The Impact of Dynamic Accounting Information System on Organizational Resilience: The Mediating Role of Business Processes Capabilities

Abstract

1. Introduction

2. Literature Review

2.1. Dynamic AIS Capability

2.2. Business Process Capabilities and Accounting Information System

3. Model Development and Hypotheses

3.1. Dynamic AIS Capability (DAISC) and Organizational Resilience (OR)

3.2. Business Process Capabilities Mediating the Impact of Dynamic AIS Capability on Organizational Resilience (OR)

4. Methodology

4.1. Research Context and Data Collection

4.2. Measurement Items

5. Results

5.1. Common Method Bias

5.2. Assessment of the Reflective Measurement Model

5.3. Assessment of Dynamic AIS Capability as a Formative Second-Order Construct

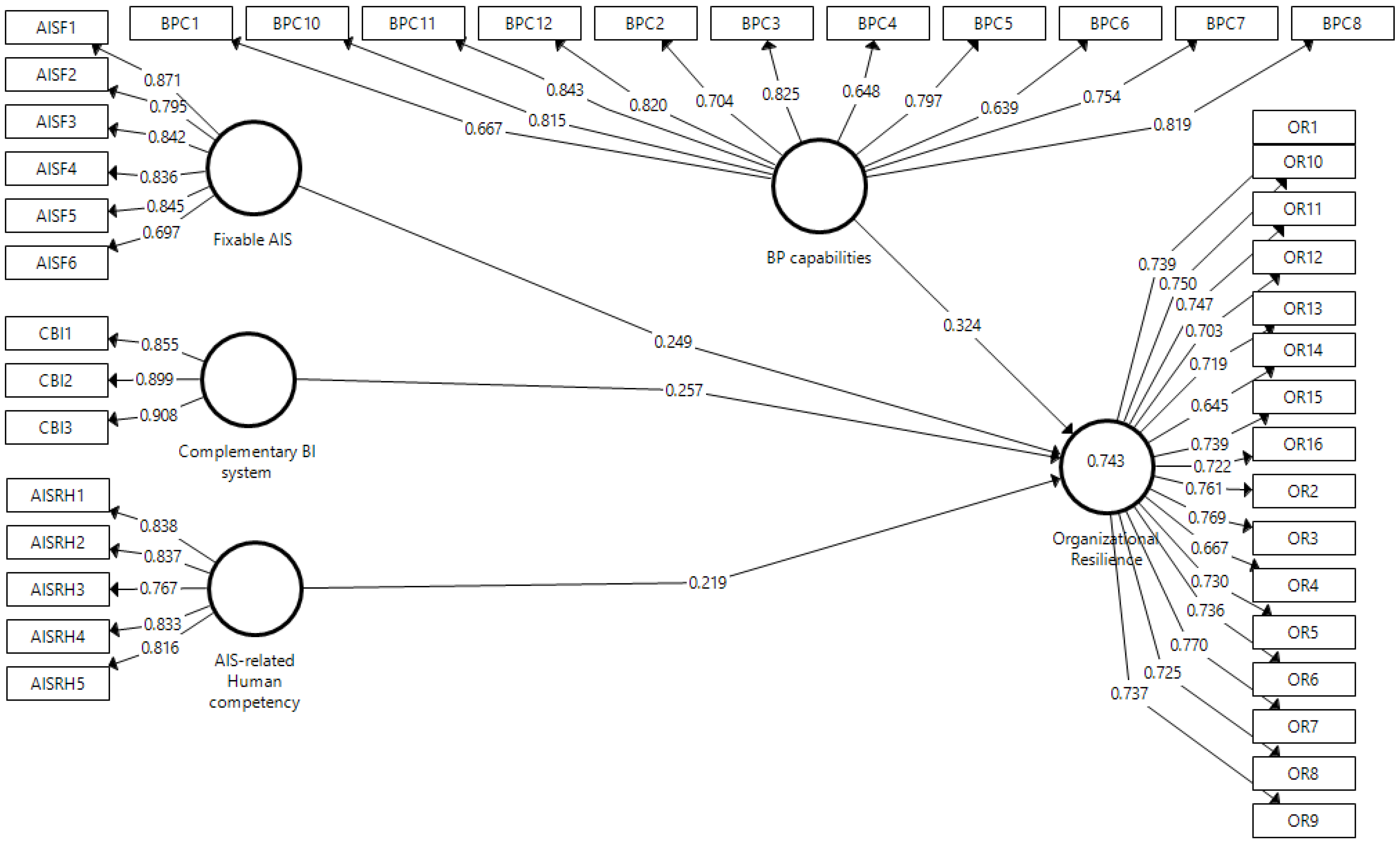

5.4. Assessment of the Structural Model Hypotheses Testing

5.5. Mediation Analysis

6. Discussions and Conclusions

6.1. Theoretical Implications

6.2. Managerial Implications

6.3. Limitations and Avenues for Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

References

- Parker, H.; Ameen, K. The role of resilience capabilities in shaping how firms respond to disruptions. J. Bus. Res. 2018, 88, 535–541. [Google Scholar] [CrossRef]

- Ballesteros, L.; Wry, T.; Useem, M. Halos or Horns. Available online: https://www.semanticscholar.org/paper/Halos-or-Horns-Reputation-and-the-Contingent-to-Ballesteros/26afbf11b0414abc460841bce11f4552e3ee17d2 (accessed on 23 July 2020).

