How Traditional Costing Methods Hinder the Development of Modular Product Architectures

, ,

, ,

Abstract

1. Introduction

2. Research Methods

2.1. Literature Study Process

- TITLE-ABS-KEY (“complexity management” OR “complexity costs” OR “quantification of complexity costs” OR “complexity reduction” OR “External Product Vari*” OR “Indirect Cost” OR “variant management” OR “variant cost*”) AND TITLE-ABS-KEY (“product architecture” OR “modular*” OR “data management” OR “MBSE” OR “SysML” OR “KPIs” OR “decision support” OR “product concept evaluation” OR “knowledge management” OR “ design knowledge”)

- TITLE-ABS-KEY (“Cost systems” OR “External Product Vari*” OR “variant cost*” OR “Activity-Based cost*” OR “ABC” OR “Cost Accounting” OR “Cost Allocation”) AND TITLE-ABS-KEY (“product architecture” OR “modular*”)

2.2. Categorization of Assessment Methods for Modularity Effects

3. Literature Review

3.1. The Effects of Product Variety

3.2. Methods for Allocation of Costs Related to Product Variety

3.3. Economic Benefits and Effects of Modular Product Architectures

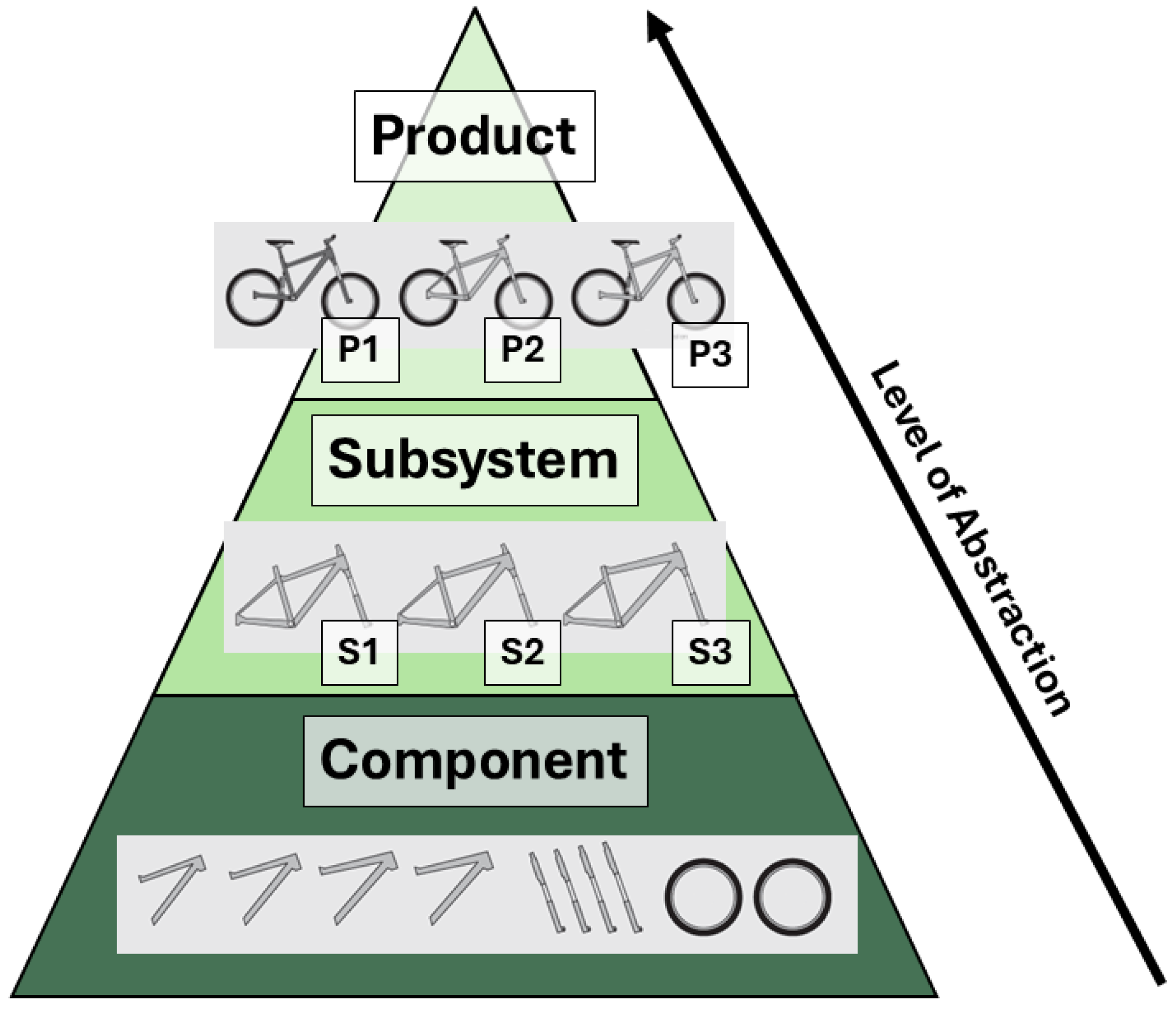

4. Categorization of Abstraction Levels

4.1. Introducing the Levels of Abstraction

4.2. Findings Following the Categorization of Abstraction Levels

5. Discussion

5.1. Development

5.2. Procurement

5.3. Production

5.4. Sales

5.5. Service

5.6. Summary of Tendencies Observed Across Life-Cycle Phases

6. Conclusions

7. Future Work

- (1)

- Current allocation models must be refined to incorporate more accurate indirect cost allocation throughout the various phases of the product life cycle, particularly for modular product structures. This may require restructuring a company’s internal financial system or implementing an external cost model.

- (2)

- To assess the potential impact of a refined cost allocation model on various types of manufacturing companies, a new costing framework should be developed. The framework should encompass the findings regarding the allocation of product variety costs across different abstraction levels addressed in this paper.

- (3)

- As the first step toward a more generalizable and holistic model, a variety of different manufacturing companies should be included in a case study observing the effects of applying a refined cost allocation model.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

References

- Kwapisz, J.; Infante, V.; Cameron, B.G. Commonality opportunity search in industrial product portfolios Virginia Infante. Int. J. Technol. Manag. 2019, 81, 258–273. [Google Scholar] [CrossRef]

