Leveraging Multi-Agent Systems and Decentralised Autonomous Organisations for Tax Credit Tracking: A Case Study of the Superbonus 110% in Italy

Abstract

1. Introduction

2. Background and Related Works

2.1. Superbonus 110%

2.1.1. The Legislation

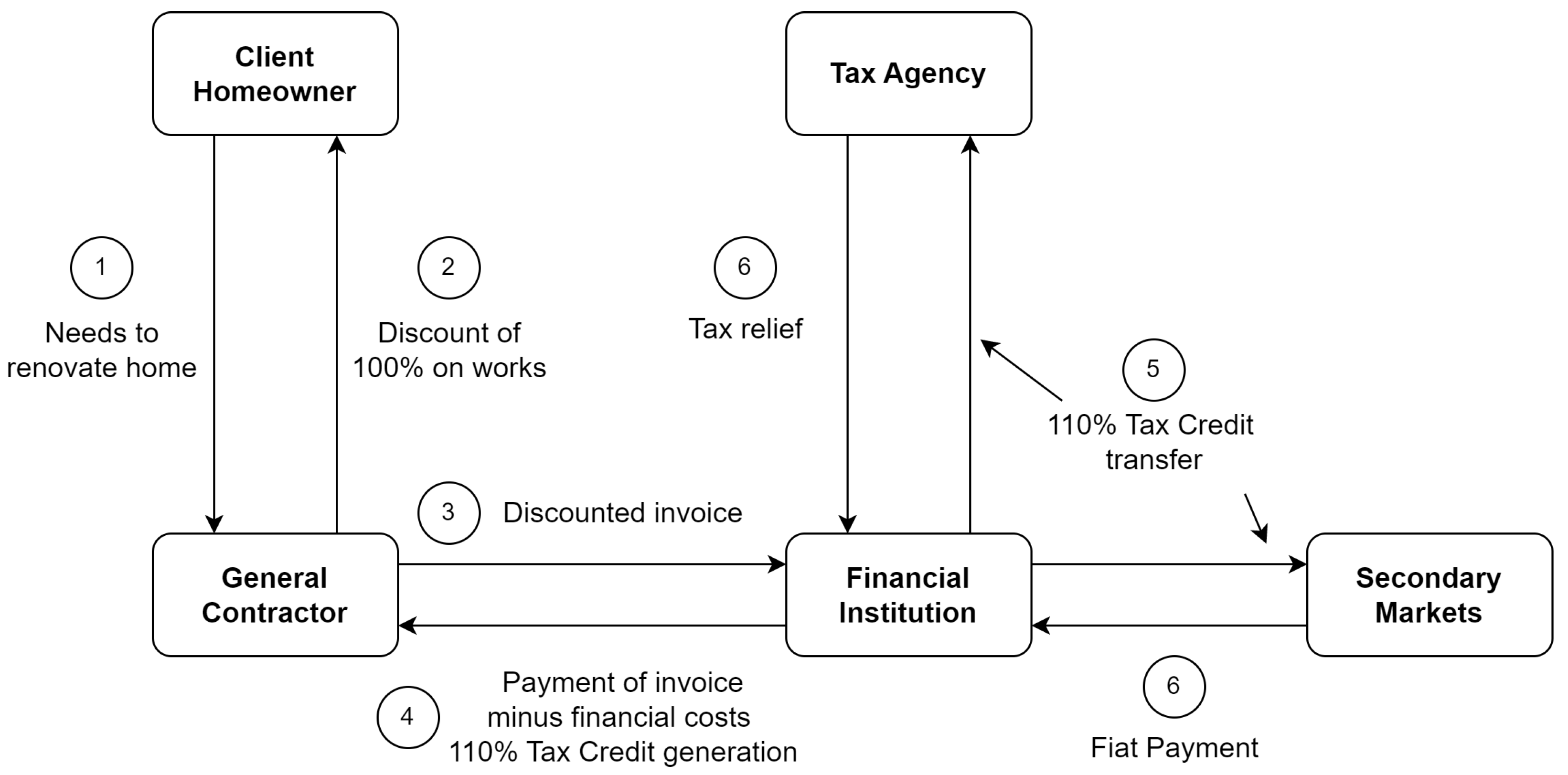

2.1.2. Discount on the Invoice and the Accrued Credit

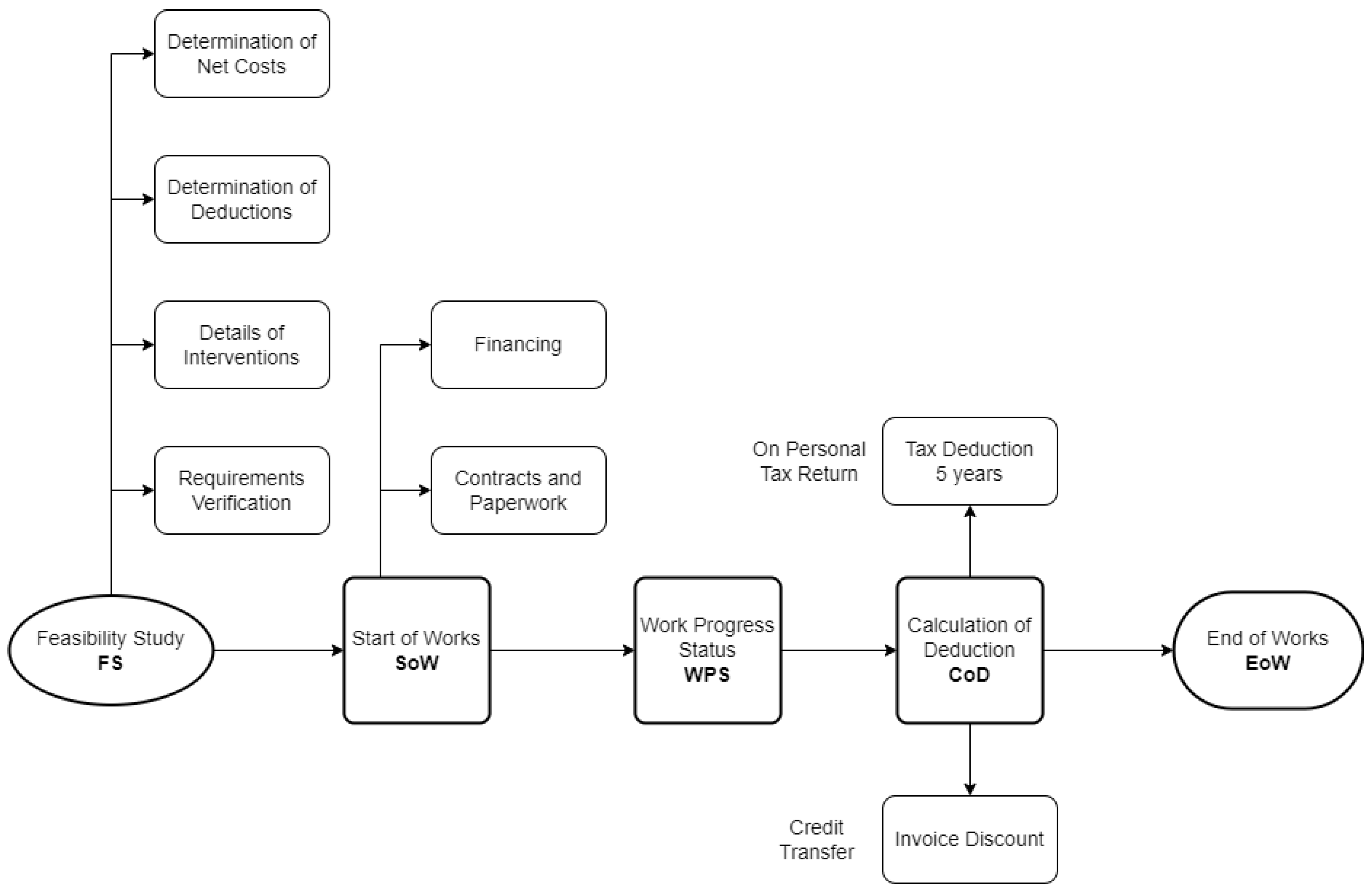

2.1.3. The Procedure

- Step 1—The feasibility study (FS) consists of three steps: (i) verification that the envisaged intervention qualifies for relief such as building permits and urban planning compliance; (ii) detailing of the hypothesised interventions and calculation of the deductions due (e.g., estimated metric calculation and detailed estimates); and (iii) determination of the net investment cost (i.e., actual expenditure credit).

