1. Introduction

The challenges posed by population change, climate change, and resource scarcity have made global sustainable development an urgent concern that has garnered significant attention worldwide. At the same time, guided by the principles of green development, enhancing the efficiency of the green economy serves as the impetus for achieving social sustainable development and attaining high-quality economic growth. The ongoing efforts of the Chinese government to accomplish the “low-carbon goals” align with the prevailing notion of green development and showcase China’s steadfast resolve to actively combat climate change, pursue a path of green and low-carbon development, and foster the collective progress of humanity. Corporate ESG construction is closely aligned with China’s low-carbon goals. Given the growing challenges of resource and environmental constraints, as well as regional economic and social disparities, it becomes imperative for companies to integrate environmental, social, and corporate governance (ESG) factors into their investment, organizational, and production decision-making processes. By incorporating ESG practices, enterprises can explore avenues to improve regional green economic efficiency at the corporate level. This approach holds not only practical value, but also significant theoretical implications.

Enterprises hold a crucial role in the development of regional economies. In China’s new stage of development, enterprises are socially responsible for enhancing the efficiency of regional green economies. As the concept of new development continues to permeate all dimensions of social and economic progress, government entities are also reinforcing requirements for ESG information disclosure by listed companies. In December 2017, the China Securities Regulatory Commission mandated that environmental protection agencies disclose key environmental information [

1]. Subsequently, according to the revised guidelines for listed companies’ annual and semi-annual reports in June 2021 [

2], emphasizing the disclosure of “environmental and social responsibility”, the objective is to strengthen the fulfillment of corporate social responsibility (CSR) in terms of green development and environmental protection through ESG information disclosure, while also pursuing profit maximization.

Currently, most scholars focus on studying the factors that influence corporate ESG construction and its relationship with corporate operations. Additionally, they explore the interpretation of indicators for regional green economic efficiency and their influencing factors. However, there is limited research on integrating corporate ESG construction with macroeconomic factors. This study aims to fill this research gap by examining the impact of corporate ESG construction on regional green economic efficiency within the same analytical framework. The objective is to investigate whether corporate ESG construction affects regional green economic efficiency and the nature of this effect. By doing so, this study intends to advance the knowledge and understanding of corporate ESG construction and its implications for green economic efficiency.

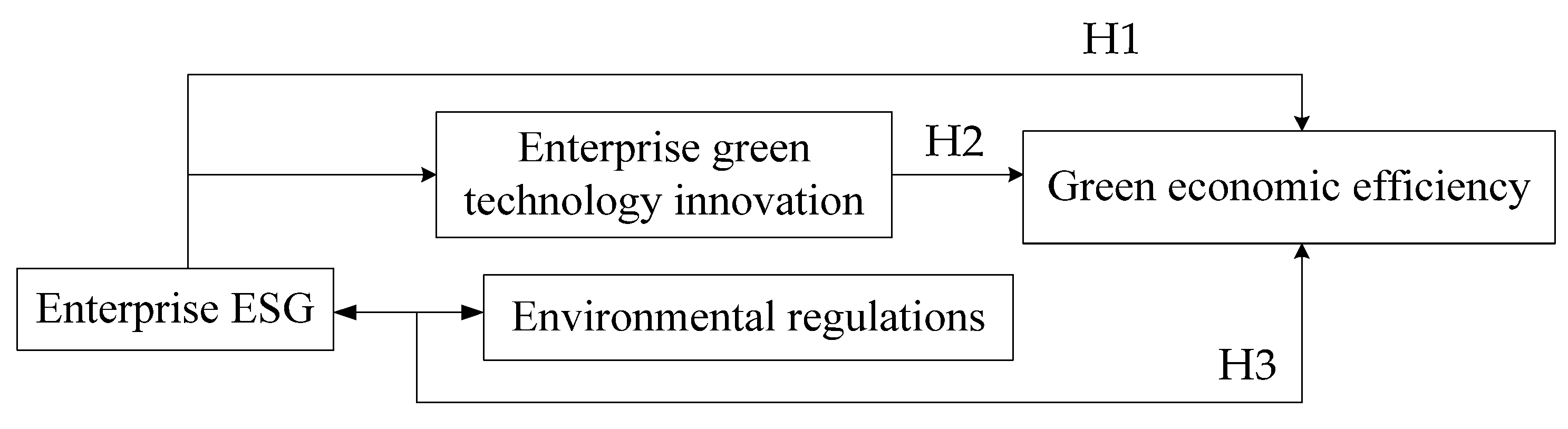

This article aims to address three key questions. (1) Does corporate ESG construction have an impact on the efficiency of a regional green economy? (2) What are the mechanisms through which corporate ESG construction influences the efficiency of a regional green economy? (3) Does the impact of corporate ESG construction on the efficiency of a regional green economy vary based on corporate characteristics? Drawing from stakeholder theory and signal transmission theory, this article focuses on analyzing the theoretical mechanisms and impact of corporate ESG construction on the efficiency of a regional green economy. To investigate this, we analyze the relationship between enterprise ESG construction and regional green economic efficiency using ESG rating data from the CSI (China Securities Index). Furthermore, we explore the potential mechanisms through which corporate green innovation and environmental regulations may influence this relationship. By addressing these questions, this study aims to enhance the long-term value of companies, promote the alignment of their social and economic values, and ultimately improve regional green economic efficiency.

