Abstract

In the evolving landscape of China’s capital markets, the integration of Environmental, Social, and Governance (ESG) considerations has become increasingly crucial for investors and decision-makers. Traditional financial performance metrics often fall short in capturing the multidimensional and long-term impacts of ESG factors. This study introduces a novel computational framework that combines domain-adapted pre-trained language models with structured financial regression analysis, aiming to empirically assess the correlation between ESG disclosures and long-term financial performance. This approach allows for the simultaneous processing of both structured and unstructured ESG data, using graph-based modeling and reinforcement learning to guide sustainability aligned policy optimization. Our empirical results show that firms with consistent and well-structured ESG strategies exhibit significantly superior long-term financial outcomes compared to those with weak or inconsistent ESG engagement. This study not only confirms the value of ESG engagement in enhancing financial resilience but also offers practical recommendations for investors, regulators, and corporate decision-makers, emphasizing consistent disclosure, sector-aligned ESG investment, and proactive adaptation to policy shifts.

1. Introduction

In recent years, integrating Environmental, Social, and Governance (ESG) principles into corporate strategy has become key to sustainable business success, especially in China’s changing regulatory and economic environment [1]. This shift is partly driven by increasing emphasis from regulatory bodies like the China Securities Regulatory Commission (CSRC), which issued the 2022 Guidelines on Strengthening ESG Disclosure, requiring more transparency on sustainability risks and governance [2]. Complementary policies such as the Green Industry Guiding Catalogue and the expansion of the green bond market have reinforced the institutional push toward ESG compliance [3]. While ESG adoption is sometimes seen as symbolic or reputational, studies show it can also bring measurable financial benefits. For example, firms with higher ESG ratings have been shown to exhibit stronger Return on Assets (ROA), lower capital costs, and improved investor sentiment, particularly in industries subject to environmental regulation [4]. Frameworks such as the China Corporate ESG Disclosure Guidelines and pilot implementations of SASB- and TCFD-aligned standards are further anchoring ESG reporting practices in China. These developments suggest that ESG strategies are not merely aspirational but are increasingly aligned with material financial outcomes and strategic competitiveness, particularly in an environment of rising investor scrutiny and evolving regulatory expectations [5].

Early studies exploring the financial implications of ESG strategies predominantly drew upon established financial theories and expert-driven evaluation criteria [6]. These models typically employed structured metrics and rule-based logic to assess firm performance, relying heavily on predefined benchmarks and regulatory disclosures [7]. While such approaches provided a systematic starting point for integrating ESG into financial assessments, they often struggled to adapt to the multidimensional and evolving nature of sustainability practices [8]. Thus, it is important to study how ESG strategies affect long-term financial outcomes in China’s changing capital markets. In 2022, the China Securities Regulatory Commission (CSRC) introduced mandatory ESG disclosure guidelines for listed companies, accompanied by enhanced green finance regulations such as the updated Green Bond Endorsed Project Catalogue. Simultaneously, institutional investors—both domestic and foreign—have begun integrating ESG metrics into valuation models and portfolio screening [9,10]. Traditional evaluation models often rely on backward-looking financial ratios and fail to account for the evolving materiality of ESG factors, especially when sustainability initiatives have long-term payoff horizons. Moreover, a critical distinction must be made between ESG disclosure (the act of reporting) and actual ESG performance (measurable improvements in environmental or social outcomes). This gap often results in “green window dressing” or symbolic compliance, which may distort assessments of financial risk and return. Our proposed approach addresses these gaps by combining structured financial data with unstructured ESG narratives, leveraging temporal dynamics and graph-based reasoning to capture the substantive effects of ESG initiatives [11].

Despite significant advances in ESG research, many existing models overlook the symbolic and dynamic nature of ESG disclosures. These models tend to focus primarily on quantitative ESG metrics, failing to capture the qualitative, context-specific aspects of ESG performance that are particularly relevant in markets like China. For instance, many traditional frameworks are rigid in their application of standardized ESG scores and do not account for the evolving regulatory context or sector-specific nuances that significantly affect ESG performance. Our model is distinct in that it integrates both structured financial data and unstructured ESG narratives, enabling it to capture not only the static ESG metrics but also the temporal and symbolic dimensions of ESG actions. By utilizing advanced natural language processing (NLP) techniques and graph-based learning, our model is able to process ESG disclosures as dynamic and contextually rich sources of information. This approach allows for more accurate predictions of long-term financial outcomes by considering the changing nature of ESG performance over time and its interaction with regulatory shifts.

Responding to the growing intricacy of ESG information, subsequent research began to incorporate algorithmic models that could uncover patterns from large-scale datasets and heterogeneous information sources [12]. These methods extended traditional frameworks by allowing more dynamic assessment of the interactions between ESG factors and financial performance [13]. For example, statistical learning techniques were increasingly applied to link firm disclosures, market indicators, and ESG ratings with financial outcomes across varying time horizons [14]. While these models contributed to enhanced empirical understanding, they also raised concerns about interpretability, consistency, and data reliability, especially in markets like China where ESG standardization remains in flux [15].

More recently, advancements in natural language processing and computational modeling have opened new possibilities for ESG analysis through the use of semantic-rich textual data [16]. These approaches utilize corporate reports, media coverage, and other narrative disclosures to extract insights that extend beyond quantitative indicators [17]. Responding to the growing complexity of ESG information, in our proposed framework, Long Short-Term Memory (LSTM) is integrated as part of the ESG temporal encoder, while Transformer-based modules are utilized for cross-sector risk propagation analysis and symbolic attention fusion, consistent with recent domain-adapted modeling practices to extract patterns from large-scale, multi-modal ESG datasets [18]. These models are typically validated through cross-validation, temporal holdout tests, or out-of-sample forecasts to ensure robustness in predicting financial or reputational outcomes. In addition to structured indicators, natural language processing (NLP) techniques have been employed to analyze ESG narratives from annual reports and news articles, using tools such as word embeddings, BERT-based classifiers, and topic modeling. Despite these advancements, challenges persist, especially in China, where ESG disclosure standards vary across sectors and lack temporal consistency. Recent research has sought to localize models by adapting them to domain-specific ESG taxonomies (e.g., CSRC guidelines), applying frequency-aware normalization techniques, and customizing entity recognition for Chinese regulatory language. To enhance transparency and interpretability, explainable AI tools such as SHAP (Shapley Additive Explanations) and attention visualization are increasingly integrated into model pipelines. However, limitations persist. Many existing models rely heavily on the quality of voluntary ESG disclosure, which can introduce reporting bias and greenwashing. Others fail to capture causal mechanisms or disentangle long-term ESG effects from short-term volatility. Our proposed approach seeks to address these issues by combining symbolic modeling with deep learning and incorporating structured priors and temporal alignment, offering a more robust and interpretable framework tailored to China’s evolving ESG environment [19].

To address the limitations of symbolic rigidity, data-driven inconsistencies, and semantic generalization, we propose a novel hybrid approach that combines domain-specific pre-trained language models with financial performance regression, tailored to the Chinese capital market. This method not only captures textual and structured ESG signals but also contextualizes them using localized knowledge and industry heterogeneity. By integrating multi-source data and advanced NLP techniques, our framework ensures both interpretability and predictive power, aligning with the unique disclosure characteristics and regulatory structures in China. Furthermore, our empirical design incorporates time-series financial performance indicators to assess long-term impact, thus bridging the gap between ESG actions and strategic financial outcomes. This integrated method offers a new paradigm for ESG evaluation that supports decision-making for investors, regulators, and corporate managers alike.

- We introduce a new domain-adapted pre-trained model that jointly encodes ESG textual disclosures and financial signals, enabling end-to-end prediction of long-term firm performance.

- The method demonstrates strong adaptability across sectors and regulatory environments in China, supporting robust, interpretable, and scalable ESG assessment.

- To operationalize this hypothesis, we propose a hybrid computational framework that integrates symbolic reasoning, temporal dynamics modeling, and graph-based learning. The full architecture—described in detail in Section 3—is designed to process heterogeneous ESG information and produce interpretable forecasts of long-term financial performance across diverse sectors and datasets.

