost of employees in the process (€/h): | 24.21 |

| The selected type of license: | Pro |

| The number of additional licenses (#): | 0 |

| The number of prepared safety data sheets (#): | 251–500 |

| The number of hazardous ingredients used (#): | 200 |

| The decision for data transfer: | No |

| The number of ingredients in the database (#): | 300 |

| The number of formulations in the database (#): | 100 |

| The number of ingredients input by the expert (#): | 0 |

| The number of formulations input by the expert (#): | 0 |

| Labor cost—expert (€/h): | 70.00 |

| The number of training preparation’s hours (h): | 3 |

| The number of training hours (h): | 3 |

| The number of knowledge repetition’s hours (h): | 3 |

| Percentage of digital transformation total costs (%): | 15 |

| The Cost Structure | At the Beginning | After 1 Month | After 2 Month | After 3 Month | After 4 Month |

|---|---|---|---|---|---|

| Process’s savings (€) | 0.00 | 6584.35 | 13,168.70 | 19,753.05 | 26,337.41 |

| Licensing costs (€) | 0.00 | 514.00 | 1028.00 | 1542.00 | 2056.00 |

| Implementation costs (€) | 4343.51 | 4343.51 | 4343.51 | 4343.51 | 4343.51 |

| Maintenance costs (€) | 0.00 | 129.24 | 258.47 | 387.71 | 516.95 |

| Training costs (€) | 726.40 | 726.40 | 726.40 | 726.40 | 726.40 |

| Change management costs (€) | 856.74 | 856.74 | 856.74 | 856.74 | 856.74 |

| Total costs (€) | 5926.65 | 6569.88 | 7213.12 | 7856.36 | 8499.59 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kern, T.; Krhač Andrašec, E.; Urh, B.; Senegačnik, M. Digital Transformation Reduces Costs of the Paints and Coatings Development Process. Coatings 2020, 10, 703. https://doi.org/10.3390/coatings10070703

Kern T, Krhač Andrašec E, Urh B, Senegačnik M. Digital Transformation Reduces Costs of the Paints and Coatings Development Process. Coatings. 2020; 10(7):703. https://doi.org/10.3390/coatings10070703

Chicago/Turabian StyleKern, Tomaž, Eva Krhač Andrašec, Benjamin Urh, and Marjan Senegačnik. 2020. "Digital Transformation Reduces Costs of the Paints and Coatings Development Process" Coatings 10, no. 7: 703. https://doi.org/10.3390/coatings10070703

APA StyleKern, T., Krhač Andrašec, E., Urh, B., & Senegačnik, M. (2020). Digital Transformation Reduces Costs of the Paints and Coatings Development Process. Coatings, 10(7), 703. https://doi.org/10.3390/coatings10070703