Evolutionary Game Analysis of Copyright Protection for NFT Digital Works Considering Collusive Behavior

Abstract

:1. Introduction

- Model the digital copyright protection issue in the NFT market as a non-cooperative game between three groups: digital content creators; NFT service platforms; and government regulatory authorities;

- Use evolutionary game theory to derive the replication dynamics of these three groups, analyze the Nash equilibrium solution of the proposed evolutionary game model, and determine the conditions for the asymptotic stability of the equilibrium solution;

- Validate our theoretical results using three-dimensional phase diagrams with state combinations and draw evolution diagrams to confirm the presence of ESS in the proposed game;

- Through digital simulation, analyze and discuss the impact of sales revenue, penalties and rewards, speculation costs, collusion costs, administrative penalties, and other factors on ESS.

2. The Related Literature

2.1. NFTs and Traditional Tokens

2.2. Infringement of NFTs

2.3. Application of EGT in Copyright Protection

3. Model Assumptions and Construction

3.1. Model Assumptions

- (1)

- The NFT digital work copyright protection system involves three populations: digital content creators; NFT service platforms; and government regulatory authorities. All players involved exhibit bounded rationality, and their strategic choices tend to converge to stable strategies over time;

- (2)

- The strategy space available for digital content creators is α = (α1, α2) = (original, non-original/fake). In the population of creators, the proportion of entities who adopt the α1 strategy is x, and the proportion of entities who adopt the α2 strategy is (1 − x); x ∈ [0, 1]. The strategy space of NFT digital publishing platforms is β = (β1, β2) = (fair detection, collusive detection). In the population of platforms, the proportion of entities who adopt the β1 strategy is y, and the proportion of entities who adopt the β2 strategy is (1 − y); y ∈ [0, 1]. The strategy selection space of regulators is γ = (γ1, γ2) = (strict supervision, loose supervision). In the population of regulators, the proportion of entities who adopt the γ1 strategy is z, and the proportion of entities who adopt the γ2 strategy is (1 − z); z ∈ [0, 1];

- (3)

- The sales revenue of NFT is Rc. The cost of designing and producing original digital works is Cco. The cost of producing non-original digital works is Ccf, Cco > Ccf. Original digital content can definitely pass similarity detection. The non-original digital content can only pass similarity detection when the NFT service platform conducts collusion detection, and the cost of collusion is Ccfr, Ccfr < (Cco − Ccf). Meanwhile, the speculative act of producing non-original works will incur speculative costs Ccfs, mainly including expenses on information search, false advertising, and others. The production activities of creators are aimed at economic benefits and require initial parameters to meet Rc > Cco > Ccf + Ccfr + Ccfs;

- (4)

- Digital content works can only be sold on the blockchain after successfully passing similarity detection, and the detection revenue is RP. When digital content is non-original, if the service platform conducts fair detection, it is not qualified. If the platform conducts collusion detection, it reaches collusion with the infringer and helps the infringing work obtain the online license. The speculative cost of conducting collusion detection for the platform is Cp, including expenses on modifying detection reports, strengthening information security management, and others. The activities of platforms are driven by economic benefits and require initial parameters to meet Ccfr > Cp;

- (5)

- When regulators enforce strict supervision, creators of non-original works will be fined with Fc; platforms conducting collusion detection will be fined with Fp; platforms conducting fair detection will receive a reward MP, and the cost of strict supervision is Cg. When the regulators enforce loose supervision, they do not impose rewards and punishments on market entities;

- (6)

- The benefits brought by the production of original digital content to society are Rg, including providing innovative development momentum for society, promoting the development of the digital economy, and strengthening the protection of intellectual property rights. When collusion is achieved between creators and platforms, the infringing works will flow into the market. In order to maintain market stability and crack down on piracy, the regulators spend cost Dg. When regulators adopt the loose supervision, they will receive an administrative penalty of Tg from the superior government; Tg > Cg.

3.2. Model Construction

4. Model Stability Analysis

4.1. Analysis of Creators

= Rc − Cco

= y(Ccfr − Rc) − zFc − Ccf − Ccfr − Ccfs + Rc

= x(1 − x)((Rc − Ccfr)y + zFc + Ccf + Ccfr + Ccfs − Cco)

- (1)