- Mikalef, P.; Pateli, A.; van de Wetering, R. IT architecture flexibility and IT governance decentralisation as drivers of IT-enabled dynamic capabilities and competitive performance: The moderating effect of the external environment. Eur. J. Inf. Syst. 2021, 30, 512–540. [Google Scholar] [CrossRef]

- Quansah, E.; Hartz, D.E.; Salipante, P. Adaptive practices in SMEs: Leveraging dynamic capabilities for strategic adaptation. J. Small Bus. Enterp. Dev. 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Dias, Á.L.; Manuel, E.C.; Dutschke, G.; Pereira, R.; Pereira, L. Economic crisis effects on SME dynamic capabilities. Int. J. Learn. Change 2021, 13, 63–80. [Google Scholar] [CrossRef]

- Bieńkowska, A.; Tworek, K. The moderating role of IT in process of shaping organizational performance by dynamic capabilities of controlling. Appl. Sci. 2021, 11, 889. [Google Scholar] [CrossRef]

- Hernández-Linares, R.; Kellermanns, F.W.; López-Fernández, M.C. Dynamic capabilities and SME performance: The moderating effect of market orientation. J. Small Bus. Manag. 2021, 59, 162–195. [Google Scholar] [CrossRef]

- Chen, Y.; Lin, Z. Business intelligence capabilities and firm performance: A study in China. Int. J. Inf. Manag. 2021, 57, 102232. [Google Scholar] [CrossRef]

- Prasad, A.; Green, P. Organizational competencies and dynamic accounting information system capability: Impact on AIS processes and firm performance. J. Inf. Syst. 2015, 29, 123–149. [Google Scholar] [CrossRef]

- de Gooyert, V. Long term investments in critical infrastructure under environmental turbulence; Dilemmas of infrastructure responsiveness. Sustain. Futures 2020, 2, 100028. [Google Scholar] [CrossRef]

- Gu, J.-W.; Jung, H.-W. The effects of IS resources, capabilities, and qualities on organizational performance: An integrated approach. Inf. Manag. 2013, 50, 87–97. [Google Scholar] [CrossRef]

- Zwyalif, I.M. Success of Accounting Information Systems and Their Impact on the Stages of Crises Management. Dirasat Adm. Sci. 2015, 42, 248–266. [Google Scholar]

- Akpan, E.E.; Johnny, E.; Sylva, W. Dynamic capabilities and organizational resilience of manufacturing firms in Nigeria. Vis. J. Bus. Perspect. 2021, 26, 48–64. [Google Scholar] [CrossRef]

- Khalil, S.; Belitski, M. Dynamic capabilities for firm performance under the information technology governance framework. Eur. Bus. Rev. 2020, 32, 129–157. [Google Scholar] [CrossRef]

- Barbera, C.; Guarini, E.; Steccolini, I. How do governments cope with austerity? The roles of accounting in shaping governmental financial resilience. Account. Audit. Account. J. 2020, 33, 529–558. [Google Scholar] [CrossRef]

- Al-Matari, A.S.; Aziz, K.A.; Amiruddin, R. Conceptualizing a Framework for Understanding the Impact of Dynamic Accounting Information Systems on the Business Processes Capabilities. In Recent Advances in Technology Acceptance Models and Theories; Al-Emran, M., Shaalan, K., Eds.; Springer International Publishing: Cham, Switzerland, 2021; pp. 107–118. [Google Scholar]

- Al-Delawi, A.S.; Ramo, W.M. The impact of accounting information system on performance management. Pol. J. Manag. Stud. 2020, 21, 36–48. [Google Scholar] [CrossRef]

- Aydiner, A.S.; Tatoglu, E.; Bayraktar, E.; Zaim, S. Information system capabilities and firm performance: Opening the black box through decision-making performance and business-process performance. Int. J. Inf. Manag. 2019, 47, 168–182. [Google Scholar] [CrossRef]

- Ahmadi, J.; Letter, T. The Impact Of IT Capability On Company Performance: The Mediating Role Of Business Process Management Capability And Supply Chain Integration Capability. J. Soc. Manag. Tour. Lett. 2021, 2021, 1–16. [Google Scholar]

- Day, G.S. The capabilities of market-driven organizations. J. Mark. 1994, 58, 37–52. [Google Scholar] [CrossRef]

- Wu, L.; Chen, J.-L. Knowledge management driven firm performance: The roles of business process capabilities and organizational learning. J. Knowl. Manag. 2014, 18, 1141–1164. [Google Scholar] [CrossRef]

- Dospinescu, O.; Dospinescu, N. Workaholism in IT: An Analysis of the Influence Factors. Adm. Sci. 2020, 10, 96. [Google Scholar] [CrossRef]

- Romney, M.B.; Steinbart, P.J. Accounting Information Systems; Pearson Education: London, UK, 2015. [Google Scholar]

- Devaraj, S.; Kohli, R. Performance impacts of information technology: Is actual usage the missing link? Manag. Sci. 2003, 49, 273–289. [Google Scholar] [CrossRef]

- Al-Emran, M.; Al-Maroof, R.; Al-Sharafi, M.A.; Arpaci, I. What impacts learning with wearables? An integrated theoretical model. Interact. Learn. Environ. 2020, 1–21. [Google Scholar] [CrossRef]

