Effects of Short-Term Uncertainties on the Revenue Estimation of PPP Sewage Treatment Projects

,

,

Abstract

1. Introduction

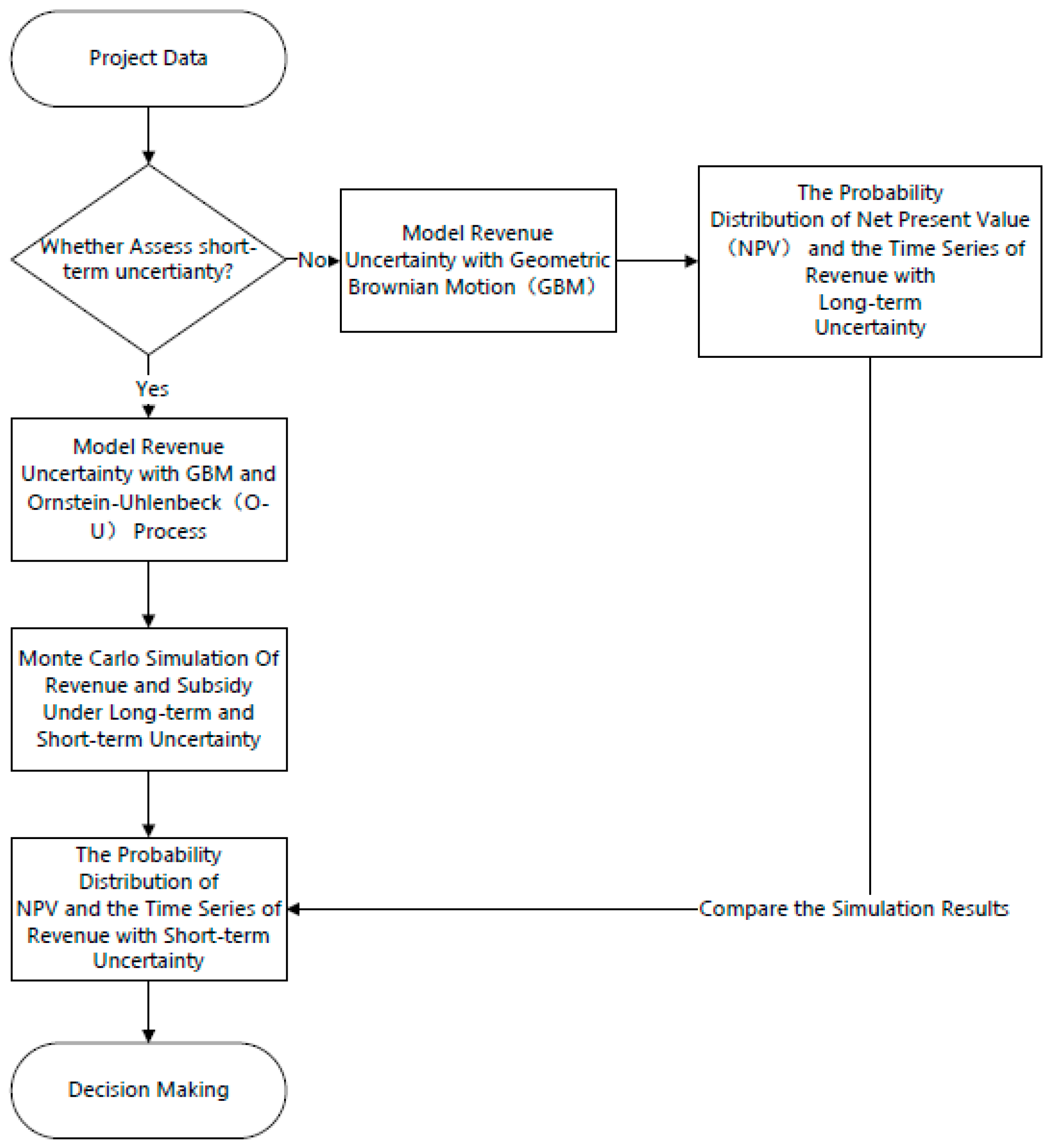

2. Methodology

2.1. Sewage Revenue in Practice