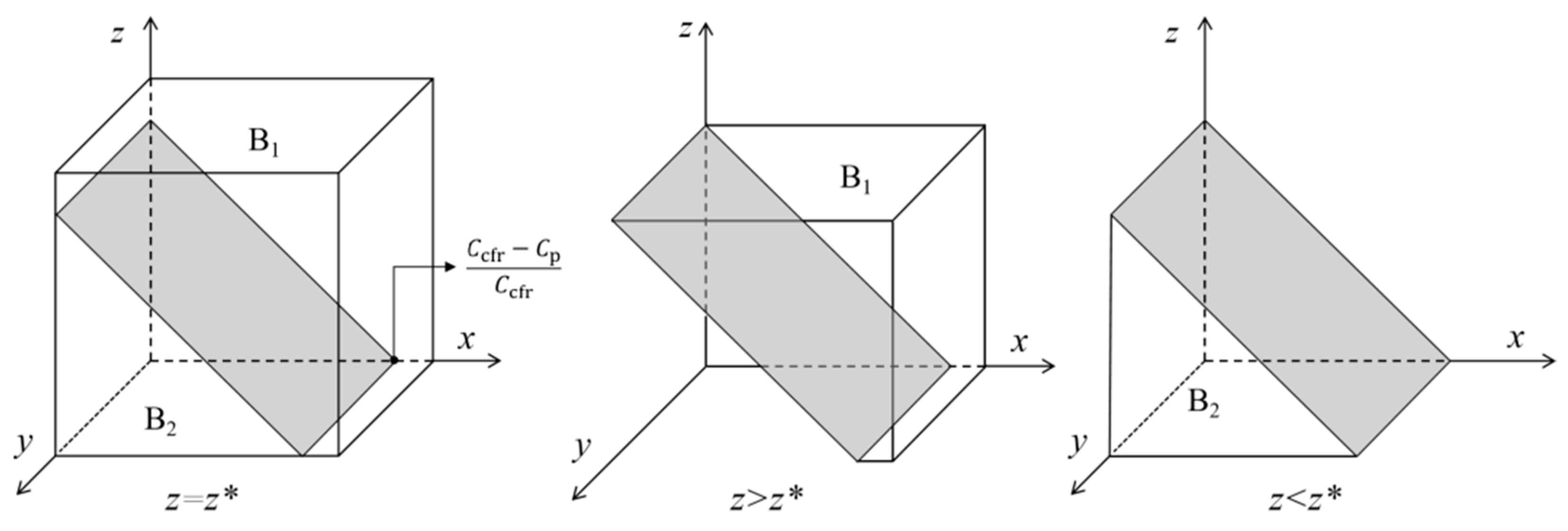

- When y = (−zFc − Ccf − Ccfr − Ccfs + Cco)/(Rc − Ccfr) = y*, there are G(y) = 0, and F(x) ≡ 0; the digital content creator’s choice of any proportion of original strategy is stable strategy, meaning that their strategic choice will not change with the passage of time;

- (2)

- Due to G(y) being a monotonically increasing function, when y < y*, there are G(y) < 0, F′(1) > 0, and F′(0) < 0; therefore, x = 0 is the ESS of the digital content creator. When y > y*, there are G(y) > 0, F′(1) < 0, and F′(0) > 0; therefore, x = 1 is ESS of the digital content creator.

4.2. Analysis of Platforms

= zMp + RP

= − xCcfr − zFp + Ccfr − Cp + RP

= y(1 − y)(xCcfr + z(Fp + Mp) − Ccfr + Cp)

- (1)

- When z = ((1 − x)Ccfr − Cp)/(Fp + Mp) = z*, there are H(z) = 0, and F(y) ≡ 0; the NFT publishing platform’s choice of any proportion of fair detection strategy is stable strategy;

- (2)

- Due to H(z) being a monotonically increasing function, when z < z*, there are H(z) < 0, F′(1) > 0, and F′(0) < 0; therefore, y = 0 is the ESS of the NFT publishing platform. When z > z*, there are H(z) > 0, F′(1) < 0, and F′(0) > 0; therefore, y = 1 is the ESS of the NFT publishing platform.

4.3. Analysis of Regulators

= x(Dg − Fc + Rg) + y(Dg − Fp − Mp) − xyDg − Cg − Dg + Fc + Fp

= x(Dg + Rg + Tg) + y(Dg + Tg) + xy(−Dg − Tg) − Dg − Tg

= z(1 − z)(x(−Fc − Tg) + y(−Fp − Mp − Tg) + xyTg − Cg + Fc + Fp + Tg)

- (1)

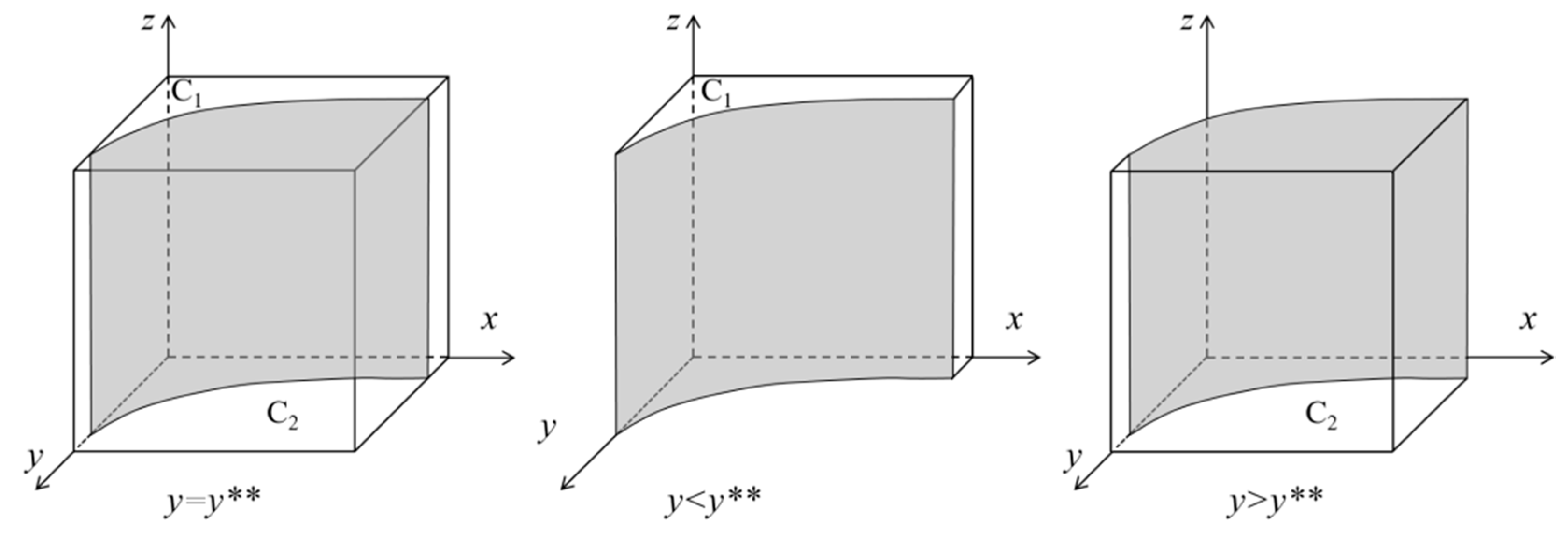

- When y = (−Cg + Fc + Fp + Tg − x(Fc + Tg))/(Fp + Mp + Tg − xTg) = y**, there are J(y) = 0, and F(z) ≡ 0, the regulator’s choice of any proportion of strict strategy is stable strategy;

- (2)

- Due to J(y) being a monotonically decreasing function, when y < y**, there are J(y) > 0, F′(1) < 0, and F′(0) > 0; therefore, z = 1 is the ESS. When y > y**, there are J(y) < 0, F′(1) > 0, and F′(0) < 0; therefore, z = 0 is the ESS of the NFT publishing platform.

