Bitcoin’s Carbon Footprint Revisited: Proof of Work Mining for Renewable Energy Expansion

Abstract

1. Introduction

2. Background and Context

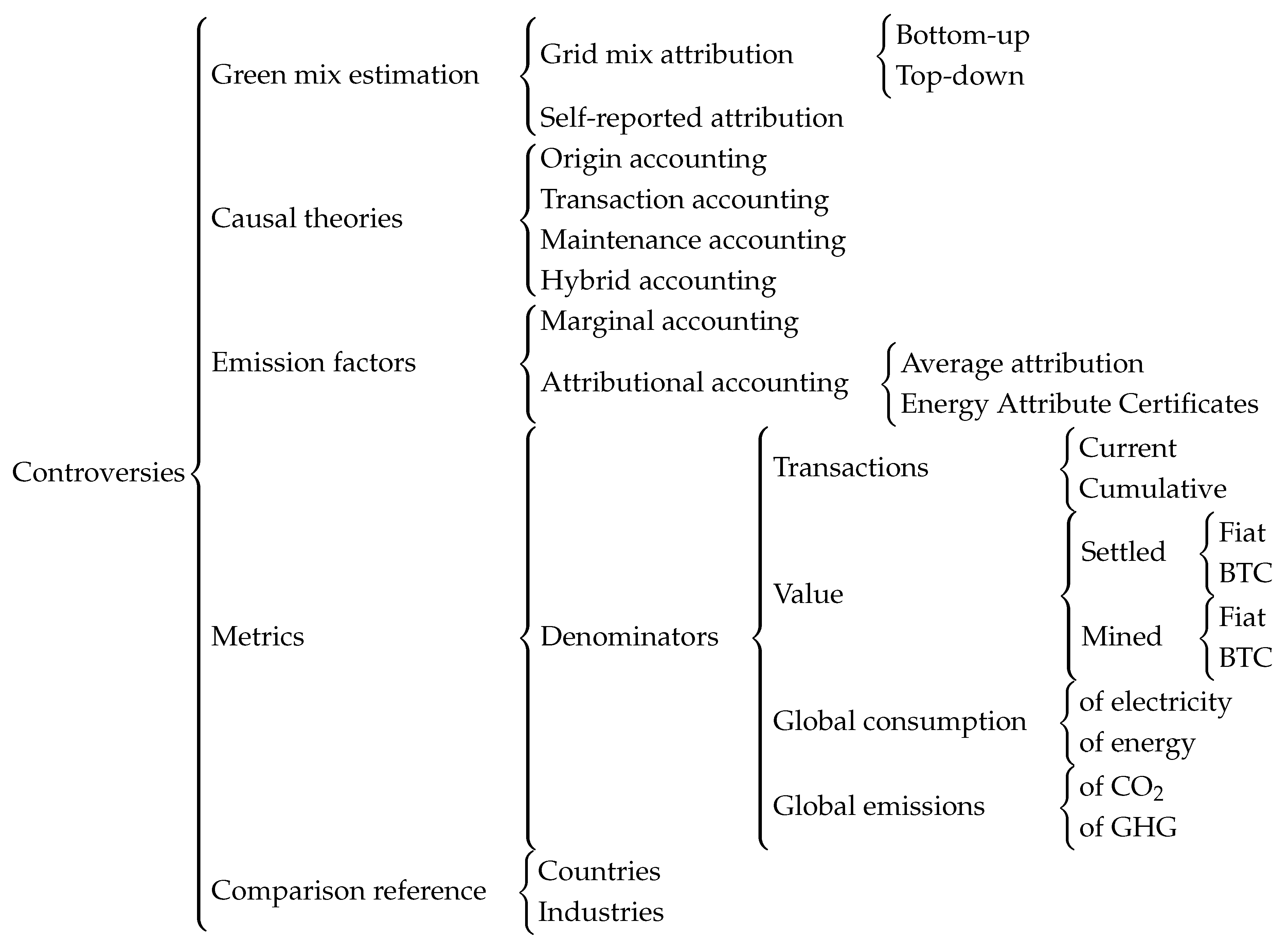

3. Bitcoin’s Environmental Impact

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Approach | Description | Limitations |

|---|---|---|

| Per-transaction basis | “Taking all the emissions (or electricity consumption) in a given time frame and dividing them by the number of transactions in the period, to arrive at a carbon (or electricity consumption) per transaction metric” [22]. A variant of this considers the entire history of past transactions as secured with every new mining event, and not just the coinage of the latest coin. | Usually overlooks L2 transactions, overlooks that Bitcoin demand for transactions is a minor contributor to mining incentives, and thus is incorrectly used to imply that Bitcoin’s throughput can only grow at the cost of more energy consumption [5,16,22,26]. |

| Per-dollar or per-coin settled basis | Considering that L2 solutions allow scaling without increasing energy usage, it focuses on value delivered per kWh [5]. | May incorrectly suggest that additional trading leads to a lower environmental impact. |

| Per-dollar or per-coin mined basis | A novel short-run perspective assuming an “origin accounting” methodology [10]. | Neglects Bitcoin’s decreasing emission rate and presents impractical long-term implications, such as assuming that when the last Bitcoin is mined, Bitcoin’s emissions will be infinite, as well as that approximately 90% of Bitcoin’s climate damages have already occurred and the rest will be spread over an increasingly carbon-neutral energy grid. |