Building upon the context outlined above, the overarching goal of this study is to investigate whether and how ESG management strategies contribute to the long-term financial performance of publicly listed firms in China.

The main objectives of the study are as follows: (i) To develop a computational framework capable of capturing both structured financial data and unstructured ESG textual information; (ii) To integrate ESG-related disclosures with firm-level financial metrics through an interpretable, graph-based, and temporally aware learning model; (iii) To conduct extensive empirical validation across multiple ESG data sources to ensure generalizability of findings; and (iv) To provide actionable insights into the strategic use of ESG policies in enhancing long-term financial outcomes under regulatory and market uncertainty. The working hypothesis of this research is the following: Firms with consistent, sector-aligned, and transparently communicated ESG strategies exhibit superior long-term financial performance compared to firms with weak or inconsistent ESG engagement. This hypothesis is tested by examining multi-year Return on Assets (ROA) and Tobin’s Q trends across ESG quartiles, supported by machine learning-based regression and policy optimization techniques. The study further explores whether the predictive relationship between ESG and financial outcomes remains stable across sectors and data sources. This study contributes to the growing body of research on ESG practices in the China Capital Market, providing insights into how Hybrid Modeling can improve financial forecasting in the context of ESG disclosures. Table 1 presents the definitions of the abbreviations used in this study, providing clarity on terms like MLP, DAG, and QKV.

Table 1.

Definitions of Abbreviations.

2. Related Work

2.1. ESG and Financial Performance

Over the past two decades, the relationship between Environmental, Social, and Governance (ESG) practices and corporate financial performance has attracted considerable academic and practitioner interest. A diverse body of empirical research—spanning cross-sectional regressions, panel data models, and event studies—has investigated how ESG adoption influences a firm’s risk-return profile [20]. While many studies report positive or non-negative associations, the findings are not uniform. For instance, Friede et al. synthesized over 2000 studies and found that approximately 90% reported non-negative results, with 60% showing statistically significant positive relationships. However, these effects vary significantly across geographies, sectors, firm sizes, and ESG dimensions. Most literature establishes correlations rather than causality. Only a limited number of studies employ quasi-experimental designs—such as difference-in-differences or instrumental variables—to address endogeneity. Even then, challenges like omitted variable bias persist. ESG performance may be confounded by firm-specific attributes such as reputation, managerial quality, or innovation capability, which influence both sustainability engagement and financial outcomes. Despite these limitations, several mechanisms have been proposed to explain how ESG practices might enhance firm value. These include reduced regulatory penalties through environmental compliance, stronger stakeholder trust via social initiatives, and lower capital costs due to governance transparency [21]. For example, companies that implement robust emission control policies or fair labor practices have been shown to improve operational efficiency and reduce litigation risks over time. Nonetheless, many of these benefits manifest over extended time horizons and may entail short-term costs, such as higher disclosure expenditures or compliance burdens. The governance pillar of ESG deserves particular attention. Practices such as board independence, shareholder rights protection, and anti-bribery controls are consistently associated with improved financial outcomes in emerging markets [22]. However, disclosure does not necessarily imply authentic performance. In jurisdictions with weak enforcement, symbolic compliance or “greenwashing” may distort ESG assessments and mislead investors. In the context of China, ESG–finance research is still developing, but evidence suggests that firms with strong ESG performance tend to access capital more efficiently and attain valuation premiums. However, results are more volatile in sectors like heavy industry, where ESG standards remain ambiguous and enforcement varies. These patterns highlight the need for context-sensitive modeling that accounts for sectoral, temporal, and regulatory heterogeneity. Our study contributes to this discourse by proposing a hybrid framework that captures both structured ESG indicators and unstructured textual disclosures, offering a more interpretable and temporally aware assessment of ESG’s financial relevance.

2.2. ESG Strategies in Emerging Markets

Emerging markets provide a unique backdrop for the development and impact of Environmental, Social, and Governance (ESG) strategies. Unlike developed economies that typically feature well-established regulatory systems and institutional investors actively promoting sustainability, emerging markets such as China exhibit diverse levels of ESG adoption, inconsistent reporting standards, and varying degrees of investor awareness. Research highlights the importance of institutional gaps, regulatory environments, and socio-political dynamics in influencing how ESG is integrated within corporate practices [23]. The institutional context in these markets significantly affects corporate governance and sustainability approaches. Weak legal enforcement and a lack of transparency in disclosure can result in superficial ESG practices—commonly referred to as “greenwashing”—where companies adopt ESG labels without meaningful execution. This complicates efforts to accurately assess ESG outcomes and necessitates the use of refined methodologies that can adapt to local specificities [24]. In China, ESG initiatives have gained traction largely due to policy-driven signals from authorities, including guidelines on green finance and sustainability objectives embedded in national development plans. Regulatory support has played a central role in directing corporate ESG behavior, especially among state-owned enterprises. This top–down approach tends to foster a compliance-based ESG culture, as opposed to one driven by market mechanisms or active stakeholder involvement [25]. At the same time, market-oriented ESG developments are emerging. Stock exchanges in major cities have begun requiring listed companies to improve ESG disclosures. These regulatory efforts are complemented by the growth of ESG-themed investment products and indices, which offer incentives for firms demonstrating strong sustainability performance. Nonetheless, the evolving nature of these initiatives presents a dual challenge: aligning with international ESG standards while adapting to the complexities of domestic institutional settings [26]. In the context of China, political connections and regulatory pressure significantly shape ESG behavior [9]. Moreover, mandatory disclosure initiatives appear to catalyze green innovation [10], underscoring the instrumental role of national policy in ESG integration.

While ESG adoption in emerging markets has made notable progress, the challenges of symbolic compliance and “greenwashing” remain pronounced. In environments where disclosure mandates are weakly enforced or non-standardized, firms may adopt ESG labels without meaningful implementation. This misalignment between ESG disclosure and actual performance complicates reliable assessment and can mislead stakeholders. Recent research emphasizes the need for methodologies that are not only data-driven but also contextually adaptive—accounting for regulatory ambiguity, language variation, and cultural framing of ESG dimensions. For example, models should integrate localized ESG taxonomies, apply soft rule-based constraints for ambiguous disclosures, and incorporate semi-supervised techniques to handle partial or inconsistent data. Such methodological innovations are essential to ensure that ESG assessments in emerging markets reflect substantive engagement rather than performative reporting.

2.3. Long-Term Financial Impact Metrics

Assessing the long-term financial implications of Environmental, Social, and Governance (ESG) strategies requires the application of robust analytical frameworks and well-defined performance indicators [27]. While traditional financial metrics such as Return on Assets (ROA), Return on Equity (ROE), and Tobin’s Q are frequently used in ESG-related studies, evaluating long-term effects calls for dynamic modeling approaches that account for the delayed impact of ESG initiatives on financial outcomes [28]. A prominent approach involves the use of longitudinal panel data to examine how ESG engagement unfolds over time and accumulates influence on firm performance. Models such as fixed-effects and random-effects are commonly employed to isolate the effect of ESG from broader economic trends, company-specific traits, and sectoral dynamics. Some studies have also adopted quasi-experimental designs, such as difference-in-differences analysis, to investigate the sustained impact of ESG-related events on market valuation, highlighting the need for consistent and long-term ESG commitments [29]. In the Chinese context, research on long-term financial outcomes often integrates factors that reflect the local institutional setting, including the extent of government support, political affiliations, and the nature of firm ownership. Findings indicate that companies with sustained ESG strategies tend to perform better in terms of profitability and market valuation, especially when their practices align with national policy objectives [30]. This alignment may act as a positive signal to stakeholders and can lead to favorable access to state-backed resources. To address methodological challenges such as endogeneity, techniques like propensity score matching and structural equation modeling are increasingly utilized to establish more accurate causal relationships between ESG practices and financial performance. The adoption of machine learning tools has become more prevalent in ESG research, enabling the analysis of complex and large-scale datasets [31]. These advanced methods help uncover non-linear relationships and deeper interactions among ESG dimensions, firm behavior, and market dynamics, offering enhanced predictive capabilities for long-term financial performance. Addressing concerns of endogeneity and time-lagged effects, studies have employed fixed-effects, IV regression, and causal models to estimate ESG impacts more precisely [32]. These techniques help disentangle ESG effects from confounding variables. Xu et al. (2023) [22] reviewed how machine learning tools can complement traditional approaches by modeling nonlinear ESG–finance dynamics.

