1. Introduction

Ship navigation data, which includes the location of the vessel, the docking time, vessel types, etc. provides huge information to researchers. The wide application of Automatic Identification System (AIS) makes the research on the ship navigation information come true. AIS is an international maritime security communication system that uses ship tracking equipment to monitor the activities of cargo ships worldwide. The information recorded by AIS includes ship position, speed, course, type and name, etc. Although the original intention of using AIS is to strengthen the personal safety at sea, improve the safety and efficiency of navigation, and protect the marine environment, the valuable information provided by AIS is now successfully used in various fields. For example, Moore, et al. [

1] explored ship traffic variability of California; Arslanalp, et al. [

2] used this raw data information to predict trade flows; Cerdeiro and Komaromi [

3] applied this new big data source to obtain the top 50 routes in terms of non-commodity import forecasts for port performance analysis; and Verschuur, et al. [

4] used it as an open-source tool to assess the disruption time and resilience of the ports and to derive vulnerability curves for US ports. In addition, it has also been applied to the areas of fisheries and marine CO

2 emission monitoring. Therefore, mining AIS data is a promising research direction.

With the rapid process of globalization, maritime transportation is continuously the main mode of international trade transportation. According to the latest review of maritime transport [

5], international seaborne trade is expected to grow by 4.3% in 2021 as commodity trade and global output continue to recover. Furthermore, the average ratio of international seaborne trade to the global gross domestic product (GDP) has remained in the range of 1% to 2% over the past 20 years, with a compound annual growth rate of 2.9% for seaborne trade, which indicates that maritime trade has undergone a period of prosperity.

As an important component of international trade, crude oil trade has always accounted for a significant share in global energy trade market. According to BP Statistical Review of World Energy [

6], the crude oil trade volume around the world in 2021 is 65,061 kb/d and the total consumption reaches 91,078 kb/d, which means the crude oil international trade accounts for about 71.43% of the total oil consumption. Among them, the Middle East as well as Russia and the CIS countries are the main crude oil exporters. As crude oil is still one of the most essential energy sources in the world so far, international crude oil seaborne transportation is always accepted to ensure a sufficient supply of basic industrial production materials for countries throughout the world, with the characteristics of large capacity and long transportation. Therefore, a market of specialized vessels designed for specific routes has been formed, which greatly enriches the international economic cooperation in crude oil resources.

The measurement of the factors influencing the crude oil market and the seaborne transportation market has been a hot topic in global maritime research. In the existing literature, Poulakidas and Joutz [

7] suggested that the demand for tanker transportation is a derivative of the demand for crude oil, and thus there is a close economic relationship between the crude oil prices and the freight rates in the tanker shipping market. In the background of globalization, crude oil is one of the most widely traded bulk energy commodities worldwide and its price is often used as a leading indicator to predict price movements in other commodity markets (e.g., metals, ores, and agriculture) and maritime transportation markets [

8]. Mou, et al. [

9] empirically found that the export cargo flows are stronger than that of the import cargo flows. Hence, with cyclicality, volatility and fluctuations in crude oil prices, crude oil trade can affect tanker freight rates and transportation costs of crude oil and refined products where they are produced or consumed [

10]. Thus, it may directly affect the revenue and cash flow of tanker owners and is significant for further estimating the profitability of the tanker industry and future investment decisions.

The rapid development of global crude oil trade impacts lots of aspects in the tanker transportation industry. Moreover, since the volatility of crude oil prices is more closely related to global economic activities, which makes the level of freight rates no longer the only measurement of the tanker transportation market. Hence, in recent years, researches on the relationship between supply and demand for tanker shipping services by analyzing port operations have also intensified. This paper focuses on the characteristics of crude oil seaborne transportation market, with the help of AIS data. We construct a monthly panel data set to study the influence of crude oil price fluctuation on tankers’ port-calls, the docking time, the operating capacity and whether there is a new tanker beginning to transport the oil. The change of those indicators under the influence of oil price is important for port managers to make operating plans which may improve the economic efficiency of the ports.

