An Empirical Approach to Integrating Climate Reputational Risk in Long-Term Scenario Analysis

Abstract

1. Introduction

2. Econometric Methodology and Data Description

2.1. A Threshold Regression Approach to Model Climate Reputational Risk

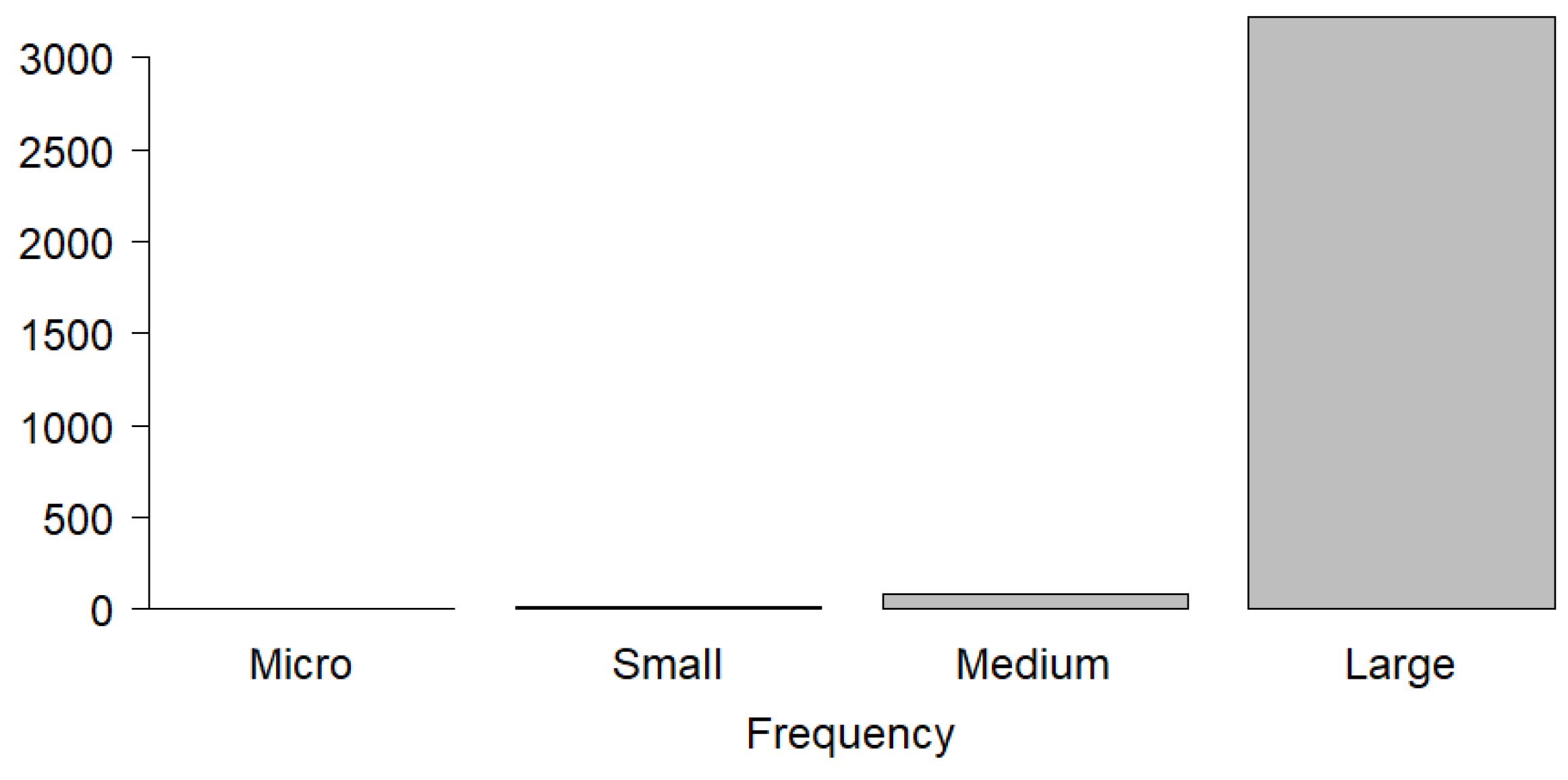

- Micro, with ≤10 employees

- Small, with <50 employees

- Medium, with <250 employees

- Large, with ≥250 employees.

