Lack of Risk Management at Insolvency Consulting Companies: An Empirical Study in Germany 2024

Abstract

1. Introduction

- (a)

- Is risk management necessary and useful in insolvency counselling?

- (b)

- What form does risk awareness take in insolvency counselling?

- (c)

- Is systematic risk management used in insolvency counselling?

2. Literature Review

3. Materials and Methods

“Every lawyer knows the practically unrealisable demands of case law on his diligence and omniscience, which ultimately amount to strict liability regardless of fault. Nevertheless, for most lawyers, ‘risk management’ is limited to ‘paying attention’, effectively monitoring deadlines and reading the NJW [Neu Juristische Wochenschrift; author’s note] every week”.

“[…] tax advisors, tax agents, auditors, sworn accountants and lawyers who prepare annual financial statements for a client must draw the client’s attention to the existence of a possible reason for insolvency in accordance with Sections 17 to 19 of the German Insolvency Code and the associated duties of the managers and members of the supervisory bodies if there are obvious indications of this and they must assume that the client is not aware of the possible insolvency and the associated duties”.

- Business with dubious independence;

- Risk transactions;

- Failure to contest or assert claims;

- Transactions below market price;

- Cover-up and concealment measures;

- The management of criminal assets in the insolvency estate.

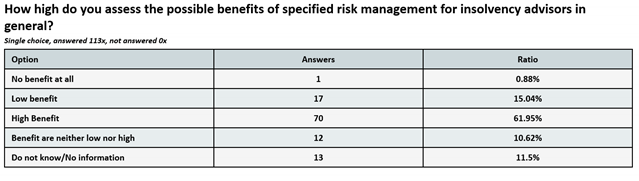

- Perception of the benefits of risk management in the industry and personally.

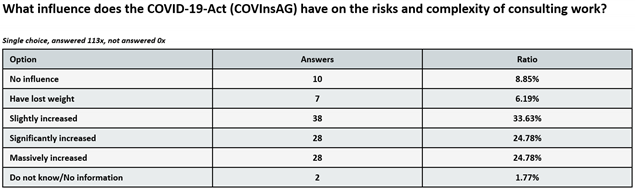

- Perceptions of increasing risks due to legal measures and support during the pandemic and other influencing factors.

- Utilisation of risk management and specific tools and methods.

- Perceptions of risks and risk-based factors in insolvency counselling.

- Attitudes and plans for risk management in the future.

- Areas in which risk management would be useful.

4. Results

4.1. Established Instruments of Strategic Risk Management

- Establishing the context;

- Risk identification;

- Risk analysis;

- Risk treatment;

- Risk avoidance;

- Risk reduction;

- Risk sharing;

- Risk transfer;

- Risk monitoring and review;

- Risk documentation.

“Preventive controls are relevant to actions that are taken before the event occurs. The nature of detective controls means that they relate to circumstances after the event has occurred”.

4.2. Descriptive Analysis of the Results of the Research Survey

4.3. Inferential Statistical Analysis of the Results

5. Discussion and Conclusions

5.1. Context and Necessity of Risk Management for Insolvency Advisors

5.2. Empirical Findings and Recommendations for Action

5.3. Testing the Hypotheses

5.4. Answering the Research Questions

- (a)

- Is risk management necessary and useful in insolvency counselling?

- (b)

- What form does risk awareness take in insolvency counselling?

- (c)

- Is risk management used in insolvency counselling?

5.5. Limitation of the Study

5.6. European Perspectives

5.7. Summary and Outlook

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Baumann, Susanne, Iris Erber, and Magdalena Gattringer. 2016. Selection of risk identification instruments. ACRN Oxford Journal of Finance and Risk Perspectives 5: 27–41. [Google Scholar]

- Becker, Marco. 2021. Zombie-Unternehmen in der Corona-Pandemie oder Phänomen der Verdeckt überschuldeten Unternehmen in Deutschland. IUCF Working Paper, No. 3. Kiel and Hamburg: ZBW—Leibniz Information Centre for Economics. [Google Scholar]

- Beißel, Stefan. 2017. Rahmenwerke für das IT-GRC-Management. In IT-GRC-Management—Governance, Risk und Compliance. Grundlagen und Anwendungen. Edited by Matthias Knoll and Strahringer Susanne. Wiesbaden: Springer Vieweg, pp. 65–81. [Google Scholar] [CrossRef]

- Berman, Noah. 2024. How Houthi Attacks in the Red Sea Threaten global Shipping. Council on Foreign Relations, January 12. Available online: https://www.cfr.org/in-brief/how-houthi-attacks-red-sea-threaten-global-shipping (accessed on 1 June 2024).