- Herzallah, F.A.; Al-Sharafi, M.A.; Alajmi, Q.; Mukhtar, M.; Arshah, R.A.; Eleyan, D. Conceptualizing a Model for the Effect of Information Culture on Electronic Commerce Adoption. In Recent Trends in Data Science and Soft Computing; Springer: Cham, Switzerland, 2019; pp. 861–870. [Google Scholar]

- Yoshikuni, A.C.; Galvão, F.R.; Albertin, A.L. Knowledge strategy planning and information system strategies enable dynamic capabilities innovation capabilities impacting firm performance. VINE J. Inf. Knowl. Manag. Syst. 2021; ahead-of-print. [Google Scholar] [CrossRef]

- Kareem, H.M.; Dauwed, M.; Meri, A.; Jarrar, M.t.; Al-Bsheish, M.; Aldujaili, A.A. The Role of Accounting Information System and Knowledge Management to Enhancing Organizational Performance in Iraqi SMEs. Sustainability 2021, 13, 12706. [Google Scholar] [CrossRef]

- Al-Sharafi, M.A.; Arshah, R.A.; Abu-Shanab, E.A.; Alajmi, Q. The Effect of Sustained Use of Cloud-Based Business Services on Organizations’ Performance: Evidence from SMEs in Malaysia. In Proceedings of the 2019 5th International Conference on Information Management (ICIM), Cambridge, UK, 24–27 March 2019; pp. 285–291. [Google Scholar]

- Qasem, Y.A.M.; Abdullah, R.; Yah, Y.; Atan, R.; Al-Sharafi, M.A.; Al-Emran, M. Towards the Development of a Comprehensive Theoretical Model for Examining the Cloud Computing Adoption at the Organizational Level. In Recent Advances in Intelligent Systems and Smart Applications; Al-Emran, M., Shaalan, K., Hassanien, A.E., Eds.; Springer International Publishing: Cham, Switzerland, 2021; Chapter 4; pp. 63–74. [Google Scholar]

- Qiu, J. Analysis of Human Interactive Accounting Management Information Systems Based on Artificial Intelligence. J. Glob. Inf. Manag. (JGIM) 2022, 30, 1–13. [Google Scholar] [CrossRef]

- Yiu, L.D.; Yeung, A.C.; Cheng, T.E. The impact of business intelligence systems on profitability and risks of firms. Int. J. Prod. Res. 2021, 59, 3951–3974. [Google Scholar] [CrossRef]

- Wilden, R.; Gudergan, S.; Akaka, M.; Averdung, A.; Teichert, T. The role of cocreation and dynamic capabilities in service provision and performance: A configurational study. Ind. Mark. Manag. 2019, 78, 43–57. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Teece, D.; Leih, S. Uncertainty, innovation, and dynamic capabilities: An introduction. Calif. Manag. Rev. 2016, 58, 5–12. [Google Scholar] [CrossRef]

- Jiang, Y.; Ritchie, B.W.; Verreynne, M.L. Building tourism organizational resilience to crises and disasters: A dynamic capabilities view. Int. J. Tour. Res. 2019, 21, 882–900. [Google Scholar] [CrossRef]

- Nava, L. Rise from ashes: A dynamic framework of organizational learning and resilience in disaster response. Bus. Soc.Rev. 2022, 127, 299–318. [Google Scholar] [CrossRef]

- Elbashir, M.Z.; Collier, P.A.; Sutton, S.G. Business intelligence systems use to leverage enterprise-wide accounting information in shared data environments. In Proceedings of the European Conference on Accounting Information Systems, Helsinki, Finland, 9–11 June 2011; pp. 1–53. [Google Scholar]

- Bharadwaj, A.S. A resource-based perspective on information technology capability and firm performance: An empirical investigation. MIS Q. 2000, 24, 169–196. [Google Scholar] [CrossRef]

- Duchek, S. Organizational resilience: A capability-based conceptualization. Bus. Res. 2020, 13, 215–246. [Google Scholar] [CrossRef]

- Connor, M.O.; Conboy, K.; Dennehy, D. COVID-19 affected remote workers: A temporal analysis of information system development during the pandemic. J. Decis. Syst. 2021, 31, 1–27. [Google Scholar] [CrossRef]

- Kpurugbara, N.; Akpos, Y.E.; Nwiduuduu, V.G.; Tams-Wariboko, I. Impact of accounting information system on organizational effectiveness: A study of selected small and medium scale enterprises in Woji, Portharcourt. Int. J. Res. Bus. Manag. Account. 2016, 2, 62–72. [Google Scholar]

- Abu Amuna, Y.M.; Al Shobaki, M.J.; Abu-Naser, S.S. The role of knowledge-based computerized management information systems in the administrative decision-making process. J. Inf. Technol. Electr. Eng. 2017, 6, 1–9. [Google Scholar]

- Chae, B.K.; Yang, C.; Olson, D.; Sheu, C. The impact of advanced analytics and data accuracy on operational performance: A contingent resource based theory (RBT) perspective. Decis. Support Syst. 2014, 59, 119–126. [Google Scholar] [CrossRef]

