3.1. Trend and Structural Change of ROA and Financing

To understand the behavior of both financing and ROA, we first studied their trend and possible structural change especially due to the COVID-19 pandemic. Note that we worked on the log-scale of financing and ROA, respectively named

LFIN and

LROA (See also

Section 2.1).

Figure 2 shows that

LROA and

LFIN have a clear increasing trend, which indicates that Indonesia Islamic Commercial Bank would handle their role as an intermediation institution properly over a long-term period. However, according to the fluctuations, both variables have a pattern that undergoes structural changes. Structural change of

LFIN seems to only occur in September 2016 mainly due to the increasing of community savings and deposits which triggers the banks to improve the distribution of financing to the community [

37]. We observe that the pattern of

LFIN does not show an obvious change during the pandemic, which might indicate that the amount of financing is still under control during the pandemic. At least two reasons could explain this finding: (1) Some debtors received financing during the pandemic but were approved before the pandemic, and (2) Islamic Commercial Banks continue distributing financing during the pandemic, but consider applying stricter rules and are more selective in terms of grant debtors and sectors [

37]. Meanwhile, structural changes of

LROA have occurred in many periods, especially during the pandemic when

LROA dropped from March 2020 to November 2020 (

Figure 2b). This could be due to the financing restructuring policies during the pandemic such as delays in payment installments and margin payment waivers for debtors or companies that are affected by the pandemic [

37]. Thus, the profit of Islamic Commercial Banks reduces, leading to the decreasing of ROA.

3.2. Model Development Using VARX and Spline Regression

To model

LFIN and

LROA using VARX model (see Equations (1) and (2)), we first conducted a stationarity test using the Philips Perron test and second determined the number of maximum lag (

p) using five criteria: LR, FPE, AIC, SC, and HQ (see

Section 2.2.1 step 3 and [

35]).

Table 1 concludes that

LROA and

LFIN are stationary at level (

p-value < 0.05), suggesting the employment of both variables for modeling without further treatment. Regarding the lag selection, the results are different depending on the criteria: SC selects 1, LR and HQ prefer 5, while FPE and AIC consider 7 lags (

Table 2). We embraced all options, i.e., VARX with lag 1, VARX with lag 5, and VARX with lag 7, and then compared them to determine the best one.

Using three VARX models, the resulting estimators and the R-adjusted are depicted in

Table 3. The VARX (7) model performs best with the R-adjusted values more than 99 percent for

LFIN, meaning that the VARX model perfectly fits the real

LFIN case. Although models for

LROA perform slightly worse with R-adjusted values around 75%, the more complex structure of

LROA could explain this result (see

Figure 2b).

Regarding the COV19, we find that the COVID-19 pandemic has significantly impacted the decline of

LROA, around 0.26 (equivalent to the decline of ROA around 1.30 percent) compared to the one before the pandemic. When the government had to issue a policy of Financial Services Authority Regulation No. 11/POJK.03/2020 for banking industry to restructure financing, the profit of Islamic Commercial Banks dropped significantly, followed by a declining of the ROA. On the other hand, the pandemic does not show a significant effect on financing, showing that Islamic Commercial Bank might have anticipated the impact of the pandemic. The strategy is to continue distributing the finance but with more selective debtors [

38]. The bank also maintains collecting funds by developing digital banking services, so the customers can get excellent services easily.