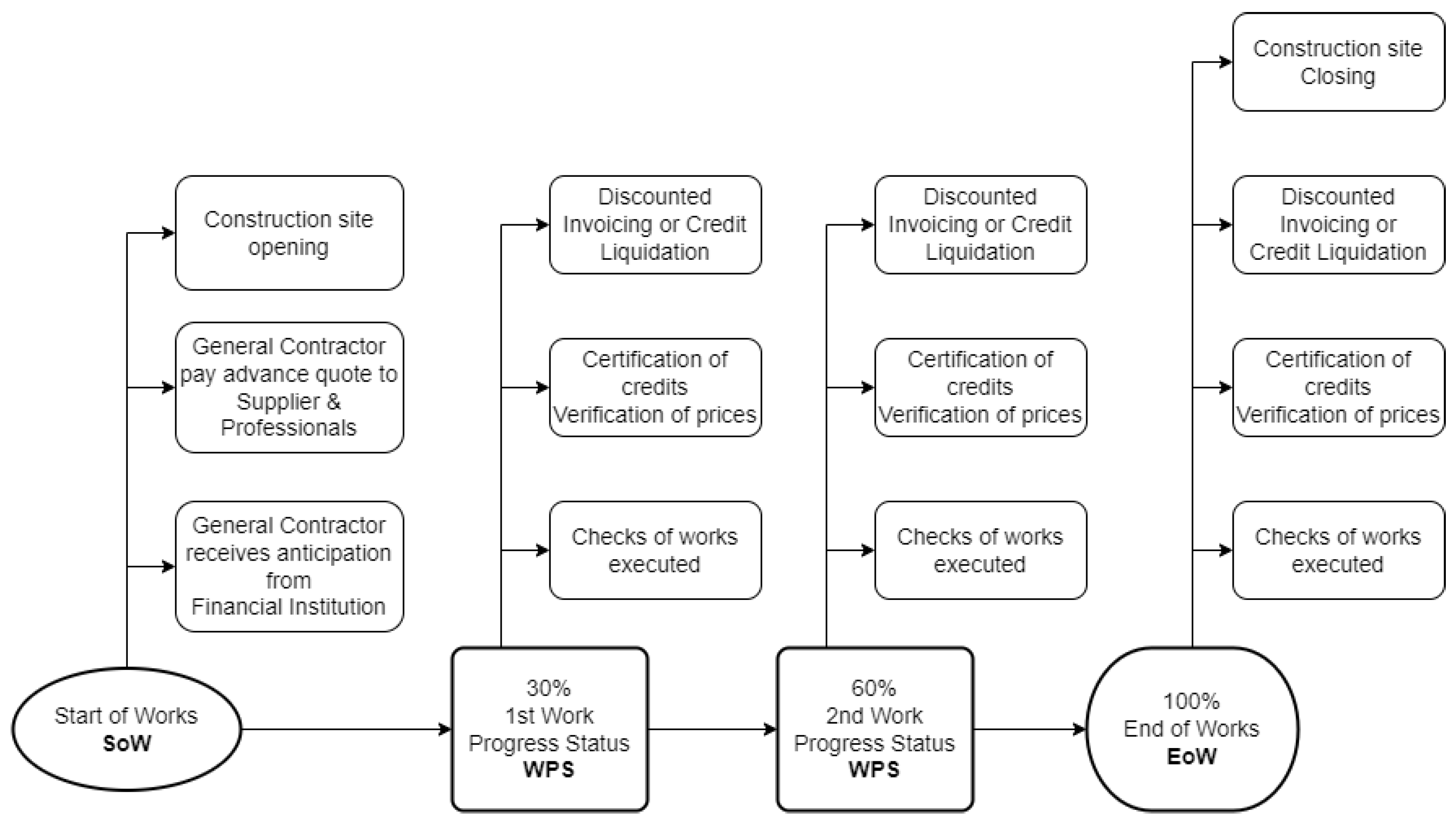

- Step 2—The Start of the Work (SoW) represents the final balance of the budget in the feasibility study. There are two scenarios: (i) the client who has the financial means, and can therefore afford, to wait until the end of the work to accrue the tax credit; (ii) the client who needs to finance the works with the accrual of the tax credit occurring in the steps during the execution of the works (Work Progress Status). This second option is the one that happens most of the time. The General Contractor usually manages to set up the bridge finance with banks/financial institutions.

- Step 3—Work Progress Status (WPS) is the accounting act functional to the payment of the work completed until that moment; it summarises all the works and all the supplies carried out from the beginning of the contract up to the day of issue. A copy of the lists of prices (Prezziari) is attached to the WPS amassimali.

- Step 4—Calculation of Deduction (CoD) The annual deduction is recoverable up to the limit of the personal gross tax (IRPEF). There are two possible scenarios: (i) if the client has sufficient gross tax to absorb the annual deduction, it will be recovered in the tax return; (ii) if the tax is insufficient, the client may opt for the discount on the invoice. For example, the supplier will request a contribution in the form of a discount on the invoice up to a maximum amount equal to the consideration. Then, the supplier recovers it by accruing a credit with the Tax Agency. This credit will be used for offsetting or assigned to third parties (i.e., the deduction due is transferred to third parties (banks, insurance companies, post office, intermediary, other companies, and individuals).

- Step 5—End of the Work (EoW) All the works are checked and tested, and a final balance of the intervention is drafted. Design Architects and Tax Auditors certify expenses and congruity on the technical and fiscal sides. Once all these activities are performed, the documents are deposited to the Italian Tax Agency, which may check them within seven years.

2.2. The Blockchain

2.3. Decentralised Autonomous Organisation (DAO)

3. Methodology

3.1. Constraints Knowledge Base

- Constraint 1. A specific agent (Director of Work) verifies compliance with the original schedule plan. Starting from a monthly forecast, the agent will be able to estimate the maturity of the WPS based on the previously mentioned criterion about the distribution of WPS. This translates into the fact that the possible states of the agents (workflow agent; see Section 5.4) are the following:or in brief . We can, at this point, formalise the following expressions for each value of the state variable:The Knowledge Base (KB) constraint can be, at this point, defined as follows:

- Constraint 2. Ensure token demand in Operator DAO aligns with Investor DAO forecasts. Based on previous WPSs, it is necessary to check financial expenditures and future needs at the closing of the WPS and thus verify that the expected demand for tokens in the Operator DAO () does not exceed that forecast in the Investor DAO (). So if is the demand for the token and is the forecast need for a token at time t, we must have:

- Constraint 3. Do not spend more than allocated. Electronic invoices will be the source of the flow of economic transactions; they allow a transparent view of all expenditures in the WPS, so all payments performed () by the workflow agent must not exceed the payments received () as anticipation for that state. Both must be made by traceable means. If is the state of the workflow agent at time t,

- Constraint 4. The homeowner may have at most two concessions per building unit to be refurbished. This translates in the condition that each client () may not have more than 2 workflow agents (w) opened:

- Constraint 5. Each project i must be certified by both technical and financial asseveration a raised by chartered engineers and accountants to grant the fairness of the expenses to the interventions listed in the WPS. Thus, if engineer j and accountant k are hired to asseverate project i:

- Constraint 6. The General Contractor (GC) may have more than one construction site assigned. The maximum limit is determined by the tax credit that may be handled or the value set in the Attestation Organisation Certification (AOC) he has in place (e.g., 1 million euros works for private buildings renovation category). So if the GC has j works of value each:

3.2. Agents Design: Actors, Roles, and Actions

- Customers are the various individuals (companies can not apply to this tax relief program) eligible for the Superbonus. They include natural persons and discuss expenses incurred for energy efficiency measures carried out on individual property units up to a maximum of two.

- Financial institutions (FIs) are the “qualified” entities acting as guarantors of the entire system composed by the DAOs. The FIs are banks or registered financial intermediaries or a company belonging to a banking group that is also registered, as are authorised insurance companies. Their role in our model is to manage both the Investor and Operator DAOs, thus minting, distributing, and burning tokens. They distribute tokens in the Operator DAO and pay back investors at the end of the program by redeeming Investor DAO tokens and giving back fiat money.

- General Contractor (GC) acts as a construction company, executing part of the works and as coordinator of other suppliers and Sub-contractors. It is also a proxy payer and coordinator for the Design Architects and professionals involved. It is in charge of managing all the paperwork involved in the Superbonus 110, like discounted invoicing and tax redemption and transfer processes; consequently, it is the subject that monitors all the payment processes. As the construction manager, it shall ascertain and record all events and works generating expenses as soon as they occur so that it can at any moment perform the following activities: (i) Issue the progress statements of the works within the deadline fixed in the tender documentation and in the contract, to prepare the paperwork for the advance payments. (ii) Monitor the progress of the works and promptly issue the necessary actions for their execution within the limits of the time and sums authorised. (iii) Communicate, as construction manager, to the financial institutions/investors in all the work progress states and interact with Tax Auditors and Design Architects to certify works and fiscal credits matured.

- Sub-contractor (SC) is the firm carrying out the works, interacts mainly with the General Contractor both for receiving working orders and for payment issues, all invoicing is done to the General Contractor and does not claim credits.

- Supplier is the entity that supplies materials. It deals with Sub-contractors or directly with GCs to procure materials for construction sites.

- Design Architect (DA) are designers such as engineers and architects. It is responsible for producing all the technical material (e.g., reports and drawings) necessary for the intervention to comply with the regulations in force. They assess the technical aspects of the project.

- Tax Auditor (TA). In the event of professional negligence or misapplication of the rules, the professionals and the technicians in charge of the asseverations and issuing the compliance certificates could be liable for the sums unduly used. In this regard, periodic checks are carried out by a Tax Auditor to ensure compliance with the constraints defined in the smart contracts. He also checks the results of financial transactions, including correct invoicing of expenses (Financial asseveration).

- Role 1: Compliance Control Agent (CCA). This role is connected with the activity of the Tax Auditor’s actor and comprises all the activities of checking and controlling fiscal and financial aspects. It also certifies all intermediate and final steps of credit maturation and liquidation, and it further controls that other professionals’ invoices are correct and adherent to price-list approval.