- Bömer, Michael, and Johann Weiß. 2024. Die Bedeutung der deutschen Wirtschaft für Europa. Edited by Vereinigung der Bayerischen Wirtschaft e. V. München. Available online: https://www.vbw-bayern.de/Redaktion/Frei-zugaengliche-Medien/Abteilungen-GS/Volkswirtschaft/2024/Downloads/Studie_Die-Bedeutung-der-deutschen-Wirtschaft-f%C3%BCr-Europa_final.pdf (accessed on 1 June 2024).

- Brauweiler, Hans-Christian. 2019. Risikomanagement in Unternehmen. Ein grundlegender Überblick für die Management-Praxis. 2, Erweiterte und Ergänzte Auflage. Wiesbaden: Springer. [Google Scholar] [CrossRef]

- Bülte, Jens. 2018. Strafbarkeitsrisiken für Insolvenzberater und Berater. ZIS-Abendsymposium am 6.2.2018—Strafbarkeit und Insolvenz. Mannheim: Fakultät für Rechtswissenschaften und Volkswirtschaftslehre. [Google Scholar]

- Ceritoğlu, A. Bahar. 2017. Risikomanagement in Lieferketten—Supply-Chain-Risikomanagement. In Risikomanagement in Unternehmen. Interkulturelle Betrachtungen zwischen Deutschland, Österreich und der Türkei. Edited by Stephan Schöning, Eva Handan Göğüş and Helmut Pernsteiner. Wiesbaden: Springer Gabler, pp. 269–96. [Google Scholar] [CrossRef]

- Coutinho, Leonor, Andreas Kappeler, and Alessandro Turrini. 2023. Insolvency Frameworks across the EU: Challenges after COVID-19. Discussion Paper 182, February 2023. Luxembourg: Publications Office of the European Union. Available online: https://economy-finance.ec.europa.eu/ecfin-publications_en (accessed on 1 June 2024).

- Creditreform Wirtschaftsforschung. 2023a. Insolvenzen in Deutschland. 1. Half year 2023. Neuss: Creditreform. [Google Scholar]

- Creditreform Wirtschaftsforschung. 2023b. Unternehmensinsolvenzen in Europa, 2022. Neuss: Creditreform. [Google Scholar]

- Diller, Martin. 2018. Risikomanagement in der Anwaltskanzlei—ein verdrängtes Thema?! Fehlerkultur in der Anwaltschaft ist mehr als Fehler vermeiden. Anwaltsblatt. Volume 68, Issue 7/2018. Deutscher Anwaltverein e.V. (ed.). Deutscher Anwaltverlag und Institut der Anwaltschaft. Available online: https://anwaltsblatt.anwaltverein.de/files/anwaltsblatt.de/Archiv/2018/anwbl_2018_07_heft.pdf (accessed on 1 June 2024).

- de Ruijter, A., and F. Guldenmund. 2016. The bowtie method: A review. Safety Science 88: 211–18. [Google Scholar] [CrossRef]

- Ebert, Christof. 2013. Risikomanagement Kompakt. Risiken und Unsicherheiten bewerten und Beherrschen. Berlin and Heidelberg: Springer-Vieweg. [Google Scholar] [CrossRef]

- European Parliament and European Council. 2019. Preventive Restructuring Frameworks, on Debt Relief and on Prohibitions on Activities, as well as on Measures to Increase the Efficiency of Restructuring, Insolvency and Discharge Procedures and Amending Directive (EU) 2017/1132 (Directive on Restructuring and Insolvency). Brussels: European Parliament and European Council. Available online: https://eur-lex.europa.eu/eli/dir/2019/1023/oj (accessed on 1 June 2024).

