The Enhanced-Earned Value Management (E-EVM) Model: A Proposal for the Aerospace Industry

Abstract

1. Introduction

2. The Earned Value Management

- Another EVM extension describes the so-called Earned Duration Management (EDM) model [8] in which the measurement of cost performance and planning are separated by introducing new parameters to check efficiency and to improve forecasting at the end of the project.

- Finally, the so-called Quality Earned Value Management (QEVM) model [9] introduces the quality parameter in the EVM model, by calculating or measuring the actual development or performance of a given project from the point of view of quality criteria.

3. The EVM in the Aerospace Industry

3.1. The Aerospace Industry

3.2. The EVM in the Airspace Industry

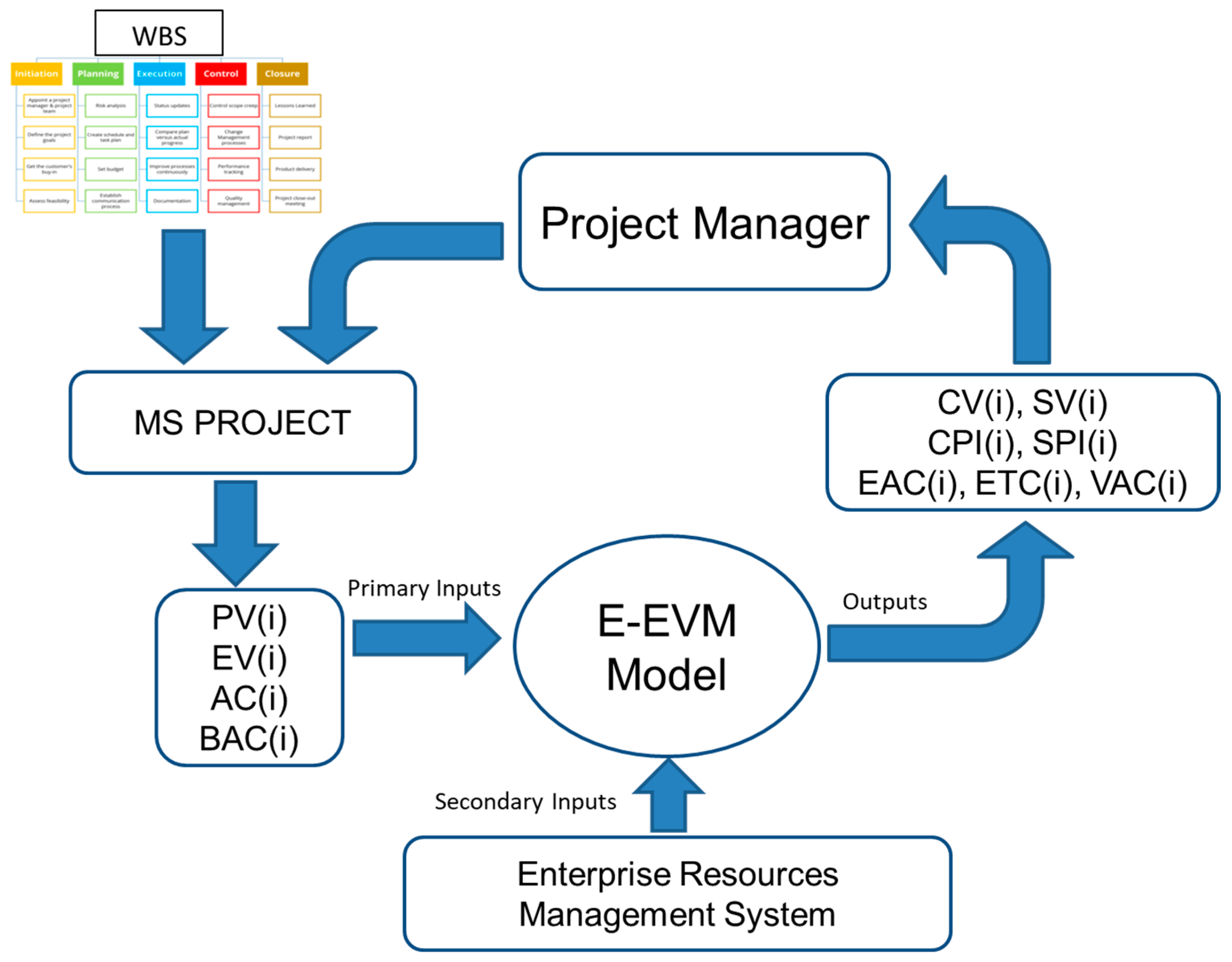

4. Defining the Enhanced-Earned Value (E-EVM) Model

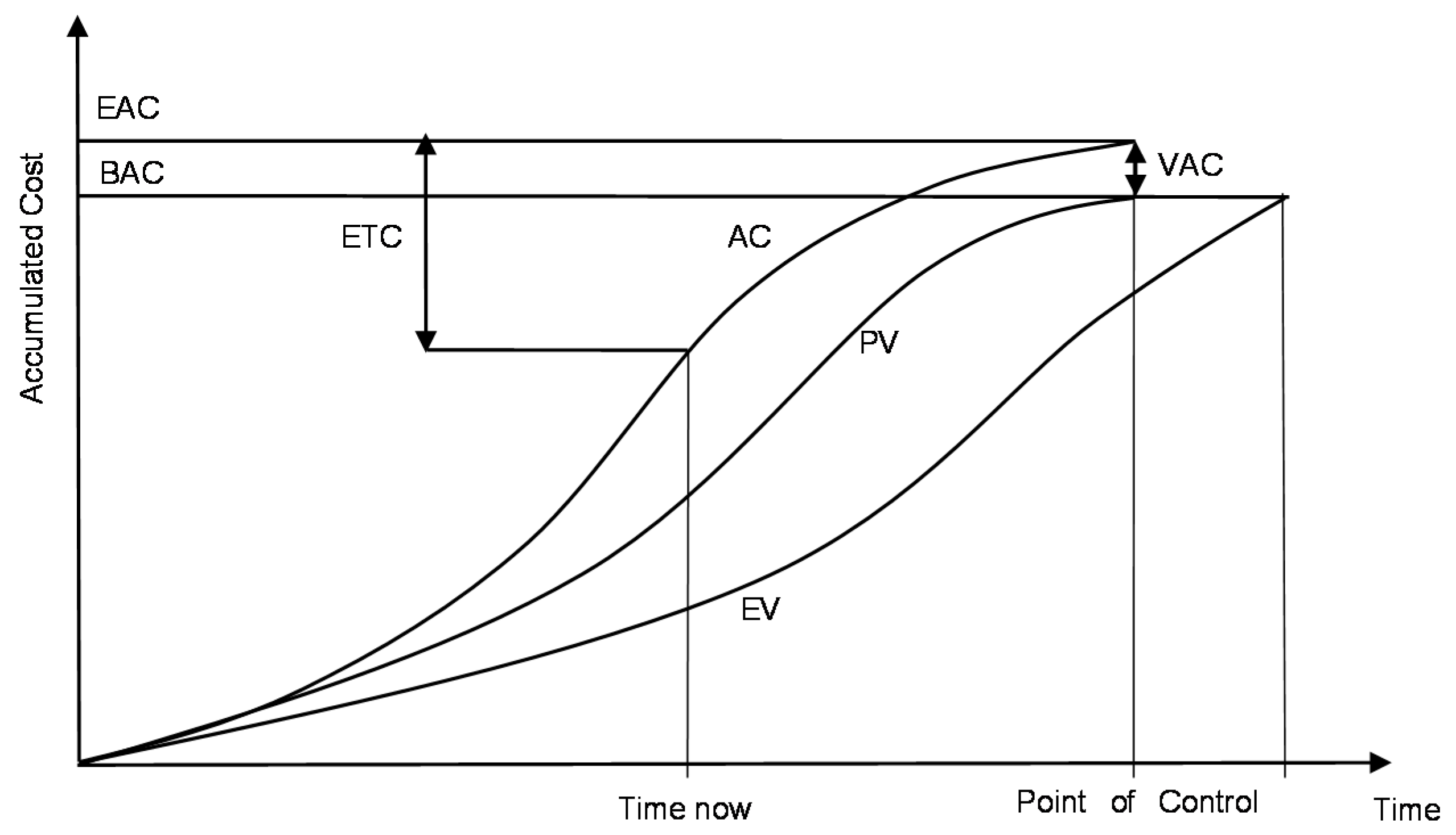

4.1. EVM Background and First improvement of the E-EVM Model

- The projected cost according to the initial budget:

- 2.

- The projected cost according to the current CPI:

- 3.

- The projected cost according to the CPI and the SPI:

- The Estimate to Complete (ETC):

- The Variance at Completion (VAC):