- Role 2: Construction Manager (CM).The General Contractor (GC) actor coordinates all administrative and operational activities on the construction site. This includes acting as a proxy for payments on behalf of the customer towards all players operating in the Superbonus process. This vital coordinating role must be considered to run all the processes smoothly.

- Role 3. Director of Work (DoW). The Design Architect (DA) actor has the task of controlling the expenditure connected with the execution of the works through the accurate and timely compilation of the accounting documents, which are public acts to all effects of the law. He also ascertains and registers the facts producing expenditure. The DoW (i) checks if the work is performed according to the project, (ii) transfers the measurements made to the accounting ledger to define the progress of the expenditure. He must pay special attention to guarantee compliance with the Superbonus Designer prescriptions, particularly the laying of materials. As a result, the Director of Works holds accountability for both the quality and outcomes of the work.

- Role 4. Checker Work (CW). During the work and at the end of the construction process, the Tax Auditor and Design Architect actors verify the work’s quality and issue a report to be sent to the investor. They also assess the financial and technical aspects of the works.

- Role 5. Suppliers Goods and Services (SG&S). The supplier, Sub-contractor, and designer architect actors are all the subjects that somehow supply materials and professional services to customers and General Contractors. The General Contractor pays suppliers and does not claim tax credits.

4. Scenarios

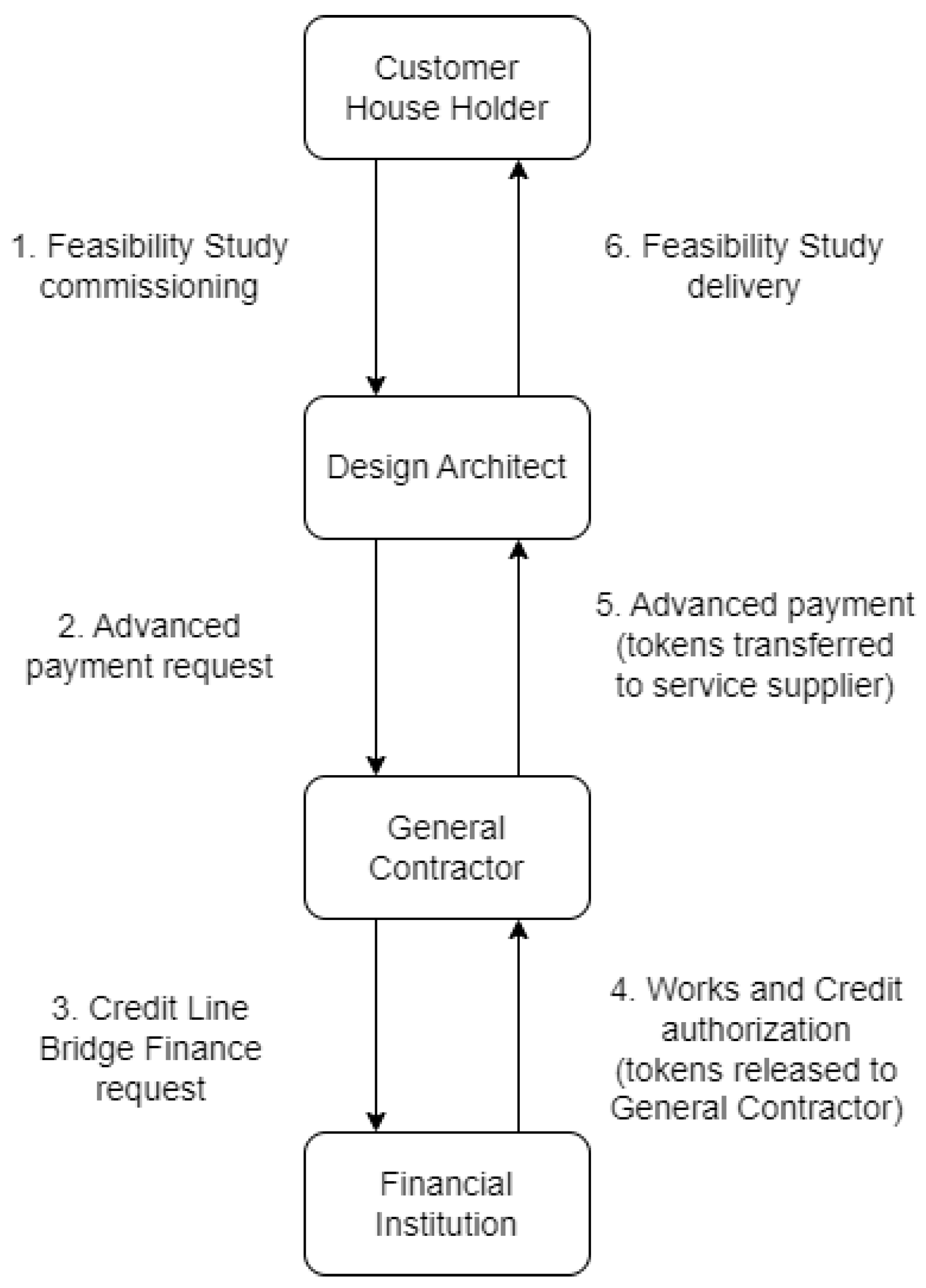

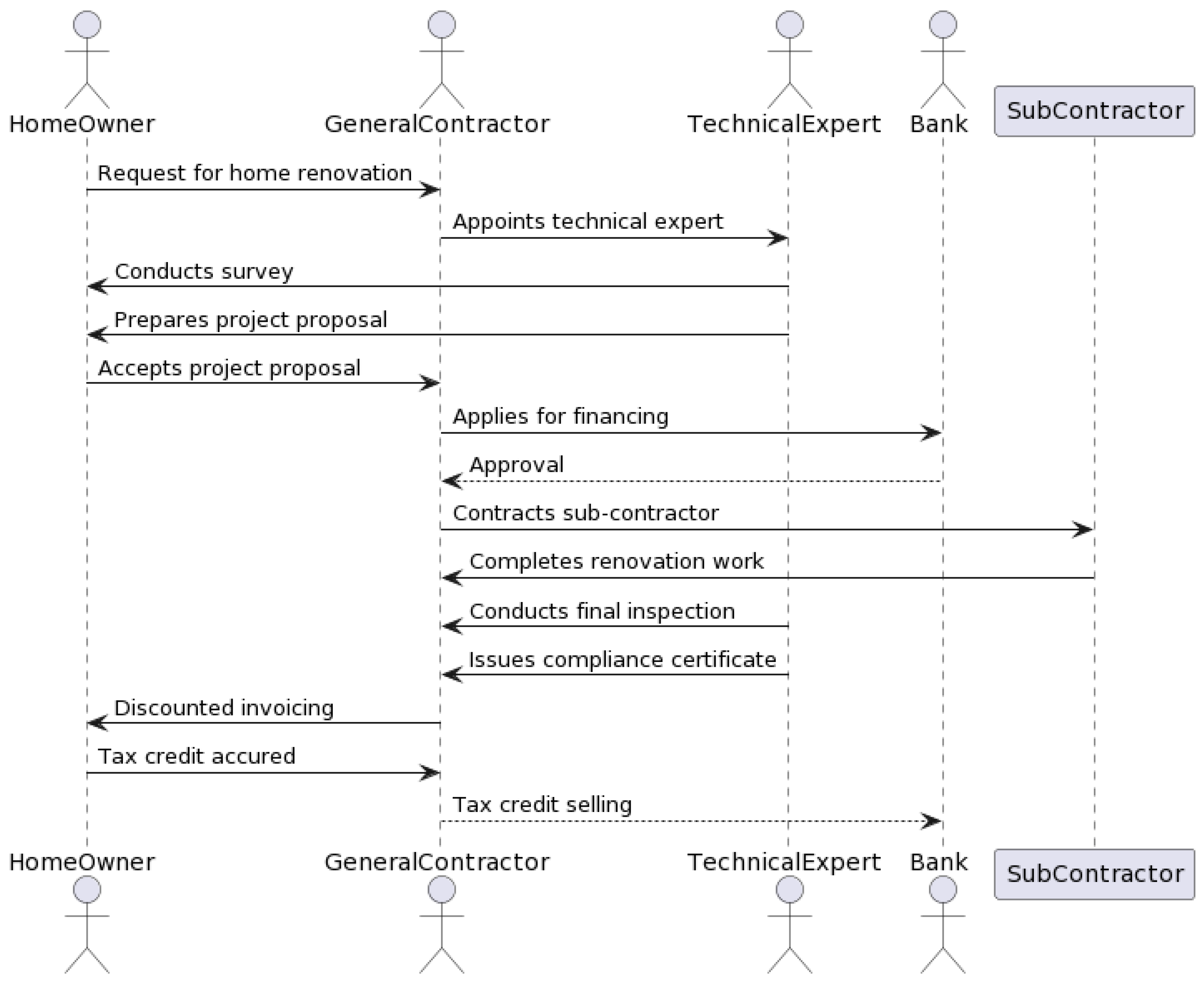