- ElMaraghy, H.; Schuh, G.; ElMaraghy, W.; Piller, F.; Schönsleben, P.; Tseng, M.; Bernard, A. Product variety management. CIRP Ann.-Manuf. Technol. 2013, 62, 629–652. [Google Scholar] [CrossRef]

- Hvam, L.; Hansen, C.L.; Forza, C.; Mortensen, N.H.; Haug, A. The reduction of product and process complexity based on the quantification of product complexity costs. Int. J. Prod. Res. 2020, 58, 350–366. [Google Scholar] [CrossRef]

- Windheim, M.; Hackl, J.; Gebhardt, N.; Krause, D. Assessing Impacts of Modular Product Architectures on The Firm: A Case Study. In Proceedings of the 14th International Design Conference, Dubrovnik, Croatia, 16–19 May 2016; pp. 1445–1454. [Google Scholar]

- Israelsen, P.; Jørgensen, B. Decentralizing decision making in modularization strategies: Overcoming barriers from dysfunctional accounting systems. Int. J. Prod. Econ. 2011, 131, 453–462. [Google Scholar] [CrossRef]

- Wouters, M.; Morales, S.; Grollmuss, S.; Scheer, M. Methods for cost management during product development: A review and comparison of different literatures. Adv. Manag. Account. 2016, 26, 139–274. [Google Scholar] [CrossRef]

- Ehrlenspiel, K.; Kiewert, A.; Lindemann, U. Cost-Efficient Design; ASME International: New York, NY, USA, 2007. [Google Scholar]

- Roy, M.A.; Abdul-Nour, G. Integrating Modular Design Concepts for Enhanced Efficiency in Digital and Sustainable Manufacturing: A Literature Review. Appl. Sci. 2024, 14, 4539. [Google Scholar] [CrossRef]

- Thyssen, J.; Israelsen, P.; Jørgensen, B. Activity-based costing as a method for assessing the economics of modularization-A case study and beyond. Int. J. Prod. Econ. 2006, 10, 252–270. [Google Scholar] [CrossRef]

- Ripperda, S.; Krause, D. Cost Effects of Modular Product Family Structures: Methods and Quantification of Impacts to Support Decision Making. J. Mech. Des. Trans. ASME 2017, 139, 021103. [Google Scholar] [CrossRef]

- Gauss, L.; Lacerda, D.P.; Cauchick Miguel, P.A. Module-based product family design: Systematic literature review and meta-synthesis. J. Intell. Manuf. 2021, 32, 265–312. [Google Scholar] [CrossRef]

- Nørgaard, M.; Grønvald, J.M.; Christensen, C.K.F.; Mortensen, N.H. Challenges in product variant costing—A case study. Proc. Des. Soc. 2024, 4, 3003–3012. [Google Scholar]

- Jiao, J.; Simpson, T.W.; Siddique, Z. Product family design and platform-based product development: A state-of-the-art review. J. Intell. Manuf. 2007, 18, 5–29. [Google Scholar] [CrossRef]

