1. Introduction

With the rapid development of the technological business landscape, artificial intelligence (AI) is playing a growing and diverse role in the decision making of small- and medium-sized enterprises (SMEs), presenting an array of opportunities and challenges. The integration of AI helps to improve predictive and prescriptive data analysis and reduce operational complexity, providing meaningful insights. This facilitates real-time decision making, driving innovation and enabling SMEs to maintain their competitive advantage in a fast-changing business landscape (

Agrawal et al., 2024;

Gunturu, 2024;

Ocran et al., 2024;

Paul et al., 2023). However, using AI in decision making also raises ethical concerns, making the legal framework surrounding AI increasingly important.

The utilisation of AI in business decision making pertains to the deployment of computational systems that are equipped to execute the human intelligence tasks, encompassing data analysis, pattern recognition, and predictive modelling (

Charles et al., 2022). AI integration encompasses a broad spectrum of decision-making domains for SMEs, from routine operational decisions to complex strategic choices with long-term implications.

Brock and von Wangenheim (

2019) revealed that SMEs successfully implementing AI technologies reported a 19% increase in operational efficiency, though many struggled with governance structures and ethical oversight. Significant disparities in AI adoption have been identified among SMEs in different sectors and regions, with technological readiness and leadership attitudes emerging as critical determinants (

Paul et al., 2023).

The implementation of AI in SMEs has been found to enhance decision quality through improved data processing capabilities and reduced human biases (

Ocran et al., 2024). It has been demonstrated to be effective in decision-making processes related to customer relationship management, supply chain optimisation, and financial forecasting (

Szukits & Móricz, 2024). However, these applications give rise to significant considerations with regard to data privacy, algorithmic transparency, and the potential displacement of human judgment in ethically sensitive decisions (

Popa & Pascariu, 2024). The European Union’s AI Act (

Regulation (EU) 2024/1689, 2024) establishes a comprehensive regulatory framework that classifies AI systems by risk level and imposes corresponding obligations on developers and users. This regulation emphasises the importance of AI literacy among employees and encourages organisations to promote education and training initiatives to improve AI-supported organisational decision making (

Bujold et al., 2024).

A conceptual basis for comprehending the role of AI in ethical decision making within SMEs can be found in the MER model of integral governance and management (

Duh & Štrukelj, 2023). The model offers a requisitely comprehensive framework for the incorporation of sustainability into organisational governance and (strategic) management via the process, institutional, and instrumental dimensions (

Duh & Štrukelj, 2023). Furthermore, the stakeholder theory (

Civera et al., 2023;

Freeman, 2010;

Freeman & Gilbert, 1988;

Freeman et al., 2010) provides valuable insights into how AI-augmented decisions must consider the interests of all affected parties. It is important to understand that integrating AI into decision-making processes significantly alters the dynamics between intuitive and analytical approaches, creating new challenges for ethical leadership in SMEs (

Haefner et al., 2021). The ethical dimensions of AI implementation entail considerations of fairness, transparency, accountability, and alignment with stakeholder interests (

Hagendorff, 2020).

Floridi and Cowls (

2019) proposed an ethical framework for AI governance that emphasised beneficence, non-maleficence, autonomy, justice, and explicability as core principles that should guide AI implementation in business contexts.

The aim of this paper is to provide a theoretical model depicting the interdependence of organisational decision-making levels and decision-making styles, with an emphasis on exploring the role of AI in organisations’ decision making, based on selected process dimension of the MER model of integral governance and management (

Belak, 2010;

Duh, 2024;

Duh & Štrukelj, 2011,

2023), particularly in relation to routine, analytical, and intuitive capabilities (

Agor, 1989;

Hodgkinson & Sadler-Smith, 2018;

Kozioł-Nadolna & Beyer, 2021;

Sinnaiah et al., 2023;

Vinod, 2021). The paper examines the intersection of the various organisational decision-making levels, the corresponding decision-making styles, and the possible implementation of AI in SMEs, focusing on how AI technologies influence intuitive, analytical and routine decision making across operational, tactical, and strategic leadership/management levels and the business policy governance level. The research question guiding this study is as follows: What is the role of AI in the decision-making processes of SMEs with reference to the different decision-making levels and decision-making styles?

There is a significant research gap in the development of a comprehensive theoretical framework that integrates the process dimensions of the MER model of integral governance and management to explain the transformative impact of AI across organisational decision-making levels and styles. Although existing research recognises the role of AI in improving analytical capabilities (

Collins et al., 2021;

Gerlich, 2025;

Miklosik et al., 2019) and addressing ethical issues (

Bankins & Formosa, 2023;

Bonsón et al., 2021;

Maiti et al., 2025), there is no model that systematically maps the interdependence of decision-making levels (business policy, strategic, tactical and operational management) and styles (routine, analytical, and intuitive) through the lens of integral governance and management.

This paper addresses the aforementioned research gap and presents a novel contribution to the discourse on AI in SME management by integrating three distinct yet interconnected dimensions that have previously been examined in isolation: organisational decision-making levels, decision-making styles, and AI regulatory frameworks. Whereas previous studies have focused primarily on technical implementation or general ethical considerations, the present study employs a systematic conceptual analysis grounded in the MER model of integral governance and management (

Duh & Štrukelj, 2023) to develop a comprehensive framework that maps the specific ethical implications of AI across different decision contexts in SMEs. This integrative approach, consistent with Dialectical Systems Theory (

Mulej et al., 2013), allows for a more nuanced understanding of how AI technologies interact with human decision-making processes at the different hierarchical levels, providing SME leaders with practical guidance for ethical AI implementation that acknowledges both the technological capabilities and normative dimensions of decision making.

Within the

Section 2 of this article, the authors present the MER model of integral government management and discuss the use of AI in the context of normative–ethical decision making, as well as the main specifics of the EU AI Act. The

Section 3 outlines the study’s methodological framework, addressing the complex interplay between the ethical use of AI and decision-making styles across different organisational levels. The main findings of the research are explored in detail in the

Section 4, followed by the discussion in the

Section 5, where the authors examine the main decision-making types (intuitive, analytical, and routine) and explore the role of AI in the interdependence between management process planning as a fundamental management function and decision making as a management process function. Next, we look into how EU AI legislation, in its capacity as both a legal–ethical AI framework and an international regulatory framework, facilitates the introduction of ethical AI. Based on these findings, we create a theoretical model depicting the interdependence of organisational decision-making levels and decision-making styles, as well as the AI regulatory framework (including EU AI legislation, AI-related ISO standards, and OECD AI guidelines). The model emphasises the role of AI in organisational decision making. The discussion of future challenges and research recommendations is integrated into the

Section 6.