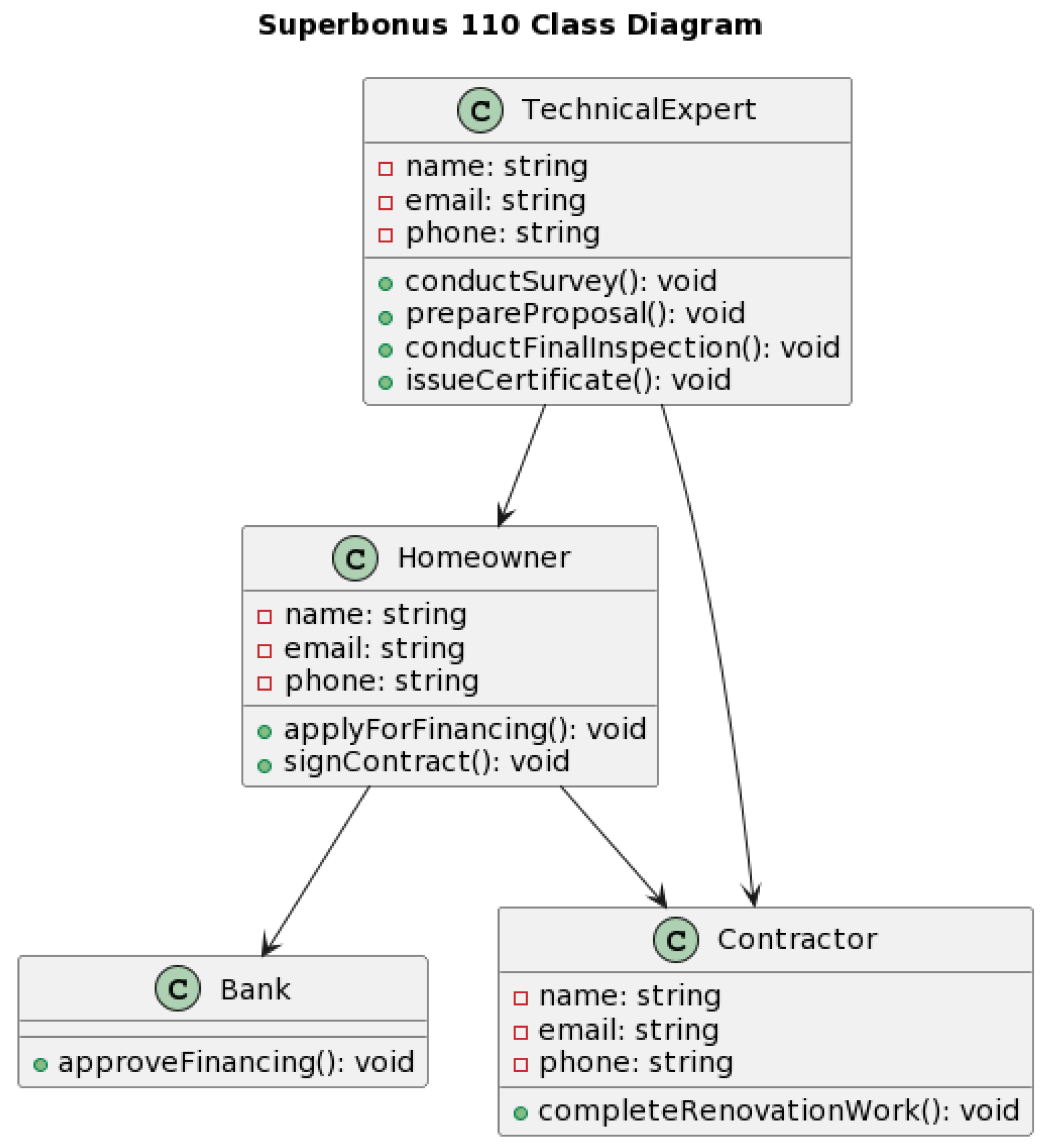

4.1. Scenario 1: Homeowner and Technical Expert

- Homeowner: The individual who owns the property that will undergo the energy efficiency and/or seismic renovation. The class has attributes such as name, email, phone, and methods such as applyForFinancing() and signContract().

- Technical Expert: The expert who conducts the energy efficiency survey and provides a project proposal for the renovation work. The technical expert class has attributes such as name, email, and phone, and methods such as conductSurvey(), prepareProposal(), conductFinalInspection(), and issueCertificate().

- Bank: The financial institution is financing the energy efficiency renovation. This class has a single method called approveFinancing().

- Contractor: The company or individual who completes the renovation work. The contractor class has attributes such as name, email, phone, and a single method called completeRenovationWork().

4.2. Scenario 2: Financial Institution, General Contractor and Investor

5. The Demonstrator

5.1. Software Architecture

- A Multi-agent System consisting of peer-to-peer connected nodes, onto which a decentralised and distributed application based on blockchain technology is implemented. It is deployed on Algorand (as outlined in Section 5.6). The system is designed using the Mesa Framework (https://mesa.readthedocs.io/stable/, accessed on 10 November 2024) an agent-based modelling framework based on Python. This framework provides a modular environment for system visualisation and testing.

- Two modules consisting of two DAOs based on the Aragon framework (see Section 5.3) used to develop the system’s business logic. Aragon makes it possible to transparently manage the communication between the dApp and the Ethereum Virtual Machine.