- European Parliament and European Council. 2022. Proposal for a Directive of the European Parliament and of the Council on the Harmonisation of Certain Aspects of Insolvency Law” (COM (2022) 702 final—2022/0408 (COD)). Brussels: European Parliament and European Council. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:8adadc6c-76e9-11ed-9887-01aa75ed71a1.0020.02/DOC_1&format=PDF (accessed on 1 June 2024).

- Fehl-Weileder, Elske. 2022. Insolvency statistics. In Insolvency and Restructuring in Germany. Yearbook 2023. Achern: Schultze & Braun, pp. 54–63. ISBN 978-3-9822268-8-0. [Google Scholar]

- Gassen, Joachim, and Urška Kosi. 2021. Insolvenzen: Ein Kollateralschaden der Pandemie? In TRR 266 Accounting for Transparency. Berlin and Paderborn: Humboldt Universität and Universität Paderborn. [Google Scholar]

- Gleißner, Werner, and Kay H. Hofmann. 2020. Unerwartete Unternehmensinsolvenz trotz testiertem Risikomanagement?—Lessons Learned aus der Insolvenz der Gerry Weber International AG. Der Betriebswirt 3: 139–54. [Google Scholar] [CrossRef]

- Grabner, Thomas. 2019. Operations Management. Auftragserfüllung bei Sach- und Dienstleistungen. Wiesbaden: Springer. [Google Scholar] [CrossRef]

- Gudehus, Timm. 2015. Dynamische Märkte. Grundlagen und Anwendungen der Analytischen Ökonomie. 2., neu Bearbeitete und Erweiterte Auflage. Wiesbaden: Springer. [Google Scholar] [CrossRef]

- Greve, Gustav. 2019. Organizational Burnout, 4th ed. Das versteckte Phänomen ausgebrannter Organisationen. Wiesbaden: Springer. [Google Scholar]

- Hallak, Issam. 2023. Briefing EU Legislation in Progress: Harmonising Certain Aspects of Insolvency Law in the EU. EPRS European Parliamentary ResearchService. Available online: https://www.europarl.europa.eu/RegData/etudes/BRIE/2023/745671/EPRS_ BRI(2023)745671_EN.pdf#:~:text=URL%3A%20https%3A%2F%2Fwww.europarl.europa.eu%2FRegData%2Fetudes%2FBRIE%2F2023%2F745671%2FEPRS_BRI%282023%29745671_EN.pdf%0AVisible%3A%200%25%20 (accessed on 1 June 2024).

- Heesen, Bernd, and Vinzenth Wieser-Linhart. 2018. Basiswissen Insolvenz. Schneller Einstieg in Insolvenzprävention und Risikomanagement. Wiesbaden: Springer. [Google Scholar] [CrossRef]

- Hefner, Veronika. 2020. Juristische Personen als Insolvenzverwalter? Spanien und Deutschland im Rechtsvergleich, 1st ed. Baden: NOMOS. [Google Scholar]

- Hesse, Jannika, and Martin Schneider. 2022. Unternehmensinsolvenzen: Auswirkungen der Hilfsmaßnahmen und Prognose bis 2023. Konjunktur aktuell, Ausgabe März. 2022. Available online: https://www.oenb.at/Publikationen/Volkswirtschaft/konjunktur-aktuell.html (accessed on 1 June 2024).

- Hopkin, Paul. 2017. Fundamentals of Risk Management. Understanding, evaluating and implementing effective risk management. London, New York and New Delhi: Kogan Page. [Google Scholar]

- Hunziker, Stefan, Ute Vanini, Mirjam Durrer, Philipp Henrizi, and Anjuli Unruh. 2020. Die Rolle der Risk Manager in der COVID-19 Krise. ERM Report 2020. Rotkreuz: Institut für Finanzdienstleistungen Zug IFZ der Hochschule Luzern. [Google Scholar]

- Huth, Michael, Sascha Düerkop, and Frank Romeike. 2017. RIMA-KIL—Risikomanagement für Kritische Infrastrukturen in der Logistik. Discussion Paper No 19 4/2017. Fulda: University of Applied Sciences. [Google Scholar]

- International Organization for Standardization. 2013. ISO/IEC 27001:2013—Information Security Management System. Available online: https://www.pqm.sk/certifikacia-manazerskych-systemov/akreditovane-systemy/system-manazerstva-informacnej-bezpecnosti-iso-iec-27001/?gad_source=1&gclid=CjwKCAjwhvi0BhA4EiwAX25uj6lZvwJZka5fV29l2guZmrfvXYqo-Jfgpc8gs-O_34Jfse-_cqMFkBoCMpkQAvD_BwE (accessed on 1 June 2024).

