The Latest Developments in Research on Sustainability and the Sustainable Development Goals in the Areas of Business, Management and Accounting

Abstract

1. Introduction

2. Methodology

2.1. The Search Protocol

2.2. The Next Steps in the Analysis

3. Results

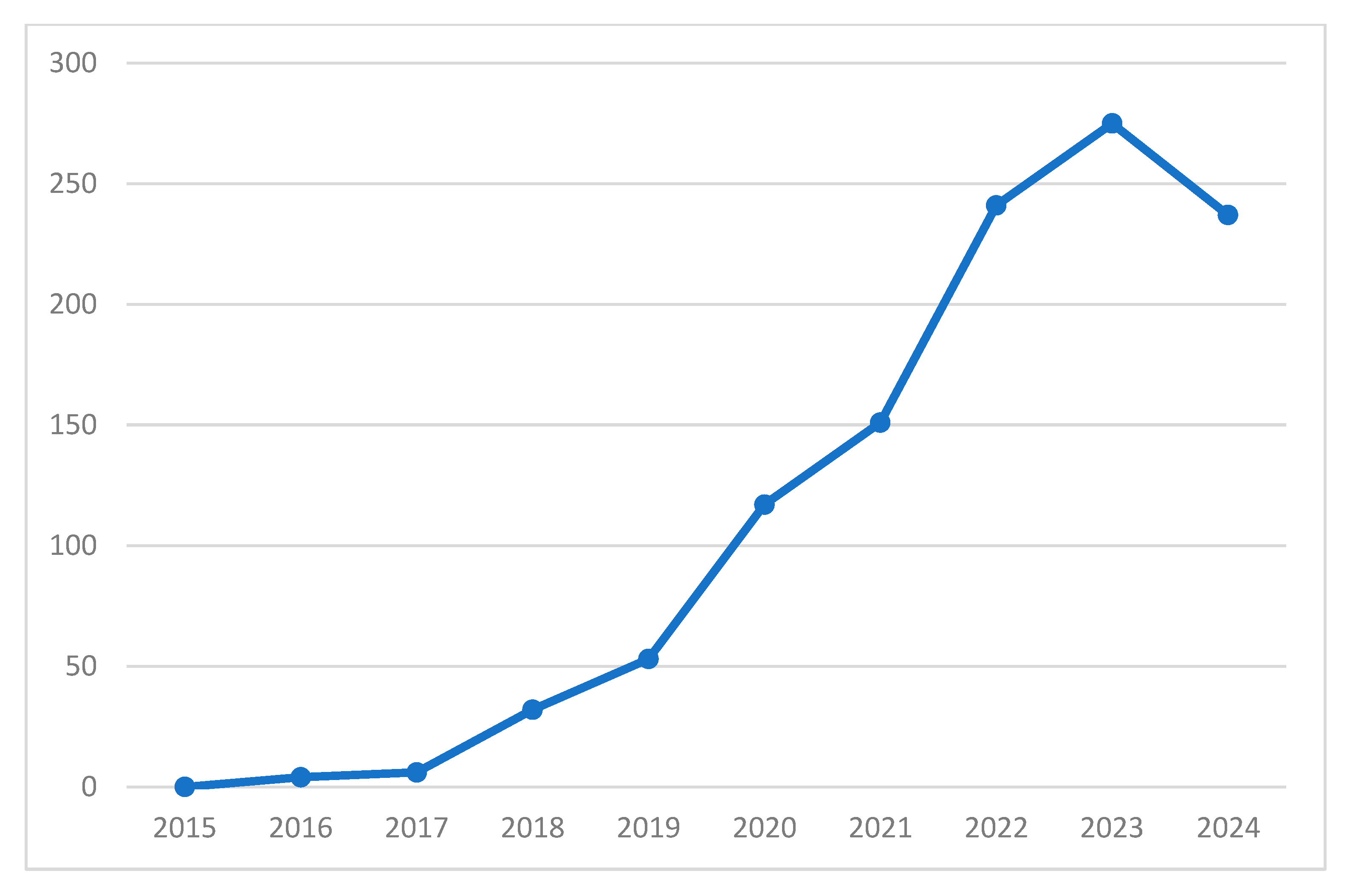

3.1. Publication Trends

3.2. Journals

3.3. Citations Analysis

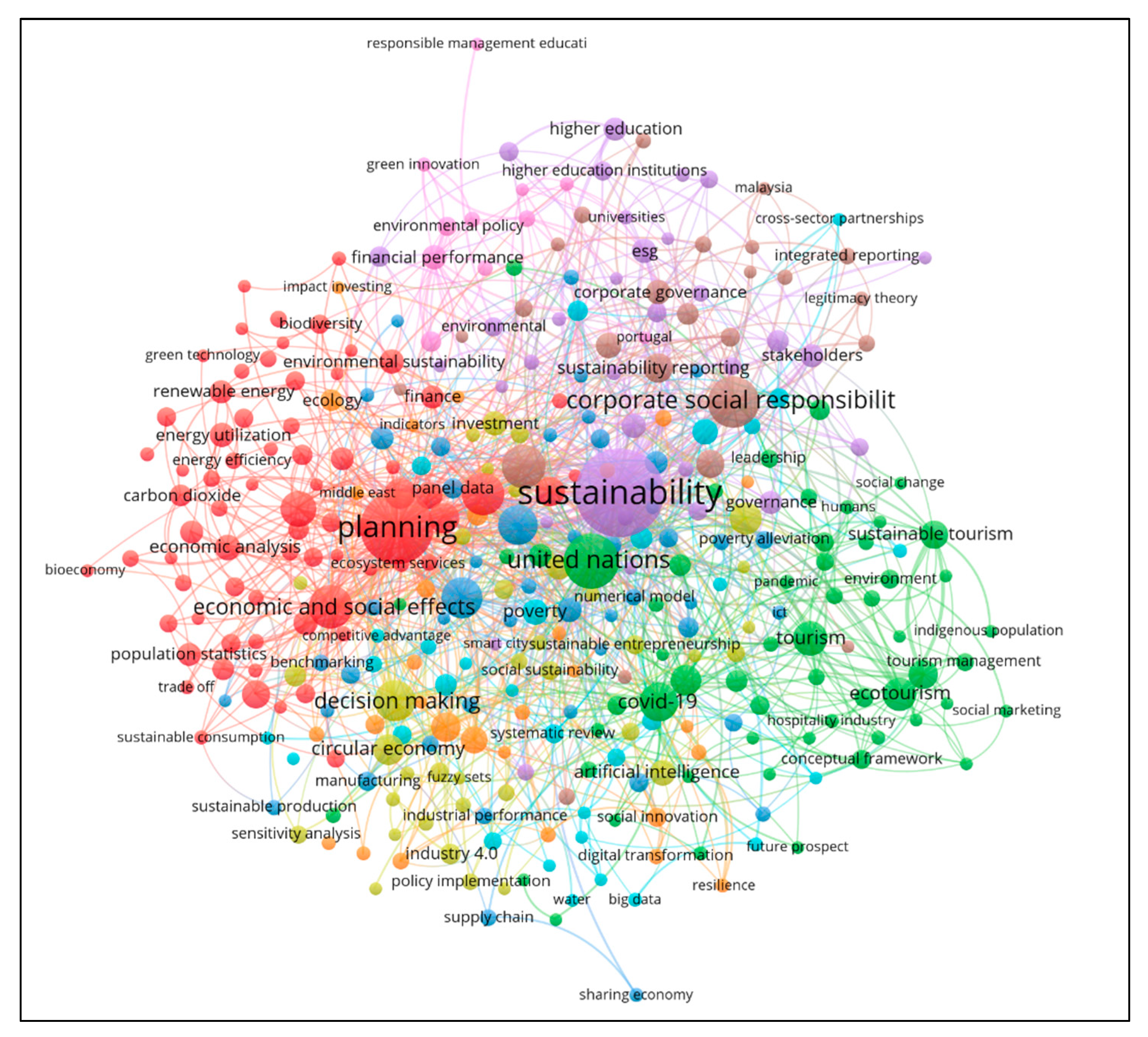

3.4. Keywords

4. The State of the Art on SDGs and Research Gaps

4.1. Business Resources: Drivers and Barriers in the Business Contribution to the SDGs

4.2. SDGs, Innovation and Business Strategies

4.3. SDGs Commitment, Business Performance and Stakeholder Engagement

4.4. Institutional Factors and Business Engagement with the SDGs

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Agrawal, Rohit, Abhijit Majumdar, Kirty Majumdar, Rakesh D. Raut, and Balkrishna E. Narkhede. 2022. Attaining sustainable development goals (SDGs) through supply chain practices and business strategies: A systematic review with bibliometric and network analyses. Business Strategy and the Environment 31: 3669–87. [Google Scholar] [CrossRef]

- Arora-Jonsson, Seema. 2023. The sustainable development goals: A universalist promise for the future. Futures 146: 103087. [Google Scholar] [CrossRef]

