1. Introduction

Koskela [

1] suggest a shift in the construction paradigm from the traditional approach with an emphasis on eliminating waste and associated non-value adding activities. The philosophy brought about the concept of lean philosophy in construction. Lean construction emerged in the mid-90s and its applications have since been explored by various researchers [

2,

3,

4,

5,

6,

7]. Additionally, since the mid-90s, the construction industry has been trying to adopt new concepts such as target-value design, target costing, and whole life costing as a panacea for the prevailing challenges of time and cost overrun [

8,

9]. The concept of lean construction is aimed at reducing material, resources, time and cost constraints [

10,

11,

12]. Lean construction has been criticised for its application drawbacks in terms of production demands, standardisation of construction procurement and execution processes, the cost of training of employees, requirement for cohesive teamwork, supplier constraints, decrease in construction employee morale when changes occur and the requirements for managerial changes [

11,

12,

13,

14]. Nonetheless, the benefits of lean concepts include just-in-time, responsiveness to change; effective relationship within the value stream, quality management, the last planner system, waste reduction, concurrent engineering, business process re-engineering, value-based system and teamwork, kaizen and kaizen costing [

15,

16]. The benefits of lean construction concepts in terms of being responsive to change and reducing waste in all forms during construction far outweigh the aforementioned drawbacks.

The concepts of lean construction, such as kaizen and kaizen costing in the construction industry, still require detailed theoretical conceptualisation for promoting their inherent benefits for construction industry application. There is a need for documentation of applications of lean construction concepts in the construction industry. The construction industry in many developing countries is still traditional and the prevailing problems of traditional construction approaches identified by Koskela [

1] are far from suggested mitigation measures. Hence, there is a need to explore new alternatives. Kaizen costing has been suggested as a viable alternative for mitigating the construction production challenges such as cost overrun [

17,

18,

19]. This study will consider the important factors and plausible influence of kaizen costing implementation in the construction industry, organisation and project in Nigeria.

In developed and developing nations, the performance of construction organisations has been measured through various metrics, standards and perspectives [

20,

21,

22,

23]. According to Sonson, Kulatunga and Pathirage [

15], various authors have measured the performance of construction organisations from the perspective of finance, the customer, internal business processes, learning and growth, project performance perspective, supplier perspective, environment and the community. In many construction organisations, construction projects are the main drivers for continuity and performance measurement. Ozorhon et al. [

24] and Keung and Shen [

25] opined that since the construction industry is project-based, many construction organisations require successful project completions as measures for project performance. Hence, the concept of post-project reviews has been stated as a driver for continuous improvement in construction organisations trying to implement kaizen costing [

26,

27]. Sonson, Kulatunga and Pathirage [

15] noted that the financial perspective is based on enhancing the financial value of the organisations to meet the expectations of the shareholders. Thus, successful construction projects and profitability of construction companies are indicators for growth.

When the financial perspective of construction organisations in developing countries is considered thoroughly, the prevalence in the incidence of cost overruns, fluctuations of prices, unstable inflation rates, the challenge of new project management innovation and unpredictable government regulations are observed [

28,

29,

30,

31]. An investigation conducted by Olawale and Sun [

32] into the factors inhibiting cost and time performance of construction projects in the UK revealed that the top five inhibiting factors emanate from internal elements of construction organisations participating in a project. These include design changes, inaccurate estimation of project duration, the complexity of work, risk and uncertainty, and non-performance of the project manager.

In recent times, kaizen costing has not just become a technique for cost control in the manufacturing sector but also for construction projects. Vivan et al. [

33] and Robert and Granja [

34] presented case studies of how kaizen costing has been used in the construction industry. Kaizen costing was adopted as an approach in construction cost management, but the lasting impact of the processes was not modelled into the project organisation. Omotayo, Kulatunga and Bjeirmi [

26] and Omotayo et al. [

27] also studied the implementation of kaizen and associated critical success factors without considering its implementation in construction cost management. Furthermore, the cause and effect of adopting kaizen costing in an organisation need to be studied. Hence, the studies by the abovementioned authors need to be modelled into a system of creating a construction organisation with continuous improvement. This study intends to fill this major gap in research by creating archetypes for incorporating kaizen costing in the Nigerian construction industry.

2. Kaizen Costing Implementation in Organisations and Projects

Kaizen costing is another word for continuous improvement in cost management [

35,

36]. For effective implementation of kaizen costing in construction organisations, the organisational structure must align with the principles of kaizen which is the Japanese word for continuous improvement [

35]. Rahmanian [

35] stated that one-way communication results in more complicated problems within the organisation from top to bottom. There is a need for a bilateral relationship between the lower layers and the senior management of the organisation. To further buttress the observation of Rahani and Al-Ashraf [

36], Sugimoto [

37] highlighted an effective organisation structure to enhance the morale of the employees in addition to their capability. The authors further stated that kaizen is not motivated by investment in mechanical equipment or kaizen technologies, rather kaizen is driven by investment in the managers, supervisors and front-line workers. The capacity building for these staff via kaizen accomplishments enable the tackling of evolved kaizen subjects advancing from simpler kaizen at the initial stage. Kaizen’s leading characteristics emphasizes workers’ empirical knowledge and logical thinking rather than the proceeds of the process in which these workers are involved with. Capacity building, besides, a sense of participation in developing interest in kaizen technologies will enhance the effective application of kaizen costing in construction companies.

From the perspective of kaizen costing for the Nigerian construction industry, Omotayo and Kulatunga [

20] discussed the need for kaizen costing in the Nigerian construction industry as a backdrop for implementing continuous improvement in construction cost management. Additionally, Omotayo and Kulatunga [

19] opined that kaizen costing is a cost management technique stemming from the kaizen philosophy/concept for construction cost management. A case study conducted by Vivan et al. [

33] adopted an action research approach in investigating the impact kaizen costing implementation has on project success, relying on a case study of 76 building projects in Brazil. The outcome proved that standardisation of construction procurement and execution processes is not always required for kaizen costing implementation. The standards required for kaizen costing implementation is similar to those deployed within the manufacturing environment where the processes followed in producing a product involves a set framework, time frame of activities, machines, and the plan–do–check–act principles in place. Imai [

38] argued that standardisation is required for the elimination of physical and non-physical waste when the plan–do–check–act is in place.

The main government policies and regulatory policies in Nigeria are derived from the Federal Ministry of Works and Housing. Other regulatory bodies such as the Nigerian Institute of Quantity Surveyors (NIQS), the Nigerian Institute of Architects (NIA) and the council for registered builders of Nigeria (CORBON) influence every construction organisation in Nigeria. Government policies on importation taxes, procurement methods, local content investments, figures of expatriates or foreign contractors sometimes affect the cost estimates in the traditional costing whereas regulatory compliance remains one of the catalysts identified as enabling the adoption and sustainability of kaizen costing [

39]. For kaizen to be implemented, there tends to be a need for approval from these construction regulatory bodies. Although the challenges that may emanate from that is the proper reinterpretation of kaizen application which signifies the proper modification to the country of the transfer due to incompatibility between the culture of the host country and the Japanese culture [

40]. Decision-making skills of the contractor, construction project manager, or the quantity surveyor involved in kaizen costing can influence the overall process of waste minimisation.

Kowsari [

41] advocated the need to deviate from traditional methods of costing wherein an examination of methods and activities improvement is not achievable. Traditional costing in an organisation negates effective communication and presentation of information concerning cost. This contributes to the wrong allocation of cost whereas with kaizen costing, effective communication within the organisation is encouraged thereby permitting the adequate flow of information. Kaizen costing has been partially adopted by some construction companies in developing countries such as Brazil and Chile [

33,

42]. Therefore, it is possible to adopt kaizen costing, a subject of kaizen, in Nigeria. Kaizen costing management has been known to stimulate effectiveness with staff gratification [

42]. Kaizen costing also promotes motivation within an organisational structure. Kaizen emphasises on waste and more importantly cost reduction. In ensuring the satisfactory delivery of projects to clients, kaizen is embedded with factors which encompass the improvement of relationships among the project’s stakeholders and productivity enhancement.

The importance of standardisation brings about the essence of kaizen costing. Suárez-Barraza, Ramis-Pujol and Kerbache [

43], Tetteh [

44], Suárez-Barraza and Miguel-Dávila [

45] and Omotayo and Kulatunga [

19] identified the utility of kaizen costing in engendering cost minimisation, value creation, profitability and, client satisfaction. Although further studies are required to evaluate the influence of kaizen costing on project cost overrun, researchers like Robert and Granja [

34] and Omotayo and Kulatunga [

19] have postulated that kaizen costing has the potential to mitigate the impact of cost overrun in minor and mega projects. In facilitating organisational enhancements, Ramezani and Razmeh [

46] noted that Japanese companies measured kaizen profits improvements by calculating the difference in cost set by senior managers and the estimated profit set by lower managers.

The actual cost is included in kaizen cost for cost reduction and maintenance, the overall aim of kaizen costing is to reduce and maintain the established cost within the accounting year [

46]. Overall, the main aim of kaizen costing is to enable a reduction in the incidence of all non-value added activities under established activity schedules and budgets. Cooper and Slagmulder [

47] view kaizen costing as a powerful tool for inter-organisational cost management as it provides a modus operandi for temporary multi-organisations in construction projects to operate a feed-forward cost reduction model. Cooper and Slagmulder [

47] also noted that the types of kaizen costing programs can be period-, item- and overhead-specific. Hence, it presents a cogent need to focus on the time frame, the content of the project and extra expenses which may result in cost overruns. Therefore, the strategies for implementing kaizen costing must encircle around some factors which must be evaluated for their level of importance in creating a reasonable model in the organisational planning and execution of contracts.

