1. Introduction

The energy transition is a process aimed at reducing energy demand that implies a profound transformation for citizens in terms of both economic and lifestyle. According to the scientific community, climate change in recent decades is largely due to greenhouse gas emissions from the energy sector. In fact, it is estimated that 90% of CO

2 emissions into the atmosphere come from this sector. Therefore, the main objective of the energy transition is to progressively replace fossil fuel sources with clean and renewable energy [

1]. New forms of energy supply are constantly tested to reduce the use of fossil fuels in various sectors [

2]. In recent years, the use of renewable energies is significantly increasing due to support policies and progressive cost reduction [

3]. The energy transition favors the economy of sectors that make use of renewable resources and penalizes, instead, those related to the production and consumption of fossil fuels [

4]. The main benefits of the energy transition include the reduction of greenhouse gas emissions, the increase in jobs in the green energy sector, and the reduction in the cost of electricity.

In the countries of the European Union (EU), the main greenhouse gas emissions come from the construction sector. Most of the residential buildings were built more than 25 years ago, so they are inefficient from an energy point of view. In 2021, in countries such as France, Belgium, and Italy, the demand for primary energy in the construction sector was about 40% of the total energy required. Also in Europe, from 2011 to 2021 the construction sector was responsible for about 36% of greenhouse gas emissions [

5]. Given the importance of the issue, it became necessary to implement new political tools to create decarbonized smart cities that use green technologies [

6]. Among the most recent regulatory instruments, it is worth noting the Commission Recommendation (EU) 2019/1658 of 25 September 2019. The goals of the directive are to reduce greenhouse gas emissions by at least 40% by 2030 compared to 1990, increase the use of renewable energy, achieve ambitious energy savings, and improve energy security and sustainability. To this end, new incentive policies aimed at the renovation of residential buildings are introduced in Europe [

7]. These measures encourage the use of renewable energy sources in the building sector to improve the energy efficiency of housing units [

8]. Thanks to government funding, the energy transition objectives are now more easily achievable [

9,

10]. In Italy, two regulatory packages have recently been launched in which the energy transition plays a central role. The first is the Integrated National Plan for Energy and Climate (PNIEC), which has implemented the indications of the European Union on issues such as energy-saving, reduction of CO

2 emissions, and the use of renewable and sustainable energy sources. The second is the National Recovery and Resilience Plan (PNRR), through which over 60 billion euros are financed to promote the energy requalification of buildings, sustainable mobility, the circular economy, the protection of water resources, and sustainable agriculture [

11,

12]. Thanks to the aforementioned plans, Italy is progressively decreasing its dependence on fossil fuels and increasing the production of renewable energy [

13]. In fact, the share of green electricity is constantly increasing year after year. As of 2021, more than a third of total electricity production is derived from renewable sources (mainly photovoltaic, hydroelectric, wind, and geothermal). Wind power is growing strongly, although photovoltaics remains the main renewable source of energy used. In particular, the production of wind energy grew by 24%, hydroelectric by 5%, and geo-thermoelectric by 1%. About the installation of photovoltaic systems, a more contained growth was recorded compared to a few years ago (+6.4%) [

14]. Nonetheless, photovoltaics remains the main renewable source used in the residential sector to make the real estate portfolio more sustainable from a technical, environmental, and financial point of view. In recent years, Building Integrated Photovoltaics (BIPV) has reached the technological and market maturity necessary to achieve the energy and climate objectives established by national and Community regulations [

15]. However, when the installation of a photovoltaic system is combined with other energy efficiency interventions (for instance, insulation of the building envelope, replacement of fixtures, installation of solar screens, etc.) the overall cost of the works increases considerably. In this case, the benefits deriving from savings in bills do not always cover the cost of the interventions in a reasonably short time. This is why it is currently very difficult to carry out complete energy interventions on the real estate portfolio without resorting to forms of state incentives, such as building bonuses. However, it must be considered that many of the government incentives are temporary measures of limited duration. Furthermore, building bonuses represent a considerable cost for the state and indirectly contribute to the increase in the prices of building materials.