- International Organization for Standardization. 2015. ISO 9001:2015—Quality Management Systems. Available online: https://www.dnv.sk/siteassets/images/pdf-documents/sk-whitepaper-iso-9001-2015-dnv-gl---dowload.pdf (accessed on 1 June 2024).

- International Organization for Standardization. 2018. ISO 31000:2018—Risk Management—Guidelines Management du Risque—Lignes Directrices. Available online: https://shahrdevelopment.ir/wp-content/uploads/2020/03/ISO-31000.pdf (accessed on 1 June 2024).

- Kuntsche, Peter, and Kirstin Börchers. 2017. Qualitäts- und Risikomanagement im Gesundheitswesen. Basis- und integrierte Systeme, Managementsystemübersichten und praktische Umsetzung. Berlin: Springer. [Google Scholar] [CrossRef]

- Littich, Alexander, and Janika Sievert. 2019. Strafbarkeit von Beratern und InsolvenzBeratern. Wegweiser für eine risikofreie Beratung. Landshut: ECOVIS L + C. [Google Scholar]

- Mohammadzai, Gulwali, Khalid Pashtoon, and Ilhamuddin Aini. 2023. Compliance Requirement for Dealing with Risks, Governance and IT Compliance. Integrated Journal for Research in Arts and Humanities 3: 150–56. [Google Scholar] [CrossRef]

- Müller, Klaus-Rainer. 2015. Handbuch Unternehmenssicherheit. Umfassendes Sicherheits-, Kontinuitätsund Risikomanagement mit System. 3., aktualisierte und erweiterte Auflage. Wiesbaden: Springer. [Google Scholar] [CrossRef]

- Müller, Stefan. 2021a. Insolvenzen in der Corona-Krise. IWH Policy Notes No. 2/2021. Halle (Saale): Leibniz-Institut für Wirtschaftsforschung Halle (IWH). [Google Scholar]

- Müller, Stefan. 2021b. Unternehmensinsolvenzen seit Ausbruch der Pandemie. Wirtschaft im Wandel 27: 35–38. [Google Scholar]

- Rack, Manfred. 2012. Risikomanagement ohne Organisationsverschulden. Ein Handbuch zum Managementsystem für gute Unternehmensführung. Frankfurt am Main: Eigenverlag. [Google Scholar]

- Reinhart, Carmen. 2022. From Health Crisis to Financial Distress. IMF Economic Review 70: 4. [Google Scholar] [CrossRef]

- Romeike, Frank. 2017. Management von Rohstoffrisiken. In Risikomanagement in Unternehmen. Interkulturelle Betrachtungen zwischen Deutschland, Österreich und der Türkei. Edited by Stephan Schöning, Eva Handan Göğüş and Helmut Pernsteiner. Wiesbaden: Springer Gabler, pp. 117–74. [Google Scholar] [CrossRef]

- Sandqvist, Pauliina, and Timo Wollmershäuser. 2021. Analyse der Firmeninsolvenzen infolge der Corona-Pandemie und Wirkungsabschätzung finanzpolitischer Maßnahmen. Studie im Auftrag des Bundesministeriums der Finanzen im Rahmen des Forschungsauftrags fe 3/19: Rahmenvertrag Wissenschaftliche (Kurz-) Expertisen zu Grundsatzfragen der Finanz-, Steuer- und Wirtschaftspolitik. München: ifo Zentrum für Makroökonomik und Befragungen. [Google Scholar]

- Scherer, Josef. 2012. Good Governance und ganzheitliches strategisches und operatives Management: Die Anreicherung des “unternehmerischen Bauchgefühls” mit Risiko-, Chancen- und Compliancemanagement. Corporate Compliance Zeitschrift (CCZ) 6: 201–11. [Google Scholar]