In addition to top–down regulatory guidance, bottom–up market mechanisms have increasingly shaped ESG practices in China. Institutional investors, ESG-themed funds, and third-party rating agencies are gaining influence, particularly among publicly traded private firms. Regional disparities are also evident: firms in economically developed zones such as the Yangtze River Delta and Pearl River Delta exhibit higher ESG disclosure scores and participation in international ESG indices compared to inland or resource-intensive regions. Furthermore, privately held firms in Shenzhen often respond more actively to ESG rating pressure, while state-owned enterprises in Beijing tend to align more closely with national policy signals.

3. Method

3.1. Overview

This section introduces a comprehensive framework for ESG (Environmental, Social, and Governance) management, developed to systematically integrate multifaceted sustainability considerations into strategic corporate decision-making processes. As contemporary enterprises increasingly recognize the critical impact of ESG factors on financial resilience, stakeholder engagement, and regulatory compliance, it becomes essential to formulate rigorous methodologies that embed ESG concerns into the core of strategic operations. The following subsections develop a structured pathway to understand, formalize, and advance a novel ESG-informed management paradigm.

Our methodological design integrates multiple machine learning techniques within a unified framework. The core model architecture is composed of a temporal encoder built upon a gated recurrent unit (GRU) to capture ESG signal sequences and a symbolic-structural module leveraging graph attention networks (GATs) to learn cross-factor dependencies. These modules feed into a Transformer-style decoder for policy prediction and ESG forecasting. The encoder–decoder pipeline is further enhanced by a dual-branch architecture that processes structured financial indicators and unstructured ESG textual content separately, fusing them at the latent representation stage. To ensure rigorous performance evaluation, the dataset is split chronologically using an 80/10/10 ratio for training, validation, and testing, ensuring no future data leaks into earlier training windows. Hyperparameters—such as learning rate, batch size, dropout, and number of attention heads—are optimized via grid search on the validation set, and early stopping is applied based on validation loss with a patience threshold of 10 epochs. All experiments are repeated three times with different random seeds to capture variability in training dynamics. Addressing data biases is crucial in ESG-related modeling. Sector imbalance is mitigated via stratified sampling to ensure equal representation across industries. In addition, ESG disclosure sparsity is handled by temporal imputation and partial masking strategies. Then, firm size bias is reduced through z-score normalization of financial indicators. To control for reporting frequency heterogeneity, we introduce frequency-aware positional encoding in the temporal encoder. These techniques jointly enhance the robustness and generalizability of our model across firms with diverse characteristics and disclosure behaviors. To capture industry-specific ESG dynamics, we incorporate sector-aware embeddings that allow the model to distinguish between disclosure norms and regulatory contexts across industries. These embeddings are learned jointly with firm-level temporal features in a GRU-based encoder and fused with graph-level structural priors derived from industrial linkage data. During training, models are validated using industry-stratified panel splits to ensure robustness of results across sectors such as energy, manufacturing, and services.

Section 3.2 introduces the foundational elements of ESG integration by formalizing the ESG strategy problem through a mathematical lens. We establish a rigorous symbolic structure that encapsulates the heterogeneity of ESG signals across firms, sectors, and temporal horizons. This symbolic formulation serves a dual purpose: To provide a clear problem definition that separates ESG assessment conventional financial evaluation and to offer a standardized representation space in which new optimization criteria and constraints are defined. We clarify key constructs such as ESG scoring tensors, time-variant disclosure matrices, regulatory compliance maps, and stakeholder-weighted utility functions. These constructs are synthesized into a unifying formulation that can be directly linked to strategic planning modules. Special attention is given to the challenge of ESG signal sparsity and inter-factor entanglement, both of which are formally modeled to expose the theoretical tension between ESG fidelity and operational tractability. Section 3.3 introduces a novel ESG modeling architecture—Strategic ESG Representation Generator (SERG)—which serves as the core of our proposed framework. Unlike traditional factor models or black-box ESG prediction pipelines, SERG is constructed with structural interpretability and domain adaptability at its center. It integrates temporal logic over ESG narratives with latent factor graphs extracted from both structured and unstructured data streams, such as annual reports, emissions disclosures, litigation risk indices, and human capital indicators. We detail how SERG encodes entity-specific ESG exposure through hybridized embeddings, including symbolic attention kernels, and semi-explicit policy-aware vector fields. The model architecture is designed to simultaneously track cross-factor diffusion and ESG-specific causality chains, allowing it to disentangle short-term ESG fluctuations from persistent thematic trends. This enables a principled decomposition of ESG risk into action-relevant, sector-specific representations that are deployable in both strategic forecasting and compliance alignment. Section 3.4 presents an advanced ESG optimization protocol, referred to as Adaptive Sustainability Policy Search (ASPS). This component constitutes a decision-theoretic framework that dynamically guides corporate actors through ESG-relevant choices under multi-objective constraints. Unlike classical portfolio optimization or CSR prioritization schemes, ASPS is built upon an evolving policy space that reflects changes in stakeholder preference distributions, regulatory regimes, and environmental baselines. The core algorithm employs a feedback-driven, model-based reinforcement schema that explores feasible sustainability transitions subject to cost–impact equilibria. The strategy optimization process is informed by the SERG outputs, which serve as policy conditionals, and it incorporates symbolic risk penalties derived from the ESG representation space. This endows ASPS with the ability to avoid overfitting to static ESG targets and to accommodate emerging sustainability narratives in a principled, mathematically sound manner.

Recognizing the potential barriers to adoption in resource-constrained or non-technical environments, we also propose a simplified variant of the framework for practical deployment. This variant removes the deep temporal components and instead leverages structured ESG scores and rule-based heuristics for risk estimation. It can be implemented in lightweight environments such as spreadsheet-based systems or low-code dashboards. In addition, the modular nature of our framework allows adaptation to different regulatory regimes and data granularities by replacing or bypassing symbolic reasoning modules and retraining on localized ESG taxonomies. We also provide guidelines on how the model may be scaled down or adjusted for industries with limited disclosure or differing ESG maturity levels. These design choices aim to balance model rigor with usability, expanding its relevance across both advanced and emerging market contexts. In response to the practical limitations associated with deploying a full symbolic ESG transition game model—particularly in resource-constrained environments—we provide a simplified configuration that removes the deep symbolic and dynamic game-theoretic modules. This version replaces temporal dynamics with rule-based heuristics and pre-aggregated ESG scores. It is designed for ease of deployment via spreadsheet tools or web dashboards, ensuring usability for organizations lacking advanced infrastructure. The model supports sector-specific configuration templates, enabling the prioritization of environmental, social, or governance components in accordance with industry-specific sustainability imperatives. To incorporate non-quantitative dimensions, we integrate reputational risk scores and sentiment analysis from external ESG news sources, which are embedded into the decision framework as soft symbolic constraints. These enhancements support interpretability and real-world alignment. Moreover, we provide mapping guides to align our symbolic variables with GRI and SASB frameworks, improving transparency and interoperability. To ensure robustness in environments with inconsistent ESG disclosures, the model applies probabilistic masking and harmonization techniques using third-party benchmark scores (e.g., Refinitiv, RepRisk), improving resilience to data gaps and enabling broader applicability across regulatory regimes.

3.2. Preliminaries

To rigorously investigate ESG management strategies, we begin by formalizing the ESG strategic integration problem into a symbolic and mathematically tractable structure. ESG decision-making, unlike traditional financial modeling, involves multiple non-commensurate objectives, dynamic stakeholder utility profiles, and intertemporal regulatory constraints. Hence, we introduce a symbolic foundation that captures these aspects through formal structures derived from multi-agent utility theory, constrained optimization, and structured semantic representations.

We let denote the set of environmental factors, the social indicators, and the governance criteria relevant to a given organization. We define the ESG signal tensor for an entity i over a time horizon T as

We define the stakeholder-weighted utility function for entity i, where

with encoding the weight of stakeholder group preference over factor j and a factor-specific transformation.

