Spatiotemporal Patterns of Risk Propagation in Complex Financial Networks

Abstract

1. Introduction

2. Literature Review

3. Data and Methods

3.1. Data

3.2. Method and Basics

4. Results

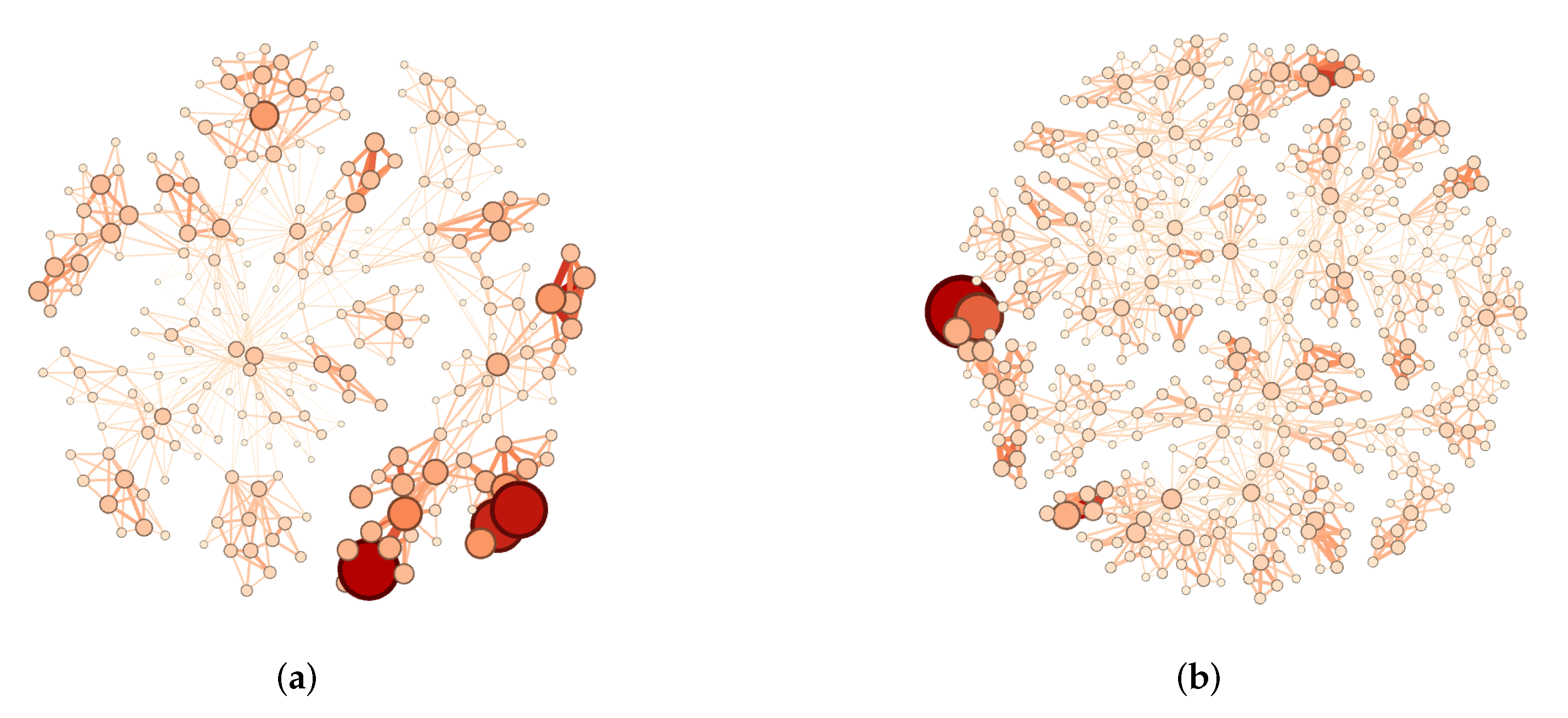

4.1. Quantifying Risk Propagation Flow

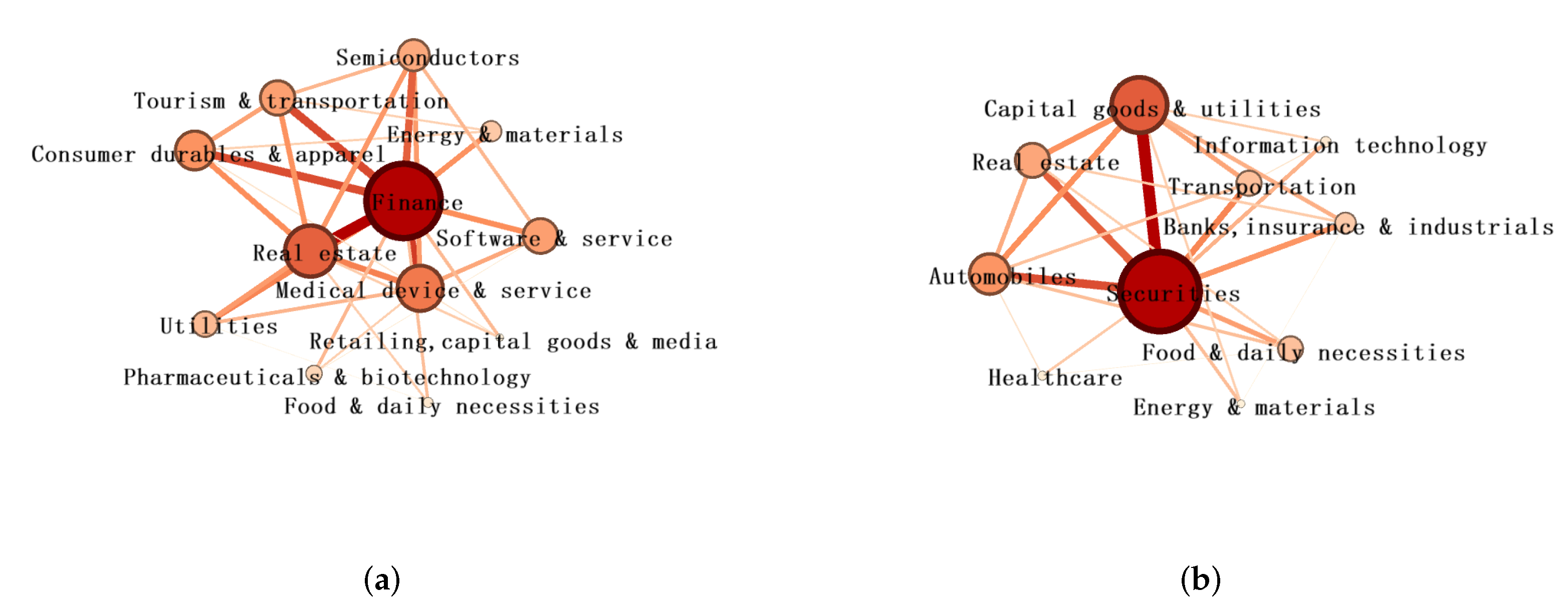

4.2. Risk Propagation Flow of Communities

4.3. Risk Propagation Flow in Extreme Market States

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| RMD | Random matrix decomposition |

| SIS | Susceptible–infected–susceptible |

| TE | Ransfer entropy |

| GITN | Global information transfer networks |

| RTE | Rényi transfer entropy |

| PMFG | Planar maximally filtered graph |

References

- Strogatz, S.H. Exploring complex networks. Nature 2001, 410, 268–276. [Google Scholar] [CrossRef]

- Albert, R.; Barabási, A.L. Statistical mechanics of complex networks. Rev. Mod. Phys. 2002, 74, 47–97. [Google Scholar] [CrossRef]

- Drogovtsev, S.N.; Mendez, J.F.F. Evolution of Networks: From Biological Nets to the Internet and WWW; Oxfrod University Press: New York, NY, USA, 2003. [Google Scholar]

- Caldarelli, G. Scale-Free Networks: Complex Webs in Nature and Technology; Oxfrod University Press: New York, NY, USA, 2007. [Google Scholar]

- Newman, M.E.J. Networks: An Introduction; Oxford University Press: New York, NY, USA, 2010. [Google Scholar]

- Girvan, M.; Newman, M.E.J. Community structure in social and biological networks. Proc. Natl. Acad. Sci. USA 2002, 99, 7821–7826. [Google Scholar] [CrossRef]