Compared to the existing literature, this study offers three potential contributions. Firstly, it investigates the impact of enterprise ESG construction on regional green economic efficiency using signaling theory and stakeholder theory. The study acknowledges that the demand for regional green development creates environmental regulatory pressure and stimulates aspirations for green innovation. As a result, companies are motivated to embrace ESG practices and fulfill their corporate social responsibility. This departure from the traditional “three highs, three lows” production model improves the expected output levels, reduces unexpected output levels, and ultimately enhances regional green economic efficiency. The study examines the underlying mechanisms and presents empirical evidence to support this process. Secondly, the study examines the mechanisms through which enterprise ESG affects regional green economic efficiency from the perspectives of corporate green innovation and environmental regulation. This novel approach provides fresh insights into the role of corporate ESG construction in enhancing regional green economic efficiency and expands the research focus within the relevant literature. Furthermore, the study utilizes ESG rating databases from two independent rating agencies, CSI and SynTao Green Finance, to explore the effects of corporate ESG construction on regional green development. This helps reduce uncertainties in research outcomes arising from the variability of enterprise ESG ratings.

The structure of this article is organized as follows:

Section 2: Literature Review provides a comprehensive overview of previous research related to the topic, serving as the basis for the current study.

Section 3: Theoretical Analysis and Hypotheses presents the analysis process of theory and proposes hypotheses.

Section 4: Methodology and Data makes explanation for the data, variables and methods used in this paper.

Section 5: Research Results and Discussion presents the statistical analysis findings, showcasing the results obtained from the study. It also includes an in-depth discussion and interpretation of these results.

Section 6: Conclusions and Implications concludes the study by summarizing the main findings and implications derived from the research. Furthermore, it offers policy suggestions based on the significance of the conclusions reached in the study.

2. Literature Review

With the increasing emphasis on green and sustainable development, corporate ESG construction has experienced a surge in growth. ESG construction serves as a crucial reflection of a company’s sustainable business capabilities and its commitment to corporate social responsibility (CSR). Many scholars have focused on studying the economic consequences of corporate ESG construction and the factors that influence it. From an economic perspective, the attention is primarily directed towards the impact of corporate ESG construction on various aspects such as corporate financing costs, corporate value, and corporate innovation. Disclosing ESG construction helps reduce the information asymmetry related to CSR, leading to companies with stronger ESG construction experiencing significantly lower financing costs [

1,

2,

3,

4]. It can also improve investment efficiency and significantly increase the market value [

5,

6,

7]. Additionally, better ESG construction is linked to enhanced levels of technological innovation [

8]. Fulfilling CSR obligations can establish a positive corporate image, garner support from stakeholders, alleviate financing constraints, and enhance resource-acquisition capabilities [

9]. Regarding corporate ESG construction, factors such as digital transformation, enterprise financial performance, and company size all demonstrate significant effects on a company’s ESG construction [

10,

11,

12,

13]. Furthermore, there is a long-term alignment between corporate ESG construction and corporate green innovation [

14,

15,

16].

Research on regional green economy efficiency primarily focuses on the factors that influence it and the measurement of relevant indicators. In order to assess regional green economic efficiency, undesirable outputs such as industrial waste, emissions, and wastewater are incorporated into analytical frameworks. This approach offers a fresh perspective on traditional total-factor productivity and provides an indicator for measuring high-quality economic development in China. The development of the digital economy plays a significant role in improving regional green economic efficiency [

17,

18], with high marketization being a crucial condition for achieving such efficiency [

19]. Additionally, the upgrading of industrial structures and the rectification of factor distortions serve as important channels through which the digital economy influences green economic efficiency [

20]. Environmental regulations also play a substantial role in promoting green economic efficiency [

21], although some studies have observed an inverted U-shaped relationship between environmental regulations and green economic efficiency [

22]. Technological innovation has been found to have a positive effect on green economic efficiency [

23], and carbon trading policies can facilitate the growth of regional green economic efficiency through technological advancements [

24]. As for the indicator measurement, several models are commonly used, including the SBM-DEA model (slack-based model-data envelopment analysis) and the DEA (data envelopment analysis) model [

25,

26].

The aforementioned study provides substantial empirical evidence for examining the relationship between corporate ESG and regional green economic efficiency, offering a valuable theoretical perspective for comprehending the development of corporate ESG and the regional green economy. However, the existing literature predominantly focuses on investigating the impact of macroeconomic policies and environmental factors on micro-level corporate behavior. For instance, it has been observed that environmental policy uncertainty significantly hinders corporate green investments, while green credit policies are beneficial in reducing the fictitiousness of heavily polluting enterprises [

27,

28]. Nonetheless, there is limited research exploring how micro-level corporate behavior influences macroeconomic policies. This neglects the research perspective that encompasses not only the micro-to-micro or macro-to-micro relationships, but also the micro-to-macro relationships, where the decisions made by micro-level companies possess interrelated attributes rather than being isolated. In the existing studies, the mechanisms and pathways of regional green economic efficiency have been analyzed, along with the exploration of the relationship between corporate ESG construction, corporate behavior, and financial performance. However, there is a gap in the research regarding the effects of corporate ESG construction on promoting regional green economic efficiency. Furthermore, though some of the literature has delved into the impact of corporate ESG construction on innovation 8, there is still a need for further investigation to deepen our understanding of the relationship between corporate ESG construction and green technological innovation within the context of environmental regulations. Additionally, the mechanisms through which corporate ESG construction enhances regional green economic efficiency require more exploration. Therefore, this study aims to address these gaps by conducting theoretical analysis and developing a mathematical model. It seeks to explore whether the behavior of micro-level companies, through ESG construction, has an impact on the development of the regional green economy. The specific research design will be discussed in detail in the subsequent sections.