We attempt to explore the impact of crude oil market price fluctuations on the tankers’ port-call features and clarify the transmission mechanism and the relationship between them. By conducting this empirical study with panel data, we also hope to provide ideas and directions for shipping companies and governmental authorities on the current situation and future expectations of the market and the tanker shipping industry, formulating strategies and energy policies in depth. The contributions of this research are three folds. Firstly, by mining the information in AIS data, this paper obtains the panel data of monthly tankers’ port-call data from January 2010 to December 2020, and creatively uses panel data to analyze the influence of crude oil price on tankers’ port-call features. Panel data can control the heterogeneity of research variables in time and space, and can avoid the problem of multicollinearity. Secondly, with the help of AIS data, this paper obtains many variables that reflect the tankers’ port-call features, such as port-call frequency, average docking time, etc. Combined with the analysis based on panel data, this paper provides an empirical basis for the role of crude oil price fluctuations on tankers’ shipping activities, specifically reflecting the direction and degree of the crude oil prices’ influences on the features of tankers’ port-call. This paper supplements the existing literature from multiple perspectives. Finally, the research conclusion can help oil shipping enterprises to make transportation capacity plans in advance, and can also help port enterprises to arrange operators in advance.

The remaining sections are organized as follows:

Section 2 reviews previous studies on the tanker transportation market and the fluctuation of future oil price;

Section 3 mainly introduces the data and the methods;

Section 4 introduces the empirical results;

Section 5 presents the robust test; and finally,

Section 6 summarizes this paper.

3. Data and Methods

3.1. Data Source

Based on the latest available OPEC [

34] statistical annual reports, this study selected 26 countries and regions, 13 of which are from OPEC (Organization of the Petroleum Exporting Countries) member countries, including Algeria, Angola, Congo, Equatorial Guinea, Gabon, Iran, Iraq, Kuwait, Libya, Nigeria, Saudi Arabia, United Arab Emirates and Venezuela. Then the remaining 13 countries are major crude oil exporting non-OPEC member countries, which involves Brazil, Canada, Colombia, Ecuador, Indonesia, Malaysia, Mexico, Norway, Oman, Qatar, Russia, Sudan and Vietnam.

In this paper, we select the monthly data from January 2010 to December 2020 for the oil loading ports located in the aforementioned countries which involve a total sample of 545 ports. The total gross tonnage of the tankers entering and exiting the first 20 largest oil exporting countries in 2020 are shown in

Figure 1. According to recent oil export data, oil exporters are mainly distributed in six regions, that is the Middle East, Russia and CIS countries, West Africa, North America, South America and a small number of Asian and Oceanian countries. In those regions, oil tanker’ loading operations are relatively frequent.

International oil prices experienced ups and downs shocks between 2010 and 2020. In order to explore the changes in crude oil transportation trade before and after the rise and fall of oil prices, we collect monthly tanker AIS data from January 2010 to December 2020, including the IMO number (IMO number refers to a unique identification number that is assigned to the marine vessel in accordance with the requirements of the International Maritime Organization (International Maritime Organization, IMO)). of the tanker, the tanker’s gross tonnage, arrival and departure time, the port the tanker calls, the latitude and longitude time zone of the port, etc. After filtering and identifying the required data, we retrieve the ship’s entry and exit port records.

The data applied in this study is downloaded from Lloyd’s Register. It focuses on ship’s activity near targeted ports, especially ships entering and leaving from port vantage points [

2]. Based on the aforementioned information recorded by AIS, we acquire how many times the tankers stop at one port per month (monthly frequency of tankers’ port-calls at one port), the average docking time of the tankers, how many different tankers stop at one port (the number of operating tankers), and the total gross tonnage of the tankers (This paper counts different tankers calling at one port repeatedly. To be specific, if a tanker calls at one port twice in one month, its gross tonnage will be added into the total gross tonnage twice in this month.) calling at the port. From AIS data, we obtain 60,540 different tanker observations, which means there are 60,540 different tankers shipping oil in these ten years totally. The numbers vividly present the distribution of crude oil trade among both OPEC and Non-OPEC member countries. We also acquire crude oil futures prices and other macro data from Clarkson, OPEC and EIA (The U.S. Energy Information Administration).