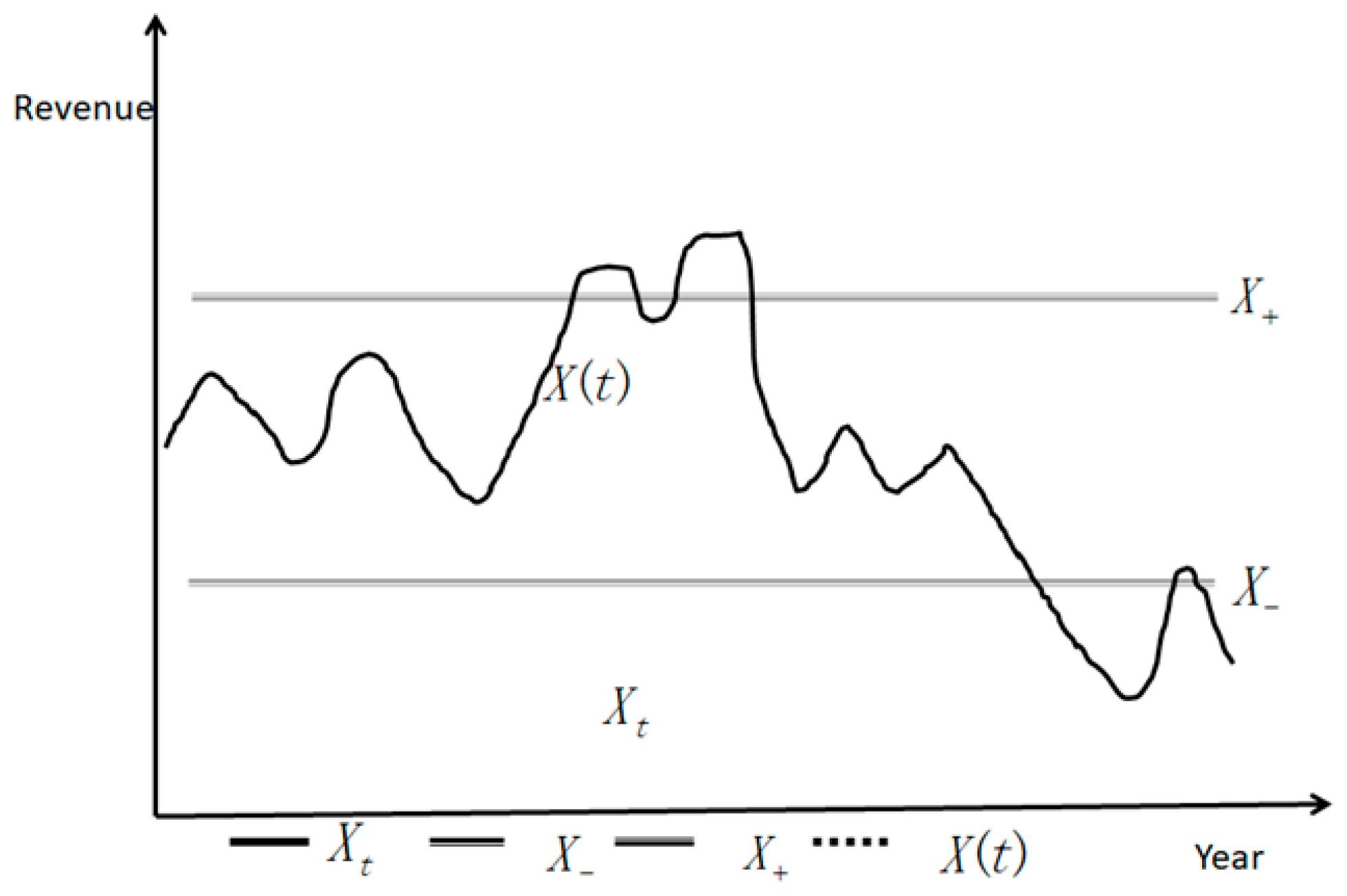

2.2. Short-Term Uncertainty and Ornstein-Uhlenbeck Process

3. Case Study

3.1. Illustrative Case Example

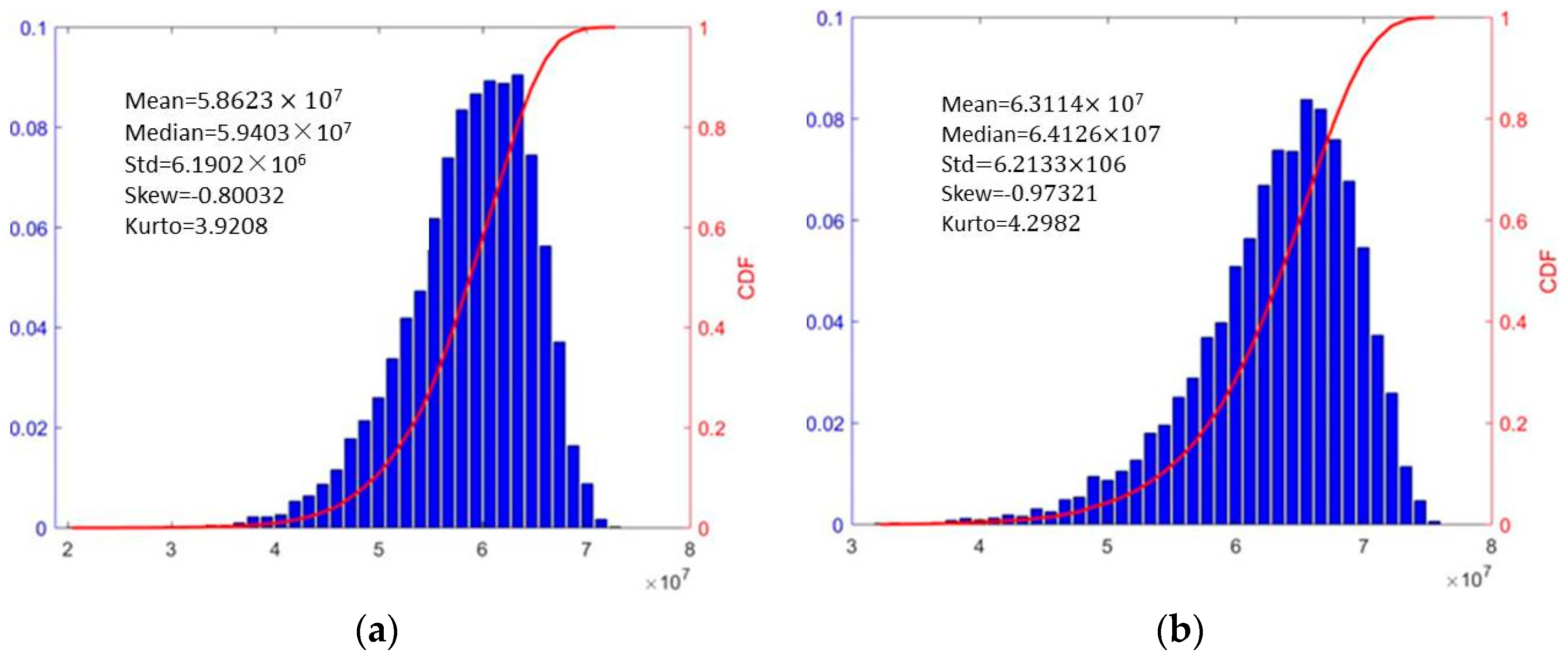

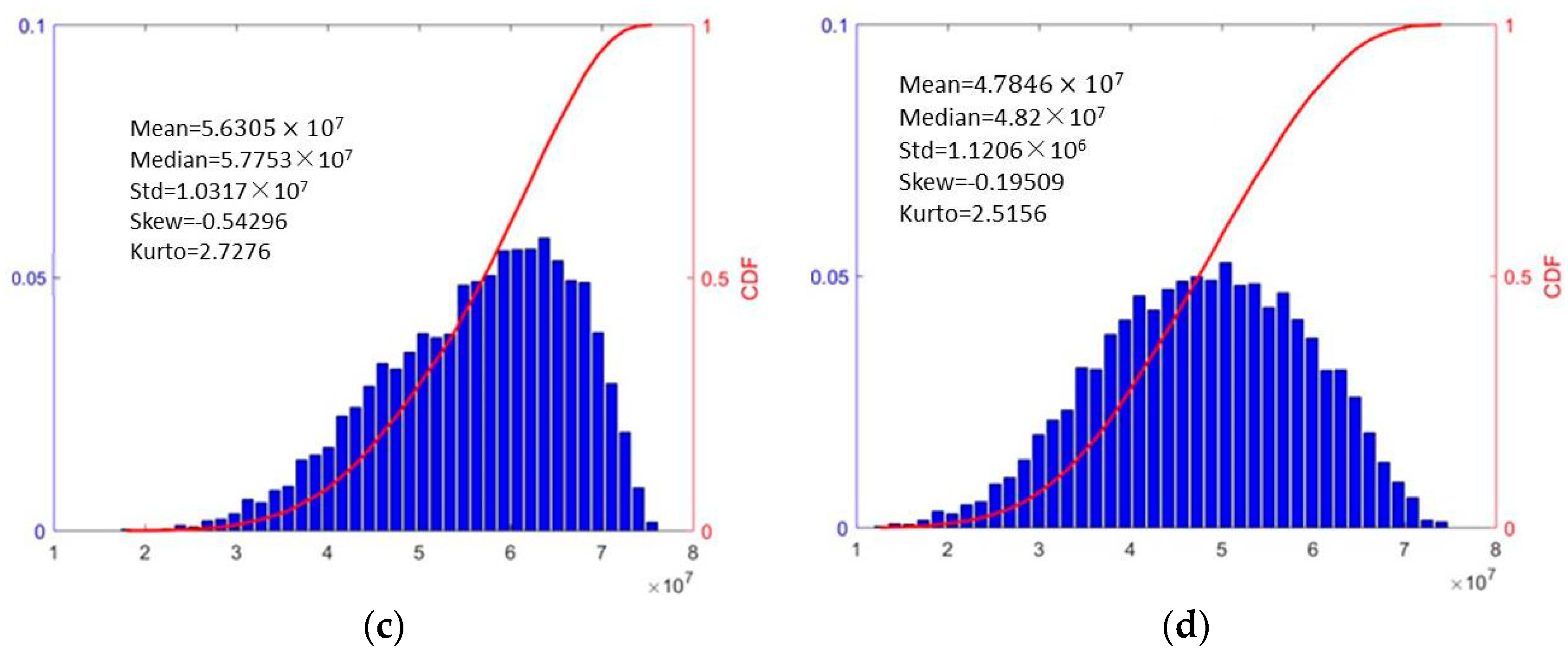

3.2. Results and Discussion

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Braadbaart, O.; Zhang, M.; Wang, Y. Managing urban wastewater in China: A survey of build-operate-transfer contracts. Water Environ. J. 2009, 23, 46–51. [Google Scholar] [CrossRef]