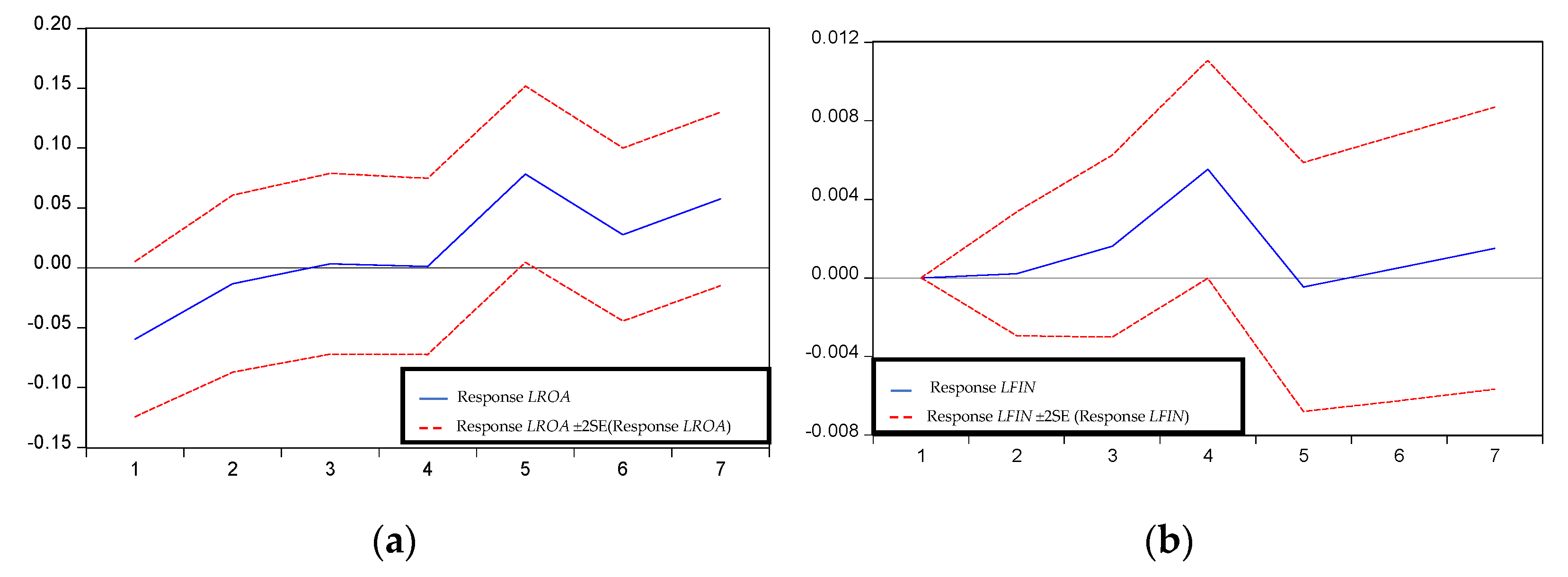

The reciprocal influence between

LFIN and

LROA is conducted using impulse response presented in

Figure 3. First,

LFIN shock in a month will be responded to positively by

LROA 5 months later (

Figure 3a), meaning that the profit of financing will impact on ROA at least 5 months after the financing is granted. Second,

LROA shock in a month will be responded to positively by

LFIN in 2 months until 4 months later, indicating the profit earned by Islamic Commercial Banks in a month can be optimized to increase financing at least two months after the banks obtain profit. An increase in ROA shows that there has been an increase in the profit of the banks by assuming assets of the banks are fixed. With good profitability, the bank will have more liberty to provide financing to debtors because the bank has good liquidity. Our findings are in line with the previous studies [

15,

17,

18,

19], but this reciprocal influence between ROA and finance of Indonesia Islamic Commercial Bank could be the first one available in the literature.

To evaluate the forecasting performance, we calculate the RMSE using the testing data, compare again all the VARX models, and select the model with the smallest RMSE. The VARX (7) is the best one for financing while the VARX (5) is best for ROA (

Table 4).

After obtaining two VARX model candidates, the next step is to make spline regression. In this study, we form three spline regression models with lag lengths of exogenous variables based on the previous selection criteria, namely 1, 5, and 7. The estimated results of spline regression model can be seen in

Table 5. The entire spline regression model in this study yields adjusted R Square above 69 percent. It means that all of the spline regression models made are good enough to explain the variation of

LFIN and

LROA because more than 69 percent of variation of

LROA and

LFIN can be explained by the spline regression models formed. Based on the results of significance test in

Table 5,

LFIN in a month is significantly affected by

LFIN in the previous month and

LROA in a month is significantly affected by

LROA in the previous month. We will now focus on the impact of the pandemic on

LROA and

LFIN based on the results of spline regression. All spline regression models formed give the result that the pandemic is insignificant to financing. In addition, only the spline regression model with a maximum exogenous variable lag of 7 provides results that the pandemic is significant to

LROA. This contrasts with the results obtained in VARX models that all show significant results of the effect of the pandemic on

LROA. It can be caused by only a small available observation used in the pandemic periods so spline regression models cannot capture the impact of the pandemic on

LROA and

LFIN.

The next step is to compare forecasting performance between VARX and spline regression model. We compare forecasting performance between VARX and spline regression model by looking at RMSE that is generated when applying the model in data testing. From

Table 6, the smallest RMSE value for ROA forecasting in data testing period is obtained from VARX model with lag 5 while the smallest RMSE value for financing forecasting in data testing period is obtained from VARX model with lag 7. Therefore, empirically, financing and ROA forecasting of Islamic Commercial Banks in Indonesia is better using VARX model than spline regression model.

Based on

Table 6, we will forecast ROA of Islamic Commercial Banks by using VARX with maximum lag of 5 (VARX (5)) while we will forecast financing of Islamic Commercial Banks by using VARX with maximum lag of 7 (VARX (7)). The next step is to form VARX (5) and VARX (7) by using all training and testing data. The VARX (5) and VARX (7) models obtained from training and testing data are written as follows.

The ROA forecasting of Islamic Commercial Banks is done by using VARX (5) model in the Equations (6) and (7). Meanwhile, the financing forecasting of Islamic Commercial Banks is done by using VARX (7) model in the Equations (8) and (9). The forecasting result can be seen in

Table 7.

