What Is the Inpatient Cost of Hip Replacement? A Time-Driven Activity Based Costing Pilot Study in an Italian Public Hospital

, , ,

, , ,  , and

, and

Abstract

1. Introduction

2. Materials and Methods

2.1. Study Design

2.2. Study Participants

2.3. Measurement

2.4. Costs Analysis of Hip Arthroplasty

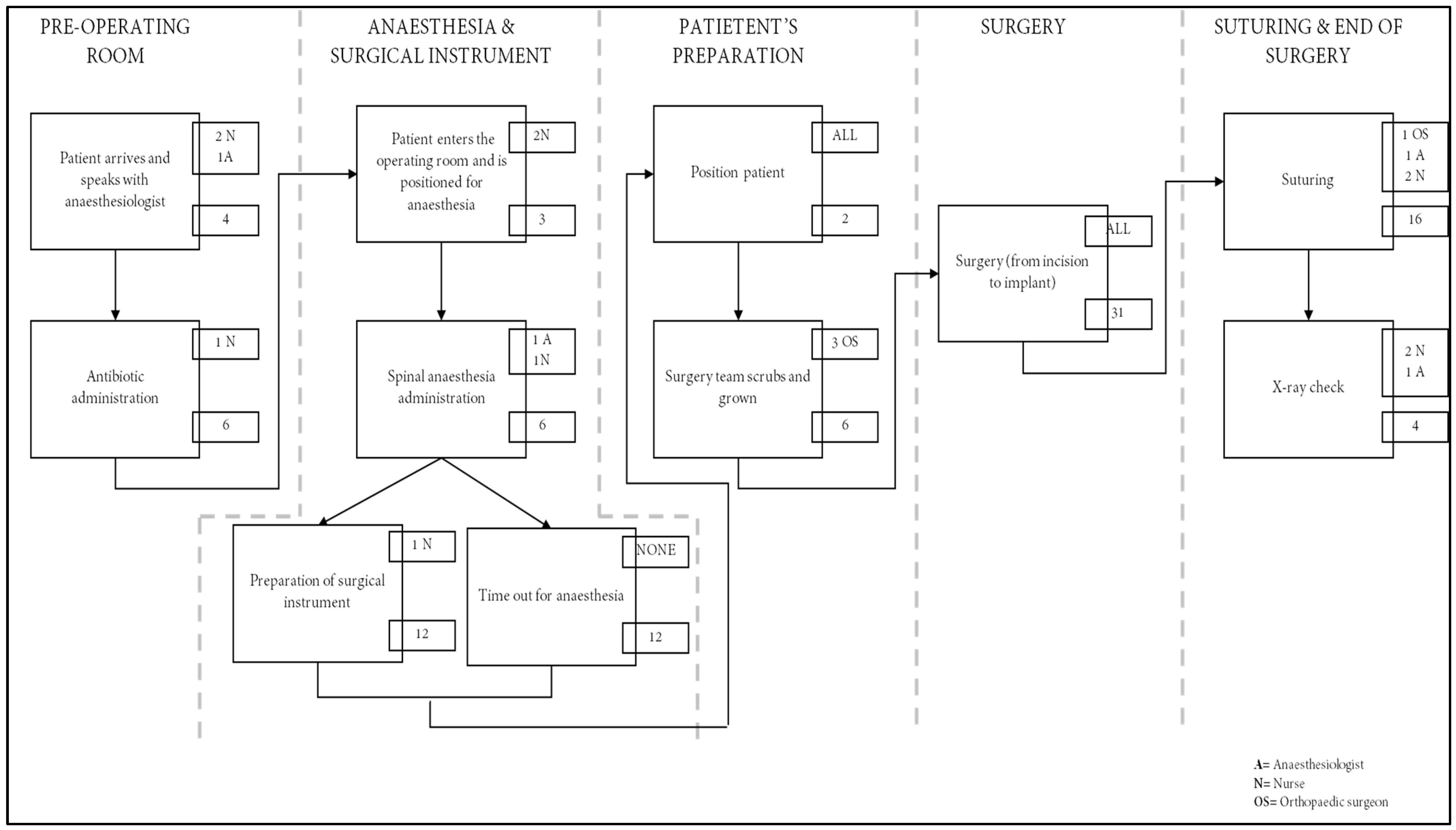

3. Results

- -

- Three orthopaedic surgeons (one involved for 55 min and two involved for 39 min);

- -

- One anaesthesiologist (involved all the time);

- -

- One nurse dedicated to the anaesthesiologist (involved all the time);

- -

- One surgical nurse (involved 85 min);

- -

- One general nurse (involved 85 min).