- Awuah, Benjamin, Hassan Yazdifar, and Hany Elbardan. 2023. Corporate reporting on the Sustainable Development Goals: A structured literature review and research agenda. Journal of Accounting & Organizational Change 20: 617–46. [Google Scholar] [CrossRef]

- Azmat, Fara, Weng Marc Lim, Abdul Moyeen, Ranjit Voola, and Girish Gupta. 2023. Convergence of business, innovation, and sustainability at the tipping point of the sustainable development goals. Journal of Business Research 167: 114170. [Google Scholar] [CrossRef]

- Banks, George C., Jeffrey M. Pollack, Jaime E. Bochantin, Bradley L. Kirkman, Christopher E. Whelpley, and Ernest H. O’Boyle. 2016. Management’s science–practice gap: A grand challenge for all stakeholders. Academy of Management Journal 59: 2205–31. [Google Scholar] [CrossRef]

- Barta, Sergio, Daniel Belanche, Marta Flavián, and Mari Cruz Terré. 2023. How implementing the UN sustainable development goals affects customers’ perceptions and loyalty. Journal of Environmental Management 331: 117325. [Google Scholar] [CrossRef]

- Bebbington, Jan, and Jeffrey Unerman. 2018. Achieving the United Nations Sustainable Development Goals: An enabling role for accounting research. Accounting, Auditing & Accountability Journal 31: 2–24. [Google Scholar] [CrossRef]