4. Bitcoin Mining and RE

4.1. Limitations of RE

4.2. Distinctive Characteristics of Proof of Work (PoW) Mining

4.3. Applications

4.4. Business Models

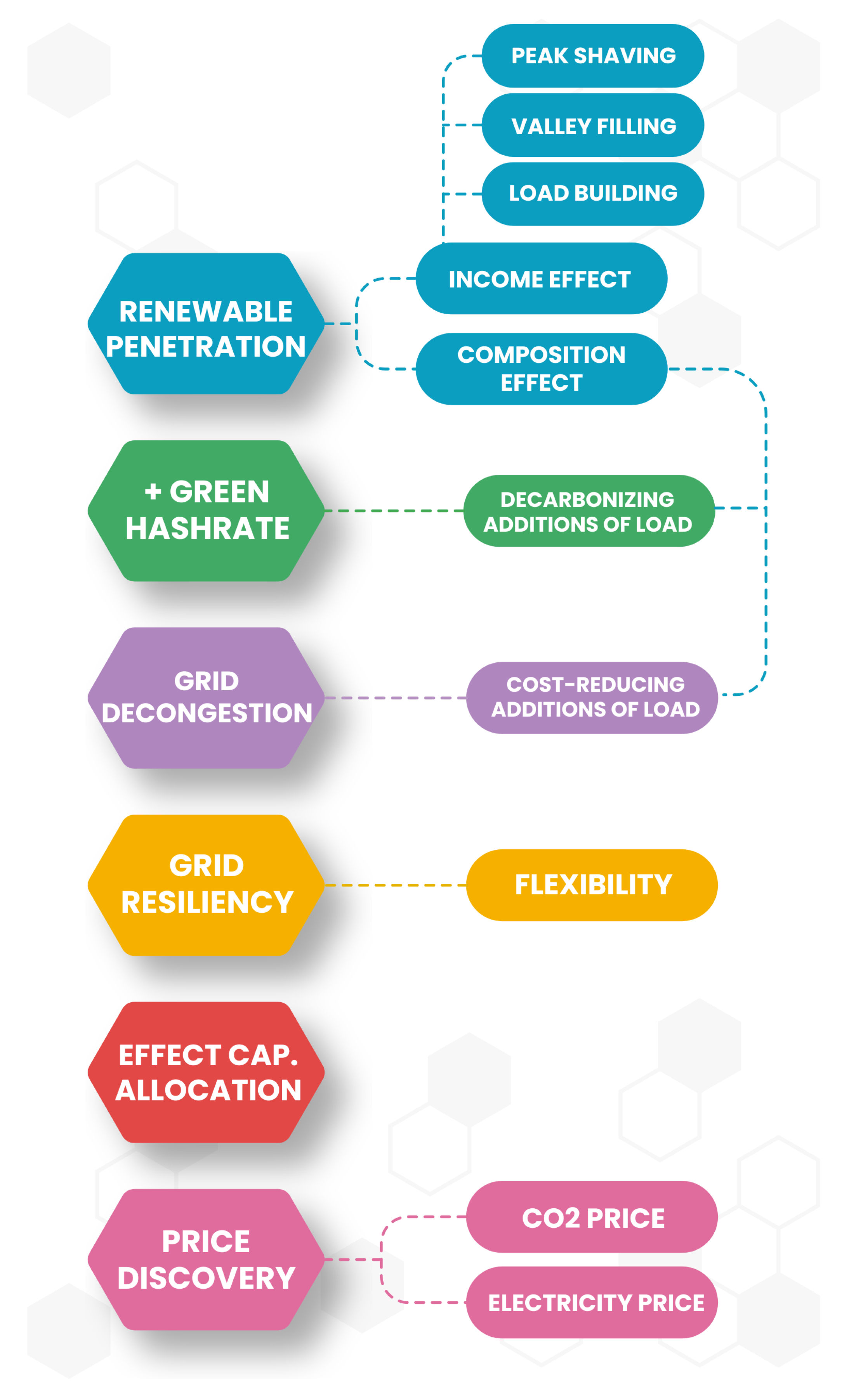

5. Potential Impact of Mining

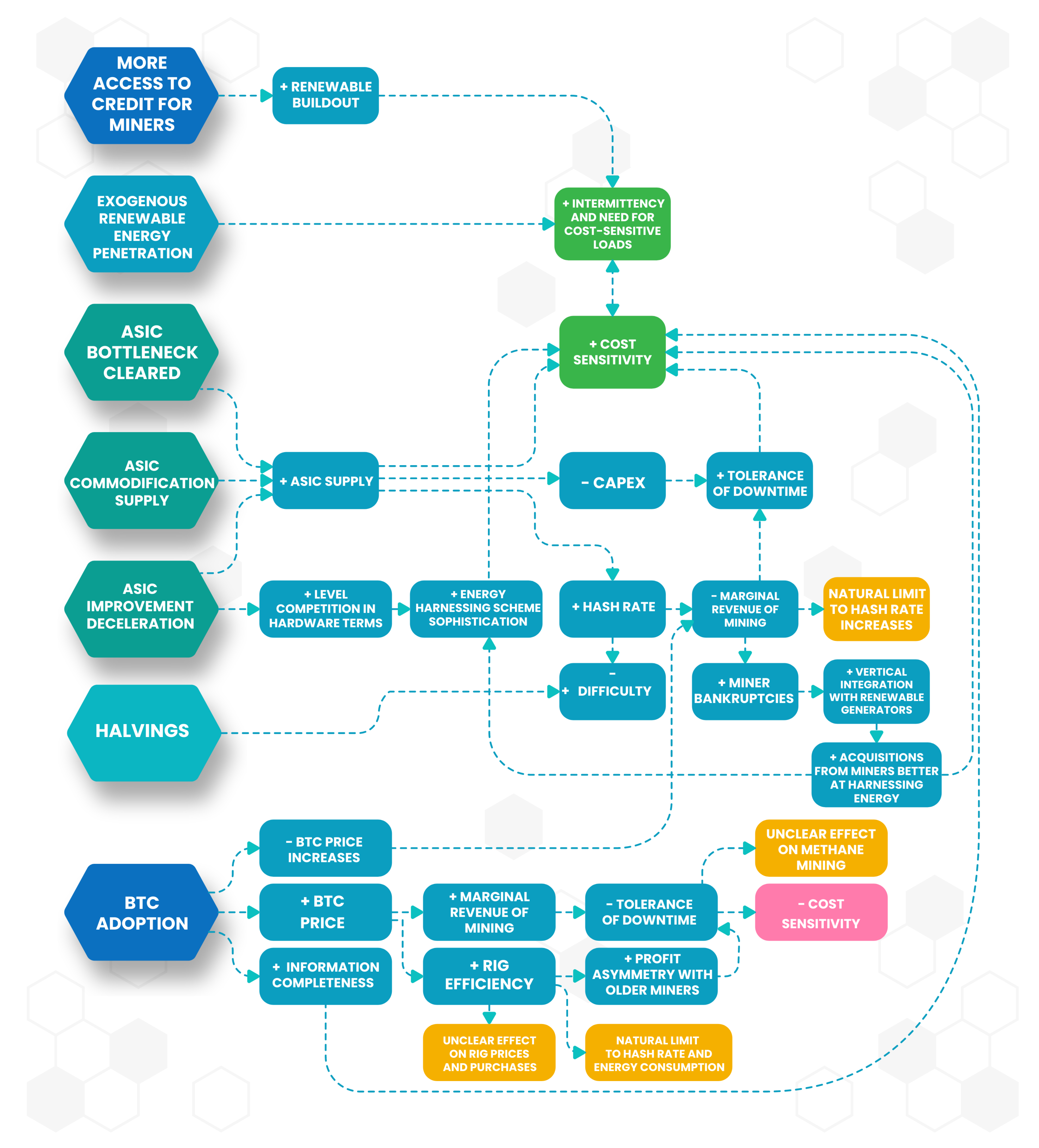

6. Challenging Trends

7. Challenger Technologies: Alternative Load Resources

8. Empirical Support for Synergies between Bitcoin and RE

9. Discussion and Critical Analysis

9.1. Intermittency, Profitability and Increasing Fierceness of Competition

9.2. Bitcoin’s Potential: A Balanced Perspective

10. Limitations and Future Work

11. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Rennie, E. Climate change and the legitimacy of Bitcoin. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Öysti, L. Bitcoin and Energy Consumption. Ph.D. Thesis, Aalto University, Espoo, Finland, 2021. [Google Scholar]

- Carter, N.; Stevens, R. Bitcoin Net Zero; Technical Report; NYDIG: New York, NY, USA, 2021. [Google Scholar]

- Platt, M.; Sedlmeir, J.; Platt, D.; Xu, J.; Tasca, P.; Vadgama, N.; Ibanez, J.I. The Energy Footprint of Blockchain Consensus Mechanisms Beyond Proof-of-Work. In Proceedings of the 2021 21st International Conference on Software Quality, Reliability and Security Companion, QRS-C, Hainan, China, 6–10 December 2021; pp. 1135–1144. [Google Scholar] [CrossRef]

- Ibañez, J.I.; Rua, F. The energy consumption of Proof-of-Stake systems: Replication and expansion. arXiv 2023, arXiv:2302.00627. [Google Scholar] [CrossRef]

- Roeck, M.; Drennen, T. Life cycle assessment of behind-the-meter Bitcoin mining at US power plant. Int. J. Life Cycle Assess. 2022, 27, 355–365. [Google Scholar] [CrossRef]