- Choi, J.-H.; Chung, J.; Lee, D.-J. Risk perception analysis: Participation in China’s water PPP market. Int. J. Proj. Manag. 2010, 28, 580–592. [Google Scholar] [CrossRef]

- Yang, T.; Long, R.; Cui, X.; Zhu, D.; Chen, H. Application of the public–private partnership model to urban sewage treatment. J. Clean. Prod. 2017, 142, 1065–1074. [Google Scholar] [CrossRef]

- Cruz, C.O.; Marques, R.C. Infrastructure Public-Private Partnerships-Decision, Management and Development; Springer press: Heidelberg, Germany, 2013. [Google Scholar] [CrossRef]

- Irwin, T. Public Money for Private Infrastructure. 2003. Available online: https://elibrary.worldbank.org/doi/abs/10.1596/978-0-8213-7928-8 (accessed on 1 March 2019).

- Froud, J.; Shaoul, J. Appraising and Evaluating PFI for NHS Hospitals. Financ. Account. Manag. 2003, 17, 247–270. [Google Scholar] [CrossRef]

- Barlow, J.; Roehrich, J.; Wright, S. Europe Sees Mixed Results from Public-Private Partnerships for Building and Managing Health Care Facilities and Services. Health Aff. 2013, 32, 146–154. [Google Scholar] [CrossRef] [PubMed]

- Wibowo, A.; Mohamed, S. Risk criticality and allocation in privatised water supply projects in Indonesia. Int. J. Proj. Manag. 2010, 28, 504–513. [Google Scholar] [CrossRef]

- Chan, A.P.; Ameyaw, E.E. Identifying public-private partnership (PPP) risks in managing water supply projects in Ghana. J. Facil. Manag. 2013, 11, 152–182. [Google Scholar]

- Ke, Y.; Wang, S.; Chan, A.P.; Lam, P.T. Preferred risk allocation in China’s public–private partnership (PPP) projects. Int. J. Proj. Manag. 2010, 28, 482–492. [Google Scholar] [CrossRef]

- Ameyaw, E.E.; Chan, A.P. Evaluation and ranking of risk factors in public–private partnership water supply projects in developing countries using fuzzy synthetic evaluation approach. Expert Syst. Appl. 2015, 42, 5102–5116. [Google Scholar] [CrossRef]

- Xu, Y.; Chan, A.P.C.; Yeung, J.F.Y. Developing a Fuzzy Risk Allocation Model for PPP Projects in China. J. Constr. Eng. Manag. 2010, 136, 894–903. [Google Scholar] [CrossRef]

- Bing, L.; Akintoye, A.; Edwards, P.; Hardcastle, C. The allocation of risk in PPP/PFI construction projects in the UK. Int. J. Proj. Manag. 2005, 23, 25–35. [Google Scholar] [CrossRef]

- Shen, L.-Y.; Platten, A.; Deng, X. Role of public private partnerships to manage risks in public sector projects in Hong Kong. Int. J. Proj. Manag. 2006, 24, 587–594. [Google Scholar] [CrossRef]

- Engle, R.F.; Rangel, J.G. The Spline-GARCH Model for Low-Frequency Volatility and Its Global Macroeconomic Causes. Rev. Financ. Stud. 2008, 21, 1187–1222. [Google Scholar] [CrossRef]

- Carbonara, N.; Costantino, N.; Pellegrino, R. Revenue guarantee in public-private partnerships: A fair risk allocation model. Constr. Manag. Econ. 2014, 32, 403–415. [Google Scholar] [CrossRef]

- Molenaar, K.R.; Ashuri, B.; Lee, S.; Kashani, H.; Lu, J. Risk-neutral pricing approach for evaluating BOT highway projects with government minimum revenue guarantee options. J. Constr. Eng. Manag. 2011, 138, 545–557. [Google Scholar]

- Black, F. Noise. J. Financ. 1986, XLI, 529–543. [Google Scholar] [CrossRef]

- Merton, R.C. Applications of option-pricing theory: Twenty-five years later. Am. Econ. Rev. 1998, 88, 323–349. [Google Scholar]

- Cheah, C.Y.J.; Liu, J. Valuing governmental support in infrastructure projects as real options using Monte Carlo simulation. Constr. Manag. Econ. 2006, 24, 545–554. [Google Scholar] [CrossRef]

- Lander, D.M.; Pinches, G.E. Challenges to the practical implementation of modeling and valuing real options. Q. Rev. Econ. Financ. 1998, 38, 537–567. [Google Scholar] [CrossRef]