With this paper, we intend to analyze the financial consequences of the energy transition in housing for the owners of apartments located in the Campania region (Italy). The goal is to evaluate through the Cost-Revenue Analysis (CRA) the level of financial sustainability of the energy retrofit projects, which include photovoltaic systems, to be built on multi-story and multi-apartment buildings. In addition, we want to estimate the incidence of photovoltaic technology on the overall financial performance of energy efficiency interventions. The financial analysis is conducted on a representative multi-family building whose characteristics (structural type, time of construction, number of floors, number of real estate units, etc.) are those most frequently found in Campania. In particular, the representative building was selected from a set of buildings on which energy retrofit projects have been carried out in the last two years, whose economic-financial feasibility was assessed by the authors of this study. The energy redevelopment interventions hypothesized in the representative building are also those most frequently carried out in Campania.

The main contributions of this paper are the following:

Evaluate for a representative multi-apartment building the financial feasibility of an ordinary energy retrofit project that includes, among other interventions, the installation of solar photovoltaic systems for private and condominium use;

Evaluate how the financial performance of an ordinary energy efficiency project varies in the presence and absence of solar photovoltaic systems;

Identify, through sensitivity analysis, the main cost components of the BIPV technology capable of significantly influencing the overall financial performance of an ordinary energy retrofit project;

Identify the two extreme scenarios (more pessimistic and more optimistic) and their relative financial performances;

Provide a probabilistic estimate, through risk analysis, of the probability of failure of an ordinary energy retrofit project including solar photovoltaic systems;

Demonstrate whether it is currently possible to carry out energy retrofit interventions in Italy that are financially sustainable without necessarily resorting to forms of state subsidies;

Provide an updated view on the savings on the bill deriving from ordinary energy retrofit interventions for private owners of multi-family residential properties in Campania.

The analyses described are conducted concerning the following two basic design hypotheses:

Energy efficiency intervention of the building envelope without providing for the installation of solar photovoltaic systems;

Energy efficiency intervention of the building envelope including the installation of photovoltaic solar systems for private and condominium use.

The main financial performance indicators of the project are estimated for both of the project hypotheses. Furthermore, for the second hypothesis, the Monte Carlo simulation is implemented in order to evaluate the probability of financial failure of the intervention.

The results obtained can play an important role in energy policy at the regional and national levels, as a knowledge base is offered about the current scenario of energy requalification of multi-family buildings.

This study is in continuity with another recent work, in which the point of view of the company carrying out the works is analyzed (only in the case in which tax incentives and subsidized credits are used).

The work is structured as follows:

Section 2 is dedicated to the analysis of the literature;

Section 3 describes the methodological approach followed;

Section 4 presents the main results of the study and their discussion;

Section 5 shows the main conclusions and future research ideas.

3. Methods

To assess the financial convenience of the energy retrofit project on the representative building, the cost-revenue analysis (CRA) was used. The starting point was the preparation of an estimative metric computation, elaborated considering the ordinary three phases that distinguish it, summarized below [

40]:

Classification: The phase in which the work to be carried out is divided into all its components, up to the most elementary ones (Work Breakdown Structure—WBS). The structure undergoes a virtual process of disaggregation into its individual parts, so as to be able to identify the necessary processing items. The result obtained is a list of articles referring to the various work items;

Measurement: In this phase, the works to be carried out are quantified according to their unit of measurement. The measurement standards must contain an indication of the geometric or physical size, the unit of measurement, the method of measurement, the elements to be excluded;

Estimation of unit prices: A phase that includes two operating modes:

