Abstract

Business groups are observed everywhere except in the U.S. and U.K.; their global presence is widely acknowledged. The most successful explanation for this preponderance has been based on the relative efficiency of business groups’ internal market vis-à-vis the external market conventionally observed in underdeveloped or emerging economies. Unsurprisingly, this view cannot explain why business groups also prosper in advanced economies where their internal market is thought to no longer match efficient external markets. This study addresses this contradiction by drawing attention to non-tradable, intangible assets and putting forward an institution-free, micro-level explanation. Specifically, we reason that the external market for organizational capabilities is bound to be missing regardless of institutional advancements and economic development due to human beings’ innate cognitive limits and information and behavioral uncertainties, while business groups’ internal markets may overcome these limits via their distinctive organizing mechanism underpinned by group identity, solidarity, mutual trust, shared organizational architecture, and enhanced communicability. In other words, business groups can outperform the external market in coordinating and facilitating exchanges of non-tradable assets and organizational capabilities in particular that are becoming increasingly crucial for successful competition. Using panel data of large business groups in Korea during the periods between 2003 and 2016, we confirm that affiliation with business groups and accessing their internal market enhances technological capability. Thus, this study extends our understanding of business groups beyond the institution-based explanation.

1. Introduction

Business groups are ubiquitous around the world, particularly outside the U.S. and U.K., and take control of a substantial portion of industrial output; their economic significance is undisputed [1,2,3,4]. Scholars have offered several explanations to understand the ubiquity of business groups. Among others, the institutional theory-based explanation, premised on the three interrelated conceptions of (1) institutional voids, (2) market failure, and (3) the internal market, has enjoyed wide currency [5,6]. This explanation holds that business groups fill or circumvent institutional voids and resultant missing or underdeveloped external markets conventionally observed in underdeveloped or emerging economies by creating the internal market from which they extract the benefits exclusively. Because standalone firms cannot access this internal market, group-affiliated firms are thought to enjoy competitive advantage over standalone firms. As such, this explanation draws on the relative efficiency of the internal market over the external market. We call this explanation “the internal market conjecture” to put added emphasis on the internal market in developing our theory.

Often neglected, however, is that this logic can go the other way around: business groups can lose advantage if the external market becomes more efficient than the internal one. In line with this, some scholars predict that business groups’ argued benefits disappear or reverse themselves into liabilities in advanced economies with well-developed institutions and efficient external markets [5,7,8]. It, therefore, is inferred that the competitive advantage enjoyed by business groups does not stay invariable but changes according to factors determining this relative efficiency, such as institutional advancement or organizational innovation. Exploring such determinants, then, can add much to our understanding of business group functioning and performance. Nevertheless, research attempts along this line have been sparse.

To redress this oversight, we delve into these determinants by drawing on the conception of the tradability of goods that occupies an essential spot in the resource-based view. The resource-based view reveals that certain productive assets are inherently non-tradable on the external market due to human beings’ bounded rationality, which often underlies, smears, or translates into social complexity, causal ambiguity, and information and behavioral uncertainties [9,10,11,12,13]. The most widely researched non-tradable assets in the strategic management literature are intangible assets such as tacit knowledge, organizational routines, and capabilities [11]. This non-tradability causes the external markets for intangible assets to fail; their market is likely to be missing or inefficient if they exist [11,14]. So viewed, intangible assets seem to tip the scales of relative efficiency in favor of the internal market.

It is worth emphasizing here that business groups’ internal market can ease, if not eliminate, the non-tradability of intangible assets via their distinctive organizational mechanisms undergirded by group identity, solidarity, trust, shared organizational architecture, and enhanced communicability [15]. In other words, intangible assets are enabled to be exchanged, shared, and transferred across firm boundaries within business groups. Inasmuch as business groups lessen the non-tradability of the valuable intangible assets, their internal market can fare better than the external market, offering competitive advantage to affiliate firms over standalone firms.