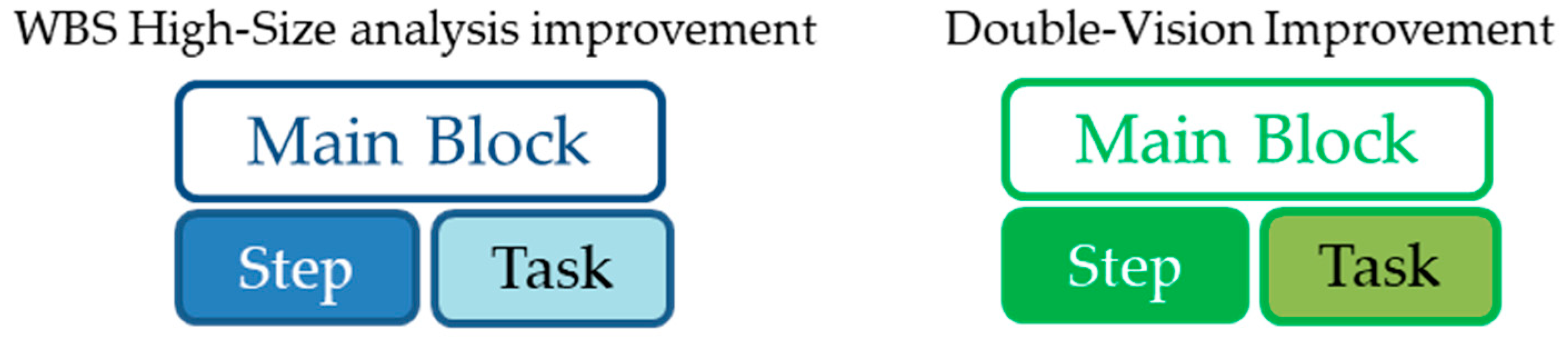

4.2. The Second Improvement of the E-EVM Model

5. Results

5.1. General Procedure E-EVM Models

- N(i): Set of subprojects i, for every i belonging to the WBS.

- AC, PV, EV, BAC, and hourly rate: Set of inputs of each subproject i.

- CV(i); CPI(i); SV(i); SPI(i); EAC(i); ETC(i); and VAC(i): Set of output of each subproject i (column vectors).

- UpL_CV and LoL_CV: Upper and lower limit of Cost Variance.

- UpL_SV and LoL_SV: Upper and lower limit of Schedule Variance.