Estimation through ordinary price lists (synthetic estimate): Generally, we use price lists provided by administrative bodies, chambers of commerce, professional orders, or specialist price lists by type of construction. These price lists are based on the principle of ordinariness, so the prices they contain are standardized by type of work and geographical areas. In these documents, only the most common processes are reported and the relative unit prices represent the most frequently adopted. In the case in question, prices borrowed from regional or DEI (Building Authority Typography) price lists are allowed;

Estimation through price analysis (analytical estimate): In the case of extraordinary processing, the production factors that contribute to the production of the individual elements are identified and the unit prices of these factors are defined. The elements that are examined are labor, materials, rentals, and transport. The basic indications can be found through periodic publications of the Building Authority (Genio Civile). The sum of these three rates constitutes the so-called technical cost. To the latter must be added a representative increase in the company’s overheads (generally between 13% and 17%). Finally, a further increase of 10% is applied to the new total for the consideration to be given to the entrepreneur [

41].

Once the works and the respective unitary and total prices were defined, we moved on to the drafting of the project’s economic framework. The costs of safety, technical expenses, general expenses, VAT, and other taxes, as well as all the items provided for by Presidential Decree no. 207/2010, have been added to the amount of the works.

The estimate of the financial discount rate to be applied in the CRA is a crucial aspect. This is why the reference was made to the review work carried out by ref. [

42] on the models adopted in the literature to estimate the discount rate for energy retrofit projects in buildings. The authors admit that households’ goal is to reduce operating costs of energy efficiency interventions. This is why property owners bear initial costs in the present and plan to recover their investment in the future thanks to savings in their bills. Therefore, the discount rate represents the time preference rate of the households. Generally, the rate is estimated by approximating the long-term preference of households to the long-term average yield on Treasury bills. This was done in the financial analysis in ref. [

43], where the estimated rate is 5%. From the analysis of the literature, it emerges that the discount rate estimates vary according to three intervals: high rates (5.5–7.5%) can be found in the literature that deals with the behavior of owner families; intermediate rates (3.5–5.5%) generally refer to the companies involved in the execution of energy requalification operations; low rates (0–3.5%) are obtained when it is decided to incorporate the intergenerational effects in a perspective of social and environmental sustainability (social discount rate). Hence, in our case, a high rate is expected. Ref. [

44] suggests a variable rate from 3.0% to 5.5% in the case of an analysis conducted from the point of view of the households, and a variable rate from 1.8% to 4.5% in the case of an analysis conducted by point of view of energy requalification companies. The International Energy Agency [

45] suggests a wider range, from 5% to 10%, regardless of the stakeholder involved. According to ref. [

46], households’ time preference rates are overestimated, as are the returns on investments in energy efficiency. For this reason, in this paper, we have preferred to estimate the discount rate with the Weighted Average Cost of Capital (WACC) method. It is shown that for the case in question the result obtained with the WACC is in line with the individual time preference assay estimated by ref. [

43], noting a perception of risk for households that is not very different from that of businesses. To estimate the expected return on equity capital, the Damodaran database was consulted in order to define the risk premium and the market risk of the reference sector in Italy [

47]. As regards the latter, given the nature of the project, it was preferred to estimate it by averaging the β

u (beta unlevered) of the following sectors: engineering/construction, environmental services, and waste, green and renewable energy, homebuilding (see

Table 1). It is assumed that the risk of the project is similar to that of the sector.

We passed from unlevered beta (β

u) to levered beta (β

l) through the following formula:

where the values of the equity (E) and of the debt (D) for the specific project are known. In particular, it is assumed that the equity invested in the project by the private owners of the real estate units amounts to 30% of the amount of the work. The remaining 70% is financed by a bank at an r

D interest rate (ten-year loan term).

Defined β

l, which measures the market risk of the reference sector, the method of the Capital Asset Pricing Model (CAPM) is used to estimate the expected return on equity:

where r

f is the risk-free interest rate, set equal to the average return on Italian multi-year Treasury bills with a ten-year duration, r

M is the market yield, r

M − r

f is the risk premium [

48,

49,

50]. It was possible to estimate the discount rate r of the project by implementing the CAPM formula:

where

t represents the marginal tax rate.