- Dogan, E.; Majeed, M.T.; Luni, T. Are clean energy and carbon emission allowances caused by bitcoin? A novel time-varying method. J. Clean. Prod. 2022, 347, 131089. [Google Scholar] [CrossRef]

- Rudd, M.A. 100 Important Questions about Bitcoin’s Energy Use and ESG Impacts. Challenges 2022, 14, 1. [Google Scholar] [CrossRef]

- IPCC. Global Warming of 1.5 °C; Technical Report; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2018. [Google Scholar]

- Jones, B.A.; Goodkind, A.L.; Berrens, R.P. Economic estimation of Bitcoin mining’s climate damages demonstrates closer resemblance to digital crude than digital gold. Nature 2022, 12, 14512. [Google Scholar] [CrossRef] [PubMed]

- Köhler, S.; Pizzol, M. Life Cycle Assessment of Bitcoin Mining. Environ. Sci. Technol. 2019, 53, 13598–13606. [Google Scholar] [CrossRef] [PubMed]

- McCook, H. Drivers of Bitcoin Energy Use and Emissions. In Proceedings of the 3rd Workshop on Coordination of Decentralized Finance (CoDecFin) 2022, St. George’s, Grenada, 6 May 2022. [Google Scholar]

- Nikzad, A.; Mehregan, M. Techno-economic, and environmental evaluations of a novel cogeneration system based on solar energy and cryptocurrency mining. Sol. Energy 2022, 232, 409–420. [Google Scholar] [CrossRef]

- Velický, M. Renewable Energy Transition Facilitated by Bitcoin. ACS Sustain. Chem. Eng. 2023, 11, 3160–3169. [Google Scholar] [CrossRef]

- Ghaebi Panah, P.; Bornapour, M.; Cui, X.; Guerrero, J.M. Investment opportunities: Hydrogen production or BTC mining? Int. J. Hydrogen Energy 2022, 47, 5733–5744. [Google Scholar] [CrossRef]

- OSTP. Climate and Energy Implications of Crypto-Assets in the United States; Technical Report; White House Office of Science and Technology Policy: Washington, DC, USA, 2022.