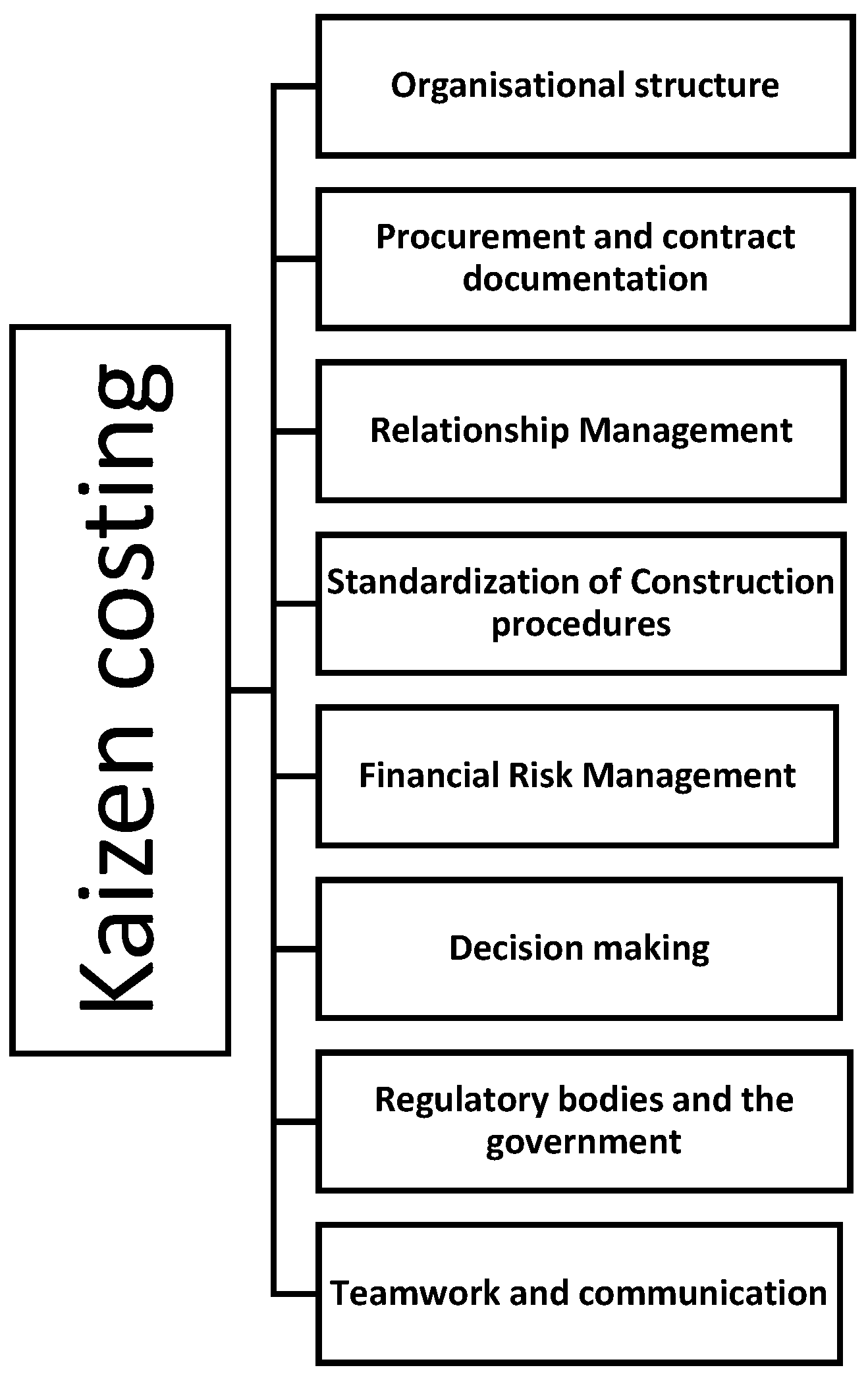

The presence of kaizen costing implementation strategies within construction organisations will further influence the deployment of kaizen costing. Authors who have identified various strategies needed for the application of kaizen costing in organisations include Puvanasvaran et al. [

48]; Shang and Pheng [

49]; Berger [

50]; Magnier-Watanabe [

51]; Chukwubuikem et al. [

52]; Arya and Jain [

53]. Some of these criteria needed for effective kaizen costing are highlighted below:

- (1)

Organisational structure: Kaizen costing thrives in a less bureaucratic management structure and where there is more teamwork and communication management. This ensures the flow of information within the company and promotes adversarial relationships between the employees and the employer. For Kaizen costing to be considered effective within the organisation, there is a need for a collective, ad-hoc and innovative system. All these are supported by Magnier-Watanabe [

51]’s remark-“

kaizen required a horizontal organisation structure and opportunistic knowledge acquisition.” Opportunistic knowledge acquisition pertains to the idea that organisations aiming to implement kaizen costing must create a learning organisation. A knowledge management database must be created for knowledge capture from post-project reviews.

- (2)

Procurement and contract documentation: The value of the project may be affected by the class of the procurement process being adopted as traditional procurement will differ from the design and build procurement system. Consequently, the contractor may possess additional resources within reach to effect (implement) the kaizen costing during project execution. More so, the stakeholders’ involvement in the project is essential during project execution. Kaizen activities may also be influenced by the estimated accuracy and “clarity of exclusions.”

- (3)

Relationship management: There is a need for managing the relationship between the stakeholders, especially in situations where claims are raised by the contractor or sub-contractor. The relationship between the client and the contractor’s cost manager determines the available resources to implement kaizen costing during construction.

- (4)

Standardisation of construction procedures: For Kaizen costing to be applied, it is essential to upgrade the construction processes to a more regulated one [

50]. Modus operandi of most of the construction companies depends on the organisation policy, nature of the projects and the regulatory bodies.

- (5)

Financial risk management: Since the project managers and the cost managers are saddled with the responsibility of monitoring the financial risk which may emanate as a result of inflation, variations, price fluctuation, building design changes, theft, kickbacks and fraudulent practices, subcontractors and suppliers cost, claims, payment delays. All these factors, in addition to preliminary items, may affect the construction project’s financial position and subsequently affects the accomplishment of kaizen costing.

- (6)

Decision making: The project cost manager’s decision during kaizen execution and follow up may impact the general outcome of kaizen costing. Litigation may ensue and affect the general performance of the kaizen costing if the “contractor or the management function in cost management is not involved in reaching some lasting decision concerning claims”; construction firms need to view “problems as opportunities” as stated by Shang and Pheng [

50]

- (7)

Regulatory bodies and the government: Several construction industries globally are impacted by the “construction regulatory bodies,” politics and government policies. Without the approval of the kaizen costing as a method of post-contract cost monitoring by the regulatory bodies, they may not be utilised. Nevertheless, some of these bodies, due to their flexibility, are not concerned about innovation as such within construction companies.

- (8)

Teamwork and communication: Kaizen team are involved in the kaizen costing processes in addition to the project or cost manager. This team essentially needs to function along with every stakeholder on the project including the clients, building materials suppliers and the sub-contractors. Communication is imperative in strategic management, construction planning and execution of the kaizen costing. As a result, consistent site meeting and post-project review meetings are essential. Communication may be easier among the stakeholder in most cases where Building Information Modelling (BIM) is being applied during the pre-tender stages.

It is important to note that these aforementioned criteria for kaizen costing are from different developing countries in South America and Asia. There are no specific criteria for kaizen costing implementation in the Nigerian construction industry. For successful kaizen costing on construction projects, the above-mentioned strategies are the main prerequisites as acknowledged by different studies. Further to this, kaizen costing and the financial perspective of evaluating the performance of construction companies must align; this alignment is a major gap in research and practice requiring a structured model.

Aim and Scope of the Study

This study aims to evaluate the criticality of the aforementioned factors in

Section 2 for a systemic implementation of kaizen costing as a planning and execution tool for cost control on construction projects by construction organisations in a developing country such as Nigeria.

Previous studies have only considered the implementation of kaizen costing from the theoretical angles of projects, construction companies and the industry [

33,

49,

50,

51,

52,

53]. This study will create and validate the initial causal loop diagram. Associated archetypes from causal relationships between construction professionals, project, construction company and the construction industry will be developed as part of the process improvement framework. This study will not empirically assess the extent to which the archetypes operate in a construction organisation but will provide a capability maturity model for possible implementation.

3. Research Methodology

The survey strategy was adopted for data collection because it provided an opportunity to reach out to a wider population with a narrow scope of questions [

54]. The research instrument targeted Construction Project Managers and Quantity Surveyors in Nigeria. The purposive sampling approach was adopted because of the scope of the study which addresses financial and project process changes. The purposive sampling was important in selecting the respondents with the median years of experience of 15 years. The median years of experience of 15 years were selected to accommodate early career, mid-career and established Construction Project Managers and Quantity Surveyors. The respondents are mostly mid-level management positions who have the background of construction process planning and cost control.

The respondents who were mainly Quantity Surveyors and Construction Project Managers were contacted based on the purposive sampling approach. The nature of the respondents’ construction organisations is small- and medium-scale, who engage in building construction and have the government as the main client. The questions asked in the research instrument sought to extract the perspectives of the respondents using the 5-point Likert scale format. The questionnaire was designed to evaluate the perception of the respondents on the criticality or otherwise of the eight (8) broad factors which had been mentioned in the literature review. The 5-point Likert scale has the highest (5) as extremely important and the lowest as not-important. Please refer to

Table A1 in the

Appendix A for the structure of the Likert Scale.

A comparison of traditional cost management tools and the relatively new kaizen costing were presented to the respondents for feedback. The feedback from the respondents provided a 54% response rate whereby one hundred and thirty-five (135) questionnaire were returned for analysis out of the targeted two hundred and fifty (250) samples. Seventy-seven (77) Quantity Surveyors and fifty-eight (58) Construction Project Managers formed the 54% response rate. The analytical hierarchy process (AHP) was used for the statistical data analysis. The AHP was used in deciding the most applicable criteria to be fed into the causal loop diagram. The utilization of a systems thinking approach afterwards culminated in the development of causal loop diagrams for exploring the patterns observed in the data. These causal loop diagrams were further validated through three (3) expert opinions as elicited through follow-up interviews. The constraints in validating the initial model led to the limitations in the number of experts for this study. Further details on the limitations of data collection and validation in this study have been discussed in

Section 8.

3.1. Analytical Hierarchy Process (AHP)

Analytical hierarchy process allows the decision-makers within an organisation to make better decisions when confronted with various alternatives [

38]. This technique also ensures that the best alternatives are selected rationally. This theory utilized pair-wise comparisons of individual judgement to prioritize the alternatives which have been scaled. Saaty’s absolute scale of 1–9 provides a major reference point of perceiving the degree of importance of criteria from the perspective of the respondent [

55]. However, due to a large number of respondents in the investigation, the weighted factors of the 5-point Likert scale figures were being used. The scale will be from 1 to 5 having the options of kaizen costing. The interpretation of 1 to 5 scale for kaizen costing is based on agreement and importance, respectively.

3.2. AHP Analysis: Important Kaizen Costing Criteria

The various levels of the analytical hierarchy process start from the decision to choose the best method for project cost control. The second level has the main alternatives which are kaizen costing, while the third level has the critical success factors which determine the level of importance for each alternative. The AHP process will be used to determine the most important criteria for implementing kaizen costing in Nigeria.

From

Figure 1, the second level of this AHP diagram highlights various critical success factors which are categorized into eight (8) different criteria, namely organisational structure (ORGSTR), contract documentation and procurement (CONDPRO), construction process (CONPROS), government and regulatory influence (GOVREGI), financial risk management and litigation (FRMLITI), communication and teamwork (COMTEM), decision making (DECMAK) and lastly relationship management (RELMAN).

Achu, Thomas and Reghunath [

56] expressed the equation for the pairwise comparison which reduces the conceptual complexity of the problem by considering two components simultaneously concerning the elements in the immediate high-level hierarchy by developing a comparison matrix, which is expressed as follows:

where

Hence, the eigenvalues are products of divisions between the weights. The importance of each criterion’s eigenvalues was normalised by comparing each of them with the overall eigenvalues of the pairwise comparison matrices.