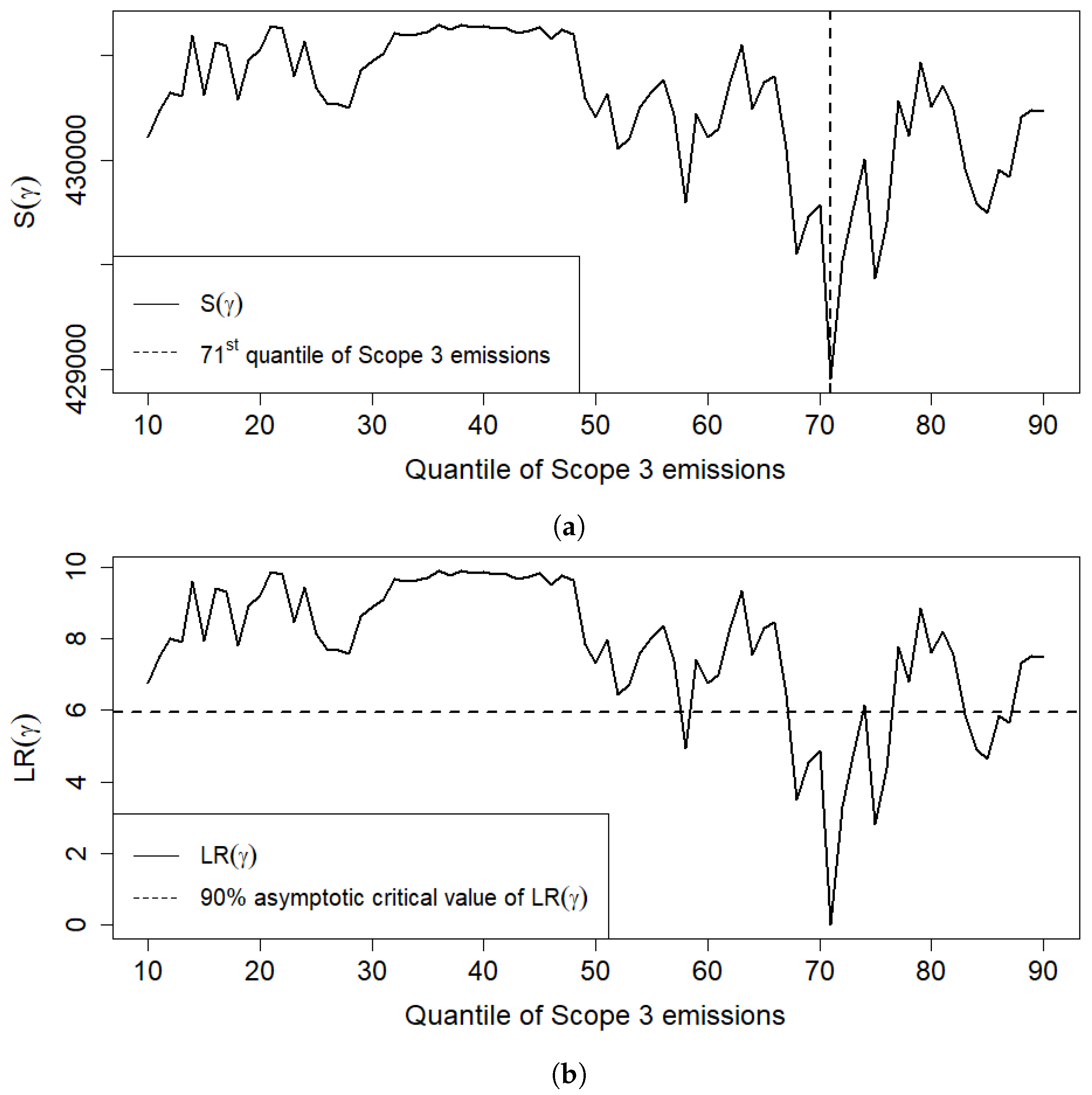

- Consider a grid of values for which spans most of the range of Scope 3 emissions’ observations. These values can therefore be equally spaced between the 10th and 90th quantiles of .

- For a gridvalue of , Equation (1) becomes linear and its coefficients can be estimated by POLS. The corresponding concentrated sum of squared residuals , which is a measure of fit, can be calculated.

- Step 2 is repeated for all grid values of . The NLLS estimator is the gridvalue of minimizing , and hence yielding the best fit of model (1).