This study focuses on organizational capabilities among the intangible assets that are valuable but less tradable on the external market. There are theoretical and empirical agreements that organizational capabilities are one of the key organizational assets bringing about sustainable competitive advantage [9,11,16,17,18,19,20]. Broadly defined as organizational capacities to achieve new resource combinations and configurations [9,21], organizational capabilities function as organizational templates or behavioral patterns to improve production efficiency. At the same time, organizational capabilities manifest non-tradability as they are less codable and articulable, causally uncertain, socially complex and embedded in the organizational process and social interactional pattern among employees, and context-specific [13,22,23]. Unsurprisingly, therefore, no organized markets are known to exist for organizational capabilities [11,19,24,25]. On balance, we hypothesize that business group affiliation enhances a firm’s organizational capabilities as business groups exclusively provide affiliate firms with an efficient internal market for organizational capabilities. We also offer two boundary conditions that supposedly alter this effect of group affiliation on organizational capabilities: prior organizational capabilities and firm age.

We develop and test our theory in the empirical context of Korea during the periods between 2003 and 2016. Korea provides a proper setting for two reasons. For one, there is a preponderance of business groups in Korea, and they, particularly Chaebol, have been extensively studied, offering valuable opportunities for cross-validation. For another, Korea is one of the most innovative countries allowing technological capability, our operational choice of organizational capabilities, to play a crucial role in successful competition.

We test our theory with carefully chosen econometric techniques. For the measurement of organizational capabilities, we employ the true fixed-effects stochastic frontier estimator [26,27,28]. Stochastic frontier estimation is widely accepted as an appropriate method for measuring organizational capabilities as they are conceptualized by strategy scholars as an efficiency with which to transform inputs into outputs [29,30,31]. Even so, prior studies relied mainly on the simple cross-sectional or random-effects estimators premised on unrealistically simplified assumptions, which renders their estimates inconsistent. Since several feasible estimators of the true fixed effects model have been recently developed [32], this study benefits from this cutting-edge technique for consistent estimation. For the regression analysis, we adopt the Arellano–Bond dynamic panel generalized method of moments (GMM) estimator [33]. This estimator can address endogeneity stemming from unobserved heterogeneity, partial adjustment, and reverse causality permeating the study of business group affiliation [34]. Using these advanced econometric techniques, we confirm that business group affiliation is positively associated with technological capability, one form of organizational capabilities. We also find that prior technological capability strengthens the positive effect of group affiliation on current technological capability, reflective of the importance of absorptive capacity [35]

We contribute to the business group literature in several ways. First, we extend the internal market conjecture, the most widely accepted view of business groups [6], by exploring its boundary condition in association with the relative efficiency. Underscoring that the external market for intangible assets suffers from non-tradability, we put forth the conditions under which business groups can sustain their presence and growth. By implication, our study also offers a clue to the question of “why do business groups continue to prosper in the advanced economies?”, one important theoretical puzzle in the business group literature [1]. Second, we add to the literature by presenting advanced empirical strategies for the analysis of organizational capabilities and business group affiliation. Whereas various kinds of potential endogeneity arise from fixed effects, partial adjustment, and reverse causality, virtually no attempts have been made thus far to relieve these endogeneity concerns. By using the true-fixed effects stochastic frontier estimator and the Arellano–Bond GMM estimator, we offer more reliable estimates for statistical inference.

2. Theory and Hypotheses

Why do business groups exist? Observing their ubiquity as well as economic and political significance, scholars have wrestled with this ontological question for about four decades since Leff [36] first brought it to attention. Perhaps the first and most widely accepted explanation is that business groups are a microeconomic response to institutional voids and market failure [3,36]. Specifically, it conceptualizes business groups as an organizational arrangement purported to fill the institutional voids and address market failure through the internal markets created and shared by group-affiliated firms; business groups function as a value-creating quasi-intermediary for missing markets for factors of input for production [5,6]. In contrast, standalone firms have no alternative but to count on the underdeveloped external market. In the worst scenario in which the markets for the needed resources do not even exist, they merely subsist with no means left for tapping the requisite resources. Therefore, in countries deficient in advanced institutions and well-developed external markets, group-affiliated firms are anticipated to outperform standalone firms. Note that this explanation postulates three interwoven conceptions: institutional voids, market failure, and the internal market. We herein call this the internal market conjecture to highlight the role of the internal market.