- Yu, W.; Chavez, R.; Jacobs, M.A.; Feng, M. Data-driven supply chain capabilities and performance: A resource-based view. Transp. Res. Part E: Logist. Transp. Rev. 2018, 114, 371–385. [Google Scholar] [CrossRef]

- Danesh, M.H.; Yu, E. Modeling enterprise capabilities with i*: Reasoning on alternatives. In Proceedings of the International Conference on Advanced Information Systems Engineering, Thessaloniki, Greece, 16–20 June 2014; Springer: Berlin/Heidelberg, Germany; pp. 112–123. [Google Scholar]

- Peng, M.W.; Heath, P.S. The growth of the firm in planned economies in transition: Institutions, organizations, and strategic choice. Acad. Manag. Rev. 1996, 21, 492–528. [Google Scholar] [CrossRef]

- Popovič, A.; Hackney, R.; Tassabehji, R.; Castelli, M. The impact of big data analytics on firms’ high value business performance. Inf. Syst. Front. 2018, 20, 209–222. [Google Scholar] [CrossRef]

- Qadir, J.; Ali, A.; ur Rasool, R.; Zwitter, A.; Sathiaseelan, A.; Crowcroft, J. Crisis analytics: Big data-driven crisis response. J. Int. Humanit. Action 2016, 1, 1–21. [Google Scholar] [CrossRef]

- Obeidat, B.Y.; Al-Suradi, M.M.; Masa’deh, R.; Tarhini, A. The impact of knowledge management on innovation: An empirical study on Jordanian consultancy firms. Manag. Res.Rev. 2016, 39, 1214–1238. [Google Scholar] [CrossRef]

- Fahy, J.; Hooley, G. Sustainable competitive advantage in electronic business: Towards a contingency perspective on the resource-based view. J. Strateg. Mark. 2002, 10, 241–253. [Google Scholar] [CrossRef]

- Wade, M.; Hulland, J. The resource-based view and information systems research: Review, extension, and suggestions for future research. MIS Q. 2004, 28, 107–142. [Google Scholar] [CrossRef]

- Banker, R.D.; Bardhan, I.R.; Chang, H.; Lin, S. Plant information systems, manufacturing capabilities, and plant performance. MIS Q. 2006, 30, 315–337. [Google Scholar] [CrossRef]

- Dickinson, J.B. The Role of Business Process Capabilities and Market-Based Assets in Creating Customer Value and Superior Performance. Ph.D. Thesis, Drexel University, Philadelphia, PA, USA, 2009. [Google Scholar]

- Eisenhardt, K.M.; Martin, J.A. Dynamic capabilities: What are they? Strateg. Manag. J. 2000, 21, 1105–1121. [Google Scholar] [CrossRef]

- Weill, P.; Subramani, M.; Broadbent, M. Building IT infrastructure for strategic agility. MIT Sloan Manag. Rev. 2002, 44, 57. [Google Scholar]

- Peng, J.; Quan, J.; Zhang, G.; Dubinsky, A.J. Mediation effect of business process and supply chain management capabilities on the impact of IT on firm performance: Evidence from Chinese firms. Int. J. Inf. Manag. 2016, 36, 89–96. [Google Scholar] [CrossRef]

- Rai, A.; Patnayakuni, R.; Seth, N. Firm performance impacts of digitally enabled supply chain integration capabilities. MIS Q. 2006, 30, 225–246. [Google Scholar] [CrossRef]

- Liang, T.-P.; You, J.-J.; Liu, C.-C. A resource-based perspective on information technology and firm performance: A meta analysis. Ind. Manag. Data Syst. 2010, 110, 1138–1158. [Google Scholar] [CrossRef]

- Karimi, J.; Somers, T.M.; Bhattacherjee, A. The role of information systems resources in ERP capability building and business process outcomes. J. Manag. Inf. Syst. 2007, 24, 221–260. [Google Scholar] [CrossRef]

- Powell, T.C.; Dent-Micallef, A. Information technology as competitive advantage: The role of human, business, and technology resources. Strateg. Manag. J. 1997, 18, 375–405. [Google Scholar] [CrossRef]

- Sun, Z.; Strang, K.; Firmin, S. Business analytics-based enterprise information systems. J. Comput. Inf. Syst. 2017, 57, 169–178. [Google Scholar] [CrossRef]

- Ravichandran, T.; Lertwongsatien, C.; Lertwongsatien, C. Effect of information systems resources and capabilities on firm performance: A resource-based perspective. J. Manag. Inf. Syst. 2005, 21, 237–276. [Google Scholar] [CrossRef]

- Holbeche, L.S. The Agile Organization: How to Build an Innovative, Sustainable and Resilient Business, 1st ed.; Kogan Page Publishers: London, UK, 2015. [Google Scholar]

- Tengblad, S.; Oudhuis, M. The Resilience Framework; Springer: Berlin/Heidelberg, Germany, 2018. [Google Scholar]

- Oh, L.-B.; Teo, H.-H. The impacts of information technology and managerial proactiveness in building net-enabled organizational resilience. In Proceedings of the IFIP International Working Conference on the Transfer and Diffusion of Information Technology for Organizational Resilience, Galway, Ireland, 7–10 June 2006; Springer: Berlin/Heidelberg, Germany; pp. 33–50. [Google Scholar]