- Trigeorgis, L. Real Options and Investment Under Uncertainty: What Do We Know? SSRN Electron. J. 2002, 22, 1–29. [Google Scholar] [CrossRef]

- Brammer, S.; Walker, H. Sustainable procurement in the public sector: An international comparative study. Int. J. Oper. Prod. Manag. 2011, 31, 452–476. [Google Scholar] [CrossRef]

- Case, K.E.; Shiller, R.J. The efficiency of the market for single-family homes. Am. Econ. Assoc. 1989, 79, 125–137. [Google Scholar]

- Vandell, K.D. Optimal Comparable Selection and Weighting in Real Property Valuation. Real Estate Econ. 1991, 19, 213–239. [Google Scholar] [CrossRef]

- Childs, P.D.; Ott, S.H.; Riddiough, T.J. Effects of Noise on Optimal Exercise Decisions: The Case of Risky Debt Secured by Renewable Lease Income. J. Real Estate Financ. Econ. 2004, 28, 109–121. [Google Scholar] [CrossRef]

- Alonso-Bonis, S.; Azofra-Palenzuela, V.; De La Fuente-Herrero, G. Real option value and random jumps: Application of a simulation model. Appl. Econ. 2009, 41, 2977–2989. [Google Scholar] [CrossRef][Green Version]

- Posen, H.E.; Leiblein, M.J.; Chen, J.S. Toward a behavioral theory of real options: Noisy signals, bias, and learning. Strat. Manag. J. 2018, 39, 1112–1138. [Google Scholar] [CrossRef]

- Merton, R.C. Option pricing when underlying stock retures are discontinuous. J. Financ. Econ. 1976, 3, 125–144. [Google Scholar] [CrossRef]

- Lee, S.; Tae, S.; Shin, S. Profit Distribution in Guaranteed Savings Contracts: Determination Based on the Collar Option Model. Sustainability 2015, 7, 16273–16289. [Google Scholar] [CrossRef]

- Almassi, A.; McCabe, B.; Thompson, M. Real Options–Based Approach for Valuation of Government Guarantees in Public–Private Partnerships. J. Infrastruct. Syst. 2012, 19, 196–204. [Google Scholar] [CrossRef]

- Shan, L.; Garvin, M.J.; Kumar, R. Collar options to manage revenue risks in real toll public-private partnership transportation projects. Constr. Manag. Econ. 2010, 28, 1057–1069. [Google Scholar] [CrossRef]

- Brandão, L.E.T.; Saraiva, E. The option value of government guarantees in infrastructure projects. Constr. Manag. Econ. 2008, 26, 1171–1180. [Google Scholar] [CrossRef]

- Wibowo, A. Valuing guarantees in a BOT infrastructure project. Eng. Constr. Arch. Manag. 2004, 11, 395–403. [Google Scholar] [CrossRef]

- Dixit, A.; Pindyck, R. Investment under Uncertainty; Princeton University Press: Princeton, NJ, USA, 1994. [Google Scholar]

- Smith, P.L. From Poisson shot noise to the integrated Ornstein-Uhlenbecled Process: Neurally principled models of information accumulation in decision-makingk and response time. J. Math. Psychol. 2010, 54, 266–283. [Google Scholar] [CrossRef]

- Brigo, D.; Dalessandro, A.; Neugebauer, M.; Triki, F. A Stochastic Processes Toolkit for Risk Management. Available online: https://ssrn.com/abstract=1109160 (accessed on 1 March 2019).

- Ma, Y.; Chen, M.; Cai, Z.; Min, Z. Mean reverting jump-diffusion model of Chian stock warrants. Syst. Eng. Theory Pract. 2010, 30, 14–21. [Google Scholar]

- Berk, A.S.; Podhraski, D. Superiority of Monte Carlo simulation in valuing real options within public-private partnerships. Risk Manag. 2018, 20, 1–28. [Google Scholar] [CrossRef]

- Samis, M.; Davis, G.A. Using Monte Carlo simulation with DCF and real options risk pricing techniques to analyse a mine financing proposal. Int. J. Financ. Eng. Risk Manag. 2014, 1, 264. [Google Scholar] [CrossRef]

- Dashuang, D.; Ning, L.; Xiaoqing, X. Methods of Infrastructure Construction Real Option Pricing Based on the Normal Cloud. Sci. Technol. Prog. Policy 2011, 28, 10–13. [Google Scholar]

- Kokkaew, N.; Chiara, N. A modeling government revenue guarantees in privately built transportation projects: A risk-adjusted approach. Transport 2013, 28, 186–192. [Google Scholar] [CrossRef]

- Bain, R. Error and optimism bias in toll road traffic forecasts. Transp. 2009, 36, 469–482. [Google Scholar] [CrossRef]

- Hong, Y. The investment evaluation of research and development project based on real option method. J. Quant. Tech. Econ. 2003, 2, 73–76. [Google Scholar]

