An Asymmetric Analysis of the Influence That Economic Policy Uncertainty, Institutional Quality, and Corruption Level Have on India’s Digital Banking Services and Banking Stability

Abstract

:1. Introduction

2. Review of Literature

2.1. Empirical Literature Review on the Nexus of EPU, Banking Stability, and Digital Financial Services

2.2. Theoretical and Conceptual Framework

3. Data, Variables, and Methodology

3.1. Data and Variables

3.2. Model Specification

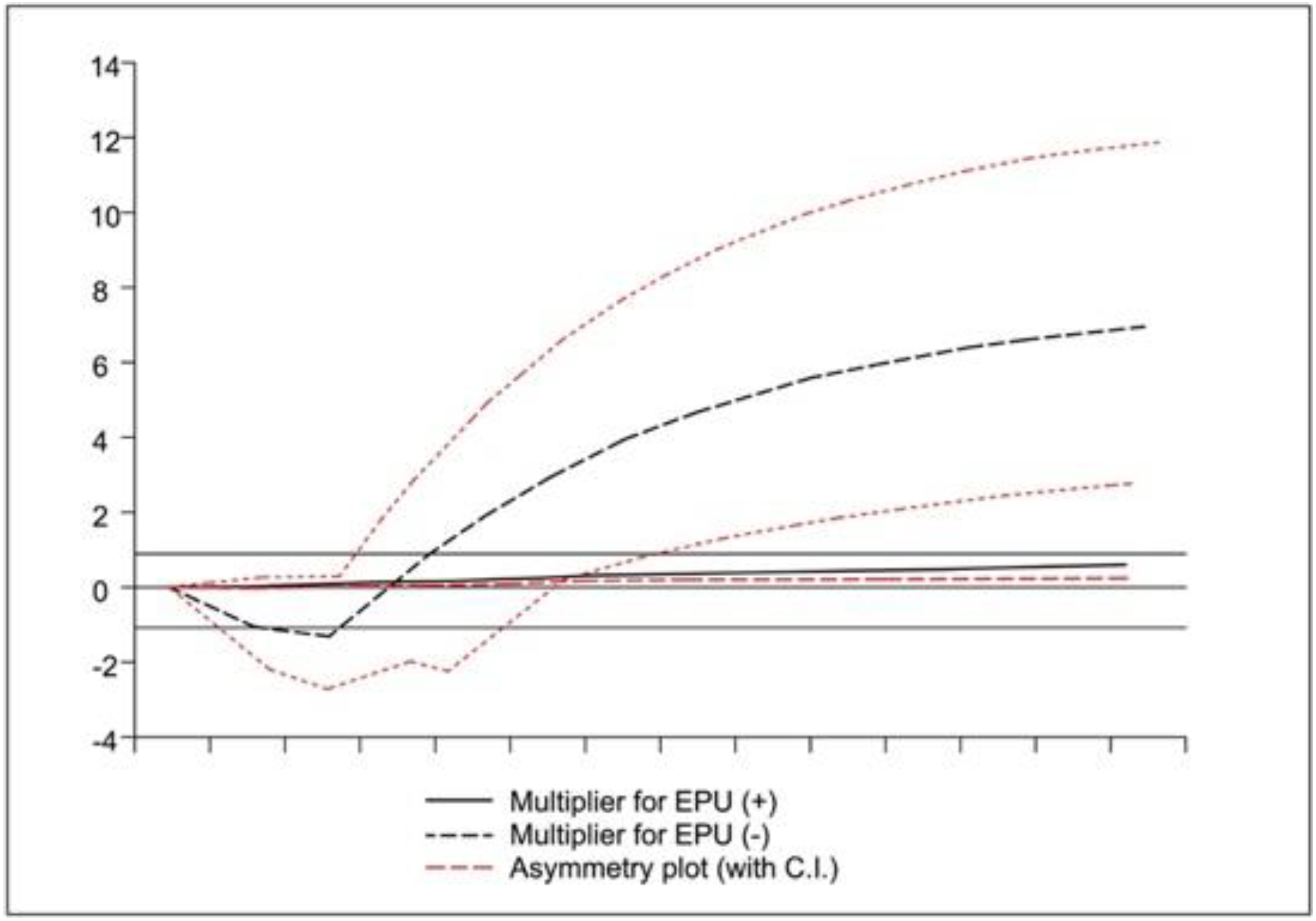

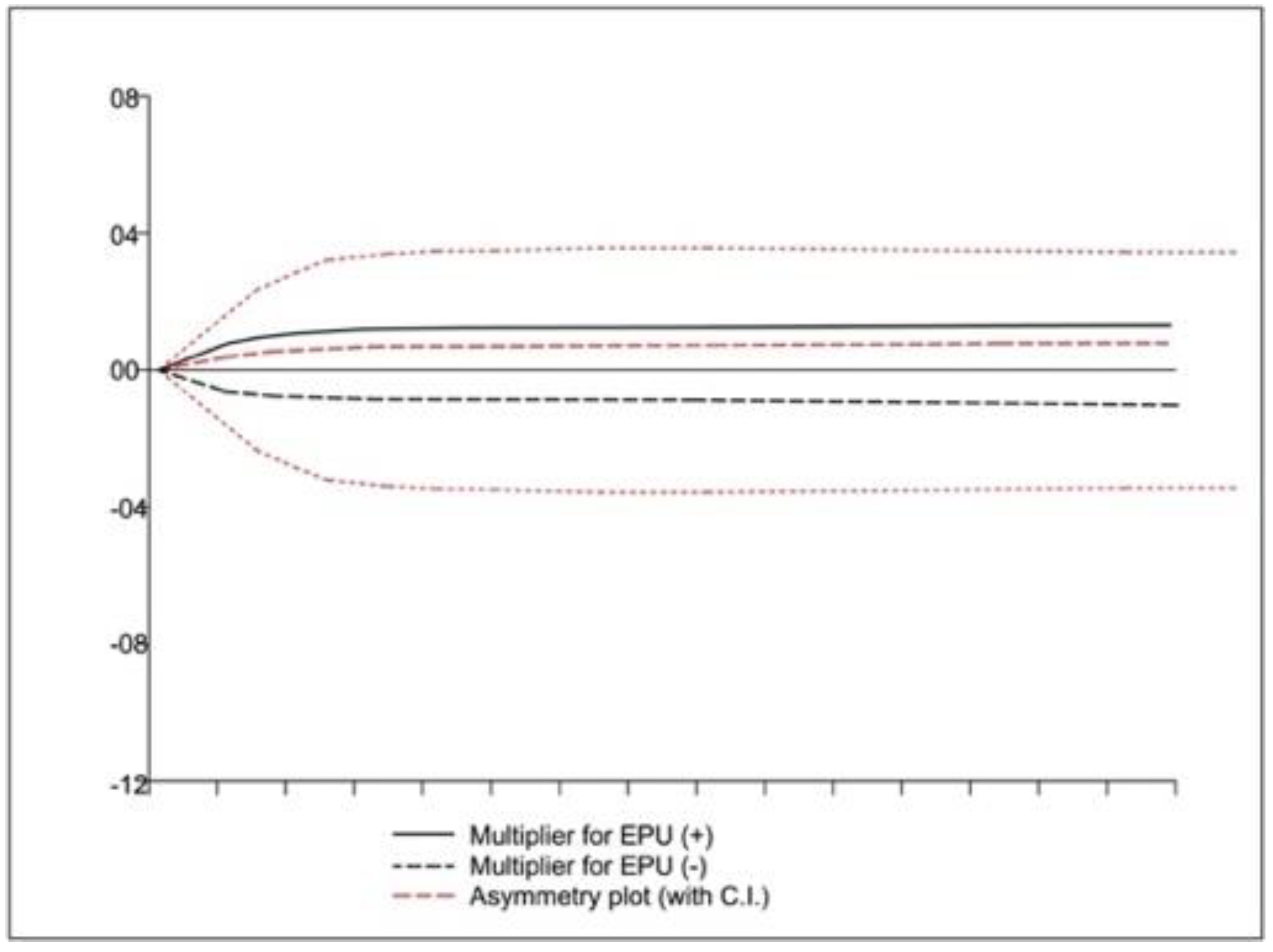

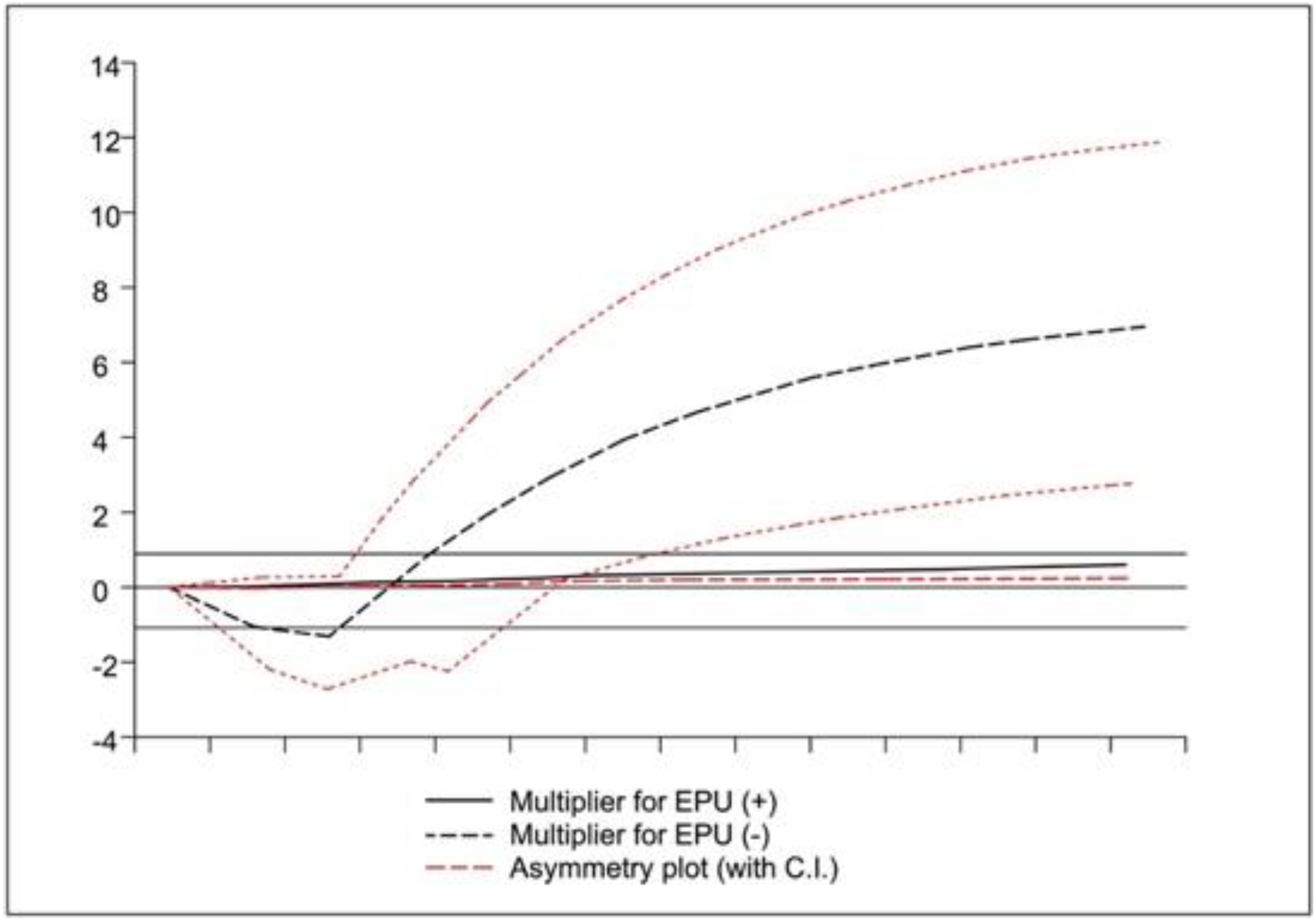

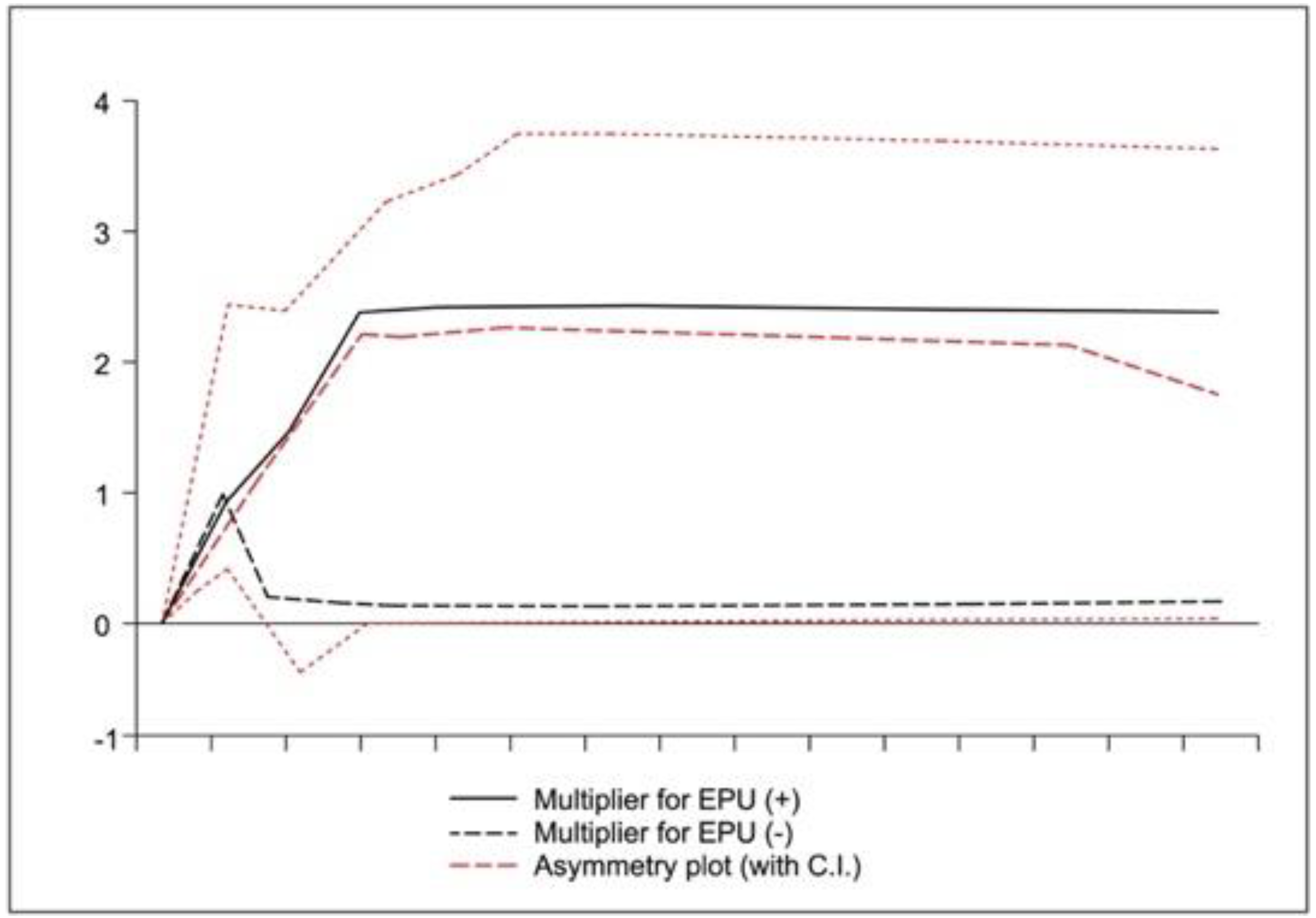

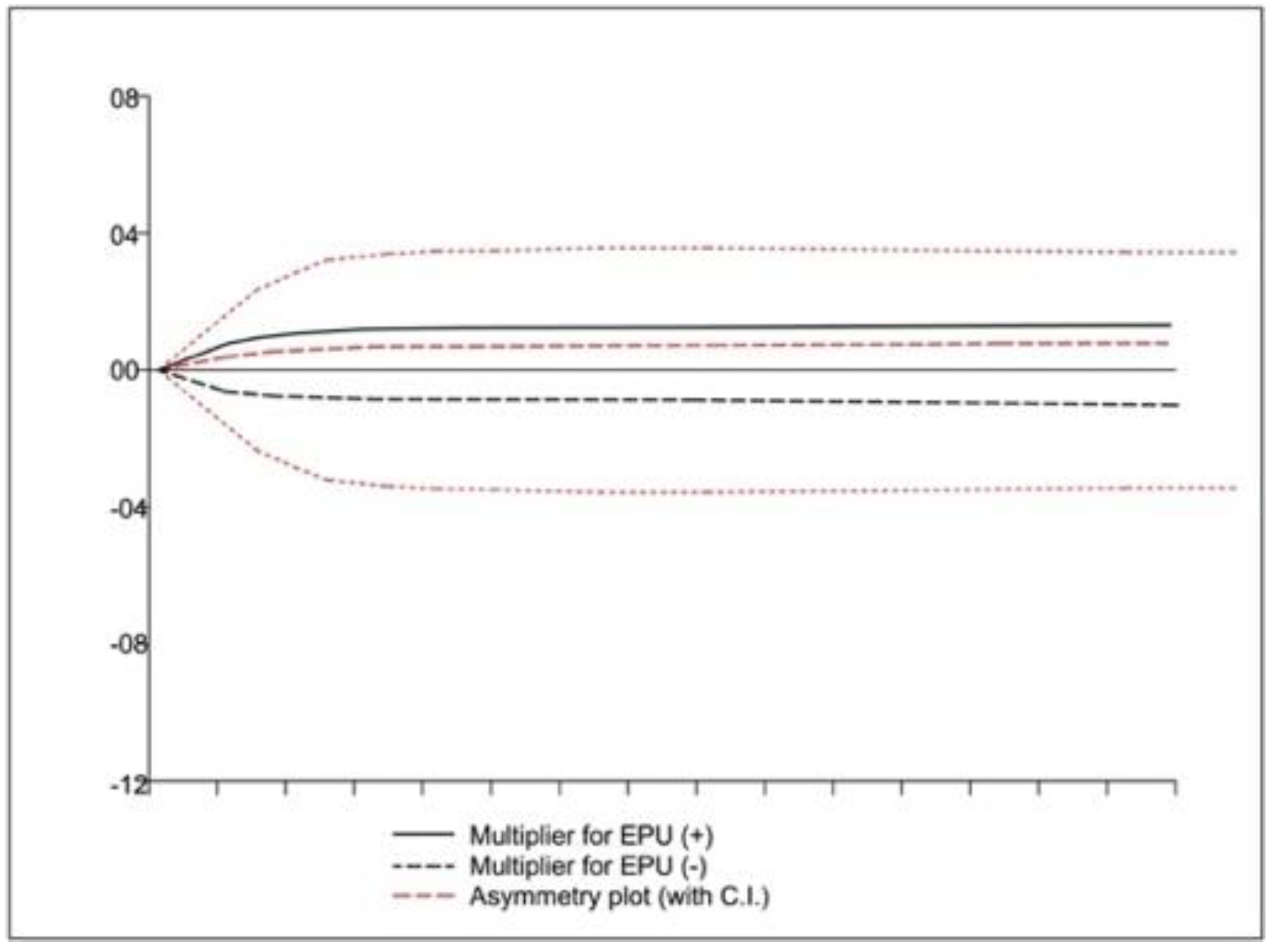

4. Empirical Analysis and Discussion

4.1. Unit Root Test

4.2. BDS Test

5. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Kaviani, M.S.; Kryzanowski, L.; Maleki, H.; Savor, P. Policy uncertainty and corporate credit spreads. J. Financ. Econ. 2020, 138, 838–865. [Google Scholar] [CrossRef]

- Drobetz, W.; El Ghoul, S.; Guedhami, O.; Janzen, M. Policy uncertainty, investment, and the cost of capital. J. Financ. Stab. 2018, 39, 28–45. [Google Scholar] [CrossRef]