- Park, J.; Simpson, T.W. Toward an activity-based costing system for product families and product platforms in the early stages of development. Int. J. Prod. Res. 2008, 46, 99–130. [Google Scholar] [CrossRef]

- Hackl, J.; Krause, D.; Otto, K.; Windheim, M.; Moon, S.K.; Bursac, N.; Lachmayer, R. Impact of Modularity Decisions on a Firm’s Economic Objectives. J. Mech. Des. Trans. ASME 2020, 142, 041403. [Google Scholar] [CrossRef]

- Simpson, T.W.; Marion, T.; De Weck, O.; Hölttä-Otto, K.; Kokkolaras, M.; Shooter, S.B. Platform-based Design and Development: Current Trends and Needs in Industry. In Proceedings of the ASME 2006 International Design Engineering Technical Conferences & Computers and Information in Engineering Conference, Philadelphia, PA, USA, 10–13 September 2006. [Google Scholar]

- Stadtherr, F.; Wouters, M. Extending target costing to include targets for R&D costs and production investments for a modular product portfolio—A case study. Int. J. Prod. Econ. 2021, 231, 107871. [Google Scholar] [CrossRef]

- Greve, E.; Fuchs, C.; Hamraz, B.; Windheim, M.; Rennpferdt, C.; Schwede, L.-N.; Krause, D. Knowledge-Based Decision Support for Concept Evaluation Using the Extended Impact Model of Modular Product Families. Appl. Sci. 2022, 12, 547. [Google Scholar] [CrossRef]

- Magnacca, F.; Giannetti, R. Management accounting and new product development: A systematic literature review and future research directions. J. Manag. Gov. 2024, 28, 651–685. [Google Scholar] [CrossRef]

- Wouters, M.; Stadtherr, F. Cost management and modular product design strategies. In The Routledge Companion to Performance Management and Control; Routledge: London, UK, 2017; pp. 54–86. [Google Scholar]

- Mortensen, N.H.; Bertram, C.A.; Lundgaard, R. Achieving long-term modularization benefits: A small- and medium-sized enterprise study. Concurr. Eng. Res. Appl. 2019, 27, 14–27. [Google Scholar] [CrossRef]

- Neri, A.; Cagno, E.; Susur, E.; Urueña, A.; Nuur, C.; Kumar, V.; Franchi, S.; Sorrentino, C. The relationship between digital technologies and the circular economy: A systematic literature review and a research agenda. R&D Manag. 2024, 55, 617–714. [Google Scholar] [CrossRef]

- Schwede, L.-N.; Greve, E.; Krause, D.; Otto, K.; Moon, S.K.; Albers, A.; Kirchner, E.; Lachmayer, R.; Bursac, N.; Inkermann, D.; et al. How to Use the Levers of Modularity Properly-Linking Modularization to Economic Targets. J. Mech. Des. Trans. ASME 2022, 144, 071401. [Google Scholar] [CrossRef]

- Gusenbauer, M.; Haddaway, N.R. Which academic search systems are suitable for systematic reviews or meta-analyses? Evaluating retrieval qualities of Google Scholar, PubMed, and 26 other resources. Res. Synth. Methods 2020, 11, 181–217. [Google Scholar] [CrossRef]

- Visser, M.; van Eck, N.J.; Waltman, L. Large-scale comparison of bibliographic data sources: Scopus, web of science, dimensions, crossref, and microsoft academic. Quant. Sci. Stud. 2021, 2, 20–41. [Google Scholar] [CrossRef]

- Micheli, G.J.L.; Trucco, P.; Sabri, Y.; Mancini, M. Modularization as a system life cycle management strategy: Drivers, barriers, mechanisms and impacts. Int. J. Eng. Bus. Manag. 2019, 11, 1847979018825041. [Google Scholar] [CrossRef]

- Mertens, K.G. Measure and Manage your Product Costs Right-Development and Use of an Extended Axiomatic Design for Cost Modeling. Ph.D. Thesis, Technische Universität Hamburg, Hamburg, Germany, 2020. [Google Scholar]

- Mertens, K.G.; Schmidt, M.; Yildiz, T.; Meyer, M. Introducing a framework to generate and evaluate the cost effects of product (family) concepts. Proc. Des. Soc. 2021, 1, 1907–1916. [Google Scholar]

- Greve, E.; Krause, D. Long-term effects of modular product architectures: An empirical follow-up study. In Procedia CIRP; Elsevier B.V.: Amsterdam, The Netherlands, 2019; Volume 84, pp. 731–736. [Google Scholar]

- Kahn, B. Variety: From the Consumer’s Perspective. In International Series in Operations Research & Management Science; Springer Science + Business Media: New York, NY, USA, 1998; pp. 19–37. [Google Scholar]