5. Systems Thinking

Systems thinking has been described as an analytical tool for expressing complex independent decision-making issues, whereby causal loop diagrams are used to create relationships between influential attributes [

27,

57,

58]. Systems thinking is the first stage in the development of a dynamic system [

59,

60]. In this study, systems thinking will only be used as a feasibility approach to understanding the archetypes required for systems dynamics. Systems thinking archetypes are subsections of the causal loop diagram revealing cogent structures of attributes [

45].

The initiative of systems thinking seeks to reveal attributes and phenomena outside the sphere of qualitative and quantitative analysis [

59,

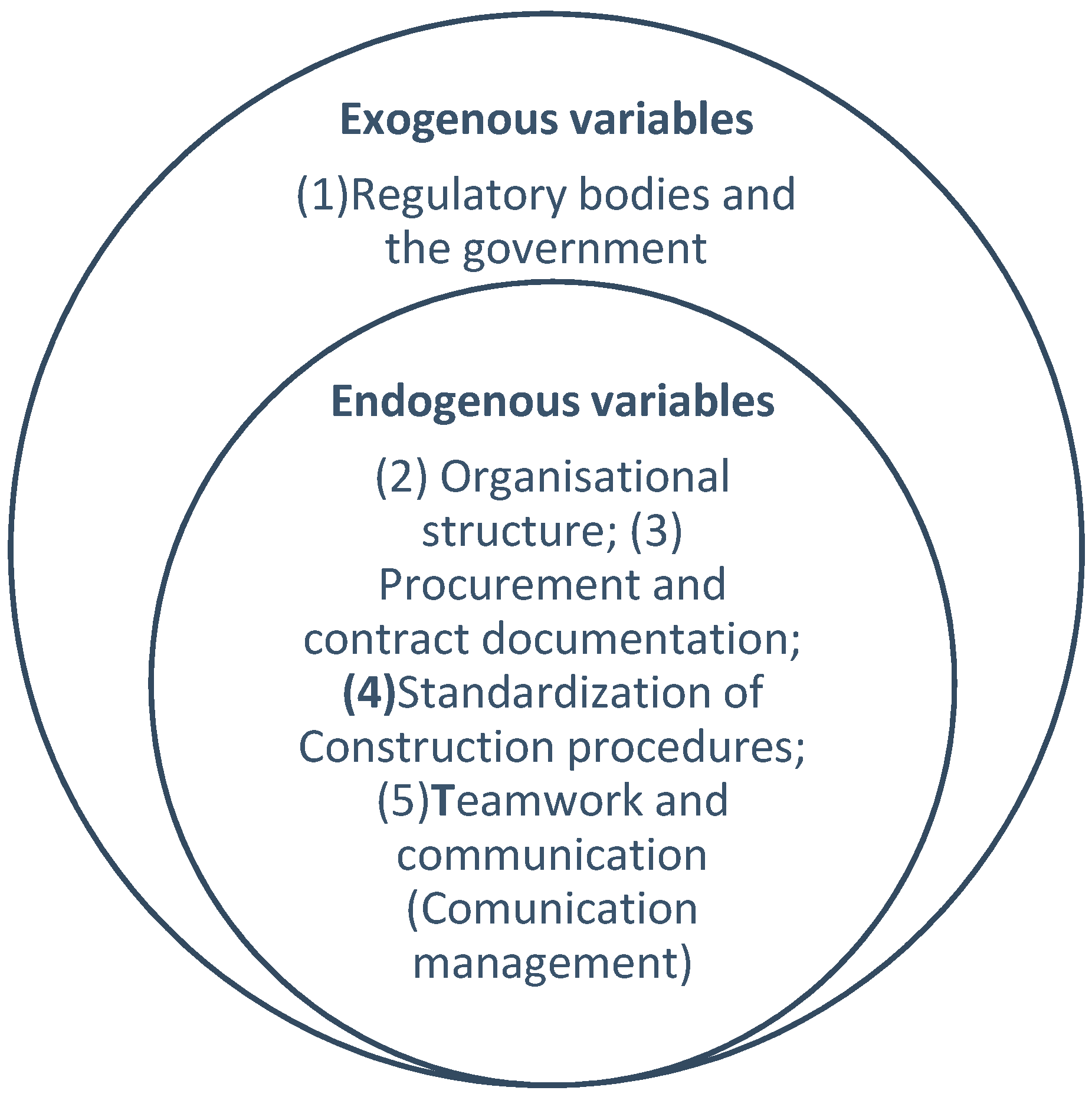

60]. In systems thinking, exogenous and endogenous variables interact to reveal what will likely happen in instances where a positive change may lead to an increase or a decrease in an attribute. The endogenous and exogenous variables, as extracted from the literature review in

Section 2 are presented below.

Figure 2 reveals that the only exogenous variable for the causal loop diagram is the regulatory body and the government. All other variables are endogenous. The above-listed variables will be expanded in the causal loop diagram. Thus, a causal loop system will indicate a reinforcing loop or a balancing loop in a counter-clockwise or clockwise direction. Teamwork and communication as communication management will be included in the causal loop diagram because of the flow of causal loops.

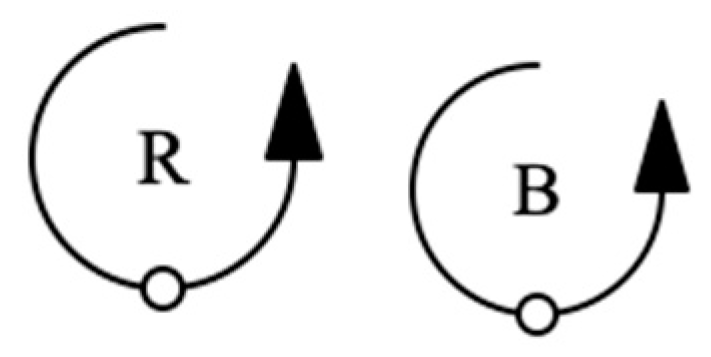

In

Figure 3, within the causal loop diagrams, the arrows indicating the directions can either have a positive (+) or negative sign (−). These signs reveal the impact one attribute may have on another. For instance, an increase in the cost of production will raise prices. Therefore, the cost of production attribute will have a positive sign right at the end of the arrow. Many authors have suggested that the first attribute in a causal loop diagram must always start with a (+) sign.

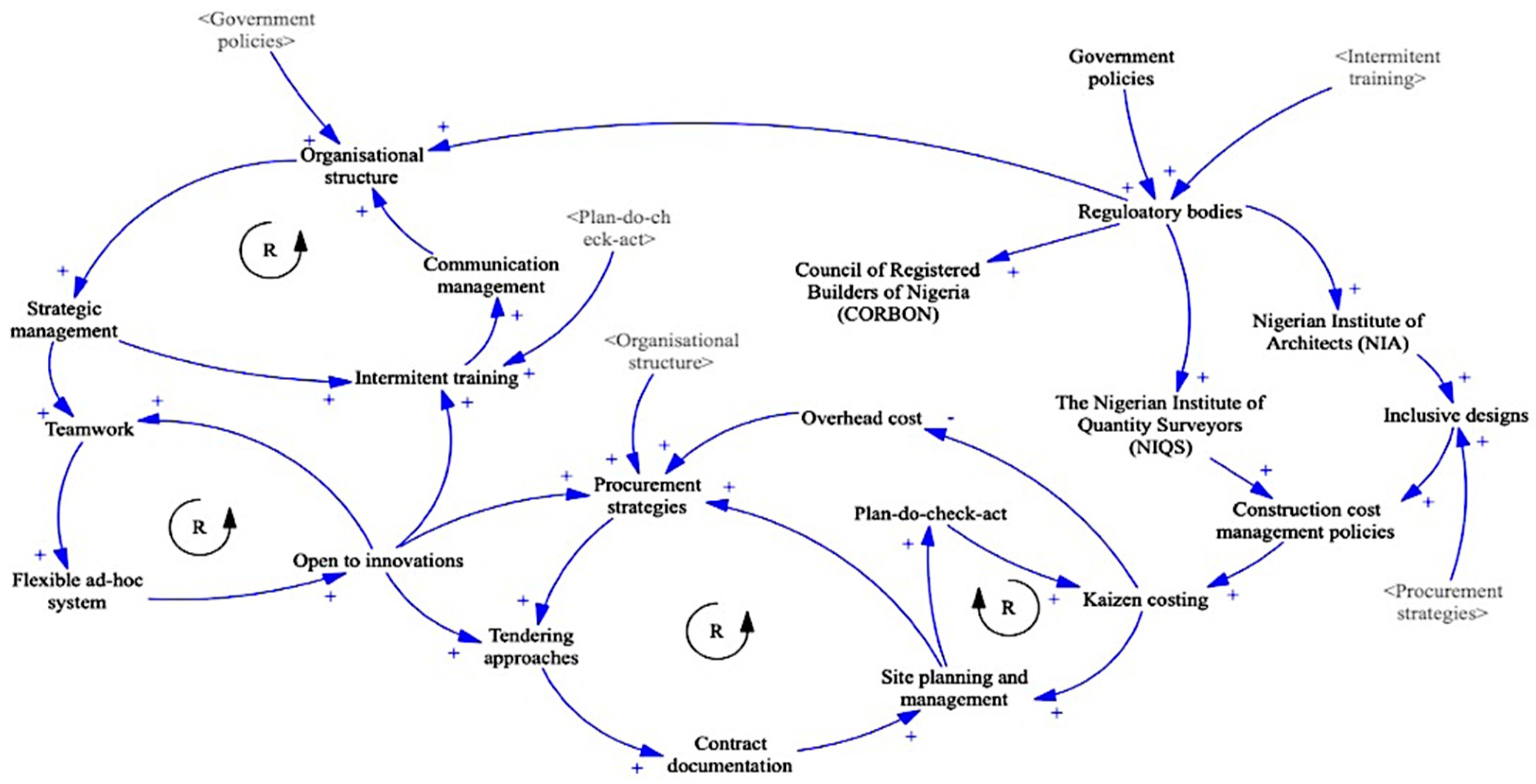

5.1. Implementing Kaizen Costing through Systems Thinking Causal Loop Diagram

The content of

Figure 2, which contains the exogenous and endogenous variables, was used to create the initial causal loop diagram in

Figure 4. From the content of

Figure 4, more attributes were discovered during the process of creating the causal loop diagram. For instance, strategic management and intermittent training were mapped into the combination of communication management and organisational structure.

The purpose of creating the causal loop diagram is to identify unidentifiable attributes. For a successful investigation into the adoption and implementation of kaizen costing in the Nigerian construction industry, there is a need to provide a system thinking model through the cause-and-effect approach [

27]. The positive organisational structure creates effective strategic management. Intermittent training is required for communication management. Government and regulatory bodies have been broken down into the major construction industry regulatory bodies such as the council or registered builders of Nigeria (CORBON); the Nigerian Institute of Architects (NIA); and the Nigerian Institute of Quantity Surveyors (NIQS). The regulatory bodies positively influence the organisational structure. A positive procurement process creates a loop of tendering, contract documentation and site planning and management leading to the plan–do–check–act principles for kaizen costing.