- Hu, S.; Gong, D. Economic policy uncertainty, prudential regulation and bank lending. Financ. Res. Lett. 2018, 29, 373–378. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring Economic Policy Uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Biswas, S.; Zhai, W. Economic policy uncertainty and cross-border lending. J. Corp. Financ. 2020, 67, 101867. [Google Scholar] [CrossRef]

- Yung, K.; Root, A. Policy uncertainty and earnings management: International evidence. J. Bus. Res. 2019, 100, 255–267. [Google Scholar] [CrossRef]

- Bhuiyan, M.A.; Dinçer, H.; Yüksel, S.; Mikhaylov, A.; Danish, M.S.S.; Pinter, G.; Uyeh, D.D.; Stepanova, D. Economic indicators and bioenergy supply in developed economies: QROF-DEMATEL and random forest models. Energy Rep. 2022, 8, 561–570. [Google Scholar] [CrossRef]

- Bloom, N.; Floetotto, M.; Jaimovich, N.; Saporta-Eksten, I.; Terry, S.J. Really Uncertain Business Cycles. Econometrica 2018, 86, 1031–1065. [Google Scholar] [CrossRef]

- Caglayan, M.; Xu, B. Economic Policy Uncertainty Effects on Credit and Stability of Financial Institutions. Bull. Econ. Res. 2018, 71, 342–347. [Google Scholar] [CrossRef]

- Altunbas, Y.; Manganelli, S.; Marques-Ibanez, D. Bank risk during the financial crisis: Do business models matter? Bang. Bus. Sch. Res. Pap. 2011, 3, 12. [Google Scholar] [CrossRef]