Table 2 shows the data needed to estimate the WACC.

The values of D and E in

Table 2 refer to the second project hypothesis, which is to that including the photovoltaic system. In the case of the absence of the photovoltaic system, the financial structure of the project changes very little, essentially leading to the same value of the discount rate.

The project business plan is structured in 20 years, at the end of which it is assumed that new restructuring interventions are required.

Once the structure of the Business Plan has been established, it is possible to use the Cost-Revenue Analysis (CRA) to verify the financial performance of the project. Once the costs and revenues that the project is able to generate over time have been defined, it is possible to estimate the synthetic indicators of profitability, such as the Net Present Value (NPV), the Internal Rate of Return (IRR), and the Payback Period (PP) [

51,

52,

53]. The analysis of the performance indicators was carried out considering two design hypotheses: (i) energy efficiency intervention of the building envelope without providing for the installation of photovoltaic solar systems; (ii) energy efficiency intervention of the building envelope including the installation of solar photovoltaic systems for both private and condominium use. As regards the latter case, it was decided to implement a sensitivity analysis. It allows you to identify the variables that most influence the performance indicator (in the case in question, the NPV was chosen as the performance indicator). Sensitivity analysis is a prediction of how a specific percentage change in a critical variable leads to a consequent percentage change in the performance indicator [

54,

55]. In the case in question, the following critical variables are identified:

The cost of the single photovoltaic panel;

The cost of installing the systems;

The cost of the inverter;

The cost of the storage system;

The cost of the heat pump;

Average percentage savings in the bill resulting from the use of photovoltaic technology.

By varying several critical variables at the same time, we then moved on to the analysis of two extreme scenarios: (i) the most pessimistic scenario, in which the critical variables affect the project NPV in the most negative way possible; (ii) the most optimistic scenario, in which the critical variables influence the project NPV as positively as possible.

Finally, a risk analysis was implemented in probabilistic terms. Once the critical variables of the project were defined in the previous step, a probability distribution is associated with each of them. A stochastic description of the risky variables is then made. The goal is to evaluate how the probability distribution of the NPV changes with the simultaneous variation of the critical variables. The described analysis is conducted through the Monte Carlo simulation. The method defines a probabilistic distribution for each variable that has intrinsic randomness. The calculation is performed with many thousands of iterations, each of which reproduces the result (NPV) corresponding to a set of values of the sensitive variables, oscillating randomly in the probabilistic analysis interval defined for each of them. A limitation of the method is that it generally does not consider the interdependencies of uncertain variables. In the subsequent risk assessment phase, the probability of project failure, expressed in terms of the cumulative frequency distribution of the performance indicator, is compared with a threshold value considered optimal (in the case in question, the probability of obtaining a positive NPV is evaluated) [

56,

57,

58].

The results of the analyses described in this paragraph are reported in the next section.

4. Results and Discussion

The representative multi-apartment building has the following characteristics: construction period between 1960 and 1970, structure framed in reinforced concrete, number of levels equal to 8 (including one underground level), number of real estate units equal to 22, average floor area of 250 m2, energy class G.

The energy retrofit interventions that are ordinarily performed on multi-apartment residential properties in Campania are as follows: replacement of the old boilers with the condensing model, replacement of traditional fixtures with thermal break models, installation of solar shading, insulation of the building envelope (structures horizontal and vertical opaque). The ordinary intervention on the building type object of analysis is able to improve energy performance by ensuring the jump of two energy classes. These interventions are also often combined with the installation of photovoltaic solar panels at the service of common and private parts, ensuring even higher energy performance.

Table 3 shows the summary of the macro-categories and categories of intervention [

59].

Table 4 shows the amounts of each macro-category of work (which include the respective share of the safety costs) and the summary from the project’s economic framework.