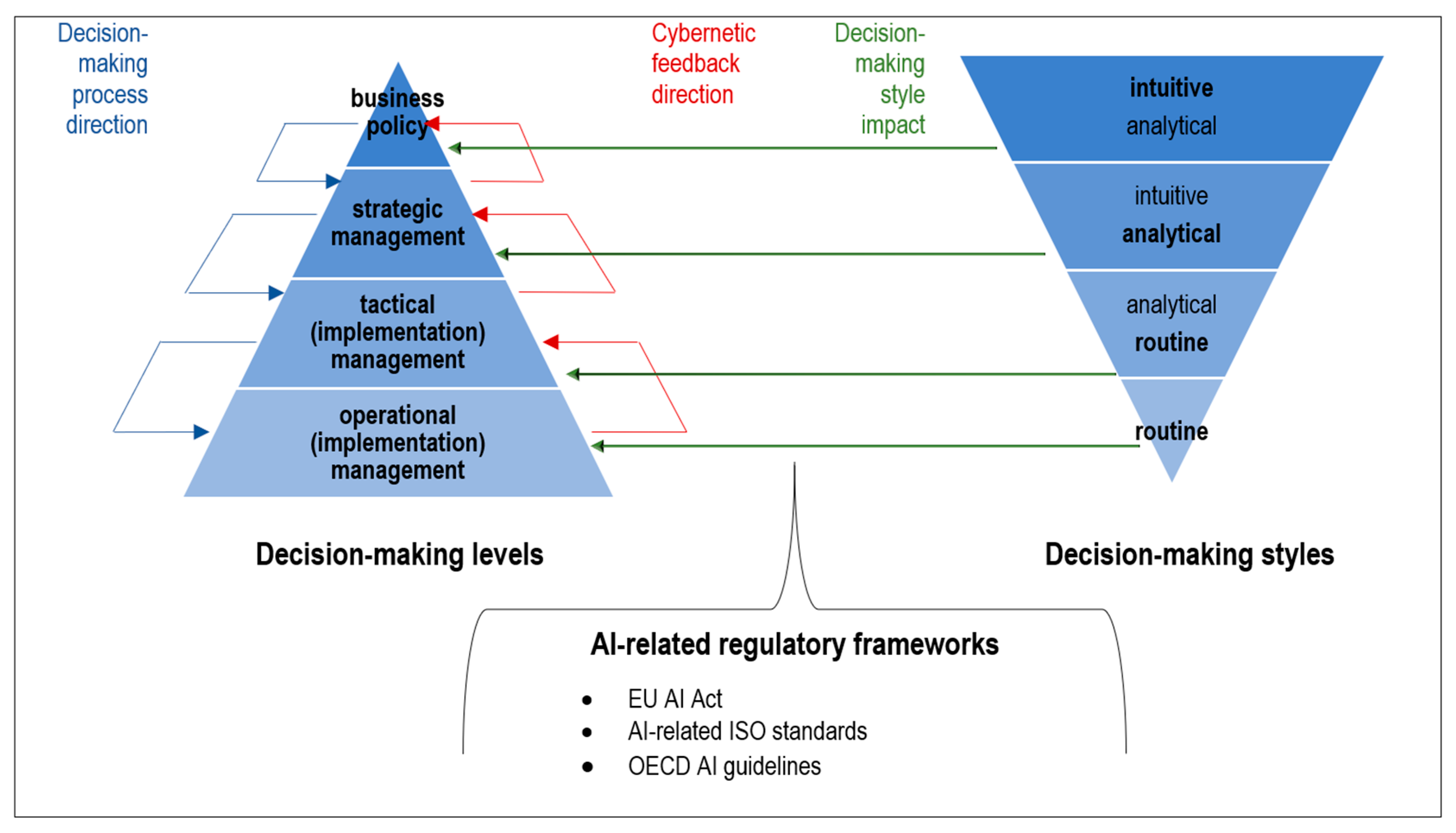

Figure 1 illustrates the main interdependent viewpoints examined in this research, highlighting the relationships between ethical leadership, management processes, and AI integration in SMEs. The figure offers a visual representation of how, within the MER model of integral governance and management, different decision-making levels (ranging from business policy to strategic, tactical, and operational management levels) interface with various decision-making styles (intuitive, analytical, and routine approaches). The framework demonstrates how these elements interact, particularly as organisations navigate ethical considerations during AI implementation in SME leadership and management. The theoretical basis for this visualisation is rooted in the MER model of integral governance and management (

Belak, 2010;

Duh, 2024;

Duh & Štrukelj, 2023), which provides a comprehensive framework for understanding and analysing the ethical dimensions within organisational decision-making processes.

Figure 1 has been developed as a conceptual guide for readers, enabling a holistic overview of the research focus and mapping the complex inter-relationships between the key theoretical constructs examined throughout the paper.

3. Methodology

This study employs a qualitative research design to examine the role of AI in decision-making processes within SMEs, including the ethical considerations involved. An integrative conceptual analysis approach was adopted (

Fuertes et al., 2020) to synthesise existing theoretical frameworks and empirical findings related to AI implementation in SME decision-making processes. Employing a qualitative conceptual analysis approach, this study developed a theoretical model. This methodological approach is particularly appropriate for emerging research areas that aim to develop comprehensive theoretical frameworks that can guide future empirical investigations. This is justified by the need to clarify theoretical constructs, identify gaps in the current literature, and integrate fragmented insights across disciplines (

Jabareen, 2009;

Meredith, 1993). Conceptual analysis is particularly suitable for under-theorised areas where empirical research is still emergent or fragmented (

Seuring & Gold, 2012). The integrative conceptual analysis involved a systematic review and synthesis of the literature across multiple disciplines, including strategic management, business ethics, decision science, and artificial intelligence. This qualitative study is based on a comprehensive literature review and should be tested in the future with primary data. However, the present study employs a structured four-step analytical process, a feature which sets it apart from a conventional literature review.