- Bebbington, Jan, and Jeffrey Unerman. 2020. Advancing research into accounting and the UN sustainable development goals. Accounting, Auditing & Accountability Journal 33: 1657–70. [Google Scholar] [CrossRef]

- Bennich, Therese, Nina Weitz, and Henrik Carlsen. 2020. Deciphering the scientific literature on SDG interactions: A review and reading guide. Science of the Total Environment 728: 138405. [Google Scholar] [CrossRef]

- Berrone, Pascual, Horacio E. Rousseau, Joan Enric Ricart, Esther Brito, and Andrea Giuliodori. 2023. How can research contribute to the implementation of sustainable development goals? An interpretive review of SDG literature in management. International Journal of Management Reviews 25: 318–39. [Google Scholar] [CrossRef]

- Biggeri, Mario, David A. Clark, Andrea Ferrannini, and Vincenzo Mauro. 2019. Tracking the SDGs in an ‘integrated’manner: A proposal for a new index to capture synergies and trade-offs between and within goals. World Development 122: 628–47. [Google Scholar] [CrossRef]

- Bose, Sudipta, and Habib Zaman Khan. 2022. Sustainable development goals (SDGs) reporting and the role of country-level institutional factors: An international evidence. Journal of Cleaner Production 335: 130290. [Google Scholar] [CrossRef]

- Bose, Sudipta, Habib Zaman Khan, and Sukanta Bakshi. 2024. Determinants and consequences of sustainable development goals disclosure: International evidence. Journal of Cleaner Production 434: 140021. [Google Scholar] [CrossRef]

- Bowen, Kathryn J., Nicholas A. Cradock-Henry, Florian Koch, James Patterson, Tiina Häyhä, Jess Vogt, and Fabiana Barbi. 2017. Implementing the “Sustainable Development Goals”: Towards addressing three key governance challenges collective action, trade-offs, and accountability. Current Opinion in Environmental Sustainability 26–27: 90–96. [Google Scholar] [CrossRef]

- Busco, Cristiano, Giovanni Fiori, Mark Frigo, and Angelo Riccaboni. 2017. Sustainable Development Goals: Integrating sustainable initiatives with long-term value creation. Strategic Finance 9: 28–37. [Google Scholar]

- Caiado, Rodrigo Goyannes Gusmão, Walter Leal Filho, Osvaldo Luiz Gonçalves Quelhas, Daniel Luiz de Mattos Nascimento, and Lucas Veigas Ávila. 2018. A literature-based review on potentials and constraints in the implementation of the sustainable development goals. Journal of Cleaner Production 198: 1276–88. [Google Scholar] [CrossRef]

- Calabrese, Armando, Roberta Costa, Nathan Levialdi Ghiron, Luigi Tiburzi, and Roberth Andres Villazon Montalvan. 2022. Is the private sector becoming cleaner? Assessing the firms’ contribution to the 2030 Agenda. Journal of Cleaner Production 363: 132324. [Google Scholar] [CrossRef]

- Carmine, Simone, and Valentina De Marchi. 2023. Addressing the complexities in implementing SDGs in international business. In International Business and Sustainable Development Goals. Progress in International Business Research. Edited by Rob van Tulder, Elisa Giuliani and Isabel Álvarez. Leeds: Emerald Publishing Limited, vol. 17, pp. 101–10. [Google Scholar] [CrossRef]

- Castaldo, Francesca, Pasqualina Porretta, and Stefania Zanda. 2024. Recovering the dormant values of accounting to navigate the challenges of the 2030 agenda and beyond. Meditari Accountancy Research 32: 1662–81. [Google Scholar] [CrossRef]

- Castro, Gema Del Río, Maria Camino Gonzalez Fernandez, and Angel Uruburu Colsa. 2021. Unleashing the convergence amid digitalization and sustainability towards pursuing the Sustainable Development Goals (SDGs): A holistic review. Journal of Cleaner Production 280: 122204. [Google Scholar] [CrossRef]

- Crane, Andrew, Guido Palazzo, Laura J. Spence, and Dirk Matten. 2014. Contesting the value of ‘creating shared value’. California Management Review 56: 130–53. [Google Scholar] [CrossRef]

- Datta, Shyamal, and Sonu Goyal. 2022. Determinants of SDG reporting by businesses: A literature analysis and conceptual model. Vision, 09722629221096047. [Google Scholar] [CrossRef]

- Di Vaio, Assunta, Rosa Palladino, Rohail Hassan, and Octavio Escobar. 2020. Artificial intelligence and business models in the sustainable development goals perspective: A systematic literature review. Journal of Business Research 121: 283–314. [Google Scholar] [CrossRef]

- Di Vaio, Assunta, Theodore Syriopoulos, Federico Alvino, and Rosa Palladino. 2021. “Integrated thinking and reporting” towards sustainable business models: A concise bibliometric analysis. Meditari Accountancy Research 29: 691–719. [Google Scholar] [CrossRef]

- Ding, Ying, Gobinda G. Chowdhury, and Schubert Foo. 2001. Bibliometric cartography of information retrieval research by using co-word analysis. Information Processing and Management 37: 817–42. [Google Scholar] [CrossRef]