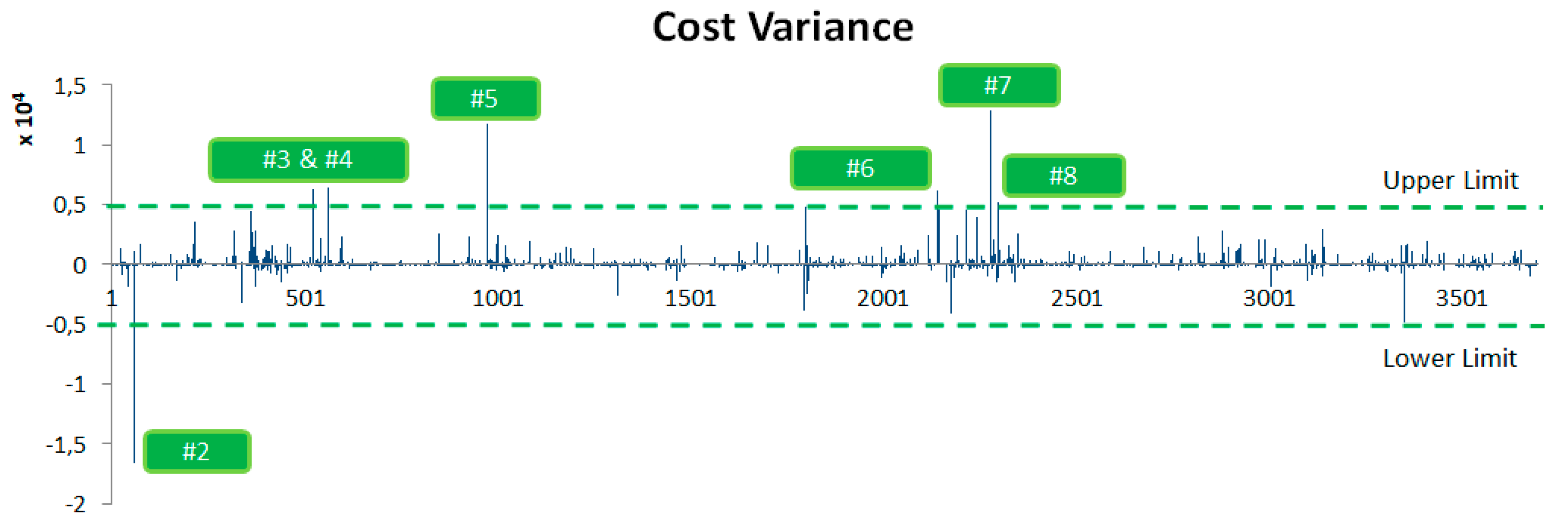

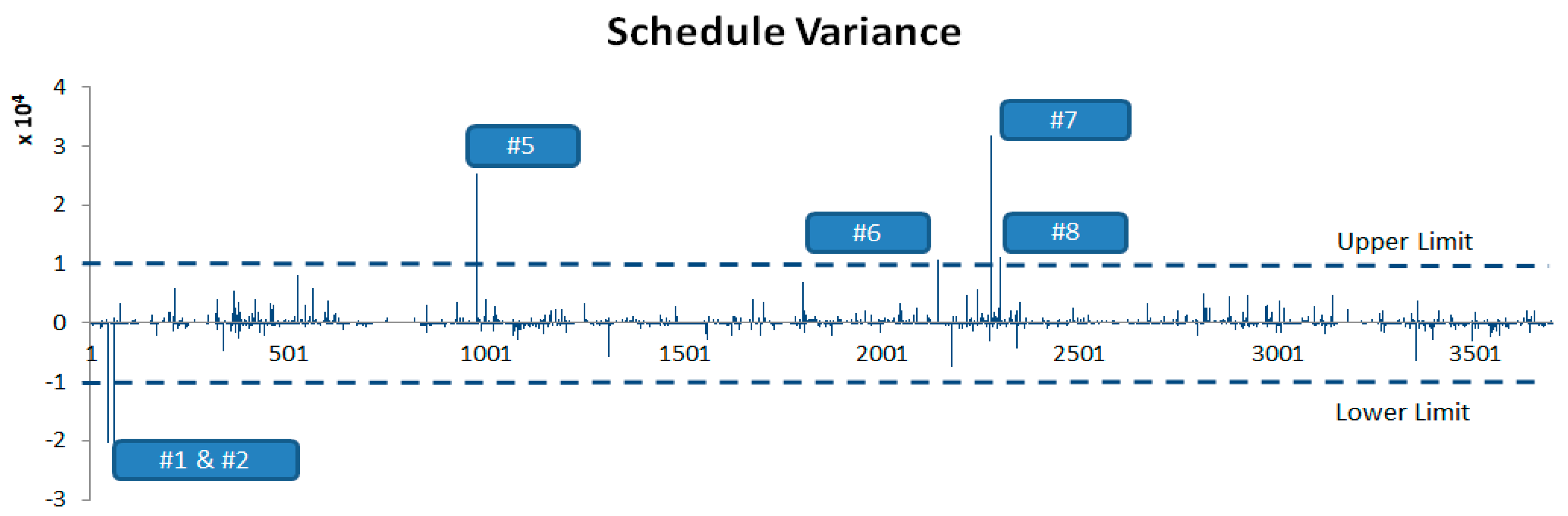

5.2. Analysis of Results (Second Improvement)

- A percentage of the subproject with the highest associated cost.

- A penalty set for contracting with the end customer.

- Reference of a possible variable financial compensation assigned to the project leader.

5.3. Double-Vision Results (First Improvement)

6. Conclusions, Limitations, and Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| E-EVM | Enhanced-Earned Value Management |

| EVM | Earned Value Management |

| ESM | Earned Scheduled Management |

| EDM | Earned Duration Model |

| QEVM | Quality Earned Value Model |

| TEDAE | Technological Defence, Aeronautical and Space Companies |

| GDP | Gross Domestic Product |

| EIM | Earned Incentive Metric |

| WBS | Work Breakdown Structure |

| MSP | Microsoft Project |

| PERT | Program Evaluation and Review Technique |

| CCPM | Critical Chain Project Management |

References

- Meléndez, J.C.; Galán, J.L. La Subcontratación en el Sector Aeronáutico: Una Aproximación a la Realidad Andaluza. Master’ Thesis, Universidad Pablo de Olavide, Sevilla, Spain, June 2007. [Google Scholar]

- Anbari, F.T. Earned value project management method and extensions. Proj. Manag. J. 2003, 34, 12–23. [Google Scholar] [CrossRef]

- Webb, A. Using Earned Value: A Project Manager’s Guide; Gower Publishing Ltd.: Aldershot, UK, 2003. [Google Scholar]

- Vanhoucke, M. Using activity sensitivity and network topology information to monitor project time performance. Omega 2010, 38, 359–370. [Google Scholar] [CrossRef]

- Lipke, W. Schedule is Different. The Measurable News, March 2003; 10–15. [Google Scholar]

- Lipke, W.; Zwikael, O.; Henderson, K.; Anbari, F. Prediction of project outcome. The application of statistical methods to earned value Management and earned schedule performance indexes. Int. J. Proj. Manag. 2009, 27, 400–407. [Google Scholar] [CrossRef]

- Lipke, W. Earned Schedule–Ten Years After. The Measurable News, March 2013; 15–21. [Google Scholar]

- Khamooshi, H.; Golafshani, H. EDM: Earned Duration Management, a new approach to schedule performance management and measurement. Int. J. Proj. Manag. 2014, 32, 1019–1041. [Google Scholar] [CrossRef]

