Analyzing Environmental Continuous Improvement for Sustainable Supply Chain Management: Focusing on Its Performance and Information Disclosure

Abstract

:1. Introduction

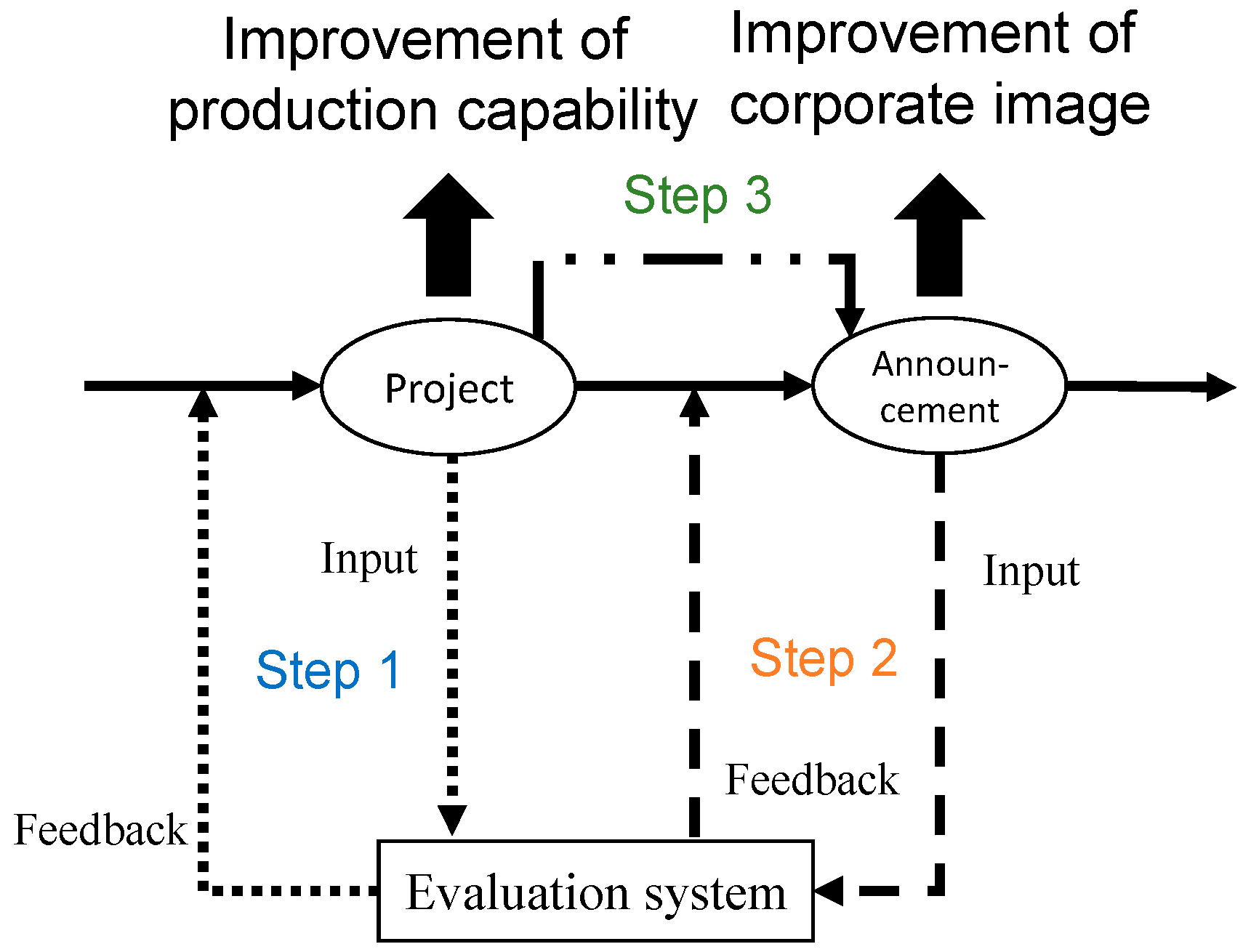

2. Research Procedure by e-CI Framework

3. Analysis of e-CI Implementation and Information Disclosure

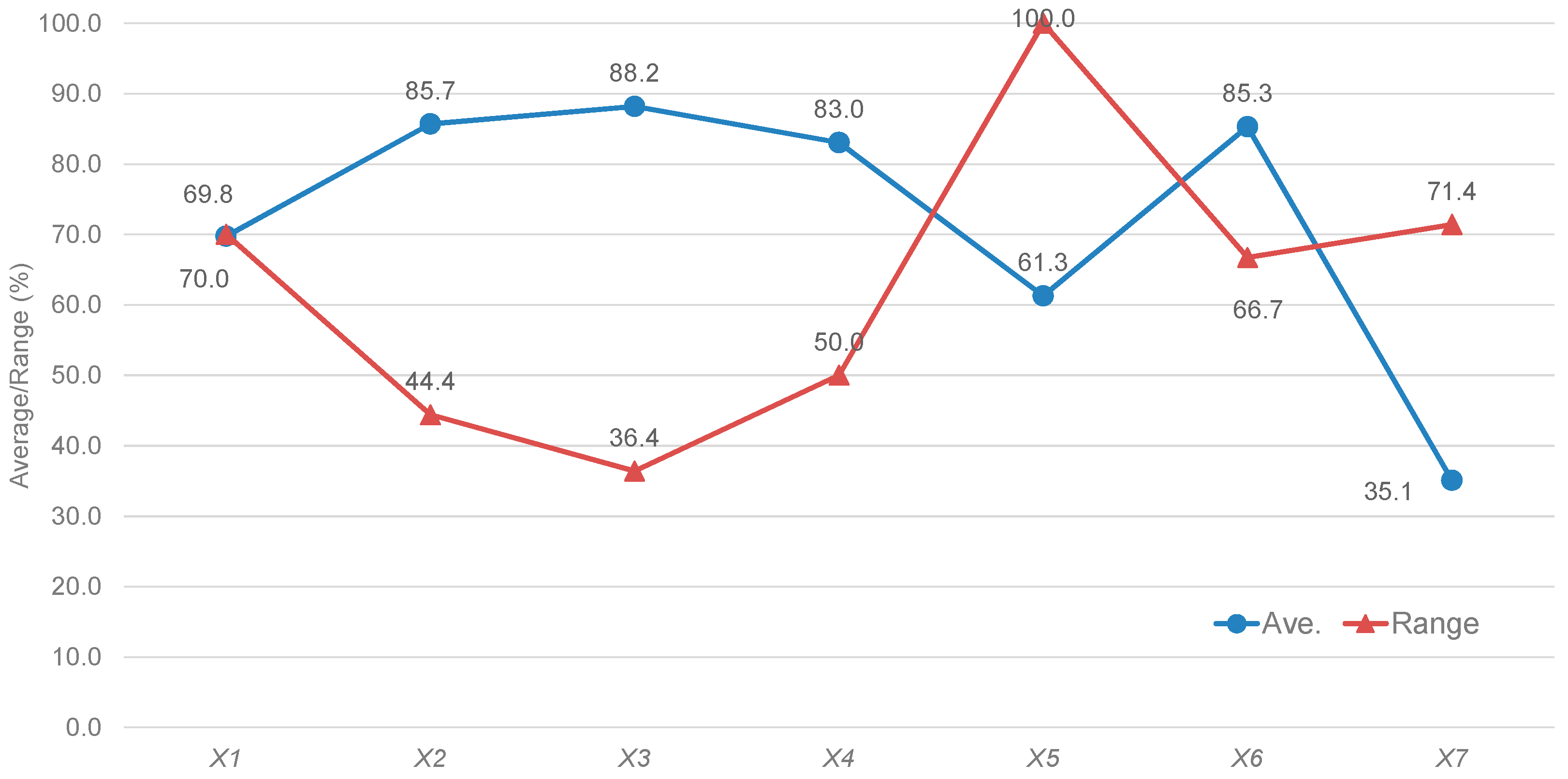

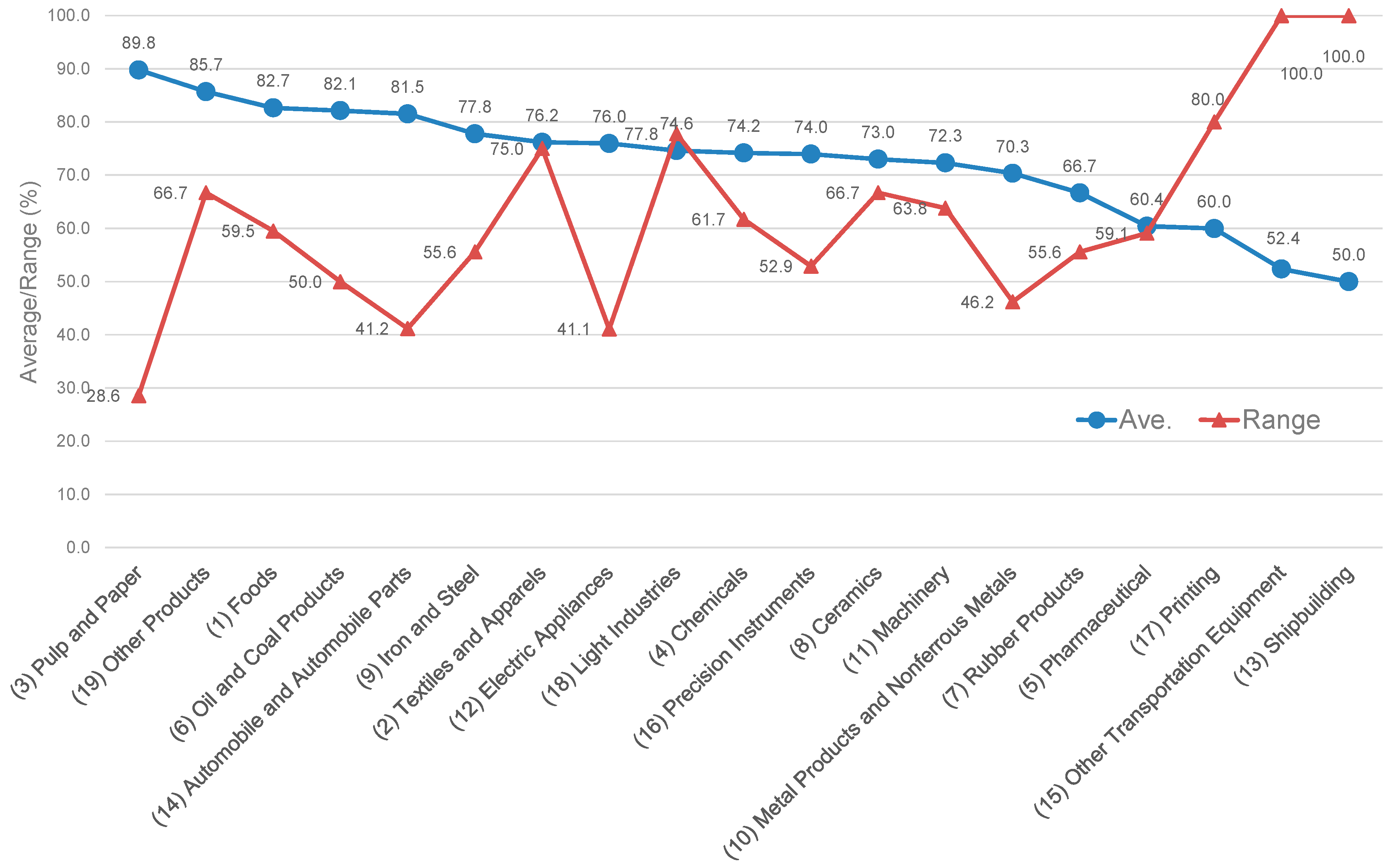

3.1. The State of Environmental Project Implementation (Step 1)

- (X1)

- A modal shift of means of transportation;

- (X2)

- A shift to a fuel-efficient or low-emissions vehicle;

- (X3)

- The shortening of transportation distances and changes in transportation routes;

- (X4)

- The improvement in the capability of packing and wrapping materials to improve loading efficiency;

- (X5)

- A cooperative distribution;

- (X6)

- Energy-saving driving to improve fuel consumption;

- (X7)

- Other SCM activities.