- Scherer, Josef. 2019. (Compliance-) Risk Management System 4.0—The Digital Transformation of Norms, Guidelines and Standards. Frankfurt am Main: Frankfurter Institut für Risikomanagement und Regulierung, FIRM Yearbook. [Google Scholar]

- Scherer, Josef, and Klaus Fruth, eds. 2019. Das interessiert Kapitalgeber: Antifragilität und der “Achilleskörper” des Ordentlichen Kaufmanns—Vermeidung der persönlichen Haftung für Missmanagement am Beispiel “Governance, Risk und Compliance (“GRC”)” und Geschäftsprozessdigitalisierung. Frankfurt am Main: Verlag für Governance, Management, Risk & Compliance, Association for Risk Management and Regulation. [Google Scholar]

- Scherer, Josef, Frank Romeike, and Shari Gursky. 2021. Mehr Risikokompetenz für eine neue Welt. JMG Journal für Medizin- und Gesundheitsrecht 2021: 159–65. [Google Scholar] [CrossRef]

- Schürholz, Markus, and Eike-Christian Spitzner. 2019. Hardware für KI. In Künstliche Intelligenz. Technologie|Anwendung|Gesellschaft. Edited by Volker Wittpahl. Berlin and Heidelberg: Springer-Vieweg, pp. 36–47. [Google Scholar] [CrossRef]

- Sorano, Enrico, and Giovanni Lombardo. 2016. Risk management and performance in public administration, as a way to better monitor the effectiveness and efficiency of processes and administrative procedures. In Risk Management: Perspectives and Open Issues. A Multi-Disciplinary Approach. Edited by Valter Cantino, Paola De Vincentiis and Gabriella Racca. New York: Mc Graw-Hill Education, pp. 280–92. ISBN 978-0-0771-8017-1. [Google Scholar]

- Sorger, Helmut. 2008. Entscheidungsorientiertes Risikomanagement in der Industrieunternehmung. Frankfurt am Main: Internationaler Verlag der Wissenschaften. [Google Scholar]

- Troßmann, Ernst, and Alexander Baumeister. 2017. Besonderheiten des Risikomanagements bei Auftragsfertigung. In Risikomanagement in Unternehmen. Interkulturelle Betrachtungen zwischen Deutschland, Österreich und der Türkei. Edited by Stephan Schöning, Eva Handan Göğüş and Helmut Pernsteiner. Wiesbaden: Springer Gabler, pp. 297–311. [Google Scholar] [CrossRef]

- United Nations. 2023. World Economic Situation and Prospects 2023. New York: United Nations. [Google Scholar]

- von Oppen, Andreas. 2019. Positionspapier zur Richtlinie (EU) 2019/1023 über präventive Restrukturierungsrahmen, über Entschuldung und über Tätigkeitsverbote sowie über Maßnahmen zur Steigerung der Effizienz von Restrukturierungs-, Insolvenz- und Entschuldungsverfahren und zur Änderung der Richtlinie (EU) 2017/1132. Available online: https://die-dk.de/media/files/2019_09_19_DK_Positionspapier_RestruktRiLi.pdf (accessed on 19 September 2019).

- Wälder, Konrad, and Olga Wälder. 2017. Methoden zur Risikomodellierung und des Risikomanagements. Wiesbaden: Springer. [Google Scholar] [CrossRef]

- Weinbeer, Alexander. 2019. Die Größten Haftungsrisiken des Anwalts. Bonn: Typische Fälle von A bis Z. Deutscher Anwaltverlag. [Google Scholar]

- Wessing, Jürgen. 2018. Compliance in Anwaltskanzleien. ZIS—Zeitschrift für Internationale Strafrechtsdogmatik. 13th Year. Issue 9/2018. pp. 368–374. Available online: https://www.zis-online.com/dat/artikel/2018_9_1225.pdf (accessed on 1 June 2024).