However, this internal market conjecture has one theoretical boundary condition that ensures the superior efficiency of the internal market vis-à-vis the external market: institutional voids and market failure. Absent this condition, business groups will lose the putative economic advantage or may even fall victim to the inefficiency of the internal market derived from value-destroying pathologies such as mutual insurance strategy [6,37,38] and principal-principal conflicts [3,7,39]. Considering this, some scholars even have gone so far as to foretell the eventual dismantlement of business groups [5,7,8].

Out of tune with this conjecture, however, research yields a mixed bag of results, failing to lend general support to the prediction that business groups’ economic advantage dissipates in advanced economies [3,6,40]. Carney and colleagues [1] even run counter to the prediction by providing evidence that business group affiliates in countries with the near-perfect development of institutions, such as Singapore and Sweden, outperform standalone firms. From the internal market conjecture viewpoint, this contradiction poses a non-trivial puzzle [41,42]. To address this puzzle, we diverge from the view that takes institutions as a sole determinant of the relative efficiency and put intangible assets on the table instead. Doing this requires us to discuss first why the external market fails from the institutional economics perspective.

2.1. Institutions, Transaction Costs, and Market Failure

Douglass North, one of the prominent figures of the institutional theory, views institutions as “the rules of the game in a society” or “a guide to human interactions” that clarifies what behaviors are allowed or disallowed [14] (p. 3). According to him, institutions are a gestalt of three complementary interrelated elements: informal constraints, formal constraints, and voluntary organizations. Informal constraints lay the social foundations for behaviors such as social codes of conduct, norms, customs, conventions, traditions, and the like; formal constraints are formalized, written rules such as property rights and are closely related to the entire system of the judicial process; and voluntary organizations, as a third party (e.g., intermediaries), assist the informal and formal constraints in achieving the institutional aims, i.e., governing human behaviors.

From the economic system perspective, well-developed institutions of a country give rise to efficiently functioning external markets by diminishing transaction costs [14]. Transaction costs comprise two different types. One is the measurement costs or “the costs of measuring the valuable attributes of what is being exchanged” [14] (p. 27) that arise as a result of ex-ante information asymmetry between exchange parties compounded by the cognitive limit of human beings. High measurement costs interfere with accurate pricing, rendering the external market imperfect [43] and decreasing the likelihood of exchanges occurring on the external market. The other is enforcement costs or “the costs of protecting rights and policing and enforcing agreements” [14] (p. 27). Costs of this sort typically arise from ex-post behavioral uncertainties or opportunism of the parties involved.

A well-established institutional infrastructure efficaciously reduces both costs. Informal and formal constraints drive down the net benefit from opportunistic behaviors by imposing severe penalties along the social (i.e., informal) and legal (i.e., formal) dimensions. Under advanced institutions, social and legal sanctions are enforced with less cost, such that any deviant behaviors (or behavioral uncertainties), once detected, are effortlessly punished. Further, any attempt to deceive the exchange party by concealing or distorting information will also be penalized once revealed, which lowers the measurement costs. Likewise, voluntary organizations such as intermediaries help decrease both costs. Intermediaries offer such valuable services as price setting, match-making, and guaranteeing and monitoring [44]. In a sense, measurement costs and pricing decisions are delegated to intermediaries with extensive information and specialty and experience in pricing.

Taken together, to the extent that a country’s institutions are immature and underdeveloped, the transaction costs will arguably heighten, putting a drag on external market efficiency [6]. Accordingly, economic exchanges and activities will take place increasingly less in the external markets, reinforcing firms’ tendency to place their economic activities inside the firm boundary. Naturally, then, the number of market participants for exchange will decrease, which again raises transaction costs [45]. A vicious circle of this sort goes on until an equilibrium is reached, at which point just a few market participants are left. To sum, in the presence of the institutional voids, the external markets fail, whereas business groups that fill the voids thrive. Equivalently, in the absence of institutional voids, the external markets gravitate toward perfection, driving out business groups. This logic is at the heart of the prediction that business groups will perish or disaggregate in advanced economies with near-perfect institutional development [5].