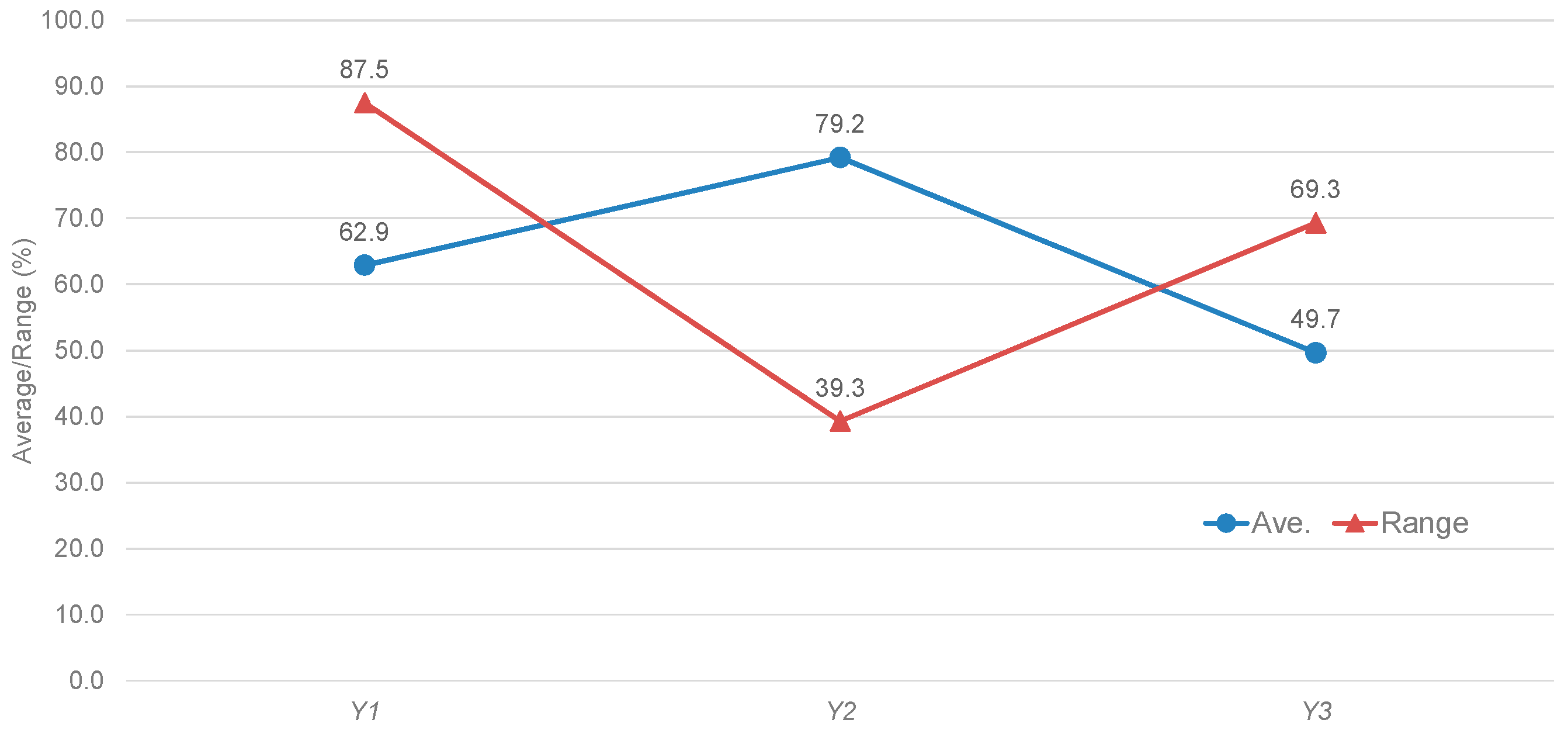

3.2. The State of Information Disclosure for Environmental Indicators (Step 2)

- (Y1)

- A distribution from materials/part companies to your factory;

- (Y2)

- A distribution from your factory to retailers;

- (Y3)

- A distribution to dispose of or recycle used products.

- (Level 1)

- This company has already calculated and announced.

- (Level 2)

- This company has already calculated and plans to announce in the future.

- (Level 3)

- This company has already calculated and does not plan to announce in the future.

- (Level 4)

- This company has no plans to calculate.