- Zimmermann, Volker. 2022. Vielfältige Hemmnisse bremsen die Digitalisierungsaktivitäten deutscher Unternehmen. Ifo Schnelldienst 75: 8–11. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 2022 | 2021 | 2020 | 2019 | 2018 | Change 2021 in Percent | |

|---|---|---|---|---|---|---|

| Belgium | 9260 | 6533 | 7203 | 10,598 | 9878 | +41.7 |

| Denmark | 7818 | 8339 | 5614 | 8474 | 7155 | −6.2 |

| Germany | 14,660 | 14,130 | 16,040 | 18,830 | 19,410 | +3.8 |

| Finland | 2656 | 2473 | 2135 | 2597 | 2534 | +7.4 |

| France | 41,215 | 27,470 | 31,036 | 51,201 | 53,887 | +50.0 |

| Greece | 46 | 108 | 102 | 107 | 84 | −57.4 |

| Great Britain | 23,104 | 14,820 | 13,298 | 18,256 | 18,773 | +55.9 |

| Ireland | 500 | 401 | 575 | 568 | 767 | +24.7 |

| Italy | 7164 | 9017 | 7650 | 11,161 | 11,259 | −20.6 |

| Luxembourg | 1054 | 1199 | 1199 | 1263 | 1195 | −12.1 |

| Netherlands | 1854 | 1536 | 2703 | 3209 | 3145 | +20.7 |

| Norway | 3040 | 2688 | 4100 | 5013 | 5010 | +13.1 |

| Austria | 4913 | 3076 | 3106 | 5235 | 5224 | +59.7 |

| Portugal | 3869 | 4770 | 5000 | 5071 | 5888 | −18.9 |

| Sweden | 7266 | 6901 | 7695 | 7776 | 7599 | +5.3 |

| Switzerland | 6799 | 5127 | 4893 | 6009 | 6878 | +32.6 |

| Spain | 4755 | 4098 | 4097 | 4464 | 4131 | +16.0 |

| Total | 139,973 | 112,686 | 116,446 | 159,832 | 162,777 | +24.2 |

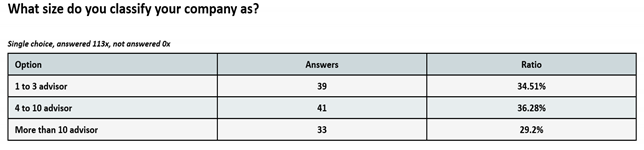

| Option | Answers | Ratio |

|---|---|---|

| 1 to 3 advisors | 39 | 34.51% |

| 4 to 10 advisors | 41 | 36.28% |

| More than 10 advisors | 33 | 29.2% |

| Question | Option | Answers | Ratio |

|---|---|---|---|

| Q. 4 In your opinion, how many of the insolvency advisors in Germany use risk management? | 0–24% | 77 | 68.14% |

| 25–49% | 28 | 24.78% | |

| 50–74% | 7 | 6.19% | |

| 75–100% | 1 | 0.88% |

| Statistic for Test: | |

|---|---|

| Question 4 (Q. 4): | In your opinion, how many of the insolvency advisors in Germany use risk management? |

| Chi-Square: | 131.142 |

| Df: | 3 |

| Asymptotic significance: | 0.000 |

| For 0 cells (0.0%), fewer than 5 frequencies are expected. The smallest expected cell frequency is 28.3. | |

| Q. 9: In which areas of your work do you use risk management? | In no area | ; p < 0.005 | Most selected in small law companies |

| Identification of compliance risks | ; p < 0.005 | Most selected in large law companies | |

| Data protection | ; p < 0.005 | Most selected in large law companies | |

| Q. 10: Which standards, internal regulations and quality seal requirements do you use as a guide for your consulting activities? | ISO 31000:2018 (ISO 2018) | ; p < 0.005 | Most selected in large law companies |

| ISO 9001:2015 (ISO 2015) | 5,836; p < 0.005 | Most selected in large law companies | |

| ISO/IEC 27001:2013 (ISO 2013) | ; p < 0.005 | Most selected in large law companies | |

| VID-CERT | ; p < 0.005 | Most selected in large law companies | |

| InsO Excellence | ; p < 0.005 | Most selected in large law companies | |

| None | ; p < 0.005 | Most selected in individual law companies | |

| Other | ; p < 0.005 | Most selected in large law companies | |

| Q. 11: Which of the following specific risk management tools and methods do you use? | Quantitative risk analysis | ; p < 0.005 | Most selected in large law companies |