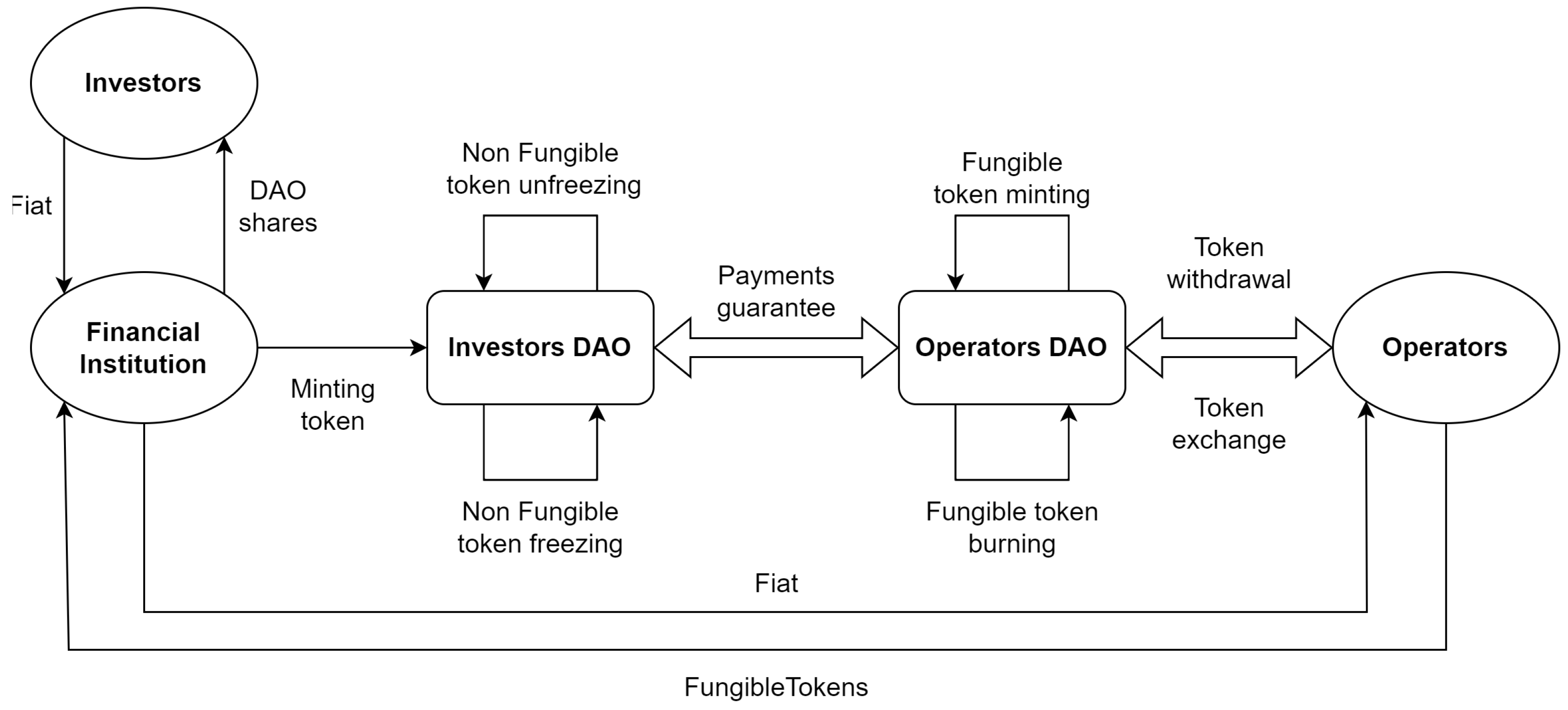

5.2. Secured Fiscal Credit DAOs

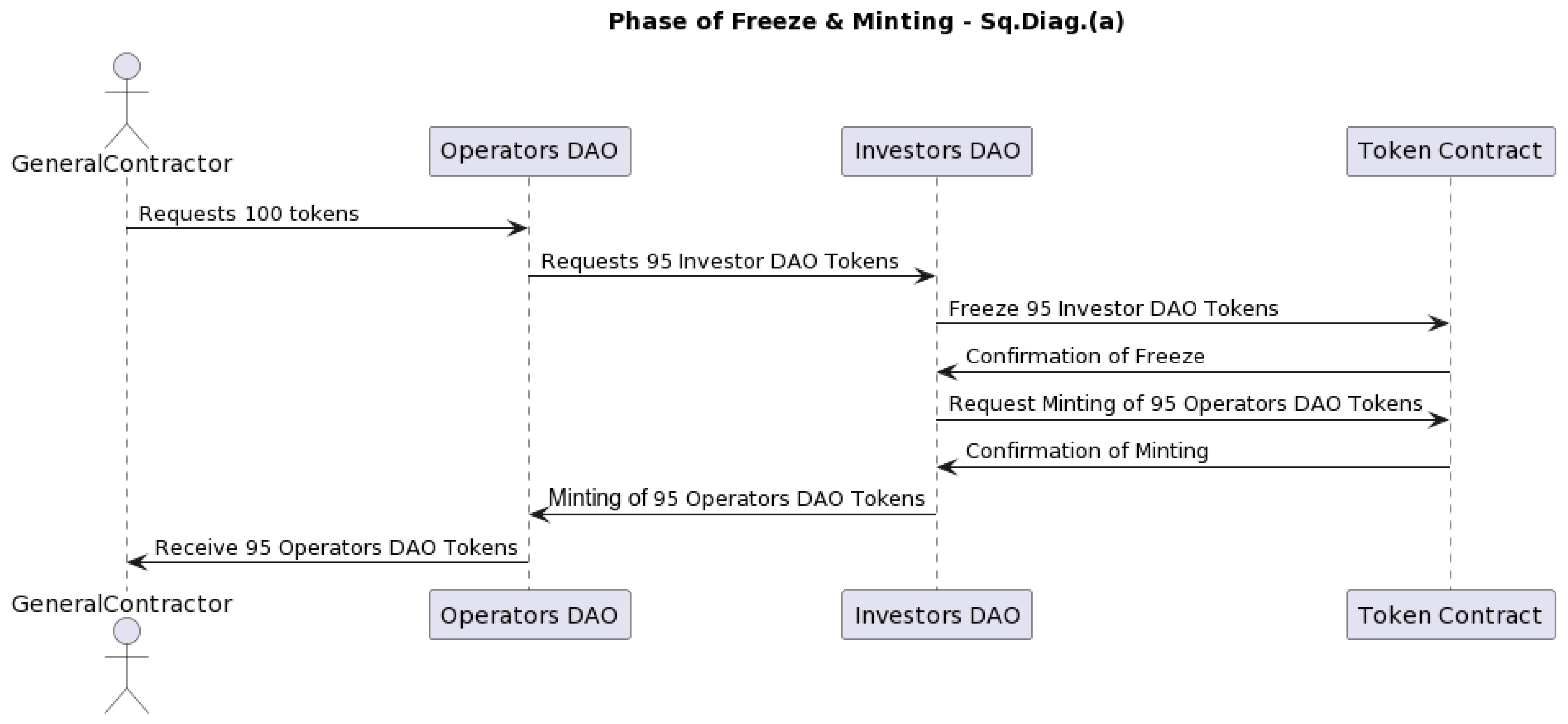

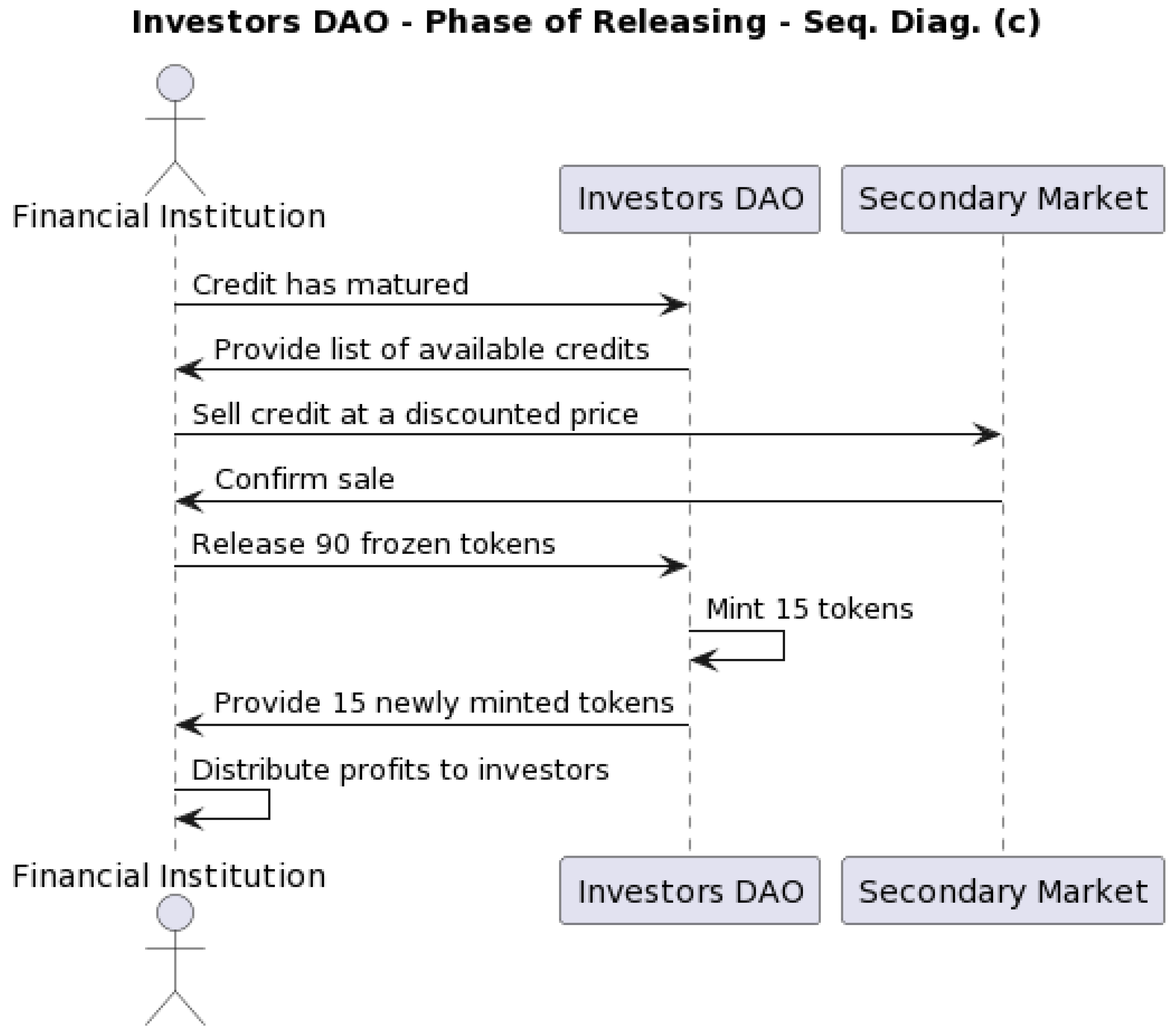

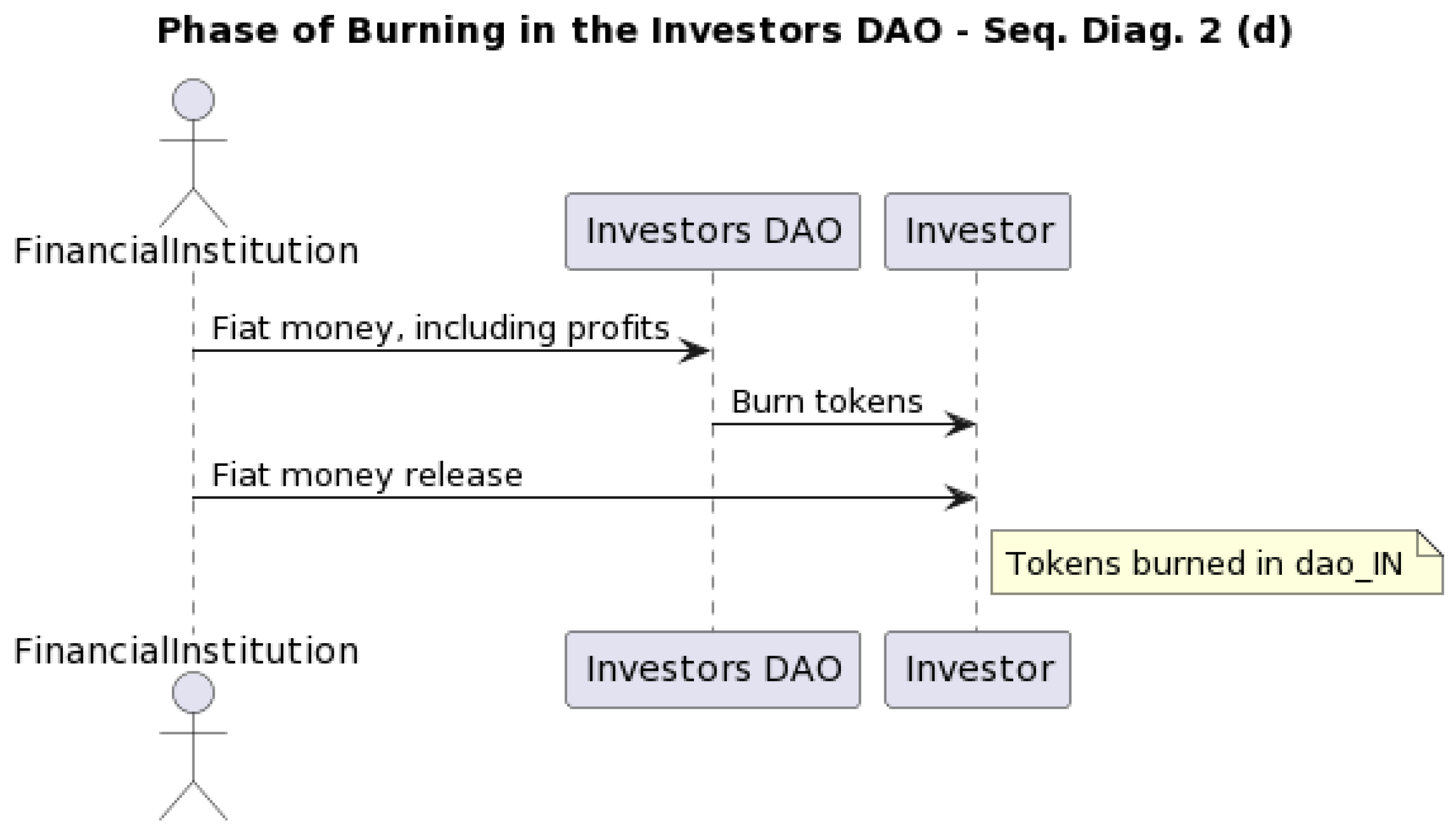

- Investor DAO: At the fund’s closing, the FI will convert the tokens accumulated in investors’ wallets into fiat and redistribute the shares to them, including dividends. On the one hand, the excess tokens will be generated by the disposals towards the Operator DAO, which considers 100 to be the amount of the work and will receive a lower share of tokens, for example, 95, to compensate for the financial costs.On the other hand, the 100 tokens will generate 110 tax credits that the FI will sell on secondary markets to obtain, for example, 105. Thus, the investors for an investment of 100 will receive 115 (see Section 4 on token burning and minting).

- Operator DAO: For example, the GC receives 100 tokens, of which 30 go to the supplier, 20 to the Design Architect, and 10 to the Tax Auditor for audits based on invoices they have issued. The GC can make a profit of 40 tokens for the operation. All these tokens are redeemable into fiat either upfront or after a determined time to consent of the financial institution to organise payments.

5.3. DAOs Development

5.4. Multi-Agent System Module

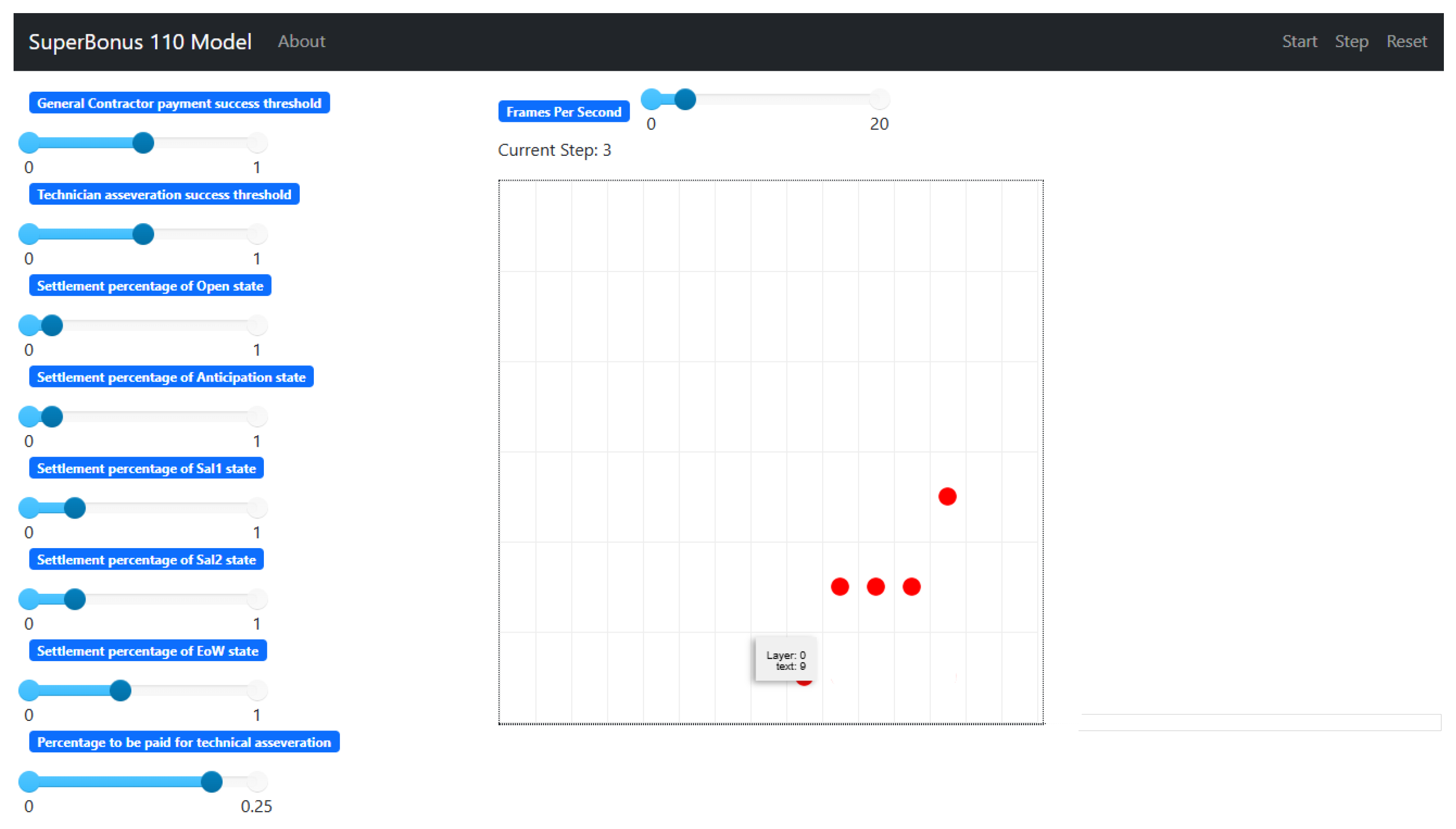

- The workflow agent represents each Superbonus 110% process opened. Once the instance is created, the agent will be on position ; as soon as the work is approved, it will move to position corresponding to the SoW state. It will move once the state passage condition is met (e.g., the related Tax Auditor agent approves the credit for that stage) until it reaches the final position . Once the paperwork is complete, the agent will be archived (possibly for five months). The agent logic thus evaluates if the represented paperwork is due to be moved to the next state, i.e., the technicians have asseverated the current SoW, and the General Contractor has paid the