- Fadeyi, J.A.; Monplaisir, L. Instilling lifecycle costs into modular product development for improved remanufacturing-product service system enterprise. Int. J. Prod. Econ. 2022, 246, 108404. [Google Scholar] [CrossRef]

- Asiedu, Y.; Gu, P. Product life cycle cost analysis: State of the art review. Int. J. Prod. Res. 1998, 36, 883–908. [Google Scholar] [CrossRef]

- Fixson, S.K. Product architecture assessment: A tool to link product, process, and supply chain design decisions. J. Oper. Manag. 2005, 23, 345–369. [Google Scholar] [CrossRef]

- Windheim, M.; Gebhardt, N.; Krause, D. Towards a Decision-Making Framework for Multi-Criteria Product Modularization in Cooperative Environments. Procedia CIRP 2018, 70, 380–385. [Google Scholar] [CrossRef]

- Martin, M.V.; Ishii, K. Design for Variety: Development of Complexity Indices and Design Charts. In Proceedings of the DETC ‘97 1997 ASME Design Engineering Technical Conferences, Sacramento, CA, USA, 14–17 September 1997; ASME: New York, NY, USA, 1997. [Google Scholar]

- Siguenza-Guzman, L.; Van Den Abbeele, A.; Vandewalle, J.; Verhaaren, H.; Cattrysse, D. Recent evolutions in costing systems: A literature review of Time-Driven Activity-Based Costing. Rev. Bus. Econ. Lit. 2013, 58, 34–64. [Google Scholar]

- Horngren, C.T.; Datar, S.M.; Rajan, M.V. Cost Accounting a Managerial Emphasis, 13th ed.; Pearson Internation Edition: London, UK, 2009. [Google Scholar]

- Drury, C. Cost and Management Accounting—An Introduction; Cengage Learning EMEA: Hampshire, UK, 2015. [Google Scholar]

- Wilson, S.A.; Perumal, A. Reshape your cost structure, free up cash flows, and boost productivity by attacking process, product and organizational complexity. In Waging War on Complexity Costs; McGraw-Hill: New York, NY, USA, 2010. [Google Scholar]

- Cooper, R.; Kaplan, R.S. Measure Costs Right: Make the Right Decisions. Harv. Bus. Rev. 1988, 66, 96–103. [Google Scholar]

- Kaplan, R.S.; Cooper, R. Cost & Effect: Using Integrated Cost Systems to Drive Profitability and Performance; Harvard Business Press: Brighton, UK, 1998. [Google Scholar]

- Park, J.; Simpson, T.W. Development of a production cost estimation framework to support product family design. Int. J. Prod. Res. 2005, 43, 731–772. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Anderson, S.R. Time-Driven Activity-Based Costing; Harvard Business Review: Brighton, UK, 2004; Volume 82. [Google Scholar] [CrossRef]

- Trattner, A.; Hvam, L.; Forza, C.; Nadja Lee Herbert-Hansen, Z. Product complexity and operational performance: A systematic literature review. CIRP J. Manuf. Sci. Technol. 2019, 25, 65–83. [Google Scholar] [CrossRef]

- Thonemann, U.W.; Brandeau, M.L. Optimal Commonality in Component Design. Oper. Res. 2000, 48, 1–19. [Google Scholar] [CrossRef]

- Myrodia, A.; Hvam, L.; Sandrin, E.; Forza, C.; Haug, A. Identifying variety-induced complexity cost factors in manufacturing companies and their impact on product profitability. J. Manuf. Syst. 2021, 60, 373–391. [Google Scholar] [CrossRef]

- Yano, C.; Dobson, G. Profit-Optimizing Product Line Design, Selection and Pricing with Manufacturing Cost Consideration. In Product Variety Management; Springer: Berlin/Heidelberg, Germany, 1998; pp. 146–175. [Google Scholar]

- Wouters, M.; Morales, S. The contemporary art of cost management methods during product development. Adv. Manag. Account. 2014, 24, 259–346. [Google Scholar] [CrossRef]

- Bonvoisin, J.; Halstenberg, F.; Buchert, T.; Stark, R. A systematic literature review on modular product design. J. Eng. Des. 2016, 27, 488–514. [Google Scholar] [CrossRef]

- Ericsson, A.; Erixon, G. Controlling Design Variants: Modular Product Platforms; Society of Manufacturing Engineers: Southfield, MI, USA, 1999. [Google Scholar]

- Otto, K.N.; Wood, K.L. Product Design: Techniques in Reverse Engineering and New Product Development; PrenticeHall: Upper Saddle River, NJ, USA, 2001. [Google Scholar]

- Ulrich, K.T.; Eppinger, S.D. Product Design and Development, 5th ed.; McGraw Hill: New York, NY, USA, 2012. [Google Scholar]