- Palla, G.; Derenyi, I.; Farkas, I.; Vicsek, T. Uncovering the overlapping community structure of complex networks in nature and society. Nature 2005, 435, 814–818. [Google Scholar] [CrossRef]

- Zhang, J.; Cao, X.B.; Du, W.B.; Cai, K.Q. Evolution of Chinese airport network. Phys. A 2010, 389, 3922–3931. [Google Scholar] [CrossRef]

- Du, W.B.; Zhou, X.L.; Lordand, O.; Wang, Z.; Zhao, C.; Zhu, Y.B. Analysis of the chinese airline network as multi-layer networks. Transp. Res. E Logist. Transp. Rev. 2016, 89, 108–116. [Google Scholar] [CrossRef]

- Lu, L.Y.; Chen, D.B.; Ren, X.L.; Zhang, Q.M.; Zhou, T. Vital nodes identification in complex networks. Phys. Rev. 2016, 650, 1–63. [Google Scholar]

- Jiang, X.F.; Xiong, L.; Bai, L.; Zhao, N.; Zhang, J.; Xia, K.; Deng, K.; Zheng, B. Quantifying the social structure of elites in ancient China. Phys. A 2021, 573, 125976. [Google Scholar] [CrossRef]

- Newman, M.E.J.; Girvan, M. Finding and evaluating community structure in networks. Phys. Rev. E 2003, 69, 026113. [Google Scholar] [CrossRef] [PubMed]

- Fortunato, S. Community detection in graphs. Phys. Rep. 2010, 486, 75–174. [Google Scholar] [CrossRef]

- Fortunato, S.; Latora, V.; Marchiori, M. Method to find community structures based on information centrality. Phys. Rev. E 2004, 70, 056104. [Google Scholar] [CrossRef] [PubMed]

- Sun, P.G.; Gao, L.; Yang, Y. Maximizing modularity intensity for community partition and evolution. Inf. Sci. 2013, 236, 83–92. [Google Scholar] [CrossRef]

- Rosvall, M.; Bergstrom, C.T. Maps of random wakls on complex networks reveal community structure. Proc. Natl. Acad. Sci. USA 2007, 105, 1118–1123. [Google Scholar] [CrossRef] [PubMed]

- Radicchi, F.; Castellano, C.; Cecconi, F.; Loreto, V.; Parisi, D. Defining and identifying communities in networks. Proc. Natl. Acad. Sci. USA 2004, 101, 2658–2663. [Google Scholar] [CrossRef]

- Sun, P.G.; Gao, L.; Han, S. Identification of overlapping and non-overlapping community structure by fuzzy clustering. Inf. Sci. 2011, 181, 1060–1071. [Google Scholar] [CrossRef]

- Lizier, J.T.; Prokopenko, M.; Zomaya, A.Y. Local information transfer as a spatiotemporal filter for complex systems. Phys. Rev. E 2008, 77, 026110. [Google Scholar] [CrossRef]

- Telesford, Q.K.; Simpson, S.L.; Burdette, J.H.; Hayasaka, S.; Laurienti, P.J. The brain as a complex system: Using network science as a tool for understanding the brain. Brain Connect. 2011, 1, 295–308. [Google Scholar] [CrossRef]

- Kwon, O.; Yang, J.S. Information flow between stock indices. Europhys. Lett. 2008, 82, 68003. [Google Scholar] [CrossRef]

- Allali, A.; Oueslati, A.; Trabelsi, A. Detection of Information Flow in Major International Financial Markets by Interactivity Network Analysis. Asia-Pac. Financ. Markets 2011, 18, 319–344. [Google Scholar] [CrossRef]

- Saito, K.; Kimura, M.; Ohara, K.; Motoda, H. Detecting critical links in complex network to maintain information flow/reachability. In Proceedings of the Pacific Rim International Conference on Artificial Intelligence, Phuket, Thailand, 22–26 August 2016; Springer: Cham, Switzerland, 2016; p. 419. [Google Scholar]