anticipation for the next state. When the agents have instantiated, the total value of the work is generated by a random procedure with a value comprised of 1 mln and ten mln microAlgos.To avoid excessive complexity, we model five pieces of paperwork for the demonstrator to handle, thus having five workflow agents. The logic is realised through a smart contract deployed on the Algorand testnet wallets of agents and is activated by opting into such a smart contract. Considering the current state of the workflow agent as , the last asseverated state as , and the previous paid as , the propositional logic notation for such a constraint evaluation is the following:The workflow agents also pay the technician agents once the state is successfully updated; this happens by sending between Algorand wallets the amount calculated as a percentage (adjustable from the specific home page slider) of the state value (adjustable again from relevant sliders); see Figure 12 on Section 5.5.

- The General Contractor agent has the function of approving, on the financial side, the evolution to the next step of the paperwork. It simulates the passage of state, generating a random number to be checked against a threshold configurable as an input parameter similar to the workflow agent’s procedure. If the approval is successful, the agent sends the amount due from their wallet on Algorand in anticipation of the next state to the related workflow agent. The amount is configurable, and the percentages of each state are set against the total value of the paperwork. To keep the system simple, we model a single General Contractor agent.

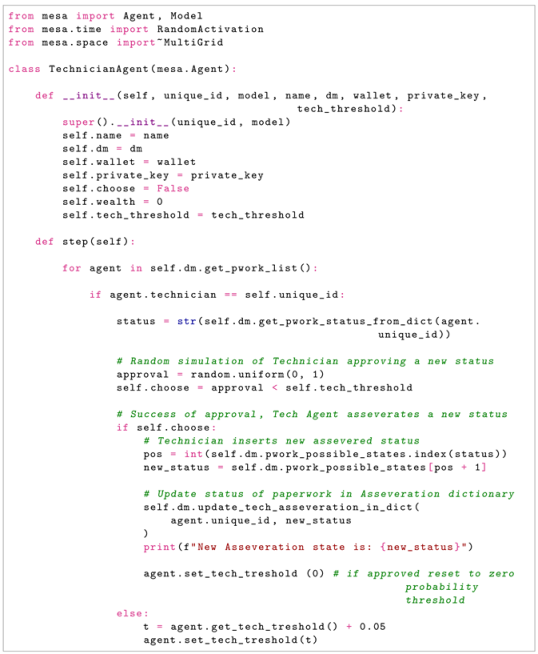

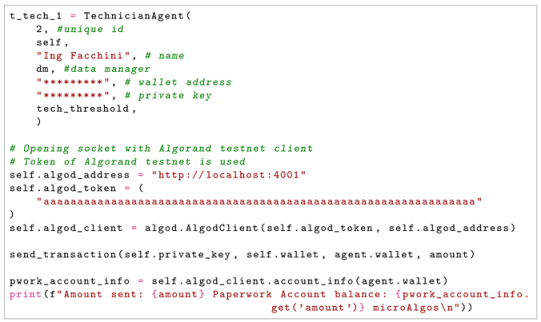

- Technical agent: This class merges the functionalities of both Design Architects and Tax Auditors with approvals randomly generated and checked against adjustable thresholds. In our simulator, we model two technician agents, each with an Algorand wallet, to obtain payments for asseverations.