The initial causal loop diagram in

Figure 4 contains reinforcing loops which are building from positive interactions between the attributes. The reinforcing loops (R) were not numbered because the final discussions of the loops will be conducted after the validation process.

Figure 4 is an original causal loop diagram which will be validated with expert interviews.

5.2. Validation of the Models: Expert Opinions

Due to the cross-sectional nature of this study, three (3) respondents who have worked in the Nigerian construction industry for a mean range of 26 years as Construction Project Managers (2 respondents) and a Quantity Surveyor (1 respondent) were contracted to evaluate the initial causal loop diagram. The comments raised by the three experts were used to review the causal loop diagram and the associated changes have been stated in

Table 4. The questions asked for the validation problems around the application, content, flow, structure and additional attributes for the causal loop diagram. The process of analysing the content of the experts’ responses follows the protocol of content analysis whereby:

- (1)

There is a transcription of the responses

- (2)

The clear objectives of the questions were compared to the responses provided by the three (3) experts

- (3)

The categorisation of the responses is compiled in

Table 4- (4)

Structured commonalities were reviewed in the table. However, the responses are dissimilar

In

Table 4, the “CODE “ represents Quantity Surveying (QS) expert (EXP) was identified as EXP1-QS, and the Construction Project Managers (CPM) are identified as EXP2-CPM1 and EX3P-CPM2. The changes proposed by the respondents involved in the validation have been highlighted in red within the validate causal loop diagram (

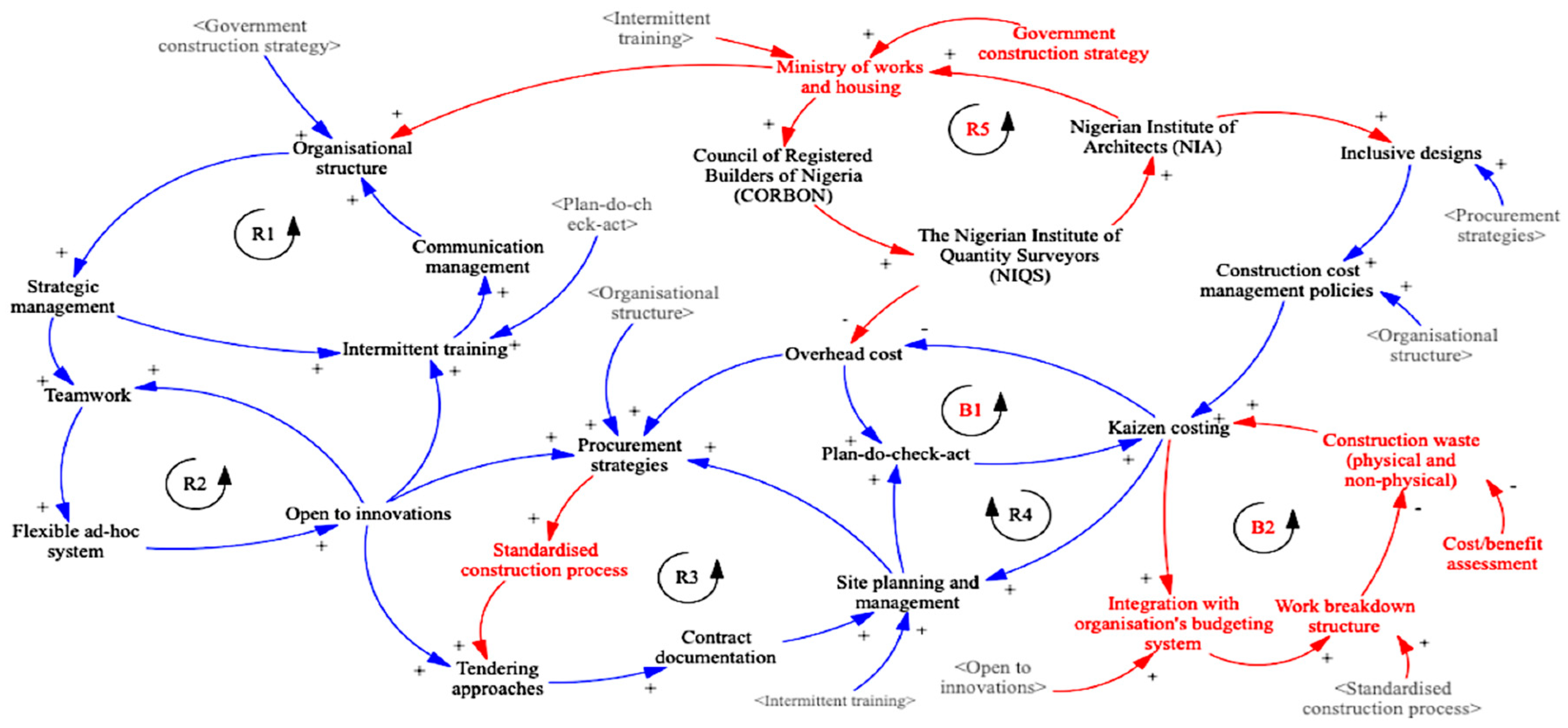

Figure 5). The new attributes identified during the causal loop diagram are the “integration with the organisation’s budgeting system”, “work breakdown structure”, and “cost–benefit assessment”. The changes also highlight new numbered balancing and reinforcing loops. The experts opined that the initial causal loop diagram did not have a negative attribute and a balancing loop must be included. The government construction strategy replaced government policy. The regulatory bodies attribute was removed, and a loop has been created for the main regulatory bodies such as CORBON, NIQS and NIA. The attributes in red are the new attributes which emerged from the validation process. Two (2) balancing loops emerge and five (5) reinforcing loops were constructed.

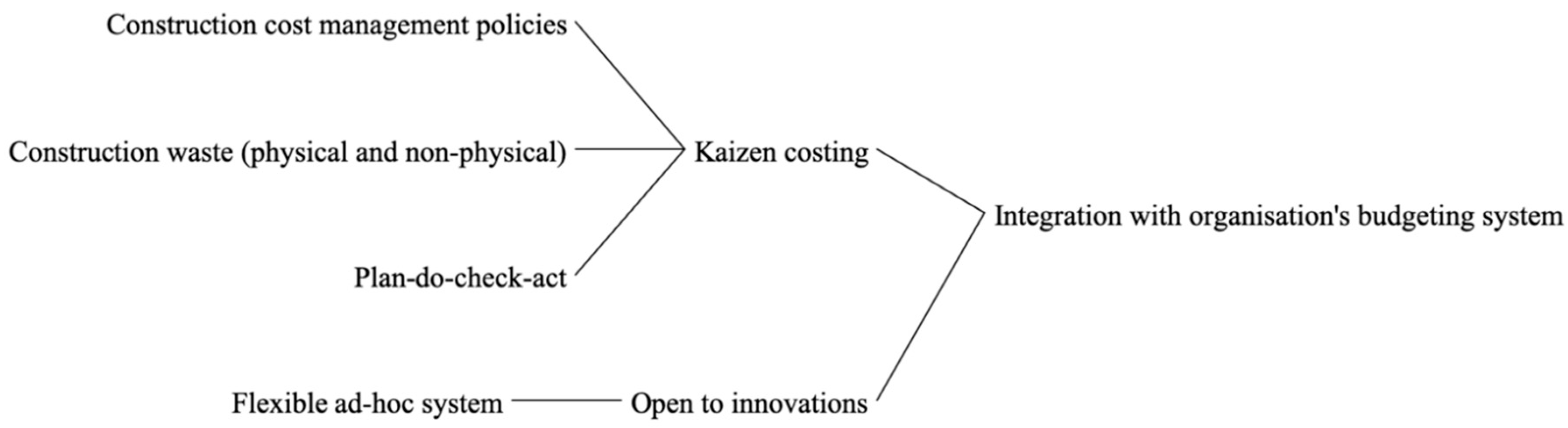

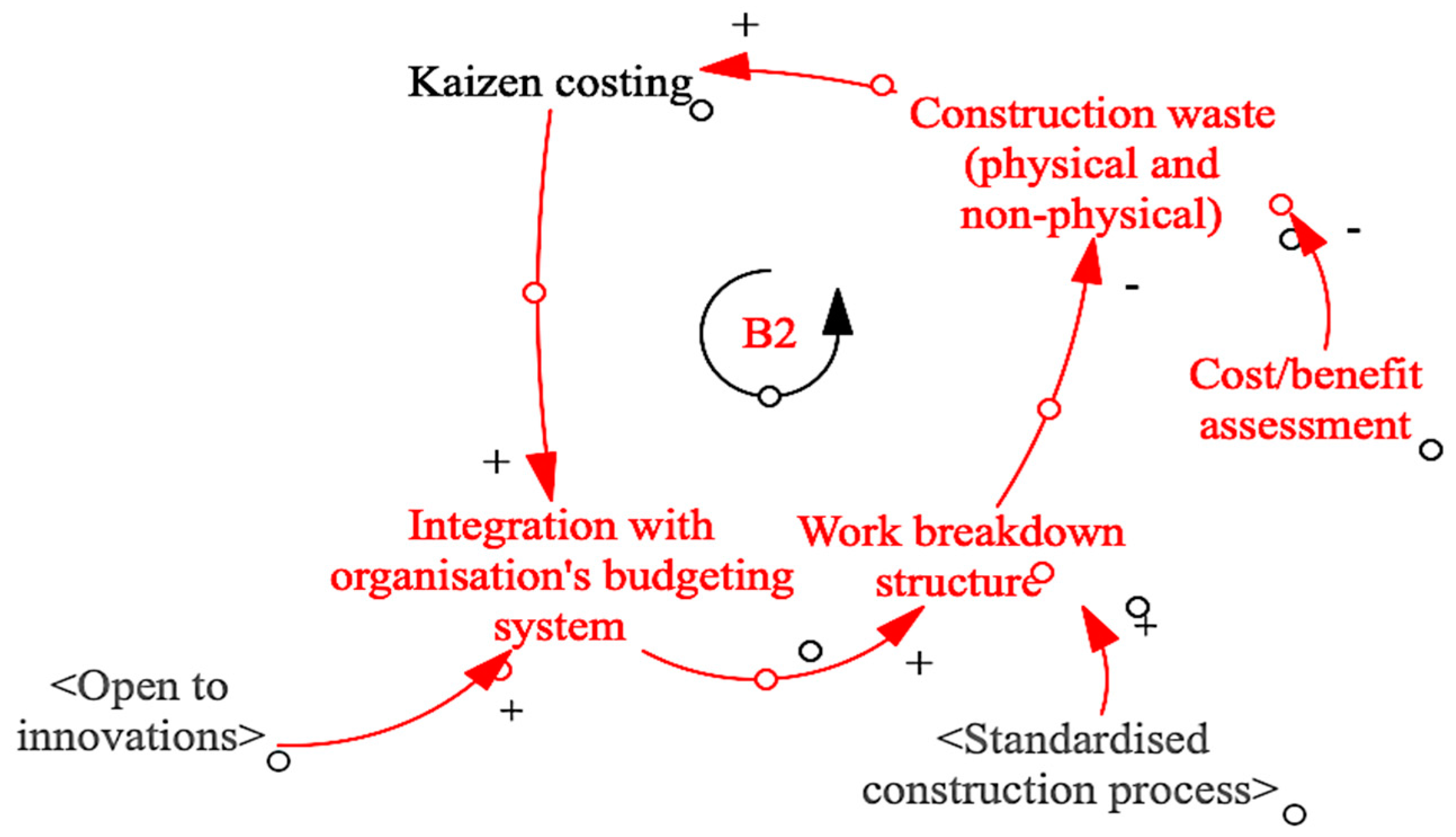

The kaizen costing loop in

Figure 6 emanates from a balancing loop structure whereby the integration of kaizen costing in the budgeting system of an organisation is positively influenced by the organisation’s willingness to allow innovations, which may lead to work breakdown structure improvements and a reduction in construction waste. The standardised process is crucial for waste reduction and an evaluation of the cost and benefits of activities will further reduce physical and non-physical construction waste. Flexibility and openness to innovation in an organisation are two major attributes that construction companies in developing countries require for an integration of kaizen costing in the budgeting system. The interaction of this structure will be discussed further under balancing loop B2.