- Park, C.-Y.; Shin, K. COVID-19, nonperforming loans, and cross-border bank lending. J. Bank. Financ. 2021, 133, 106233. [Google Scholar] [CrossRef]

- Bermpei, T.; Kalyvas, A.; Nguyen, T.C. Does institutional quality condition the effect of bank regulations and supervision on bank stability? Evidence from emerging and developing economies. Int. Rev. Financ. Anal. 2018, 59, 255–275. [Google Scholar] [CrossRef]

- Nguyen, T.C. Economic policy uncertainty and bank stability: Does bank regulation and supervision matter in major European economies? J. Int. Financ. Mark. Inst. Money 2021, 74, 101387. [Google Scholar] [CrossRef]

- Bilgin, M.H.; Danisman, G.O.; Demir, E.; Tarazi, A. Economic uncertainty and bank stability: Conventional vs. Islamic banking. J. Financ. Stab. 2021, 56, 100911. [Google Scholar] [CrossRef]

- Banna, H.; Alam, M.R. Impact of digital financial inclusion on ASEAN banking stability: Implications for the post-COVID-19 era. Stud. Econ. Financ. 2021, 38, 504–523. [Google Scholar] [CrossRef]

- Syed, A.A.; Ahmed, F.; Kamal, M.A.; Segovia, J.E.T. Assessing the Role of Digital Finance on Shadow Economy and Financial Instability: An Empirical Analysis of Selected South Asian Countries. Mathematics 2021, 9, 3018. [Google Scholar] [CrossRef]

- Rakshit, B.; Bardhan, S. Bank Competition and its Determinants: Evidence from Indian Banking. Int. J. Econ. Bus. 2018, 26, 283–313. [Google Scholar] [CrossRef]

- Jia, Z.; Mehta, A.M.; Qamruzzaman, M.; Ali, M. Economic Policy Uncertainty and Financial Innovation: Is There Any Affiliation? Front. Psychol. 2021, 12, 1781. [Google Scholar] [CrossRef]

- Ozili, P.K. Impact of digital finance on financial inclusion and stability. Borsa Istanb. Rev. 2018, 18, 329–340. [Google Scholar] [CrossRef]

- Khan, K.; Su, C.-W.; Xiao, Y.-D.; Zhu, H.; Zhang, X. Trends in tourism under economic uncertainty. Tour. Econ. 2020, 27, 841–858. [Google Scholar] [CrossRef]

- Gupta, R.; Ma, J.; Risse, M.; Wohar, M.E. Common business cycles and volatilities in US states and MSAs: The role of economic uncertainty. J. Macroecon. 2018, 57, 317–337. [Google Scholar] [CrossRef] [Green Version]

- Wang, G.-J.; Xie, C.; Wen, D.; Zhao, L. When Bitcoin meets economic policy uncertainty (EPU): Measuring risk spillover effect from EPU to Bitcoin. Financ. Res. Lett. 2018, 31, 28. [Google Scholar] [CrossRef]