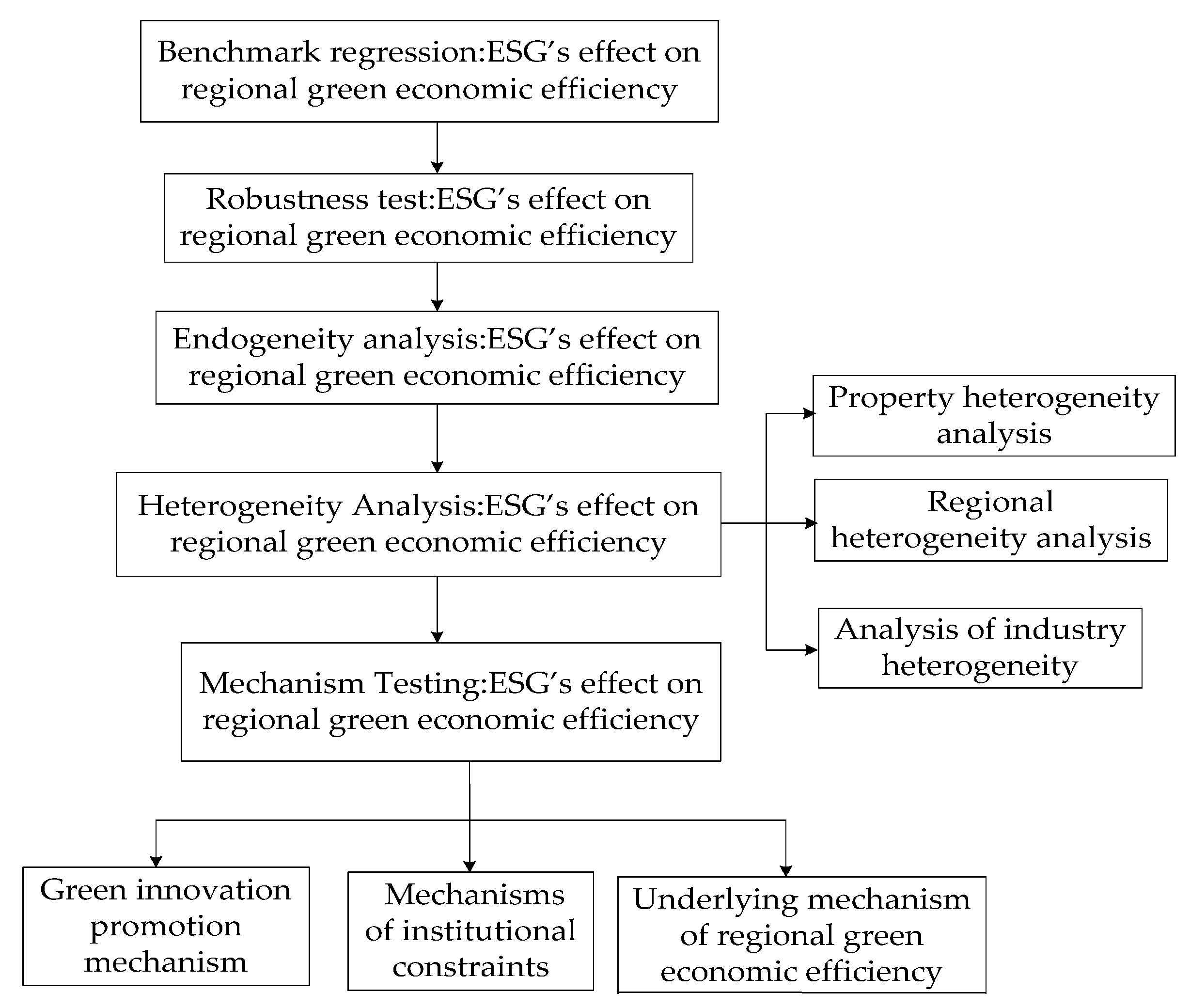

5. Empirical Results and Discussion

In order to test the research hypothesis regarding the impact of corporate ESG construction on regional green economic efficiency, this study employs several empirical tests. These tests include a benchmark regression analysis, an endogeneity test, a robustness test, a heterogeneity test, and a mechanism test.

5.1. Benchmark Regression Results

Columns (1) and (2) in

Table 2 present the benchmark regression results for the impact of enterprise ESG on regional green economic efficiency. In column (1), the regression is conducted without incorporating other control variables. The coefficient of corporate ESG construction is found to be significantly positive at the 1% level. Moving to Model (2), control variables are added to the regression in column (1). The coefficients of corporate ESG construction remain statistically significant at the 1% level. This suggests that corporate ESG construction has a positive effect on regional green economic efficiency. Moreover, for each improvement in the ESG construction level, there is a 0.7% increase in green technology efficiency. These findings highlight that corporate ESG construction enhances regional green economic efficiency and contributes to the realization of a green economy by improving ESG practices. It is evident that corporate ESG construction not only influences firm performance, but also promotes regional green economic efficiency by elevating the level of corporate ESG construction. This fosters a coordinated development between the regional economy and green practices.