3.2. Descriptive Analysis

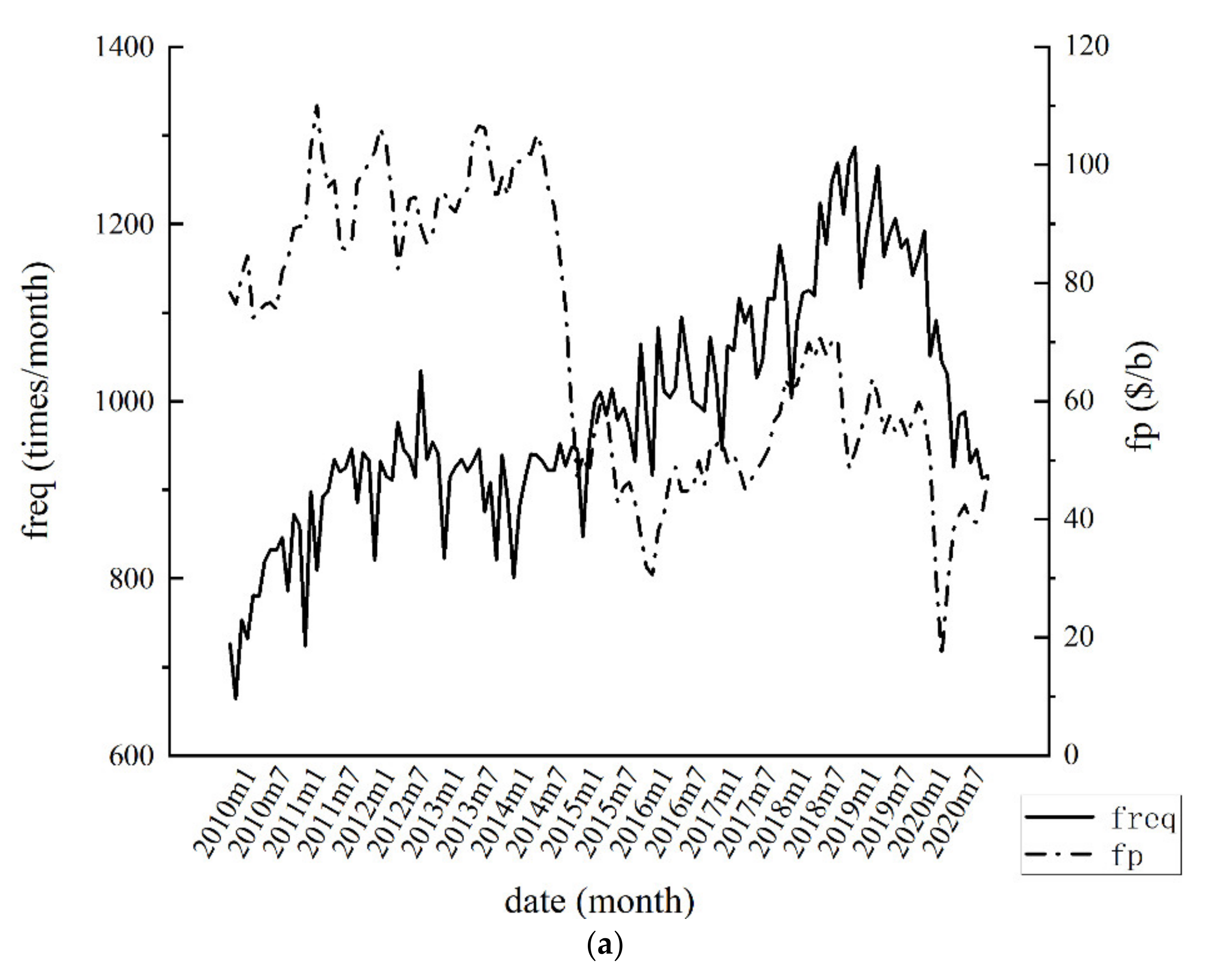

In this paper, we obtain 390,628 real-time records of tankers’ movements based on the major crude oil trade ports around the world with the help of AIS.

Figure 2 illustrates the number of port-calls (indicated by the horizontal axis), the tanker’s average docking time (indicated by the vertical axis) and the monthly average total gross tonnage of the tankers stopping at the 545 ports. The total gross tonnage is shown by circle. It can be found that generally speaking if the total tonnage of all tankers stopped at a port is larger, the number of tankers stopped at the port is also larger, and the average berthing time of the tankers is shorter. This is absolutely in line with common sense. In the right part of

Figure 2, the circles indicate the busy oil loading ports. In every month these ports accommodate many oil tankers, as a result, the loading and unloading efficiency is also very high.

In order to construct the panel data set, we focus on the statistical data associated with different ports. We count the port call numbers and sum up the different variables based on the IMO number of ships, such as the tankers’ port-call numbers (freq), the average docking time (duration) and the total gross tonnage (GT) of the tankers, respectively, to reflect the tankers port-call features in different angles. Monthly crude oil futures price (fp) released by EIA is the core independent variable.

Then considering that the same ship may repeatedly load oil at one port in one month, we use the number of different tankers calling at a port (num) to generate a dummy variable new_add, which indicates whether there is a new tanker stopping at the port to load oil. To be specific, if there are four different tankers stopping at a port in January and there are five different tankers stopping at the port in February, new_add equals 1. In other situations, new_add equals 0. Based on this variable, we apply a logit model to check whether oil price can affect the mobilization of idle tankers’ shipping capacity.