- Korbel, J.; Jiang, X.F.; Zheng, B. Transfer Entropy between Communities in Complex Financial Networks. Entropy 2019, 21, 1124. [Google Scholar] [CrossRef]

- Min, J.; Zhu, J.J.; Yang, J.B. The Risk Monitoring of the Financial Ecological Environment in Chinese Outward Foreign Direct Investment Based on a Complex Network. Sustainability 2020, 12, 9456. [Google Scholar] [CrossRef]

- Barzel, B.; Barabási, A.L. Universality in network dynamics. Nat. Phys. 2013, 9, 673–681. [Google Scholar] [CrossRef]

- Gao, J.; Barzel, B.; Barabási, A.L. Universal resilience patterns in complex networks. Nature 2016, 530, 307312. [Google Scholar] [CrossRef] [PubMed]

- Bai, L.; Xiong, L.; Zhao, N.; Xia, K.; Jiang, X.F. Dynamical structure of social map in ancient China. Phys. A 2022, 607, 128209. [Google Scholar] [CrossRef]

- Hens, C.; Harush, U.; Haber, S.; Cohen, R.; Barzel, B. Spatiotemporal signal propagation in complex networks. Nat. Phys. 2019, 15, 403–412. [Google Scholar] [CrossRef]

- Liu, Y.Y.; Slotine, J.J.; Barabási, A.L. Controllability of complex networks. Nature 2011, 473, 167–173. [Google Scholar] [CrossRef] [PubMed]

- Yan, G.; Ren, J.; Lai, Y.C.; Lai, C.H.; Li, B. Controlling complex networks: How much energy is needed? Phys. Rev. Lett. 2012, 108, 218703. [Google Scholar] [CrossRef]

- Wang, W.X.; Ni, X.; Lai, Y.C.; Grebogi, C. Optimizing controllability of complex networks by small structural perturbations. Phys. Rev. E 2012, 85, 026115. [Google Scholar] [CrossRef] [PubMed]

- Cornelius, S.P.; Kath, W.L.; Motter, A.E. Realistic control of network dynamics. Nat. Commun. 2013, 4, 1942. [Google Scholar] [CrossRef]

- Nacher, J.C.; Akutsu, T. Structurally robust control of complex networks. Phys. Rev. E 2015, 91, 012826. [Google Scholar] [CrossRef]

- Onnela, J.P. Flow of control in networks. Science 2014, 343, 1325. [Google Scholar] [CrossRef]

- Ruths, J.; Ruths, D. Control profiles of complex networks. Science 2014, 343, 1373–1376. [Google Scholar] [CrossRef]

- Sun, P.G. Controllability and modularity of complex networks. Inf. Sci. 2015, 325, 20–32. [Google Scholar] [CrossRef]

- Harush, U.; Barzel, B. Dynamic patterns of information flow in complex networks. Nat. Commun. 2017, 8, 2181. [Google Scholar] [CrossRef] [PubMed]

- Reichardt, J.; Bornholdt, S. Statistical mechanics of community detection. Phys. Rev. E 2006, 74, 016110. [Google Scholar] [CrossRef] [PubMed]

- Newman, M.E.J. Modularity and community structure in networks. Proc. Natl. Acad. Sci. USA 2006, 103, 8577–8582. [Google Scholar] [CrossRef] [PubMed]

- Li, H.J.; Wang, Y.; Wu, L.Y.; Liu, Z.P.; Chen, L.N.; Zhang, X.S. Community structure detection based on Potts model and network’s spectral characterization. Europhys. Lett. 2012, 97, 48005. [Google Scholar] [CrossRef]

- Pan, R.K.; Sinha, S. Collective behavior of stock price movements in an emerging market. Phys. Rev. E 2007, 76, 046116. [Google Scholar] [CrossRef]

- Jiang, X.F.; Zheng, B. Anti-correlation and subsector structure in financial systems. Europhys. Lett. 2012, 97, 48006. [Google Scholar] [CrossRef]

- Jiang, X.F.; Chen, T.T.; Zheng, B. Structure of local interactions in complex financial dynamics. Sci. Rep. 2014, 4, 5321. [Google Scholar] [CrossRef] [PubMed]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.A.N.; Guhr, T.; Stanley, H.E. Random matrix approach to cross-correlations in financial data. Phys. Rev. E 2002, 65, 066126. [Google Scholar] [CrossRef] [PubMed]