Our research is grounded in the MER model of integral governance and management (

Belak, 2010;

Duh, 2024;

Duh & Štrukelj, 2023), which provides a requisitely holistic theoretical framework for understanding the integration of sustainability and ethical considerations into the strategic management of organisations regardless of the size of an organisation. This model emphasises the interconnectedness of the process, institutional, and instrumental dimensions in organisational governance and management (

Duh & Štrukelj, 2011,

2023). We extended this framework to incorporate AI-augmented decision making by examining how AI technologies influence each dimension of the MER model. We furthermore drew on established typologies of decision-making styles, particularly the distinction between intuitive, analytical, and routine approaches to decision making (see

Hodgkinson & Sadler-Smith, 2018). This theoretical lens allowed us to analyse how AI technologies interact with different decision-making styles across business policy, strategic, operational, and tactical leadership/management levels within SMEs.

The data collection process involved a comprehensive review of the scientific literature published mainly between 2010 and 2024, with a focus on three primary domains: (1) AI implementation in SMEs, (2) ethical decision making in strategic management, and (3) regulatory frameworks governing AI use in business contexts. A systematic search strategy was employed using academic databases, primarily the Web of Science (WoS) and Scopus, alongside Google Scholar. The search terms used keywords relating to artificial intelligence, decision making, business ethics, organisational governance, strategic management, and SMEs. Search terms included combinations of keywords such as “decision-making levels”, “decision-making styles”, “artificial intelligence in organisations”, “AI-based decision support”, “ethical decision-making”, and “strategic management and AI.” Boolean operators (AND, OR) and quotation marks were used to enhance precision.

To ensure relevance and quality, the inclusion criteria for the literature selection were as follows: (1) peer-reviewed journal articles or scholarly books, indexed in the WoS or Scopus; (2) publications focusing on AI applications in business decision making addressing at least one of the core dimensions: organisational decision-making levels, decision styles, or AI in management; (3) studies addressing the ethical dimensions of AI implementation; (4) research examining decision-making processes in SMEs; (5) publications discussing regulatory frameworks for AI governance; and (6) English language. Exclusion criteria included (1) non-peer-reviewed sources, conference abstracts, and articles lacking theoretical grounding; (2) articles focused purely on technical AI development without organisational relevance; and (3) duplicates or inaccessible full texts.

After abstract screening and full-text reviews, 86 high-quality sources were included in the final analysis. To assess the quality of sources, we considered citation counts, journal impact factors, and methodological clarity, as

Tranfield et al. (

2003) suggested. Following the initial search, we employed a snowball sampling technique to identify additional relevant sources from the reference lists of selected publications. This approach ensured comprehensive coverage of the research domain and helped to identify seminal works that might not have appeared in the initial database search.

Whilst the present research does not present experimental data in the conventional sense, it constitutes original research by virtue of its systematic conceptual analysis methodology, which aligns with established qualitative research approaches (

Snyder, 2019;

Tranfield et al., 2003). The development of new theoretical frameworks through rigorous conceptual analysis represents a legitimate form of original research that generates substantial new knowledge (

Corbin & Strauss, 2015). The conceptual analysis was conducted in four structured steps: (1) coding key concepts from each article (e.g., typologies of decision making, ethical frameworks, and AI functions); (2) clustering related themes across the literature using thematic mapping; (3) cross-comparing definitions and models, including those from adjacent fields (e.g., cognitive psychology and organisational theory); and (4) synthesizing the findings into a coherent framework that integrates the levels and styles of decision making with AI’s normative and practical implications. The analysis was grounded by theory techniques for concept development (

Charmaz, 2024) and the constant comparison method to iteratively refine categories (

Corbin & Strauss, 2015).

This methodological approach, grounded in Dialectical Systems Theory (

Mulej et al., 2013), has resulted in an original theoretical contribution that offers new insights into the complex interaction between AI internal and external regulations, decision-making levels and styles, and ethical considerations in SMEs. In line with Dialectical Systems Theory (

Mulej et al., 2013), we have taken into account all essential aspects (requisitely holistic approach) and their interdependence. In this respect, the partly subjective starting points derived from the authors’ professional specialisations played an influencing role in the interdisciplinary approach that characterises systems thinking. As

Saunders et al. (

2019) point out, research that develops new conceptual frameworks through systematic analysis of existing knowledge constitutes original research when it produces novel theoretical constructs that advance understanding in the field. The present study proposes a framework representing a significant advancement in the field by providing a comprehensively holistic model that integrates the organisational, regulatory, technological, and ethical dimensions of AI implementation in a manner that has hitherto not been conceptualised in the extant literature.

Potential biases related to source selection were mitigated by adopting a systematic and transparent review protocol (

Snyder, 2019). To reduce confirmation bias, two researchers performed coding independently and cross-validated their research in discussion sessions. The validity of the conceptual framework was enhanced through the triangulation of concepts across disciplines and explicit inclusion of conflicting perspectives (e.g., techno-optimism vs. ethical scepticism). The replicability of the process is ensured by adhering to the outlined steps.

The developed theoretical framework is based on the role of AI in the management of SMEs discussed under the MER model of integral governance and management (

Belak, 2010;

Duh, 2024;

Duh & Štrukelj, 2023). The decision-making literature is analysed to explore how AI fits the intuitive, analytical, and routine decision-making models (

Agor, 1989;

Csaszar et al., 2024;

Hodgkinson & Sadler-Smith, 2018;

Keppeler et al., 2025;

Szukits & Móricz, 2024). The regulatory framework is examined to highlight selected regulatory specificities of the European Union enacted Regulation (EU) 2024/1689, also known as the EU AI Act (

Regulation (EU) 2024/1689, 2024), which the authors consider to be relevant for all organisations, including SMEs.

A theoretical model was developed to illustrate the integration of SME management, decision making, and AI regulation. The model positions AI as a moderating factor between (1) leadership and management structures and (2) business decision making. It theorises the relationships between AI-driven decision making and ethical business practices. The research methodology is based on Dialectical Systems Theory (

Mulej, 1974 and later;

Mulej et al., 2013).

4. Results

AI plays an increasing part in the leadership, governance, management, and decision making of organisations, whether in terms of development (long, medium, or short term) or the resulting business operations (

Csaszar et al., 2024;

Keppeler et al., 2025;

Paul et al., 2023;

Sinnaiah et al., 2023). The utilisation of AI can potentially provide valuable assistance to business owners and managers. Nevertheless, the integration of AI into decision-making processes also raises many ethical concerns that must be addressed. It is important to consider ethical considerations when making AI-driven business decisions. The utilisation of AI should be confined to the data collection domain; it should not be employed as a tool for producing definitive analyses or making decisions as a decision maker. In establishing business values and business policy (

Duh, 2024), it is incumbent upon organisational owners to prioritise the interests of all stakeholders while also considering their interests. Furthermore, it is of the utmost importance that these decision definitions are both responsible and sustainable (

Duh & Štrukelj, 2023).