Green development is a crucial concept that underpins the overall development of our country. It represents an inevitable choice in achieving sustainable and high-quality development. Enterprises serve as the source of market vitality, and macroeconomic development reflects the collective behavior of these micro-level enterprises. The construction of enterprise ESG reflects the attitude and progress of enterprise green transformation. Currently, our country is dedicated to achieving green development goals by providing financial and policy support. This includes encouraging enterprises to actively engage in green transformation, improve their ESG construction level, and ultimately enhance the efficiency of the regional green economy. These efforts align with Hypothesis 1. Distinguishing itself from prior studies, this research breaks through the existing literature’s perspective by transitioning from the micro-to-macro level. It begins from the standpoint of individual enterprises and endeavors to explore the impact of changes in enterprise behavioral decision-making on macroeconomic development. Through this approach, enterprises are encouraged to fulfill their social responsibilities and contribute to the task of economic development.

5.2. Robustness Test of ESG’s Effect on Regional Green Economic Efficiency

To further ensure the robustness of our benchmark regression results, we conduct three robustness analyses. First, we replace the original data with ESG rating data from SynTao Green Finance to analyze the uncertainty in ESG construction stemming from subjective ESG ratings. This allows us to explore any potential variations in the effects on regional green economic efficiency. Second, we utilize different rating assignment methods for enterprise ESG. Specifically, we assign a value of 1 to companies with ratings of BBB or above, and a value of 0 to those with lower ratings. Third, we apply a standardization technique, specifically Z-scores, to the core explanatory variable. This involves transforming the data by subtracting the mean and dividing it by the sample standard deviation. The result is a new variable with a mean of 0 and a standard deviation of 1. Columns (3)–(5) in

Table 2 present the regression results obtained from these robustness tests, allowing us to evaluate the stability and consistency of our findings.

Column (3) illustrates the regression results using the SynTao Green Finance (sdesg) rating index as the core explanatory variable. The coefficient is found to be significantly positive at the 1% level. This suggests that the regression results for corporate ratings obtained from different rating agencies also demonstrate a significant positive effect on regional green economic efficiency. Moving to column (4), we observe the regression results after changing the rating assignment method. Remarkably, the coefficient remains significantly positive, indicating that the positive effect of enterprise ESG on green economic efficiency persists irrespective of the rating assignment approach. Proceeding to column (5), we present the results after standardizing the corporate ESG construction rating score. Encouragingly, the coefficient remains significantly positive. These consistent findings indicate that different measurement approaches do not alter the positive effect of enterprise ESG on regional green economic efficiency. Overall, the robustness test results consistently demonstrate the significant and robust positive effect of ESG on regional green economic efficiency.

5.3. Endogeneity Analysis

To address potential endogeneity in the model, we employ three analyses and treatments.

Firstly, following the approach of Xi et al. [

55], we use the earliest ESG construction rating score of each company as an instrumental variable in a two-stage regression. This instrumental variable satisfies the relevance and exclusivity constraints as it impacts the subsequent ESG construction of the firm, but does not directly impact the green economic efficiency of the region. The regression results are presented in columns (1) and (2) of

Table 3. Notably, the coefficient remains significant at the 5% level, indicating that the results remain robust even after accounting for endogeneity.

Secondly, it is worth noting that better corporate ESG construction exhibits a stronger promotion effect on green economic efficiency. However, we also need to consider the possibility that regions with higher levels of green economic development may experience more intense market competition and stricter regulatory supervision of corporate behavior. This, in turn, encourages companies to improve their ESG construction. Such influences can give rise to endogeneity issues due to bidirectional causality. To address this concern, we incorporate lagged explanatory variables in our analysis to alleviate the problem of bidirectional causality. Specifically, we include lagged ESG construction variables (L.esg, L2.esg) as explanatory variables. Columns (3) and (4) in

Table 3 present the regression results obtained after incorporating these lagged variables. Notably, the coefficients of both lagged variables are found to be significantly positive at the 1% level, providing support for Hypothesis 1. This indicates that good corporate ESG construction has a positive and long-term impact on green economic efficiency.