- Flyvbjerg, B.; Holm, M.K.S.; Buhl, S.L. How (In)accurate are Demand Forecasts in Public Works Projects? The Case of Transportation. J. Am. Plan. Assoc. 2005, 71, 131–146. [Google Scholar] [CrossRef]

- Xu, Y.; Yeung, J.F.Y.; Jiang, S. Determining appropriate government guarantees for concession contract: Lessons learned from 10 ppp projects in china. Int. J. Strat. Prop. Manag. 2014, 18, 356–367. [Google Scholar] [CrossRef]

- Luo, M.; Kou, Y. Market driven ship investment decision using the real option approach. Transp. Res. Part A Policy Pract. 2018, 118, 714–729. [Google Scholar]

- Zhao, B.; Yan, C.; Hodges, S. Three One-Factor Processes for Option Pricing with a Mean-Reverting Underlying: The Case of VIX. Financ. Rev. 2019, 54, 165–199. [Google Scholar] [CrossRef]

- Roehrich, J.K.; Lewis, M.A.; George, G. Are public–private partnerships a healthy option? A systematic literature review. Soc. Sci. Med. 2014, 113, 110–119. [Google Scholar] [CrossRef] [PubMed]

- Bekaert, G.; Harvey, C.R. Emerging equity market volatility. J. Financ. Econ. 1997, 43, 29–77. [Google Scholar] [CrossRef]

- Wang, H.; Liu, Y.; Xiong, W.; Song, J. The moderating role of governance environment on the relationship between risk allocation and private investment in PPP markets: Evidence from developing countries. Int. J. Proj. Manag. 2019, 37, 117–130. [Google Scholar] [CrossRef]

- Wang, C.; Zhang, C.; Fang, Z. Jumping Noise Impact on the European Option Pricing. Syst. Eng. 2016, 34, 40–44. [Google Scholar]

- Wang, L.; Pan, H.; Liu, X. Dynamic Linkage of Gold Future Liquidity and Future—Cash Basis in China Market. Sci. Decis. Making 2013, 19–44. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