In practice, the weights are derived using a multi-criteria decision analysis (MCDA) framework, such as the Analytic Hierarchy Process (AHP), incorporating stakeholder input through ESG surveys. For example, environmental dimensions are prioritized in energy-intensive sectors, while governance is emphasized in financial services. These weights are normalized and sector-specific to reflect domain-relevant ESG priorities.

To encode regulatory constraints, we define a feasible ESG state manifold characterized by

where encodes multi-jurisdictional ESG compliance constraints.

The ESG strategy problem is then formalized as

where denotes a relevance-weighted Mahalanobis distance and controls alignment with benchmark expectations.

We define a symbolic ESG transition game among competing agents , where each entity’s ESG state influences others through shared resources, reputational contagion, and regulatory interdependence. This is captured via a dynamic game:

with denoting the policies of all agents except i and expectation taken over the joint ESG evolution process.

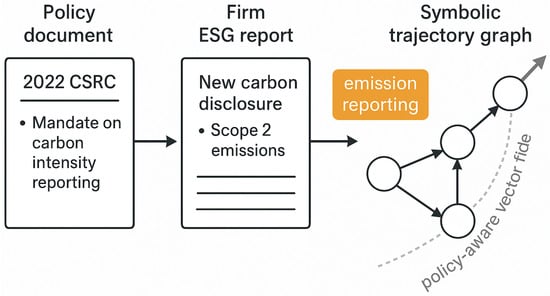

To further clarify the notion of a symbolic ESG transition game, we define it as a dynamic sequence of ESG-aligned behavioral changes that firms undertake in response to external regulatory or policy shifts. These transitions are symbolic in the sense that each action—such as disclosing carbon neutrality plans or improving board diversity—is mapped to a semantically labeled ESG strategy. For example, from a CSRC disclosure document issued in 2022 requiring mandatory carbon intensity reporting, a firm’s published ESG report may introduce a new section detailing Scope 2 emission metrics and renewable energy initiatives. This policy–action pair constitutes a symbolic ESG transition. Repeating this process across multiple firms and over time enables us to construct a symbolic trajectory graph, where each node represents a firm-time ESG state and edges reflect temporal transitions conditioned on external policy stimuli. A policy-aware vector field is then defined as a latent directional map within the ESG embedding space, where each vector encodes how policy-driven signals (e.g., carbon tax implementation, social labor law updates) guide ESG representations toward compliance-optimized zones. These vectors are parameterized based on historical firm adaptations, regulatory enforcement timelines, and sector norms. We provide a schematic overview of this construction pipeline in Figure 1.

Figure 1.

Constructing symbolic ESG transitions from policy and firm disclosures. The diagram illustrates how regulatory mandates (e.g., 2022 CSRC carbon intensity requirements) influence firm-level ESG reports. Policy actions are mapped into symbolic ESG behaviors, which are then structured as a temporal trajectory graph. The graph captures policy-conditioned ESG transitions and supports policy-aware vector field modeling.

To address real-world constraints, particularly in low-resource or data-scarce environments, we also introduce a simplified symbolic integration layer. This configuration relies on binary ESG compliance indicators or aggregated third-party ESG scores instead of dense ESG tensors. It enables firms with limited internal ESG tracking capacity to utilize the model using externally verifiable inputs. The stakeholder-weighted utility functions are customizable per sector, allowing environmental dimensions to be prioritized in energy-intensive industries, while governance factors dominate in sectors like finance or public administration. We also provide mapping templates aligning our symbolic indicators with GRI and SASB frameworks to ensure practical interoperability with existing ESG disclosure practices. The symbolic utility structure can incorporate qualitative elements such as sentiment scores or reputational indices derived from textual ESG narratives and news coverage. These can be modeled as external modifiers or embedded soft signals, enhancing the completeness and realism of ESG reasoning. We introduce relaxed constraint modeling strategies to accommodate inconsistent or missing ESG disclosures. These include probabilistic masking, imputation-based approximations, and penalized deviation formulations within the optimization problem.

3.3. Strategic ESG Representation Generator (SERG)

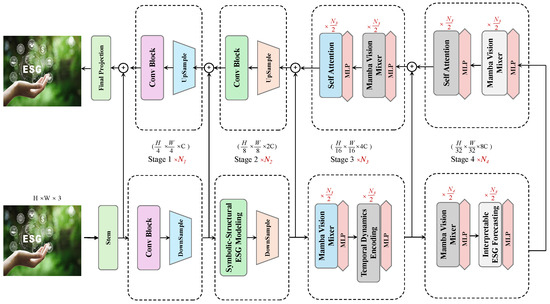

To effectively embed ESG factors into strategic-level decision-making, we propose a novel model architecture termed Strategic ESG Representation Generator (SERG). Unlike traditional ESG scoring systems or black-box predictive tools, SERG is a symbolic-structural representation model that captures heterogeneous ESG signals, inter-factor dependencies, policy dynamics, and stakeholder contextuality through a unified multi-layered architecture (as shown in Figure 2).

Figure 2.

Architecture of the Strategic ESG Representation Generator (SERG). The SERG model processes multi-modal ESG data through a dual-branch encoder. One path performs high-resolution spatial processing while the other incorporates symbolic-structural ESG modeling. The architecture features hierarchical convolution and attention-based modules that fuse temporal dynamics, contextual factors, and symbolic graph reasoning across four stages. The output integrates interpretability modules and MLPs to yield structured, temporally aware, and policy-aligned ESG representations for forecasting and decision-making.

Symbolic-Structural ESG Modeling

The objective of the Symbolic-Structural ESG Representation Generator (SERG) is to build a structured, interpretable, and temporally aware representation space for each entity i at time t defined as

where denotes the historical ESG signal sequences, is the sequence of ESG policy changes, encodes entity-level constraint sets (such as compliance requirements or sectoral rules), and represents external contextual embeddings, such as geopolitical shifts, industrial cycles, and climate indicators.

We first construct a dynamic ESG dependency graph , where nodes represent ESG dimensions, and edges in capture influence relationships among these factors. To capture high-order dynamic interactions, we define a bilinear attention-based adjacency matrix as

where is a learnable kernel and ⊗ denotes the outer product across ESG signal dimensions. The softmax operation normalizes the adjacency matrix to represent weighted dependencies among ESG nodes.

Based on this structure, we introduce a symbolic structure parsing module , which assigns semantic labels to edges in , such as regulatory causality, sectoral coupling, or climate cross-risk. To this end, we define a structural label tensor , where l is the number of symbolic relation types. It is constructed as

where can be implemented using logic rules, graph attention networks, or domain-specific reasoning frameworks to enhance the interpretability of causal and logical ESG structures. To enhance reproducibility and operational clarity, we provide a selection framework for implementing the symbolic parser . When domain-specific rules are well established (e.g., emission regulations in the energy sector), logic-rule-based parsing offers high interpretability with low computational demand. In contrast, graph attention networks (GATs) are more suited to data-rich contexts where ESG factor interactions are latent or temporal. In mixed scenarios, a hybrid implementation may combine logic filters followed by learnable attention refinement. We offer a configuration template for selecting among these modes based on data density, computational budget, and target industry.

Next, we define a state evolution encoder that integrates graph structure and external context to produce the final latent representation :

where and are the sequences of adjacency matrices and symbolic label tensors up to time t and may leverage graph sequence models combined with Transformer encoders to capture dynamic dependencies and context awareness.

We introduce a constraint-consistency evaluator , which assesses whether the latent state satisfies the entity-specific constraint set :

where is a learnable weight matrix, denotes the trace operator, and is a sigmoid function that outputs a soft consistency score in , providing a differentiable objective for alignment with constraints during training.