- The financial agent represents the financial institution and acts as a sort of notary and banking entity, where all other General Contractor agents refer for funding approval, payment requests, and other Superbonus 110%-related financial issues. This agent also interacts with Communication Agents to perform all the token operations between the DAOs but will be modelled in the next version of the demonstrator.

- Client agents: Clients model the homeowners’ activating Superbonus 110% interventions, appointing the General Contractor and technicians executing all the relevant works and certifications required by law. Following the condominium assembly, the workflow is created, and the agents described above are assigned. It is not modelled in this demonstrator version, and the General Contractor and technicians assignment to workflow agents is hard coded.

- Property 1. [Workflow Agent] To increase the performance of the operative players of the Superbonus 110% environment, the workflow agent evaluates the performance of its suppliers. The penalties and rewards are based on parameters like request response time, tariff discounts, and respect for delivery deadlines. Thus, at each WPS step, the agent evaluates the bonus or malus of each supplier involved in its construction site, modifying their score. It also applies a token penalty to “bad” agents that can be used to reward “good” agents. Operators who are not performing well must increase their performance to avoid losing their reputation and money. Consider to be the historical average time for General Contractor GC to complete WPS states , the actual discount proposed for such a state, and the historical percentage of on-time WPS completed. We can calculate a weighted valueof such parameters for supplier and check it against a threshold limit value l to determine if a supplier is “good” or “bad”:

- Property 2. [Financial Agent] This functionality is a credit anomaly detector that checks anomalous credit transfers. The idea is to spot and evaluate possible fraud and misuse situations and prevent them from damaging customers, financial institutions, and operators. It enriches constraints 2, 3, and 4 of Section 3.1 and is realised through a more complex analysis of token movements between parties, such as too-fast token redemption, meaning works claimed could be fake. If General Contractor asks for a WPS credit redeem, having performed WPS states and in time , then we can spot the suspicious behaviour of ifwhere s is a suspicion rate percentage to be tuned with data from simulation (e.g., if , this means that claims performed in half the average time are considered suspicious).

5.5. MAS Framework and Implementation

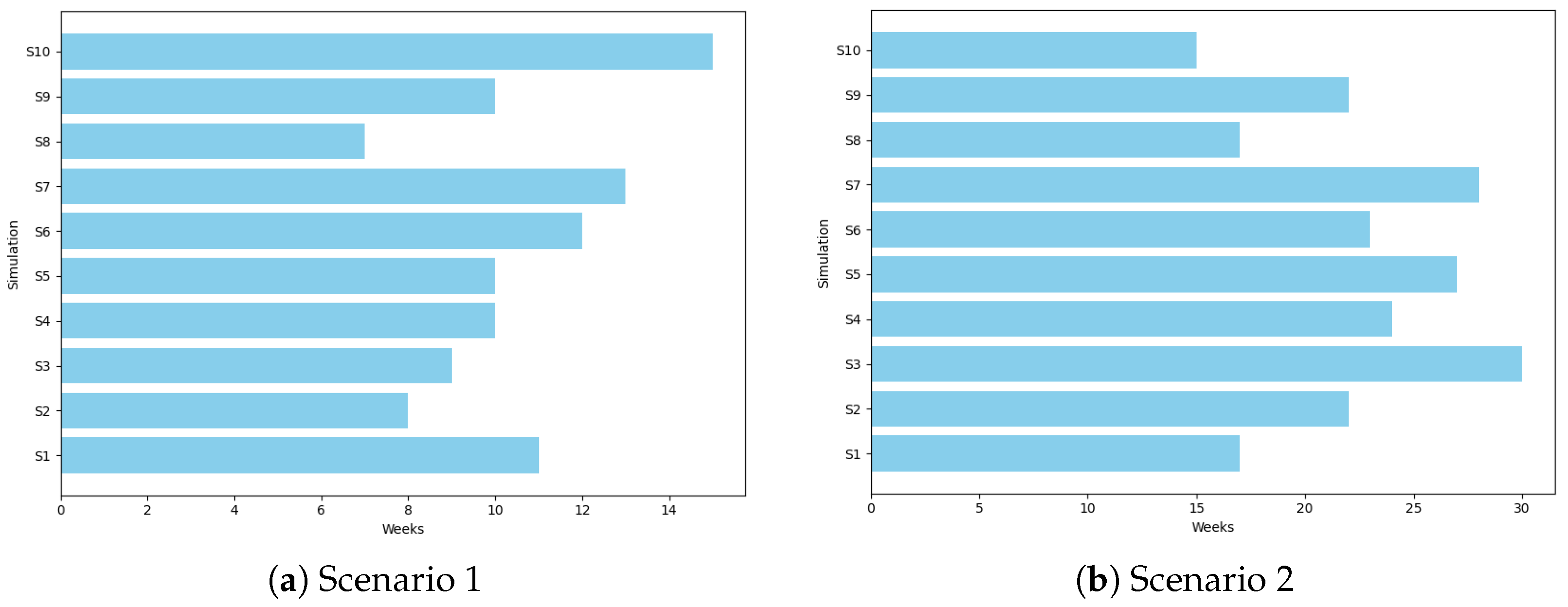

- Scenario 1. High GC approval and high technician asseveration success rates: This scenario examines the system’s behaviour under a high rate of both GC approval and technician asseveration for the submitted SALs. We simulate a 50% probability of approval for SALs in each cycle of the demonstrator. It is important to note that unapproved SALs are not rejected but remain pending and are carried over to the subsequent cycle. This introduces a time delay, mirroring real-world situations where approvals might be delayed due to factors such as the following:

- –

- Variations in local authority processing times;

- –

- The temporary unavailability of key personnel;

- –

- The need for additional documentation or clarifications.

As depicted in Figure 14a, high SAL approval rates result in a fluid workflow. State transitions occur with minimal delays, leading to an average project completion time (EoW: End of Work) of 10.3 weeks. - Scenario 2. Low GC approval and low technician asseveration success rates: This scenario simulates a less efficient approval process, reflecting potential bottlenecks stemming from contractor-side factors. We set a 25% approval probability per cycle but introduce delays to represent challenges such as the following:

- –

- Contractor-induced rework due to quality issues;

- –

- Delays in submitting required documentation by the contractor;

- –

- Resource constraints on the contractor’s end.

Figure 14b illustrates the impact of low SAL approval rates. The workflow progresses more slowly, with pronounced delays at various stages. Consequently, the average time to reach EoW increases to 23.9 weeks.

5.6. Blockchain Integration

5.6.1. Algorand Blockchain

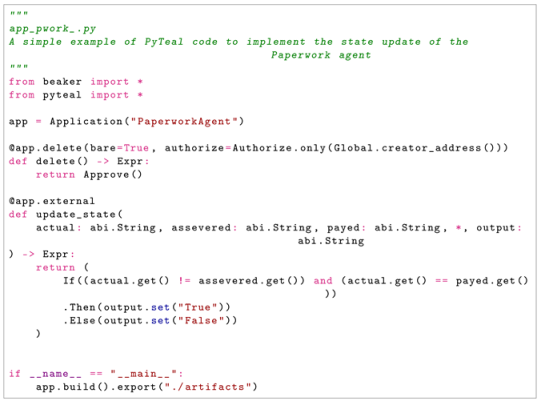

5.6.2. Implementation of Smart Contracts Using PyTeal

5.6.3. Setting Up and Running Simulations with MESA

5.6.4. Agent-Blockchain Connectivity

6. Conclusions

7. Authors Disclaimer

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| DAO | Decentralised Autonomous Organisation |

| MAS | Multi-agent System |

| SFCM | Secured Fiscal Credits Model |

| AI | Artificial Intelligence |

| FS | Feasibility Study |

| SoW | Start of the Work |

| WPS | Work Progress Status |

| CoD | Calculation of Deduction |

| EoW | End of Work |

| DLT | Distributed Ledger Technology |

| GC | General Contractor |

| SC | Sub-contractor |

| DA | Design Architect |

| TA | Tax Auditor |

| CCA | Compliance Control Agent |

| CM | Construction Manager |

| DoW | Director of Work |

| CW | Checker Work |

| SG&S | Suppliers Goods and Services |

| NFT | Non-Fungible Token |

| ANT | Aragon Network Token |

References

- Romano, V. Euractiv Superbonus 110 Description. 2022. Available online: http://www.euractiv.com/section/energy/news/italys-feted-superbonus-for-building-renovation-comes-under-scrutiny/ (accessed on 1 November 2024).