| Risk scoring models | ; p < 0.005 | Most selected in large law companies | |

| None | ; p < 0.005 | Most selected in small law companies | |

| Q. 12: Which of the following methods of risk identification and assessment do you use? | Risk matrix | 3,056; p < 0.005 | Most selected in large law companies |

| FMEA | 0,483; p < 0.005 | Most selected in large law companies | |

| None | ; p < 0.005 | Most selected in small law companies | |

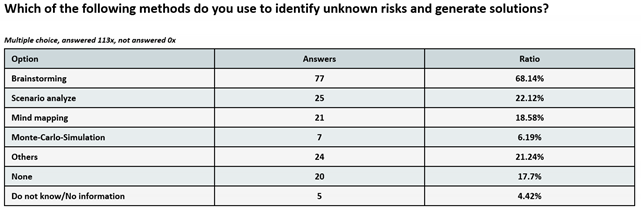

| Q. 13: Which of the following methods do you use to identify unknown risks and generate solutions? | Mind mapping | ; p < 0.005 | Most selected in large law companies |

| Monte Carlo simulations | ; p < 0.005 | Most selected in large law companies | |

| Other | ; p < 0.005 | Most selected in large law companies | |

| None | ; p < 0.005 | Most selected in small law companies | |

| Q. 16: How do you ensure in your advisory work that you receive all relevant information from clients? | Clarification | ; p < 0.005 | Most selected in individual law companies |

| Communication and information guidelines | ; p < 0.005 | Most selected in large law companies | |

| Questionnaire, checklist | ; p < 0.005 | Most selected in large law companies | |

| Status meeting | ; p < 0.005 | Most selected in large law companies | |

| Q. 17: How do you deal with the risk that clients might (unconsciously or consciously) withhold potentially critical information? | Compliance check | ; p < 0.005 | Most selected in large law companies |

| Emergency plan | ; p < 0.005 | Most selected in large law companies | |

| Other | ; p < 0.005 | Most selected in large law companies | |

| None | ; p < 0.005 | Most selected in small law companies | |

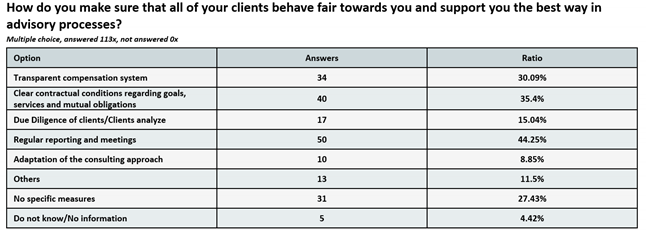

| Q. 18: How do you ensure that your clients act fairly towards you and provide you with the best possible support in the advisory process? | Transparent remuneration system | ; p < 0.005 | Most selected in large law companies |

| Due diligence | 3,770; p < 0.005 | Most selected in large law companies | |

| Adaptation of the counselling approach | ; p < 0.005 | Most selected in individual law companies | |

| None | ; p < 0.005 | Most selected in large law companies |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Seehaus, S.R.; Peráček, T. Lack of Risk Management at Insolvency Consulting Companies: An Empirical Study in Germany 2024. Adm. Sci. 2024, 14, 160. https://doi.org/10.3390/admsci14080160

Seehaus SR, Peráček T. Lack of Risk Management at Insolvency Consulting Companies: An Empirical Study in Germany 2024. Administrative Sciences. 2024; 14(8):160. https://doi.org/10.3390/admsci14080160

Chicago/Turabian StyleSeehaus, Sascha Rudolf, and Tomáš Peráček. 2024. "Lack of Risk Management at Insolvency Consulting Companies: An Empirical Study in Germany 2024" Administrative Sciences 14, no. 8: 160. https://doi.org/10.3390/admsci14080160

APA StyleSeehaus, S. R., & Peráček, T. (2024). Lack of Risk Management at Insolvency Consulting Companies: An Empirical Study in Germany 2024. Administrative Sciences, 14(8), 160. https://doi.org/10.3390/admsci14080160