To control other factors influenced by the tankers’ shipping features, three aspects are considered: the economic growth, crude oil reserve and tanker’s freight rate.

In general, a country’s crude oil reserves and the local oil supply always reflect the degree of dependence on foreign supplies and capability against oil risks in the country or certain region. Behrouzifar, et al. [

35] illustrated that the increase in OPEC oil reserves has an impact on the crude oil production and supply behavior of member countries, propelling the shipping market demand to respond. Furthermore, large oil fields and crude oil reserves are essential for domestic oil production in either country producers or private producers around the world [

13,

36,

37]. Thus, crude oil reserve is one of the factors that may determine whether a tanker loads oil frequently at a crude oil exporting country.

Next, for the world’s major crude oil exporters, it has been primarily proven that the crude oil export sector can make a significant positive contribution to their economic growth [

38,

39]. The economic growth of a country’s tanker transportation demand is a derivative of crude oil consumption demand [

15,

40], especially in the oil-producing Middle East [

41]. Hence, we also select the net export volume of crude oil trade to measure the effect of the country’s economic development and trade status on the tanker transportation market.

Finally, it has been proven by many literatures that there is a correlation between crude oil prices and tanker’s freight rate [

7,

8,

40,

42], this paper controls the transportation cost. To be specific, this paper uses the average of Baltic Clean Tanker Index (BCTI) and Baltic Dirty Tanker Index (BDTI) to measure the transportation cost.

As a consequence, all these influencing factors mentioned above may ultimately affect the transportation trajectory and tankers’ port-call features through the supply and demand side. The national crude oil reserves (reserve), the volume of oil trade (nx) and the mean value of Baltic Clean Tanker Index and Baltic Dirty Tanker Index (BTI) are selected as control variables in the following regression. The nomenclature is shown as

Table 1.

Table 2 shows the descriptive information for the aforementioned variables in the research period. It can be seen that the highest crude oil futures price reaches 110.04 and the lowest is 16.70, with a mean of 69.65 and a standard deviation of 22.88, indicating that oil prices fluctuate widely during the study period. Similarly, there are also large volatilities in other variables. In addition, the dummy variable new-add statistic description reflects that 36% of the sample port has mobilized new tankers to help loading and transportation operations compared to the previous period. As also expected, the hypothesis of normality is rejected for all variables according to the Jarque-Bera statistical tests, since the statical value are huge and the

p-values are very small.

Figure 3a–c reflects the correlation among monthly international crude oil futures price (fp) and the monthly port-call numbers of all the ports (freq), average docking time of all the tankers every month (duration) and total gross tonnage of the tankers (GT), respectively. According to the analysis of the monthly data of AIS from 2010 to 2020, it is found that the relative fluctuation of oil price will have a roughly negative feedback effect on the freq and GT, but an approximately positive feedback effect duration.

3.3. Research Design

Through tidying the data, we achieve a panel data set. The panel data linear regression model is selected for the following advantages. Firstly, compared with cross-sectional model or time series model, panel data model can control individual heterogeneity better and deal with some unobservable individual effects, which makes the results more convincing. Secondly, it contains more information, which reduces the possibility of collinearity among variables and increases the degree of freedom and the validity of estimation [

43]. Thirdly, because of different countries and regions, the causal analysis may contain a set of interfering factors such as economic growth and national crude oil reserves, so compared to other models, the panel model can estimate the effect of crude oil futures prices on different selected dependent variables by controlling other variables on the premise of individual port characteristics fixed [

44].

To deal with the panel data, individual fixed-effect model is one of the most common static ones to choose. As it is unavoidable for different tanker ports in various countries and regions to have individual heterogeneity, such as geographic situation, country policy and historic culture. To control all these unobservable factors on the regression results and identify the overall effect more accurately, a panel fixed-effect model is applied by conducting each port as an individual at the same time dimension on the ordinary least squares (OLS) regression. Next, we can analyze the individual effect on the selected tanker port. In recent years, there have been many articles applying panel fixed-effect model to the field of port economy. The representative literatures include Shan, Yu and Lee [

44], Bottasso, et al. [

45], An, et al. [

46], and Xu, et al. [

47].