- Bernal, O.; Gnabo, J.-Y.; Guilmin, G. Economic policy uncertainty and risk spillovers in the Eurozone. J. Int. Money Financ. 2016, 65, 24–45. [Google Scholar] [CrossRef]

- Francis, B.B.; Hasan, I.; Zhu, Y. Political uncertainty and bank loan contracting. J. Empir. Financ. 2014, 29, 281–286. [Google Scholar] [CrossRef]

- Chi, Q.; Li, W. Economic policy uncertainty, credit risks and banks’ lending decisions: Evidence from Chinese commercial banks. China J. Account. Res. 2017, 10, 33–50. [Google Scholar] [CrossRef]

- Aastveit, K.A.; Natvik, G.J.; Sola, S. Economic uncertainty and the influence of monetary policy. J. Int. Money Financ. 2017, 76, 50–67. [Google Scholar] [CrossRef]

- Caggiano, G.; Castelnuovo, E.; Figueres, J.M. Economic policy uncertainty and unemployment in the United States: A nonlinear approach. Econ. Lett. 2017, 151, 31–34. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Y.; Tian, G.; Wu, Y.; Mo, B. Impacts of geopolitical risks and economic policy uncertainty on Chinese tourism-listed company stock. Int. J. Financ. Econ. 2020, 27, 320–333. [Google Scholar] [CrossRef]

- Ashraf, B.N.; Shen, Y. Economic policy uncertainty and banks’ loan pricing. J. Financ. Stab. 2019, 44, 100695. [Google Scholar] [CrossRef]

- Boumparis, P.; Milas, C.; Panagiotidis, T. Economic policy uncertainty and sovereign credit rating decisions: Panel quantile evidence for the Eurozone. J. Int. Money Financ. 2017, 79, 39–71. [Google Scholar] [CrossRef] [Green Version]

- Ng, J.; Saffar, W.; Zhang, J.J. Policy uncertainty and loan loss provisions in the banking industry. Rev. Account. Stud. 2020, 25, 726–777. [Google Scholar] [CrossRef] [Green Version]

- Bekaert, G.; Hoerova, M.; Duca, M.L. Risk, uncertainty and monetary policy. J. Monet. Econ. 2013, 60, 771–788. [Google Scholar] [CrossRef] [Green Version]

- Belkhir, M.; Boubakri, N.; Grira, J. Political risk and the cost of capital in the MENA region. Emerg. Mark. Rev. 2017, 33, 155–172. [Google Scholar] [CrossRef]

- Bordo, M.D.; Duca, J.V.; Koch, C. Economic policy uncertainty and the credit channel: Aggregate and bank level U.S. evidence over several decades. J. Financ. Stab. 2016, 26, 90–106. [Google Scholar] [CrossRef] [Green Version]

- Hu, C.; Liu, X.; Pan, B.; Chen, B.; Xia, X. Asymmetric impact of oil price shock on stock market in China: A combination analysis based on SVAR model and NARDL model. Emerg. Mark. Financ. Trade 2018, 54, 1693–1705. [Google Scholar] [CrossRef]

- Niankara, I.; Muqattash, R. The impact of financial inclusion on consumers saving and borrowing behaviours: A retrospective cross-sectional evidence from the UAE and the USA. Int. J. Econ. Bus. Res. 2020, 20, 217. [Google Scholar] [CrossRef]

- Amoah, A.; Korle, K.; Asiama, R.K. Mobile money as a financial inclusion instrument: What are the determinants? Int. J. Soc. Econ. 2020, 47, 1283–1297. [Google Scholar] [CrossRef]

- Shaughnessy, H. Innovation in Financial Services: The Elastic Innovation Index Report; Innotribe: Washington, DC, USA, 2015; p. 21. [Google Scholar]

- Li, Z.; Zhong, J. Impact of economic policy uncertainty shocks on China's financial conditions. Financ. Res. Lett. 2019, 35, 101303. [Google Scholar] [CrossRef]

- Dutta, K.D.; Saha, M. Do competition and efficiency lead to bank stability? Evidence from Bangladesh. Futur. Bus. J. 2021, 7, 6. [Google Scholar] [CrossRef]

- van Duuren, T.; de Haan, J.; van Kerkhoff, H. Does institutional quality condition the impact of financial stability transparency on financial stability? Appl. Econ. Lett. 2020, 27, 1635–1638. [Google Scholar] [CrossRef] [Green Version]

- Fazio, D.M.; Silva, T.C.; Tabak, B.M.; Cajueiro, D.O. Inflation targeting and financial stability: Does the quality of institutions matter? Econ. Model. 2018, 71, 1–15. [Google Scholar] [CrossRef]

- Gulen, H.; Ion, M. Policy Uncertainty and Corporate Investment. Rev. Financ. Stud. 2015, 29, 523–564. [Google Scholar] [CrossRef]

- Cui, X.; Wang, C.; Liao, J.; Fang, Z.; Cheng, F. Economic policy uncertainty exposure and corporate innovation investment: Evidence from China. Pac.-Basin Financ. J. 2021, 67, 101533. [Google Scholar] [CrossRef]

- Tang, D.Y.; Yan, H. Market conditions, default risk and credit spreads. J. Bank. Financ. 2010, 34, 743–753. [Google Scholar] [CrossRef] [Green Version]

- Phan, D.H.B.; Iyke, B.N.; Sharma, S.S.; Affandi, Y. Economic policy uncertainty and financial stability—Is there a relation? Econ. Model. 2020, 94, 1018–1029. [Google Scholar] [CrossRef]

- Siddik, M.N.A.; Kabiraj, S. Digital finance for financial inclusion and inclusive growth. In Digital Transformation in Business and Society; Palgrave Macmillan: Cham, Switzerland, 2020; pp. 155–168. [Google Scholar]

- Oman, C.; Arndt, C. Governance Indicators for Development; OECD Development Centre Policy Insights 33; OECD Publishing: Paris, France, 2006. [Google Scholar] [CrossRef]

- Shabir, M.; Jiang, P.; Bakhsh, S.; Zhao, Z. Economic policy uncertainty and bank stability: Threshold effect of institutional quality and competition. Pac.-Basin Financ. J. 2021, 68, 101610. [Google Scholar] [CrossRef]