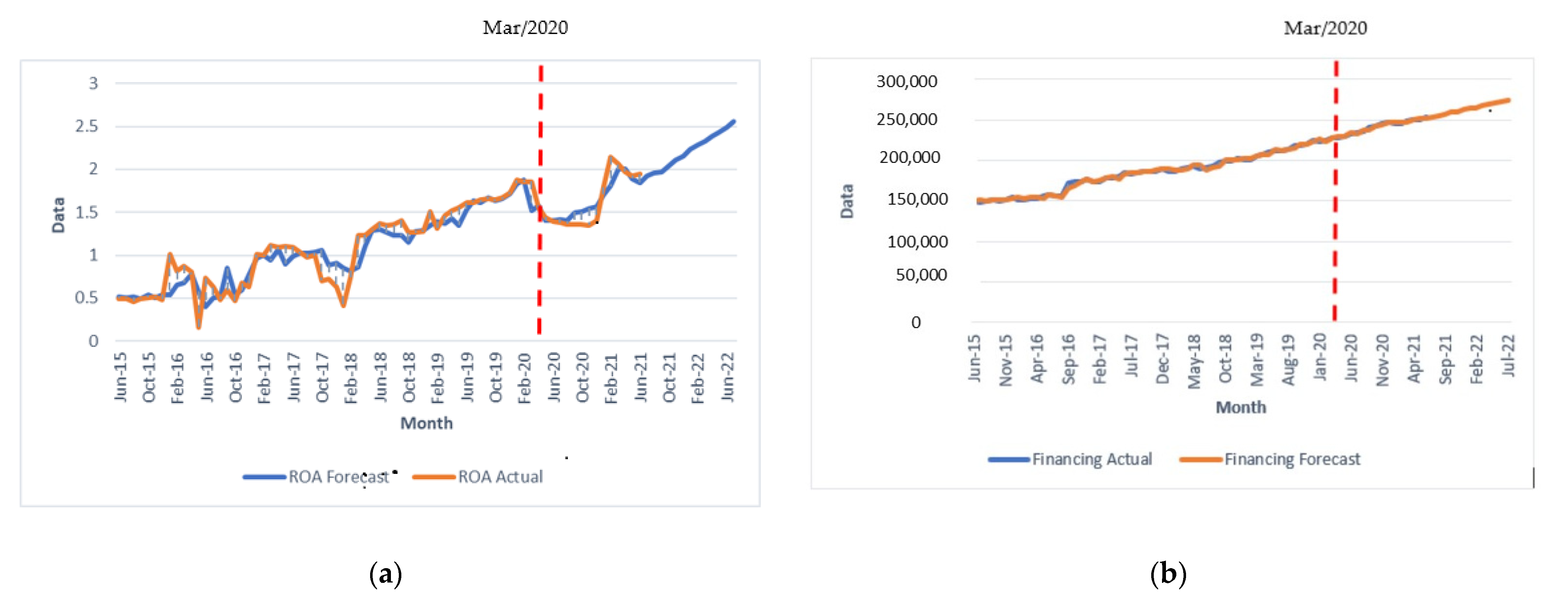

To see the difference between actual and forecast ROA and finance, we also compare them in

Figure 4. In general, the actual and forecast data are quite similar. The forecast of financing is even very close to the reality. Although ROA is more difficult to predict, our model could detect the impact of the COVID-19 pandemic, showing that the ROA dropped from March 2020 (pandemic begins in Indonesia) to November 2020.

Our results could supplement previous studies, especially the one conducted by Nugroho et al. [

39] which used three kinds of scenarios to predict the performance of Islamic Commercial Banks. In a scenario where economic growth conditions decrease from 5.3 percent to 4.6 percent and the rupiah exchange rate against the dollar amounted to Rp16.500, Islamic Commercial Banks can still run their business well. In addition, Nugroho et al. [

39] suggested the steps taken by the government to strengthen Islamic Commercial Banks in Indonesia, including strengthening liquidation, implementing financing restructuration rules, and merging Islamic Commercial Banks.

Related to the explanation of previous paragraph, the determination of state revenue and spending budget draft in 2022 uses the assumption of economic growth of 5.2 to 5.5 percent and the rupiah against dollar exchange rate is Rp. 14,350. On 1 February 2021, three Indonesia Islamic Commercial Banks, namely BRI Syariah, Bank Syariah Mandiri, and BNI Syariah, officially merged into Bank Syariah Indonesia [

40]. In addition, the government, through the regulation of the financial services authority number 11/POJK.03/2020, has implemented a policy on credit restructuring and financing for debtors who are experiencing difficulty to fulfill obligations to the banks due to debtors or businesses debtors affected by the spread of COVID-19. Considering the conditions and efforts that have been made, ROA and financing could be getting better in 2022, as obtained by our results (

Figure 4). In

Figure 4a, we can see that the graph of the ROA forecasting line (blue line) is similar to the graph of the actual data line (orange line). In March 2020, when the pandemic was first detected in Indonesia, ROA estimation shows a similar pattern of decline with actual data. From July 2021 until July 2022, the ROA of Islamic Commercial Banks is predicted to continue to increase. Meanwhile, in

Figure 4b, the financing forecasting graph (blue line) has an increasing pattern similar to the graph of actual data (orange line).

{kind=link}

{kind=link}

{kind=link}

{kind=link}