In the event of the absence of a photovoltaic system, the project’s total amount goes from 1,006,336.65 euros to 962,118.19 euros. The following subsections show the business plans in the two hypotheses of the absence and presence of the photovoltaic system.

4.1. Business Plan and CRA in the Absence of a Photovoltaic System

Table 5 shows the business plan of the energy efficiency project. In the first instance, the installation of the photovoltaic solar system is considered absent.

The estimated savings in the bill refers to the average figure built with respect to the set of projects carried out in the Campania region in recent years and followed by the authors of this study. In class G buildings, average consumption can reach about 162 kWh per m2 per year. This implies that for an apartment of 80 m2 the annual consumption is about 13,000 kWh, which translates into an expense in the bill of about 145 euros per month. The described efficiency interventions, if carried out on a building that has characteristics comparable to the representative one, are able to guarantee the jump of two energy classes. From the empirical experience it is clear that for each class jump, a savings of about 20% is obtained in the bill (i.e., 40% in the case of a jump of two classes). As a result, an overall annual saving of about €15,840 is obtained for the entire building, that is, about €720 per year per property unit.

The performance indicators estimated through the CRA are shown in

Table 6.

Considering a time horizon of 20 years (beyond which it is assumed that new restructuring interventions are required), we obtain a negative NPV. The intervention is therefore unsustainable. One begins to have a positive NPV only from the 24th year.

4.2. Business Plan and CRA in the Presence of a Photovoltaic System

If the photovoltaic system is present, the respective cost of which is shown in

Table 3, the business plan to be considered is that of

Table 7.

The performance indicators estimated through the CRA are shown in

Table 8.

The hypothesized system is 6 kW and includes components such as storage, inverter, and heat pump. Photovoltaics can significantly contribute to the reduction of energy consumption and the reduction of the electricity bill, especially if the heating and domestic hot water are produced with electricity, for example via a condensing boiler. In all other cases, the energy improvement is marginal, or in the order of 2–4%. By this, the project assumes the presence of a hybrid system (condensing boiler/heat pump/photovoltaic), capable of increasing the savings on the bill by 6% on average. In any case, the self-consumption of the energy produced through the system adopted is not a determining factor for a further increase in the energy class. However, it remains clear that, in the case in question, the payback time is reduced by four years. At the end of the 20th year, we get a positive NPV equal to 723.17 euros. Although the savings in the bill (equal to about 828 euros per year per property unit) is greater than in the previous hypothesis, the investment is still far from being defined as financially sustainable [

60].

4.3. Sensitivity Analysis

For the second design hypothesis (presence of the photovoltaic system) the sensitivity analysis was implemented. Usually, those variables are considered sensitive which, increased or decreased by 1%, contribute to an increase or decrease in the performance indicator by more than 1%. The total cost of a 6 kW photovoltaic system with storage and heat pump depends on the price of the various components. From the analysis of the set of energy retrofit projects, carried out in Campania in the last two years and assessed on an economic-financial level by the authors of this study, the following price ranges per component were found:

Cost of a single photovoltaic panel: it depends on numerous factors (technology, quality, module efficiency, power, size). Polycrystalline and mono-crystalline modules are the cheapest (starting from 70–90 euros per panel), while for high-efficiency modules it can go up to 200–250 euros per panel.

Cost of installation of the systems: generally for a 6 kW system it varies between 600 and 900 euros. Any system maintenance costs are not included in the calculation.

Cost of the inverter: the average cost for a 6 kW photovoltaic inverter is approximately 900–1000 euros for a single-phase model, while for a three-phase device it is approximately 1100–1200 euros.

Cost of the storage system: depends on the technology and storage capacity. A 9.6 kWh lithium storage system suitable for a 6 kW photovoltaic system can cost around 10,000 euros, dropping to 7000–8000 euros for 7.2 kWh lithium batteries.