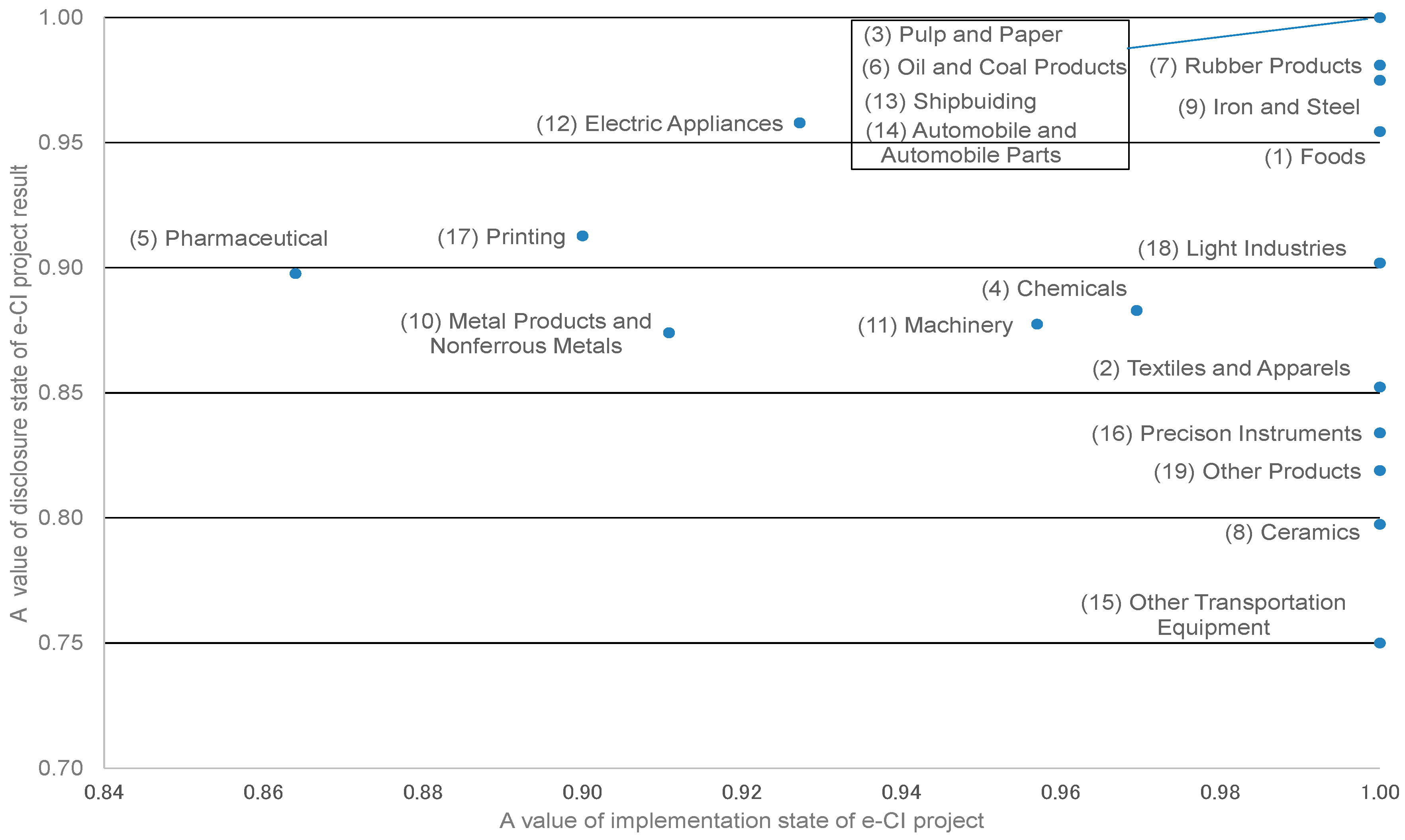

4. Comprehensive Analysis of e-CI (Step 3)

4.1. Conventional Model

4.2. Proposed Model

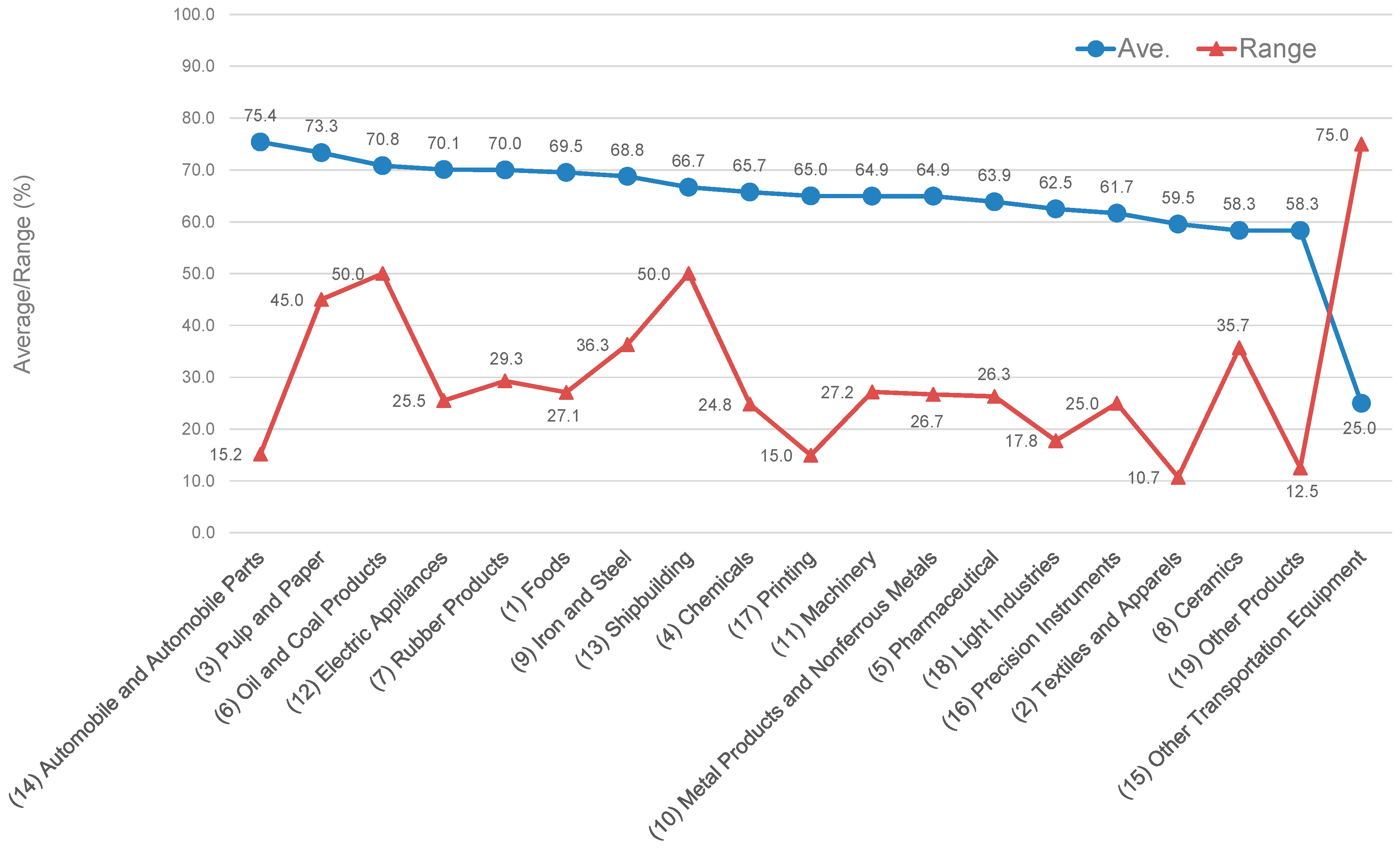

4.3. Calculation Result

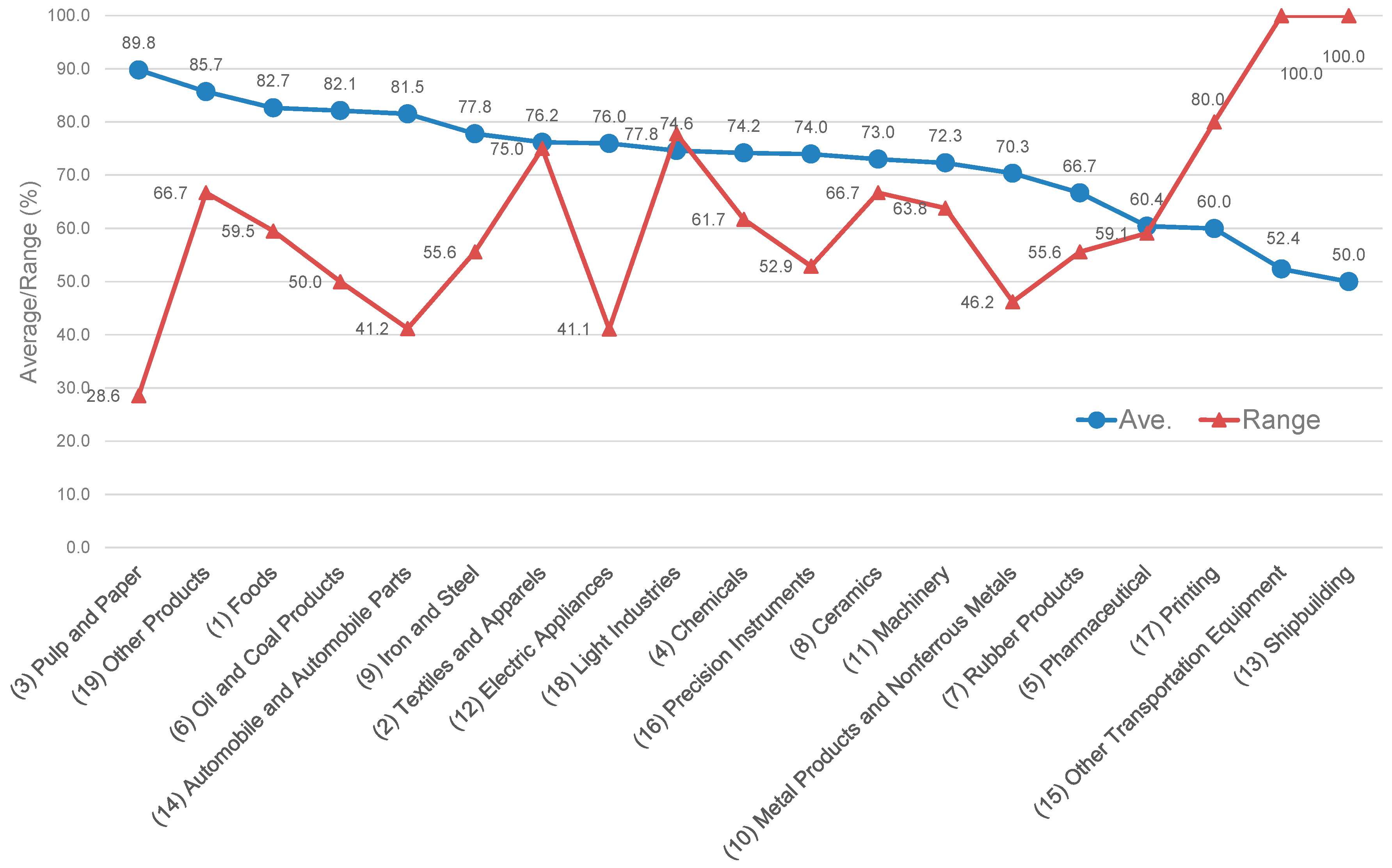

- (3) Pulp and Paper and (15) Other Transportation Equipment -> X1

- (8) Ceramics and (13) Shipbuilding -> X2

- (7) Rubber Products -> X3

- (19) Other Products -> X5

- (2) Textiles and Apparel; (9) Iron and Steel; and (18) Light Industries -> X6

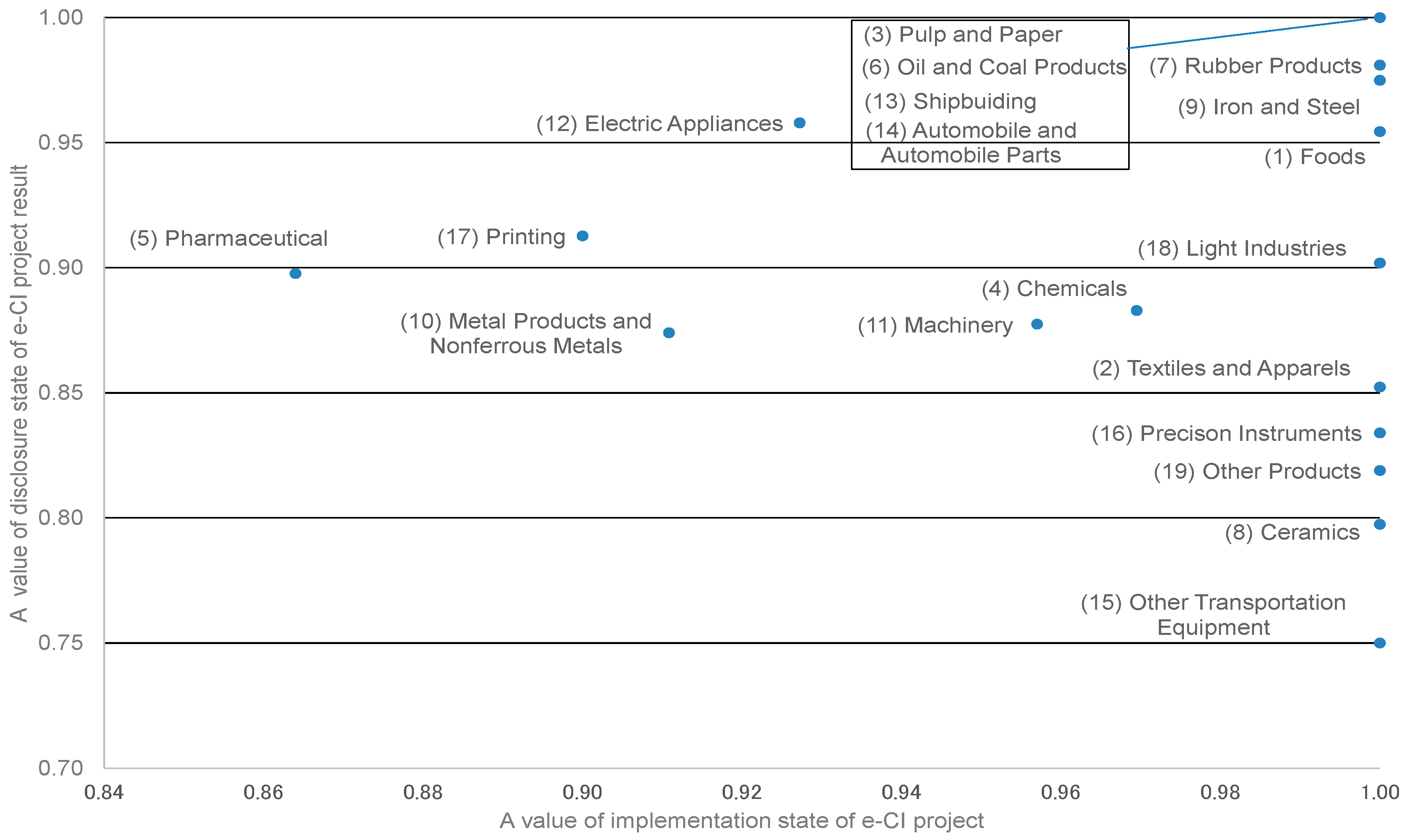

4.4. Classification of Manufacturing Types

- First group:

- Above average values for the two states

- Second group:

- Above average value for implementation stateBelow average value for disclosure state

- Third group:

- Below average value for implementation stateAbove average value for disclosure state

- Fourth group:

- Below average values for the two states

5. Conclusions

References

- Lohman, C.; Fortuin, L.; Wouters, M. Designing a performance measurement system: A case study. Eur. J. Oper. Res. 2004, 156, 267–286. [Google Scholar] [CrossRef]

- Xiong, G.; Qin, T.; Wang, F.; Hu, L.; Shi, Q. Design and improvement of KPI system for materials management in Power Group Enterprise. In Proceedings of the 2010 IEEE International Conference on Service Operations and Logistics and Informatics (SOLI), Qingdao, China, 15–17 July 2010; pp. 171–176.