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

Appendix A

{kind=link}

|

| Unit Cost | Cost by Quantity | |

|---|---|---|

| Pre operating room: | ||

| Cannula | 0.3416 EUR | 0.3416 EUR |

| Betadine | 0.99 EUR | 0.99 EUR |

| Patch (9 mt roll) | 0.28 EUR | 0.005612 EUR |

| Saline solution 0.5 lt | 0.37 EUR | 1.122 EUR |

| Antibiotic: | ||

| 0.87 EUR | 0.869 EUR |

| 0.55 EUR | 0.55 EUR |

| Anti-allergic prophylaxis: | ||

| 3.25 EUR | 3.245 EUR |

| 0.99 EUR | 0.99 EUR |

| Needle | 0.01 EUR | 0.03 EUR |

| ECG Electrodes | 0.10 EUR | 0.2928 EUR |

| Washing: | ||

| 0.38 EUR | 1.891 EUR |

| 0.02 EUR | 0.1952 EUR |

| 0.05 EUR | 0.3416 EUR |

| Anesthesiologist: | ||

| Sterile dressing (3 pack) | 0.46 EUR | 0.9272 EUR |

| Latex gloves | 0.20 EUR | 1.7568 EUR |

| Spinal needle | 0.85 EUR | 0.854 EUR |

| Syringe | 0.02 EUR | 0.0488 EUR |

| Chirocaine | 8.80 EUR | 8.8 EUR |

| Dressing | 0.28 EUR | 0.2806 EUR |

| Surgeons/Nurse: | ||

| Nurse Scrub | 5.25 EUR | 5.246 EUR |

| Surgeons scrubs | 5.25 EUR | 15.738 EUR |

| Hip prosthesis disposable kit | 24.34 EUR | 24.339 EUR |

| Aspirator/Hoses | 0.76 EUR | 0.7564 EUR |

| Electrosurgery equipment | 3.12 EUR | 3.1232 EUR |

| Scalpel blade | 0.06 EUR | 0.122 EUR |

| Disinfection pads (pack of 10) | 0.05 EUR | 0.0976 EUR |

| Oprafol | 8.91 EUR | 8.906 EUR |

| Drainage | 4.39 EUR | 4.392 EUR |

| Silkam 0 | 1.10 EUR | 2.196 EUR |

| Safil1 | 2.81 EUR | 5.612 EUR |

| Vicryl 2 | 1.10 EUR | 2.196 EUR |

| Absorbent dressing. | 0.73 EUR | 0.732 EUR |

| Specific patch (10 mt roll) | 1.71 EUR | 0.03416 EUR |

References

- Veronese, N.; Cereda, E.; Maggi, S.; Luchini, C.; Solmi, M.; Smith, T.; Denkinger, M.; Hurley, M.; Thompson, T.; Manzato, E. Osteoarthritis and Mortality: A Prospective Cohort Study and Systematic Review with Meta-Analysis. Semin. Arthritis Rheum. 2016, 46, 160–167. [Google Scholar] [CrossRef] [PubMed]

- Fidanza, A.; Leonardi, E.; Migliore, E.; Calvisi, V.; Indelli, P.F. Isolation, Cell Culture and Characterization of Autologous Mesenchymal Stem Cells from Adipose Tissue and Bone Marrow Older Donors: An Alternative Approach of Cell Therapy in the Orthopaedics. G. Ital. Di Ortop. E Traumatol. 2022, 48, 82–92. [Google Scholar]

- Ghirardelli, S.; Touloupakis, G.; Antonini, G.; Violante, B.; Fidanza, A.; Indelli, P.F. Debridement, Antibiotic, Pearls, Irrigation and Retention of the Implant and Other Local Strategies on Hip Periprosthetic Joint Infections. Minerva 2022, 73, 409–415. [Google Scholar] [CrossRef]