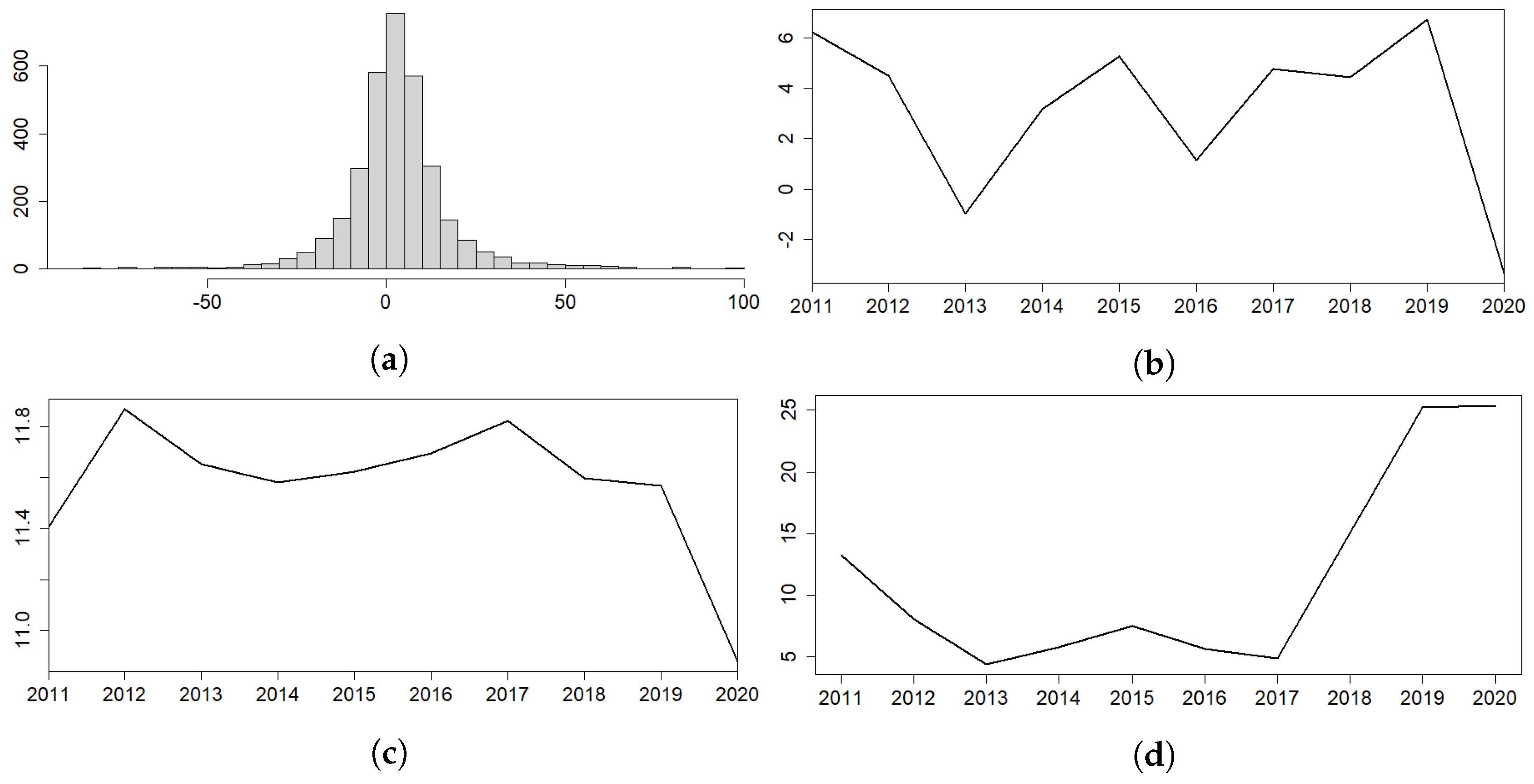

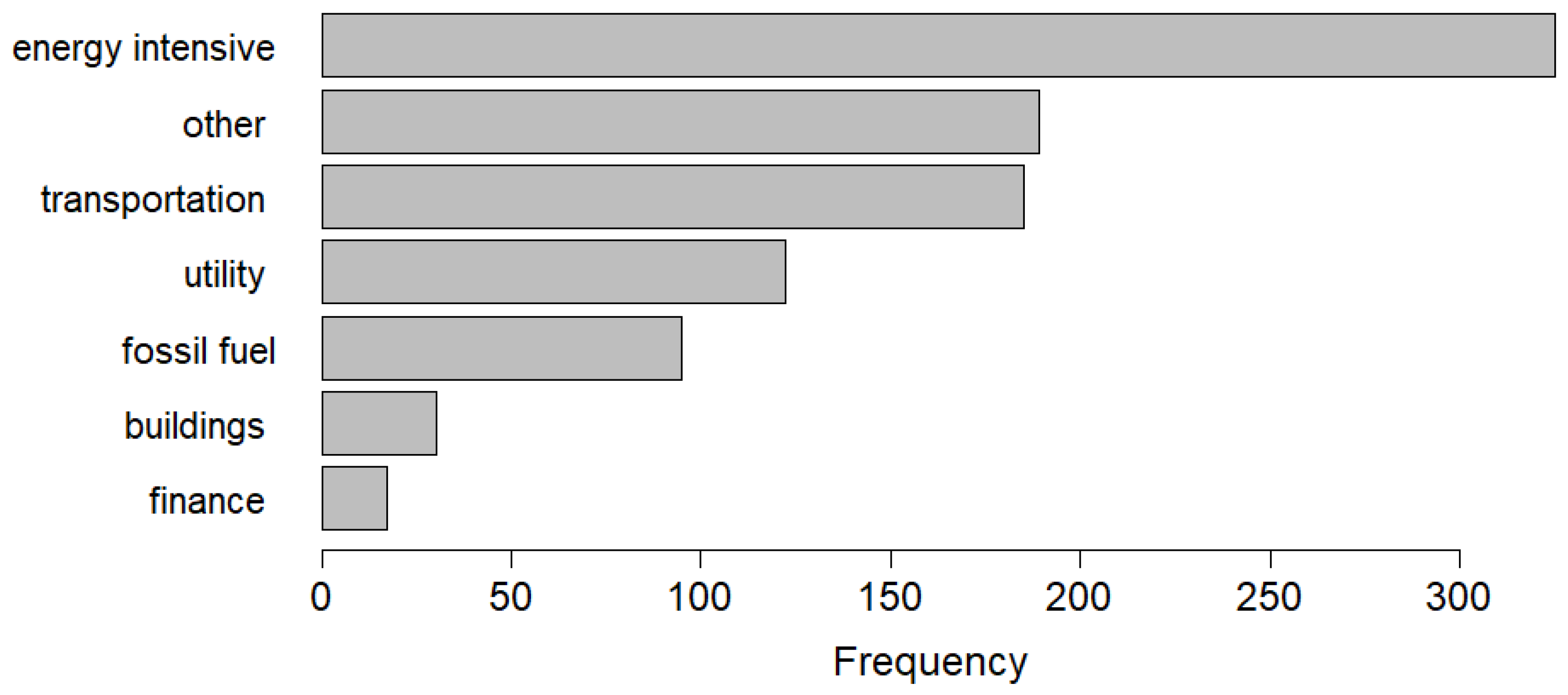

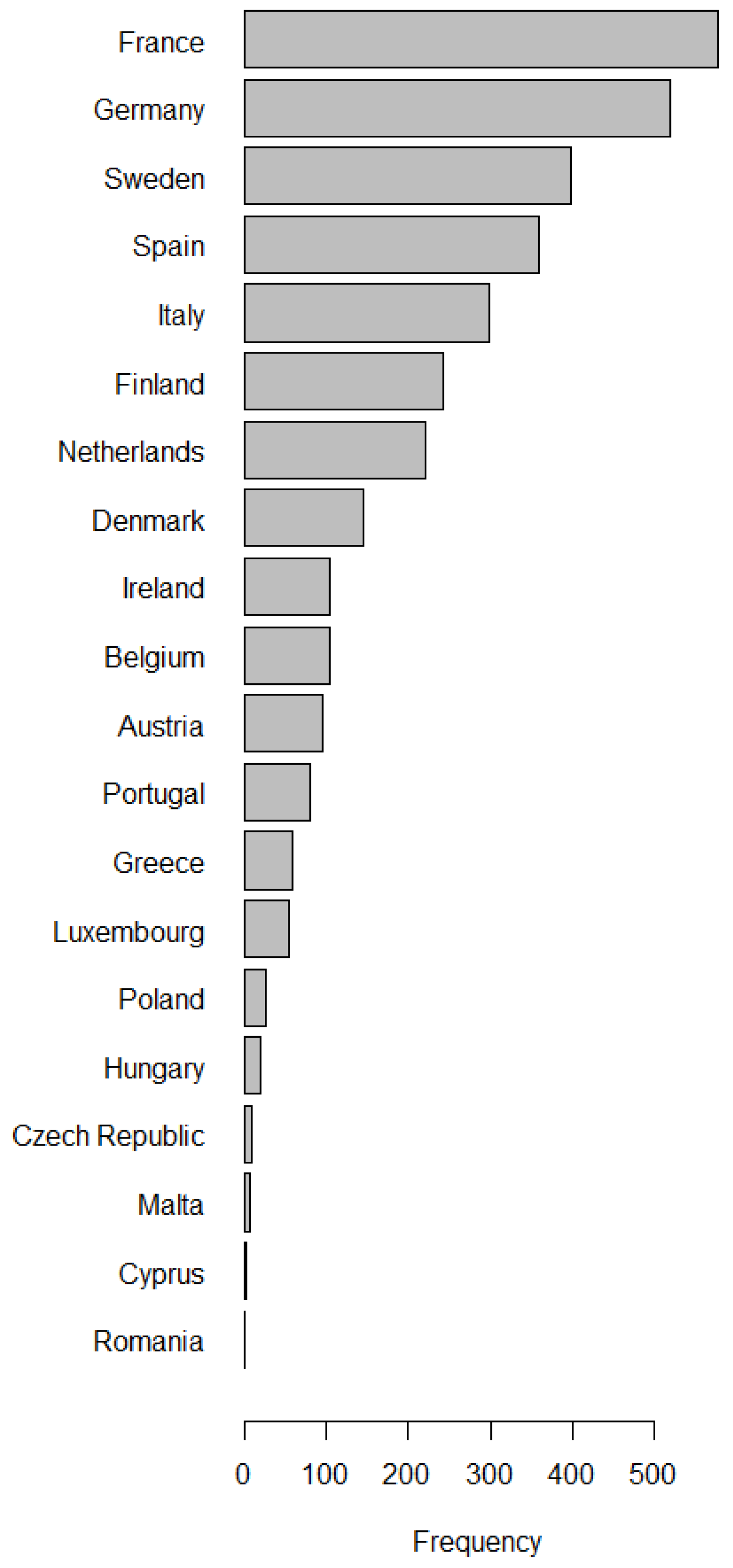

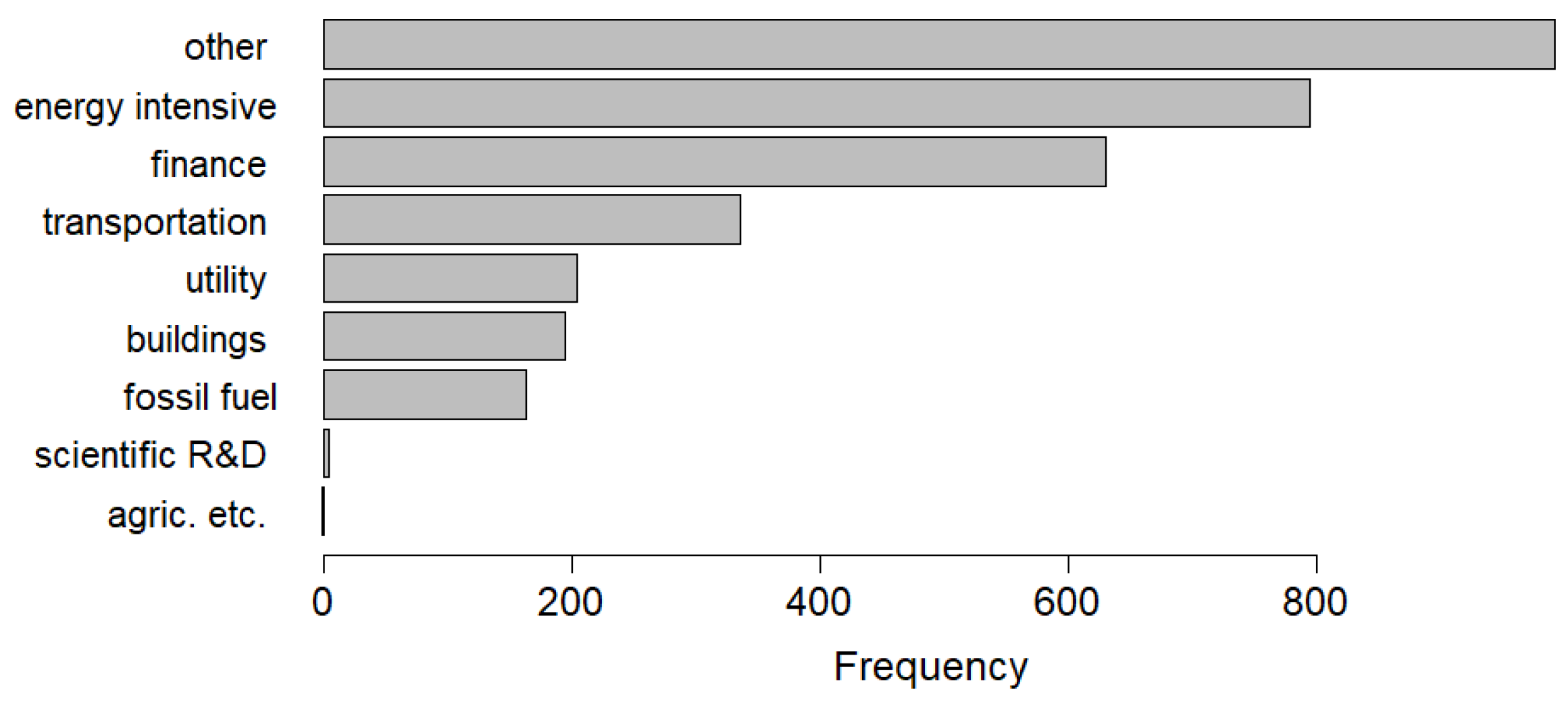

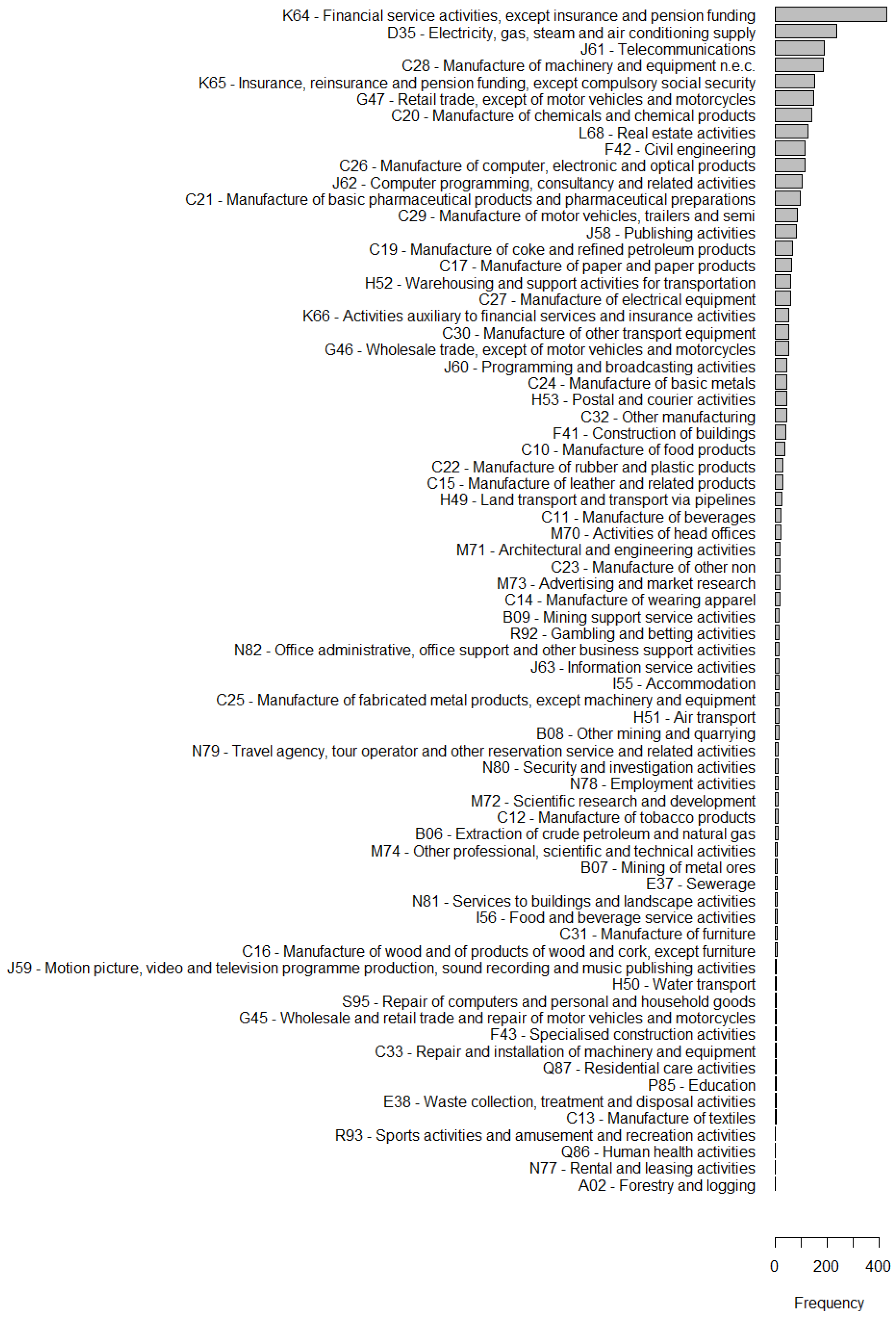

2.2. Sample and Data Exploration

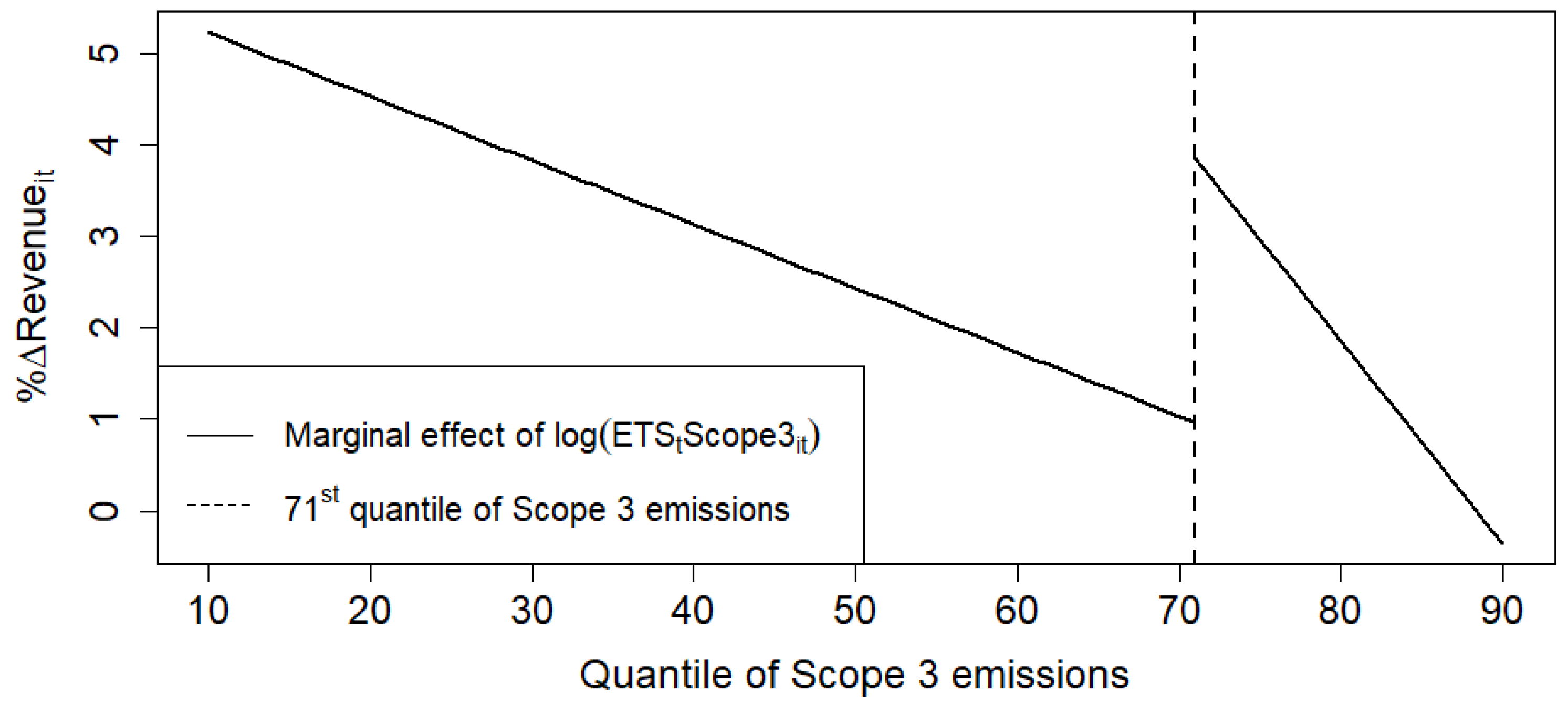

3. Empirical Results and Discussion

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Description | Unit of Measure | Source |

|---|---|---|---|

| Yearly percentage change of the total revenue of a company. Total revenue includes: revenue from goods and services; revenue from financing-related operations; revenue from business-related activities. | % | Refinitiv | |

| Yearly percentage change of total assets reported by a company. | % | Refinitiv | |

| Price of the European Emission Allowances of the EU Emissions Trading System | €/ton of CO2 | Refinitiv | |

| Emissions from contractor-owned vehicles, employee business travel (by rail or air), waste disposal, outsourced activities, emissions from product use by customers, emission from the production of purchased materials, emissions from electricity purchased for resale. | Tonnes | Refinitiv | |

| Value Added Tax rate. The VAT is a consumption tax that is applied to nearly all goods and services that are bought and sold for use or consumption in the EU. | % | OECD & European Commission | |

| Country of Headquarters, also known as Country of Domicile. | Refinitiv | ||

| The size of a company is determined (as described in Section 2.1) by the number of full-time employees, as reported, as of the fiscal period end date (we download data about firms’ number of full-time employees). | Refinitiv | ||