- ElAlfy, Amr, Kareem M. Darwish, and Olaf Weber. 2020. Corporations and sustainable development goals communication on social media: Corporate social responsibility or just another buzzword? Sustainable Development 28: 1418–30. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Beatriz Aibar-Guzmán, Cristina Aibar-Guzmán, and Lazaro Rodriguez-Ariza. 2020a. “Sell” recommendations by analysts in response to business communication strategies concerning the Sustainable Development Goals and the SDG compass. Journal of Cleaner Production 255: 120194. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Beatriz Aibar-Guzmán, Cristina Aibar-Guzmán, and Francisco-Manuel Somohano-Rodríguez. 2022a. The drivers of the integration of the sustainable development goals into the non-financial information system: Individual and joint analysis of their influence. Sustainable Development 30: 513–24. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Cristina Aibar-Guzmán, Miriam Núnez-Torrado, and Beatriz Aibar-Guzmán. 2023a. Women leaders and female same-sex groups: The same 2030 Agenda objectives along different roads. Journal of Business Research 157: 113582. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Cristina Aibar-Guzmán, Miriam Núñez-Torrado, and Beatriz Aibar-Guzmán. 2022b. Are institutional investors “in love” with the sustainable development goals? Understanding the idyll in the case of governments and pension funds. Sustainable Development 30: 1099–116. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Davi-Jonatas Cunha-Araujo, Víctor Amor-Esteban, and Saudi-Yulieth Enciso-Alfaro. 2024. Leadership and Agenda 2030 in the Context of Big Challenges: Sustainable Development Goals on the Agenda of the Most Powerful CEOs. Administrative Sciences 14: 146. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Lázaro Rodríguez-Ariza, Beatriz Aibar-Guzmán, and Cristina Aibar-Guzmán. 2020b. Do institutional investors drive corporate transparency regarding business contribution to the sustainable development goals? Business Strategy and the Environment 29: 2019–36. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Víctor Amor-Esteban, Cristina Aibar-Guzmán, and Beatriz Aibar-Guzmán. 2023b. Translating the 2030 Agenda into reality through stakeholder engagement. Sustainable Development 31: 941–58. [Google Scholar] [CrossRef]

- Garrido-Ruso, María, Beatriz Aibar-Guzmán, and Albertina Paula Monteiro. 2022. Businesses’ role in the fulfillment of the 2030 Agenda: A bibliometric analysis. Sustainability 14: 8754. [Google Scholar] [CrossRef]

- Garrido-Ruso, María, Beatriz Aibar-Guzmán, and Óscar Suárez-Fernández. 2023. What kind of leaders can promote the disclosure of information on the sustainable development goals? Sustainable Development 31: 2694–710. [Google Scholar] [CrossRef]

- Giri, Felipe Suárez, and Teresa Sánchez Chaparro. 2023. Measuring business impacts on the SDGs: A systematic literature review. Sustainable Technology and Entrepreneurship 2: 100044. [Google Scholar] [CrossRef]

- Guarini, Enrico, Elisa Mori, and Elena Zuffada. 2022. Localizing the Sustainable Development Goals: A managerial perspective. Journal of Public Budgeting, Accounting & Financial Management 34: 583–601. [Google Scholar] [CrossRef]

- Harrison, Joseph S., Gary R. Thurgood, Steven Boivie, and Michael D. Pfarrer. 2020. Perception is reality: How ceos’ observed personality influences market perceptions of firm risk and shareholder returns. Academy of Management Journal 63: 1166–95. [Google Scholar] [CrossRef]

- Holden, E., K. Linnerud, and D. Banister. 2017. The imperatives of sustainable development. Sustainable Development 25: 213–26. [Google Scholar] [CrossRef]

- Howard-Grenville, Jennifer, Gerald F. Davis, Thomas Dyllick, C. Chet Miller, Stefan Thau, and Anne S. Tsui. 2019. Sustainable development for a better world: Contributions of leadership, management, and organizations. Academy of Management Discoveries 5: 355–66. [Google Scholar] [CrossRef]

- Hummel, Katrin, and Manuel Szekely. 2022. Disclosure on the Sustainable Development Goals—Evidence from Europe. Accounting in Europe 19: 152–89. [Google Scholar] [CrossRef]

- Ike, Masayoshi, Jerome Denis Donovan, Cheree Topple, and Eryadi Kordi Masli. 2019. The process of selecting and prioritising corporate sustainability issues: Insights for achieving the Sustainable Development Goals. Journal of Cleaner Production 236: 117661. [Google Scholar] [CrossRef]

- Ikuta, Takafumi, and Hidemichi Fujii. 2022. An analysis of the progress of Japanese companies’ commitment to the SDGs and their economic systems and social activities for communities. Sustainability 14: 4833. [Google Scholar] [CrossRef]

- Ivanaj, Silvester, Vera Ivanaj, John McIntyre, and Nuno Guimaraes da Costa. 2021. What can multinational enterprises do to implement sustainable development goals? Journal of Cleaner Production 296: 126586. [Google Scholar] [CrossRef]

- Jimenez, Dayana, Isabel B. Franco, and Tahlia Smith. 2021. A review of corporate purpose: An approach to actioning the sustainable development goals (SDGs). Sustainability 13: 3899. [Google Scholar] [CrossRef]

- Jun, Hannah, and Minseok Kim. 2021. From stakeholder communication to engagement for the sustainable development goals (SDGs): A case study of LG electronics. Sustainability 13: 8624. [Google Scholar] [CrossRef]

- Khemani, Purnima, and Dilip Kumar. 2022. Is financial development crucial to achieving the “2030 agenda of sustainable development”? Evidence from Asian countries. International Journal of Emerging Markets 18: 5009–27. [Google Scholar] [CrossRef]

- KPMG. 2022. Big Shifts, Small Steps. Survey of Sustainability Reporting 2022. Available online: https://assets.kpmg.com/content/dam/kpmg/se/pdf/komm/2022/Global-Survey-of-Sustainability-Reporting-2022.pdf (accessed on 29 September 2024).