4.4. Analysis of System

5. Model Simulation Analysis

5.1. Evolution Path Simulation

5.2. Parameter Simulation

- (1)

- Sales Revenue. Setting Rc = 100, Rc = 150, and Rc = 200, the system evolution simulation results are shown in Figure 6. The growth of NFT sales revenue can accelerate the evolution of digital content creators toward original strategy. With the increase in Rc, the probability of digital content creation choosing the original strategy increases, and the probability of the regulators choosing strict supervision decreases. Therefore, while the regulators strictly control the price of NFT to avoid a bubble economy, they also must strengthen the quality supervision of NFT and appropriately relax price controls on some high-quality works;

- (2)

- Collusive Costs. Setting Ccfr = 10, Ccfr = 30, and Ccfr = 50, the system evolution simulation results are shown in Figure 7. Figure 7 indicates that as the collusive costs of Ccfr increase, the probability of creators choosing the original strategy increases, and the probability of NFT service platforms choosing fair detection decreases. At this point, regulators can increase collusive costs by increasing media disclosure and cultivating copyright awareness of creators and consumers to increase the probability of producing original digital content;

- (3)

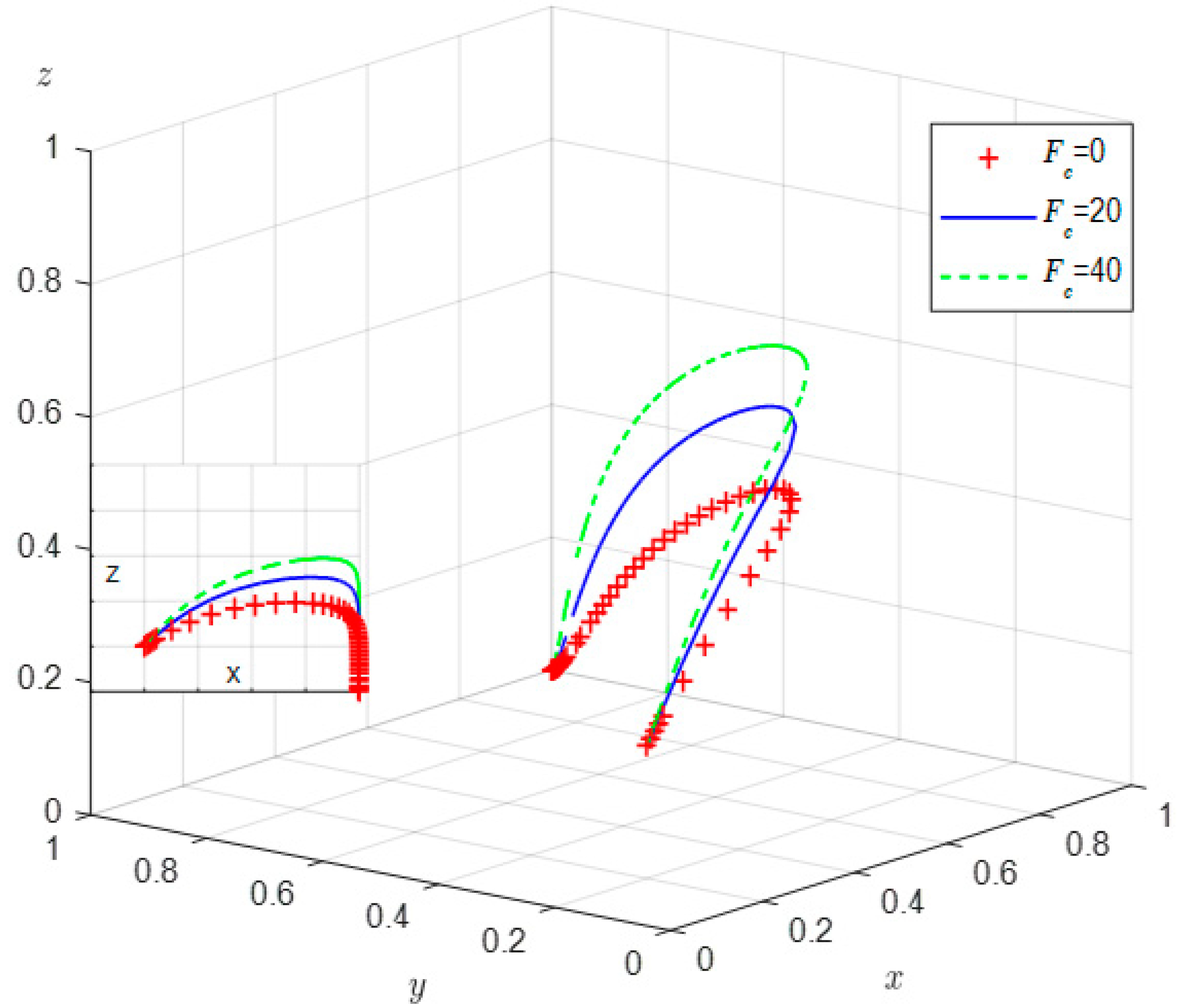

- Fines Borne By Creators. Setting Fc = 0, Fc = 20, and Fc = 40, the system evolution simulation results are shown in Figure 8. Figure 8 shows that the probability of creators choosing the original strategy increases with the increase in the fines Fc. Before the probability of digital content, creators choosing original strategies evolve to 1, and the probability of strict supervision increases with the increase in Fc. After the probability of digital content producers choosing original strategies evolves to 1, the probability of strict supervision gradually decreases and eventually stabilizes at 0;

- (4)