Cost of the heat pump: varies according to the size and type of system. From the analysis conducted, it was found to be between 6000 and 8000 euros.

Another sensitive variable taken into consideration is the percentage savings in the bill resulting from the installation of the photovoltaic system. The estimation was carried out following three different approaches. First, a reference was made to the estimations of energy performances made by the energy certifiers on the projects taken as a reference (from which the representative building was defined). Secondly, the estimates obtained were compared with the actual energy savings achieved in previous years in the same geographical area following the installation of photovoltaic systems. Thirdly, reference was made to the scientific literature on the subject (for example, the works of ref. [

61] and ref. [

62]) to validate the estimated values. For the representative building, the percentage savings in the bill determined by photovoltaics varies between 2% and 10%. The central value (6%) was assumed to be the most probable. This result is in line with the study conducted by ref. [

62] in the Italian context.

Once the sensitive variables were defined, the sensitivity analysis was implemented by making the critical predictors assume the maximum and minimum values and estimating the NPV each time. The results are reported in

Table 9.

Due to the particular structure of cash flows (which from positive become negative due to the presence of the bank loan at the beginning of the first year), the logic of the IRR is reversed. The project is convenient when the IRR is lower than the discount rate of the project. To avoid misunderstandings, it was therefore decided to follow only the NPV criterion to evaluate the investment performance.

The cost component that most influences (both positively and negatively) the financial performance of the project is that linked to the storage system. To follow, we have the cost of the single panel and the cost of the heat pump. The installation cost and the cost of the inverter represent the least influencing sensitive variables and affect financial performance equally both negatively and positively.

4.4. Scenario Analysis

Still referring to the second business plan, let us now move on to the scenario analysis. The two extreme reference scenarios were defined as follows:

Most pessimistic scenario: the percentage saving in the bill assumes its minimum value. It is logical to think that this happens when all the cost variables are minimum. Cheaper plant components (and therefore, generally, of lower quality) reduce energy performance.

Most optimistic scenario: the percentage saving in the bill takes on its maximum value. It is logical to think that this happens when all the cost variables are maximum. More expensive plant components (and therefore, generally, of higher quality) increase energy performance. The results of the scenario analysis are shown in

Table 10.

In the most pessimistic scenario, there is still a negative NPV at the 20th year of the analysis period. The savings in the bill contribute to making it positive only starting from the 23th year. On the other hand, in the most optimistic scenario, a positive NPV starts from the 18th year. The PP is quite high even in the best circumstances, which is why it can be assumed that for households this type of investment is currently convenient only if one makes use of tax deduction and subsidized credit mechanisms.

4.5. Risk Analysis

For the project that includes the installation of photovoltaic systems, it was decided to implement the Monte Carlo simulation to estimate its probability of success. Following the analyses conducted on the ceiling of available projects, it was possible to associate the sensitive variables of

Table 9 with the triangular probability distributions whose fundamental parameters are reported in

Table 11.