- Dodson, M.; Defavari, G.; de Carvalho, V. Quality: The third element of Earned Value Management. Procedia Comput. Sci. 2015, 64, 932–939. [Google Scholar] [CrossRef][Green Version]

- Nizam, A.; Elshannaway, A. Review of earned value management (EVM) methodology, its limitations, and applicable extensions. J. Manag. Eng. Integr. 2019, 12, 59–70. [Google Scholar]

- Webb, A. Project Management for Successful Product Innovation; Gower Publishing Ltd.: Aldershot, UK, 2000; p. 433. [Google Scholar]

- Webb, A. Managing Innovate Projects; Chapman & Hall: London, UK, 1993; p. 379. [Google Scholar]

- Chen, H.L.; Chen, W.T.; Lin, Y.L. Earned value project management: Improving the predictive power of planned value. Int. J. Proj. Manag. 2016, 34, 22–29. [Google Scholar] [CrossRef]

- Atkinson, R. Project management: Cost, time and quality, two best guesses and a phenomenon, its time to accept other success criteria. Int. J. Proj. Manag. 1999, 17, 337–342. [Google Scholar] [CrossRef]

- Babu, A.J.G.; Suresh, N. Project management with time, cost, and quality considerations. J. Oper. Res. 1996, 88, 320–327. [Google Scholar] [CrossRef]

- Khang, D.B.; Myint, Y.M. Time, cost and quality trade-off in project management: A case study. Int. J. Proj. Manag. 1999, 17, 249–256. [Google Scholar] [CrossRef]

- Basu, R. Managing quality in projects: An empirical study. Int. J. Proj. Manag. 2014, 32, 178–187. [Google Scholar] [CrossRef]

- Chen, H.L. Improving forecasting accuracy of project earned value metrics: Linear modeling approach. J. Manag. Eng. 2014, 30, 135–145. [Google Scholar] [CrossRef]

- Colin, J.; Vanhoucke, M. A comparison of the performance of various project control methods using earned value management systems. Expert Syst. Appl. 2015, 42, 3159–3175. [Google Scholar] [CrossRef]

- Pajares, J.; López-Paredes, A. An extension of the EVM analysis for project monitoring: The cost control index and the schedule control index. Int. J. Proj. Manag. 2011, 29, 615–621. [Google Scholar] [CrossRef]

- Acebes, F.; Pajares, J.; Galán, J.M.; López-Paredes, A. Beyond earned value management: A graphical framework for integrated cost, schedule and risk monitoring. Procedia Soc. Behav. Sci. 2013, 74, 181–189. [Google Scholar] [CrossRef]

- Khodakarami, V.; Abdi, A. Project cost risk analysis: A Bayesian networks approach for modeling dependencies between cost items. Int. J. Proj. Manag. 2014, 32, 1233–1245. [Google Scholar] [CrossRef]

- Kerkhove, L.P.; Vanhoucke, M. Extensions of earned value management: Using the earned incentive metric to improve signal quality. Int. J. Proj. Manag. 2017, 35, 148–168. [Google Scholar] [CrossRef]

- Moradi, N.; Mousavi, S.M.; Vahdani, B. An earned value model with risk analysis for project management under uncertain conditions. J. Intell. Fuzzy Syst. 2017, 32, 97–113. [Google Scholar] [CrossRef]

- Mahdi, I.; Abd-Elrashed, I.; Ahmed, S.; Lamisse, R. Difficulties of implementing earned value management in construction sector in Egypt. Int. J. Eng. Res. Stud. 2018, 5, 15. [Google Scholar]

- Araszkiewicz, K.; Bochenek, M. Control of construction projects using the Earned Value Method—Case study. Gruyter 2019, 2. [Google Scholar] [CrossRef]

- Khesal, T.; Abbas, S.; Mohammad, K.; Masoud, G.; Soltani, R. Integrated cost, quality, risk and schedule control through earned value management(EVM). J. Eng. Des. Technol. 2019, 17, 183–203. [Google Scholar] [CrossRef]

- Sackey, S.; Lee, D.; Kim, B. Duration estimate at completion: Improving earned value management forecasting accuracy. KSCE J. Civ. Eng. 2020, 24, 693–702. [Google Scholar] [CrossRef]

- Koke, B.; Moehler, R.C. Earned green value management for project management: A systematic review. J. Clean. Prod. 2019, 230, 189–197. [Google Scholar] [CrossRef]

- TEDAE, Spanish Association of Technological Defence. Aeronautical and Space Companies. In Activities Report; TEDAE, Spanish Association of Technological Defence: Madrid, Spain, 2018. [Google Scholar]

- Galán, J.L.; García, J.I. El sector aeronáutico andaluz: Una industria estratégica e innovadora en transformación. In Círculo de Innovación Empresarial; Fundación BBVA: Madrid, Spain, 2015. [Google Scholar]