6. Discussion of Kaizen Costing Archetypes

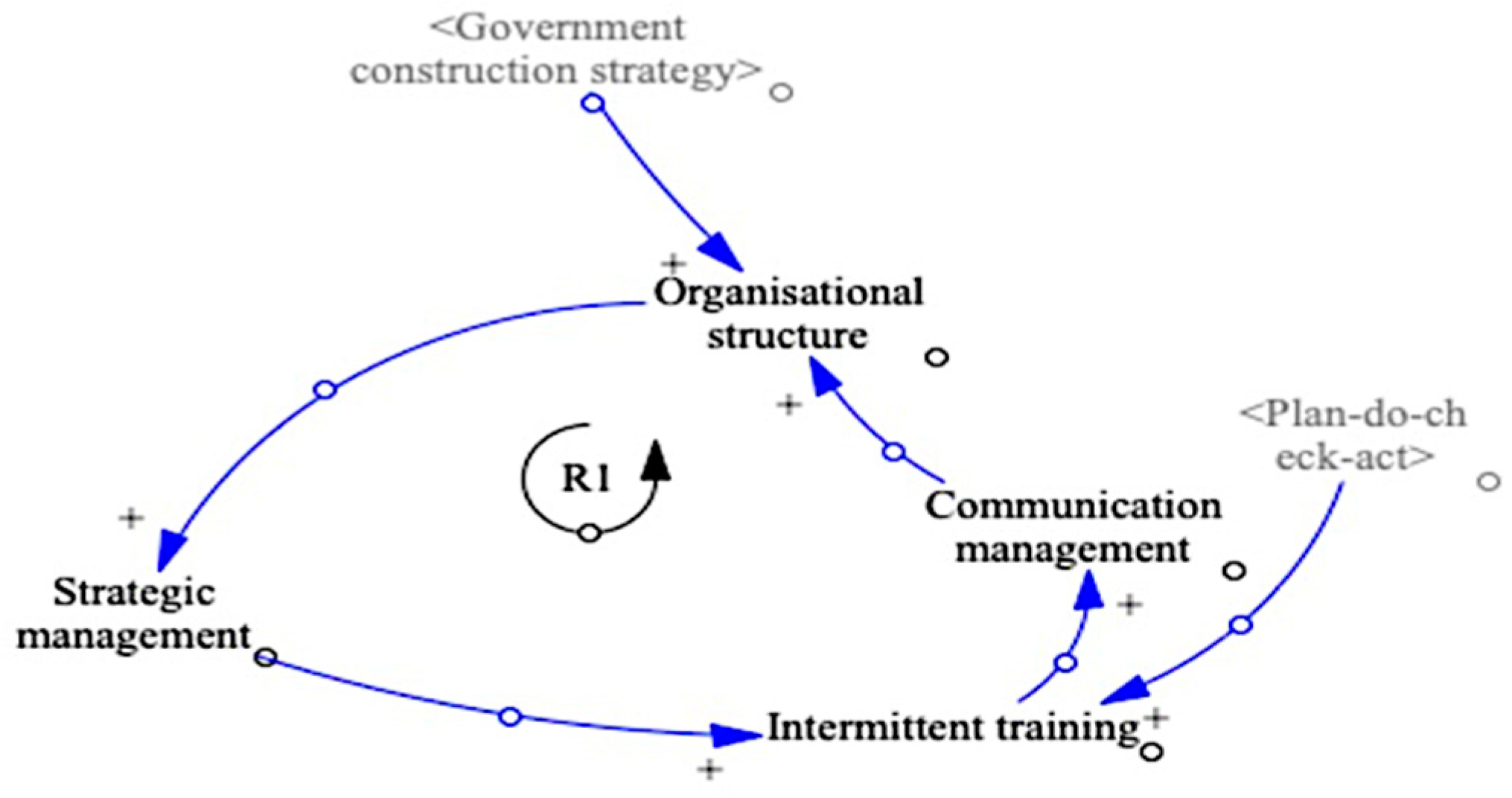

The archetypes are both reinforcing and balancing loops which can be pieced together to form the causal loop diagram. From

Figure 5, seven (7) archetypes were extracted. These archetypes are five (5) reinforcing loops (R1–R5) and two (2) balancing loops (B1 and B2). Reinforcing loop 1 (R1) has two exogenous variables influencing the archetype. These exogenous variables are government construction strategy and the plan–do–check–act principle. Year government budget for infrastructure development in Nigeria dictates the direction an organisational structure and the Nigerian construction industry will gravitate towards. A favourable government construction policy can enhance the management strategy. Omotayo et al. [

27] argued that improving the strategic management of a construction company may promote the essence of innovation through training and thus, improve the communication in an organisation.

Furthermore, the plan–do–check–act principle, otherwise known as the “Deming Wheel”, is the basis of kaizen costing [

27,

34,

47]. For a detailed implementation of kaizen costing, kaizen costing personnel must plan by identifying and analysing the problem which may occur; before the problems manifest, the potential solutions are tested on a small scale and measured (do); the results are studied for effectiveness (check), and the solutions can then be implemented (act). The plan–do–check–act principle is cyclical and provides a proactive solution to problems before they occur. In reinforcing loop R1, the plan–do–check–act is integrated into the organisational structure of a construction company in Nigeria as a proactive measure for productivity enhancement in planning, budgeting and management as illustrated in

Figure 7.

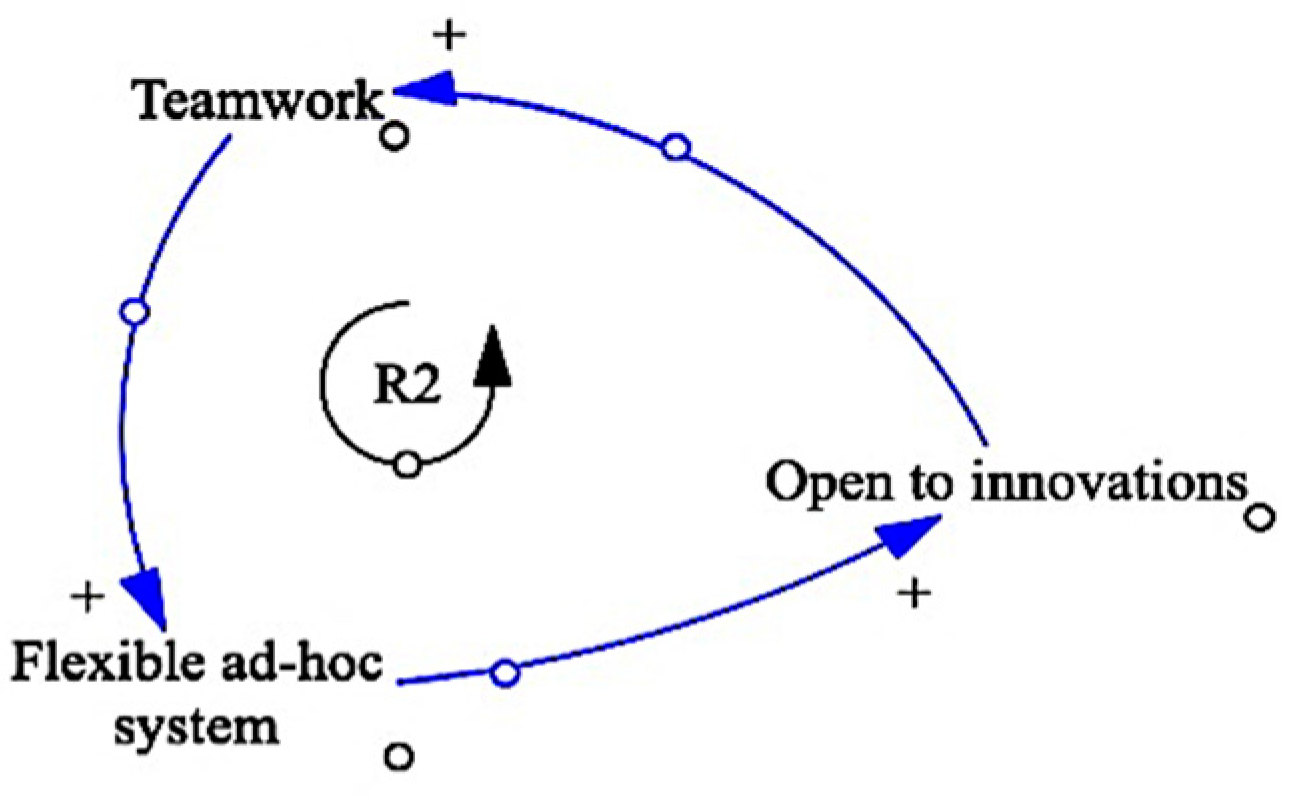

Figure 8 illustrates archetype 2 the reinforcing loop 2 (R2). The structure of R2 starts with teamwork which positively influences an increase in a flexible ad-hoc system. The flexible ad-hoc system creates more openness to innovations in a construction company. The flexibility and openness of a construction organisation is a key attribute for the furtherance of teamwork. Teamwork, flexible ad-hoc system and openness to innovation can facilitate the emergence of a learning organisation. Intermittent training influences R2 from strategic management in R1. A learning organisation provides a structure of continuous learning for its employees and management [

20,

22]. Thus, for kaizen costing to emerge in an organisation, openness to learning from previous mistakes through post-project reviews must be identified.