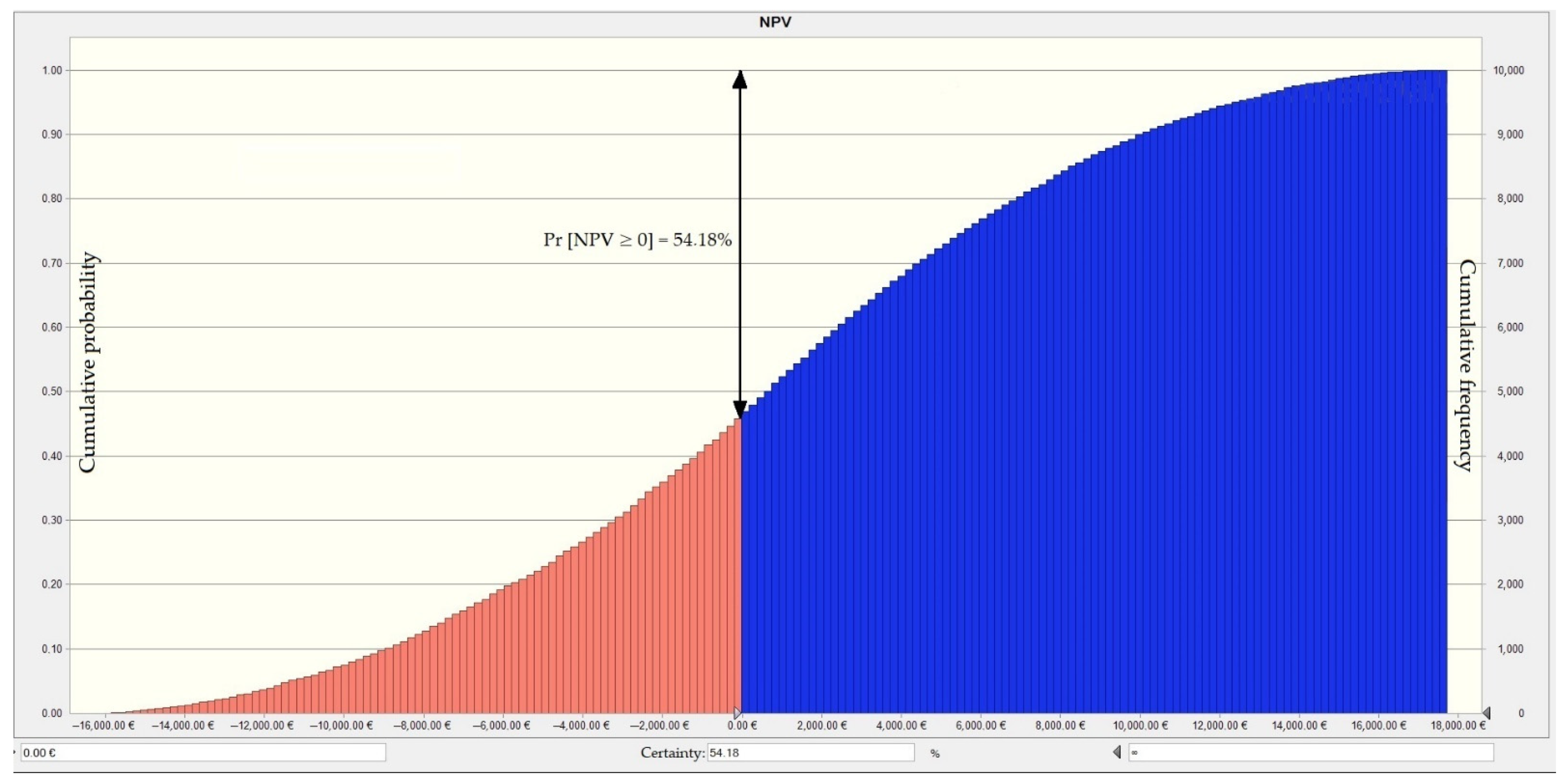

By implementing the Monte Carlo simulation, the cumulative probability of having a positive NPV is obtained (

Figure 1).

The probability of having an NPV greater than or equal to zero is 54.18%. This means that the intervention, as conceived, about once in two could lead to financially acceptable results, that is, to savings greater than those expected. This result, which places the investor in front of a strong margin of uncertainty, could depend on three factors.

First, the hybrid nature of the investment must be considered, which has both a plant and a structural component. Generally, the PP of a photovoltaic system is estimated between 7 and 12 years [

63], or equal to approximately half of its entire life cycle. However, when photovoltaics are combined with structural investments (actions on windows and the building envelope), the times in which the investment pays off tend to increase and exceed 20 years.

Secondly, the recent increase in the cost of electricity must be considered, which greatly reduces savings on the bill compared to the past.