To address computational challenges associated with large-scale symbolic label tensors () and Transformer-based encoders in , we introduce sparsity-aware approximation strategies. These include label pruning based on mutual information thresholds, low-rank tensor decomposition for , and attention head pruning in long-sequence Transformer layers. These techniques reduce memory consumption and accelerate training, especially in real-time ESG monitoring or multi-year backtesting tasks. We formalize a taxonomy of symbolic ESG relations into four categories: (i) intra-domain coherence (e.g., E→E interdependence), (ii) cross-pillar amplification (e.g., E→S spillovers), (iii) risk propagation (e.g., climate cross-risk), and (iv) compliance chaining (e.g., governance→regulatory constraint). Each symbolic label is defined based on ESG reporting standards and stress-tested using synthetic ESG disclosures. The contextual embedding vector is constructed from three channels: (1) global economic indicators (e.g., IMF/WTO datasets), (2) industry-specific news sentiment from ESG newswire corpora (pre-trained on Refinitiv ESG news), and (3) climate risk exposure signals updated quarterly. Each context input is normalized and updated at a monthly to quarterly frequency, depending on the data stream. We plan to release standardized preprocessing scripts for replicability.

Temporal Dynamics Encoding

To effectively model the temporal evolution and abrupt transitions in ESG (Environmental, Social, and Governance) indicators, we employ a gated temporal encoder applied over the partially masked signal sequence . This encoder, based on a variant of the Gated Recurrent Unit (GRU), captures long-term dependencies while naturally accommodating missing values in the sequence.

We let denote the hidden state at time t for entity i. The update equations are defined as follows:

Here, is the reset gate that controls the degree to which the previous state is forgotten, and is the update gate that balances the incorporation of new information with historical memory. This design enables the model to capture long-range ESG trends and respond quickly to shocks such as policy shifts or market disruptions.

To further enhance contextual awareness, we introduce a cross-context attention mechanism that incorporates externalities—such as regulatory updates, geopolitical risks, and macroeconomic fluctuations—represented as symbolic context variables. We let denote a set of contextual indicators associated with entity i at time t. These are projected into a latent context space and aggregated using attention weights:

In this formulation, is a nonlinear transformation into the latent context space, and denotes the inner product measuring relevance between the hidden state and context vector. The attention weights determine the influence of each external factor. The resulting context vector is concatenated with to yield an enriched temporal representation, serving as input for downstream tasks such as ESG scoring, trend prediction, or anomaly detection. To handle missing values in ESG time series , we introduce a binary mask matrix , where indicates missing feature j at time t. The GRU is modified to skip updates for missing positions by gating them out using . We apply forward-fill and temporal mean imputation for partially missing dimensions to preserve trend continuity. This dual masking-imputation approach enables robust learning on real-world ESG datasets with 10–30% sparsity. The contextual inputs are structured into a three-channel ontology: (i) geopolitical indicators (e.g., sanctions, elections), (ii) regulatory changes (e.g., disclosure mandates, green policy), and (iii) macro-climatic trends (e.g., emission targets). These are sourced from Refinitiv news corpora, IMF datasets, regional ESG policy trackers, and updated quarterly. Each context signal is encoded by a contextual vector transformation implemented as a two-layer MLP with ReLU and dropout, pretrained on ESG news tagging tasks to preserve semantic structure. For interpretability, attention maps over are visualized and validated against known ESG events (e.g., 2022 EU Taxonomy implementation). Attention weights are normalized using softmax across all context dimensions, and regularized using entropy-based sparsity loss to prevent overfitting to dominant signals. We also introduce dropout (p = 0.2) in the dot-product layer to enhance generalization under noisy inputs.

Interpretable ESG Forecasting

To enable interpretable forecasting of ESG signals, we construct a representation that fuses structural, temporal, and contextual information for each entity i at time t:

where is a temporal feature derived via Transformer-based encoding, encodes structural relations from a heterogeneous graph, and denotes contextual inputs such as regulatory or industry conditions. The operator vectorizes the matrix, and is a multi-layer perceptron with skip-connections (as shown in Figure 3).

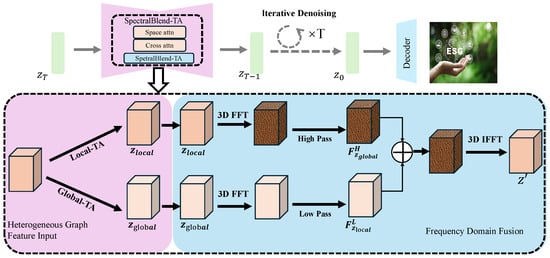

Figure 3.

Schematic diagram of Interpretable ESG Forecasting. The framework begins with heterogeneous graph inputs, processed via Local and Global Token-Aware modules. Features are transformed to the frequency domain using 3D FFT, split into high- and low-frequency components, fused, and reconstructed via 3D IFFT. An iterative SpectralBlend-TA module with space and cross-attention refines representations, which are decoded into ESG predictions. Supervised contrastive learning aligns embeddings with ESG taxonomies, enabling interpretability through human-understandable metafeatures.

To semantically constrain the embedding , we employ supervised contrastive learning guided by domain-specific ESG taxonomies , each representing a well-defined ESG concept. The contrastive loss function is defined as

where denotes cosine similarity, is the temperature parameter, and is the positive anchor aligned with sample i.

To support downstream applications such as ESG trajectory forecasting or risk of compliance violation, we integrate a prediction module that takes as input to estimate future ESG signals. We let be the prediction for horizon ; then, the forecasting loss is

where is the observed ESG signal at time .

The overall training objective balances forecasting accuracy, semantic alignment, and model regularization:

with as scalar weights and denoting regularization over trainable parameters .

To ensure interpretability, SERG enforces symbolic decomposability of the embedding . Each dimension corresponds to a human-interpretable ESG metafeature such as environmental trajectory or governance shock:

Each metafeature is either directly computed by symbolic rules or traced back via gradient attribution to the input features and external priors , enabling transparent ESG decision-making and regulatory auditing.

To enhance the accessibility and scalability of SERG across different organizational capacities, we introduce a lightweight variant of the model that omits the graph-based attention mechanism. In this configuration, structured ESG indicators and basic correlation matrices are used as substitutes for the dynamic ESG dependency graph, making the framework deployable in spreadsheet or dashboard environments without loss of core functionality. We propose that the full-featured SERG architecture be embedded into a user-facing interface, such as a web-based dashboard or an Excel-based toolkit, enabling non-technical users to upload ESG disclosures and receive interpretable outputs including predicted financial impacts and policy suggestions. To better model real-world uncertainty and stakeholder volatility, we allow the SERG structure to incorporate sentiment signals, news-derived controversy flags, and soft symbolic indicators derived via NLP. These optional inputs expand the symbolic-semantic coverage to reflect the more subjective dimensions of ESG performance. In terms of forecasting, SERG integrates a temporal forecasting head which can be instantiated using either GRU-based regressors or probabilistic scenario-based simulation models. These methods are particularly valuable in fast-changing industries such as tech or green energy, where past ESG signals may not adequately predict future risk dynamics. To ensure adaptability across diverse regulatory environments, we support region-aware constraint modules that adjust ESG compliance targets, risk penalization, and disclosure weighting according to local governance codes (e.g., CSRC for China, SEBI for India, SEC for the US). A configuration file or region-specific template can be used to tune the model accordingly.

To formalize strategic ESG decision-making, we define the optimization as a Stackelberg game, where the firm acts as the leader and market regulators or investors act as followers. The firm selects a policy trajectory anticipating possible reactions from the environment. The reward function integrates ESG utility and regulatory feedback:

where encodes the response dynamics of external stakeholders. The equilibrium strategy is approximated via iterative best response under policy-conditioned reinforcement learning.

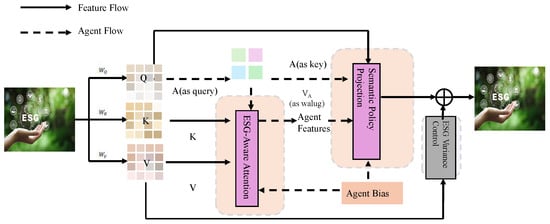

3.4. Adaptive Sustainability Policy Search (ASPS)

Building upon the structured ESG representation provided by SERG, we now introduce a novel policy search framework termed Adaptive Sustainability Policy Search (ASPS). This strategy module is designed to optimize ESG-related decisions in a dynamic, feedback-sensitive environment, incorporating multi-objective constraints, evolving stakeholder expectations and regulatory shifts (as shown in Figure 4).