- Read, C.L. (Ed.) Greenwashing in the Bitcoin Industry. In The Bitcoin Dilemma; Palgrave Macmillan: Cham, Switzerland, 2022; pp. 219–229. [Google Scholar] [CrossRef]

- GDF. Re: OSTP, Request for Information on the Climate Implications of Digital Assets; Technical Report; Global Digital Finance: London, UK, 2022. [Google Scholar]

- Gallersdörfer, U.; Klaaßen, L.; Stoll, C. Energy Efficiency and Carbon Footprint of Proof of Stake Blockchain Protocols; Technical Report; Crypto Carbon Ratings Institute: Dingolfing, Germany, 2022. [Google Scholar]

- CCRI. The Merge: Implications on the Electricity Consumption and Carbon Footprint of the Ethereum Network; Technical Report; Crypto Carbon Ratings Institute: Dingolfing, Germany, 2022. [Google Scholar]

- CCRI. Energy Efficiency and Carbon Footprint of the Polygon Blockchain; Technical Report; Crypto Carbon Ratings Institute: Dingolfing, Germany, 2022. [Google Scholar]

- Ibañez, J.I.; Freier, A. Don’t Trust, Verify: Towards a Framework for the Greening of Bitcoin. Soc. Sci. Res. Netw. (SSRN) 2023. [Google Scholar] [CrossRef]

- Gallersdörfer, U.; Klaaßen, L.; Stoll, C. Accounting for carbon emissions caused by cryptocurrency and token systems. arXiv 2021, arXiv:2111.06477. [Google Scholar] [CrossRef]

- South Pole; CCRI. Accounting for Cryptocurrency Climate Impacts; Technical Report; South Pole and Crypto Carbon Ratings Institute: Dingolfing, Germany, 2022. [Google Scholar]

- Stoll, C.; Klaaßen, L.; Gallersdörfer, U. The Carbon Footprint of Bitcoin. Joule 2019, 3, 1647–1661. [Google Scholar] [CrossRef]

- CCRI. Determining the Electricity Consumption and Carbon Footprint of Proof-of-Stake Networks; Technical Report; Crypto Carbon Ratings Institute: Dingolfing, Germany, 2022. [Google Scholar]

- SEC. The Enhancement and Standardization of Climate-Related Disclosures for Investors. SEC Proposed Rule; 2022. Available online: https://www.sec.gov/rules/proposed/2022/33-11042.pdf (accessed on 9 May 2023).

- Mankala, S.; Bansal, U.; Baker, Z. An Innovative Criterion in Evaluating Bitcoin’s Environmental Impact. Soc. Sci. Res. Netw. (SSRN) 2022. [Google Scholar] [CrossRef]

- de Vries, A.; Gallersdörfer, U.; Klaaßen, L.; Stoll, C. The true costs of digital currencies: Exploring impact beyond energy use. One Earth 2021, 4, 786–789. [Google Scholar] [CrossRef]

- Mellerud, J. Bitcoin Mining as a Demand Response in an Electric Power System: A Case Study of the ERCOT-System in Texas. Ph.D. Thesis, NORD University, Bodø, Norway, 2021. [Google Scholar]

- Yazıcı, A.F.; Olcay, A.B.; Arkalı Olcay, G. A framework for maintaining sustainable energy use in Bitcoin mining through switching efficient mining hardware. Technol. Forecast. Soc. Chang. 2023, 190, 122406. [Google Scholar] [CrossRef]

- Guo, X.; Ma, X.; Qian, T.; Mao, W. Optimization allocation method for flexible load as peaking resource. In Proceedings of the China International Conference on Electricity Distribution, CICED, Tianjin, China, 17–19 September 2018; pp. 2800–2804. [Google Scholar] [CrossRef]

- Brook, B.W.; Alonso, A.; Meneley, D.A.; Misak, J.; Blees, T.; van Erp, J.B. Why nuclear energy is sustainable and has to be part of the energy mix. Sustain. Mater. Technol. 2014, 1–2, 8–16. [Google Scholar] [CrossRef]

- Joos, M.; Staffell, I. Short-term integration costs of variable renewable energy: Wind curtailment and balancing in Britain and Germany. Renew. Sustain. Energy Rev. 2018, 86, 45–65. [Google Scholar] [CrossRef]

- Shan, R.; Sun, Y. Bitcoin Mining to Reduce the Renewable Curtailment: A Case Study of Caiso. Soc. Sci. Res. Netw. (SSRN) 2019. [Google Scholar] [CrossRef]

- Frumkin, D. Economics of Bitcoin Mining with Solar Energy. 2021. Available online: https://braiins.com/blog/economics-bitcoin-mining-solar-energy (accessed on 9 May 2023).