- Torre, M.; Carrani, E.; Luzi, I.; Ceccarelli, S.; Laricchiuta, P. Registro Italiano ArtroProtesi. Rep. Annu. 2018, 57, 132–133. [Google Scholar]

- Torre, M.; Ceccarelli, S.; Carrani, E. Il Registro Italiano ArtroProtesi: Uno Strumento per Potenziarela Sicurezza Dei Pazienti; Bollettino Epidemiologico Nazionale; ISS Istituto Superiore di Sanità: Rome, Italy, 2019. [Google Scholar]

- OECD. Hip and knee replacement. In Health at a Glance 2021: OECD Indicators; OECD Publishing: Paris, France, 2021. [Google Scholar]

- Ministero della Salute. Rapporto Annuale sull’Attività di Ricovero Ospedaliero (Dati SDO 2019). Available online: https://www.salute.gov.it/portale/documentazione/p6_2_2_1.jsp?lingua=italiano&id=3002 (accessed on 8 April 2022).

- Parisi, T.J.; Konopka, J.F.; Bedair, H.S. What Is the Long-Term Economic Societal Effect of Periprosthetic Infections after THA? A Markov Analysis. Clin. Orthop. Relat. Res. 2017, 475, 1891–1900. [Google Scholar] [CrossRef]

- Ghirardelli, S.; Fidanza, A.; Prati, P.; Iannotti, F.; Indelli, P.F. Debridement, Antibiotic Pearls, and Retention of the Implant in the Treatment of Infected Total Hip Arthroplasty. HIP Int. 2020, 30, 34–41. [Google Scholar] [CrossRef]

- Agyar, E.; Ayten, E.; Mehmet, B.; Murat, U. A Practical Application of Activity Based Costing in an Urology Department. In Proceedings of the 7th Global Conference on Business and Economics, Rome, Italy, 13–14 October 2007. [Google Scholar]

- Kaplan, R.S.; Porter, M.E. How to Solve the Cost Crisis in Health Care. Harv. Bus. Rev. 2011, 89, 46–52. [Google Scholar]

- Keel, G.; Savage, C.; Rafiq, M.; Mazzocato, P. Time-Driven Activity-Based Costing in Health Care: A Systematic Review of the Literature. Health Policy 2017, 121, 755–763. [Google Scholar] [CrossRef]

- Akhavan, S.; Ward, L.; Bozic, K.J. Time-Driven Activity-Based Costing More Accurately Reflects Costs in Arthroplasty Surgery. Clin. Orthop. Relat. Res. 2016, 474, 8–15. [Google Scholar] [CrossRef]

- DiGioia, A.M., III; Greenhouse, P.K.; Giarrusso, M.L.; Kress, J.M. Determining the True Cost to Deliver Total Hip and Knee Arthroplasty over the Full Cycle of Care: Preparing for Bundling and Reference-Based Pricing. J. Arthroplast. 2016, 31, 1–6. [Google Scholar] [CrossRef]

- Palsis, J.A.; Brehmer, T.S.; Pellegrini, V.D.; Drew, J.M.; Sachs, B.L. The Cost of Joint Replacement: Comparing Two Approaches to Evaluating Costs of Total Hip and Knee Arthroplasty. JBJS 2018, 100, 326–333. [Google Scholar] [CrossRef]

- Schettini, I.; Palozzi, G.; Chirico, A. Mapping the Service Process to Enhance Healthcare Cost-Effectiveness: Findings from the Time-Driven Activity-Based Costing Application on Orthopaedic Surgery. In Service Design Practices for Healthcare Innovation: Paradigms, Principles, Prospects; Pfannstiel, M.A., Brehmer, N., Rasche, C., Eds.; Springer International Publishing: Cham, Switzerland, 2022; pp. 235–251. ISBN 978-3-030-87273-1. [Google Scholar]

- Dombrée, M.; Crott, R.; Lawson, G.; Janne, P.; Castiaux, A.; Krug, B. Cost Comparison of Open Approach, Transoral Laser Microsurgery and Transoral Robotic Surgery for Partial and Total Laryngectomies. Eur. Arch. Otorhinolaryngol. 2014, 271, 2825–2834. [Google Scholar] [CrossRef]