- Alemanni, M.; Alessia, G.; Tornincasa, S.; Vezzetti, E. Key performance indicators for PLM benefits evaluation: The Alcatel Alenia Space case study. Comput. Ind. 2008, 59, 833–841. [Google Scholar] [CrossRef]

- Amrina, E.; Yusof, S.M. Key performance indicators for sustainable manufacturing evaluation in automotive companies. In Proceedings of the 2011 IEEE International Conference on Industrial Engineering and Engineering Management (IEEM), Hong Kong, China, 10–13 December 2011; pp. 1093–1097.

- Veleva, V.; Ellenbecker, M. Indicators of sustainable production: Framework and methodology. J. Clean. Prod. 2001, 9, 519–549. [Google Scholar] [CrossRef]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. Development of composite sustainability performance index for steel industry. Ecol. Indic. 2007, 7, 565–588. [Google Scholar] [CrossRef]

- Tseng, M.L.; Divinagracia, L.; Divinagracia, R. Evaluating firm’s sustainable production indicators in uncertainty. Comput. Ind. Eng. 2009, 57, 1393–1403. [Google Scholar] [CrossRef]

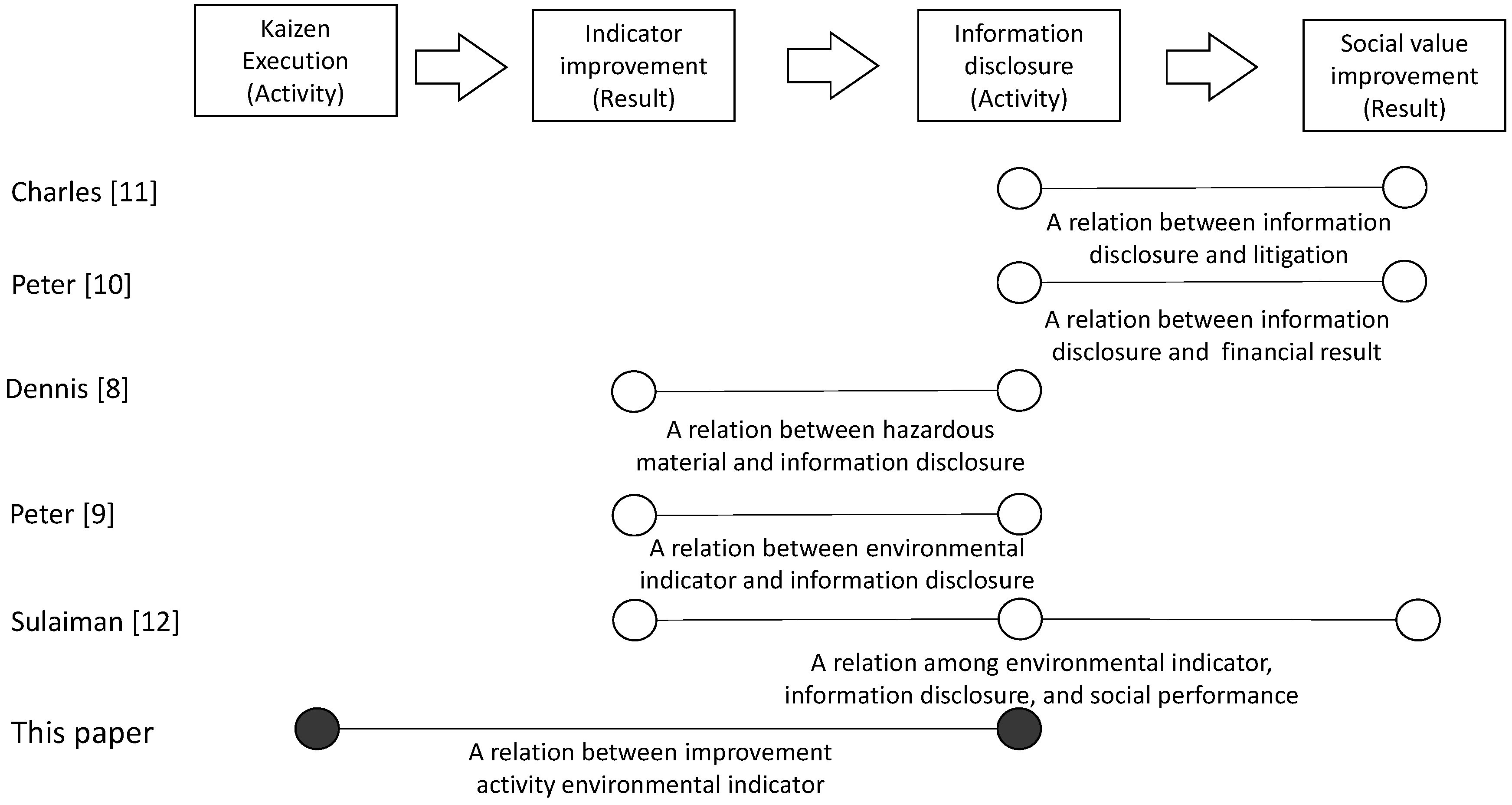

- Dennis, M.P. The relation between environmental performance and environmental disclosure: A research note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar]

- Peter, M.C.; Yue, L.; Gordon, D.R.; Florin, P.V. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 29, 303–327. [Google Scholar]

- Peter, A.S.; Sarah, D.S. The Relationship between corporate social performance, and organizational size, financial performance, and environmental performance: An empirical examination. J. Bus. Ethics 1998, 17, 195–204. [Google Scholar]

- Charles, H.C.; Dennis, M.P. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar]

- Sulaiman, A.A.-T.; Theodore, E.C.; Hughes, K.E., II. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar]

- Lillrank, P.; Kano, N. Continuous Improvement—Quality Control Circles in Japanese Industry; University of Michiganm: Ann Arbor, MI, USA, 1989. [Google Scholar]

- Nikkei Inc.; Nikkei Research Inc. (Eds.) Survey Report: 17th Survey of Environmental Management (Tyousa Houkusyo: 17kai Kankyou Keieido Tyousa); Nikkei Research Inc.: Tokyo, Japan, 2014. (In Japanese)

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Banker, D.R.; Charnes, A.; Cooper, W.W. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Manag. Sci. 1984, 30, 1078–1092. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Lewin, Y.A.; Seiford, M.L. Data Envelopment Analysis: Theory, Methodology and Applications; Kluwer Academic Publisher: Boston, MA, USA, 1994. [Google Scholar]