- Velu, S.R.; Al Mamun, A.; Kanesan, T.; Hayat, N.; Gopinathan, S. Effect of Information System Artifacts on Organizational Resilience: A Study among Malaysian SMEs. Sustainability 2019, 11, 3177. [Google Scholar] [CrossRef]

- Mithas, S.; Ramasubbu, N.; Sambamurthy, V. How information management capability influences firm performance. MIS Q. 2011, 35, 237–256. [Google Scholar] [CrossRef]

- Rai, A.; Tang, X. Leveraging IT capabilities and competitive process capabilities for the management of interorganizational relationship portfolios. Inf. Syst. Res. 2010, 21, 516–542. [Google Scholar] [CrossRef]

- IşıK, Ö.; Jones, M.C.; Sidorova, A. Business intelligence success: The roles of BI capabilities and decision environments. Inf. Manag. 2013, 50, 13–23. [Google Scholar] [CrossRef]

- Kanellou, A.; Spathis, C. Accounting benefits and satisfaction in an ERP environment. Int. J. Account. Inf. Syst. 2013, 14, 209–234. [Google Scholar] [CrossRef]

- Chen, X.; Siau, K. Impact of business intelligence and IT infrastructure flexibility on competitive performance: An organizational agility perspective. In Proceedings of the Thirty Second International Conference on Information Systems, Shanghai, China, 4–7 December 2011; pp. 1–11. [Google Scholar]

- Ross, J.W.; Beath, C.M.; Goodhue, D.L. Develop long-term competitiveness through IT assets. Sloan Manag. Rev. 1996, 38, 31–42. [Google Scholar]

- Elbashir, M.Z.; Collier, P.A.; Davern, M.J. Measuring the effects of business intelligence systems: The relationship between business process and organizational performance. Int. J. Account. Inf. Syst. 2008, 9, 135–153. [Google Scholar] [CrossRef]

- Ashrafi, A.; Ravasan, A.Z.; Trkman, P.; Afshari, S. The role of business analytics capabilities in bolstering firms’ agility and performance. Int. J. Inf. Manag. 2019, 47, 1–15. [Google Scholar] [CrossRef]

- Lönnqvist, A.; Pirttimäki, V. The measurement of business intelligence. Inf. Syst. Manag. 2006, 23, 32–40. [Google Scholar] [CrossRef]

- Maharjan, A. Business Intelligence in Strategic Management: Study of Automation Modifying the Strategy of Business. Available online: https://www.theseus.fi/handle/10024/267979 (accessed on 23 April 2020).

- Mishra, D.; Luo, Z.; Hazen, B.T. The Role of Informational and Human Resource Capabilities for Enabling Diffusion of Big Data and Predictive Analytics and Ensuing Performance. In Innovation and Supply Chain Management. Contributions to Management Science; Springer: Cham, Switzerland, 2018; pp. 283–302. [Google Scholar]

- Ulrich, D.; Dulebohn, J.H. Are we there yet? What’s next for HR? Hum. Resour. Manag. Rev. 2015, 25, 188–204. [Google Scholar] [CrossRef]

- e Cunha, M.P.; Gomes, E.; Mellahi, K.; Miner, A.S.; Rego, A. Strategic agility through improvisational capabilities: Implications for a paradox-sensitive HRM. Hum. Resour. Manag. Rev. 2020, 30, 100695. [Google Scholar] [CrossRef]

- Chatrakul Na Ayudhya, U.; Prouska, R.; Beauregard, T.A. The impact of global economic crisis and austerity on quality of working life and work-life balance: A capabilities perspective. Eur. Manag. Rev. 2019, 16, 847–862. [Google Scholar] [CrossRef]

- Roepke, R.; Agarwal, R.; Ferratt, T.W. Aligning the IT human resource with business vision: The leadership initiative at 3M. MIS Q. 2000, 24, 327–353. [Google Scholar] [CrossRef]

- Ravichandran, T. Exploring the relationships between IT competence, innovation capacity and organizational agility. J. Strateg. Inf. Syst. 2018, 27, 22–42. [Google Scholar] [CrossRef]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Hesterly, B. Strategic Management and Competitive Advantage; Pearson Education: London, UK, 2012. [Google Scholar]

- Miller, D.; Shamsie, J. The Resource-Based View of the Firm in Two Environments: The Hollywood Film Studios From 1936 to 1965. Acad. Manag.J. 1996, 39, 519–543. [Google Scholar]

- Liu, H.; Ke, W.; Wei, K.K.; Hua, Z. The impact of IT capabilities on firm performance: The mediating roles of absorptive capacity and supply chain agility. Decis. Support Syst. 2013, 54, 1452–1462. [Google Scholar] [CrossRef]

- Amit, R.; Shoemaker, P. Specialized assets and organizational rent. Strateg. Manag. J. 1993, 14, 33–47. [Google Scholar] [CrossRef]

- Aringhieri, R.; Carello, G.; Morale, D. Supporting decision making to improve the performance of an Italian Emergency Medical Service. Ann. Oper. Res. 2016, 236, 131–148. [Google Scholar] [CrossRef]

- Luo, J.; Fan, M.; Zhang, H. Information technology and organizational capabilities: A longitudinal study of the apparel industry. Decis. Support Syst. 2012, 53, 186–194. [Google Scholar] [CrossRef]