- Baratti, D.; Scivales, A.; Balestra, M.R.; Ponzi, P.; Di Stasi, F.; Kusamura, S.; Laterza, B.; Deraco, M. Cost Analysis of the Combined Procedure of Cytoreductive Surgery and Hyperthermic Intraperitoneal Chemotherapy (HIPEC). Eur. J. Surg. Oncol. (EJSO) 2010, 36, 463–469. [Google Scholar] [CrossRef] [PubMed]

- Demeere, N.; Stouthuysen, K.; Roodhooft, F. Time-Driven Activity-Based Costing in an Outpatient Clinic Environment: Development, Relevance and Managerial Impact. Health Policy 2009, 92, 296–304. [Google Scholar] [CrossRef] [PubMed]

- Yin, R.K. Case Study Research and Applications: Design and Methods; Sage Publications: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Scapens, R.W. Doing Case Study Research. In The Real Life Guide to Accounting Research; Elsevier: Amsterdam, The Netherlands, 2004; pp. 257–279. [Google Scholar]

- Available online: https://sanita.regione.abruzzo.it/canale-assistenza-territoriale/catalogo-prestazioni (accessed on 11 November 2022).

- di Lino Cinquini, P.M.V.; Pitzalis, A.; Campanale, C. Titolo: Il Costo Dell’intervento Chirurgico in Laparoscopia con l’Activity Based Costing; Associazione Italiana Economia Sanitaria: Milan, Italy, 2003; pp. 1–23. [Google Scholar]

- Italia Ministero dell’Economia e delle Finanze; Commissione Tecnica per la Finanza Pubblica. Libro Verde Sulla Spesa Pubblica. Spendere Meglio: Alcune Prime Indicazioni; Ministero dell’Economia e delle Finanze: Roma, Italy, 2007; pp. 36–57. [Google Scholar]

- Porter, M.E. What Is Value in Health Care. N. Engl. J. Med. 2010, 363, 2477–2481. [Google Scholar] [CrossRef]

- Porter, M.E. A Strategy for Health Care Reform-Toward a Value-Based System. N. Engl. J. Med. 2009, 361, 109–112. [Google Scholar] [CrossRef] [PubMed]

- Porter, M.E.; Teisberg, E.O. Redefining Health Care: Creating Value-Based Competition on Results; Harvard Business Press: Boston, MA, USA, 2006. [Google Scholar]

- Pathak, S.; Snyder, D.; Kroshus, T.; Keswani, A.; Jayakumar, P.; Esposito, K.; Koenig, K.; Jevsevar, D.; Bozic, K.; Moucha, C. What Are the Uses and Limitations of Time-Driven Activity-Based Costing in Total Joint Replacement? Clin. Orthop. Relat. Res. 2019, 477, 2071–2081. [Google Scholar] [CrossRef]

- Navathe, A.S.; Troxel, A.B.; Liao, J.M.; Nan, N.; Zhu, J.; Zhong, W.; Emanuel, E.J. Cost of Joint Replacement Using Bundled Payment Models. JAMA Intern. Med. 2017, 177, 214–222. [Google Scholar] [CrossRef]

- Menendez, M.E.; Lawler, S.M.; Shaker, J.; Bassoff, N.W.; Warner, J.J.P.; Jawa, A. Time-Driven Activity-Based Costing to Identify Patients Incurring High Inpatient Cost for Total Shoulder Arthroplasty. J. Bone Joint Surg. Am. 2018, 100, 2050–2056. [Google Scholar] [CrossRef] [PubMed]

- Robinson, J.C.; Pozen, A.; Tseng, S.; Bozic, K.J. Variability in Costs Associated with Total Hip and Knee Replacement Implants. JBJS 2012, 94, 1693–1698. [Google Scholar] [CrossRef]

- Haas, D.A.; Bozic, K.J.; DiGioia, A.M.; Song, Z.; Kaplan, R.S. Drivers of the Variation in Prosthetic Implant Purchase Prices for Total Knee and Total Hip Arthroplasties. J. Arthroplast. 2017, 32, 347–350. [Google Scholar] [CrossRef] [PubMed]