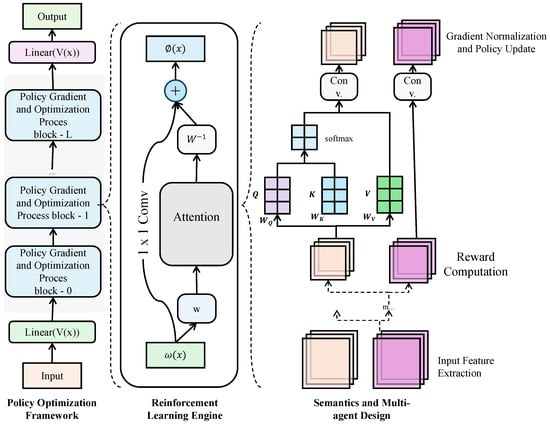

Figure 4.

Overview of the Adaptive Sustainability Policy Search (ASPS) system. The architecture integrates structured ESG inputs with policy optimization via stacked gradient blocks. A central reinforcement learning engine uses attention and stakeholder feedback to adapt policies dynamically. Semantic and multi-agent modules apply symbolic ESG constraints and coordinate policy updates, ensuring interpretability and alignment with long-term sustainability goals.

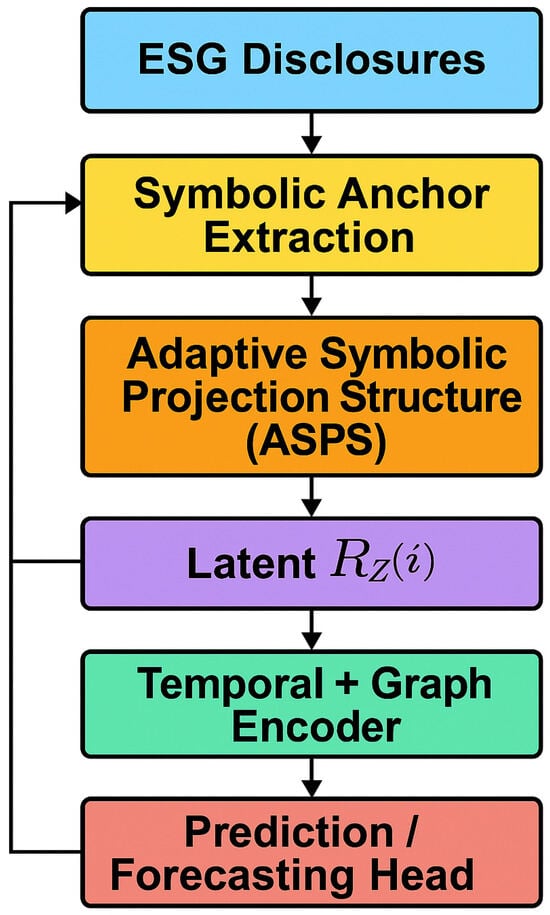

To address limitations of conventional MLP or Transformer architectures—which typically operate on homogeneous vector inputs and lack symbolic interpretability—we propose an Adaptive Symbolic Projection Structure (ASPS). This module explicitly incorporates symbolic ESG constructs into the learning process by projecting high-dimensional textual and numeric ESG features into a structured latent space guided by policy-driven priors. Unlike standard MLPs that perform dense transformations over concatenated features, ASPS first encodes symbolic meta-concepts (e.g., emission compliance, board independence) as projection anchors in the latent space. ESG input data are then adaptively aligned to these anchors via a policy-aware attention mechanism, enabling semantically interpretable dimensions. This mechanism resembles attention but is constrained by domain-specific symbolic priors instead of being purely data-driven. In contrast to Transformer models, which excel at sequence encoding but often obscure feature semantics, ASPS enforces symbolic alignment at each projection layer and dynamically adjusts projection weights based on external policy conditions. The result is a hybrid latent representation that preserves symbolic traceability while enabling downstream neural computation. We provide a flowchart of the full modeling pipeline in Figure 5, illustrating how ESG data, symbolic anchors, policy priors, and prediction targets are processed through the ASPS and subsequent modules.

Figure 5.

Overview of the end-to-end modeling pipeline. The pipeline begins with ESG disclosures, followed by symbolic anchor extraction and adaptive symbolic projection through ASPS. Latent representations are encoded via temporal and graph modules before final prediction. Color-coded modules distinguish each processing stage.

Policy Optimization Framework

The Adaptive Sustainable Policy Search (ASPS) framework is designed to learn an optimal policy trajectory for each entity i, dynamically responding to evolving ESG structural representations generated by the Structural Embedding for Responsible Governance (SERG) module. Each policy aims to strategically balance long-term utility gains against ESG-specific costs while adhering to sectoral benchmarks and risk constraints.

We let denote the admissible ESG action space, encompassing quantifiable decisions such as capital reallocation to sustainable initiatives, workforce well-being programs, or regulatory compliance reforms. At every timestep t, the policy maps an entity’s structural ESG state to an action:

At each time step t, the model observes the ESG state of firm i and outputs a policy action , such as increasing renewable investments or improving governance structure. The action space includes all feasible ESG actions aligned with industry and regulatory constraints.

The transition dynamics of the structural state are modeled as a stochastic process governed by a policy-conditioned evolution function , influenced by exogenous uncertainty :

where is assumed to be Markovian and smooth, encoding structural dependencies such as regulatory lags or environmental inertia. The ESG state of a firm evolves over time based on its current status, the chosen ESG policy action, and random external factors like market shocks or regulatory changes.

The objective is to maximize the discounted cumulative ESG-aligned utility, accounting for both direct stakeholder impact and regulatory or resource penalties. The utility function reflects a time- and entity-specific aggregation of stakeholder preferences, while quantifies ESG-relevant cost terms. Formally,

with denoting a temporal discount factor and a scalar controlling the utility–cost trade-off. This equation represents the long-term net benefit for firm i, balancing ESG utility (e.g., improved reputation or resilience) with the cost of ESG actions (e.g., investment expenses). The discount factor reflects time preference, and controls how much penalty is placed on cost.

To incorporate external compliance or sectoral alignment, we impose a benchmark guidance term using a reference trajectory , which may represent an idealized ESG evolution path defined by policy standards, industry consensus, or decarbonization targets. The divergence penalty is structured as

where is a diagonal importance-weighting matrix reflecting differential emphasis across ESG dimensions. This term penalizes deviation from ideal ESG trajectories (such as decarbonization goals), helping firms align with external ESG benchmarks or policy guidelines.

Risk management is integrated through a volatility-aware constraint. ESG state uncertainty is quantified via the empirical covariance matrix of , with total variance captured by its trace:

This metric captures the uncertainty in a firm’s ESG profile over time. High variance may indicate unstable or inconsistent ESG behavior, which could pose risks to investors or regulators.

To ensure robustness under ESG uncertainty, we enforce a variance ceiling:

where is a domain-dependent hyperparameter informed by regulatory thresholds, social sensitivity, or investment risk profiles. This constraint encourages policy stability and protects against excessive fluctuation in ESG trajectories.

Reinforcement Learning Engine

We implement a model-based reinforcement learning (MBRL) framework that incorporates dynamic stakeholder preferences through a utility-weighted value function. The agent operates in a partially observable environment, with latent state inferred from observations, and adapts its policy through iterative value updates. At each time step t, the agent selects action based on a soft or greedy policy derived from the state-action value function .

The state-action value function is defined as

where is the stakeholder-specific utility function, is a penalty scaling factor, is the action cost, is the discount factor, and is the next latent state under transition dynamics . This value represents the total expected benefit of taking action a from ESG state , considering both immediate utility and future gains. It serves as the basis for ESG policy evaluation.

The value function is obtained by maximizing over the action space:

This forms the basis for value iteration and policy improvement. Given the updated , the policy is revised using

This policy update reflects rational action selection aimed at maximizing the expected cumulative utility while accounting for action costs and temporal preferences.

To account for evolving preferences, we introduce a dynamic stakeholder modeling mechanism. Each stakeholder i maintains a preference weight vector , which governs the shape and slope of the utility function. This vector evolves in time based on observed feedback and environmental responses. The update rule for is given by

where is the adaptation rate and is the feedback-induced gradient of preference change, obtained from direct feedback or implicit behavioral signals.