- Jenkins, J.D.; Farbes, J.; Jones, R.; Patankar, N.; Schivley, G. Electricity Transmission Is Key to Unlock the Full Potential of the Inflation Reduction Act; REPEAT Project: Princeton, NJ, USA, 2022. [Google Scholar] [CrossRef]

- Menati, A.; Lee, K.; Xie, L. Modeling and Analysis of Utilizing Cryptocurrency Mining for Demand Flexibility in Electric Energy Systems: A Synthetic Texas Grid Case Study. Trans. Energy Mark. Policy Regul. 2023, 1, 1–10. [Google Scholar] [CrossRef]

- Frew, B.; Sergi, B.; Denholm, P.; Cole, W.; Gates, N.; Levie, D.; Margolis, R. The curtailment paradox in the transition to high solar power systems. Joule 2021, 5, 1143–1167. [Google Scholar] [CrossRef]

- Bird, L.; Cochran, J.; Wang, X. Wind and Solar Energy Curtailment: Experience and Practices in the United States; National Renewable Energy Labratory (NREL): Golden, CO, USA, 2014. [CrossRef]

- Braiins. Optimizations for Bitcoin Mining with Intermittent Energy Sources. 2021. Available online: https://braiins.com/blog/optimizations-bitcoin-mining-intermittent-energy (accessed on 9 May 2023).

- Eid, B.; Islam, M.R.; Shah, R.; Nahid, A.A.; Kouzani, A.Z.; Mahmud, M.A. Enhanced profitability of photovoltaic plants by utilizing cryptocurrency-based mining load. IEEE Trans. Appl. Supercond. 2021, 31, 0602105. [Google Scholar] [CrossRef]

- Ramsebner, J.; Haas, R.; Ajanovic, A.; Wietschel, M. The sector coupling concept: A critical review. Wiley Interdiscip. Rev. Energy Environ. 2021, 10, e396. [Google Scholar] [CrossRef]

- Sternberg, A.; Bardow, A. Power-to-What?—Environmental assessment of energy storage systems. Energy Environ. Sci. 2015, 8, 389–400. [Google Scholar] [CrossRef]

- Lund, P.D.; Lindgren, J.; Mikkola, J.; Salpakari, J. Review of energy system flexibility measures to enable high levels of variable renewable electricity. Renew. Sustain. Energy Rev. 2015, 45, 785–807. [Google Scholar] [CrossRef]

- Bastian-Pinto, C.L.; Araujo, F.V.S.; Brandão, L.E.; Gomes, L.L. Hedging renewable energy investments with Bitcoin mining. Renew. Sustain. Energy Rev. 2021, 138, 110520. [Google Scholar] [CrossRef]

- Rhodes, J.D.; Deetjen, T.; Smith, C. Impacts of Large, Flexible Data Center Operations on the Future of ERCOT; Idea Smiths LLC.: Austin, TX, USA, 2021. [Google Scholar]

- Bonaparte, Y. Time horizon and cryptocurrency ownership: Is crypto not speculative? J. Int. Financ. Mark. Inst. Money 2022, 79, 101609. [Google Scholar] [CrossRef]

- Ammous, S.; D’Andrea, F.A.M.C. Hard Money and Time Preference. MISES Interdiscip. J. Philos. Law Econ. 2022, 10. [Google Scholar] [CrossRef]

- Hajipour, E.; Khavari, F.; Hajiaghapour-Moghimi, M.; Azimi Hosseini, K.; Vakilian, M. An economic evaluation framework for cryptocurrency mining operation in microgrids. Int. J. Electr. Power Energy Syst. 2022, 142, 108329. [Google Scholar] [CrossRef]

- Ströhle, P.; Flath, C.M. Local matching of flexible load in smart grids. Eur. J. Oper. Res. 2016, 253, 811–824. [Google Scholar] [CrossRef]

- Wang, L.; Dong, Y.; Liu, N.; Liang, X.; Yu, J.; Dou, X. A Novel Modeling Method for Multi-Regional Flexible Load Aggregation based on Monte Carlo Method. In Proceedings of the 2021 IEEE 11th Annual International Conference on CYBER Technology in Automation, Control, and Intelligent Systems, CYBER, Jiaxing, China, 27–31 July 2021; pp. 632–637. [Google Scholar] [CrossRef]

- Sarquella, M.B. Bitcoin Mining, the Clean Energy Accelerator. Ph.D. Thesis, Universitat Politécnica de Catalunya, Barcelona, Spain, 2022. [Google Scholar]

- Decker, L.A. Bitcoin Mining and Innovations in the Oil Field. Nat. Resour. Environ. 2021, 36, 50–52. [Google Scholar]

- US EPA. Basic Information about Landfill Gas; US Environmental Protection Agency: Washington, DC, USA, 2022.