- Menendez, M.E.; Baker, D.K.; Fryberger, C.T.; Ponce, B.A. Predictors of Extended Length of Stay after Elective Shoulder Arthroplasty. J. Shoulder Elbow. Surg. 2015, 24, 1527–1533. [Google Scholar] [CrossRef] [PubMed]

- Koolmees, D.; Bernstein, D.N.; Makhni, E.C. Time-Driven Activity-Based Costing Provides a Lower and More Accurate Assessment of Costs in the Field of Orthopaedic Surgery Compared With Traditional Accounting Methods. Arthroscopy 2021, 37, 1620–1627. [Google Scholar] [CrossRef] [PubMed]

| Helthcare Professional | Monthly Pay | Total Time Spent | Total Cost |

|---|---|---|---|

| Orthopaedic Surgeons (x 2) | EUR 5330 | 39 min for each surgeon | EUR 45.59 |

| Orthopaedic surgeon (x 1) | EUR 5330 | 55 min | EUR 32.14 |

| Anaesthesiologist | EUR 6000 | 90 min | EUR 59.21 |

| Nurses (x 2) | EUR 2052 | 85 min for each nurse | EUR 40.80 |

| Nurse (x 1) | EUR 2052 | 90 min | EUR 21.60 |

| TOTAL COST | EUR 201.74 |

| Stage | Cost of Consumables |

|---|---|

| Pre-operating room | EUR 8.44 |

| Anesthesia and surgical field | EUR 42.25 |

| Position of patient | EUR 18.16 |

| Surgery (prosthetic implant excluded) | EUR 13.01 |

| Suture and dressing | EUR 15.16 |

| TOTAL COST | EUR 97.02 |

| Purchase Prices of Prostheses | |

|---|---|

| EUR 786.60 |

| EUR 425.60 |

| EUR 280.25 |

| EUR 1420.25 |

| Total without VAT | EUR 2912.70 |

| VAT | EUR 4% |

| TOTAL COST | EUR 3029.21 |

| Inpatient Total Cost of Tha | |

|---|---|

| 1. Pre-operative tests | EUR 90.29 |

| 2. Hospitalization | EUR 2493.80 |

| 3. Operating room | EUR 135.00 |

| 4. Consumables | EUR 97.02 |

| 5. Prosthesis | EUR 3029.21 |

| 6. Personnel | EUR 201.74 |

| FINAL COST | EUR 6002.06 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fidanza, A.; Schettini, I.; Palozzi, G.; Mitrousias, V.; Logroscino, G.; Romanini, E.; Calvisi, V. What Is the Inpatient Cost of Hip Replacement? A Time-Driven Activity Based Costing Pilot Study in an Italian Public Hospital. J. Clin. Med. 2022, 11, 6928. https://doi.org/10.3390/jcm11236928

Fidanza A, Schettini I, Palozzi G, Mitrousias V, Logroscino G, Romanini E, Calvisi V. What Is the Inpatient Cost of Hip Replacement? A Time-Driven Activity Based Costing Pilot Study in an Italian Public Hospital. Journal of Clinical Medicine. 2022; 11(23):6928. https://doi.org/10.3390/jcm11236928

Chicago/Turabian StyleFidanza, Andrea, Irene Schettini, Gabriele Palozzi, Vasileios Mitrousias, Giandomenico Logroscino, Emilio Romanini, and Vittorio Calvisi. 2022. "What Is the Inpatient Cost of Hip Replacement? A Time-Driven Activity Based Costing Pilot Study in an Italian Public Hospital" Journal of Clinical Medicine 11, no. 23: 6928. https://doi.org/10.3390/jcm11236928

APA StyleFidanza, A., Schettini, I., Palozzi, G., Mitrousias, V., Logroscino, G., Romanini, E., & Calvisi, V. (2022). What Is the Inpatient Cost of Hip Replacement? A Time-Driven Activity Based Costing Pilot Study in an Italian Public Hospital. Journal of Clinical Medicine, 11(23), 6928. https://doi.org/10.3390/jcm11236928