- Kraus, Sascha, Matthias Breier, and Sonia Dasí-Rodríguez. 2020. The art of crafting a systematic literature review in entrepreneurship research. International Entrepreneurship and Management Journal 16: 1023–42. [Google Scholar] [CrossRef]

- Leal Filho, Walter, Chris Shiel, Arminda Paço, Mark Mifsud, Lucas Veiga Ávila, Luciana Londero Brandli, Petra Molthan-Hill, Paul Pace, Ulisses M. Azeiteiro, Valeria Ruiz Vargas, and et al. 2019. Sustainable Development Goals and sustainability teaching at universities: Falling behind or getting ahead of the pack? Journal of Cleaner Production 232: 285–94. [Google Scholar] [CrossRef]

- Lenort, Radim, Pavel Wicher, and František Zapletal. 2023. On influencing factors for Sustainable Development goal prioritisation in the automotive industry. Journal of Cleaner Production 387: 135718. [Google Scholar] [CrossRef]

- López-Concepción, Arelys, Ana I. Gil-Lacruz, and Isabel Saz-Gil. 2022. Stakeholder engagement, Csr development and Sdgs compliance: A systematic review from 2015 to 2021. Corporate Social Responsibility and Environmental Management 29: 19–31. [Google Scholar] [CrossRef]

- Low, See Mei, Dewi Fariha Abdullah, and Saleh F. A. Khatib. 2023. Research trend in Sustainable Development Goals reporting: A systematic literature review. Environmental Science and Pollution Research 30: 111648–111675. [Google Scholar] [CrossRef] [PubMed]

- Lukšić, Igor, Bojana Bošković, Aleksandra Novikova, and Rastislav Vrbensky. 2022. Innovative financing of the sustainable development goals in the countries of the Western Balkans. Energy, Sustainability and Society 12: 15. [Google Scholar] [CrossRef] [PubMed]

- Ma, Minxun, Nannan Wang, Wenjian Mu, and Lin Zhang. 2022. The instrumentality of public-private partnerships for achieving Sustainable Development Goals. Sustainability 14: 13756. [Google Scholar] [CrossRef]

- Mahajan, Ritika, Satish Kumar, Weng Marc Lim, and Monica Sareen. 2024. The role of business and management in driving the sustainable development goals (SDGs): Current insights and future directions from a systematic review. Business Strategy and the Environment 33: 4493–4529. [Google Scholar] [CrossRef]

- Manes-Rossi, Francesca, and Giuseppe Nicolo. 2022. Exploring sustainable development goals reporting practices: From symbolic to substantive approaches—Evidence from the energy sector. Corporate Social Responsibility and Environmental Management 29: 1799–815. [Google Scholar] [CrossRef]

- Mariani, Laura, Benedetta Trivellato, Mattia Martini, and Elisabetta Marafioti. 2022. Achieving sustainable development goals through collaborative innovation: Evidence from four European initiatives. Journal of Business Ethics 180: 1075–95. [Google Scholar] [CrossRef]

- Martínez-Falcó, Javier, Bartolomé Marco-Lajara, Eduardo Sánchez-García, and Luis A. Millan-Tudela. 2023. Sustainable Development Goals in the business sphere: A bibliometric review. Sustainability 15: 5075. [Google Scholar] [CrossRef]

- Martins, Adelaide, Manuel Castelo Branco, Pedro Novo Melo, and Carolina Machado. 2022. Sustainability in small and medium-sized enterprises: A systematic literature review and future research agenda. Sustainability 14: 6493. [Google Scholar] [CrossRef]

- Mio, Chiara, Silvia Panfilo, and Benedetta Blundo. 2020. Sustainable development goals and the strategic role of business: A systematic literature review. Business Strategy and the Environment 29: 3220–45. [Google Scholar] [CrossRef]

- Montiel, Ivan, Alvaro Cuervo-Cazurra, Junghoon Park, Raquel Antolín-López, and Bryan W. Husted. 2021. Implementing the United Nations’ Sustainable Development Goals in international business. Journal of International Business Studies 52: 999–1030. [Google Scholar] [CrossRef]

- Muhmad, Siti Nurain, and Rusnah Muhamad. 2021. Sustainable business practices and financial performance during pre-and post-SDG adoption periods: A systematic review. Journal of Sustainable Finance & Investment 11: 291–309. [Google Scholar] [CrossRef]

- Nicoló, Giuseppe, Giovanni Zampone, Serena De Iorio, and Giuseppe Sannino. 2024. Does SDG disclosure reflect corporate underlying sustainability performance? Evidence from UN Global Compact participants. Journal of International Financial Management & Accounting 35: 214–60. [Google Scholar] [CrossRef]