- Rahimi, F.; Møller, C.; Hvam, L. Business process management and IT management: The missing integration. Int. J. Inf. Manag. 2016, 36, 142–154. [Google Scholar] [CrossRef]

- Mooney, J.G.; Gurbaxani, V.; Kraemer, K.L. A process oriented framework for assessing the business value of information technology. ACM SIGMIS Database Database Adv. Inf. Syst. 1996, 27, 68–81. [Google Scholar] [CrossRef]

- Jaakkola, M.; Frösén, J.; Tikkanen, H.; Aspara, J.; Vassinen, A.; Parvinen, P. Is more capability always beneficial for firm performance? Market orientation, core business process capabilities and business environment. J. Mark. Manag. 2016, 32, 1359–1385. [Google Scholar] [CrossRef]

- Irfan, M.; Wang, M.; Akhtar, N. Impact of IT capabilities on supply chain capabilities and organizational agility: A dynamic capability view. Oper. Manag. Res. 2019, 12, 113–128. [Google Scholar] [CrossRef]

- Segars, A.; Grover, V. Strategic group analysis: A methodological approach for exploring the industry level impact of information technology. Omega 1994, 22, 13–34. [Google Scholar] [CrossRef]

- Marchalina, L.; Ahmad, H. The Effect of Internal Communication on Employees’ Commitment to Change in Malaysian Large Companies. Bus. Manag. Strategy 2017, 8, 1–17. [Google Scholar] [CrossRef][Green Version]

- Raymond, L.; Magnenat-Thalmann, N. Information Systems in Small Business: Are They Used in Managerial Decisions? Am. J. Small Bus. 1982, 6, 20–26. [Google Scholar] [CrossRef]

- Sedera, D.; Lokuge, S. The role of enterprise systems in innovation in the contemporary organization. In The Routledge Companion to Management Information Systems, 1st ed.; Routledge Companions in Business, Management and Accounting; Galliers, R.D., Stein, M.-K., Eds.; Routledge: London, UK, 2018; pp. 374–391. [Google Scholar] [CrossRef]

- Uwizeyemungu, S.; Raymond, L. Impact of an ERP system’s capabilities upon the realisation of its business value: A resource-based perspective. Inf. Technol. Manag. Account. Rev. 2012, 13, 69–90. [Google Scholar] [CrossRef]

- Torres, R.; Sidorova, A.; Jones, M.C. Enabling firm performance through business intelligence and analytics: A dynamic capabilities perspective. Inf. Manag. 2018, 55, 822–839. [Google Scholar] [CrossRef]

- Terry, A.B.; Douglas, E.T. Measuring the flexibility of information technology infrastructure: Exploratory analysis of a construct. J. Manag. Inf. Syst. 2000, 17, 167–208. [Google Scholar]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.-Y.; Podsakoff, N.P. Common Method Biases in Behavioral Research: A Critical Review of the Literature and Recommended Remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Matthews, L.M.; Matthews, R.L.; Sarstedt, M. PLS-SEM or CB-SEM: Updated guidelines on which method to use. Int. J. Multivar. Data Anal. 2017, 1, 107–123. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Sarstedt, M.; Matthews, L.M.; Ringle, C.M.J. Identifying and treating unobserved heterogeneity with FIMIX-PLS: Part I–method. Eur. Bus. Rev. 2016, 28, 63–76. [Google Scholar] [CrossRef]

- Arpaci, I.; Al-Emran, M.; Al-Sharafi, M.A.; Shaalan, K. A Novel Approach for Predicting the Adoption of Smartwatches Using Machine Learning Algorithms. In Recent Advances in Intelligent Systems and Smart Applications; Al-Emran, M., Shaalan, K., Hassanien, A.E., Eds.; Studies in Systems, Decision and Control; Springer International Publishing: Cham, Switzerland, 2021; Chapter 10; pp. 185–195. [Google Scholar]

- Al-Sharafi, M.A.; Al-Qaysi, N.; Iahad, N.A.; Al-Emran, M. Evaluating the sustainable use of mobile payment contactless technologies within and beyond the COVID-19 pandemic using a hybrid SEM-ANN approach. Int. J. Bank Mark. 2021. [Google Scholar] [CrossRef]

- Alshaafee, A.A.; Iahad, N.A.; Al-Sharafi, M.A. Benefits or Risks: What Influences Novice Drivers Regarding Adopting Smart Cars? Sustainability 2021, 13, 11916. [Google Scholar] [CrossRef]

- Al Sharafi, M.A.; Herzallah, F.A.; Alajmi, Q.; Mukhtar, M.; Arshah, R.A.; Eleyan, D. Information culture effect on e-commerce adoption in small and medium enterprises: A structural equation modelling approach. Int. J. Bus. Inf. Syst. 2020, 35, 415–438. [Google Scholar] [CrossRef]

- Qasem, Y.A.M.; Asadi, S.; Abdullah, R.; Yah, Y.; Atan, R.; Al-Sharafi, M.A.; Yassin, A.A. A Multi-Analytical Approach to Predict the Determinants of Cloud Computing Adoption in Higher Education Institutions. Appl. Sci. 2020, 10, 4905. [Google Scholar] [CrossRef]

- Al-Sharafi, M.A.; Mufadhal, M.E.; Arshah, R.A.; Sahabudin, N.A. Acceptance of online social networks as technology-based education tools among higher institution students: Structural equation modeling approach. Sci. Iran. 2019, 26, 136–144. [Google Scholar]