- Utsugi, A.; Ino, K.; Oshikawa, M. Random matrix theory analysis of cross-correlations in financial markets. Phys. Rev. E 2004, 70, 026110. [Google Scholar] [CrossRef] [PubMed]

- Pan, R.K.; Sinha, S. Self-organization of price fluctuation distribution in evolving markets. Europhys. Lett. 2007, 77, 58004. [Google Scholar] [CrossRef]

- Sornette, D. Critical market crashes. Phys. Rep. 2003, 378, 1. [Google Scholar] [CrossRef]

- Mu, G.H.; Zhou, W.X. Relaxation dynamics of aftershocks after large volatility shocks in the ssec index. Phys. A 2008, 387, 5211. [Google Scholar] [CrossRef]

- Sornette, D.; Woodard, R.; Zhou, W.X. The 2006–2008 oil bubble: Evidence of speculation, and prediction. Phys. A 2009, 388, 1571–1576. [Google Scholar] [CrossRef]

- Jiang, X.F.; Chen, T.T.; Zheng, B. Time-reversal asymmetry in financial systems. Phys. A 2013, 392, 5369. [Google Scholar] [CrossRef]

- Nobi, A.; Maeng, S.E.; Ha, G.G.; Lee, J.W. Effects of global financial crisis on network structure in a local stock market. Phys. A 2014, 03, 083. [Google Scholar] [CrossRef]

- Daron, A.; Asuma, O.; Alireza, T.S. Systemic risk and stability in financial networks. Am. Econ. Rev. 2015, 105, 564. [Google Scholar]

- Bardoscia, M.; Battiston, S.; Caccioli, F.; Caldarelli, G. Pathways towards instability in financial networks. Nat. Commun. 2017, 8, 14416. [Google Scholar] [CrossRef]

- Battiston, S.; Caldarelli, G.; May, R.; Roukny, T.; Stiglitz, J.E. The price of complexity in financial networks. Proc. Natl. Acad. Sci. USA 2016, 113, 10031. [Google Scholar] [CrossRef] [PubMed]

- Chen, T.T.; Zheng, B.; Li, Y.; Jiang, X.F. Temporal correlation functions of dynamic systems in non-stationary states. New J. Phys. 2018, 20, 073005. [Google Scholar] [CrossRef]

- Samanidou, E.; Zschischang, E.; Stauffer, D.; Lux, T. Agent-based models of financial markets. Rep. Prog. Phys. 2007, 70, 409. [Google Scholar] [CrossRef]

- Shive, S. An Epidemic Model of Investor Behavior. J. Financ. Quant. Anal. 2010, 45, 169. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Kertész, J. Focus on statistical physics modeling in economics and finance. New J. Phys. 2011, 13, 25011. [Google Scholar] [CrossRef]

- Chakraborti, A.; Toke, I.M.; Patriarca, M.; Abergel, F. Econophysics review: II. Agent-based models. Quant. Financ. 2011, 11, 1013. [Google Scholar] [CrossRef]

- Sornette, D. Physics and financial economics (1776–2014): Puzzles, Ising and agent-based models. Rep. Prog. Phys. 2014, 77, 62001. [Google Scholar] [CrossRef]

- Demiris, N.; Kypraios, T.; Smith, L.V. On the epidemic of financial crises. J. R. Statist. Soc. A 2014, 177, 697. [Google Scholar] [CrossRef]

- Balci, M.A. Fractional virus epidemic model on financial networks. Open Math. 2016, 14, 1074. [Google Scholar] [CrossRef]

- Martikainen, T.; Puttonen, V. On the informational flow between financial markets: International evidence from thin stock and stock index futures markets. Econ. Lett. 1992, 38, 213–216. [Google Scholar] [CrossRef]

- Eom, C.; Jung, W.S.; Choi, S.; Oh, G.; Kim, S. Effects of time dependency and efficiency on information flow in financial markets. Phys. A Stat. Mech. Its Appl. 2008, 387, 5219–5224. [Google Scholar] [CrossRef]