- Ordonez-Ponce, Eduardo, and David Talbot. 2023. Multinational enterprises’ sustainability practices and focus on developing countries: Contributions and unexpected results of SDG implementation. Journal of International Development 35: 201–32. [Google Scholar] [CrossRef]

- Ordonez-Ponce, Eduardo, and Olaf Weber. 2022. Multinational financial corporations and the sustainable development goals in developing countries. Journal of Environmental Planning and Management 65: 975–1000. [Google Scholar] [CrossRef]

- Palau-Pinyana, Erola, Josep Llach, and Llorenç Bagur-Femenías. 2023. Mapping enablers for SDG implementation in the private sector: A systematic literature review and research agenda. Management Review Quarterly 74: 1–30. [Google Scholar] [CrossRef]

- Patuelli, Alessia, Jonida Carungu, and Nicola Lattanzi. 2022. Drivers and nuances of sustainable development goals: Transcending corporate social responsibility in family firms. Journal of Cleaner Production 373: 133723. [Google Scholar] [CrossRef]

- Pham-Truffert, Myriam, Florence Metz, Manuel Fischer, Henri Rueff, and Peter Messerli. 2020. Interactions among Sustainable Development Goals: Knowledge for identifying multipliers and virtuous cycles. Sustainable Development 28: 1236–50. [Google Scholar] [CrossRef]

- Pillai, Kamala Vainy, Pavel Slutsky, Katharina Wolf, Gaelle Duthler, and Inka Stever. 2017. Companies’ accountability in sustainability: A comparative analysis of SDGs in five countries. In Sustainable Development Goals in the Asian Context. Communication, Culture and Change in Asia. Edited by J. Servaes. Singapore: Springer, vol. 2, pp. 85–106. [Google Scholar] [CrossRef]

- Pizzi, Simone, Andrea Caputo, Antonio Corvino, and Andrea Venturelli. 2020. Management research and the UN sustainable development goals (SDGs): A bibliometric investigation and systematic review. Journal of Cleaner Production 276: 124033. [Google Scholar] [CrossRef]

- Pizzi, Simone, Francesco Rosati, and Andrea Venturelli. 2021. The determinants of business contribution to the 2030 Agenda: Introducing the SDG Reporting Score. Business Strategy and the Environment 30: 404–21. [Google Scholar] [CrossRef]

- Raub, Steffen P., and Carlos Martin-Rios. 2019. “Think sustainable, act local”–a stakeholder-filter-model for translating SDGs into sustainability initiatives with local impact. International Journal of Contemporary Hospitality Management 31: 2428–47. [Google Scholar] [CrossRef]

- Rosati, Francesco, and Lourenço G. D. Faria. 2019a. Addressing the SDGs in sustainability reports: The relationship with institutional factors. Journal of Cleaner Production 215: 1312–26. [Google Scholar] [CrossRef]

- Rosati, Francesco, and Lourenço Galvão Diniz Faria. 2019b. Business contribution to the Sustainable Development Agenda: Organizational factors related to early adoption of SDG reporting. Corporate Social Responsibility and Environmental Management 26: 588–97. [Google Scholar] [CrossRef]

- Rosati, Francesco, Vinicius P. Rodrigues, Federico Cosenz, and Jason Li-Ying. 2023. Business model innovation for the Sustainable Development Goals. Business Strategy and the Environment 32: 3752–65. [Google Scholar] [CrossRef]

- Sachs, Jeffrey D., Guido Schmidt-Traub, Mariana Mazzucato, Dirk Messner, Nebojsa Nakicenovic, and Johan Rockström. 2019. Six transformations to achieve the sustainable development goals. Nature Sustainability 2: 805–14. [Google Scholar] [CrossRef]

- Salvia, Amanda Lange, Walter Leal Filho, Luciana Londero Brandli, and Juliane Sapper Griebeler. 2019. Assessing research trends related to Sustainable Development Goals: Local and global issues. Journal of Cleaner Production 208: 841–49. [Google Scholar] [CrossRef]

- Schramade, Willem. 2017. Investing in the UN Sustainable Development Goals: Opportunities for companies and investors. Journal of Applied Corporate Finance 29: 87–99. [Google Scholar] [CrossRef]

- Siegel, Jordan, Lynn Pyun, and B. Y. Cheon. 2019. Multinational firms, labor market discrimination, and the capture of outsider’s advantage by exploiting the social divide. Administrative Science Quarterly 64: 370–97. [Google Scholar] [CrossRef]

- Smith, Hannah, Roberta Discetti, Marco Bellucci, and Diletta Acuti. 2022. SMEs engagement with the Sustainable Development Goals: A power perspective. Journal of Business Research 149: 112–22. [Google Scholar] [CrossRef]

- Sousa, Manuel, Maria Fatima Almeida, and Rodrigo Calili. 2021. Multiple criteria decision making for the achievement of the UN sustainable development goals: A systematic literature review and a research agenda. Sustainability 13: 4129. [Google Scholar] [CrossRef]

- Strozzi, Fernanda, Claudia Colicchia, Alessandro Creazza, and Carlo Noè. 2017. Literature review on the ‘smart factory’ concept using bibliometric tools. International Journal of Production Research 55: 6572–91. [Google Scholar] [CrossRef]