An overview of key theoretical findings, which were used as input for the research framework, is presented in

Table 2. It shows that the MER model (

Belak, 2010;

Duh, 2024) provides a requisitely integrative framework for understanding governance and management as dynamic processes across three levels: business policy, strategic management, and implementation management. It also states that ethical decision making must go beyond legal compliance and integrate stakeholder interests, including those without direct representation (e.g., environment and marginalised groups), and that the EU AI Act (

Regulation (EU) 2024/1689, 2024) is the first legally binding instrument for AI governance, aiming to ensure that AI use is trustworthy and human centric and aligned with fundamental rights. These findings formed the basis of the research

Section 4, in which we expanded upon them and developed the proposed theoretical model.

Table 2 provides a summary of the key theoretical findings from the research. It offers a clear overview of the conceptual foundations that support the study’s framework. The table systematically organises the main theoretical insights derived from the literature review. It highlights important concepts, their connections, and implications relevant to ethical leadership, AI integration, and decision making in SMEs. This table constitutes a crucial link between the theoretical background and the theoretical model developed in the study. The theoretical findings presented in

Table 2 draw from multiple disciplines, including strategic management, business ethics, and external and internal AI regulations. This emphasises the interdisciplinary nature of the research, as advocated by the Dialectical Systems Theory approach (

Mulej, 1974 onwards;

Mulej et al., 2013). The table serves as a valuable reference for the theoretical basis of the research, facilitating a deeper understanding of the conceptual framework and its applications for implementing ethical AI in SMEs.

As outlined below, the various decision-making styles are associated with distinct characteristics. These characteristics serve to determine their possible use at different management decision-making levels (based on

Agor, 1989;

Csaszar et al., 2024;

Hodgkinson & Sadler-Smith, 2018;

Keppeler et al., 2025;

Sinnaiah et al., 2023;

Kozioł-Nadolna & Beyer, 2021;

Sinnaiah et al., 2023;

Szukits & Móricz, 2024;

Vinod, 2021; and authors’ knowledge). The authors have conducted a benchmark analysis of the decision-making styles examined, and the results are summarised in

Table 3.

Intuitive decision making is based on feelings, personal insights, and unconscious pattern recognition; it is very quick and characterised by immediate judgment; it is based on the decision maker’s previous experience and emotional intelligence; it is less structured and defined by a more holistic approach. The key characteristics of this decision-making type include rapid information processing, minimal conscious thought, reliance on personal expertise, and frequent use in high-pressure or time-critical situations (

Svenson et al., 2023;

Szanto, 2022). Intuitive decision making is experience based, very quick, and requires tacit knowledge (

Agor, 1989;

Hodgkinson & Sadler-Smith, 2018;

Vinod, 2021). The typical contexts to apply this decision-making style include leadership decisions, emergency response, creative problem solving, and entrepreneurial ventures. Owners or governors primarily make intuitive decisions at the business policy level. For them, the utilisation of AI has the potential to facilitate the development of innovative ideas and the proposal of various variants of the organisation’s vision and business policy. To a lesser extent, innovative decisions are also made by senior/top managers at the level of strategic management, where their overall view is important in the form of strategic control, which requires sufficiently rapid recognition of changes in the organisation itself and of development trends in the organisational environment on which the organisation’s strategic decisions are based (

Belak, 2010;

Csaszar et al., 2024;

Duh, 2024;

Duh & Štrukelj, 2023;

Keppeler et al., 2025;

Sinnaiah et al., 2023;

Szukits & Móricz, 2024;

Veršič et al., 2022).

Analytical decision making is characterised by a systematic and logical approach that emphases data, facts, rigorous evaluation, and a methodical analysis of available information based on rational thinking and step-by-step reasoning. The key characteristics of this decision-making type include a thorough overview of strengths and weaknesses, the use of quantitative data and statistical analysis, the application of structured decision frameworks, and minimisation of the influence of emotional factors. The managerial contexts in which this decision-making style is typically applied include strategic business planning, scientific research, financial investments, and complex problem solving. Analytical decision making is data driven, structured, and systematic (

Hodgkinson & Sadler-Smith, 2018;

Szukits & Móricz, 2024). Senior/top managers usually make analytical decisions. The employment of AI has the potential to assist them in identifying development opportunities within the domains of sales, resources, and labour and capital markets. Furthermore, it can facilitate the execution of analytical procedures and computational operations, which are instrumental in the economic evaluation and selection of potential strategies. To a lesser extent, analytical decisions are made by owners/governors at the level of business policy (particularly for researching and forecasting starting points for vision and business policy planning) and by middle managers at the tactical (implementation) management level (particularly for analysing potential resource suppliers) (

Belak, 2010;

Csaszar et al., 2024;

Duh, 2024;

Duh & Štrukelj, 2023;

Keppeler et al., 2025;

Sinnaiah et al., 2023;

Szukits & Móricz, 2024).

Routine decision making comprises standardised and predetermined processes, minimal cognitive effort required, adherence to established protocols and guidelines, and high predictability and consistency. The key characteristics of this decision-making type include predefined decision paths, minimal variation in procedure, efficiency through repetition, and low cognitive load. The managerial contexts in which this decision-making style is typically applied include operational tasks, standard operating procedures, and repetitive organisational processes in compliance-driven environments. Routine decision making is rule based, automated, and suitable for repetitive tasks (

Kozioł-Nadolna & Beyer, 2021;

Sinnaiah et al., 2023). Routine decisions are typically made by first-line managers at the operative (implementation) management level and middle managers at the tactical level of implementation management. AI can be used to a limited extent for routine decisions at the implementation management level to make suggestions for improving the organisation’s business processes (

Belak, 2010;

Csaszar et al., 2024;

Duh, 2024;

Duh & Štrukelj, 2023;

Keppeler et al., 2025;

Sinnaiah et al., 2023;

Szukits & Móricz, 2024).

Table 3 offers a detailed comparison between intuitive, analytical, and routine decision-making styles across multiple dimensions. It presents a systematic analysis of each decision-making style according to five key aspects: speed (ranging from very fast to moderate), complexity (ranging from high to low), cognitive load (ranging from low to very low), flexibility (ranging from high to low), and risk level (ranging from variable to minimal). This comparative structure serves to highlight the distinctive characteristics of each decision-making approach, as well as their relative strengths and limitations. It serves as a quick-reference guide, e.g., intuitive decisions are fast but can be risky, analytical ones take more time but tend to be thorough, and routine decisions are predictable and associated with low levels of risk. This comparative analysis is founded upon established decision-making theories and research in the field of cognitive psychology, thereby providing a structured framework for understanding how different decision-making approaches operate within organisational contexts (

Hodgkinson & Sadler-Smith, 2018;

Svenson et al., 2023). The table enables SME leaders to identify the distinguishing characteristics of each decision-making style, facilitating more informed choices about which approach might be most appropriate in different organisational contexts and how AI might be integrated accordingly. It provides a practical framework for selecting the most appropriate style for a given decision-making context.