However, when it comes to explaining a qualitative event concerning binary dependent variables, logit model is usually used instead of traditionally linear probability model, as it is estimated by maximum likelihood (MLE), not OLS [

48]. The theory has been applied to analyze the choices made in the transportation field for many years, initially for passengers, then for goods and recently port choices [

49,

50,

51]. Therefore, combined with the advantages of the panel data mentioned above, we attempt to further explore the possibility that more different tankers are calling at a port when crude oil futures price changes.

3.4. Empirical Models

The disruptions and shocks in supply side in crude oil exporting countries have an impact on price fluctuations and instability in crude oil and its product markets [

40]. Considering the important role played by ports in the crude oil trade in the docking and loading chain, Peng, et al. [

52] proposed to use tanker’s sailing activity to study global crude oil trade, which solves the problem from a more microscopic perspective.

Based on existing literatures, this paper first uses linear regression to find the relationship between crude oil futures prices and tankers’ port-call features reflected by three aspects-the port-call numbers, the average docking time in ports and total gross tonnage of the docking tankers. Furthermore, this paper uses logit regression to explore whether oil price can affect the mobilization of idle tankers’ shipping capacity.

3.4.1. Individual Fixed-Effect Model

The models used in this research are presented as follows:

where

freqit,

durationit,

GTit, respectively, denote the monthly frequency of port-call’s, average docking time and gross tonnage of the docking tankers at port

i in month

t;

fpit denotes crude oil futures prices at month

t; Control

it is the vector of three control variables, i.e., net export of crude oil by country (nx), proven crude oil reserves by country (reserve) and tanker freight rates (BTI) for port

i in month

t. Here ln denotes the natural logarithmic forms of these variables, in use of obtaining a constant elasticity model and ensuring that the estimated coefficients are robust to the result [

48].

β1,

β2,

β3 are the parameters to be estimated, which capture the average effect of the oil price fluctuation on respective dependent variables.

α1,

α2,

α3 are the regression coefficients of the intercept terms;

c1,

c2,

c3 are the regression coefficients of control variables;

μi1,

μi2,

μi3 indicate the port fixed effects;

εit1,

εit2,

εit3 are the randomized error terms.

Since ports in different countries can be affected by different factors, there can be omitted variables that do not change over time. Therefore, we choose a fixed-effect model for regression analysis.

3.4.2. Logit Regression Model

Logit regression here is applied and the cumulative standard Logit distribution function is constructed as follows:

where

;

pi,t is the probability that idle tankers begin to transport crude oil and ln denotes the natural logarithm. γ

1 captures the effect of the fluctuation of crude oil price on the probability of a new tanker stopping at a port.

6. Conclusions

With the help of AIS data, this paper conducts a monthly panel data of tanker ports located in the world’s major crude oil exporting countries from 2010 to 2020. To measure tankers’ port-call features from all around, we innovatively select four variables to verify that crude oil market price fluctuations can have a significant impact on tankers’ port-call features, which is consistent with the statistical data published by Drewry Shipping Consultants Limited. The conclusions of the paper can be drawn as follows: (1) The tankers’ monthly port-call number is significantly negative related with oil futures prices, i.e., when oil futures prices rise, the frequency of tankers’ loading work and departures decreases accordingly. (2) The average docking time of the tankers is significantly positive correlated with the oil price, i.e., when the oil price increases, the average docking time of a single tanker will be extended. It may be resulted from the increasing loading time or waiting time. (3) The total gross tonnage of the tankers docking at the port is significantly negative correlated with the oil price, i.e., when the oil price increases, the volume of tanker exports will be lowered accordingly. (4) The probability of new tankers stopping at a port also shows significant negative relations with oil prices, as proved by the result that for every 1 % increase in crude oil futures prices, the probability of ports adding new tankers decreases by 11.4%. To sum up, we can draw a conclusion that price changes in crude oil price can drive the demand changes for crude oil seaborne transportation.

According to the results of this study, the increase of oil price will inevitably lead to a structural contradiction between the demand for oil seaborne transportation capacity and high cost of international tanker transportation. When oil price increases, the profit of tanker owners is at a low level, directly causing a decline in supply for shipping and an extension of docking time. Knowing this, the port managers will increase operators when the oil price drops or is low, because port-call numbers increase and docking time decreases. Likewise, they will reduce operators when the oil price is high because port-call numbers decrease and docking time increases. The shipowner is prepared to cope with the reduction of demand when the oil price is high, and to improve the supply of the transportation capacity when the oil price is low. Therefore, the empirical results of this paper can provide ideas and directions for delving into the global crude oil seaborne transportation market and formulate strategies and energy policies for expectations of future sustainable development as well.

{kind=link}

{kind=link}

{kind=link}

{kind=link}