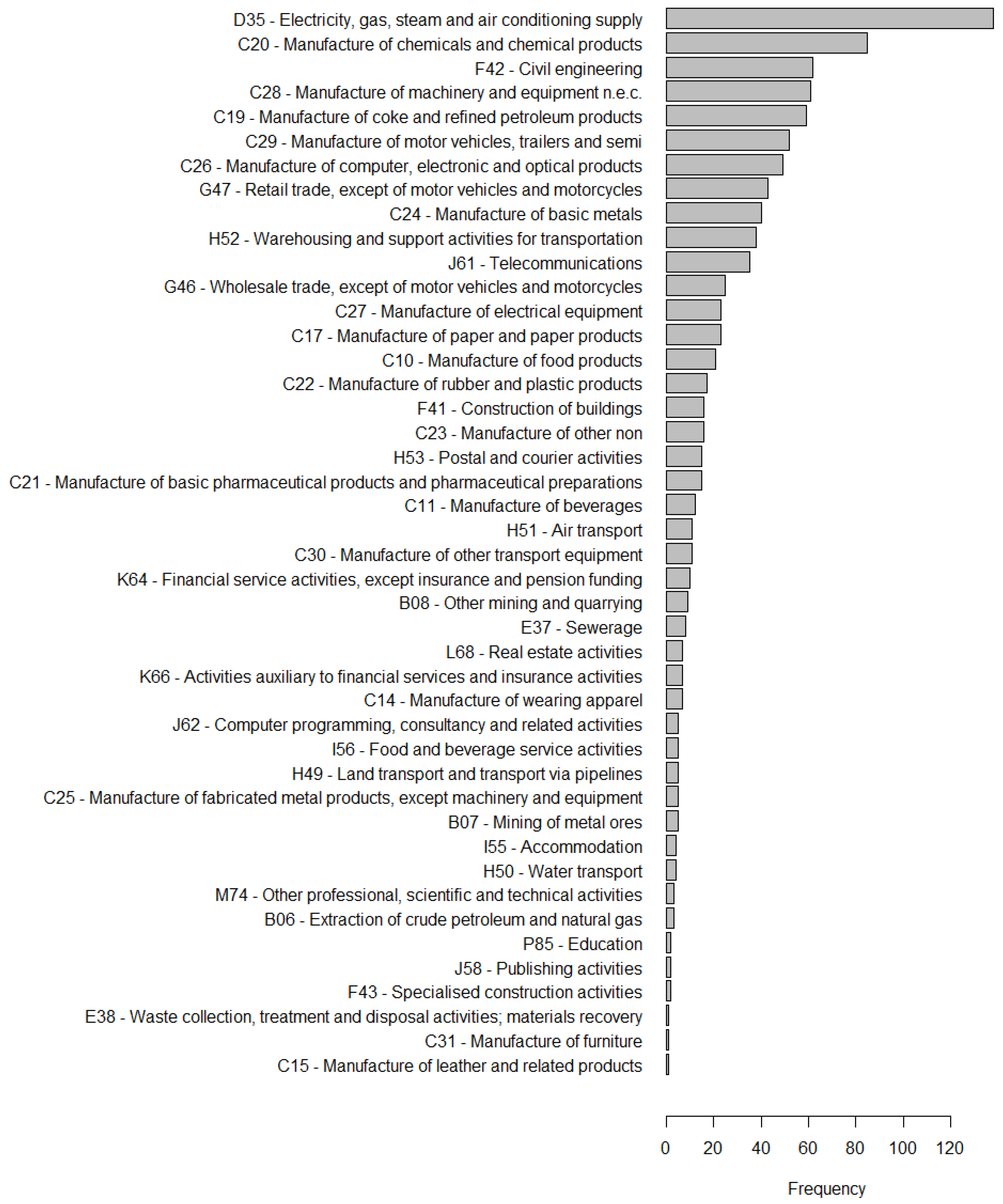

| NACE (for the French term “Nomenclature statistique des Activités Economiques dans la Communauté Européenne”), is the industry standard classification system used in the European Union. | Refinitiv |

References

- Pörtner, H.O.; Roberts, D.C.; Adams, H.; Adler, C.; Aldunce, P.; Ali, E.; Begum, R.A.; Betts, R.; Kerr, R.B.; Biesbroek, R.; et al. Climate Change 2022: Impacts, Adaptation and Vulnerability. In IPCC Sixth Assessment Report; United Nations: New York, NY, USA, 2022; pp. 37–118. [Google Scholar]

- Newbold, T.; Oppenheimer, P.; Etard, A.; Williams, J.J. Tropical and Mediterranean Biodiversity is Disproportionately Sensitive to Land-use and Climate Change. Nat. Ecol. Evol. 2020, 4, 1630–1638. [Google Scholar] [CrossRef] [PubMed]

- Sillmann, J.; Aunan, K.; Emberson, L.; Büker, P.; Van Oort, B.; O’Neill, C.; Otero, N.; Pandey, D.; Brisebois, A. Combined Impacts of Climate and Air Pollution on Human Health and Agricultural Productivity. Environ. Res. Lett. 2021, 16, 093004. [Google Scholar] [CrossRef]

- Kaczan, D.J.; Orgill-Meyer, J. The Impact of Climate Change on Migration: A Synthesis of Recent Empirical Insights. Clim. Chang. 2020, 158, 281–300. [Google Scholar] [CrossRef]

- Trenberth, K.E.; Fasullo, J.T.; Shepherd, T.G. Attribution of Climate Extreme Events. Nat. Clim. Chang. 2015, 5, 725–730. [Google Scholar] [CrossRef]

- Overpeck, J.T.; Conde, C. A Call to Climate Action. Science 2019, 364, 807. [Google Scholar] [CrossRef] [PubMed]

- OECD. Investing in Climate, Investing in Growth; OECD: Paris, France, 2017; p. 312. [Google Scholar]

- Challinor, A.J.; Watson, J.; Lobell, D.B.; Howden, S.; Smith, D.; Chhetri, N. A Meta-analysis of Crop Yield under Climate Change and Adaptation. Nat. Clim. Chang. 2014, 4, 287–291. [Google Scholar] [CrossRef]

- Chen, C.C.; McCarl, B.A.; Schimmelpfennig, D.E. Yield Variability as Influenced by Climate: A Statistical Investigation. Clim. Chang. 2004, 66, 239–261. [Google Scholar] [CrossRef]