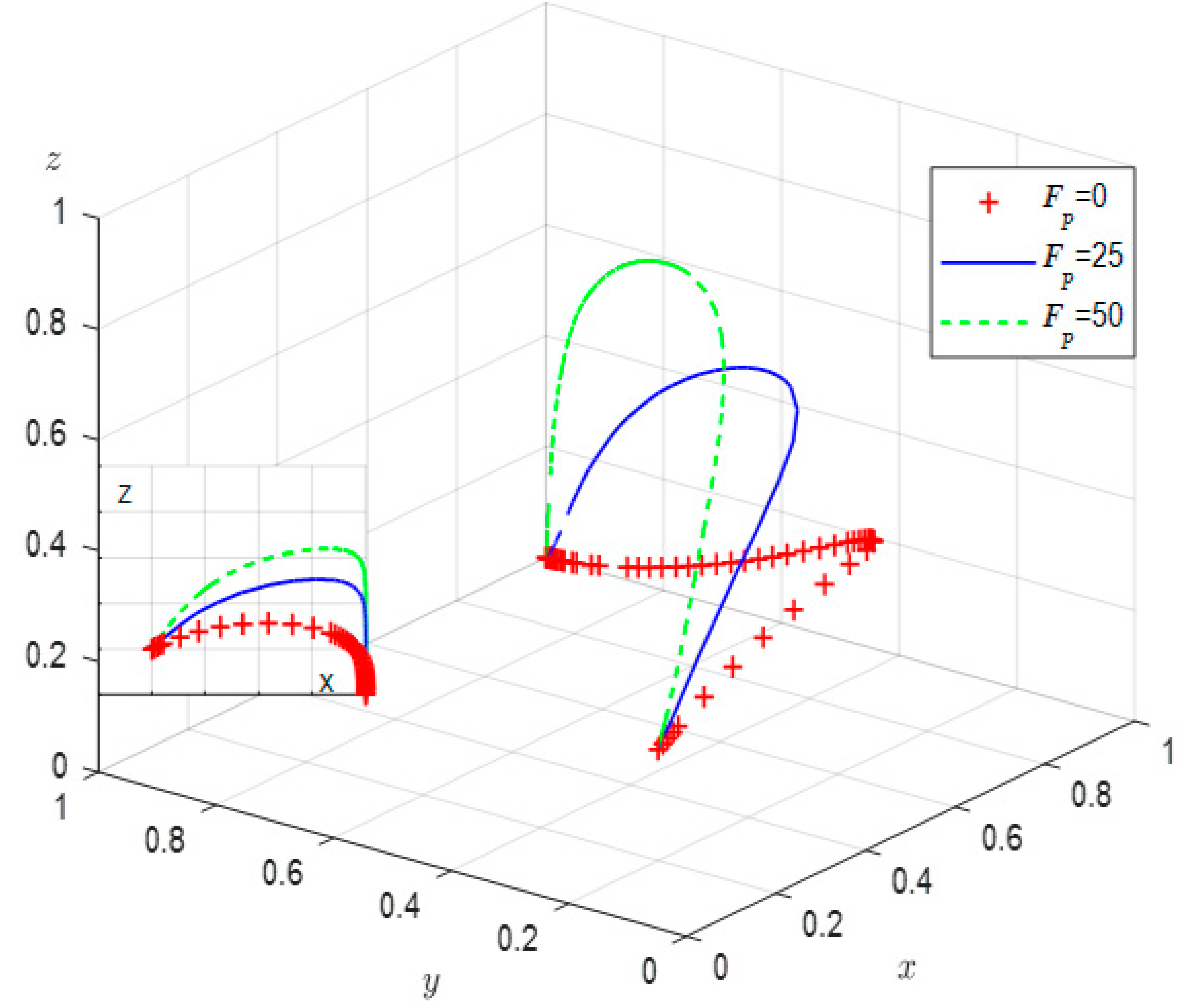

- Fines Borne By Platforms. Setting Fp = 0, Fp = 25, and Fp = 50, the system evolution simulation results are shown in Figure 9. Similar to Figure 8, the probability of NFT service platforms conducting fair detection increases with the increase in fines Fp. Before the probability of digital content creators choosing original strategies evolves to 1, the probability of strict supervision increases with the increase in Fp. After the probability of digital content producers choosing original strategies evolves to 1, the probability of strict supervision gradually decreases and eventually stabilizes at 0;

- (5)

- Rewards Received By Platforms. Setting Mp = 0, Mp = 15, and Mp = 30, the system evolution simulation results are shown in Figure 10. Figure 10 shows that an increase in Mp will reduce the probability of strict supervision and increase the probability of fair detection. Therefore, the regulators should reasonably establish a reward and punishment mechanism to reward NFT service platforms in the form of bonuses so that NFT service platforms can share the responsibility of ensuring the healthy development of the cultural digital economy with the regulators;