- Jacobs, T. Innovators Seek To Transform Flaring Into Money and Power. J. Pet. Technol. 2020, 72, 24–29. [Google Scholar] [CrossRef]

- Snytnikov, P.; Potemkin, D. Flare gas monetization and greener hydrogen production via combination with cryptocurrency mining and carbon dioxide capture. iScience 2022, 25, 103769. [Google Scholar] [CrossRef] [PubMed]

- Allen, M.R.; Shine, K.P.; Fuglestvedt, J.S.; Millar, R.J.; Cain, M.; Frame, D.J.; Macey, A.H. A solution to the misrepresentations of CO2-equivalent emissions of short-lived climate pollutants under ambitious mitigation. NPJ Clim. Atmos. Sci. 2018, 1, 1–8. [Google Scholar] [CrossRef]

- Vazquez, J.; Crumbley, D.L. Flared Gas Can Reduce Some Risks in Crypto Mining as Well as Oil and Gas Operations. Risks 2022, 10, 127. [Google Scholar] [CrossRef]

- Denholm, P.; King, J.C.; Kutcher, C.F.; Wilson, P.P. Decarbonizing the electric sector: Combining renewable and nuclear energy using thermal storage. Energy Policy 2012, 44, 301–311. [Google Scholar] [CrossRef]

- Yüksel, S.; Dinçer, H.; Çağlayan, Ç.; Uluer, G.S.; Lisin, A. Bitcoin Mining with Nuclear Energy. In Multidimensional Strategic Outlook on Global Competitive Energy Economics and Finance; Emerald Publishing Ltd.: Bingley, UK, 2022; pp. 165–177. [Google Scholar] [CrossRef]

- Gonzalez, E.S. Investment in Alternative Applications for Next-Generation Nuclear Reactors in the United States. In IAEA Net Zero Challenge. Policy Recommendations for a Transition to Net Zero with Nuclear Power; International Atomic Energy Agency (IAEA): Vienna, Austria, 2021. [Google Scholar]

- Liu, B.; Liao, S.; Cheng, C.; Chen, F.; Li, W. Hydropower curtailment in Yunnan Province, southwestern China: Constraint analysis and suggestions. Renew. Energy 2018, 121, 700–711. [Google Scholar] [CrossRef]

- Malfuzi, A.; Mehr, A.S.; Rosen, M.A.; Alharthi, M.; Kurilova, A.A. Economic viability of bitcoin mining using a renewable-based SOFC power system to supply the electrical power demand. Energy 2020, 203, 117843. [Google Scholar] [CrossRef]

- Kumar, S. Review of geothermal energy as an alternate energy source for Bitcoin mining. J. Econ. Econ. Educ. Res. 2022, 23, 1–12. [Google Scholar]

- Corbet, S.; Lucey, B.; Yarovaya, L. Bitcoin-energy markets interrelationships—New evidence. Resour. Policy 2021, 70, 101916. [Google Scholar] [CrossRef]

- Attia, H.A. Mathematical Formulation of the Demand Side Management (DSM) Problem and its Optimal Solution. In Proceedings of the 14th International Middle East Power Systems Conference (MEPCON’10), Giza, Egypt, 19–21 December 2010; pp. 19–21. [Google Scholar]

- Caballero, R.J.; Hammour, M.L. On the Timing and Efficiency of Creative Destruction. Q. J. Econ. 1996, 111, 805–852. [Google Scholar] [CrossRef]

- Atia, A.A.; Fthenakis, V. Active-salinity-control reverse osmosis desalination as a flexible load resource. Desalination 2019, 468, 114062. [Google Scholar] [CrossRef]

- Liang, Y.; Saner, C.B.; Kwang Lim, B.M.; Hong, K.T.; Chong Lim, J.W.; Hwee Ho, K.J.; Lim, L.Z.; Loh, Y.Y. Sustainable Energy-based Cryptocurrency Mining. In Proceedings of the 11th International Conference on Innovative Smart Grid Technologies-Asia, ISGT-Asia 2022, Singapore, 1–5 November 2022; pp. 789–793. [Google Scholar] [CrossRef]

- Bruno, A.; Weber, P.; Yates, A.J. Can Bitcoin mining increase renewable electricity capacity? Resour. Energy Econ. 2023, 74, 101376. [Google Scholar] [CrossRef]

- Hallinan, K.P.; Hao, L.; Mulford, R.; Bower, L.; Russell, K.; Mitchell, A.; Schroeder, A. Review and Demonstration of the Potential of Bitcoin Mining as a Productive Use of Energy (PUE) to Aid Equitable Investment in Solar Micro- and Mini-Grids Worldwide. Energies 2023, 16, 1200. [Google Scholar] [CrossRef]

- Vega-Marcos, R.; Colmenar-Santos, A.; Mur-Pérez, F.; Pérez-Molina, C.; Rosales-Asensio, E. Study on the economics of wind energy through cryptocurrency. Energy Rep. 2022, 8, 970–979. [Google Scholar] [CrossRef]

- Halaburda, H.; Yermack, D. Bitcoin Mining Meets Wall Street: A Study of Publicly Traded Crypto Mining Companies. Soc. Sci. Res. Netw. (SSRN) 2023. [Google Scholar] [CrossRef]

- Fridgen, G.; Körner, M.F.; Walters, S.; Weibelzahl, M. Not All Doom and Gloom: How Energy-Intensive and Temporally Flexible Data Center Applications May Actually Promote Renewable Energy Sources. Bus. Inf. Syst. Eng. 2021, 63, 243–256. [Google Scholar] [CrossRef]

- Mcdonald, M.T.; Hayibo, K.S.; Hafting, F.; Pearce, J.M. Economics of Open-Source Solar Photovoltaic Powered Cryptocurrency Mining. Ledger 2023, 8. [Google Scholar] [CrossRef]

- Di Febo, E.; Ortolano, A.; Foglia, M.; Leone, M.; Angelini, E. From Bitcoin to carbon allowances: An asymmetric extreme risk spillover. J. Environ. Manag. 2021, 298, 113384. [Google Scholar] [CrossRef]

- Menati, A.; Zheng, X.; Lee, K.; Shi, R.; Du, P.; Singh, C.; Xie, L. High resolution modeling and analysis of cryptocurrency mining’s impact on power grids: Carbon footprint, reliability, and electricity price. Adv. Appl. Energy 2023, 10, 100136. [Google Scholar] [CrossRef]