Thirdly, the financial performance of the interventions is closely correlated with the prices of building materials and processing. The multiplication of government subsidy instruments (such as the Superbonus regulated by Law No. 234/2021) aimed at encouraging the energy transition process in the residential sector has led to an increase in the demand for building materials. As a result, there has been an increase in prices (of 20%, 30% or even 40%) on the part of the supplier companies. Therefore, given the new price system, it has now become prohibitive for households to energetically renovate their homes without resorting to the aforementioned bonuses. Through the wide range of state incentives (Ecobonus, Superbonus, Facade Bonus, Restructuring Bonus, etc.) provided in the Italian legislative panorama, it is also possible for the owners of economically disadvantaged properties to be able to redevelop their homes. For example, concerning the business plan in

Table 5, using the 110% Superbonus and, specifically, the invoice discount mechanism, an NPV of 174.783 euros would be obtained, an IRR of 79%, and an immediate PP. The only cost to the tenants, equal to 23,819 euros (just over 1000 euros per household to be paid in a single solution), is that relating to the portion of the cost of the photovoltaic system exceeding the spending limits set by law (which, in the case in question, amounts to €20,440).

5. Conclusions

The energy transition, a path already started in the main economies of the planet, including Italy, must exploit the maximum possible number of levers from below to be accelerated. In this context, construction can promote both economic growth and the reduction of the environmental impact of human activities, playing an important role in enhancing research strategies on energy efficiency. Given the relevance of the issue, in this work it was decided to analyze the financial effects of the energy transition in multi-family residential buildings in Campania (Italy), identifying a representative building on which to plan ordinary energy efficiency measures. The study, which made use of various analysis techniques (ACB, sensitivity analysis, scenario analysis, risk analysis) made it possible to achieve the objectives listed in the introductory section. The main results of the study are summarized below:

In the Campania region, the PP of an ordinary energy restructuring intervention is of 20 years if it includes, in addition to the traditional energy-saving measures (efficiency of the building envelope, replacement of the fixtures, solar screens, and boilers), also the installation of solar photovoltaic systems;

Considering the same intervention, but excluding the photovoltaic technology from the project, the PP increases by four years;

The cost of the storage system represents the main variable capable of significantly influencing the financial performance of the entire energy retrofit project;

In the most optimistic scenario, the PP is reduced by only two years, passing from 20 to 18 years. The most pessimistic scenario guarantees almost the same performance in terms of energy-saving that occurs in the absence of photovoltaics;

Just under half of the regional energy interventions risk being financially unsustainable. Each surgery has a risk of failure of approximately 46%.

To date, energy retrofit interventions become unsustainable for property owners if government building bonuses are not used.

The average regional savings in the bill deriving from photovoltaics alone is approximately 6%. In combination with the other ordinary energy interventions, the average savings in the bill is around 46%. The latter can increase up to 50% if you opt for the best photovoltaic technology on the market. Nevertheless, even considering the most optimistic scenario, the financial benefits deriving from the project are disproportionate to the mortgage payments to be paid to cover the cost of the works.

Despite the significant results obtained, the proposed study has some limitations. A first limitation derives from the statistical sample of properties taken as a reference. It could represent a partial vision of the actual situation present in the Campania region. It is, therefore, necessary to acquire a growing amount of information, through the analysis of new projects. Another limit is linked to the not always simple correlation between energy class and savings in the bill. The consumptions obtained are calculated on the basis of standard parameters (full functionality of the heating system, hot water needs estimated on the basis of specific regulations, continuous occupation of the building, etc.), so they may not reflect the actual consumption of users. Furthermore, the study focuses solely on the financial convenience of the interventions, not considering other important benefits, such as greater thermal comfort, the improvement in the general health of the tenants, and the increase in value of the property following the work.

Part of the aforementioned limits will be the subject of further research and future study. Furthermore, the approach followed could also be applied to redevelopment and energy efficiency interventions on public buildings and infrastructures or on the historical-architectural heritage [

64,

65,

66,

67,

68].

{kind=link}