- Boer, H.E.E. Product, Organizational and Performance Effects of Product Modularity. In Proceedings of the 7th World Conference on Mass Customization, Personalization and Co-Creation (MCPC 2014), Aalborg, Denmark, 4–7 February 2014; Springer Nature: Berlin/Heidelberg, Germany, 2014; Volume Part F1148, pp. 449–460. [Google Scholar]

- Jacobs, M.; Droge, C.; Vickery, S.K.; Calantone, R. Product and Process Modularity’s Effects on Manufacturing Agility and Firm Growth Performance. J. Prod. Innov. Manag. 2011, 28, 123–137. [Google Scholar] [CrossRef]

- Robertson, D.; Ulrich, K. Planning for Product Platforms. Sloan Manag. Rev. 1998, 39, 19–32. [Google Scholar]

- Salvador, F. Toward a product system modularity construct: Literature review and reconceptualization. IEEE Trans. Eng. Manag. 2007, 54, 219–240. [Google Scholar] [CrossRef]

- Fixson, S.K. A Road Map For Product Architecture Costing. In Product Platform and Product Family Design: Methods and Applications; Simpson, T.W., Siddique, Z., Jiao, J., Eds.; Springer Science + Business Media: New York, NY, USA, 2006; pp. 305–334. [Google Scholar]

- Meyer, M.H.; Lehnerd, A.P. The Power of Product Platforms: Building Value and Cost Leadership; The Free Press: Los Angeles, CA, USA, 1997. [Google Scholar]

- Perera, H.S.C.; Nagarur, N.; Tabucanon, M.T. Component part standardization: A way to reduce the life-cycle costs of products. Int. J. Prod. Econ. 1999, 60–61, 109–116. [Google Scholar] [CrossRef]

- Cameron, B.G.; Rhodes, R.; Boas, R.; Crawley, E.F. Divergence In Platform Commonality: Examination of Potential Cost Implications. In Proceedings of the 11th International Design Conference—Design, Dubrovnik, Croatia, 3–10 March 2010; pp. 157–162. [Google Scholar]

- Sohrt, M.; Blinkenberg, W.; Mortensen, N.H.; Haug, A.; Hvam, L. A Method for Modelling Business-Critical Architecture Decisions in Engineer-to-Order Companies. Appl. Sci. 2025, 15, 1998. [Google Scholar] [CrossRef]

- Taipaleenmäki, J. Absence and Variant Modes of Presence of Management Accounting in New Product Development—Theoretical Refinement and Some Empirical Evidence. Eur. Account. Rev. 2014, 23, 291–334. [Google Scholar] [CrossRef]

- Horber, D.; Pickel, J.; Goetz, S.; Wartzack, S. Utilizing System Models for Multicriteria Decision-Making—A Systematic Literature Review on the Current State of the Art. IEEE Open J. Syst. Eng. 2024, 2, 135–147. [Google Scholar] [CrossRef]

- Boas, R.; Cameron, B.G.; Crawley, E.F. Divergence and lifecycle offsets in product families with commonality. Syst. Eng. 2013, 16, 175–192. [Google Scholar] [CrossRef]

- Gershenson, J.K.; Prasad, G.J.; Zhang, Y. Product modularity: Definitions and benefits. J. Eng. Des. 2003, 14, 295–313. [Google Scholar] [CrossRef]

- Weiser, A.K.; Baasner, B.; Hosch, M.; Schlueter, M.; Ovtcharova, J. Complexity Assessment of Modular Product Families. Procedia CIRP 2016, 50, 595–600. [Google Scholar] [CrossRef]

- Sigsgaard, K.V.; Agergaard, J.K.; Bertram, C.A.; Mortensen, N.H.; Soleymani, I.; Khalid, W.; Hansen, K.B.; Mueller, G.O. Structuring and Contextualizing Historical Data for Decision Making in Early Development. In Design 2020, Proceedings of 16th International Design Conference, Dubrovnik, Croatia, 18–21 May 2020; Cambridge University Press: Cambridge, UK, 2020; Volume 1, pp. 393–402. [Google Scholar]

- Chiu, M.-C.; Okudan, G. An Investigation on the Impact of Product Modularity Level on Supply Chain Performance Metrics: An Industrial Case Study. J. Intell. Manuf. 2014, 25, 129–145. [Google Scholar] [CrossRef]

- Harland, P.E.; Uddin, Z. Effects of Product Platform Development: Fostering Lean Product Development and Production. Int. J. Prod. Dev. 2014, 19, 259. [Google Scholar] [CrossRef]