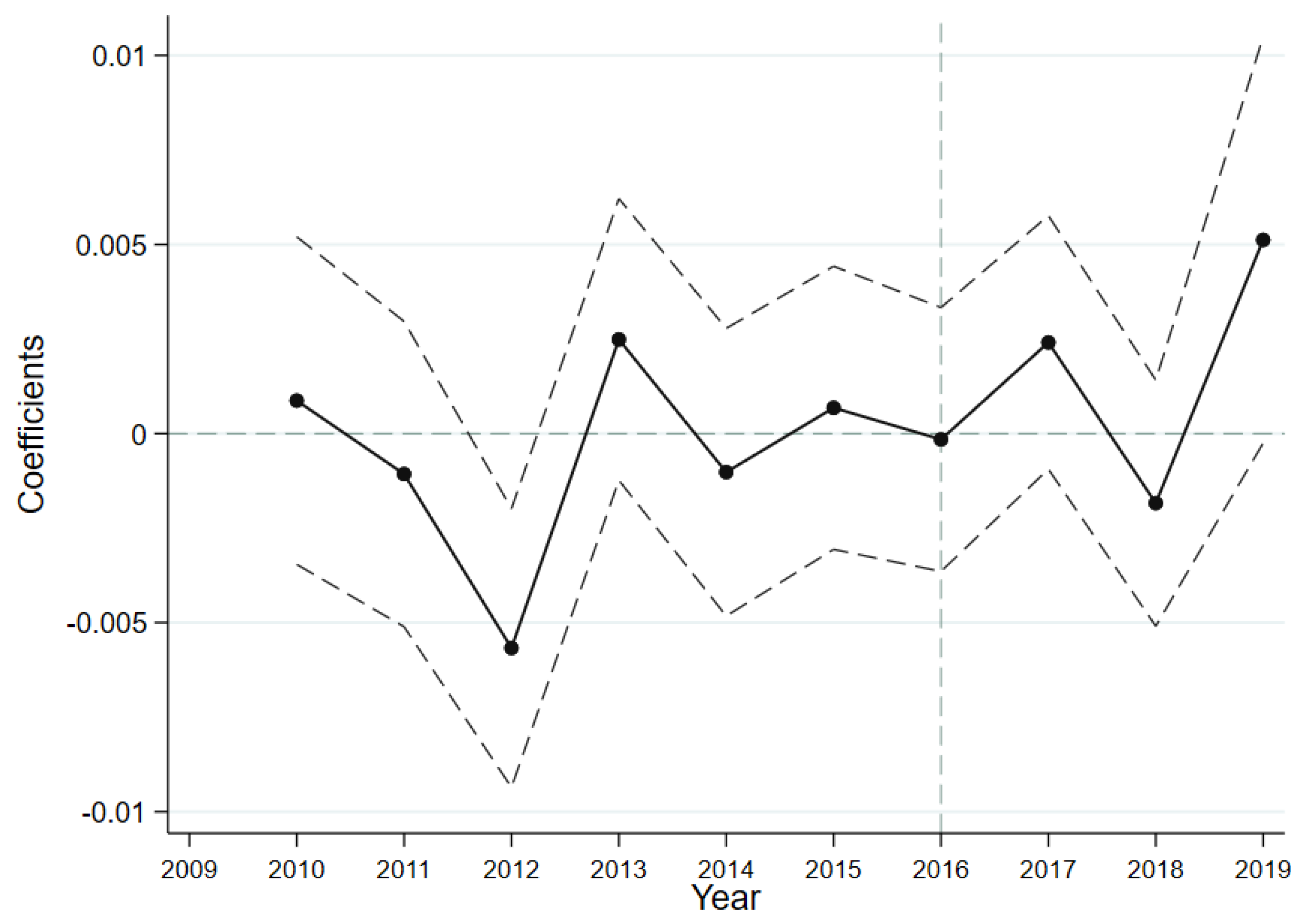

Finally, to address potential endogeneity issues stemming from other factors, we adopt the difference-in-differences method, following the approach outlined by Song et al. [

56]. In recent years, China has been making continuous improvements to regulatory policies regarding ESG information disclosure by listed companies. In August 2016, a significant policy development took place when the People’s Bank of China, the China Securities Regulatory Commission, and seven other departments jointly issued the “Guiding Opinions on Building a Green Financial System” [

57]. This policy introduced a mandatory environmental information disclosure system for listed companies. We consider this policy as a quasi-natural experiment, with the year 2016 marking its implementation. Given that the majority of listed companies are affected by ESG regulatory policies, it becomes challenging to distinguish clear experimental and control groups. Hence, in line with Nunn et al. [

58], we employ a continuous difference-in-differences model for estimation. In this model, we set a policy dummy variable, called “Time,” to 0 when the year <2016 and 1 otherwise.

The regression results, presented in column (5) of

Table 3, provide insights into the effect of ESG regulatory policy shocks on regional green economic efficiency. The coefficient of the interaction term, time × egg, reflects this effect. Notably, the coefficient before the interaction term is 0.01 and significantly positive at the 1% level, indicating a positive impact of ESG policy implementation on regional green economic efficiency. These findings align with the baseline regression results. Additionally, the balance trend test, illustrated in

Figure 4, confirms that prior to the policy’s implementation in 2016, its effect was not significant. However, from 2017 onwards, the policy’s impact gradually became evident, which is consistent with the conclusion given in column (5) of

Table 3. This further strengthens the robustness of the baseline regression results. Overall, these findings indicate that the implementation of ESG regulatory policies has a certain influence on regional green economic efficiency.

5.4. Heterogeneity Analysis

5.4.1. Property Heterogeneity Analysis

To examine potential differences in the impact of ESG on regional green economic efficiency between enterprises with different property rights we divide the sample enterprises into two categories: state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs), based on their ownership. We then conduct a subsample regression analysis. The results, presented in columns (1) and (2) of

Table 4, reveal that the coefficient of ESG for the SOE sample is 0.011, which is statistically significant at the 1% level. However, the coefficient of ESG for the non-SOE sample is not found to be statistically significant. From this, we can infer that the positive effect of enterprise ESG on regional green economic efficiency is more prominent among SOEs compared to non-SOEs.

This could be attributed to the fact that SOEs carry dual social and economic responsibilities. In comparison to non-SOEs, their strategic management objectives and organizational management are influenced by national policies, and they possess stronger corporate social responsibility (CSR) and political affiliations. Consequently, they are subjected to more stringent government regulations. Fulfilling ESG responsibilities helps improve the internal governance of SOEs, enhances management’s willingness to take risks through innovative incentive mechanisms, promotes innovative decision-making, develops a competitive advantage, and receives more resource support. Furthermore, as significant entities in socio-economic development, SOEs play a crucial role in demonstrating policy compliance and fulfilling political responsibilities in ESG construction. Therefore, when compared to non-SOEs, SOEs exhibit greater motivation to fulfill ESG responsibilities, leading to a more pronounced impact of ESG construction on regional green economic efficiency.