The updated preferences are integrated into the utility gradient that shapes the Q-function. The stakeholder-aware utility can be expressed as

where denotes a feature representation of the latent state and the inner product with reflects the current stakeholder valuation. This allows the system to respond to changes in stakeholder importance over time and align action selection with nuanced, evolving utility landscapes.

Semantics and Multi-agent Design

To ensure that learned policies remain interpretable, verifiable, and robustly aligned with Environmental, Social, and Governance (ESG) objectives, the Adaptive Symbolic Policy System (ASPS) integrates semantic constraints grounded in symbolic taxonomies . Each corresponds to a directional anchor in a structured ESG semantic space. These anchors guide the policy’s gradient evolution by penalizing deviations from established semantic directions (as shown in Figure 6).

where denotes the ESG-aligned latent state of agent i at time t and is the corresponding policy action. This term penalizes policy updates that violate known ESG causal semantics, ensuring that the learning process remains tethered to expert-validated priorities. This term ensures that ESG actions stay aligned with expert-defined semantic directions, such as reducing emissions or improving diversity, based on the ESG taxonomy .

Figure 6.

Semantics and Multi-agent ESG Policy Framework. This figure illustrates a multi-agent attention-based architecture for ESG policy optimization with symbolic semantic constraints.

In environments with multiple interacting stakeholders or entities—such as firms, government regulators, and civil society actors—ASPS operates as a multi-agent policy optimization framework. Each agent i maintains its own policy , interacting with others in a game-theoretic structure. The optimization objective for agent i becomes

where denotes the fixed strategies of all other agents and is a utility function incorporating both ESG impact and agent-specific preferences. The system’s ESG evolution is influenced by both intra-agent policy and inter-agent dynamics, leading to coupled transitions of the form

where models the internal ESG transition dynamics of agent i and encodes how ESG shifts in agent j impact agent i. This formulation captures ESG externalities in decentralized systems. In multi-agent settings, the ESG outcome of one agent (firm or stakeholder) is affected not only by its own policy but also by the behavior of others, capturing ESG externalities like shared environmental resources.

The weights , , and in the overall training loss are selected via grid search on the validation set. We evaluate their sensitivity across values from 0.1 to 1.0 with step size 0.1. balances forecasting accuracy, enforces semantic alignment through contrastive learning, and controls regularization. The best setting found is , , and based on validation MAE and embedding quality.

To robustly optimize policies under these settings, the full ASPS loss function aggregates multi-objective trade-offs:

where is the cumulative utility for agent i, regularizes policy deviation from established ESG baselines or historical benchmarks, and the final term penalizes excessive volatility in ESG state transitions (with threshold ). This encourages policies that are not only goal-aligned but also stable and realistic in dynamic operational environments. The total loss combines long-term ESG benefit (negative ) with penalties for deviating from policy benchmarks, violating semantic expectations, or exhibiting unstable ESG patterns.

To support strategic foresight, ASPS integrates with SERG (Symbolic ESG Representation Generator), which models the high-level causal structure of ESG indicators across time and agents. Given SERG-generated latent states , ASPS outputs adaptive, context-sensitive policy actions that are optimized not only for immediate utility but also for long-term structural ESG integrity.

For enhanced expressivity in institutional modeling, we extend the semantic constraint term using dynamic weights over taxonomy anchors:

where are temporal attention weights reflecting changing ESG priorities. These weights can be learned from external events, stakeholder salience models, or policy agendas, allowing the system to dynamically reorient toward emergent ESG hotspots without manual intervention.

The methodological framework introduced in this section integrates symbolic modeling, temporal dynamics, and reinforcement learning to form a unified ESG–financial analysis pipeline. The first core module, Strategic ESG Representation Generator (SERG), constructs interpretable and temporally aware representations by combining structured ESG signals with semantic graph modeling and attention-based feature extraction. This enables the model to capture the complex, dynamic, and cross-factor interactions among ESG indicators in a domain-specific context. Adaptive Sustainability Policy Search (ASPS) builds upon these representations to guide corporate decision-making through reinforcement learning. ASPS dynamically optimizes ESG-related actions under multi-objective constraints—balancing long-term financial performance, compliance stability, and stakeholder preferences. It incorporates semantic constraints and ESG variance control mechanisms to ensure policy interpretability, robustness, and alignment with strategic ESG objectives. Together, SERG and ASPS form a unified and end-to-end framework for modeling, forecasting, and optimizing ESG strategies, tailored to the structural and regulatory characteristics of China’s evolving capital market. The proposed framework not only addresses the technical challenges of ESG data heterogeneity and policy alignment but also provides practical tools for institutional investors and regulators seeking to operationalize ESG principles in long-term financial planning.

The decoder function maps the ESG latent representation to the forecasted target (e.g., ROA, ESG rating). We implement g as a three-layer fully connected neural network with ReLU activation and dropout (rate = 0.2). The output is either a continuous regression value or classification label depending on the prediction task.

The constraint matrix C introduced in Section 3.2 is constructed based on real-world ESG compliance regulations. Examples include:

- -

- Energy Sector (China): emissions must not exceed annual reduction targets as per the “Dual Carbon” policy (encoded as ).

- -

- Finance Sector (EU): Firms must disclose ESG-aligned asset ratios under the SFDR framework, represented as a minimum bound on ESG reporting completeness.

- -

- Manufacturing Sector (Global): Waste treatment compliance under ISO 14001 is represented by bounded environmental risk scores.

These regulatory limits are translated into linear constraints of the form .

The SERG and ASPS modules are co-trained in an end-to-end learning framework. ASPS serves as the symbolic alignment and feature projection layer within the SERG architecture. The latent ESG representations generated by ASPS are directly passed to SERG’s temporal encoder, enabling consistent symbolic grounding throughout the modeling pipeline. We avoid separate pre-training of ASPS to ensure that projection weights adapt to downstream supervision signals, such as forecasting losses and taxonomy alignment. All parameters are updated jointly via backpropagation, allowing the symbolic projection structure to remain sensitive to end-task objectives.

To improve reproducibility and transparency, we summarize the key hyperparameters and training settings in Table 2. We performed a grid search over loss weight coefficients using a 10 × 10 grid. Other parameters such as embedding size, learning rate, and batch size were selected based on prior benchmarks. We reserved 20% of the training data for validation and adopted early stopping with a patience of 10 epochs to avoid overfitting. Cross-validation was not used due to computational cost, but results were consistent across 3 random seeds.

Table 2.

Model Training Configuration and Hyperparameters.