- Dogramaci, A. Design of Common Components Considering Implications of Inventory Costs and Forecasting. AIIE Trans. 1979, 11, 129–135. [Google Scholar] [CrossRef]

- Eynan, A.; Rosenblatt, M.J. Component commonality effects on inventory costs. IIE Trans. 1996, 28, 93–104. [Google Scholar] [CrossRef]

- Collier, D.A. The Measurement and Operating Benefits of Component Part Commonality. Decis. Sci. 1981, 12, 85–96. [Google Scholar] [CrossRef]

- Danese, P.; Filippini, R. Direct and Mediated Effects of Product Modularity on Development Time and Product Performance. IEEE Trans. Eng. Manag. 2013, 60, 260–271. [Google Scholar] [CrossRef]

- Abdelkafi, N. Variety-Induced Complexity in Mass Customization Concepts and Management; Blecker, T., Huang, G.Q., Salvador, F., Eds.; Erich Schmidt: Berlin, Germany, 2008. [Google Scholar]

- Mikkola, J.H.; Gassmann, O. Managing Modularity of Product Architectures: Toward an Integrated Theory. IEEE Trans. Eng. Manag. 2003, 50, 204–218. [Google Scholar] [CrossRef]

- Baldwin, C.Y.; Clark, K.B. Design Rules; The MIT Press: Cambridge, MA, USA, 2000. [Google Scholar]

- Ulrich, K. The Role of Product Architecture in the Manufacturing Firm. Res. Policy 1995, 24, 419–440. [Google Scholar] [CrossRef]

- Hansen, P.; Andreasen, M.; Ulf, H.; Gubi, E.; Mortensen, N. Understanding the Phenomenon of Modularization. In Design 2002, Proceedings of the 7th International Design Conference, Dubrovnik, Croatia, 14–17 May 2002; Marjanovic, D., Ed.; University of Zagreb, Faculty Mechanical Engineering & Naval Architecture: Zagreb, Croatia, 2002. [Google Scholar]

- Lau Antonio, K.W.; Yam, R.C.M.; Tang, E. The Impacts of Product Modularity on Competitive Capabilities and Performance: An Empirical Study. Int. J. Prod. Econ. 2007, 105, 1–20. [Google Scholar] [CrossRef]

- Vogt, J.; Woeller, L.N.; Krause, D. Effects of Product Personalization: Considering Personalizability in the Product Architecture of Modular Product Families. J. Mech. Des. 2024, 146, 1–47. [Google Scholar] [CrossRef]

- Ulrich, K. Fundamentals of Product Modularity. In Management of Design; Springer: Dordrecht, The Netherlands, 1994; pp. 219–231. [Google Scholar]

- Hölttä-Otto, K. Modular Product Platform Design. Ph.D. Thesis, Helsinki University of Technology, Espoo, Finland, 2005. [Google Scholar]

- Salonen, M.; Otto, K.H.; Otto, K. Effecting Product Reliability and Life Cycle Costs with Early Design Phase Product Architecture Decisions. Int. J. Prod. Dev. 2008, 5, 109. [Google Scholar] [CrossRef]

- OuYang, T.; Li, J.; Chen, Z. Research on Product Innovation Mode Based on Modularity Theory: A Case Study on Haier Product Innovation. In Proceedings of the 2008 IEEE International Conference on Service Operations and Logistics and Informatics, Beijing, China, 12–15 October 2008; IEEE: New York, NY, USA, 2008; pp. 250–255. [Google Scholar]

- Pil, F.K.; Cohen, S.K. Modularity: Implications for Imitation, Innovation, and Sustained Advantage. Acad. Manag. Rev. 2006, 31, 995–1011. [Google Scholar] [CrossRef]

- Arnheiter, E.D.; Harren, H. Quality Management in a Modular World. TQM Mag. 2006, 18, 87–96. [Google Scholar] [CrossRef]

- Gershenson, J.K.; Prasad, G.J. Product modularity and its effect on service and maintenance. In Proceedings of the 1997 Maintenance and Reliability Conference, Knoxville, TN, USA, 20–22 May 1997; p. 13. [Google Scholar]

- Hohnen, T. Kennzahlbasierte Optimierung der Produktmodularität zur Reduktion der Produktkosten; Shaker GmbH: Düren, Germany, 2014. [Google Scholar]

- Dong, M.; Chen, F.F. The Impacts of Component Commonality on Integrated Supply Chain Network Performance: A State and Resource-Based Simulation Study. Int. J. Adv. Manuf. Technol. 2005, 27, 397–406. [Google Scholar] [CrossRef]

- Brière-Côté, A.; Rivest, L.; Desrochers, A. Adaptive generic product structure modelling for design reuse in engineer-to-order products. Comput. Ind. 2010, 61, 53–65. [Google Scholar] [CrossRef]