In formulating strategies, senior/top management should focus on genuine development opportunities and market needs that the organisation can satisfy responsibly and sustainably (socially, environmentally, and also towards owners) (

Belak, 2010;

Duh, 2024;

Veršič et al., 2022). Middle- and first-line-level managers must ensure that resources are appropriately provided and allocated and that tasks are implemented according to the owners’ justifications and top management guidelines (

Belak, 2010;

Duh, 2024). According to their tasks, first-line and middle managers make the most routine decisions (

Agrawal et al., 2024;

Collins et al., 2021;

Hagendorff, 2020;

Langer et al., 2025;

Laux & Ruschemeier, 2025), while senior managers are tasked with making decisions mainly analytically (

Bonsón et al., 2021;

Charles et al., 2022;

Csaszar et al., 2024;

Gunturu, 2024;

Laux, 2023;

Ocran et al., 2024;

Haefner et al., 2021) and with the support of a range of strategic tools, and owners typically consider their intuition in addition to the information sources at their disposal (

Bankins & Formosa, 2023;

Bujold et al., 2024;

Gerlich, 2025;

Glikson & Woolley, 2020;

Vinod, 2021). When making these decisions with the assistance of AI, decision makers must acknowledge that AI is merely an instrument. Consequently, the ultimate responsibility for ensuring the suitability and ethical considerations of the decisions rests with the decision makers (

Glikson & Woolley, 2020;

Maiti et al., 2025;

Paul et al., 2023;

Shrestha et al., 2019).

Cost effectiveness and resource allocation must also be considered when integrating AI into organisational frameworks (

Brock & von Wangenheim, 2019;

Paul et al., 2023). Currently, it is impossible to navigate cross-border AI regulations and the associated compliance challenges. Therefore, it is imperative to consider future regulatory efforts on a global scale, as well as strategies for business adaptation. The development of appropriate AI auditing frameworks is paramount for establishing organisational accountability in this area. This holds particular significance for SMEs (

Haefner et al., 2021), wherein owners/governors frequently assume the roles of strategic managers, often encompassing tactical or even operational management positions, and it is not uncommon for them to engage directly in the fundamental implementation processes. In such cases, it becomes imperative for individuals to comprehend the scope of their decision-making authority and the various factors influencing those decisions, including AI (

Agrawal et al., 2024;

Gunturu, 2024;

Ocran et al., 2024;

Paul et al., 2023).

Based on the theoretical research findings, requisitely holistic interdependently connected according to Dialectical Systems Theory findings (

Mulej, 1974 and onwards;

Mulej et al., 2013), the authors of this study used a conceptual research approach to develop a theoretical model that reveals the most important interdependencies between decision-making levels (

Belak, 2010;

Duh, 2024;

Duh & Štrukelj, 2023) and decision-making styles (

Csaszar et al., 2024;

Hodgkinson & Sadler-Smith, 2018;

Keppeler et al., 2025;

Khudabadi & Shankaran, 2023;

Kozioł-Nadolna & Beyer, 2021;

Peng, 2024;

Sinnaiah et al., 2023;

Szukits & Móricz, 2024;

Vinod, 2021). The necessity to take into account the AI-related regulatory framework as a research outcome (

Langer et al., 2025;

Laux, 2023;

Laux & Ruschemeier, 2025;

Popa & Pascariu, 2024;

Regulation (EU) 2024/1689, 2024; see also AI-related ISO standards and OECD AI guidelines) was also emphasised (

Figure 2). A theoretical model was developed to integrate the three key dimensions: (1) organisational leadership/governance and management decision-making levels, where the role of AI is primarily important in shaping organisational leadership, accountability, and compliance; (2) decision-making types, where the interplay between intuitive, analytical, and routine decision-making processes is primarily important; and (3) AI regulations, where the impact of EU AI Act, ISO standards, and OECD AI guidelines on ethical AI use in business is primarily focused on. This theoretical model is applicable to SMEs, even though the core governance and management functions of such organisations often pertain to a single decision-making individual (

Duh, 2024, pp. 25–26, 126–127).

The theoretical model, presented in

Figure 2, illustrates the interdependence between organisational decision-making levels, decision-making styles, and AI-related regulatory frameworks in the context of SME governance/management. The figure demonstrates how these elements interact and influence each other in the context of AI implementation in SMEs. The theoretical model was developed using a research approach based on Dialectical Systems Theory (

Mulej, 1974 and onwards;

Mulej et al., 2013), which emphasises the importance of requisitely holistic, interdependently connected understanding of complex systems and phenomena. The figure provides a comprehensive visual framework that helps readers understand the complex inter-relationships between different levels of organisational decision making, various decision-making styles, and relevant AI regulatory considerations. It provides practical guidance for ethical AI implementation in SMEs.

The results of this study, theoretical model developed in

Figure 2 and the classification presented in

Table 3 provide a sufficiently comprehensive overview of the three decision-making styles, each with unique characteristics, strengths, and suitable application contexts. Understanding these differences enables individuals and organisations to select the most suitable approach for particular situations in specific leadership and management processes at different levels of decision making. These styles are not mutually exclusive. Effective decision makers frequently integrate these approaches and adapt them to the context’s unique characteristics, the problem’s complexity, and the available resources.

5. Discussion

Despite considerable advances in AI providing powerful and sophisticated support for decision-making processes, AI lacks the capacity for ethical reasoning. Consequently, the notion of human responsibility remains indispensable. Ethical and responsible decision making depends on individual accountability and responsibility, whether of decision makers, employees, or citizens. The human role in decision making remains significant, regardless of whether the process is routine, analytical, or intuitive. Human oversight in AI-driven decision making is necessary because decision makers are still developing the skills required to utilise AI effectively. Decision makers—whether owners, managers, or policymakers—must remain accountable for ensuring that AI-driven decisions align with ethical principles, regulatory expectations, and sustainable business practices. It is of crucial importance for humanity to balance AI efficiency with ethical accountability.