- Al-Emran, M.; Granić, A.; Al-Sharafi Mohammed, A.; Ameen, N.; Sarrab, M. Examining the roles of students’ beliefs and security concerns for using smartwatches in higher education. J. Enterp. Inf. Manag. 2020, 34, 1229–1251. [Google Scholar] [CrossRef]

- Ayyash, M.M.; Herzallah, F.A.T.; Al-Sharafi, M.A. Arab cultural dimensions model for e-government services adoption in public sector organisations: An empirical examination. Electron. Gov. Int. J. 2022, 18, 9–44. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modeling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Ringle, C.M.; Sarstedt, M.; Straub, D. A critical look at the use of PLS-SEM in MIS Quarterly. MIS Q. 2012, 36, iii-xiv. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage Publications: Thousand Oaks, CA, USA, 2016. [Google Scholar]

- Kock, N. Common method bias in PLS-SEM: A full collinearity assessment approach. Int. J. e-Collab. (IJeC) 2015, 11, 1–10. [Google Scholar] [CrossRef]

- Preacher, K.J.; Hayes, A.F. Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behav. Res. Methods 2008, 40, 879–891. [Google Scholar] [CrossRef]

- Gao, P.; Zhang, J.; Gong, Y.; Li, H. Effects of technical IT capabilities on organizational agility. Ind. Manag. Data Syst. 2020, 120, 941–961. [Google Scholar] [CrossRef]

- Bustinza, O.F.; Vendrell-Herrero, F.; Perez-Arostegui, M.N.; Parry, G. Technological capabilities, resilience capabilities and organizational effectiveness. Int. J. Hum. Resour. Manag. 2019, 30, 1370–1392. [Google Scholar] [CrossRef]

- Aydiner, A.S.; Tatoglu, E.; Bayraktar, E.; Zaim, S.; Delen, D. Business analytics and firm performance: The mediating role of business process performance. J. Bus. Res. 2019, 96, 228–237. [Google Scholar] [CrossRef]

- Ray, G.; Barney, J.B.; Muhanna, W.A. Capabilities, business processes, and competitive advantage: Choosing the dependent variable in empirical tests of the resource-based view. Strateg. Manag. J. 2004, 25, 23–37. [Google Scholar] [CrossRef]

- Grant, R.M. Prospering in dynamically-competitive environments: Organizational capability as knowledge integration. Organ. Sci. 1996, 7, 375–387. [Google Scholar] [CrossRef]

- Pavlou, P.A.; El Sawy, O.A. From IT leveraging competence to competitive advantage in turbulent environments: The case of new product development. Inf. Syst. Res. 2006, 17, 198–227. [Google Scholar] [CrossRef]

- Wu, F.; Yeniyurt, S.; Kim, D.; Cavusgil, S.T. The impact of information technology on supply chain capabilities and firm performance: A resource-based view. Ind. Mark. Manag. 2006, 35, 493–504. [Google Scholar] [CrossRef]

- Chang, K.; Kettinger, W.J.; Zhang, C. Assimilation of enterprise systems: The mediating role of information integration of information impact. ICIS Proc. 2009, 1–12. [Google Scholar]

- Mikalef, P.; Pateli, A. Information technology-enabled dynamic capabilities and their indirect effect on competitive performance: Findings from PLS-SEM and fsQCA. J. Bus. Res. 2017, 70, 1–16. [Google Scholar] [CrossRef]

- Barreto, I. Dynamic capabilities: A review of past research and an agenda for the future. J. Manag. 2010, 36, 256–280. [Google Scholar] [CrossRef]

- Sabahi, S.; Parast, M.M. Firm innovation and supply chain resilience: A dynamic capability perspective. Int. J. Logist. Res. Appl. 2020, 23, 254–269. [Google Scholar] [CrossRef]

- Ochie, C.; Nyuur, R.B.; Ludwig, G.; Cunningham, J.A. Dynamic capabilities and organizational ambidexterity: New strategies from emerging market multinational enterprises in Nigeria. Int. Bus. Rev. 2022, 1–17. [Google Scholar] [CrossRef]

- Hu, Y.-P.; Chang, I.-C.; Hsu, W.-Y. Mediating effects of business process for international trade industry on the relationship between information capital and company performance. Int. J. Inf. Manag. 2017, 37, 473–483. [Google Scholar] [CrossRef]

- Lu, Y.; Ramamurthy, K. Understanding the link between information technology capability and organizational agility: An empirical examination. MIS Q. 2011, 35, 931–954. [Google Scholar] [CrossRef]

- Chen, X.; Siau, K. Business analytics/business intelligence and IT infrastructure: Impact on organizational agility. J. Organ. End User Comput. 2020, 32, 138–161. [Google Scholar] [CrossRef]