- IEA. Net Zero by 2050—A Roadmap for the Global Energy Sector; Technical Report; International Energy Agency: Paris, France, 2021. [Google Scholar]

- IEA. Renewables 2022: Analysis and Forecast to 2027; Technical Report; International Energy Agency: Paris, France, 2023. [Google Scholar]

- Google. Moving toward 24 × 7 Carbon-Free Energy at Google Data Centers: Progress and Insights; Technical Report; Google: Mountainview, CA, USA, 2018. [Google Scholar]

- Tol, R.S. Targets for global climate policy: An overview. J. Econ. Dyn. Control 2013, 37, 911–928. [Google Scholar] [CrossRef]

| Strategy | Description | Challenges |

|---|---|---|

| Transmission | Importing and exporting energy from areas with excess supply to areas with excess demand is an effective way to balance electricity markets [30,37]. | Transmission lines have limited capacity, experience congestion, struggle to keep up with electrification trends, suffer from energy losses proportional to their length, and require substantial initial investments [1,3,38]. “Stranded” energy cannot be transmitted. RE generation is often most efficient in remote locations. |

| Capacity Expansion | Investing in excess RE infrastructure to meet demand during low supply periods. | Over-building or over-investing impacts the sector’s profitability, leading to low or negative prices during high supply periods and necessitating government subsidies [30] and curtailment, often intentionally built into capacity expansion projects [39]. |

| Curtailment | When RE production infrastructure is built, excess energy is wasted to avoid issues such as overloading transmission capacity or negative pricing [12,35,40]. | Curtailment has an opportunity cost in terms of unsold energy, decreasing the profitability of VRE generation. Curtailment is projected to increase over time [34,41]. |

| Storage | Storing energy during excess supply and using it during excess demand periods through batteries or other methods, such as pumped hydroelectric storage [14,30,42]. | Batteries and storage solutions are expensive [3,30,42] and have limited capacity, restricting their large-scale effectiveness. |

| Demand-Response Programs | A form of sector coupling [43] and “power-to-X” solutions [15,44,45] where grid operators influence electricity demand patterns to match supply patterns, using flexible load response and compensating energy customers for not consuming electricity during peak events [30,32,38]. | Most loads are not flexible enough for large-scale implementation without significant costs or opportunity losses. |

| Characteristic | Description |

|---|---|

| Flexibility of Load | Bitcoin miners can be activated or deactivated with sub-second responsiveness with little reaction costs (inertia, cooling, warming up). The load can furthermore be “available” in the long term, i.e., it can be reliably providing a stable load due to extended time-horizons and a cash-flow break-even level generally below the ROI break-even level [2,30,47,48,49]. |

| Interruptibility | As mining relies on non-time-sensitive computation, it allows for immediate output switching, and interruptions result in no lost work. This high interruptibility, with the only nuances of difficulty adjustments and mining pool stability reward programs, can support grid stability [2,12,16,30,32,46,50]. |

| Portability/Mobility | Bitcoin mining is location-agnostic, as it requires minimal investment in immovable assets, equipment is easily transportable, there is no need for a grid connection, there are modularised mining solutions, and there is an empirical track record of geographic flexibility under seasonal weather and country-wide bans [1,2,3,12,14,30,38,51,52]. |

| Price Sensitivity | Bitcoin mining is one of the most price-sensitive industries due to its few inputs (mainly electricity) and outputs (primarily BTC, the prices of which are location-agnostic). This results in high OPEX sensitivity, particularly to electricity costs, making miners highly reactive to volatile energy prices. Furthermore, the different (and well known) profitability profiles of various ASIC models offer significant complementarities with multiple energy system niches and patterns [30,35]. |

| Scale Agnosticity | Mining operations can adapt to a wide range of scales, from small home mining to large-scale industrial operations. This scalability makes the industry versatile in its role in the electrical grid [2,6,30]. |

| Consumption-level Granularity | Energy-intensive ASICs with varying break-even points allow for precise adjustments in energy consumption levels, contrasting to binary consumption options, making Bitcoin mining a flexible participant in the energy market [30,41,47,50]. |

| Non-rival Energy Consumption | Mining’s energy consumption does not necessarily result in increased energy generation or emissions. It can utilize otherwise wasted energy (already-generated energy) or harness emissions that would have been produced regardless, implying that miners may not compete directly with other energy consumers [2,12]. |

| Diversification | The distinct and uncorrelated stochastic processes of global Bitcoin prices/hash rates and electricity prices enhance the value of switching outputs, offering a valuable source of income diversification and stability for RE sellers [46,53]. |

| Waste Heat Utilization | The mining process generates significant waste heat, which can potentially be repurposed for various applications such as residential heating or commercial use [7,31]. |