- Bertram, C.A.; Mueller, G.O.; Lokkegaard, M.; Mortensen, N.H.; Hvam, L. Why Engineer-to-Order Portfolio Rationalization Stalls: Challenges in Standardization, Modularization, Platform Design and Mass Customization. In Design 2020, Proceedings of 16th International Design Conference, Dubrovnik, Croatia, 18–21 May 2020; Cambridge University Press: Cambridge, UK, 2020; Volume 1, pp. 2265–2273. [Google Scholar]

- Hackl, J.; Krause, D. Towards an Impact Model of Modular Product. In Proceedings of the 21st International Conference on Engineering Design (ICED17), Vancouver, BC, Canada, 21–25 August 2017; Volume 3. [Google Scholar]

- Wouters, M.; Stecher, J. Development of real-time product cost measurement: A case study in a medium-sized manufacturing company. Int. J. Prod. Econ. 2017, 183, 235–244. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Cost Allocation Methods | References |

|---|---|

| Volume-Based Costing | Horngren et al. [37]; Drury [38] |

| Activity-Based Costing (ABC) | Horngren et al. [37]; Cooper and Kaplan [40] |

| Time-Driven ABC (TDABC) | Kaplan and Anderson [43] |

| Target Costing (TC) | Ehrlenspiel et al. [7]; Stadtherr and Wouters [17] |

| Unique-to-One Solution | Modular Solution | |||||||

|---|---|---|---|---|---|---|---|---|

| Revenue | P1 | P2 | P3 | Sum | P1 | P2 | P3 | Sum |

| # of Units Sold | 100 | 80 | 50 | 100 | 80 | 50 | ||

| Sales Price | 150 | 200 | 250 | 150 | 200 | 250 | ||

| Total Revenue | 15,000 | 16,000 | 12,500 | 43,500 | 15,000 | 16,000 | 12,500 | 43,500 |

| Direct Costs (DCs) | ||||||||

| Material | 30 | 35 | 40 | 40 | 40 | 40 | ||

| Labor | 20 | 20 | 25 | 25 | 25 | 25 | ||

| Total DCs | 5000 | 4400 | 3250 | 12,650 | 6400 | 5200 | 3250 | 14,950 |

| Indirect Costs (ICs) | ||||||||

| Development Cost | 4000 | 4000 | 4000 | 12,000 | 3500 | 3500 | 3500 | 10,500 |

| Batch Cost | 50 | 50 | 50 | 40 | 40 | 40 | ||

| Total ICs | 9000 | 8000 | 6500 | 23,500 | 7500 | 6700 | 5500 | 19,700 |

| Result | ||||||||

| Gross Profit | 10,000 | 11,600 | 9250 | 30,850 | 8500 | 10,800 | 9250 | 28,550 |

| Profit w. IC | 1000 | 3600 | 2750 | 7.350 | 1000 | 4100 | 3750 | 8850 |

| LCP | Modularity Effect | Abstraction Level—#Instances | #Ref | Sources | ||

|---|---|---|---|---|---|---|

| P | S | C | ||||

| Development | Improve outsourcing of development tasks | 2 | 2 | 1 | 4 | [18,73,74,75] |

| Improve parallel development/prototyping | 8 | 2 | 8 | [18,50,65,76,77,78,79,80] | ||

| Improve adaptability upgradeability | 2 | 3 | [65,81,82] | |||

| Improve reliability of product (component reuse) | 6 | 2 | 6 | [18,23,51,52,69,83] | ||

| Increase probability of spreading error | 2 | 2 | [18,23] | |||

| Decrease in failure rate | 2 | 2 | 4 | [18,23,69,84] | ||

| Improve/reduce product innovation | 5 | 1 | 6 | [18,23,65,68,84,85] | ||

| Reduce freedom of design/product differentiation | 5 | 1 | 6 | [18,23,29,65,68,85] | ||

| Improve variant derivation | 6 | 4 | 6 | [18,51,57,65,69,78] | ||

| Increase initial development investment | 5 | 2 | 6 | [18,55,68,69,77,80] | ||

| Reduce development cost per unit | 1 | 1 | [10] | |||

| Reduce time for part search | 2 | 2 | [18,23] | |||

| Reduce documentation and coordination effort | 3 | 3 | [18,23,29] | |||

| Improve part administration | 2 | 2 | [18,50] | |||

| Increase in volume | 5 | 2 | 6 | [18,59,65,68,82,86] | ||

| Increase in weight | 5 | 2 | 6 | [18,59,65,68,82,86] | ||

| Increase in no. of unused features | 5 | 3 | 5 | [18,65,68,82,86] | ||

| Procurement | Reduce safety stock and inventory levels | 5 | 6 | 9 | 9 | [18,23,59,65,68,70,71,75,87] |