4. Experimental Setup

4.1. Dataset

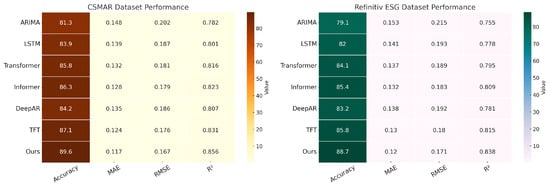

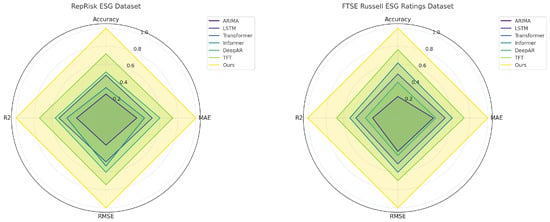

The CSMAR Dataset [33] is a comprehensive financial database widely used in Chinese capital market research. It contains a rich collection of firm-level accounting, stock market, and corporate governance data for Chinese listed firms. The dataset is structured similarly to the CRSP and Compustat datasets and is updated regularly, making it suitable for both cross-sectional and panel data analyses. For Environmental, Social, and Governance (ESG)-related research, CSMAR offers detailed information such as board structure, executive compensation, and ownership concentration, which can serve as critical indicators for corporate governance assessment. Its coverage includes thousands of firms across various industries, offering both historical depth and data consistency, thereby enabling robust empirical studies on corporate behavior in China. The Refinitiv ESG Dataset [34] provides standardized ESG scores and detailed indicators for global firms, making it a vital source for international comparative ESG research. It covers over 10 companies and includes more than 400 ESG metrics, ranging from carbon emissions and resource use to diversity and community involvement. Refinitiv employs a transparent methodology by collecting publicly available information from company reports, news sources, and NGO datasets. Each company receives three pillar scores—Environmental, Social, and Governance—and an overall ESG combined score. This dataset is particularly valuable for machine learning applications due to its scale and feature diversity. Refinitiv assigns controversies scores, which capture significant ESG-related negative incidents, enhancing the temporal dynamics of ESG risk assessments. The RepRisk ESG Dataset [35] is uniquely positioned as a risk-focused dataset built upon daily data collection and artificial intelligence techniques. It captures ESG risks by analyzing media, stakeholder, and third-party sources in 20 languages, covering over 200,000 public and private companies worldwide. RepRisk emphasizes ESG-related controversies such as corruption, labor violations, and environmental damage, making it highly suitable for real-time risk monitoring and reputational analysis. Unlike traditional ESG ratings, RepRisk does not rely on self-disclosures but instead focuses on external perspectives, offering an alternative angle to ESG assessment. The data are updated daily and a RepRisk Index (RRI) is assigned to reflect a firm’s current ESG risk exposure, facilitating dynamic integration into financial models. The FTSE Russell ESG Ratings Dataset [36] provides a multidimensional view of ESG performance through industry-specific criteria and weighted ESG factors. It covers over 7200 securities across 47 countries, with each firm evaluated based on over 300 indicators. The dataset’s structure reflects the materiality of ESG issues within each industry, ensuring the comparability of ratings across sectors. FTSE Russell implements a hierarchical framework, aggregating data from indicator to theme and to pillar level, culminating in a composite ESG score. A unique feature of this dataset is its integration with financial indexes, making it popular among institutional investors. Furthermore, the ratings are aligned with international frameworks such as SASB and TCFD, supporting regulatory compliance and sustainable investment strategies.

We conduct independent training and evaluation for each dataset to avoid distributional bias. No multi-source data fusion is performed. However, we experiment with transfer learning by pretraining on CSMAR and finetuning on RepRisk to assess cross-market generalization. We utilize four major ESG data sources—CSMAR, Refinitiv ESG, RepRisk, and FTSE Russell—to construct a comprehensive multi-source ESG dataset tailored to Chinese publicly listed firms. Each source provides a unique emphasis across the ESG dimensions: CSMAR focuses on structured corporate disclosures and regulatory filings in China, with a strong emphasis on Governance (G) and Social (S) indicators, such as board structure, audit transparency, and employee welfare. Refinitiv ESG provides globally standardized ESG scores derived from company reports and media analytics, offering balanced coverage across all three dimensions but with relatively deeper Environmental (E) granularity (e.g., carbon emissions, energy intensity). RepRisk is a controversy- and sentiment-focused source, emphasizing negative ESG events such as labor violations or environmental accidents, particularly strong on Social (S) risk tracking and governance failures. FTSE Russell offers ESG factor exposure scores used in ESG index construction, with a structured taxonomy and a strong emphasis on Environmental (E) and Governance (G) compliance benchmarks. While some overlap exists—particularly on board-level governance indicators and carbon-related disclosures—we treat these signals as complementary. Where duplicate variables arise, we retain the version with higher time resolution and fewer missing values. For example, we prioritize Refinitiv’s emission data due to its quarterly frequency. Before feeding data into the model, we apply the following preprocessing steps: Imputation: Missing values within ESG time series are imputed using forward-fill and time-windowed mean substitution. Normalization: All continuous features are normalized via z-score scaling within each source, while binary flags (e.g., violation reported) are preserved. Alignment: Time-series data from different sources are synchronized to quarterly resolution using backward padding and temporal interpolation where needed. Dimensionality Matching: All ESG indicators are mapped into a shared latent taxonomy to enable joint encoding in the SERG module. This preprocessing pipeline ensures that multi-source ESG data can be jointly embedded and interpreted with minimal bias from data sparsity or source discrepancies (Table 3).

Table 3.

Summary Statistics of the ESG Datasets Used.

The CSMAR dataset utilized in this study encompasses firm-level data for over 3200 publicly listed companies, accounting for approximately 85% of the total A-share market in China, both in terms of market capitalization and industry distribution. This extensive coverage ensures that the dataset captures a representative cross-section of China’s diverse capital market landscape, including state-owned enterprises, private sector leaders, and emerging industry players. The dataset spans the period from 2010 to 2022, providing 13 years of longitudinal data. All financial indicators used in the analysis, including Return on Assets (ROA) and Tobin’s Q, are sampled at a quarterly frequency. ESG indicators are also updated quarterly, based on company disclosures, industry reports, and third-party ESG databases. To ensure temporal coherence and mitigate reverse causality, we implement a one-year lag between ESG inputs and financial performance outcomes. ESG disclosures from fiscal year t are aligned with financial metrics in fiscal year t + 1. This alignment assumes that ESG strategies require a minimum lead time before materially influencing financial outcomes, a practice aligned with established ESG–finance literature. The one-year lag also helps reduce simultaneity bias, allowing for more credible inference about directional relationships between ESG strategy and long-term performance. When constructing machine learning features, we ensure that no future financial data leak into the ESG prediction horizon, adhering strictly to out-of-sample validation principles. The data’s granularity, temporal span, and breadth of firm coverage make them both statistically robust and practically relevant for modeling ESG–financial interactions in the Chinese context. We revise Section 4.1 accordingly to include these clarifications and ensure transparency in data usage and alignment strategy.

4.2. Experimental Details

In our experiments, we implement the proposed model using PyTorch 1.13 and conduct training on NVIDIA A100 GPUs with 80 GB memory. All models are trained using the AdamW optimizer with an initial learning rate of 1 × and weight decay of 0.01. A cosine annealing learning rate scheduler is applied with a warm-up ratio of 0.1. Batch size is set to 64 for all experiments, and we train each model for 100 epochs. Gradient clipping is applied at a maximum norm of 1.0 to ensure stable training dynamics. For fairness and reproducibility, all experiments are repeated three times with different random seeds, and the average performance is reported. Input features for each company include both numerical and categorical data, covering financial indicators, ESG scores, and text-based sentiment features. Numerical features are normalized using z-score standardization, while categorical variables are embedded using learnable embedding layers. Missing data are handled through median imputation for continuous variables and mode imputation for categorical ones. ESG scores from Refinitiv, RepRisk, and FTSE Russell are aligned temporally and structurally across datasets to ensure consistency. We employ early stopping with a patience of 10 epochs based on validation loss to avoid overfitting. For comparison, we use several baseline models, including Random Forest and XGBoost, as well as neural architectures such as MLP and GAT. LSTM is employed as a baseline for capturing temporal dependencies, and Transformer is used as a comparative model for attention-based mechanisms. Both of these models are adapted to our temporal feature encoding (TFE) and attention-guided ESG risk assessment framework, respectively. For deep models, we use a hidden dimension of 256 and a dropout rate of 0.2, and we apply batch normalization. For graph-based experiments using GAT, we construct firm-level graphs based on industry and supply chain linkages. Each node represents a firm, and edges are defined by either same-industry relationships or significant transactional exposure. We use two GAT layers with 8 attention heads each, followed by a global mean pooling layer before classification. The model is trained with a binary cross-entropy loss when predicting binary ESG risk labels, and with mean squared error loss for continuous ESG score regression tasks. Evaluation metrics include accuracy, F1 score, AUC-ROC, and mean absolute error (MAE), depending on the task type. For classification tasks such as ESG controversy prediction, we emphasize AUC and F1 as primary metrics. For regression tasks, we use MAE and R-squared. Hyperparameter tuning is conducted via grid search on the validation set, optimizing the main evaluation metric for each task. We also apply SHAP analysis to interpret the model’s feature importance and contribution patterns, providing insights into which variables most influence predictions. The experimental pipeline is fully automated via configuration files for reproducibility. All datasets are split chronologically with an 80/10/10 ratio for training, validation, and test sets to reflect realistic financial forecasting scenarios. No future data leaks are allowed into the training window. To assess model robustness, we introduce a temporal shift test by evaluating the models on data from different fiscal years and perform stress testing by introducing synthetic ESG shocks. All code and configuration files will be released upon publication to ensure full transparency and facilitate reproducibility.