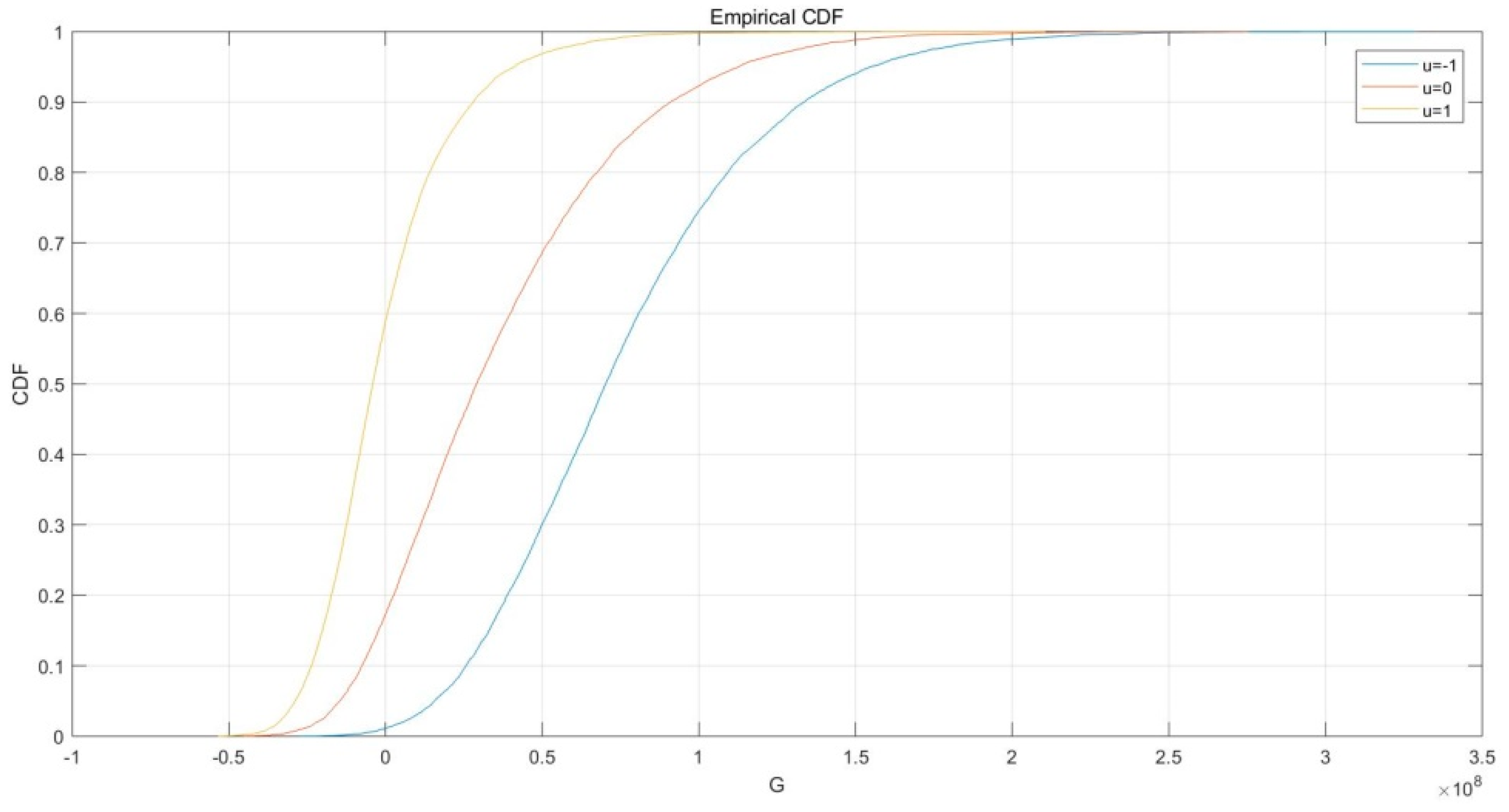

| Project Parameters | Symbol | Value |

|---|---|---|

| Construction cost | 101.18 million | |

| Operation and maintain costs | 2 million | |

| Construction period | 2 years | |

| Operation period | 20 years | |

| Toll Rate | 0.8285 yuan | |

| Design capacity | 80,000 T | |

| Discount rate | 6.90% | |

| Upper threshold | 110% | |

| Lower threshold | 70% | |

| Annual growth rate | 8.40% | |

| Long-term volatility | 6.20% | |

| Mean reverting rate | 0.1 | |

| Short-term volatility | 0.2 | |

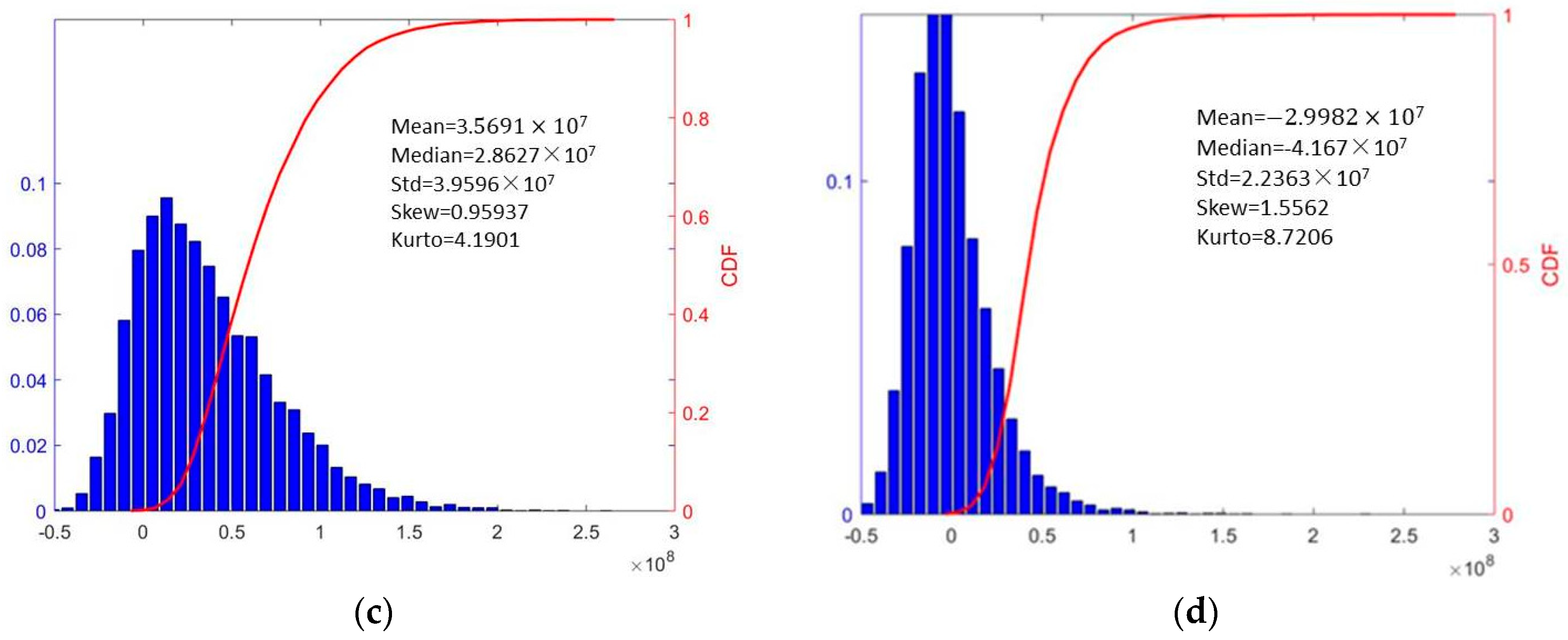

| Mean reversion value | –1 |

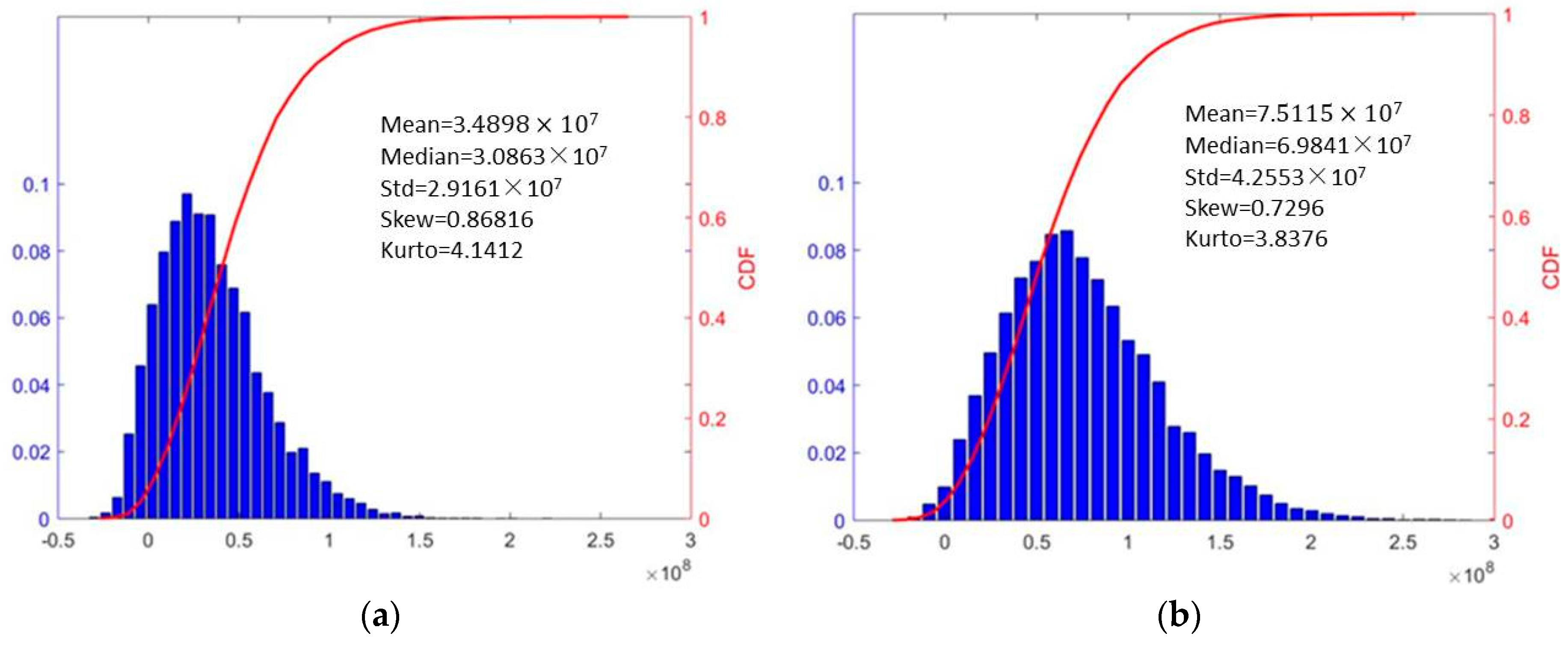

| Parameters | Subplot a | Subplot b | Subplot c | Subplot d |

|---|---|---|---|---|

| Reverting speed () | 0.1 | 1 | 0.1 | 0.1 |

| −1 | −1 | 1 | −1 | |