{kind=link}

| Frequency | Percent | Valid Percent | Cumulative Percent | |

|---|---|---|---|---|

| CFO | 66 | 45.8 | 45.8 | 45.8 |

| CIO | 13 | 9.0 | 9.0 | 54.9 |

| Director of MIS | 13 | 9.0 | 9.0 | 63.9 |

| Senior System Analyst | 7 | 4.9 | 4.9 | 68.8 |

| Database Administration Director | 3 | 2.1 | 2.1 | 70.8 |

| Other | 42 | 29.2 | 29.2 | 100.0 |

| Total | 144 | 100.0 | 100.0 |

| Constructs | Items | Loadings | CA | CR | AVE |

|---|---|---|---|---|---|

| Fixable AIS | AISF1 | 0.871 | 0.899 | 0.923 | 0.667 |

| AISF2 | 0.795 | ||||

| AISF3 | 0.842 | ||||

| AISF4 | 0.836 | ||||

| AISF5 | 0.845 | ||||

| AISF6 | 0.697 | ||||

| AIS-related Human Competency | AISRH1 | 0.838 | 0.877 | 0.910 | 0.670 |

| AISRH2 | 0.837 | ||||

| AISRH3 | 0.767 | ||||

| AISRH4 | 0.833 | ||||

| AISRH5 | 0.816 | ||||

| BP Capabilities | BPC1 | 0.667 | 0.926 | 0.937 | 0.579 |

| BPC10 | 0.815 | ||||

| BPC11 | 0.843 | ||||

| BPC12 | 0.820 | ||||

| BPC2 | 0.704 | ||||

| BPC3 | 0.825 | ||||

| BPC4 | 0.648 | ||||

| BPC5 | 0.797 | ||||

| BPC6 | 0.639 | ||||

| BPC7 | 0.754 | ||||

| BPC8 | 0.819 | ||||

| Complementary BI System | CBI1 | 0.855 | 0.865 | 0.918 | 0.788 |

| CBI2 | 0.899 | ||||

| CBI3 | 0.908 | ||||

| Organizational Resilience | OR1 | 0.739 | 0.941 | 0.948 | 0.532 |

| OR10 | 0.750 | ||||

| OR11 | 0.747 | ||||

| OR12 | 0.703 | ||||

| OR13 | 0.719 | ||||

| OR14 | 0.645 | ||||

| OR15 | 0.739 | ||||

| OR16 | 0.722 | ||||

| OR2 | 0.761 | ||||

| OR3 | 0.769 | ||||

| OR4 | 0.667 | ||||

| OR5 | 0.730 | ||||

| OR6 | 0.736 | ||||

| OR7 | 0.770 | ||||

| OR8 | 0.725 | ||||

| OR9 | 0.737 |

| AIS-Related Human Competency | BP Capabilities | Complementary BI System | Fixable AIS | Organizational Resilience | |

|---|---|---|---|---|---|

| AIS-related Human Competency | |||||

| BP Capabilities | 0.523 | ||||

| Complementary BI System | 0.715 | 0.518 | |||

| Fixable AIS | 0.796 | 0.599 | 0.697 | ||

| Organizational Resilience | 0.772 | 0.729 | 0.767 | 0.798 |

| Path | VIF |

|---|---|

| AIS-related Human Competency | 2.289 |

| Complementary BI system | 1.814 |

| Flexible AIS | 2.258 |

| Relationship | Path Coefficients | T Statistics | p-Value |

|---|---|---|---|

| AIS-related Human Competency -> Dynamic AIS Capability | 0.286 | 2.713 | 0.003 |

| Complementary BI System -> Dynamic AIS Capability | 0.344 | 4.046 | 0.000 |

| Flexible AIS -> Dynamic AIS Capability | 0.506 | 4.849 | 0.000 |

| H | Path | Path Coefficient | t-Value | p-Value | f2 | R2 | Q2 |

|---|---|---|---|---|---|---|---|

| H1 | Dynamic AIS Capability -> Organizational Resilience | 0.632 | 8.094 | 0.000 | 1.037 | 0.736 | 0.376 |

| H1.1 | AIS-related Human Competency -> Organizational Resilience | 0.219 | 3.470 | 0.000 | 0.081 | ||

| H1.2 | Complementary BI System -> Organizational Resilience | 0.257 | 3.825 | 0.000 | 0.138 | ||

| H1.2 | Fixable AIS -> Organizational Resilience | 0.249 | 3.714 | 0.000 | 0.098 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Al-Matari, A.S.; Amiruddin, R.; Aziz, K.A.; Al-Sharafi, M.A. The Impact of Dynamic Accounting Information System on Organizational Resilience: The Mediating Role of Business Processes Capabilities. Sustainability 2022, 14, 4967. https://doi.org/10.3390/su14094967

Al-Matari AS, Amiruddin R, Aziz KA, Al-Sharafi MA. The Impact of Dynamic Accounting Information System on Organizational Resilience: The Mediating Role of Business Processes Capabilities. Sustainability. 2022; 14(9):4967. https://doi.org/10.3390/su14094967

Chicago/Turabian StyleAl-Matari, Ahmed Saleh, Rozita Amiruddin, Khairul Azman Aziz, and Mohammed A. Al-Sharafi. 2022. "The Impact of Dynamic Accounting Information System on Organizational Resilience: The Mediating Role of Business Processes Capabilities" Sustainability 14, no. 9: 4967. https://doi.org/10.3390/su14094967

APA StyleAl-Matari, A. S., Amiruddin, R., Aziz, K. A., & Al-Sharafi, M. A. (2022). The Impact of Dynamic Accounting Information System on Organizational Resilience: The Mediating Role of Business Processes Capabilities. Sustainability, 14(9), 4967. https://doi.org/10.3390/su14094967