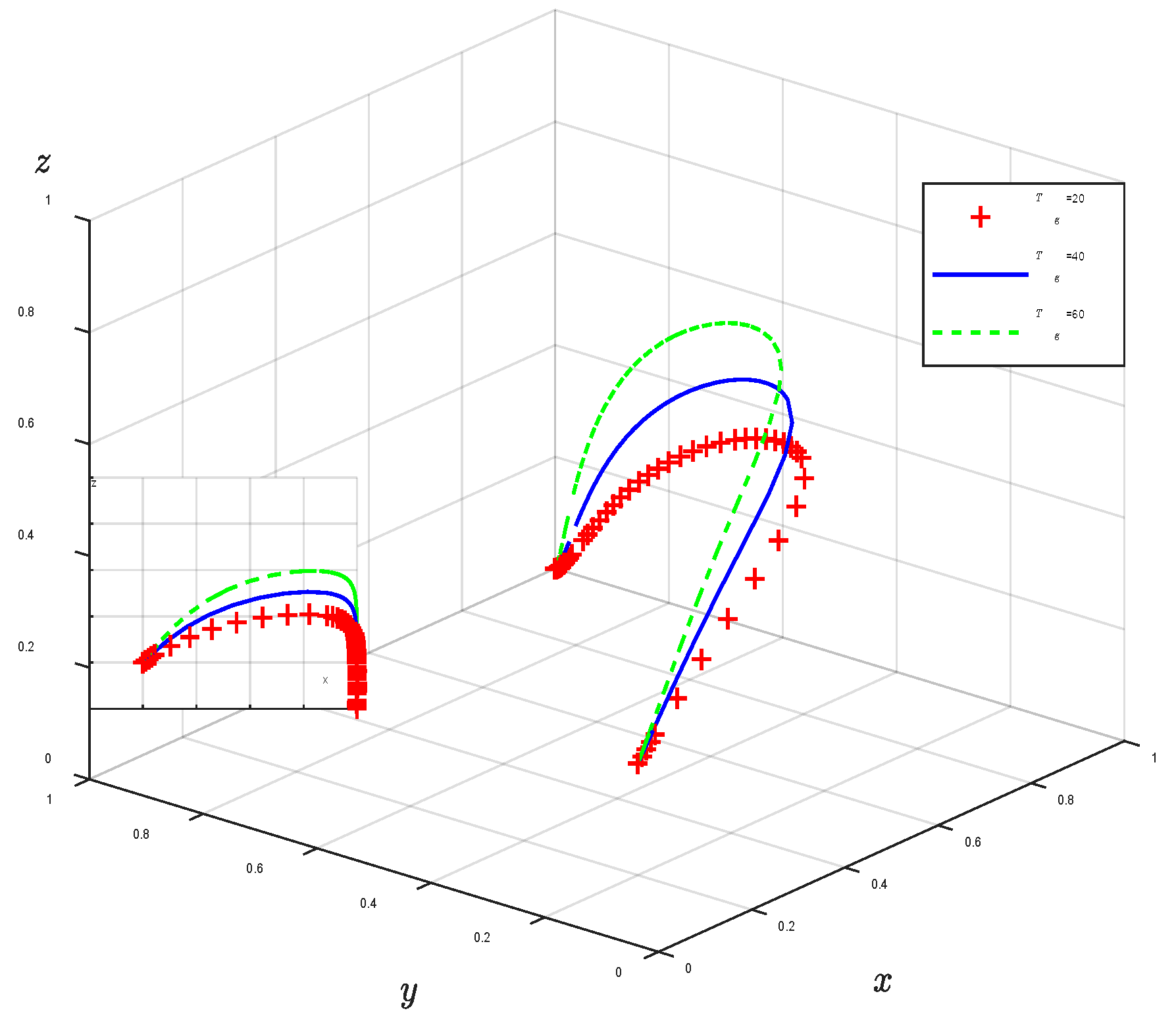

- (6)

- Penalties Borne By Regulators. Setting Tg = 20, Tg = 40, and Tg = 60; the system evolution simulation results are shown in Figure 11. Figure 11 shows that before the probability of digital content creators choosing original strategies evolves to 1, the probability of strict supervision increases with the increase in Tg. After the probability of digital content producers choosing original strategies evolves to 1, the probability of strict supervision gradually decreases and eventually stabilizes at 0.

6. Conclusions and Suggestions

- (1)

- The digital rights governance mechanism in the NFT market requires the coordinated participation of multiple entities at different levels, and the government plays a leading role in the governance process. Strengthening the government’s incentives and punishments can help promote the production of original works by digital content creators and the implementation of fair similarity testing on NFT service platforms. However, it is worth mentioning that there is a non-linear relationship between rewards and strategic choices. Excessive rewards can make the government face a trade-off between costs and benefits, leading to regulatory difficulties. In this regard, the government can establish clear legal norms before the actors implement their actions, providing reasonable standards and a theoretical basis for the scale of punishment and rewards. The government can also try to establish a credit database that includes integrity and dishonesty records of creators and service platforms and use intelligent digital statistical analysis technology to reduce the cost of strict regulation, thereby partially offsetting the costs brought about by reward mechanisms;

- (2)

- The digital rights governance mechanism in the NFT market is spirally evolving, and its evolution process is influenced by the respective interest parameters of multiple governance entities. Specifically, only when the sum of penalties and rewards set by the government on the platform and creators is greater than the profits brought to the platform and creators by collusive behavior the difference between penalties and rewards for creators is greater than the cost of strict supervision, and the penalties for platforms are greater than the cost of strict supervision too, the evolutionary game system of digital rights protection in the NFT market can avoid the emergence of mixed strategy equilibrium points and ensure that the game only evolves toward the only ideal equilibrium state of the original, fair detection and loose supervision. In this regard, the government can strengthen market research, establish and complete information collection channels, timely and accurately grasp market information such as speculative costs, collusive costs, and sales returns, and dynamically adjust the punishment and reward intensity based on this information to ensure the rationality and effectiveness of regulatory mechanisms;

- (3)

- The benefits brought to both parties by the collusive behavior of users and platforms are key factors that hinder the platform from choosing fair detection and creators to produce original digital content. The greater accountability faced by regulatory authorities can help improve the robustness of the original NFT market. On the one hand, the government can strengthen the construction of new government media, increase media disclosure capabilities, and enhance the professional literacy of testing personnel. This can increase the speculative cost of NFT service platforms performing collusive testing and compress the profit space of their illegal operations. On the other hand, the government can also cultivate consumers’ copyright awareness and actively handle and protect the complaints and legitimate rights and interests of rights holders. This can increase the speculative cost of creators’ plagiarism and may also create psychological pressure on infringers to give up plagiarism, thereby eliminating the phenomenon of NFT infringement from the source. In addition, the above two methods, to some extent, increased the participation of service platforms and creators in the governance process, which has a significant impact on improving the robustness of governance.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wang, Q.; Li, R.; Wang, Q.; Chen, S. Non-Fungible Token (NFT): Overview, Evaluation, Opportunities and Challenges. arXiv 2021, arXiv:2105.07447. [Google Scholar]

- Idelberger, F.; Mezei, P. Non-Fungible Tokens. Internet Policy Rev. 2022, 11. [Google Scholar] [CrossRef]

- Bamakan, S.M.H.; Nezhadsistani, N.; Bodaghi, O.; Qu, Q. Patents and Intellectual Property Assets as Non-Fungible Tokens; Key Technologies and Challenges. Sci. Rep. 2022, 12, 2178. [Google Scholar] [CrossRef] [PubMed]

- Nonfungible Corporation. NFT Market Report 2021. Available online: https://nonfungible.com/reports/2021/en/yearly-nft-market-report (accessed on 5 July 2023).