Archetype 3 in

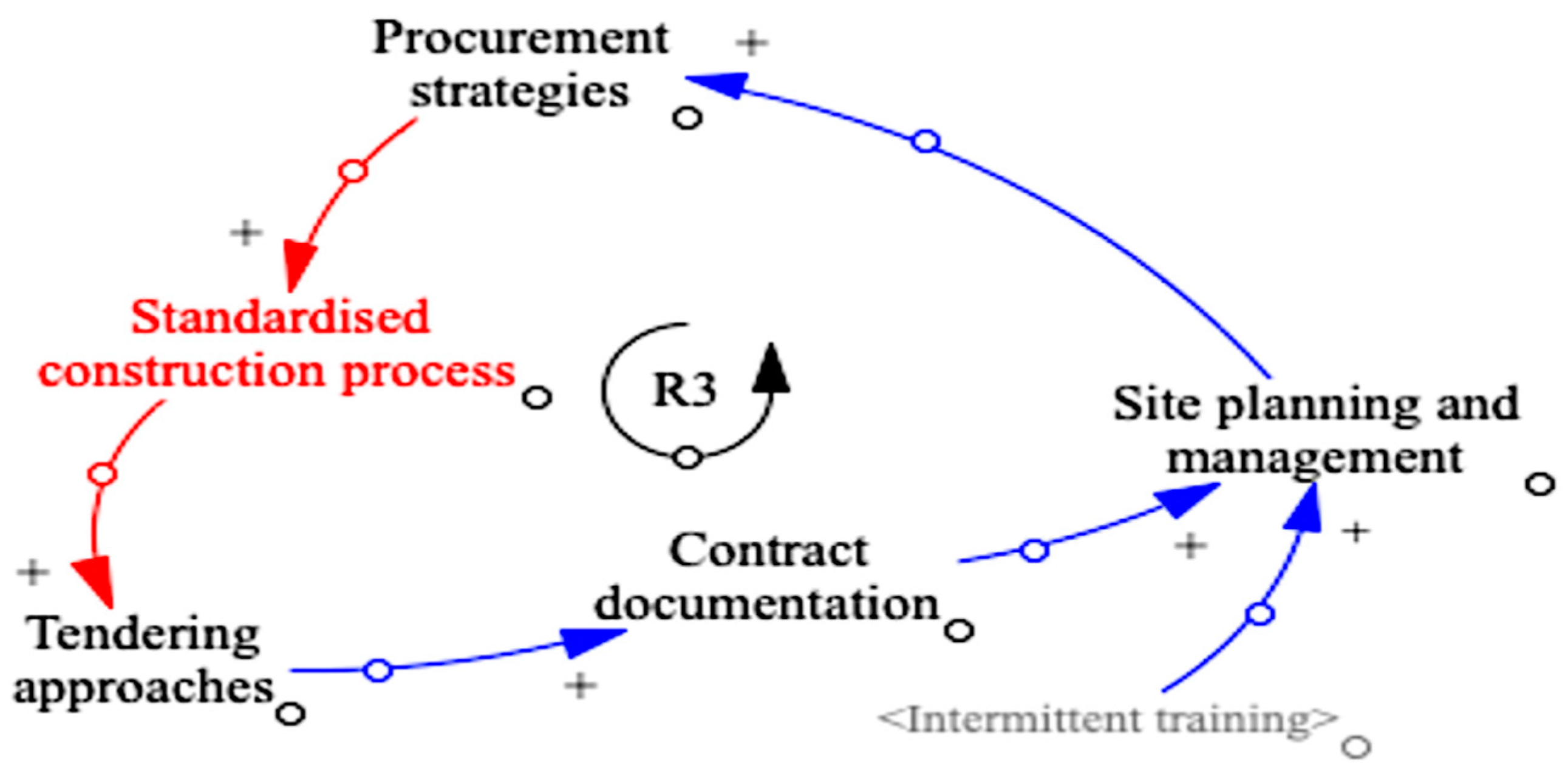

Figure 9 illustrates reinforcing loop 3 (R3) with procurement strategy influencing the standardisation of the construction process positively. Standardisation has been argued to be a major driver for kaizen costing implementation in

Section 2 of this article. Standardisation of the construction process was also mentioned by one of the reviewers during the validation process of the causal loop diagram. Standardisation of the construction process starts with procurement, contractor selection and contract documentation. Consequently, the planning phase of construction must have defined standards before the execution phase of the project. Standardisation is required to stabilise the structure of any construction organisation for continuous improvement. An increase in standardisation can provide a positive tendering arrangement, and an excellent tendering arrangement can lead to better contract documentation. When there is favourable contract documentation for all interested parties, the site planning and management activities will yield positive results. A feedback mechanism through post-project reviews will further improvements in the procurement process.

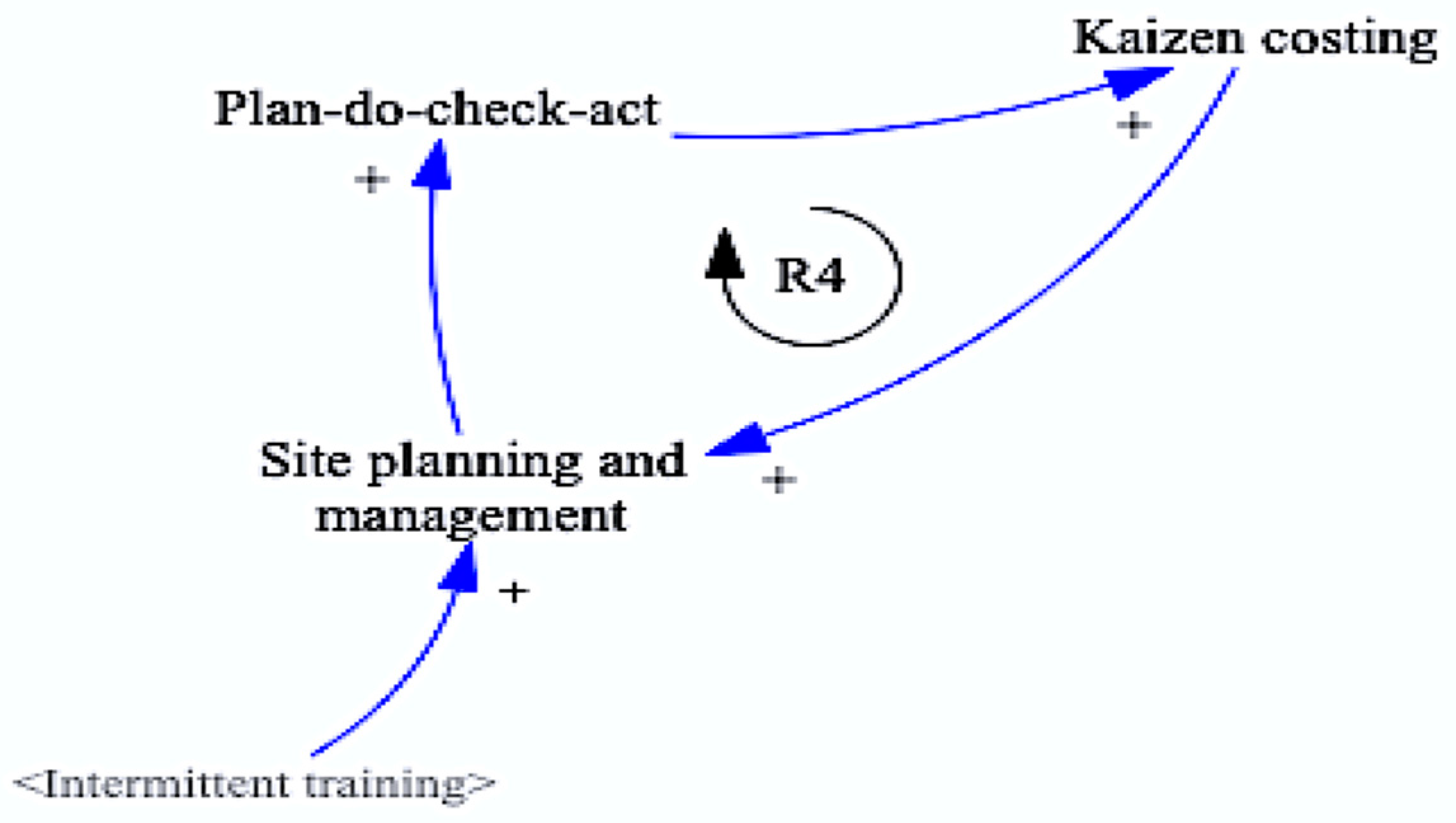

Figure 10 illustrates reinforcing loop 4 (R4) with the plan–do–check–act positively leading to the adopting of kaizen costing in the construction process. The kaizen costing process with an embedded plan–do–check–act reduced waste to enhance productivity in the construction site. Thus, leading to better site planning and management for the continuance of the plan–do–check–act principle. Kaizen costing thrives with increasing application of the plan–do–check–act principle for the elimination of non-value adding activities.

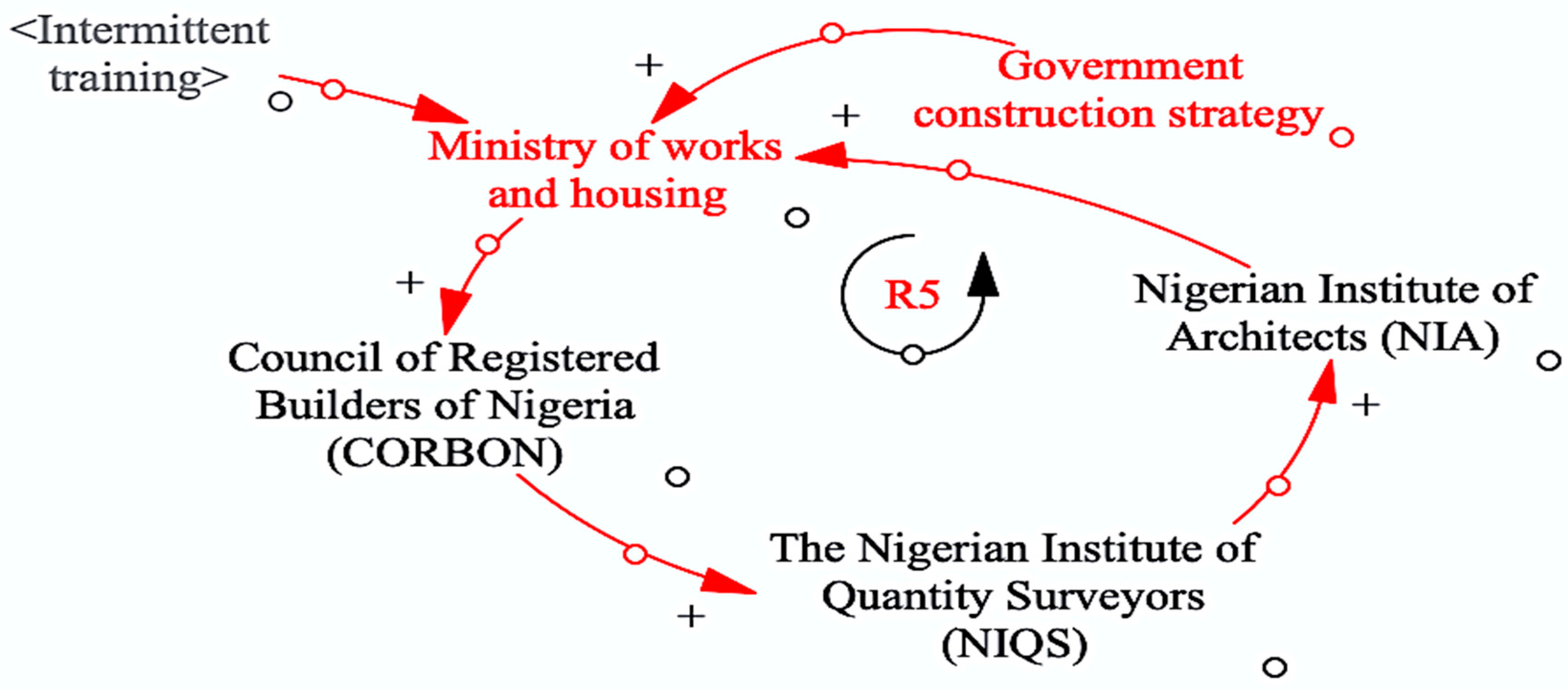

Unlike many developed countries where a new concept or technology can easily become a trend in the construction industry, many developing construction economies, such as Nigeria’s, are mainly influenced by the government. In this instance, the Federal executive council headed by the politicians have a massive influence on the national Ministry of Works and Housing [

61]. Thus, policies about payments, public and private procurement approaches, as well as innovation such as kaizen costing derive their implementation strengths from regulatory bodies such as the NIQS and CORBON, who are under the Federal Ministry of Works and Housing.