- Goertzel, B.; Iklé, M.; Potapov, A.; Ponomaryov, D. Artificial General Intelligence: 15th International Conference, AGI 2022, Seattle, WA, USA, 19–22 August 2022, Proceedings; Springer Nature: Berlin/Heidelberg, Germany, 2023; Volume 13539. [Google Scholar]

- Dyoub, A.; Costantini, S.; Lisi, F.A.; Letteri, I. Ethical Monitoring and Evaluation of Dialogues with a MAS. In Proceedings of the 36th Italian Conference on Computational Logic, Parma, Italy, 7–9 September 2021; CEUR Workshop Proceedings. Monica, S., Bergenti, F., Eds.; CEUR-WS.org, 2001. Volume 3002, pp. 158–172. [Google Scholar]

- Dyoub, A.; Costantini, S.; Lisi, F.A.; Gasperis, G.D. Demo Paper: Monitoring and Evaluation of Ethical Behavior in Dialog Systems. In Proceedings of the Advances in Practical Applications of Agents, Multi-Agent Systems, and Trustworthiness. The PAAMS Collection—18th International Conference, PAAMS 2020, L’Aquila, Italy, 7–9 October 2020, Proceedings; Lecture Notes in Computer Science; Demazeau, Y., Holvoet, T., Corchado, J.M., Costantini, S., Eds.; Springer: Cham, Switzerland, 2020; Volume 12092, pp. 403–407. [Google Scholar] [CrossRef]

- De Gasperis, G.; Facchini, S.D.; Susco, A. Demonstrator of Decentralized Autonomous Organizations for Tax Credit’s Tracking. In Proceedings of the Advances in Practical Applications of Agents, Multi-Agent Systems, and Complex Systems Simulation. The PAAMS Collection; Dignum, F., Mathieu, P., Corchado, J.M., De La Prieta, F., Eds.; Springer: Cham, Switzerland, 2022; pp. 480–486. [Google Scholar]

- Facchini, S.D. Decentralized Autonomous Organizations and Multi-agent Systems for Artificial Intelligence Applications and Data Analysis. In Proceedings of the Thirty-First International Joint Conference on Artificial Intelligence, IJCAI-22, Vienna, Austria, 23–29 July 2022; Doctoral Consortium. Raedt, L.D., Ed.; International Joint Conferences on Artificial Intelligence Organization: Montreal, Canada, 2022; pp. 5851–5852. [Google Scholar] [CrossRef]

- Huerto-Cardenas, H.E.; Aste, N.; Buzzetti, M.; Del Pero, C.; Leonforte, F.; Miglioli, A. Examining the role of the superbonus 110% incentive in Italy through analyses of two residential buildings. E3S Web Conf. 2024, 546, 2007. [Google Scholar] [CrossRef]

- Codogno, L. Italy’s Superbonus 110%: Messing Up with Demand Stimulus and the Need to Reinvent Fiscal Policy; IMK Studies 93-2024; IMK at the Hans Boeckler Foundation, Macroeconomic Policy Institute: Düsseldorf, Germany, 2024. [Google Scholar]

- Karakostas, D.; Kiayias, A. Filling the Tax Gap via Programmable Money. In Proceedings of the Data Privacy Management, Cryptocurrencies and Blockchain Technology; Garcia-Alfaro, J., Muñoz-Tapia, J.L., Navarro-Arribas, G., Soriano, M., Eds.; Springer: Cham, Switzerland, 2022; pp. 281–288. [Google Scholar] [CrossRef]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. 2008. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 1 July 2015).

- Gervais, A.; Karame, G.O.; Wüst, K.; Glykantzis, V.; Ritzdorf, H.; Capkun, S. On the Security and Performance of Proof of Work Blockchains. In Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security, New York, NY, USA, 24–28 October 2016; CCS ’16. pp. 3–16. [Google Scholar] [CrossRef]

- Catalini, C.; Gans, J.S. Some Simple Economics of the Blockchain. Commun. ACM 2020, 63, 80–90. [Google Scholar] [CrossRef]

- Voshmgir, S.; Zargham, M. Foundations of Cryptoeconomic Systems. Working Paper Series/Institute for Cryptoeconomics/Interdisciplinary Research 1; WU Vienna University of Economics and Business: Vienna, Austria, 2020. [Google Scholar]

- Buterin, V. A next-generation smart contract and decentralized application platform. White Pap. 2014, 3, 2-1. [Google Scholar]

- Baninemeh, E.; Farshidi, S.; Jansen, S. A decision model for decentralized autonomous organization platform selection: Three industry case studies. Blockchain Res. Appl. 2023, 4, 100127. [Google Scholar] [CrossRef]

- Farshidi, S.; Jansen, S.; de Jong, R.; Brinkkemper, S. A Decision Support System for Cloud Service Provider Selection Problem in Software Producing Organizations. In Proceedings of the 2018 IEEE 20th Conference on Business Informatics (CBI), Vienna, Austria, 11–13 July 2018; Volume 01, pp. 139–148. [Google Scholar] [CrossRef]

- Dilger, W. Decentralized autonomous organization of the intelligent home according to the principle of the immune system. In Proceedings of the 1997 IEEE International Conference on Systems, Man, and Cybernetics. Computational Cybernetics and Simulation, Orlando, FL, USA, 12–15 October 1997; 1, pp. 351–356. [Google Scholar] [CrossRef]

- Kypriotaki, K.; Zamani, E.; Giaglis, G. From Bitcoin to Decentralized Autonomous Corporations - Extending the Application Scope of Decentralized Peer-to-Peer Networks and Blockchains. In Proceedings of the 17th International Conference on Enterprise Information Systems—Volume 3, Barcelona, Spain, 27–30 April 2015; ICEIS, INSTICC. SciTePress: Setúbal Municipality, Portugal, 2015; pp. 284–290. [Google Scholar] [CrossRef]

- Sun, X.; Stasinakis, C.; Sermpinis, G. Decentralization illusion in DeFi: Evidence from MakerDAO. arXiv 2022, arXiv:2203.16612. [Google Scholar] [CrossRef]

- Ozkaya, M. Analysing UML-based software modelling languages. J. Aeronaut. Space Technol. 2018, 11, 119–134. [Google Scholar]

- Masad, D.; Kazil, J. MESA: An agent-based modeling framework. In Proceedings of the 14th PYTHON in Science Conference, Citeseer, Austin, TX, USA, 6–12 July 2015; Volume 2015, pp. 53–60. [Google Scholar]

- De Gasperis, G.; Facchini, S.D.; Letteri, I. Leveraging Multi-Agent Systems and Decentralised Autonomous Organisations for Tax Credit Tracking: A Case Study of the Superbonus 110% in Italy. Available online: https://zenodo.org/records/13742335 (accessed on 10 November 2024).

- Chohan, U. The Decentralized Autonomous Organization and Governance Issues. SSRN Electron. J. 2017. [Google Scholar] [CrossRef]

- Bellini, E.; Iraqi, Y.; Damiani, E. Blockchain-Based Distributed Trust and Reputation Management Systems: A Survey. IEEE Access 2020, 8, 21127–21151. [Google Scholar] [CrossRef]

- Huang, Y.; Zhang, T.; Fang, S.; Tan, Y. Deep Smart Contract Intent Detection. arXiv 2022, arXiv:2211.10724. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| DAO | Actor | Actions |

|---|---|---|

| Investors | Investor | Invest money to buy credits and benefits from its selling |

| Investors Operators | Financial institution | Banks that buy/sell credits and lend money to Operators |

| Investors Operators | Customer | House owner sells/transfers tax credits from works |

| Operators | General Contractor | Manages work, obtains credits from customers, sells to financial institutions |

| Operators | Sub-contractor | Hired and paid by General Contractor |

| Operators | Supplier | Hired and paid by General Contractor |

| Operators | Design Architect | Hired and paid by General Contractor |

| Operators | Tax Auditor | Hired and paid by General Contractor |

| Role | Actor | Assignments |

|---|---|---|

| CCA | TA | Check and control fiscal and financial aspects |

| CM | GC | Supervises activities on the construction site |

| DoW | DA | Control expenditures of the works |

| CW | TA and DA | Check technical and administrative compliance |

| SG&S | Supplier, Sub contractor, DA | Supply materials and professional services |

| Scenario | GC Payment | Tech Asseveration | Open | ANT | SAL1 | SAL2 | EOW | Tech Fee |

|---|---|---|---|---|---|---|---|---|

| 1 | 50% | 50% | 10% | 10% | 30% | 40% | 10% | 15% |

| 2 | 25% | 25% | 10% | 10% | 30% | 40% | 10% | 15% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

De Gasperis, G.; Facchini, S.D.; Letteri, I. Leveraging Multi-Agent Systems and Decentralised Autonomous Organisations for Tax Credit Tracking: A Case Study of the Superbonus 110% in Italy. Appl. Sci. 2024, 14, 10622. https://doi.org/10.3390/app142210622

De Gasperis G, Facchini SD, Letteri I. Leveraging Multi-Agent Systems and Decentralised Autonomous Organisations for Tax Credit Tracking: A Case Study of the Superbonus 110% in Italy. Applied Sciences. 2024; 14(22):10622. https://doi.org/10.3390/app142210622

Chicago/Turabian StyleDe Gasperis, Giovanni, Sante Dino Facchini, and Ivan Letteri. 2024. "Leveraging Multi-Agent Systems and Decentralised Autonomous Organisations for Tax Credit Tracking: A Case Study of the Superbonus 110% in Italy" Applied Sciences 14, no. 22: 10622. https://doi.org/10.3390/app142210622

APA StyleDe Gasperis, G., Facchini, S. D., & Letteri, I. (2024). Leveraging Multi-Agent Systems and Decentralised Autonomous Organisations for Tax Credit Tracking: A Case Study of the Superbonus 110% in Italy. Applied Sciences, 14(22), 10622. https://doi.org/10.3390/app142210622