| Volatility () | 0.5 | 0.5 | 0.5 | 1 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, Q.; Liao, Z.; Guo, Q.; Degefu, D.M.; Wang, S.; Jian, F. Effects of Short-Term Uncertainties on the Revenue Estimation of PPP Sewage Treatment Projects. Water 2019, 11, 1203. https://doi.org/10.3390/w11061203

Liu Q, Liao Z, Guo Q, Degefu DM, Wang S, Jian F. Effects of Short-Term Uncertainties on the Revenue Estimation of PPP Sewage Treatment Projects. Water. 2019; 11(6):1203. https://doi.org/10.3390/w11061203

Chicago/Turabian StyleLiu, Qian, Zaiyi Liao, Qi Guo, Dagmawi Mulugeta Degefu, Song Wang, and Feihong Jian. 2019. "Effects of Short-Term Uncertainties on the Revenue Estimation of PPP Sewage Treatment Projects" Water 11, no. 6: 1203. https://doi.org/10.3390/w11061203

APA StyleLiu, Q., Liao, Z., Guo, Q., Degefu, D. M., Wang, S., & Jian, F. (2019). Effects of Short-Term Uncertainties on the Revenue Estimation of PPP Sewage Treatment Projects. Water, 11(6), 1203. https://doi.org/10.3390/w11061203