- Kim, Y.; Kim, J.; Yook, S.H. Information transfer network of global market indices. Phys. A Stat. Mech. Its Appl. 2015, 430, 39–45. [Google Scholar] [CrossRef]

- Xie, W.J.; Yong, Y.; Wei, N.; Yue, P.; Zhou, W.X. Identifying states of global financial market based on information flow network motifs. N. Am. J. Econ. Financ. 2021, 58, 101459. [Google Scholar] [CrossRef]

- Park, S.; Jang, K.; Yang, J.S. Information flow between bitcoin and other financial assets. Phys. A Stat. Mech. Its Appl. 2021, 566, 125604. [Google Scholar] [CrossRef]

- Teng, Y.; Shang, P. Transfer entropy coefficient: Quantifying level of information flow between financial time series. Phys. A Stat. Mech. Its Appl. 2017, 469, 60–70. [Google Scholar] [CrossRef]

- Dimpfl, T.; Peter, F.J. The impact of the financial crisis on transatlantic information flows: An intraday analysis. J. Int. Financ. Mark. Institutions Money 2014, 31, 1–13. [Google Scholar] [CrossRef]

- Yang, H.; Qi, S.; Zhang, Z.; Koslowsky, D. A model of information diffusion with asymmetry and confidence effects in financial markets. N. Am. J. Econ. Financ. 2021, 57, 101404. [Google Scholar] [CrossRef]

- Lu, J.; Chen, X.; Liu, X. Stock market information flow: Explanations from market status and information-related behavior. Phys. A Stat. Mech. Its Appl. 2018, 512, 837–848. [Google Scholar] [CrossRef]

- Shen, J.; Zheng, B. Cross-correlation in financial dynamics. Europhys. Lett. 2009, 86, 48005. [Google Scholar] [CrossRef]

- Podobnik, B.; Wang, D.; Horvatic, D.; Grosse, I.; Stanley, H.E. Time-lag cross-correlations in collective phenomena. Europhys. Lett. 2010, 90, 68001. [Google Scholar] [CrossRef]

- Laloux, L.; Cizeau, P.; Bouchaud, J.P.; Potters, M. Noise dressing of financial correlation matrices. Phys. Rev. Lett. 1999, 83, 1467. [Google Scholar] [CrossRef]

- Gopikrishnan, P.; Rosenow, B.; Plerou, V.; Stanley, H.E. Quantifying and interpreting collective behavior in financial markets. Phys. Rev. E 2001, 64, 035106. [Google Scholar] [CrossRef]

- Tumminello, M.; Aste, T.; Matteo, T.D.; Mantegna, R.N. A tool for filtering information in complex systems. Proc. Natl. Acad. Sci. USA 2005, 102, 10421. [Google Scholar] [CrossRef]

- Dodds, P.S.; Watts, D.J. A generalized model of social and biological contagion. J. Theor. Biol. 2005, 232, 587–604. [Google Scholar] [CrossRef] [PubMed]

- Pastor-Satorras, R.; Vespignani, A. Epidemic spreading in scale-free networks. Phys. Rev. Lett. 2001, 86, 3200. [Google Scholar] [CrossRef]

- Hufnagel, L.; Brockmann, D.; Geisel, T. Forecast and control of epidemics in a globalized world. Proc. Natl. Acad. Sci. USA 2004, 101, 15124. [Google Scholar] [CrossRef] [PubMed]

- Matthew, E.; Benjamin, G.; Matthew, O.J. Financial networks and contagion. Am. Econ. Rev. 2014, 104, 3115–3153. [Google Scholar]

- Barzel, B.; Biham, O. Quantifying the connectivity of a network: The network correlation function method. Phys. Rev. E 2009, 80, 046104. [Google Scholar] [CrossRef]

- Dyson, F.J. Distribution of eigenvalues for a class of real symmetric matrices. Rev. Mex. Fis. 1971, 20, 231. [Google Scholar]

- Sengupta, A.M.; Mitra, P.P. Distributions of singular values for some random matrices. Phys. Rev. E 1999, 60, 3389. [Google Scholar] [CrossRef]

- Rosvall, M.; Bergstrom, C.T. Mapping change in large networks. PLoS ONE 2010, 5, e8694. [Google Scholar] [CrossRef] [PubMed]