Figure 11, provides the archetype, reinforcing loop R5. Archetype 5 was redesigned after the validation of the causal loop diagram to include more exogenous variables. The annual government construction strategy may positively influence the Federal Ministry of Works and Housing in Nigeria. The positive influence of intermittent training in the Federal Ministry of Works and Housing can spur positive changes in the regulatory bodies such as CORBON, NIQS and NIA. Archetype 5 can be regarded as an exogenous archetype because they all exist outside the sphere of the construction organisation. Archetype 5 is highly influential in the validation causal loop diagram of

Figure 5 because any negativity in the archetype will lead to a negative reinforcing loop in R1 to R4.

Archetype 6, in

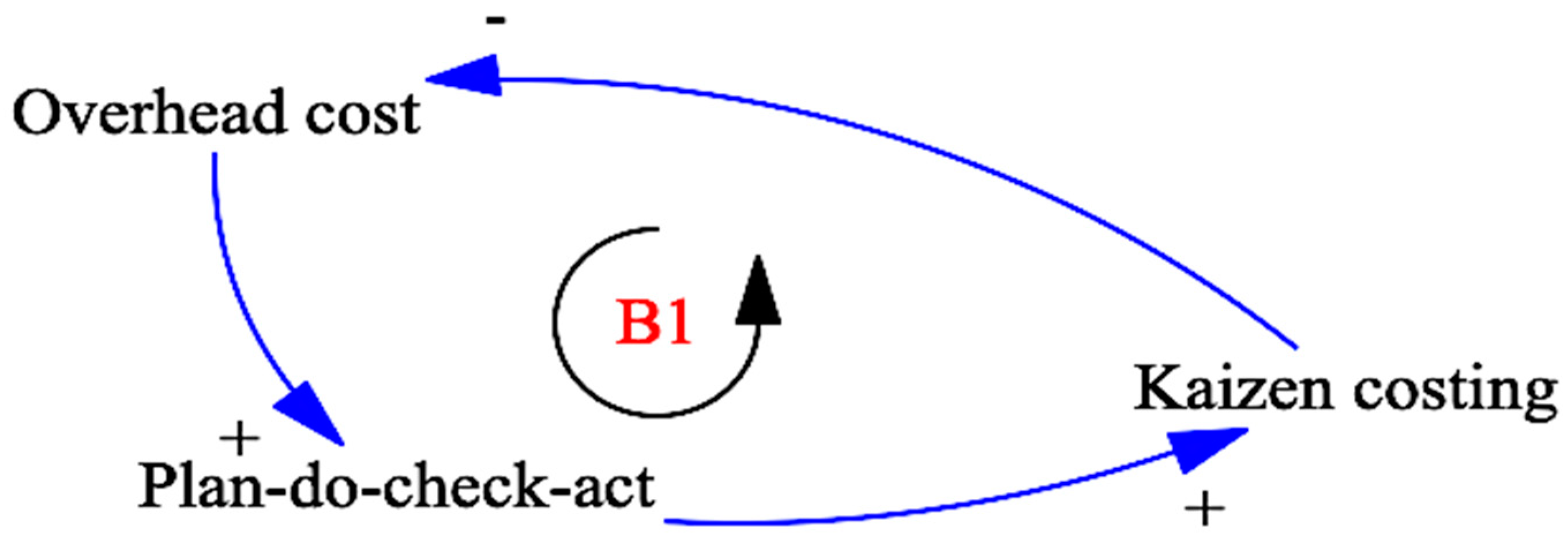

Figure 12, illustrates a balancing loop B1 whereby overhead cost during construction is reduced continually with the aid of kaizen costing. Just archetype 4, has the kaizen costing propelled by the plan–do–check–act, a continual elimination of non-value adding activities in overhead cost will practically lead to cost reduction and maintenance. By applying kaizen costing in overhead cost management, construction variations can be minimised. Since the plan–do–check–act approach to kaizen costing does not end even after the project completion, post-project reviews provide a practical approach to future project cost control and management if archetype 6 is applied.

Archetype 7 in

Figure 13 is a continuation of archetype 6. Archetype 7 contains the balancing loop B2 where kaizen costing is fully implemented in the budgeting system of a construction organisation to increase the development of the work breakdown structure and elimination of construction waste. Construction waste in this archetype may be physical material waste or non-physical waste. Omotayo et al. [

61] developed the causal loop diagram for the elimination of non-physical waste. Omotayo et al. [

61] opined that high overhead cost associated with drawing reviews, mobilisation and equipment set up, payments, preliminary items of works, general planning activities, and construction variations all contribute to non-physical waste in construction projects.

The exogenous attributes required for this archetype to function effectively are openness to innovations and standardised construction process. These attributes emerge from archetypes 2 and 3. Openness to innovations and standardisation of the construction process have been discussed as attributes for construction planning phase improvement with kaizen costing. The need for kaizen costing during the planning stages of a project reflects the sustenance of kaizen costing in a construction establishment.

The practical implications of the causal loop diagram in

Figure 4 and all the archetypes will be discussed below.

7. Practical Implications of the Archetypes

The problem of cost and time overruns hinder construction companies in developing and developed economies that require a non-linear solution. Adeleke et al. [

62] affirmed that political factor is the main external attribute that influences construction risk in Nigerian. Considering the benefits of archetype 5, where the external factors of government construction strategy enhance the regulatory bodies, an encouraging move from the political office holders will provide an opportunity to motivate competition in the construction industry and facilitate innovation in small- and medium-scale construction companies. Regulatory bodies such as CORBON, NIA, and NIQS have a role to play in promoting the adopting of kaizen costing. The aforementioned regulatory bodies can incorporate kaizen costing techniques in associated University courses and conferences. Ojelabi et al. [

63] also identify lack of construction business strategy as a barrier to client satisfaction. Client relationship management is enhanced where kaizen costing has been adopted [

18,

23,

48]. The import of archetypes 6 and 7 in the construction process is successful project delivery and client satisfaction.

In most case studies where kaizen costing has been adopted, the profit margin has been considerably higher, and the motivation of all stakeholders seemed higher. As opposed to traditional costing where there is an immense combination of challenges within construction organisations and projects, kaizen costing is an innovative cost controlling technique many construction companies need to adopt for profit margin enhancement through the plan–do–check–act principle. Archetypes 1 and 2 exemplified kaizen costing from the perspective of innovation in management strategy. Openness to innovation and standardisation of the construction process will require constant training and the modification of construction companies’ policies to encourage research and new ideas. The cost of innovation in small- or medium-scale construction companies in a developing economy such as Nigeria needs to be a barrier for the implementation of kaizen. Notwithstanding, the proactiveness of kaizen costing is rather cultural and less financial. Thus, the concept of kaizen philosophy which implies “change for better”.

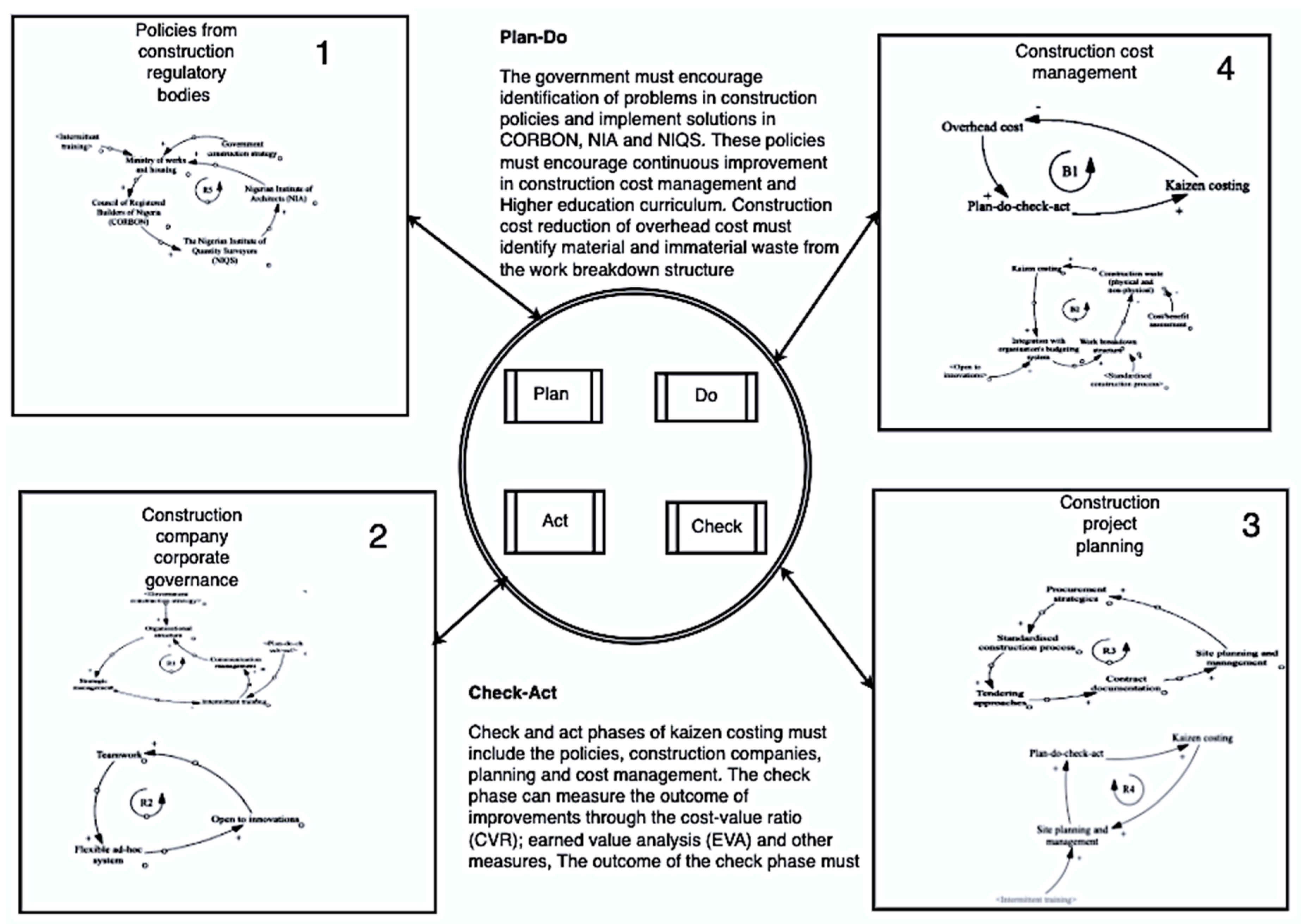

In

Figure 14, the kaizen costing archetypes from

Figure 7,

Figure 8,

Figure 9,

Figure 10,

Figure 11 and

Figure 12 were grouped into four categories for practicality and implementation purposes. The first group is policies from construction regulatory bodies, the second is construction company corporate governance, the third is construction project planning and finally, construction cost management.