- Watson, R. MetaBirkins Lost to Hermès. But Be They Art or Merchandise, NFTs are Being Taken Seriously. Available online: https://www.theblock.co/post/210317/metabirkins-lost-to-hermes-but-be-they-art-or-merchandise-nfts-are-being-taken-seriously (accessed on 5 July 2023).

- Handono, M.; Widiyanti, I.D.; Andini, P.P. Dispute Resolution for Non-Fungible Token (NFT) Businesses in Indonesia. Int. J. Soc. Sci. Educ. Res. Stud. 2023, 3, 1519–1526. [Google Scholar] [CrossRef]

- Manoylov, M. OpenSea Reveals That Over 80% of Its Free NFT Mints Were Plagiarized, Spam or Fake. Available online: https://www.theblock.co/linked/132511/opensea-reveals-that-over-80-ofits-free-nft-mints-were-plagiarized-spam-or-fake (accessed on 5 July 2023).

- Zhao, L.; Zhang, J.; Jing, H. Blockchain-Enabled Digital Rights Management for Museum-Digital Property Rights. Intell. Autom. Soft Comput. 2022, 34, 1785–1801. [Google Scholar] [CrossRef]

- Mochram, R.A.A.; Makawowor, C.T.; Tanujaya, K.M.; Moniaga, J.V.; Jabar, B.A. Systematic Literature Review: Blockchain Security in NFT Ownership. In Proceedings of the 2022 International Conference on Electrical and Information Technology (IEIT), Malang, Indonesia, 15–16 September 2022; pp. 302–306. [Google Scholar]

- Park, K.S. A study on copyright issues as regards NFT art under the Korean copyright system: Focusing on Works of Art. Q. Copyr. 2021, 34, 5–43. [Google Scholar] [CrossRef]

- Park, K.S. The Study on NFT Art and the Allowable Scope of Use of Trademark. J. Korea. Inf. Law 2022, 26, 1–45. [Google Scholar]

- Dong, Y.; Wang, C. Copyright Protection on NFT Digital Works in the Metaverse. Secur. Saf. 2023, 2, 2023013. [Google Scholar] [CrossRef]

- Dong, Y.; Wu, H. Copyright of NFT Works in China: Infringement, Liability, and Remedies. SSRN Electron. J. 2023. [Google Scholar] [CrossRef]

- Xiao, C.; Wang, W.; Lin, X.; Yu, J.X.; Wang, G. Efficient Similarity Joins for Near-Duplicate Detection. ACM Trans. Database Syst. 2011, 36, 1–41. [Google Scholar] [CrossRef]

- Porter, R.H. Detecting collusion. Rev. Ind. Organ. 2005, 26, 147–167. [Google Scholar] [CrossRef]

- Alexander, J.M. Evolutionary Game Theory. In The Stanford Encyclopedia of Philosophy; Zalta, E.N., Ed.; Metaphysics Research Lab, Stanford University: Stanford, CA, USA, 2021. [Google Scholar]

- Rosenfeld, M. Overview of Colored Coins. Available online: https://bitcoil.co.il/BitcoinX.pdf (accessed on 16 September 2023).

- Steinwold, A. The History of Non-Fungible Tokens (NFTs). Available online: http://108.166.64.190/omeka222/files/original/453bc3985fdc186319dcaa6c0fcc9f8a.pdf (accessed on 16 September 2023).

- Buterin, V. A Next-Generation Smart Contract and Decentralized Application Platform. Available online: https://finpedia.vn/wp-content/uploads/2022/02/Ethereum_white_paper-a_next_generation_smart_contract_and_decentralized_application_platform-vitalik-buterin.pdf (accessed on 16 September 2023).

- Vujičić, D.; Jagodic, D.; Ranđić, S. Blockchain Technology, Bitcoin, and Ethereum: A Brief Overview. In Proceedings of the 2018 17th International Symposium on INFOTEH-JAHORINA, East Sarajevo, Bosnia and Herzegovina, 21–23 March 2018; pp. 1–6. [Google Scholar]

- Chirtoaca, D.; Ellul, J.; Azzopardi, G. A framework for creating deployable smart contracts for non-fungible tokens on the Ethereum blockchain. In Proceedings of the 2020 IEEE International Conference on Decentralized Applications and Infrastructures (DAPPS), Oxford, UK, 3–6 August 2020; pp. 100–105. [Google Scholar]

- Vogelsteller, F.; Buterin, V. ERC-20: Token Standard. Available online: https://eips.ethereum.org/EIPS/eip-20 (accessed on 10 October 2023).

- Entriken, W.; Shirley, D.; Evans, J.; Sachs, N. ERC-721: Non-Fungible Token Standard. Available online: https://eips.ethereum.org/EIPS/eip-721 (accessed on 10 October 2023).

- Beanie Beanie on Twitter: “ERC-721 Is a Non Fungible Token by Default and Is, and Always Will Be the Gold Standard of a Valuable Collectible NFT. ERC-1155 Is a Dual Purpose Fungible and Non Fungible Token. It Was Developed by Enjin, to Tokenize Things Like Common Gaming Skins and Other Commoditized Items”. Available online: https://mobile.twitter.com/beaniemaxi/status/1397280788597641217 (accessed on 17 September 2023).

- Lockyer, M.; Mudge, N.; Schalm, J.; Echeverry, S.; Zhou, Z. ERC-998: Composable Non-Fungible Token. Available online: https://eips.ethereum.org/EIPS/eip-998 (accessed on 10 October 2023).

- Radomski, W.; Cooke, A.; Castonguay, P.; Therien, J.; Binet, E.; Sandford, R. ERC-1155: Multi Token Standard. Available online: https://eips.ethereum.org/EIPS/eip-1155 (accessed on 10 October 2023).

- Vogelsteller, F.; Yasaka, T. ERC-725: General Data Key/Value Store and Execution. Available online: https://eips.ethereum.org/EIPS/eip-725 (accessed on 10 October 2023).