5.4.2. Regional Heterogeneity Analysis

Different levels of economic development can contribute to variations in the impact of ESG initiatives. There are also disparities in the levels of green economic efficiency and firm development across different regions. To examine this, we classify the sample companies into two groups based on their registered locations: the eastern region and the central and western regions. Analyzing the regression results presented in columns (3) and (4) of

Table 4, we find that the ESG coefficient for companies in the eastern region is 0.03, which is statistically significant at the 10% level. However, the coefficient for companies in the central and western regions is not statistically significant. This suggests that ESG initiatives have a more pronounced effect on promoting green economic efficiency in the eastern region. This can be attributed to several factors. Firstly, the eastern region benefits from clear resource advantages, higher levels of economic development, and a more comprehensive institutional environment. Secondly, evolving investment philosophies among investors now place greater emphasis on non-financial indicators such as ESG, while government regulations impose stricter requirements on companies. These factors have compelled companies in the eastern region to pay more attention to ESG in order to reduce regulatory and public pressures. Additionally, the eastern region boasts a more developed economy and is able to provide more resources and financial policy support to companies. This enhances firms’ motivation to improve their ESG practices. On the other hand, the relatively lower levels of economic development in the central and western regions result in a lack of motivation and resources for companies to prioritize ESG initiatives. Furthermore, in the central and western regions, governments, societies, and companies primarily emphasize economic benefits to promote economic development, often neglecting CSR considerations. As a result, ESG investment by companies in these regions is relatively lower. In conclusion, for companies located in the eastern region, the effect of ESG initiatives on regional green economic efficiency is more significant due to the region’s clear resource advantages, higher levels of economic development, evolving investment philosophies, stricter government regulations, and greater availability of resources and financial policy support.

5.4.3. Analysis of Industry Heterogeneity

To examine the impact of ESG on regional green economic efficiency among companies with varying degrees of pollution, we classify the sample into two categories: polluting and non-polluting companies. This classification is based on the “Industry Classification Management Directory for Environmental Inspection of Listed Companies” published by the Ministry of Environmental Protection of China [

59], and the “Industry Classification Guidelines for Listed Companies” (revised in 2012) published by the China Securities Regulatory Commission [

60]. We then conduct a sub-sample regression analysis, and the results are presented in columns (5) and (6) of

Table 4. The regression results indicate that the ESG coefficient for polluting companies is significantly positive at the 1% level. However, for non-polluting companies, the ESG coefficient is not statistically significant. This suggests that the positive effect of ESG on regional green economic efficiency is more pronounced among polluting companies. The differential impact can be attributed to the varying levels of environmental regulatory constraints faced by different industries. Polluting companies, in particular, are subjected to stricter environmental regulations and garner more public attention due to their environmental impact. As a result, they are compelled to address pollution issues more actively. Moreover, polluting companies can improve their public image and environmental reputation by implementing pollution control measures. This, in turn, broadens their potential customer base and enhances their ESG performance. Consequently, their efforts contribute to influencing regional green economic efficiency positively. In summary, polluting companies, facing stricter environmental constraints and greater public scrutiny, have a stronger incentive to address pollution issues and improve their ESG practices. This enables them to enhance their influence over regional green economic efficiency.

5.5. Mechanism Testing

5.5.1. Green Innovation Promotion Mechanism

The promotion of green economic transformation has become a globally discussed topic, and China has been actively committed to green development, with a particular focus on the green transformation of enterprises. To further analyze the mechanism through which firms’ ESG practices impact regional green economic efficiency, we introduce green technological innovation as a mediating variable and construct a model to test its mediating effect. The regression results, presented in columns (1)–(6) of

Table 5, provide insights into this analysis. In column (1), the positive effect of ESG on the overall level of green technological innovation in enterprises is evident, with a coefficient of 0.152. This coefficient is statistically significant at the 1% level, indicating that enterprises’ ESG practices significantly promote green innovation. Moving forward, in columns (2) and (3), we explore the effect of enterprise ESG practices on the quality and quantity of green technological innovation. The regression coefficients for these variables are 0.128 and 0.092, respectively, both of which are statistically significant at the 1% level. These findings suggest that enterprise ESG construction can improve both the quality and quantity of green technological innovation. Expanding our analysis, columns (4)–(6) present the regression results obtained by incorporating both ESG and green technological innovation into the model. In all three cases, the coefficients of ESG remain statistically significant at the 1% level. This indicates that enterprise ESG practices enhance regional green economic efficiency by promoting firms’ green innovation. To summarize, the findings confirm that enterprise ESG practices have a positive and significant impact on the overall level, quality, and quantity of green technological innovation. Moreover, incorporating ESG into the model further demonstrates its role in enhancing regional green economic efficiency through the promotion of firms’ green innovation.