Government policies influence Federal construction parastatals, construction regulatory bodies and private construction companies [

39,

64]. For overarching kaizen costing implementation in the Nigerian construction industry, policies from regulatory bodies such as the NIQS affect the practice of construction companies. For instance, the standard methods of measurement in Nigeria are determined by key stakeholders in the NIQS. In implementing kaizen costing approaches in policies emanating from construction regulatory bodies, such as the Federal Ministry of Works and Housing, NIQS and CORBON, the Deming’s circle involving the plan–do–check was used to detail the process required for kaizen costing adoption. Archetype R5 provides a structure for intermittent training of key stakeholders in the Federal Ministry of Works and Housing; NIQS, CORBON and NIA. The next phase of “do” should involve pilot projects on the new concept of kaizen costing in a small-scale construction project. This will be followed by the “check” phase where the results are analysed and further full-scale implementation will be adopted.

Archetypes R1 and R2 were adopted for construction company corporate governance. Strategic management of construction companies must consider intermittent kaizen costing training of their construction employees as an important investment for their development. Kaizen costing in an organisation may be perceived as an opportunity to reduce immaterial and material waste. This corporate governance with kaizen costing may lead to improving the construction planning process.

In the construction project planning, R3 and R4 must consider the concept of mitigating waste in terms of the cost of procurement, tendering and site management through standardisation of the process. The concept of lean construction is applicable in implementing the plan–do–check–act in construction planning. Post-project reviews are very crucial in promoting the concept of kaizen costing during the construction phase. Hence, kaizen costing experts may be required to supervise planning approaches requiring additional standardisation.

The plan–do–check principle of identifying challenges in construction cost planning for implementation purposes may consider, procurement, tendering, contract documentation and site management plans involving the supply chain. Standardisation of key processes using the Deming’s circle can afford construction cost planners in organisations the opportunity to enhance their cost management practices.

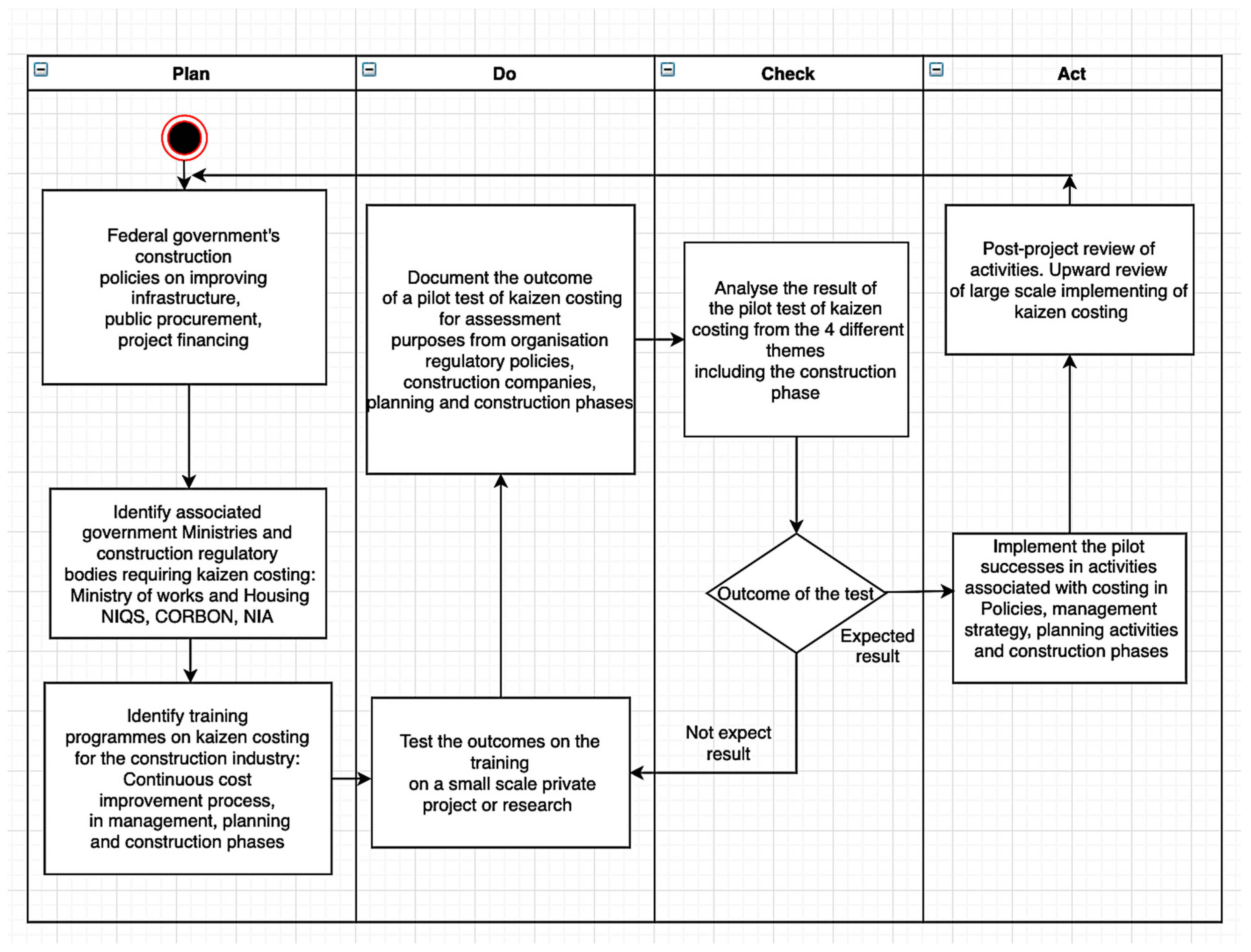

Figure 15 identified the plan–do–check–act process within the concepts of policymaking, corporate governance in a construction company, construction planning and activities. The “do” phase of the process will require incorporation of kaizen costing in the small-scale project along the lines of the four (4) categories requiring implementation. The check phase will evaluate the outcome of the small-scale project for final implementation in the “act” phase.

Target costing has been considered by Robert and Granja [

34] to be a crucial approach in incremental cost reduction. The main driver of incremental cost reduction is big mark-up and overhead cost. Overhead costs are important in the construction process and cannot be eliminated. However, the contractor’s profit tends to rise when high overheads cost is kept at the barest minimum. The application of the Deming’s circle in the construction phase must be taken from the perspective of the work breakdown structure. Consideration of a framework for kaizen costing by Vivan et al. [

33] in

Figure 15 elicits a case of a housing construction from the excavations, raft foundation, masonry in the foundation, floor screed, ground floor and slabs.

The execution strategy, high production lead times, unclear definition of production rate, inadequate monitoring, changes in the pace of production, delays arising from unnecessary site monitoring, errors in construction schedule and supply chain of the subcontractor, are primary problem areas identified in the case of a building construction project [

33]. This case project in Brazil also presents a replica of problems in building construction projects in Nigeria. The resultant effect of identified problems emanating from kaizen costing may lead to cost overrun. In addressing the identified problems in the aforementioned case, lean thinking in construction may be adopted. The kaizen costing is a lean thinking concept and tools such as the spaghetti diagram and Kanban may be used to reduce schedule and resource allocation challenges.

9. Conclusions and Potential for Further Research

This study aimed to develop a causal loop diagram for the adoption of kaizen costing in the Nigerian construction industry. The archetypes 1 to 7 provide a structured model of where kaizen costing can be adopted in government and regulatory agencies, privately-owned construction companies and in a construction project. Construction productivity is a key element for successful implementation of a system that boosts the effective running and smooth operation of construction projects. From the analytical hierarchical process, the organisation structure emerged top on the list for kaizen costing. This indicates that small- and medium-scale construction firms need to look inward to find the effective organisational structure for enhanced productivity. This requires a paradigm shift from equipment-centred organisations to personnel-centred organisations. This will also enhance managerial aspects and vibrant knowledge acquisition. The logical thinking and capability building of the personnel via kaizen will boost the efficiency of construction companies, reduce cost and time overruns and place them at the competitive edge with the large-scale firms.

The order of importance in construction companies, in line with kaizen costing requirement, is an effective organisation structure which is critical for effective implementation of kaizen costing. Government regulation, which is second in importance, is essential since kaizen is still new. There is a need for government approval for the deployment of kaizen which will ensure it penetration into wide construction and also communicate and instigate its approval. On the other hand, contract documentation and procurement from the contractor’s perspective determines the strategy that will be adopted by the contractor to be involved in the kaizen activities on any project.

Kaizen implementation in the SMSCFs will no doubt improve the standardisation of construction process depending on policies and regulation. Effective decision-making during Kaizen activities in the organisation when implemented will allow every problem or risk to be viewed, not only as problems, but as opportunities as well. Implementation of the kaizen system of costing in construction companies will augment relationship among the stakeholders and reduce the intensity of claims by the contractor be it, main contractor or subcontractor. The financial risk and litigation are issues erupting from inadequate financial preparation which may pose a negative impact on the kaizen activities. This may be the reason for the low ranking. Communication and teamwork will be more effective with the kaizen team and BIM will further enhance the effectiveness. The findings and implications of this study reveal that the inclusion of kaizen costing practices in government and regulatory policies for the Nigerian construction industry can spur other lean construction concepts in the construction industry. Further empirical studies are required to assess the impact kaizen costing has on corporate governance of construction companies, project delivery and project cost performance.

In terms of future research, the dynamics of the system of kaizen costing implementation can be created from the archetypes. The system dynamics will provide more depth to the causal loop diagram by creating stock-flow diagrams for organisational performance and cost reduction in construction projects. The systems dynamics of kaizen costing will practically validate the stock-flow diagrams with data extracted for a construction project. Furthermore, this research has provided a basis for studies into new techniques for cost control in a construction project. Therefore, action research into cost reduction and maintenance using kaizen costing suffices as a backdrop for alleviating the plethora of challenges facing construction companies and projects.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}