- Frank, S.; Böttcher, H.; Gusti, M.; Havlík, P.; Klaassen, G.; Kindermann, G.; Obersteiner, M. Dynamics of the Land Use, Land Use Change, and Forestry Sink in the European Union: The Impacts of Energy and Climate Targets for 2030. Clim. Chang. 2016, 138, 253–266. [Google Scholar] [CrossRef]

- Hasegawa, T.; Fujimori, S.; Havlík, P.; Valin, H.; Bodirsky, B.L.; Doelman, J.C.; Fellmann, T.; Kyle, P.; Koopman, J.F.; Lotze-Campen, H.; et al. Risk of Increased Food Insecurity under Stringent Global Climate Change Mitigation Policy. Nat. Clim. Chang. 2018, 8, 699–703. [Google Scholar] [CrossRef]

- Hatfield, J.L.; Boote, K.J.; Kimball, B.A.; Ziska, L.; Izaurralde, R.C.; Ort, D.; Thomson, A.M.; Wolfe, D. Climate Impacts on Agriculture: Implications for Crop Production. Agron. J. 2011, 103, 351–370. [Google Scholar] [CrossRef]

- Huntingford, C.; Zelazowski, P.; Galbraith, D.; Mercado, L.M.; Sitch, S.; Fisher, R.; Lomas, M.; Walker, A.P.; Jones, C.D.; Booth, B.B.; et al. Simulated Resilience of Tropical Rainforests to CO2-Induced Climate Change. Nat. Geosci. 2013, 6, 268–273. [Google Scholar] [CrossRef]

- Leclère, D.; Havlík, P.; Fuss, S.; Schmid, E.; Mosnier, A.; Walsh, B.; Valin, H.; Herrero, M.; Khabarov, N.; Obersteiner, M. Climate Change Induced Transformations of Agricultural Systems: Insights from a Global Model. Environ. Res. Lett. 2014, 9, 124018. [Google Scholar] [CrossRef]

- Nelson, G.C.; Valin, H.; Sands, R.D.; Havlík, P.; Ahammad, H.; Deryng, D.; Elliott, J.; Fujimori, S.; Hasegawa, T.; Heyhoe, E.; et al. Climate Change Effects on Agriculture: Economic Responses to Biophysical Shocks. Proc. Natl. Acad. Sci. USA 2014, 111, 3274–3279. [Google Scholar] [CrossRef]

- Alfieri, L.; Feyen, L.; Dottori, F.; Bianchi, A. Ensemble Flood Risk Assessment in Europe under High end Climate Scenarios. Glob. Environ. Chang. 2015, 35, 199–212. [Google Scholar] [CrossRef]

- Camia, A.; Libertá, G.; San-Miguel-Ayanz, J. Modeling the Impacts of Climate Change on Forest Fire Danger in Europe. Jt. Res. Cent. (JRC) Tech. Rep. 2017, 1, 22. [Google Scholar]

- Hinkel, J.; Jaeger, C.; Nicholls, R.J.; Lowe, J.; Renn, O.; Peijun, S. Sea-level Rise Scenarios and Coastal Risk Management. Nat. Clim. Chang. 2015, 5, 188–190. [Google Scholar] [CrossRef]

- Semieniuk, G.; Campiglio, E.; Mercure, J.F.; Volz, U.; Edwards, N.R. Low-carbon Transition Risks for Finance. Wiley Interdiscip. Rev. Clim. Chang. 2021, 12, e678. [Google Scholar] [CrossRef]

- Bertram, C.; Hilaire, J.; Kriegler, E.; Beck, T.; Bresch, D.; Clarke, L.; Cui, R.; Edmonds, J.; Min, J.; Piontek, F.; et al. NGFS Climate Scenarios Database: Technical Documentation; NGFS: Paris, France, 2020. [Google Scholar]

- Zhang, S.Y. Are Investors Sensitive to Climate-related Transition and Physical Risks? Evidence from Global Stock Markets. Res. Int. Bus. Financ. 2022, 62, 101710. [Google Scholar] [CrossRef]

- Monasterolo, I.; De Angelis, L. Blind to Carbon Risk? An Analysis of Stock Market Reaction to the Paris Agreement. Ecol. Econ. 2020, 170, 106571. [Google Scholar] [CrossRef]

- Bolton, P.; Kacperczyk, M. Do Investors Care about Carbon Risk? J. Financ. Econ. 2021, 142, 517–549. [Google Scholar] [CrossRef]

- Ilhan, E.; Sautner, Z.; Vilkov, G. Carbon Tail Risk. Rev. Financ. Stud. 2021, 34, 1540–1571. [Google Scholar] [CrossRef]

- Alessi, L.; Ossola, E.; Panzica, R. What Greenium Matters in the Stock Market? The Role of Greenhouse Gas Emissions and Environmental Disclosures. J. Financ. Stab. 2021, 54, 100869. [Google Scholar] [CrossRef]

- Basse Mama, H.; Mandaroux, R. Do Investors Care About Carbon Emissions under the European Environmental Policy? Bus. Strategy Environ. 2022, 31, 268–283. [Google Scholar] [CrossRef]

- TCFD. Recommendations of the Task Force on Climate-Related Financial Disclosures; TCFD: New York, NY, USA, 2017. [Google Scholar]

- FSB-NGFS. Climate Scenario Analysis by Jurisdictions: Initial Findings and Lessons; Financial Stability Board: Basel, Switzerland, 2022. [Google Scholar]

- Dai, R.; Duan, R.; Liang, H.; Ng, L. Enabling Full Supply Chain Corporate Responsibility: Scope 3 Emissions Targets for Ambitious Climate Change Mitigation; Finance Working Paper No. 723/2021; European Corporate Governance Institute: Brussels, Belgium, 2021. [Google Scholar]

- Alogoskoufis, S.; Dunz, N.; Emambakhsh, T.; Hennig, T.; Kaijser, M.; Kouratzoglou, C.; Muñoz, M.A.; Parisi, L.; Salleo, C. ECB Economy-Wide Climate Stress Test: Methodology and Results; Occasional Paper Series; European Central Bank: Frankfurt, Germany, 2021. [Google Scholar]

- Dai, R.; Duan, R.; Liang, H.; Ng, L. Outsourcing Climate Change; Finance Working Paper No. 723/2021; European Corporate Governance Institute: Brussels, Belgium, 2021. [Google Scholar]

- Scott, M.; Van Huizen, J.; Jung, C. The Bank’s Response to Climate Change; Bank of England Quarterly Bulletin; Bank of England: London, UK, 2017; p. Q2. [Google Scholar]