- Fokri, W.N.I.W.M.; Alib, E.M.T.E.; Nordinc, N.; Chikd, W.M.Y.W.; Azize, S.A.; Jusoh, A.J.M. Classification of Cryptocurrency: A Review of the Literature. Turk. J. Comput. Math. Educ. TURCOMAT 2021, 12, 1353–1360. [Google Scholar]

- FINMA. Guidelines for Enquiries Regarding the Regulatory Framework for Initial Coin Offerings (ICOs); FINMA: Bern, Switzerland, 2018. [Google Scholar]

- Bao, H.; Rouband, D. Non-Fungible Token: A Systematic Review and Research Agenda. J. Risk Financ. Manag. 2022, 15, 215. [Google Scholar] [CrossRef]

- Dowling, M. Fertile LAND: Pricing Non-Fungible Tokens. Financ. Res. Lett. 2022, 44, 102096. [Google Scholar] [CrossRef]

- Dowling, M. Is Non-Fungible Token Pricing Driven by Cryptocurrencies? Financ. Res. Lett. 2022, 44, 102097. [Google Scholar] [CrossRef]

- Kong, D.-R.; Lin, T.-C. Alternative Investments in the Fintech Era: The Risk and Return of Non-Fungible Token (NFT). SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Kushwaha, S.S.; Joshi, S.; Singh, D.; Kaur, M.; Lee, H.N. Ethereum Smart Contract Analysis Tools: A Systematic Review. IEEE Access 2022, 10, 57037–57062. [Google Scholar] [CrossRef]

- Chen, Z.; Omote, K. Toward Achieving Anonymous NFT Trading. IEEE Access 2022, 10, 130166–130176. [Google Scholar] [CrossRef]

- White, J.T.; Wilkoff, S.; Yildiz, S. The Role of the Media in Speculative Markets: Evidence from Non-Fungible Tokens (NFTs). SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Maouchi, Y.; Charfeddine, L.; El Montasser, G. Understanding Digital Bubbles amidst the COVID-19 Pandemic: Evidence from DeFi and NFTs. Financ. Res. Lett. 2022, 47, 102584. [Google Scholar] [CrossRef]

- Kim, C.G. A Study On Technology To Counter Copyright Infringement According To Nft Transaction Types. J. Semicond. Disp. Technol. 2021, 20, 187–191. [Google Scholar]

- Chen, J.; Friedmann, D. Jumping from Mother Monkey to Bored Ape: The Value of NFTs from an Artist’s and Intellectual Property Perspective. Asia Pac. Law Rev. 2023, 31, 100–122. [Google Scholar] [CrossRef]

- Baiyang, X. Chinese court rules on NFT transactions and responsibility of trading platforms. J. Intellect. Prop. Law 2022, 17, 604–606. [Google Scholar] [CrossRef]

- Evsutin, O.; Dzhanashia, K. Watermarking Schemes for Digital Images: Robustness Overview. Signal Process. Image Commun. 2022, 100, 116523. [Google Scholar] [CrossRef]

- Ansori, M.R.R.; Alief, R.N.; Igboanusi, I.S.; Lee, J.M.; Kim, D.-S. Watermarking-Based Fake Audio NFT Detection in NFT Marketplace. Available online: https://journal-home.s3.ap-northeast-2.amazonaws.com/site/2023w/abs/0716-XEAFX.pdf (accessed on 3 October 2023).

- Cao, Z.; Wang, L. A secure video watermarking technique based on hyperchaotic Lorentz system. Multimed. Tools Appl. 2019, 78, 26089–26109. [Google Scholar] [CrossRef]

- Lin, C.; Xu, X. An Electronic Bill Encryption Algorithm Based on Multiple Watermark Encryption. Trait. Signal 2021, 38, 127–133. [Google Scholar] [CrossRef]

- Prihatno, A.T.; Suryanto, N.; Oh, S.; Le, T.-T.-H.; Kim, H. NFT Image Plagiarism Check Using EfficientNet-Based Deep Neural Network with Triplet Semi-Hard Loss. Appl. Sci. 2023, 13, 3072. [Google Scholar] [CrossRef]

- Pungila, C.; Galis, D.; Negru, V. A New High-Performance Approach to Approximate Pattern-Matching for Plagiarism Detection in Blockchain-Based Non-Fungible Tokens (NFTs). arXiv 2022. [Google Scholar] [CrossRef]

- Traulsen, A.; Glynatsi, N.E. The future of theoretical evolutionary game theory. Philos. Trans. R. Soc. B 2023, 378, 20210508. [Google Scholar] [CrossRef]

- Wang, Z.; Yuan, C.; Li, X. Evolutionary Analysis of the Regulation of Data Abuse in Digital Platforms. Systems 2023, 11, 188. [Google Scholar] [CrossRef]

- Yang, Z.L.; Shi, Y.Y.; Li, Y.C. Analysis of intellectual property cooperation behavior and its simulation under two types of scenarios using evolutionary game theory. Comput. Ind. Eng. 2018, 125, 739–750. [Google Scholar] [CrossRef]

- Wang, X.; Xie, J.; Fan, Z.P. B2C cross-border E-commerce logistics mode selection considering product returns. Int. J. Prod. Res. 2021, 59, 3841–3860. [Google Scholar] [CrossRef]

- Yang, S. Evolutionary Game Analysis of UGC Copyright Infringement Governance. Available online: https://assets.researchsquare.com/files/rs-2645420/v1_covered_f5e1ba86-5750-4db7-a2de-6d653da37a65.pdf?c=1695056859 (accessed on 3 October 2023).