The subject under discussion in this paper, which explores the intricate connections that exist between the leadership and management processes at the different levels of organisational decision making with the various decision-making types and AI-related regulatory frameworks (see

Table 4), is not only novel but also, for the most part, significantly underexplored, particularly concerning its depth and complexity. We have identified significant possible legal and ethical challenges emerging in this context. These challenges address a wide range of subjects, including recommendations to integrate AI technologies with ethical frameworks that guide decision-making processes. The evolving role of AI within the spheres of business ethics and sustainability represents a rapidly expanding field of study, wherein a plethora of potential conflicts may arise between the automation brought forth by AI and the established ethical business practices that have traditionally governed organisational conduct. Therefore, researchers and business professionals must proactively address AI bias issues and the concerns surrounding fairness and equity in decision making. As AI is increasingly adopted within organisations, particularly with regard to decisions driven by AI technologies, it is crucial to ensure high transparency and explainability. The recent proliferation of innovative AI technologies has engendered many development opportunities, including their extensive implications for the leadership and management of organisations. The management of AI–human collaboration in leadership and management roles remains a largely unexplored field, particularly in the context of resistance to AI integration within traditional decision-making frameworks.

Table 4 presents a comprehensive framework mapping the intersections between various organisational decision-making levels, decision-making styles, and corresponding AI applications relevant to SME leadership/governance and management. The table is structured into three main sections: (1) Firstly, it delineates the levels of governance/management decision making, ranging from broad business policy and strategic management to tactical and operational implementation management. (2) Secondly, it categorises decision-making styles—intuitive, analytical, and routine—along with their defining characteristics. (3) Thirdly, it identifies specific AI applications aligned to each style, with particular attention to the EU AI Act’s human-centric regulatory approach and providing specific examples for each decision-making style. For the routine decision-making style, we recommend using RPA, Robotic Process Automation technology, i.e., for routine, stable tasks and activities, such as data entry, information transfer, and information processing. RPA automates repetitive tasks with low complexity, requiring no changes to systems (

Bernardini, 1999). For the analytical decision-making style, we recommend using BPA, Business Process Automation systems (e.g., ERP and CRM), i.e., for cross-departmental, time-consuming tasks that affect the optimisation and redesign of larger business processes. BPA is applicable for process reorganisation or other highly complex organisational strategic approaches (

Agostinelli et al., 2025;

Hu et al., 2022). For the intuitive decision-making style, we recommend using iPA, Intelligent Process Automation technologies, i.e., for complex, cognitive tasks such as understanding business documentation, analysing emails, or other forms of information preparation to facilitate decision making. iPA augments RPA technologies and BPA systems with AI and uses highly complex, advanced AI algorithms (

Liu et al., 2021;

Zaidi et al., 2025).

The structure delineated in

Table 4 demonstrates that the implementation of tailored AI solutions has the potential to support the different decision-making styles across organisational levels, thereby enabling improved governance and management across organisational hierarchies. It builds on the MER model of integral governance and management by introducing new responsibility and sustainability directions (

Duh & Štrukelj, 2023). It also integrates current understanding of AI capabilities and regulatory requirements, with a particular focus on the significance of ethical, human-centric, rights-based AI deployment as outlined in the EU AI Act (

Regulation (EU) 2024/1689, 2024). The proposed table provides SMEs leaders with practical guidance on the deployment of AI in alignment with different organisational levels and decision-making contexts, ensuring regulatory compliance and adherence to ethical standards.

The practical implications of this study pertain to the use of AI in the decision-making process of SMEs as follows:

At the business policy level, for example, AI can accelerate the generation of insights for rapid scenario modelling, augmenting leaders’ intuition with data-driven foresight. Additionally, “explainability interfaces” can be implemented to translate AI outputs into intuitive dashboards, thereby ensuring human oversight of high-stakes decisions.

At the strategic and tactical management levels, AI can be used for data processing, with strict human validation of assumptions, and for optimising resources by equipping middle managers with AI tools for dynamic resource allocation.

At the operational level, AI can be useful for automating rule-based tasks and identifying bottlenecks in routine tasks.

Each core management function (planning, organising, direct leadership/management, and control) encompasses specific process management activities (phases). These include preparatory information tasks, where the ethical application of AI can offer valuable support, and decision making, where AI should be calibrated according to the decision level. This development reflects the evolving practical role of AI, transitioning from a mere supportive tool to an active participant in decision-making processes, thus underscoring the critical importance of ethical considerations in corporate governance and management. Such a transformation necessitates a clear strategic orientation grounded in responsibility and foresight.

Implications for responsible and sustainable leadership and management also include fostering a culture of ethical AI adoption and reinforcing regulatory compliance. Thus, business ethics must play a central role in this paradigm shift, and this transformation must be actively supported through educational initiatives, training programmes, and policy frameworks. Business schools and universities must take the lead in educating future leaders about the ethical dimensions in general and of AI. Similarly, economic policymakers must develop supportive frameworks that ensure ethical decision making across economic and non-economic domains.

The theoretical framework developed in this study has the potential to offer further practical applications for SMEs implementing AI in various decision-making situations. Supply chain optimisation is one field in which SMEs can utilise AI in their routine decision-making processes, such as inventory management and logistics planning. This builds upon

Hodgkinson and Sadler-Smith’s (

2018) typology of decision-making styles by demonstrating the feasibility of delegating routine decisions to AI systems under appropriate oversight. Adoption of such systems by manufacturing SMEs has the potential to enhance operational efficiencies whilst ensuring the establishment of clear protocols for human oversight of AI-generated recommendations (

Agrawal et al., 2024). This is a significant development, as it enables SMEs to allocate human resources to more complex decisions that require ethical judgment. In customer relationship management, SMEs can implement AI-driven analytics to improve analytical decision making while upholding ethical standards. For instance, a medium-sized retail organisation could utilise AI to analyse customer purchasing patterns while concurrently establishing explicit limits for data usage and ensuring transparency (

Gunturu, 2024). This approach extends the MER model by demonstrating how the instrumental dimension of management can incorporate AI while adhering to ethical principles in stakeholder relationships. This can be of great importance for SMEs, as it allows them to retain customer trust, maintain customer relations based on trust, and consequently compete successfully with larger organisations. SMEs can also employ AI as a supportive tool for intuitive decision making rather than a replacement in strategic planning. This challenges traditional views of AI as primarily analytical by demonstrating its capacity to support human intuition through pattern recognition in complex (market or other external or internal environment) data. As