- Vermeulen, R.; Schets, E.; Lohuis, M.; Kolbl, B.; Jansen, D.J.; Heeringa, W. An Energy Transition Risk Stress Test for the Financial System of the Netherlands; Research Department, Netherlands Central Bank: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Gros, D.; Lane, P.R.; Langfield, S.; Matikainen, S.; Pagano, M.; Schoenmaker, D.; Suarez, J. Too Late, Too Sudden: Transition to a Low-Carbon Economy and Systemic Risk; Number 6, Reports of the Advisory Scientific Committee; ESRB: New York, NY, USA, 2016. [Google Scholar]

- Allen, T.; Dees, S.; Caicedo Graciano, C.M.; Chouard, V.; Clerc, L.; de Gaye, A.; Devulder, A.; Diot, S.; Lisack, N.; Pegoraro, F.; et al. Climate-Related Scenarios for Financial Stability Assessment: An Application to France; Banque de France Working Paper; Banque de France: Paris, France, 2020. [Google Scholar]

- Vermeulen, R.; Schets, E.; Lohuis, M.; Kölbl, B.; Jansen, D.J.; Heeringa, W. The Heat is on: A Framework for Measuring Financial Stress under Disruptive Energy Transition Scenarios. Ecol. Econ. 2021, 190, 107205. [Google Scholar] [CrossRef]

- Battiston, S.; Mandel, A.; Monasterolo, I.; Schütze, F.; Visentin, G. A Climate Stress-test of the Sinancial System. Nat. Clim. Chang. 2017, 7, 283–288. [Google Scholar] [CrossRef]

- Chenet, H. Climate Change and Financial Risk; Springer: Berlin/Heidelberg, Germany, 2021. [Google Scholar]

- Hogan, J.; Lodhia, S. Sustainability Reporting and Reputation Risk Management: An Australian Case Study. Int. J. Account. Inf. Manag. 2011, 19, 267–287. [Google Scholar] [CrossRef]

- Blanco, C.; Caro, F.; Corbett, C.J. The State of Supply Chain Carbon Footprinting: Analysis of CDP Disclosures by US Firms. J. Clean. Prod. 2016, 135, 1189–1197. [Google Scholar] [CrossRef]

- Guastella, G.; Mazzarano, M.; Pareglio, S.; Xepapadeas, A. Climate Reputation Risk and Abnormal Returns in the Stock Markets: A Focus on Large Emitters. Int. Rev. Financ. Anal. 2022, 84, 102365. [Google Scholar] [CrossRef]

- Diaz-Rainey, I.; Gehricke, S.A.; Roberts, H.; Zhang, R. Trump vs. Paris: The Impact of Climate Policy on US Listed Oil and Gas Firm Returns and Volatility. Int. Rev. Financ. Anal. 2021, 76, 101746. [Google Scholar] [CrossRef]

- Hansen, B.E. Sample Splitting and Threshold Estimation. Econometrica 2000, 68, 575–603. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Selection Corrections for Panel Data Models Under Conditional Mean Independence Assumptions. J. Econom. 1995, 68, 115–132. [Google Scholar] [CrossRef]

- OECD. OECD SME and Entrepreneurship Outlook: 2005; OECD: Paris, France, 2005; p. 17. [Google Scholar]

- Eurostat. NACE Rev. 2 Statistical Classification of Economic Activities in the European Community; Methodologies and Working Papers; Eurostat: Luxembourg, 2008. [Google Scholar]

- Downie, J.; Stubbs, W. Corporate Carbon Strategies and Greenhouse Gas Emission Assessments: The Implications of Scope 3 Emission Factor Selection. Bus. Strategy Environ. 2012, 21, 412–422. [Google Scholar] [CrossRef]

- European Commission. EU ETS Handbook; European Commission: Bangkok, Thailand, 2015. [Google Scholar]

- Hansen, B.E. Econometrics; Princeton University Press: Princeton, NJ, USA, 2022. [Google Scholar]

- Chan, K.S. Consistency and Limiting Distribution of the Least Squares Estimator of a Threshold Autoregressive Model. Ann. Stat. 1993, 21, 520–533. [Google Scholar] [CrossRef]

- Schmidt, M.; Nill, M.; Scholz, J. Determining the Scope 3 Emissions of Companies. Chem. Eng. Technol. 2022, 45, 1218–1230. [Google Scholar] [CrossRef]

- Gale, G.W.; Gelfond, H.; Krupkin, A. Entrepreneurship and Small Business Under a Value-Added Tax; Economic Studies at Brookings; Brookings: Washington, DC, USA, 2016. [Google Scholar]

| Coefficient Estimate | Std. Error | t Statistic | p-Value | ||

|---|---|---|---|---|---|

| Intercept | 5.82 | 12.39 | 0.47 | 0.64 | |

| 0.07 | 0.02 | 3.64 | 2.8 × 10−9 | *** | |

| 0.21 | 0.01 | 16.07 | 2.2 × 10−16 | *** | |

| −0.29 | 0.18 | −1.62 | 0.11 | ||

| 13.43 | 5.85 | 2.29 | 0.02 | ** | |

| −0.63 | 0.34 | −1.87 | 0.06 | * | |

| 1.14 | 0.55 | 2.09 | 0.04 | ** | |

| t | −0.64 | 0.11 | −5.92 | 3.7 × 10−9 | *** |

| 619,628.4 | |||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Guastella, G.; Pareglio, S.; Schiavoni, C. An Empirical Approach to Integrating Climate Reputational Risk in Long-Term Scenario Analysis. Sustainability 2023, 15, 5886. https://doi.org/10.3390/su15075886

Guastella G, Pareglio S, Schiavoni C. An Empirical Approach to Integrating Climate Reputational Risk in Long-Term Scenario Analysis. Sustainability. 2023; 15(7):5886. https://doi.org/10.3390/su15075886

Chicago/Turabian StyleGuastella, Gianni, Stefano Pareglio, and Caterina Schiavoni. 2023. "An Empirical Approach to Integrating Climate Reputational Risk in Long-Term Scenario Analysis" Sustainability 15, no. 7: 5886. https://doi.org/10.3390/su15075886

APA StyleGuastella, G., Pareglio, S., & Schiavoni, C. (2023). An Empirical Approach to Integrating Climate Reputational Risk in Long-Term Scenario Analysis. Sustainability, 15(7), 5886. https://doi.org/10.3390/su15075886