- Shin, Y.; Yu, B.; Greenwood-Nimmo, M. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in Honor of Peter Schmidt; Springer: New York, NY, USA, 2014; pp. 281–314. [Google Scholar]

- Dufrénot, G.; Mignon, V. Recent Developments in Nonlinear Cointegration with Applications to Macroeconomics and Finance; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2002. [Google Scholar] [CrossRef]

- Shahzad, S.J.H.; Nor, S.M.; Ferrer, R.; Hammoudeh, S. Asymmetric determinants of CDS spreads: US indus-try-level evidence through the NARDL approach. Econ. Model. 2017, 60, 211–230. [Google Scholar] [CrossRef]

- Hu, H.; Wei, W.; Chang, C.-P. Do shale gas and oil productions move in convergence? An investigation using unit root tests with structural breaks. Econ. Model. 2019, 77, 21–33. [Google Scholar] [CrossRef]

- Altinay, G.; Karagol, E. Structural break, unit root, and the causality between energy consumption and GDP in Turkey. Energy Econ. 2004, 26, 985–994. [Google Scholar] [CrossRef]

- Zivot, E.; Andrews, D.W.K. Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. J. Bus. Econ. Stat. 2002, 20, 25–44. [Google Scholar] [CrossRef]

- Brock, W.A.; Scheinkman, J.A.; Dechert, W.D.; LeBaron, B. A test for independence based on the correlation dimension. Econom. Rev. 1996, 15, 197–235. [Google Scholar] [CrossRef]

- Ozili, P.K. Economic policy uncertainty: Are there regional and country correlations? Int. Rev. Appl. Econ. 2021, 35, 714–728. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Bohl, M.T. German monetary unification and the stability of the German M3 money demand function. Econ. Lett. 2000, 66, 203–208. [Google Scholar] [CrossRef]

- Stock, J.; Watson, M. Disentangling the Channels of the 2007–2009 Recession. Natl. Bur. Econ. Res. 2012, 11, 18094. [Google Scholar] [CrossRef]

- Karadima, M.; Louri, H. Non-performing loans in the euro area: Does bank market power matter? Int. Rev. Financ. Anal. 2020, 72, 101593. [Google Scholar] [CrossRef]

- Bougatef, K. The impact of corruption on the soundness of Islamic banks. Borsa Istanb. Rev. 2015, 15, 283–295. [Google Scholar] [CrossRef] [Green Version]

- Goel, R.; Hasan, I. Economy-wide corruption and bad loans in banking: International evidence. Appl. Financ. Econ. 2011, 21, 455–461. [Google Scholar] [CrossRef]

- Son, T.H.; Liem, N.T.; Khuong, N.V. Corruption, non-performing loans, and economic growth: International ev-idence. Cogent Bus. Manag. 2020, 7, 1735691. [Google Scholar] [CrossRef]

- Kalfaoglou, F. NPLs resolution regimes: Challenges for regulatory authorities. J. Risk Manag. Financ. Inst. 2018, 11, 173–186. [Google Scholar]

- Syed, A.A.; Tripathi, R. Non-performing loans in BRICS nations: Determinants and macroeconomic impact. Indian J. Financ. 2019, 13, 22–35. [Google Scholar] [CrossRef]

- An, J.; Mikhaylov, A. Russian energy projects in South Africa. J. Energy South. Afr. 2020, 31, 58–64. [Google Scholar] [CrossRef]

- Wewege, L.; Lee, J.; Thomsett, M.C. Disruptions and Digital Banking Trends. J. Appl. Financ. Bank. 2020, 10, 15–56. [Google Scholar]

- Hua, X.; Huang, Y. Understanding China’s fintech sector: Development, impacts and risks. Eur. J. Financ. 2021, 27, 321–333. [Google Scholar] [CrossRef]

- Syed, A.A.; Ahmed, F.; Kamal, M.A.; Ullah, A.; Ramos-Requena, J.P. Is There an Asymmetric Relationship between Economic Policy Uncertainty, Cryptocurrencies, and Global Green Bonds? Evidence from the United States of America. Mathematics 2022, 10, 720. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable (Abbreviation) | Source |

|---|---|

| Dependent Variables: | |

| Banking stability (NPLs and Z-score) | IMF financial statistic database |

| Mobile money transaction percentage of GDP (MMT) | Financial Access Survey |

| Independent Variables: | |

| Economic policy uncertainty (EPU) | Baker et al. (2016) Policyuncertainty.com |

| Institutional regulation (IR) | World governance indicator |

| Corruption Index (COR) | International Country Risk Guide |

| Control Variables: | |

| Gross Domestic Product (GDP) | World Development indicators |

| Inflation (INF) | World Development indicators |

| Return on Assets percent of GDP (ROA) | IMF financial statistic database |

| Non-interest income to total income (NII) | IMF financial statistic database |

| (Annual data 2004–2019) | |

| Variables | |||||||

|---|---|---|---|---|---|---|---|

| Mean | Median | Maximum | Minimum | Std.Dev | Jarque–Bera | Probability | |

| NPLs | 6.13 | 5.11 | 9.98 | 3.37 | 3.06 | 1.251 | 0.6100 |

| Z-score | 15.95 | 17.01 | 17.28 | 16.64 | 0.26 | 0.342 | 0.0632 |

| MMT | 1.88 | 0.46 | 7.46 | 0.018 | 2.99 | 3.245 | 0.1901 |

| EPU | 105.47 | 85.32 | 185.46 | 70.89 | 45.82 | 2.525 | 0.4201 |

| IR | −0.29 | −0.27 | −0.16 | −0.44 | 0.10 | 1.342 | 0.6110 |

| COR | 2.4 | 2.50 | 2.61 | 2.00 | 0.20 | 3.667 | 0.0031 |

| GDP | 6.88 | 6.89 | 8.16 | 5.46 | 0.93 | 1.354 | 0.0723 |

| INF | 10.66 | 10.80 | 13.90 | 7.20 | 2.90 | 2.453 | 0.1625 |

| ROA | 0.91 | 0.88 | 1.38 | 0.48 | 0.41 | 0.352 | 0.0101 |

| NII | 30.04 | 28.08 | 35.64 | 26.62 | 3.98 | 2.346 | 0.0001 |

| Variables | Levels | First Difference | ||

|---|---|---|---|---|

| Constant (at 5 Percent) | Constant and Trends (at 5 Percent) | Constant (at 5 Percent) | Constant and Trends (at 5 Percent) | |