- Sullivan, Kieran, Sebastian Thomas, and Michele Rosano. 2018. Using industrial ecology and strategic management concepts to pursue the Sustainable Development Goals. Journal of Cleaner Production 174: 237–46. [Google Scholar] [CrossRef]

- Sytnik, Olga E., Natalia V. Kulish, Sergey A. Tunin, Aleksandr V. Frolov, and Viktoria S. Germanova. 2021. Accounting as a Tool for Achieving Global Sustainable Development Goals. In The Challenge of Sustainability in Agricultural Systems. Lecture Notes in Networks and Systems. Edited by A. V. Bogoviz. Cham: Springer, vol. 206. [Google Scholar] [CrossRef]

- Trane, Matteo, Luisa Marelli, Alice Siragusa, Riccardo Pollo, and Patrizia Lombardi. 2023. Progress by research to achieve the sustainable development goals in the EU: A systematic literature review. Sustainability 15: 7055. [Google Scholar] [CrossRef]

- United Nations (UN). 2023. Times of Crisis, Times of Change. Science for Accelerating Transformations to Sustainable Development. Available online: https://sdgs.un.org/sites/default/files/2023-09/FINAL%20GSDR%202023-Digital%20-110923_1.pdf (accessed on 29 September 2024).

- United Nations (UN). 2024. The Sustainable Development Goals Report. United Nations Publications. Available online: https://unstats.un.org/sdgs/report/2024/The-Sustainable-Development-Goals-Report-2024.pdf (accessed on 29 September 2024).

- Van Zanten, Jan Anton, and Rob Van Tulder. 2018. Multinational enterprises and the Sustainable Development Goals: An institutional approach to corporate engagement. Journal of International Business Policy 1: 208–33. [Google Scholar] [CrossRef]

- Verboven, Hans, and Lise Vanherck. 2016. Sustainability management of SMEs and the UN sustainable development goals. uwf UmweltWirtschaftsForum 24: 165–78. [Google Scholar] [CrossRef]

- Vildåsen, Sigurd Sagen. 2018. Corporate sustainability in practice: An exploratory study of the sustainable development goals (SDG s). Business Strategy & Development 1: 256–64. [Google Scholar] [CrossRef]

- Wang, Shouwen, Jawad Abbas, Muhammad Safdar Sial, Susana Álvarez-Otero, and Lucian-Ionel Cioca. 2022. Achieving green innovation and sustainable development goals through green knowledge management: Moderating role of organizational green culture. Journal of Innovation and Knowledge 7: 100272. [Google Scholar] [CrossRef]

- Whiteman, Gail, Brian Walker, and Paolo Perego. 2013. Planetary boundaries: Ecological foundations for corporate sustainability. Journal of Management Studies 50: 307–36. [Google Scholar] [CrossRef]

- York, Jeffrey G., Isobel O’Neil, and Saras D. Sarasvathy. 2016. Exploring environmental entrepreneurship: Identity coupling, venture goals, and stakeholder incentives. Journal of Management Studies 53: 695–737. [Google Scholar] [CrossRef]

- Zhao, Dangzhi, and Andreas Strotmann. 2015. Analysis and visualization of citation networks. Synthesis Lectures on Information Concepts, Retrieval, and Services 7: 1–207. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Database | Scopus |

| Topic Lab | Article Title, Abstract, Keywords |

| Keywords | (sustainable development goal*) OR (sdg*) |

| Time period | From 2015 |

| Document types | Articles |

| Language | English |

| Categories | Business, Management and Accounting |

| Journal | N. of Papers |

|---|---|

| Journal of Cleaner Production | 204 |

| Business Strategy and the Environment | 57 |

| Technological Forecasting and Social Change | 57 |

| Journal of Sustainable Tourism | 50 |

| Business Strategy and Development | 27 |

| Corporate Social Responsibility and Environmental Management | 25 |

| Journal of Business Research | 20 |

| Socio Economic Planning Sciences | 16 |

| Sustainability, Accounting Management and Policy Journal | 13 |

| Utilities Policy | 12 |

| Tourism Review | 12 |

| Journal of Sustainable Finance and Investment | 11 |

| Corporate Governance (Bingley) | 11 |

| Journal of Risk and Financial Management | 10 |

| Administrative Sciences | 10 |

| Meditari Accountancy Research | 9 |

| Journal of Business Ethics | 9 |

| Journal of Innovation and Knowledge | 8 |

| International Journal of Innovation and Sustainable Development | 8 |

| Cogent Business and Management | 8 |

| Clean Technologies and Environmental Policy | 8 |

| IEEE Transactions on Engineering Management | 7 |

| Tourism Management Perspectives | 6 |

| Problems and Perspectives in Management | 6 |

| Journal of International Business Policy | 6 |

| Accounting, Auditing and Accountability Journal | 6 |

| World Review of Entrepreneurship Management and Sustainable Development | 5 |

| World Journal of Science Technology and Sustainable Development | 5 |

| World Journal of Entrepreneurship Management and Sustainable Development | 5 |

| Organization and Environment | 5 |

| Journal of Management and Organization | 5 |

| Journal of Global Responsibility | 5 |

| Journal of Applied Accounting Research | 5 |

| International Journal of Finance and Economics | 5 |

| Evaluation and Program Planning | 5 |

| Critical Perspectives on International Business | 5 |

| Annals of Tourism Research | 5 |

| Rank | Title | Author | Journal | Year | GCS |

|---|---|---|---|---|---|

| 1 | Achieving the United Nations Sustainable Development Goals: An enabling role for accounting research | Bebbington, J., Unerman, J. | Accounting, Auditing and Accountability Journal | 2018 | 547 |