Based on the literature review, one possible explanation is that corporate ESG practices can enhance the level of green technological innovation within the company. This is primarily achieved through increased investment in research and development (R&D) activities. Additionally, such R&D investments can positively impact the company’s green economic efficiency [

61], particularly by improving its level of green innovation. The presence of green innovation within the company, by enhancing technological efficiency and promoting technological progress, significantly contributes to green economic efficiency [

62]. This improvement is mainly observed in the quality of the company’s green innovation. Furthermore, according to the “Guiding Opinions on Building a Market-oriented Green Technology Innovation System” proposed by The National Development and Reform Commission and the Ministry of Science and Technology [

63], the emphasis is placed on strengthening the role of enterprises in green innovation and increasing support for their green technology innovation. This initiative provides Chinese enterprises with a reliable market environment to engage in green technology innovation and promotes the overall green development of the economy. In summary, corporate ESG practices have the potential to enhance regional green economic efficiency by influencing green technological innovation. This hypothesis can be further verified by research studies.

5.5.2. Mechanisms of Institutional Constraints

To examine the influence of the institutional environment on the effect of ESG practices on regional green economic efficiency, we introduce environmental regulations as a moderating variable and construct a moderation effect model. The regression results are presented in columns (7) and (8) of

Table 5. In column (7), we present the regression results without including moderating and control variables. Here, the coefficient of ESG is significantly positive, indicating that enterprise ESG practices contribute positively to regional green economic efficiency. Moving to column (8), we present the regression results after incorporating the intensity of environmental regulations and the interaction term between environmental regulations and ESG (ESG × ER). In this case, the coefficient of ESG remains significantly positive. However, both the coefficients of environmental regulations and the interaction term are significantly negative. This suggests that environmental regulations have a notable inhibitory effect on green economic efficiency and weaken the positive impact of enterprise ESG practices. One possible explanation for these findings is the implementation of stringent environmental management policies. These policies have resulted in more stringent environmental regulations. The increased costs associated with compliance to these regulations may have led to reduced investment by companies in improving their green technologies. As a result, the advancement of corporate ESG practices has been hindered, leading to a suppression of improvements in green economic efficiency. This confirms Hypothesis 3, which suggests that environmental regulations have an inhibitory effect on the relationship between ESG practices and regional green economic efficiency.

5.5.3. Underlying Mechanism of Regional Green Economic Efficiency

We utilize the Malmquist index decomposition method to analyze and decompose green economic efficiency into two components: green scale efficiency and green pure technical efficiency. In order to achieve this, we construct the following models:

In Equations (5) and (6), green scale efficiency and green pure technical efficiency are represented by and, respectively, with the same variable meanings as in model (1). Models (1) and (2) in

Table 6 display the regression results obtained by examining the relationship between enterprise ESG and pure green technical efficiency, as well as green scale efficiency, respectively. When pure green technical efficiency serves as the dependent variable, the coefficients, after adding control variables, are not statistically significant, indicating that the impact of ESG on pure green technical efficiency is not significant. However, when the dependent variable is green scale efficiency, as demonstrated in models (3) and (4), the regression coefficients are 0.006 and 0.006, respectively, both significantly positive at the 1% level. This suggests that enterprise ESG practices significantly promote green scale efficiency. Comparing the regression results in

Table 2 and

Table 6, and considering the relationship between green technical efficiency, pure green technical efficiency, and green scale efficiency, it becomes evident that enterprise ESG practices have a substantial impact on green technical efficiency and green scale efficiency, while the effect on pure green technical efficiency is not significant. These findings indicate that the positive influence of enterprise ESG practices on regional green economic efficiency is primarily achieved through its impact on green scale efficiency.

6. Conclusions and Limitations

Enhancing the efficiency of the regional green economy is crucial for achieving high-quality economic development in China. Therefore, it is imperative to thoroughly examine whether corporate ESG construction can promote the improvement of regional green economy efficiency in China. To investigate this, the study utilizes unbalanced panel data consisting of 15,192 samples from 1454 Chinese A-share listed companies spanning the period from 2009 to 2019. The findings of this study are as follows: Firstly, the research demonstrates that corporate ESG construction has a significant positive impact on regional green economic efficiency. This suggests that stronger ESG construction leads to a more pronounced promotion of regional green economic efficiency. Secondly, with regards to the mechanism, enterprise ESG influences regional green economic efficiency by facilitating firms’ green technological innovation. Notably, the effect of enterprise ESG on regional green economic efficiency is negatively moderated by environmental regulation. Under the influence of environmental regulation, the positive effect of enterprise ESG on regional green economic efficiency is weakened. This implies that the impact of enterprise ESG on regional green economic efficiency is dampened by environmental regulations. When examining the decomposed variables of regional green economic efficiency, it is found that the significance and direction of enterprise ESG’s effect on both green economic efficiency and green scale efficiency are consistent. This consistency suggests that enterprise ESG has a consistent impact on different aspects of regional green economic efficiency. Moreover, the promoting effect of ESG on regional green economic efficiency is found to be more significant for State-Owned Enterprises (SOEs), enterprises located in economically developed regions, and polluting enterprises. This indicates that these specific types of companies experience a stronger influence from enterprise ESG on regional green economic efficiency. These three conclusions effectively address the three questions posed in the introduction section of this paper: the first question is whether corporate ESG affects the efficiency of the regional green economy; the second question is how corporate ESG influences the efficiency of the regional green economy; the third question is whether the impact of corporate ESG on the efficiency of the regional green economy varies based on company characteristics.