| NPLs | −1.09 (−1.043) * | −1.19 (−2.713) | −3.59 (−1.208) | −4.19 (−2.137) |

| Z-score | −2.18 (−2.012) | −2.91 (−2.012) | −2.91 (−2.746) * | −2.98 (−3.045) |

| MMT | −1.28 (−1.142) | −1.85 (−2.817) | −2.21 (−2.429) ** | −3.01 (−2.178) |

| EPU | 1.18 (−1.081) | −2.63 (−2.095) * | −2.87 (−1.853) | −3.12 (−2.409) * |

| IR | −2.03 (−2.291) | −2.32 (−2.843) | −3.09 (−2.417) * | −3.45 (−2.912) |

| COR | 1.31 (−1.837) * | −1.22 (−2.109) | −2.17 (−1.971) | −3.41 (−2.194) * |

| GDP | −2.12 (−2.018) | −2.82 (−2.071) | −2.00 (−2.116) * | −3.99 (−2.240) |

| INF | −2.15 (−2.110) * | −2.81 (−1.108) | −0.94 (−1.576) | −2.91 (−2.751) |

| ROA | −1.94 (−2.121) | −2.20 (−2.144) | −3.52 (−2.988) * | −3.82 (−2.392) |

| NII | −1.84 (−1.912) | −1.87 (−1.619) | −2.69 (−3.943) * | −2.09 (−2.328) |

| Variables | Levels | First Difference | ||

|---|---|---|---|---|

| t-Statistic | Time Break | t-Statistics | Time Break | |

| NPLs | −1.742 * | 2008 | −2.1091 * | 2008 |

| Z-score | −2.1983 * | 2008 | −3.4742 * | 2010 |

| MMT | −3.5284 * | 2012, 2017 | −3.8734 *** | 2012, 2017 |

| EPU | −2.6793 | 2009 | −4.1834 * | 2010 |

| IR | −3.2464 | 2008 | −2.8231 * | 2008 |

| COR | −2.9032 | 2010 | −5.7263 * | 2010 |

| GDP | −3.2577 * | 2010 | −4.6180 ** | 2010 |

| INF | −2.4722 * | 2004 | −2.6590 * | 2005 |

| ROA | −2.1983 ** | 2009 | −4.3853 *** | 2009 |

| NII | −2.3732 * | 2008 | −3.4212 * | 2008 |

| BDS Variables | Embedded Dimensions = m | ||||

|---|---|---|---|---|---|

| m = 2 | m = 3 | m = 4 | m = 5 | m = 6 | |

| NPLs | 0.1812 ** | 0.1965 ** | 0.2122 *** | 0.2389 ** | 0.2399 ** |

| Z-score | 0.2378 ** | 0.3327 ** | 0.3764 ** | 0.3891 *** | 0.2184 ** |

| MMT | 0.1129 ** | 0.1781 *** | 0.2342 ** | 0.2843 ** | 0.3128 ** |

| EPU | 0.1992 ** | 0.2198 ** | 0.2764 ** | −0.2931 *** | 0.3185 *** |

| IR | 0.2842 ** | 0.2954 ** | 0.3175 ** | 0.3983 * | 0.3871 *** |

| COR | 0.1274 ** | 0.1883 *** | 0.2147 ** | 0.2582 *** | 0.2743 ** |

| GDP | 0.1338 *** | −0.0572 ** | 0.1454 ** | 0.1783 ** | 0.2421 ** |

| INF | 0.2182 ** | 0.1809 *** | 0.1933 *** | 0.1965 *** | 0.1997 ** |

| ROA | 0.2313 ** | 0.2753 *** | 0.3532 * | −0.3771 ** | 0.3939 *** |

| NII | 0.0572 ** | 0.3133 ** | 0.2914 *** | 0.2859 *** | 0.1742 *** |

| NARDL Short-Run Result | Lags | |||

|---|---|---|---|---|

| Dependent Variable: NPLs | 0 | 1 | 2 | |

| EPU+ | 0.12 (0.32) ** | 0.18 (0.07) | 0.32 (1.95) | |

| EPU− | −0.56 (−0.15) * | 0.31 (0.82) | −0.62 (−0.43) | |

| IR+ | 0.21 (0.51) | −0.11 (−0.12) * | 0.31 (0.11) | |

| IR− | 0.63 (0.11) | 0.16 (0.91) * | 0.33 (1.14) | |

| COR+ | 0.06 (1.75) | 0.51 (0.76) * | 0.41 (2.84) | |

| COR− | 0.17 (0.39) | −0.44 (−0.43) ** | 0.65 (1.19) | |

| GDP | −0.23 (−0.49) | 0.22 (0.18) | −0.65 (−0.83) | |

| INF | 0.24 (0.31) ** | 0.09 (0.23) | 0.19 (1.19) | |

| ROA | 0.84 (0.14) | 0.18 (1.02) | 0.54 (0.89) | |

| NII | 0.11 (0.34) | 0.41 (1.23) | 0.06 (1.19) | |

| NARDL Long-Run Result | ||||

| Ln EPU− | Ln EPU+ | Ln COR− | Ln COR+ | Ln IR− |

| −0.10 (−1.01) ** | 0.03 (1.48) * | −0.18 (−1.15) * | 0.17 (1.67) ** | 0.19 (1.09) * |

| Ln IR+ | Ln GDP | Ln INF | Ln ROA | Ln NII |

| −0.09 (−1.14) * | −0.12 (−1.02) * | 0.25 (1.57) ** | −1.23 (−0.53) * | −0.23 (−1.12) ** |