- Guerras, L.A.; Navas, J.E. La Dirección Estratégica de la Empresa. Teoría y Aplicaciones, 4th ed.; Thomson-Civitas Editorial: Roma, Italy, 2007. [Google Scholar]

- Silver, A. The Gripen programme. Air Space Eur. 1999, 1, 20–23. [Google Scholar]

- Antvik, S. Earned value management in Sweden-Experiences and examples: The Gripen project. In Proceedings of the Project Managment Institute Annual Seminars & Symposium, San Antonio, TX, USA, 3 October 2002; Project Management Institute: Newtown Square, PA, USA, 2002. [Google Scholar]

- Abba, W. How earned value got to primetime: A short look back and a glance ahead. In Proceedings of the Project Management Institute Annual Seminars & Symposium, San Antonio, TX, USA, 7 September 2000; Project Management Institute: Newtown Square, PA, USA, 2000. [Google Scholar]

- Atkins, K.L.; Martin, B.D.; Vellinga, J.M.; Rick, A.P. STARDUST: Implementing a new manage-to-budget paradigm. Acta Astronaut. 2003, 52, 87–97. [Google Scholar] [CrossRef]

- Putz, P.; Maluf, D.; Bell, D.G.; Gurram, M.M.; Hsu, J.; Patel, H.N.; Swanson, K.J. Earned value management at NASA: An integrated, lightweight solution. Aerosp. Conf. IEEEAC 2007, 2, 1–8. [Google Scholar]

- Hunter, H.; Fitzgerald, R.; Barlow, D. Improved cost monitoring and control through the Earned Value Management System. Acta Astronaut. 2014, 93, 497–500. [Google Scholar] [CrossRef]

- Dibert, J.C.; Velez, J.C. An Analysis of Earned Value Management Implementation within the F-22 System Program Office’s Software Development; Naval Postgraduate School: Monterey, CA, USA, 2006. [Google Scholar]

- Robinson, R. Earned value management. The Boeing Company Single EVMS. In Proceedings of the 13th Annual International Conference, Istanbul, Turkey, 13–17 April 2001. [Google Scholar]

- Christ, D.K. Theory of Constraints Project Management in Aircraft Assembly; The Boeing Company: Chicago, IL, USA, 2001. [Google Scholar]

- Laporte, C.Y.; Doucet, M.; Roy, D.; Drolet, M. Improvement of software engineering performances an experience report at bombardier transportation–Total transit systems signalling group. In Proceedings of the 17th Annual International Symposium, International Council on Systems Engineering, San Diego, CA, USA, 24–28 June 2007. [Google Scholar]

- Locksley, R.H.; Rice, C.B. Establishing a program for applying Earned Value Metrics to flight test. IEEE Aerosp. Conf. 2000, 2, 1–8. [Google Scholar]

- Meléndez Rodríguez, J.C.; Lopez Pascual, J.; Cañamero, P.; García, F.P. Big Data and Earned Value Management in Airspace Industry. Book Chapter Big Data Management; Springer International Publishing: Berlin/Heidelberg, Germany, 2017; pp. 257–267. [Google Scholar] [CrossRef]

- Meléndez Rodríguez, J.C.; López Pascual, J.; Cañamero, P.; García, F.P. An overview of earned value management in airspace industry. In Proceedings of the Tenth International Conference on Management Science and Engineering Management. Advances in Intelligent Systems and Computing; Springer: Berlin/Heidelberg, Germany, 2017; Volume 502, pp. 1465–1477. [Google Scholar] [CrossRef]

- 5th Edition PMBOK® Guide-Chapter 7: Earned Value Management (Part 1). 2013. Available online: https://4squareviews.com/2013/05/09/5th-edition-pmbok-guide-chapter-7-earned-value-measurement-part-1/ (accessed on 15 December 2020).

- Richardson, G.L. EVM2—A new look at the earned value management model. Am. J. Manag. 2017, 17, 71. [Google Scholar]

- Mishakova, A.; Vakhrushkinaa, A.; Murgula, V.; Sazonova, T. Project control based on a mutual application of pert and earned value management methods. Procedia Eng. 2016, 165, 1812–1817. [Google Scholar] [CrossRef]

- Bovteev, S.V.; Petrochenko, M. Method “Earned Value Management” for timescale controlling in construction projects. Appl. Mech. Mater. 2015, 725, 1025–1030. [Google Scholar] [CrossRef]

- Acebes, F.; Pajares, J.; Galán, J.M.; López-Paredes, A. A new approach for project control under uncertainty. Going back to the basics. Int. J. Proj. Manag. 2014, 32, 423–434. [Google Scholar] [CrossRef]