- Cooper, W.W.; Seiford, L.M.; Tone, K. Data Envelopment Analysis: A Comprehensive Text with Models, Applications, References, and DEA-Solver Software; Springer: Dordrecht, The Netherlands, 1999. [Google Scholar]

- Murata, K.; Katayama, H. An evaluation of factory performance utilized KPI/KAI with data envelopment analysis. J. Oper. Res. Soc. Jpn. (JORSJ) 2009, 52, 204–220. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Environmental Project | X1 | X2 | X3 | X4 | X5 | X6 | X7 | |

|---|---|---|---|---|---|---|---|---|

| Type of Manufacturing Industry | ||||||||

| (1) Foods | 88.1 | 81.0 | 100.0 | 88.1 | 90.5 | 90.5 | 40.5 | |

| (2) Textiles and Apparel | 83.3 | 83.3 | 100.0 | 91.7 | 50.0 | 100.0 | 25.0 | |

| (3) Pulp and Paper | 100.0 | 100.0 | 85.7 | 85.7 | 85.7 | 100.0 | 71.4 | |

| (4) Chemicals | 85.3 | 75.0 | 94.1 | 86.8 | 64.7 | 80.9 | 32.4 | |

| (5) Pharmaceutical | 36.4 | 86.4 | 63.6 | 63.6 | 59.1 | 86.4 | 27.3 | |

| (6) Oil and Coal Products | 75.0 | 100.0 | 100.0 | 75.0 | 75.0 | 100.0 | 50.0 | |

| (7) Rubber Products | 66.7 | 55.6 | 100.0 | 88.9 | 66.7 | 44.4 | 44.4 | |

| (8) Ceramics | 55.6 | 100.0 | 88.9 | 88.9 | 33.3 | 100.0 | 44.4 | |

| (9) Iron and Steel | 88.9 | 88.9 | 88.9 | 66.7 | 66.7 | 100 | 44.4 | |

| (10) Metal Products and Nonferrous Metals | 65.4 | 73.1 | 80.8 | 88.5 | 57.7 | 84.6 | 42.3 | |

| (11) Machinery | 66.0 | 91.5 | 85.1 | 87.2 | 48.9 | 95.7 | 31.9 | |

| (12) Electric Appliances | 65.9 | 87.1 | 87.1 | 87.1 | 69.4 | 88.2 | 47.1 | |

| (13) Shipbuilding | 50.0 | 100.0 | 100.0 | 50.0 | 0.0 | 50.0 | 0.0 | |

| (14) Automobile and Automobile Parts | 70.6 | 82.4 | 94.1 | 94.1 | 82.4 | 94.1 | 52.9 | |

| (15) Other Transportation Equipment | 100 | 66.7 | 66.7 | 66.7 | 33.3 | 33.3 | 0.0 | |

| (16) Precision Instruments | 64.7 | 88.2 | 82.4 | 100 | 52.9 | 82.4 | 47.1 | |

| (17) Printing | 30.0 | 80.0 | 80.0 | 80.0 | 50.0 | 90.0 | 10.0 | |

| (18) Light Industries | 66.7 | 88.9 | 77.8 | 88.9 | 77.8 | 100 | 22.2 | |

| (19) Other Products | 66.7 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 33.3 | |

| Environmental Indicator | Y1 | Y2 | Y3 | |

|---|---|---|---|---|

| Type of Manufacturing Industry | ||||

| (1) Foods | 63.8 | 85.9 | 58.8 | |

| (2) Textiles and Apparel | 64.3 | 60.7 | 53.6 | |

| (3) Pulp and Paper | 75.0 | 95.0 | 50.0 | |

| (4) Chemicals | 65.2 | 78.4 | 53.6 | |

| (5) Pharmaceutical | 72.5 | 72.7 | 46.4 | |

| (6) Oil and Coal Products | 87.5 | 87.5 | 37.5 | |

| (7) Rubber Products | 60.7 | 89.3 | 60.0 | |

| (8) Ceramics | 60.7 | 75.0 | 39.3 | |

| (9) Iron and Steel | 81.3 | 80.0 | 45.0 | |

| (10) Metal Products and Nonferrous Metals | 64.3 | 78.6 | 51.9 | |

| (11) Machinery | 66.2 | 77.9 | 50.7 | |

| (12) Electric Appliances | 64.8 | 85.5 | 60.0 | |

| (13) Shipbuilding | 50.0 | 100.0 | 50.0 | |

| (14) Automobile and Automobile Parts | 72.4 | 84.5 | 69.3 | |

| (15) Other Transportation Equipment | 0.0 | 75.0 | 0.0 | |

| (16) Precision Instruments | 60.0 | 75.0 | 50.0 | |

| (17) Printing | 70.0 | 70.0 | 55.0 | |

| (18) Light Industries | 53.6 | 71.4 | 62.5 | |

| (19) Other Products | 62.5 | 62.5 | 50.0 | |

| Type of Manufacturing Industry | ||

|---|---|---|

| (1) Foods | 1.00 | 0.95 |

| (2) Textiles and Apparel | 1.00 | 0.85 |

| (3) Pulp and Paper | 1.00 | 1.00 |

| (4) Chemicals | 0.97 | 0.88 |

| (5) Pharmaceutical | 0.86 | 0.90 |

| (6) Oil and Coal Products | 1.00 | 1.00 |

| (7) Rubber Products | 1.00 | 0.98 |

| (8) Ceramics | 1.00 | 0.80 |

| (9) Iron and Steel | 1.00 | 0.97 |

| (10) Metal Products and Nonferrous Metals | 0.91 | 0.87 |

| (11) Machinery | 0.96 | 0.88 |

| (12) Electric Appliances | 0.93 | 0.96 |

| (13) Shipbuilding | 1.00 | 1.00 |

| (14) Automobile and Automobile Parts | 1.00 | 1.00 |

| (15) Other Transportation Equipment | 1.00 | 0.75 |

| (16) Precision Instruments | 1.00 | 0.83 |

| (17) Printing | 0.90 | 0.91 |

| (18) Light Industries | 1.00 | 0.90 |

| (19) Other Products | 1.00 | 0.82 |

| Ave. | 0.98 | 0.91 |

| Range | 0.14 | 0.25 |

| Type of Manufacturing Industry | Iu*1 | Iu*2 | Iu*3 | Iu*4 | Iu*5 | Iu*6 | Iu*7 |