| Diagnostic Test Results: | ||||

| ECMt−1 | (Joint Sig) | Adj. R2 | RESET | LM |

| −0.010 (0.00 ***) | 8.16 *** | 0.61 | 4.091 (0.512) | 0.78 (0.452) |

| F Statistic | Ln EPUSR | Ln EPULR | Ln CORSR | Ln CORLR |

| 6.36 | 0.03 (0.002) * | 2.31 (0.05) * | 0.76 (0.01) | 1.12 (0.002) * |

| Ln IRSR | Ln IRLR | |||

| 1.09 (0.005) | 1.22 (0.000) ** | |||

| NARDL Short-Run Result | Lags | |||

|---|---|---|---|---|

| Dependent Variable: Z-Score | 0 | 1 | 2 | |

| EPU+ | 0.19 (0.02) | −0.04 (−0.63) ** | 0.18 (0.67) | |

| EPU− | 0. 45 (1.05) | 0.11 (0.91) ** | 1.16 (0.23) | |

| IR+ | 0.04 (0.11) * | 0.09 (0.35) | 0.16 (0.18) | |

| IR− | −0.23 (−0.43) * | 1.21 (0.27) | 0.62 (0.09) | |

| COR+ | −0.13 (−1.19) * | 0.43 (1.03) | 0.26 (1.33) | |

| COR− | 0.17 (1.03) * | 0.12 (1.84) | 0.10 (1.14) | |

| GDP | 0.11 (1.31) * | 1.22 (1.08) | 0.21 (0.38) | |

| INF | −0.39 (−0.17) * | 0.08 (0.49) | 0.41 (1.07) | |

| ROA | 0.14 (0.18) | 0.22 (0.17) * | 0.35 (0.61) | |

| NII | 0.10 (0.37) | 0.22 (1.16) * | 0.13 (1.73) | |

| NARDL Long-Run Result | ||||

| Ln EPU− | Ln EPU+ | Ln COR− | Ln COR+ | Ln IR− |

| 0.11 (0.82) * | −0.37 (−1.12) ** | 0.62 (0.15) * | −0.25 (−1.54) * | −0.38 (−1.31) * |

| Ln IR+ | Ln GDP | Ln INF | Ln ROA | Ln NII |

| 0.16 (1.27) * | 0.16 (1.54) * | 0.19 (1.02) | 1.15 (0.28)* | 0.15 (0.75) * |

| Diagnostic Test Results: | ||||

| ECMt-1 | (Joint Sig) | Adj. R2 | RESET | LM |

| −0.009 (0.00 **) | 6.16 ** | 0.68 | 6.09 | 14 |

| F | Ln EPUSR | Ln EPULR | Ln CORSR | Ln CORLR |

| 4.59 | 0.06 (0.00) * | 1.01 (0.03) * | 0.36 (0.00) | 1.03 (0.00) * |

| Ln IRSR | Ln IRLR | |||

| 1.00 (0.01) * | 1.09 (0.00) * | |||

| NARDL Short-Run Result | Lags | |||

|---|---|---|---|---|

| Dependent Variable: MMT | 0 | 1 | 2 | |

| EPU+ | −0.18 (−0.51) ** | 1.11 (0.06) | 0.12 (1.45) | |

| EPU− | 0.23 (0.44) * | 0.38 (0.64) | 0.29 (0.21) | |

| IR+ | 0.05 (0.11) | 0.09 (0.48) | 0.48 (1.09) | |

| IR− | 0.74 (1.54) | 1.14 (0.70) | 0.27 (1.39) | |

| COR+ | 0.27 (1.25) | −0.32 (−0.30) ** | 1.19 (1.04) | |

| COR− | 0.21 (0.62) | 0.35 (1.03) * | 0.28 (2.29) | |

| GDP | 0.56 (0.28) * | 0.19 (1.18) | 0.70 (0.39) | |

| INF | 0.36 (0.53) | 0.17 (0.03) | 0.47 (1.52) | |

| ROA | 0.09 (0.02) * | 0.37 (1.63) | 0.65 (0.56) | |

| NII | 0.48 (1.03) | 0.26 (1.02) | 0.39 (1.41) | |

| NARDL Long-Run Result | ||||

| Ln EPU− | Ln EPU+ | Ln COR− | Ln COR+ | Ln IR− |

| 0.51 (1.01) * | −0.24 (−1.23) ** | 0.12 (0.36) * | −0.47 (−2.04) ** | −0.19 (−0.37) * |

| Ln IR+ | Ln GDP | Ln INF | Ln ROA | Ln NII |

| 0.28 (0.87) * | 0.20 (1.12)* | 0.19 (0.27) | 1.29 (0.31) * | 0.28 (0.49) * |

| Diagnostic Test | ||||

| ECMt-1 | (Joint Sig) | Adj. R2 | RESET | LM |

| −0.007 (0.00 **) | 9.21 *** | 0.64 | 6.11 | 13 |

| F | Ln EPUSR | Ln EPULR | Ln CORSR | Ln CORLR |

| 5.81 | 1.01 (0.000) * | 1.87 (0.01) * | 0.18 (0.002) * | 1.07 (0.00) * |

| Ln IRSR | Ln IRLR | |||

| 1.00 (0.36) | 1.02 (0.00) * | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Syed, A.A.; Kamal, M.A.; Ullah, A.; Grima, S. An Asymmetric Analysis of the Influence That Economic Policy Uncertainty, Institutional Quality, and Corruption Level Have on India’s Digital Banking Services and Banking Stability. Sustainability 2022, 14, 3238. https://doi.org/10.3390/su14063238

Syed AA, Kamal MA, Ullah A, Grima S. An Asymmetric Analysis of the Influence That Economic Policy Uncertainty, Institutional Quality, and Corruption Level Have on India’s Digital Banking Services and Banking Stability. Sustainability. 2022; 14(6):3238. https://doi.org/10.3390/su14063238

Chicago/Turabian StyleSyed, Aamir Aijaz, Muhammad Abdul Kamal, Assad Ullah, and Simon Grima. 2022. "An Asymmetric Analysis of the Influence That Economic Policy Uncertainty, Institutional Quality, and Corruption Level Have on India’s Digital Banking Services and Banking Stability" Sustainability 14, no. 6: 3238. https://doi.org/10.3390/su14063238

APA StyleSyed, A. A., Kamal, M. A., Ullah, A., & Grima, S. (2022). An Asymmetric Analysis of the Influence That Economic Policy Uncertainty, Institutional Quality, and Corruption Level Have on India’s Digital Banking Services and Banking Stability. Sustainability, 14(6), 3238. https://doi.org/10.3390/su14063238