Peng (

2024) observes, emotions continue to play a pivotal role in decision-making processes, particularly in strategic domains, and our model aims to provide a balanced approach by integrating AI capabilities with human judgment. This is of particular importance for SMEs, as strategic decisions often determine long-term impact on sustainability and competitive positioning. In regard to regulatory compliance, SMEs can adopt AI regulation frameworks that are alignment with the EU AI Act (

Regulation (EU) 2024/1689, 2024) and other international AI regulatory frameworks. These practical propositions extend the scope of theoretical AI ethics discussions by proposing the implementation of AI internal and external regulations by SMEs, despite their limited resources (

Owusu et al., 2021). Adopting the stakeholder-oriented approach proposed in this paper enables SMEs to position themselves at the forefront of responsible AI use, potentially conferring a competitive advantage through ethical leadership (

Popa & Pascariu, 2024). The practical proposals set out in this study demonstrate how SMEs can leverage AI capabilities while maintaining ethical standards and meeting regulatory demands across different decision-making areas.

This research also provides substantial theoretical contributions to the understanding of AI integration in SMEs’ decision-making processes. Our findings have contributed to the enhancement of the MER model of integral governance and management (

Belak, 2010;

Duh, 2024;

Duh & Štrukelj, 2023) through the development of the proposed theoretical model. In the newly established model, the decision-making process is derived from the MER model and is further explicitly complemented by a cybernetic feedback loop for control and reversed action. The MER model has been expanded to encompass a taxonomy of decision-making styles, which have been categorised according to their utilisation at various decision-making levels, as delineated in the reviewed literature according to authors’ systems thinking. In the newly developed theoretical model, the inter-relation between different decision-making styles and the varying decision-making levels has been demonstrated. The significance of incorporating AI regulatory frameworks within organisational decision-making processes has been underscored, and AI-specific dimensions have been integrated into the MER model, demonstrating how technological capabilities interact with existing governance and management structures across different organisational levels. This integration provides a more comprehensive theoretical framework for understanding the complicated relationship between technological systems and human decision-making processes in SMEs. The theoretical model that was developed provides a new basis for further development of theory and practice, thus making a key contribution to the development of the strategic management field.

Our research contributes to the development of decision-making theory by systematically demonstrating, at a meta-theoretical level, how AI technologies influence intuitive, analytical, and routine decision-making styles differently (

Hodgkinson & Sadler-Smith, 2018;

Svenson et al., 2023), revealing that the ethical implications of AI implementation vary significantly depending on the decision-making type. This research contributes to the stakeholder theory (

Freeman & Gilbert, 1988;

Freeman et al., 2010) by highlighting the challenges posed by AI-augmented decision making to the balancing of stakeholder interests, particularly when algorithmic processes are inapplicable or do not adequately account for normative–ethical considerations. Furthermore, this study serves as a critical link between the extant literature on technical AI implementation and existing business ethics frameworks (

Carroll, 1979;

Weiss, 2021) by proposing a theoretically based approach to responsible AI governance that acknowledges both the practical advantages and the ethical challenges posed by AI technologies. Finally, by adopting a Dialectical Systems Theory approach (

Mulej et al., 2013) this research highlights the importance of holistic thinking when addressing complex socio-technical challenges. It provides a methodological framework for future research examining the relationships between technology, ethics, and organisational decision making in SMEs.

The methodological approach adopted in this paper is subject to several limitations. Firstly, reliance on the published literature means that our analysis may fail to capture the most recent developments in AI technologies and their applications in SMEs. Secondly, the conceptual nature of our analysis restricts our capacity to formulate definitive causal assertions regarding the interplay between AI implementation, decision-making frameworks, and ethical outcomes. Thirdly, our focus on theoretical integration may not fully capture the contextual nuances and practical challenges SMEs face in different industries and regions.

This research focuses on the planning function as part of the basic management functions (which include planning, organising, direct leadership/management, and control) and on the decision-making function as part of the process management functions (which include preparatory information activities, decision making, and action). A significant limitation of the study is also that it does not consider the influence of the (external) environment on decision making. The (external) environment is characterised by constant change, and SMEs must consider the potential ramifications of these developments on their decision-making processes. However, it is important to note that organisations may be aware of these developments/changes, or they may not be aware of them. Even in cases where awareness exists, the consideration or incorporation of these factors into decision-making processes may vary (

Veršič et al., 2022). We have briefly examined the European Union AI Act (

Regulation (EU) 2024/1689, 2024); however, the AI-related ISO standards and OECD AI guidelines have not been covered. The theoretical model developed in this article has not been empirically verified; this should be carried out in the future with primary data.

Notwithstanding the limitations mentioned above, the methodological approach adopted provides a robust foundation for understanding the complex interplay between AI technologies, decision-making processes, and ethical considerations in SMEs (

Kozioł-Nadolna & Beyer, 2021;

Rüegg-Stürm & Grand, 2019). The resulting theoretical framework offers valuable insights for researchers and practitioners interested in the ethical implementation of AI in business decision making.

6. Conclusions

SMEs constitute an essential element of the economic landscape (

Agrawal et al., 2024;

Brock & von Wangenheim, 2019;

Charles et al., 2022;

Gunturu, 2024;

Ocran et al., 2024;

Paul et al., 2023;

Veršič et al., 2022). In their pursuit of navigating increasingly complex business contexts, the incorporation of AI into their decision-making frameworks offers substantial opportunities alongside significant ethical challenges. Despite the potential benefits, critical ethical considerations remain regarding the appropriate boundaries of AI in decision-making processes, particularly with regard to accountability, transparency, and preserving human agency (

Peng, 2024). AI systems should be designed to support rather than replace human ethical judgment, especially in decisions with significant moral implications (

Martin, 2019). Organisations must develop governance and management structures that can effectively oversee AI systems while maintaining human accountability for decisions with ethical dimensions (

Glikson & Woolley, 2020).

This paper contributes to the evolving dialogue on AI in SME leadership by examining the role of AI across different decision-making levels and styles, with particular attention to normative ethical considerations. By synthesising theoretical perspectives with practical implications, we provide SME leaders with insights for responsible AI integration that supports sustainable development goals while maintaining ethical integrity in business development and operations. Future research must address the development of practical frameworks that enable SME leaders to integrate AI ethically while navigating the complex interplay between technological capabilities, regulatory requirements, and stakeholder expectations (

Svenson et al., 2023).