|---|---|---|---|---|---|---|---|

| (X1) | (X2) | (X3) | (X4) | (X5) | (X6) | (X7) | |

| (1) Foods | 3.34 × 10−3 | 0.00 | 2.54 × 10−4 | 0.00 | 7.52 × 10−3 | 0 | 0.00 |

| (2) Textiles and Apparel | 5.20 × 10−17 | 0.00 | 0 | 2.17 × 10−18 | 0.00 | 1.00 × 10−2 | 0.00 |

| (3) Pulp and Paper | 1.00 × 10−2 | 0.00 | 0 | 0.00 | 0.00 | 0.00 | 0.00 |

| (4) Chemicals | 3.75 × 10−3 | 0.00 | 2.28 × 10−3 | 5.00 × 10−3 | 0.00 | 0.00 | 0.00 |

| (5) Pharmaceutical | 0.00 | 1.00 × 10−2 | 0 | 0.00 | 0.00 | 0.00 | 0.00 |

| (6) Oil and Coal Products | 3.14 × 10−3 | 2.16 × 10−3 | 5.48 × 10−3 | 0.00 | 0.00 | 0.00 | 0.00 |

| (7) Rubber Products | 0.00 | 0.00 | 1.00 × 10−2 | 6.51 × 10−19 | 0.00 | 0.00 | 4.34 × 10−18 |

| (8) Ceramics | 0.00 | 1.00 × 10−2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| (9) Iron and Steel | 5.20 × 10−17 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 × 10−2 | 0.00 |

| (10) Metal Products and Nonferrous Metals | 0.00 | 0.00 | 0.00 | 7.05 × 10−3 | 0.00 | 2.07 × 10−3 | 2.64 × 10−3 |

| (11) Machinery | 5.20 × 10−17 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 × 10−2 | 0.00 |

| (12) Electric Appliances | 0.00 | 6.85 × 10−4 | 6.20 × 10−3 | 2.08 × 10−3 | 0.00 | 0.00 | 3.11 × 10−3 |

| (13) Shipbuilding | 0.00 | 1.00 × 10−2 | 4.34 × 10−19 | 0 | 0.00 | 0.00 | 0.00 |

| (14) Automobile and Automobile Parts | 0.00 | 0.00 | 6.66 × 10−3 | 1.13 × 10−3 | 1.10 × 10−3 | 0.00 | 3.34 × 10−3 |

| (15) Other Transportation Equipment | 1.00 × 10−2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| (16) Precision Instruments | 2.92 × 10−3 | 0.00 | 0.00 | 7.91 × 10−3 | 0.00 | 0.00 | 4.23 × 10−4 |

| (17) Printing | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 × 10−2 | 0.00 |

| (18) Light Industries | 4.21 × 10−17 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 × 10−2 | 0.00 |

| (19) Other Products | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 × 10−2 | 0.00 | 0.00 |

| Type of Manufacturing Industry | Au*1 | Au*2 | Au*3 |

|---|---|---|---|

| (Y1) | (Y2) | (Y3) | |

| (1) Foods | 1.44 × 10−3 | 7.22 × 10−3 | 4.12 × 10−3 |

| (2) Textiles and Apparel | 9.50 × 10−3 | 0.00 | 4.51 × 10−3 |

| (3) Pulp and Paper | 1.82 × 10−3 | 9.09 × 10−3 | 0.00 |

| (4) Chemicals | 5.74 × 10−3 | 4.34 × 10−3 | 3.14 × 10−3 |

| (5) Pharmaceutical | 9.50 × 10−3 | 0.00 | 4.51 × 10−3 |

| (6) Oil and Coal Products | 1.14 × 10−2 | 0.00 | 0.00 |

| (7) Rubber Products | 0.00 | 7.13 × 10−3 | 5.73 × 10−3 |

| (8) Ceramics | 5.74 × 10−3 | 4.34 × 10−3 | 3.14 × 10−3 |

| (9) Iron and Steel | 9.50 × 10−3 | 0.00 | 4.51 × 10−3 |

| (10) Metal Products and Nonferrous Metals | 1.44 × 10−3 | 7.22 × 10−3 | 4.12 × 10−3 |

| (11) Machinery | 5.74 × 10−3 | 4.34 × 10−3 | 3.14 × 10−3 |

| (12) Electric Appliances | 1.44 × 10−3 | 7.22 × 10−3 | 4.12 × 10−3 |

| (13) Shipbuilding | 0.00 | 1.00 × 10−2 | 0.00 |

| (14) Automobile and Automobile Parts | 1.44 × 10−3 | 7.22 × 10−3 | 4.12 × 10−3 |

| (15) Other Transportation Equipment | 0.00 | 1.00 × 10−2 | 0.00 |

| (16) Precision Instruments | 1.44 × 10−3 | 7.22 × 10−3 | 4.12 × 10−3 |

| (17) Printing | 9.50 × 10−3 | 0.00 | 4.51 × 10−3 |

| (18) Light Industries | 0.00 | 0.00 | 1.44 × 10−2 |

| (19) Other Products | 9.50 × 10−3 | 0.00 | 4.51 × 10−3 |

| (a) | Three + | Two | One | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| (b) | Three | Two | One | Three | Two | One | Three | Two | One | |

| First Group | (1) Foods (14) Automobile and Automobile Parts | (6) Oil and Coal Products | (3) Pulp and Paper (7) Rubber Products (9) Iron and Steel | (13) Shipbuilding | ||||||

| Second Group | (16) Precision Instruments | (8) Ceramics | (2) Textiles and Apparel (19) Other Products | (15) Other Transportation Equipment (18) Light Industries | ||||||

| Third Group | (12) Electric Appliances | (5) Pharmaceutical (17) Printing | ||||||||

| Fourth Group | (4) Chemicals (10) Metal Products and Nonferrous Metals | (11) Machinery | ||||||||

© 2016 by the author; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Murata, K. Analyzing Environmental Continuous Improvement for Sustainable Supply Chain Management: Focusing on Its Performance and Information Disclosure. Sustainability 2016, 8, 1256. https://doi.org/10.3390/su8121256

Murata K. Analyzing Environmental Continuous Improvement for Sustainable Supply Chain Management: Focusing on Its Performance and Information Disclosure. Sustainability. 2016; 8(12):1256. https://doi.org/10.3390/su8121256

Chicago/Turabian StyleMurata, Koichi. 2016. "Analyzing Environmental Continuous Improvement for Sustainable Supply Chain Management: Focusing on Its Performance and Information Disclosure" Sustainability 8, no. 12: 1256. https://doi.org/10.3390/su8121256

APA StyleMurata, K. (2016). Analyzing Environmental Continuous Improvement for Sustainable Supply Chain Management: Focusing on Its Performance and Information Disclosure. Sustainability, 8(12), 1256. https://doi.org/10.3390/su8121256