- Association for Project Management. Earned Value Management Handbook; Association for Project Management: Buckinghamshire, UK, 2013; ISBN 10-1-903494-47-8. [Google Scholar]

- Caron, F.; Ruggeri, F.; Merli, A. A bayesian approach to improve estimate at completion in earned value management. Proj. Manag. J. 2013, 44, 3–16. [Google Scholar] [CrossRef]

- Sunarti, N.; Mastan, Z.; Cin, L. The application and challenges of earned value management (EVM) as cost monitoring tool in the construction industry. Int. J. Eng. Technol. 2018, 7, 96. [Google Scholar] [CrossRef]

- De Marco, A.; Narbaev, T. Earned value-based performance monitoring of facility construction projects. J. Facil. Manag. 2013, 11, 69–80. [Google Scholar] [CrossRef]

- Chin Keng, T.; Shahdan, N. The application of Earned Value Management (EVM) in costruction project management. J. Technol. Manag. Bus. 2015, 2, 2289–7224. [Google Scholar]

- Sruthia, M.D.; Aravindanb, A. Performance measurement of schedule and cost analysis by using earned value management for a residential building. Mater. Today Proc. 2020, 33, 524–532. [Google Scholar] [CrossRef]

- Hendiania, S.; Bagherpoura, M.; Mahmoudib, A.; Liaoc, H. Z-number based earned value management (ZEVM): A novel pragmatic contribution towards a possibilistic cost-duration assessment. Comp. Ind. Eng. 2020, 143, 106430. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sector | Reference | Main topics | Publication |

|---|---|---|---|

| Aerospace | (a) 13, 28 (b) 14, 15, 16, 17, 20, 21, 23, 27 (c) 18, 25, 25 | Subcontracting management, aircraft manufacturing and assembly, spacecrafts manufacturing, flight test, general application. | (a) 1990–2000 (b) 2001–2010 (c) 2011– |

| Software development and computational research | (a) 32 (b) 14, 6, 19, 22 (c) 35, 37, 39, 50 | Simulation, statistical methods, embedded software, critical path method application, network dataset, graphical framework, incentive metrics, work breakdown structure improvement. | (a) 1990–2000 (b) 2001–2010 (c) 2011– |

| Products | (a) 5 (b) 57 | High technology products and manufacturer equipment. | (a) 2003 (b) 2020 |

| Army forces | 8 | New schedule approach applied to us coast guard. | 2014 |

| Miscellaneous | (a) 26 (b) 31 (c) 36 | EVM methodology revision. | (a) 2019 (b) 1999 (c) 2011– |

| Chemical | 29 | Improving forecasting models. | 2016 |

| Building construction | (a) 30, 34, 38, 40, 41, 42, 43, 44, 51, 52, 53, 54, 55, 56 | Linear modeling in electrical sector, new quality models, cost risk analysis, Malaysia, Europe and Egypt real building cases, integrated cost, quality and risk models approach. | (a) 2011– |

| Cement factory | 33 | Time, cost, and quality trade-off approach. | 1999 |

| Oil and gas | 55 | Bayesian model approach. | 2013 |

| Environment | 45 | Measurement of project sustainability and performance. | 2019 |

| Characteristics | EVM | E-EVM |

|---|---|---|

| Metrics | EV, AC, PV | EV(i), AC(i), PV(i) |

| Performance indicator (variances) | CV, SV | CV(i), SV(i) |

| Performance indicator (indices) | CPI, SPI | CPI(i), SPI(i) |

| Forecast method | EAC, ETC, VAC | EAC(i), ETC(i), VAC(i) |

| “Double” vision cost/time (first improvement) | No | Yes |

| Inputs | Cost units | Cost and time units |

| Outputs | Cost units | Cost and time units |

| Large-size work breakdown structure (WBS; second improvement) | No | Yes |

| Scope of the model/applicability | One project | i projects |

| Continuous revision and improvement usage | One project | i projects |

| Decision-making process | One project | i projects |

| Parameter | Condition | Meaning |

|---|---|---|

| Schedule Variance (SV) | SV < 0 | Behind schedule |

| SV > 0 | Ahead of schedule | |

| Schedule Performance Index (SPI) | SPI < 1 | Non-efficient use of time |

| SPI > 1 | Efficient use of time | |

| Cost Variance (CV) | CV < 0 | Over budget |

| CV > 0 | Under budget | |

| Cost Performance Index (CPI) | CPI < 1 | Non-efficient use of resources |

| CPI > 1 | Efficient use of resources |

| Subproject # | AC | PV | EV | BAC | CV | SV | CPI | SPI | EAC | ETC | VAC |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 7 | 20,891 | 1805 | 33,703 | 30,820 | 12,812 | 31,898 | 1.6 | 18.7 | 18,008 | −2883 | 12,812 |