- Friedman, D. Evolutionary Games in Economics. Econometrica 1991, 59, 637–666. [Google Scholar] [CrossRef]

- Eshel, I. Evolutionary and Continuous Stability. J. Theor. Biol. 1983, 103, 99–111. [Google Scholar] [CrossRef]

- Newton, J. Evolutionary Game Theory: A Renaissance. Games 2018, 9, 31. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Type of Token | Explanation | Representative | Characteristics/Essence |

|---|---|---|---|

| Payment tokens/ Cryptocurrencies/ Fungible tokens | Payment tokens are meant to be used as means of payment for goods or services external to the platform on which they are issued. | Bitcoin Ether Tether | Interchangeability: Can exchange tokens of the same type. Consistency: The same token has the same specification. Divisibility: Tokens can be divided into smaller units for easy splitting and exchange. |

| Utility tokens | Utility tokens are intended to provide digital access to an application or service. | Minetrix Chainlink | Providing privileged services to token holders, but not considered an investment. |

| Asset tokens | Asset tokens represent a broad range of tradable assets with investment or collectible attributes. It is the result of issuing digital or physical assets on the blockchain. | Security tokens | A financial product used to prove that the holder enjoys certain specific rights and interests. |

| Non-fungible tokens | Non-interchangeability and uniqueness: Each NFT is unique and non-interchangeable. For example, in the physical world, each person’s birth certificate is unique and cannot be exchanged with others. Indivisibility: The basic unit is 1 token and cannot be divided into smaller units |

| Parameters | Description |

|---|---|

| x | Proportion of creators choosing “α1”. |

| Rc | Sales revenue of NFT. |

| Cco | The cost of producing and creating original digital content. |

| Ccf | The cost of producing non-original digital content. |

| Ccfr | The speculative cost of producing non-original digital works. |

| Ccfs | The collusive cost of casting non-original digital content into NFT. |

| y | Proportion of platforms choosing “β1”. |

| RP | Revenue of similarity detection. |

| Cp | Speculative costs collusion detection. |

| z | Proportion of regulators choosing “γ1”. |

| Cg | Cost of strict supervision. |

| Rg | Social benefits brought by original digital content |

| Fc | Fines imposed on creators. |

| Fp | Fines imposed on platforms. |

| Mp | Rewards set for the platforms. |

| Dg | The cost of regulators rectifying infringement. |

| Tg | Administrative penalties brought about by loose supervision. |

| Platforms | Regulators | |||

|---|---|---|---|---|

| γ1 (z) | γ2 (1 − z) | |||

| Creators | α1 (x) | β1 (y) | (Rc − Cco, RP + Mp, −Cg − Mp + Rg) | (Rc − Cco, RP, Rg) |

| β2 (1 − y) | (Rc − Cco, RP − Cp − Fp, −Cg + Fp + Rg) | (Rc − Cco, RP − Cp, Rg) | ||

| α2 (1 − x) | β1 (y) | (−Ccf − Ccfs − Fc, RP + Mp, −Cg + Fc − Mp) | (−Ccf − Ccfs, RP, 0) | |

| β2 (1 − y) | (Rc − Ccf − Ccfs − Ccfr − Fc, RP − Cp + Ccfr − Fp, −Cg + Fp + Fc − Dg) | (Rc − Ccf − Ccfs − Ccfr, RP − Cp + Ccfr, −Dg − Tg) | ||

| Equilibrium Point | Eigenvalue λ1, λ2, λ3 | Sign or Condition | Stability |

|---|---|---|---|

| E1(0, 0, 0) | −Cco + Ccf + Ccfr + Ccfs, Cp − Ccfr, −Cg + Fc + Fp + Tg | (−, −, +) | Unstable |

| E2(1, 0, 0) | Cco − Ccf − Ccfr − Ccfs, Cp, − Cg + Fp | (+, +, ×) | Unstable |

| E3(0, 1, 0) | −Cco + Ccf + Ccfs + Rc, −Cp + Ccfr, −Cg + Fc − Mp | (−, +, ×) | Unstable |

| E4(0, 0, 1) | −Cco + Ccf + Ccfr + Ccfs + Fc, Cp − Ccfr + Fp + Mp, Cg − Fc − Fp − Tg | (−, −, −) Condition ① | ESS |

| E5(1, 1, 0) | Cco − Ccf − Ccfs − Rc, −Cp, − Cg − Mp | (−, −, −) | ESS |

| E6(1, 0, 1) | Cco − Ccf − Ccfr − Ccfs − Fc, Cp + Fp + Mp, Cg − Fp | (×, +, ×) | Unstable |

| E7(0, 1, 1) | −Cco + Ccf + Ccfs + Fc + Rc, − Cp + Ccfr − Fp − Mp, Cg − Fc + Mp | (+, ×, ×) | Unstable |

| E8(1, 1, 1) | Cco − Ccf − Ccfs − Rc − Fc, − Fp − Mp − Cp, Cg + Mp | (−, −, +) | Unstable |

| E9(0, y1, z1) | a1, | (−, 0, 0) Condition ② | Uncertain |

| E10(x1, 0, z2) | a2, | (−, 0, 0) Condition ③ | Uncertain |

| E12(x2, y2, 0) | a2, | (×, +, −) Condition ④ | Unstable |

| E13(x3, y3, 1) | a4, | (×, +, −) Condition ⑤ | Unstable |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gao, Y.; Xie, X.; Ni, Y. Evolutionary Game Analysis of Copyright Protection for NFT Digital Works Considering Collusive Behavior. Appl. Sci. 2023, 13, 11261. https://doi.org/10.3390/app132011261

Gao Y, Xie X, Ni Y. Evolutionary Game Analysis of Copyright Protection for NFT Digital Works Considering Collusive Behavior. Applied Sciences. 2023; 13(20):11261. https://doi.org/10.3390/app132011261

Chicago/Turabian StyleGao, Yudong, Xuemei Xie, and Yuan Ni. 2023. "Evolutionary Game Analysis of Copyright Protection for NFT Digital Works Considering Collusive Behavior" Applied Sciences 13, no. 20: 11261. https://doi.org/10.3390/app132011261

APA StyleGao, Y., Xie, X., & Ni, Y. (2023). Evolutionary Game Analysis of Copyright Protection for NFT Digital Works Considering Collusive Behavior. Applied Sciences, 13(20), 11261. https://doi.org/10.3390/app132011261