- Bastian, M.; Heymann, S.; Jacomy, M. Gephi: An open source software for exploring and manipulating networks. In Proceedings of the International AAAI Conference on Weblogs and Social Media, San Jose, CA, USA, 17–20 May 2009; Volume 3, p. 361. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Market | Top 10 Nodes | Top 10 Links |

|---|---|---|

| S&P500 | CAG.N CPB.N DG.N MNST.O AMGN.O GIS.N K.N REGN.O MSFT.O ABT.N | CZR.O ↔ VFC.N CZR.O ↔ SPGI.N CNP.N ↔ CZR.O AME.N ↔ PM.N FITB.O ↔ IQV.N PM.N ↔ TXT.N CNP.N ↔ VFC.N BXP.N ↔ FITB.O CZR.O ↔ DHR.N BXP.N ↔ IQV.N |

| HS300 | 002773.SZ 600521.SH 002555.SZ 600763.SH 002624.SZ 600196.SH 300498.SZ 002008.SZ 600436.SH 603939.SH | 002714.SZ ↔ 300498.SZ 000876.SZ ↔ 300498.SZ 002311.SZ ↔ 300498.SZ 002157.SZ ↔ 300498.SZ 600196.SH ↔ 600521.SH 600196.SH ↔ 601607.SH 002773.SZ ↔ 600079.SH 600763.SH ↔ 603939.SH 000876.SZ ↔ 002714.SZ 002773.SZ ↔ 600763.SH |

| Market | Community Name | Top 1 Node | Nodes No. | Weight |

|---|---|---|---|---|

| S&P500 | Medical device and service | BXP.N | 59 | 27.75% |

| Finance | LNC.N | 40 | 22.81% | |

| Food and daily necessities | CAG.N | 37 | 29.42% | |

| Consumer durables and apparel | GPS.N | 14 | 25.18% | |

| Pharmaceuticals and biotechnology | LLY.N | 28 | 23.84% | |

| Energy and materials | CTSH.O | 27 | 21.30% | |

| Retailing, capital goods, and media | DLTR.O | 27 | 25.02% | |

| Software and service | AJG.N | 63 | 30.42% | |

| Tourism and transportation | PENN.O | 44 | 28.43% | |

| Utilities | AEE.N | 75 | 32.52% | |

| Real estate | ITW.N | 48 | 25.74% | |

| Semiconductors | AMAT.O | 21 | 25.51% | |

| HS300 | Securities | 601211.SH | 22 | 26.39% |

| Food and daily necessities | 600050.SH | 25 | 24.35% | |

| Healthcare | 600763.SH | 28 | 27.90% | |

| Energy and materials | 000876.SZ | 29 | 33.58% | |

| Real estate | 002271.SZ | 14 | 24.43% | |

| Information technology | 600584.SH | 35 | 27.40% | |

| Transportation | 601021.SH | 15 | 37.20% | |

| Capital goods | 601618.SH | 15 | 21.82% | |

| Automobiles | 000625.SZ | 11 | 24.43% | |

| Banks, insurance, and industrials | 601818.SH | 46 | 27.07% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, T.; Li, Y.; Jiang, X.; Shao, L. Spatiotemporal Patterns of Risk Propagation in Complex Financial Networks. Appl. Sci. 2023, 13, 1129. https://doi.org/10.3390/app13021129

Chen T, Li Y, Jiang X, Shao L. Spatiotemporal Patterns of Risk Propagation in Complex Financial Networks. Applied Sciences. 2023; 13(2):1129. https://doi.org/10.3390/app13021129

Chicago/Turabian StyleChen, Tingting, Yan Li, Xiongfei Jiang, and Lingjie Shao. 2023. "Spatiotemporal Patterns of Risk Propagation in Complex Financial Networks" Applied Sciences 13, no. 2: 1129. https://doi.org/10.3390/app13021129

APA StyleChen, T., Li, Y., Jiang, X., & Shao, L. (2023). Spatiotemporal Patterns of Risk Propagation in Complex Financial Networks. Applied Sciences, 13(2), 1129. https://doi.org/10.3390/app13021129