| Improve predictability | 5 | 5 | [18,55,68,70,82] | |||

| Improve purchasing conditions (economy of scale) | 7 | 7 | [18,50,59,65,68,69,84] | |||

| Reduce the number of purchase orders | 4 | 4 | [18,50,65,88] | |||

| Improve purchase of prefabricated modules | 1 | 1 | [23] | |||

| Reduce no. of suppl./easier suppl. management | 1 | 4 | 5 | [18,23,68,74,89] | ||

| Improve repetition rate/less clarification w. supplier | 2 | 2 | [18,23] | |||

| Improve dependency on suppl. performance | 2 | 2 | [18,23] | |||

| Production | Improve outsourcing of manufacturing tasks | 2 | 2 | 2 | 2 | [18,23] |

| Improve parallel testing | 3 | 1 | 4 | [18,23,50,74] | ||

| Improve parallel manufacturing processes | 4 | 2 | 6 | [18,23,50,54,65,74] | ||

| Reduce time to start production planning | 2 | 2 | [18,23] | |||

| Improve production planning and control | 2 | 2 | [18,29] | |||

| Improve postponement in production (CODP) | 6 | 1 | 6 | [18,23,53,68,74,78] | ||

| Reduce time for failure detection | 3 | 3 | 3 | [18,23,65] | ||

| Reduce the number of errors/rework/rejected parts | 6 | 6 | 5 | 7 | [18,23,29,68,69,77] | |

| Reduce tool inventory (inventory holding cost) | 6 | 4 | 6 | [18,23,55,57,58,59] | ||

| Improve potential for automation | 3 | 3 | [18,23,57] | |||

| Improve balance of machine utilization | 3 | 3 | [18,23,57] | |||

| Reduce setup changes (setup times/queuing delays) | 3 | 3 | 4 | [18,23,68,72] | ||

| Reduce manufacturing cost per unit | 9 | 8 | 9 | 9 | [18,54,55,57,58,59,77,78,88] | |

| Improve production flexibility | 2 | 2 | [18,29] | |||

| Improve learning curve gradient | 3 | 3 | 6 | 6 | [18,23,65,68,69,77] | |

| Sales | Improve time to offer preparation | 2 | 2 | [18,23] | ||

| Improve easier price calculation | 1 | 1 | [29] | |||

| Improve customer satisfaction | 3 | 3 | [18,23,29] | |||

| Improve consumer-based configurability | 3 | 3 | [18,23,65] | |||

| Reduce/increase cannibalizing sales | 2 | 2 | 2 | [18,23] | ||

| Reduce costs related to training employees | 2 | 2 | [18,23] | |||

| Improve responsiveness | 3 | 3 | [18,23] | |||

| Reduce exotic product variants | 2 | 2 | [18,23] | |||

| Service | Improve the risk of replacement of intact module parts | 2 | 2 | 2 | [18,23] | |

| Reduce service, maintenance, and repair costs | 4 | 4 | [18,23,29,65] | |||

| Reduce number of stock items (spare parts) | 3 | 3 | [29,65,87] | |||

| Reduce the number of specialized tools for repair/service | 2 | 2 | [18,23] | |||

| Improve learning curve for training staff | 2 | 2 | [18,23] | |||

| Ease of failure diagnosis/reactivity | 2 | 2 | [18,23] | |||

| Improve reuse, recycling, and disposal due to dis-ass. effort | 2 | 2 | [23,65] | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nørgaard, M.; Grønvald, J.M.; Christensen, C.K.F.; Mortensen, N.H. How Traditional Costing Methods Hinder the Development of Modular Product Architectures. Appl. Sci. 2025, 15, 6307. https://doi.org/10.3390/app15116307

Nørgaard M, Grønvald JM, Christensen CKF, Mortensen NH. How Traditional Costing Methods Hinder the Development of Modular Product Architectures. Applied Sciences. 2025; 15(11):6307. https://doi.org/10.3390/app15116307

Chicago/Turabian StyleNørgaard, Morten, Jakob Meinertz Grønvald, Carsten Keinicke Fjord Christensen, and Niels Henrik Mortensen. 2025. "How Traditional Costing Methods Hinder the Development of Modular Product Architectures" Applied Sciences 15, no. 11: 6307. https://doi.org/10.3390/app15116307

APA StyleNørgaard, M., Grønvald, J. M., Christensen, C. K. F., & Mortensen, N. H. (2025). How Traditional Costing Methods Hinder the Development of Modular Product Architectures. Applied Sciences, 15(11), 6307. https://doi.org/10.3390/app15116307