This paper explored the role of AI in the decision-making process at various organisational leadership and management levels. We investigated the role of AI in the interdependence between planning (as a basic function of management) and decision making (as a process function of management) as a tool for planning decisions at all leadership and management levels within all the basic functions of management. The research revealed that intuitive, analytical, and routine decision-making types are used to varying degrees at different levels of leadership and management processes.

Furthermore, it has been demonstrated that the role of AI differs significantly depending on the type and scope of the decision making. It has been established that application decision makers need to consider factors beyond legal obligations in the context of AI. The increasing integration of AI into business decision making and organisations’ leadership and management is a rapidly evolving field. This has given rise to the necessity for ethical considerations with high ethical standards to ensure responsible AI use. This study demonstrates that AI can be effectively incorporated into organisational decision making across all governance/management levels. AI can facilitate the generation of innovative ideas at the business policy level. Moreover, it can assist senior management in resolving analytical tasks in strategic decision making. In addition to this, it can enhance routine decisions through process optimisation at the tactical and operational management levels. The multifaceted applications underscore the necessity for a nuanced and ethically grounded approach to the adoption of AI in organisational leadership and management (

Belak, 2010;

Csaszar et al., 2024;

Duh, 2024;

Duh & Štrukelj, 2023;

Keppeler et al., 2025;

Sinnaiah et al., 2023;

Szukits & Móricz, 2024).

Our analysis of AI’s role in the decision-making processes of SMEs reveals several important insights that extend beyond theoretical considerations to bring real-world, practical implications. The integration of AI technologies across business policy, strategic, tactical, and operational management levels and decision-making types/styles significantly changes how SME leaders respond to ethical dilemmas. Despite the capacity of AI to substantially augment analytical decision making through enhanced data processing capabilities (

Vinod, 2021), our findings underscore the assertion that normative–ethical decisions invariably necessitate human judgement, stakeholder context consideration, and values/principles alignment. Nevertheless, it is not possible to integrate these into AI systems at the present time (

Bankins & Formosa, 2023).

The practical significance of this research lies in the proposed framework for responsible AI integration in SMEs. It is imperative for leaders to acknowledge that AI should be regarded as a complementary tool, rather than a replacement, for human judgment, particularly in decisions that bear significant ethical implications. The resolution of these issues necessitates the establishment of transparent governance and management structures by SMEs, thereby enabling human responsibility while leveraging the analytical advantages of AI (

Bonsón et al., 2021). As

Csaszar et al. (

2024) demonstrate, organisations that successfully integrate AI while maintaining human oversight in ethical decision making create more sustainable outcomes and stronger relations with stakeholders.

The findings of our research provide several practical recommendations for SME leaders navigating this complex landscape. The implementation of AI systems within organisations must be accompanied by transparent algorithms and explainable outputs. The overarching aim should be to facilitate transparent decision-making processes, particularly in cases where such decisions have ramifications for multiple stakeholders. It is imperative that clear boundaries are established between decisions that can be safely delegated to AI and those requiring human ethical judgment. This should be supported by the decision-making typology on the recommended manner presented in our framework. It is also important to continue to build and invest in developing both AI literacy and positive ethical reasoning capabilities among leadership/management teams, as well as promoting a culture in which technological advancement and ethical considerations mutually reinforce rather than compete with each other (

Szukits & Móricz, 2024).

The findings of our research extend beyond the scope of individual SMEs to encompass broader implications for society and potential future applications of AI. As AI becomes increasingly important in business decision making, the behaviour of SMEs, which form the majority of the world’s business entities, will significantly determine whether AI serves as a force for ethical improvement or ethical decline in business practices. Adopting the stakeholder-oriented framework proposed in this study can position SMEs at the forefront of responsible AI implementation, demonstrating that progress and technological evolution can occur alongside ethical engagement (

Carroll, 1979;

Carroll & Brown, 2022;

Weiss, 2021).

Authors recommend that future research focus on the practical implementation of the theoretical model proposed in this paper. In order to empirically validate the proposed theoretical model of the interdependence between organisational decision-making levels, decision-making styles, and the role of AI, future research should thus adopt a mixed-methods approach. Theoretical insights should be evaluated through empirical testing in real-world organisational case studies or quantitative surveys. Focus group discussions with senior/top and middle-level managers could provide valuable insights into the actual perception and integration of AI into the decision-making process at the various management/leadership levels (

Saunders et al., 2019). Furthermore, experimental simulations involving AI-driven decision-making scenarios could examine how decision makers adapt their styles when interacting with algorithmic tools (

Shrestha et al., 2019). The model should be evaluated to ascertain its applicability across different industries (e.g., finance, HR, or supply chain). The application of structured surveys across diverse sectors could facilitate the statistical evaluation of the model’s applicability and the identification of sector-specific variations. Longitudinal designs could further explore how AI-supported decision making evolves across business policy level, strategic management, tactical, and operative management levels (

Marabelli & Galliers, 2017). The employment of these methodologies would engender more robust and generalisable insights, thereby supporting future refinements of the theoretical model.

Further research is also required on AI auditing mechanisms, AI ethics training, and interdisciplinary approaches to AI governance and management. The authors also recommend examining how AI influences corporate decision making, different AI-driven governance and management models and frameworks, the interdependence between corporate governance theories (e.g., agency theory and stakeholder theory) and AI, risks and challenges of AI in decision making (bias, transparency, and accountability), AI’s role in corporate governance, enhancing board-level decision making with data insights, AI-powered compliance monitoring and fraud detection, automating corporate reporting and regulatory compliance, AI’s role in management and strategic planning, business operations and resource allocation, AI in talent acquisition and HR management (bias risks and fairness concerns), AI-powered financial forecasting and risk assessment, ethical considerations, balancing efficiency with transparency and accountability, managing AI bias and algorithmic discrimination, ensuring AI-driven decisions align with corporate social responsibility goals, and similar topics.

The future of ethical leadership practice in SMEs will not depend on the utilisation of AI (whether or not AI is adopted) but rather on how it will be incorporated into organisational decision-making processes. The present study provides a set of guidelines for incorporating AI into a decision-making process that preserves the fundamental human components of ethical reasoning while embracing the analytical capabilities of AI technologies. This balanced approach is considered to represent the most viable future for SMEs to succeed in an increasingly complex and technology-driven business environment while maintaining their commitment to effective ethical leadership that considers stakeholder health and well-being. This balanced approach offers a viable future for SMEs seeking to succeed in an increasingly complex and technology-driven business environment while maintaining their commitment to effective ethical leadership, with the consideration of stakeholders’ well-being.

{kind=link}

{kind=link}