| 5 | 15,100 | 1493 | 26,804 | 22,295 | 11,704 | 25,311 | 1.8 | 18.0 | 10,591 | −4509 | 11,704 |

| 4 | 8447 | 8630 | 14,699 | 23,504 | 6252 | 6069 | 1.7 | 1.7 | 17,252 | 8805 | 6252 |

| 3 | 11,895 | 10,148 | 18,143 | 17,860 | 6248 | 7995 | 1.5 | 1.8 | 11,612 | −283 | 6248 |

| 6 | 6754 | 2160 | 12,950 | 10,000 | 6196 | 10,790 | 1.9 | 6.0 | 3804 | −2950 | 6196 |

| 8 | 9301 | 3499 | 14,551 | 15,267 | 5250 | 11,052 | 1.6 | 4.2 | 10,017 | 716 | 5250 |

| 2 | 34,150 | 37,800 | 17,460 | 113,189 | −16,690 | −20,340 | 0.5 | 0.5 | 129,879 | 95,729 | −16,690 |

| Subproject # | AC | PV | EV | BAC | CV | SV | CPI | SPI | EAC | ETC | VAC |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 7 | 20,891 | 1805 | 33,703 | 30,820 | 12,812 | 31,898 | 1.6 | 18.7 | 18,008 | −2883 | 12,812 |

| 5 | 15,100 | 1493 | 26,804 | 22,295 | 11,704 | 25,311 | 1.8 | 18.0 | 10,591 | −4509 | 11,704 |

| 8 | 9301 | 3499 | 14,551 | 15,267 | 5250 | 11,052 | 1.6 | 4.2 | 10,017 | 716 | 5250 |

| 6 | 6754 | 2160 | 12,950 | 10,000 | 6196 | 10,790 | 1.9 | 6.0 | 3804 | −2950 | 6196 |

| 2 | 34,150 | 37,801 | 17,461 | 113,189 | −16,689 | −20,340 | 0.5 | 0.5 | 129,878 | 95,728 | −16,689 |

| 1 | 13,657 | 32,204 | 11,867 | 89,600 | −1790 | −20,337 | 0.9 | 0.4 | 91,390 | 77,733 | −1790 |

| Functional Area | Hourly Rate EUR/h | Function Code |

|---|---|---|

| Design office | 50 | DO |

| Operations | 45 | OP |

| Marketing and sales | 60 | MS |

| Quality | 75 | QL |

| Functional Area | Subproject # | BAC | EAC | ETC (Hours) | ETC (EUR) | VAC | Status |

|---|---|---|---|---|---|---|---|

| DO | 1 | 89,600 | 91,390 | 77,733 | 3,886,650 | −1790 | Over planned budget |

| DO | 2 | 113,189 | 129,878 | 95,728 | 4,786,400 | −16,689 | Over planned budget |

| OP | 3 | 17,860 | 11,612 | −283 | −12,735 | 6248 | Under planned budget |

| OP | 4 | 23,504 | 17,252 | 8805 | 396,225 | 6252 | Under planned budget |

| OP | 5 | 22,295 | 10,591 | −4509 | −202,905 | 11,704 | Under planned budget |

| MS | 6 | 10,000 | 3,804 | −2950 | −177,000 | 6196 | Under planned budget |

| QL | 7 | 30,820 | 18,008 | −2883 | −216,225 | 12,812 | Under planned budget |

| QL | 8 | 15,267 | 10,017 | 716 | 53,700 | 5250 | Under planned budget |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

López Pascual, J.; Meléndez Rodríguez, J.C.; Cruz Rambaud, S. The Enhanced-Earned Value Management (E-EVM) Model: A Proposal for the Aerospace Industry. Symmetry 2021, 13, 232. https://doi.org/10.3390/sym13020232

López Pascual J, Meléndez Rodríguez JC, Cruz Rambaud S. The Enhanced-Earned Value Management (E-EVM) Model: A Proposal for the Aerospace Industry. Symmetry. 2021; 13(2):232. https://doi.org/10.3390/sym13020232

Chicago/Turabian StyleLópez Pascual, Joaquín, Juan Carlos Meléndez Rodríguez, and Salvador Cruz Rambaud. 2021. "The Enhanced-Earned Value Management (E-EVM) Model: A Proposal for the Aerospace Industry" Symmetry 13, no. 2: 232. https://doi.org/10.3390/sym13020232

APA StyleLópez Pascual, J., Meléndez Rodríguez, J. C., & Cruz Rambaud, S. (2021). The Enhanced-Earned Value Management (E-EVM) Model: A Proposal for the Aerospace Industry. Symmetry, 13(2), 232. https://doi.org/10.3390/sym13020232