| 2 | Constructing sustainable tourism development: The 2030 agenda and the managerial ecology of sustainable tourism | Hall, C.M. | Journal of Sustainable Tourism | 2019 | 408 |

| 3 | Sustainable Development Goals and sustainability teaching at universities: Falling behind or getting ahead of the pack? | Leal Filho, W., Shiel, C., Paço, A., ... Vargas, V.R., Caeiro, S. | Journal of Cleaner Production | 2019 | 357 |

| 4 | Assessing research trends related to Sustainable Development Goals: local and global issues | Salvia, A.L., Leal Filho, W., Brandli, L.L., Griebeler, J.S. | Journal of Cleaner Production | 2019 | 346 |

| 5 | Multinational enterprises and the Sustainable Development Goals: An institutional approach to corporate engagement | van Zanten, J.A., van Tulder, R. | Journal of International Business Policy | 2018 | 345 |

| Cluster | Keyword | Publication Year | Occurrences | Cluster | Keyword | Publication Year | Occurrences |

|---|---|---|---|---|---|---|---|

| 1 | Planning | 2020 | 143 | 2 | United Nations | 2021 | 83 |

| Economic and social effects | 2022 | 51 | COVID-19 | 2022 | 41 | ||

| Climate change | 2021 | 49 | Tourism | 2021 | 32 | ||

| Economics | 2021 | 34 | Ecotourism | 2021 | 30 | ||

| Environmental Protection | 2020 | 27 | India | 2021 | 27 | ||

| Investments | 2022 | 26 | Tourism development | 2021 | 24 | ||

| 3 | Developing countries | 2021 | 46 | 4 | Decision making | 2022 | 45 |

| Environmental economics | 2022 | 42 | Stakeholder | 2021 | 29 | ||

| Europe | 2022 | 17 | Circular economy | 2022 | 26 | ||

| Governance approach | 2021 | 14 | Artificial intelligence | 2022 | 19 | ||

| Consumption behaviour | 2022 | 12 | Life cycle | 2021 | 13 | ||

| Waste management | 2022 | 11 | Industry 4.0 | 2022 | 12 | ||

| 5 | Sustainability | 2022 | 206 | 6 | CSR | 2022 | 19 |

| ESG | 2023 | 17 | Poverty | 2021 | 19 | ||

| Systematic literature review | 2022 | 17 | Machine learning | 2022 | 13 | ||

| Stakeholders | 2022 | 15 | Performance | 2022 | 13 | ||

| Governance | 2022 | 14 | Sustainable cities | 2022 | 12 | ||

| Gender equality | 2023 | 13 | Economic development | 2021 | 11 | ||

| 7 | Supply chain management | 2022 | 24 | 8 | Innovation | 2022 | 50 |

| Energy | 2022 | 20 | Sustainability reporting | 2022 | 23 | ||

| Ecology | 2022 | 13 | Business | 2021 | 21 | ||

| Case study | 2022 | 12 | Corporate sustainability | 2021 | 18 | ||

| Sanitation | 2021 | 10 | Corporate governance | 2021 | 16 | ||

| Social innovation | 2022 | 10 | Integrated reporting | 2022 | 8 | ||

| 9 | Financial performance | 2022 | 16 | ||||

| Environmental performance | 2022 | 12 | |||||

| Environmental policy | 2021 | 11 | |||||

| Firm performance | 2021 | 8 | |||||

| SMEs | 2021 | 7 | |||||

| Thailand | 2020 | 7 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Minutiello, V.; García-Sánchez, I.-M.; Aibar-Guzmán, B. The Latest Developments in Research on Sustainability and the Sustainable Development Goals in the Areas of Business, Management and Accounting. Adm. Sci. 2024, 14, 254. https://doi.org/10.3390/admsci14100254

Minutiello V, García-Sánchez I-M, Aibar-Guzmán B. The Latest Developments in Research on Sustainability and the Sustainable Development Goals in the Areas of Business, Management and Accounting. Administrative Sciences. 2024; 14(10):254. https://doi.org/10.3390/admsci14100254

Chicago/Turabian StyleMinutiello, Valentina, Isabel-María García-Sánchez, and Beatriz Aibar-Guzmán. 2024. "The Latest Developments in Research on Sustainability and the Sustainable Development Goals in the Areas of Business, Management and Accounting" Administrative Sciences 14, no. 10: 254. https://doi.org/10.3390/admsci14100254

APA StyleMinutiello, V., García-Sánchez, I.-M., & Aibar-Guzmán, B. (2024). The Latest Developments in Research on Sustainability and the Sustainable Development Goals in the Areas of Business, Management and Accounting. Administrative Sciences, 14(10), 254. https://doi.org/10.3390/admsci14100254