| Salient Characteristics of Bitcoin Mining | ||

|---|---|---|

| Category | Characteristic | Sub-Characteristics |

| Flexibility of Load | Availability of Load | Stability of Load |

| Reliability of Load | ||

| Long Time Horizon | ||

| Interruptibility | Quick Reaction Time | |

| Consumption Granularity | ||

| Price Sensitivity | Bitcoin Price Sensitivity | |

| Cost Sensitivity | ||

| Granularity | ||

| Information Completeness | ||

| Near-Zero Reaction Costs | ||

| Scalability | Scale Agnosticity | Scalability |

| Energy Intensity | ||

| Portability | Location Agnosticity | Movable Goods |

| Geography Independence | ||

| Modularized Solutions | ||

| Unnecessary Grid Connection | ||

| Low Labor Intensity | ||

| Transferability of Output | ||

| Other Characteristics | Non-Rivalrousness | |

| Non-Correlation | ||

| Heat Output | ||

| Category | Details |

|---|---|

| First or Last Resort Buyers | Mining can provide a primary demand source that pays more than selling to the grid, encouraging new plant installations. Bitcoin miners do not replace other consumers in first-resort scenarios caused by a connection queue. It can also provide last resort demand for periods of excess supply [1,46,53]. |

| Uptime | Modern and efficient ASIC miners can run almost 24/7, suited for peak shaving. Older, less efficient miners become profitable during low energy prices only, with “ASIC retirement homes” absorbing excess supply as an ancillary service to stabilize the grid [2,3]. |

| Miner Location | BTM mining reduces transmission costs by placing miners at renewable energy plants, whereas front-of-the-meter mining connects to the grid as a regular consumer [6,30,50]. |

| Pricing Model | A PPA offers fixed prices to miners, facilitating external funding. It can include an option for the seller to switch off the buyer’s ASICs (in exchange for fixed compensation), leading to cost savings during off-peak times. However, regions with high renewable energy use or frequent severe weather may experience above-median PPA prices. PPAs can be used to integrate miners as emergency load resources for regulated ancillary service demand-response programs, as in Texas. Without PPAs (usually front-of-the-meter), a price-responsive model (usually BTM) is generally adopted, where the seller sells to the market if the market price is above the miners break-even point, and to the miner when it is below. This reduces cooling costs and may reduce prices as extreme price events do not affect the miner’s break even [30,41]. |

| Relationship between Miner and RE Producer | Relationships range from mere proximity for efficiency gains to direct contracting for control over operations or vertical integration for full internalization of costs [1,3,6,30,35,46]. |

| Gas Mining Models | Models include “pay for the gas”, where the miner pays for the gas used and keeps the mining proceeds, and “pay for the equipment”, where the miner provides a data center to the gas company, who keeps mining proceeds. Other models include “mobile market hubs” to alleviate pipeline constraints [59]. |

| Operations and Portfolio Greening | Operations can be made greener through renewable energy certificates, guarantees of origin, carbon credits, or offsets. Investors may make their portfolio greener by investing in green hashrate (incentive offsets), purchasing sui generis green Bitcoin attributes. More controversial options include colored coin proposals to trace sustainably mined Bitcoin, which may break fungibility [3,7,15,17,22,35,66]. |

| Technology | Potential for Decarbonization | Limitations |

|---|---|---|

| Water Desalination | Flexible and interruptible; can use nonrival energy sources; there are proposals for Bitcoin mining and water desalination as complementary infrastructures [69]. | Less portable due to infrastructure requirements (tanks, pumping) [69]. |

| Green Hydrogen and Synthetic Methane | Flexible and interruptible; could potentially use nonrival energy sources [15,45,57]. | Electrolysis can be more expensive (e.g., requires storage infrastructure) and risky than mining; less flexible and less portable output; the business model is not battle-tested; a hydrogen economy would entail an energy consumption so large that curtailed energy could not meet it but in a fraction [3,12,15,30,54]. |

| CO2 Removal | Potentially flexible and interruptible; could use nonrival energy sources. | Profitability is uncertain; public good subject to the tragedy of the commons without significant subsidies. |

| Batteries | Can solve part of the daily intermittency problem by balancing load; are flexible and interruptible; their price is expected to continue falling; may complement Bitcoin mining in the “right mix” [2,3,33,35,42]. | Expensive and lower ROI in large scales due to physical limitations to the ability to store energy without dissipation; offer no additional profit other than flexibility itself; offer a smaller energy sink [2,30,33,42]. |

| Other Flexible Data Centers | Other forms of non-time sensitive computation can have a net decarbonizing effect; can increase grid resiliency [14]. | Inferior to cryptocurrency mining facilities in terms of flexibility and efficiency; although there are leaders in the area, many players are lagging behind [38,47]. |

| Other Load Resources (aluminum smelters, sector coupling, Power-to-X solutions, demand-response programs, load shedding, etc.) | Can provide alternative forms of load balancing [14,15,30]. | Power-to-X solutions require “a meaningful probability of occurrence to make it economically viable” [15] (p. 5734); inferior to cryptocurrency mining facilities in terms of flexibility and efficiency [14]. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ibañez, J.I.; Freier, A. Bitcoin’s Carbon Footprint Revisited: Proof of Work Mining for Renewable Energy Expansion. Challenges 2023, 14, 35. https://doi.org/10.3390/challe14030035

Ibañez JI, Freier A. Bitcoin’s Carbon Footprint Revisited: Proof of Work Mining for Renewable Energy Expansion. Challenges. 2023; 14(3):35. https://doi.org/10.3390/challe14030035

Chicago/Turabian StyleIbañez, Juan Ignacio, and Alexander Freier. 2023. "Bitcoin’s Carbon Footprint Revisited: Proof of Work Mining for Renewable Energy Expansion" Challenges 14, no. 3: 35. https://doi.org/10.3390/challe14030035

APA StyleIbañez, J. I., & Freier, A. (2023). Bitcoin’s Carbon Footprint Revisited: Proof of Work Mining for Renewable Energy Expansion. Challenges, 14(3), 35. https://doi.org/10.3390/challe14030035