The existing literature on the study of regional green economy efficiency has identified a non-linear relationship between regional green economy efficiency and both the digital economy and environmental regulations. This relationship exhibits an inverted U-shape, as observed from a macro–macro perspective [

64,

65]. On the other hand, research focused on corporate ESG construction suggests a non-linear relationship between ESG construction and intangible assets of the company, displaying an inverted S-shape [

66]. Additionally, companies with better ESG performance tend to have higher stock returns, which can be understood from a micro–micro perspective [

67]. The similarity between this study and existing research lies in their exploration of the economic consequences of ESG construction in enterprises or the factors that influence regional green economy efficiency. The research findings of this paper not only contribute to the existing literature on the study of corporate ESG and green economy efficiency, but also offer a fresh perspective by breaking through the traditional research perspectives that focus solely on micro-to-micro or macro-to-macro relationships. Specifically, this paper explores the impact of corporate ESG construction on regional green economy efficiency from the perspective of micro enterprises, providing theoretical and empirical evidence. The study further investigates the mechanisms through which green innovation and environmental regulations mediate this relationship. By examining how changes in enterprises’ behavioral decision making can influence macroeconomic development, this research emphasizes the importance of companies fulfilling their social responsibilities and presents a new direction for promoting regional green development. Based on the empirical conclusions mentioned above, several suggestions are proposed for practical application.

Initially, the green development of enterprises is crucial for regional green economic development. Corporate ESG construction has been identified as a means to improve regional green economic efficiency. According to the “A-Share ESG Rating Analysis Report 2023” [

68], the ESG level of A-share-listed companies in China is steadily increasing, indicating the growing importance placed on ESG by these companies. However, there is still room for improvement in terms of the professionalism and completeness of ESG information disclosure. Therefore, it is imperative for enterprises to enhance their ESG system and integrate improved ESG practices into their strategic planning for value enhancement and sustainable development. By doing so, enterprises can contribute to their own healthy green development and, consequently, promote regional green economic efficiency. This is particularly significant for non-State-Owned Enterprises (non-SOEs) and enterprises located in underdeveloped regions. These companies can optimize their ESG practices, enhance their image value, attract more investors, and gain access to additional resources. This, in turn, can elevate their ESG performance and further enhance regional green economic efficiency.

The government can play a significant role in promoting regional green economic efficiency by taking several measures. Firstly, increasing subsidies for pollution reduction by polluting enterprises can incentivize them to undertake green and low-carbon transformations, thereby improving their ESG construction. This, in turn, contributes to regional green economic efficiency. To encourage enterprises to prioritize ESG construction, the government could consider establishing a benchmark to reward and subsidize different levels of ESG construction. The growth rate of ESG construction at enterprises, combined with the growth value of regional green economic efficiency and financial budget expenditure, can be used to determine the methods and standards for rewarding and subsidizing ESG construction in different locations. For instance, if a company demonstrates a one-percentage-point increase in its ESG construction level, its tax revenue could decrease by several percentage points or units as a form of reward. These measures create a favorable environment for enterprises to actively engage in ESG construction, contributing to the enhancement of regional green economic efficiency.

In order to promote the construction of enterprise ESG, the government can consider establishing and improving the system for the accounting verification, audit, and mandatory information disclosure of ESG construction. This would effectively compel enterprises to enhance their level of ESG construction. The research findings also indicate that a higher level of enterprise ESG construction is more conducive to promoting regional green economic efficiency. From the perspective of signal transmission theory, in a market economy, the timely and accurate disclosure of enterprise ESG construction information in a legal and compliant manner can influence the decision-making behavior of stakeholders. This, in turn, establishes a market supervision and forcing mechanism for enterprise ESG construction. Simultaneously, a robust ESG construction information disclosure system can play a crucial role in effectively enhancing regional green economic efficiency through ESG construction. By implementing these measures, the government can encourage enterprises to prioritize ESG construction, promote transparency and accountability, and contribute to the overall improvement of regional green economic efficiency.

Currently, the ESG information disclosure system in China remains incomplete, leading to discrepancies between the domestic system and the international mainstream ESG rating system. Consequently, the evaluation of Chinese companies’ ESG performance becomes less objective, making it challenging for investment institutions to comprehensively analyze the risks and values of companies through ESG ratings. Therefore, it is crucial to further enhance the ESG information disclosure system. Improving the ESG information disclosure system is essential to ensure transparency, authenticity, and effectiveness in the disclosure of information. This will help reduce financing costs, strengthen the construction of national innovation platforms, promote corporate green innovation, and enhance regional green economic efficiency. By addressing these issues, China can bridge the gaps in its ESG information disclosure system, align with international standards, and create an environment conducive to the accurate assessment of companies’ ESG performance. This will not only attract more responsible investment, but also contribute to sustainable development and the advancement of the regional green economy.

The study has three main limitations, pertaining to theoretical analysis, sample selection, and data. Firstly, from a theoretical perspective, the analysis may not be exhaustive due to limited knowledge in the field. Secondly, the study focuses solely on Chinese listed companies and lacks analysis of foreign companies. To address this, future research intends to investigate the effectiveness of corporate ESG construction on regional green economic efficiency in other countries. Additionally, a unified ESG rating system is currently unavailable. This study relies on ESG scores from two representative rating agencies, which may limit the sample’s representativeness. Therefore, future research aims to expand the selection of ESG rating agencies to enhance the validity of the conclusions. Lastly, there are limitations in the research data as they only cover information until 2019, primarily due to the significant impact of the pandemic on the Chinese economy. The next step of this study involves updating the empirical research using more recent data.

{kind=link}

{kind=link}

{kind=link}

{kind=link}