2.2. Intangible Assets, Market Failure, and Business Groups

What has mostly gone unnoticed in this prediction is the recognition that not every external market is the same in its potential to reach the state of the perfect and complete market [9,20,46]. The external market for intangible assets is one example. As Diericks and Cool (1989) elucidated, intangible assets are not readily tradable on the external market, examples of which encompass corporate reputation [47], trust [25], customer loyalty [48], knowledge [22], and routine [19]. We henceforth zero in on organizational capabilities among others in part because they, as a source of sustainable competitive advantage, enjoy wide currency and practical significance in the strategic management literature [18,20,23] and in part because their inter-firm transactions, if possible, should entail severe information asymmetry that has a direct bearing on transaction costs and market failure.

Defined as “organizational routines by which firms achieve new resource configuration” [18], organizational capabilities serve as a kind of organizational templates or behavioral patterns and help the firms operate more efficiently without wasting organizational members’ cognitive resources. Arguably, the following two distinctive facets of organizational capabilities inhibit them from being readily traded on the external market [22]. First, organizational capabilities are tacit by nature [23]. In other words, it is difficult to articulate what organizational capabilities precisely are. Besides, it is also challenging to demarcate their exact boundaries as an item for exchange and thereby separate them from a firm up for sales on the external market. Figuratively speaking, an attempt to isolate an organizational capability embedded in organizational processes and social interactional patterns of employees is akin to an attempt to uproot a plant that takes deep root, which is next to impossible without losing some lateral roots and root hairs that are unobservable from above the ground.

Second, they are socially complex [18,21,49]. A capability is developed and engraved by a group of people through repeated interactions and collaborative trial-and-error processes in quest of the optimal behavioral templates or patterns [50]. By implication, their final outcome tends to come into being by happenstance or luck rather than out of deliberate cognitive calculation and planned decision-making. That is, organizational capabilities are (1) causally uncertain and ambiguous [51] and (2) firm(or context)-specific [9,17]. Their precise replication in terms of functionality and economic values is next to impossible.

These two features of organizational capabilities translate into measurement and enforcement costs. Their tacit nature and social complexity prevent sellers and buyers from doing accurate pricing due to the inarticulability, causal ambiguity, and context-dependency; accordingly, the external market for organizational capabilities inherently confronts substantial information uncertainty leading to market failure [24]. Institutions are not capable of addressing this problem irrespective of how advanced they are, given that they, as “a guide to human interactions” [14] (p. 3), do not develop so much to overcome the inherent cognitive limits of human beings as to reduce behavioral uncertainties and their unfavorable consequences [52]. Moreover, enforcement costs substantially rise in the context of organizational capabilities transfer as organizational capabilities are generally firm-specific and, therefore, not guaranteed to function the same way as in the selling firm; their values are indeterminate at best. Such variability makes intended deviant behavior and innocent behavior indistinguishable, sending enforcement costs even higher. Consequently, the external market for intangible assets in general and organizational capabilities in particular is ordinarily missing regardless of institutional advancements and is likely to be inefficient and incomplete even if it happens to exist [11].

We argue that all these problems may be relieved, if not fully addressed, within the business group boundary. Notably, the crux of all these problems is uncertainties about the transfer of property rights [53,54,55,56] and the resulting redistribution of values of the goods or services that cannot be addressed even by institutions [14]. The value of a seller’s good remains uncertain not only to prospective buyers but also to the seller itself. In effect, these uncertainties matter less to business groups. Defined as “sets of legally separate firms bound together in persistent formal and/or informal ways” [15] (p. 429), business groups are de facto a single entity sharing identity and destiny as well [15]; therefore their objective function lies more in the betterment of joint utility than of an individual firm’s utility [37,38]. When it comes to inter-affiliate transactions, a specific affiliate firm’s gain or loss is less likely put on the table as long as its business group in its entirety gets better off as a result. So, any welfare-improving transactions that would have been discouraged in the external market are encouraged within the business group boundary if the business group’s joint utility improves. In a sense, business groups’ maximizing principle of this kind is interpreted to have the potential to achieve the welfare maximum by relaxing the constraint on Pareto improvement that does not necessarily lead to the social welfare maximum.

Business groups also have other complementary organizational mechanisms through which to underpin and encourage transactions of the sort discussed above. First, all affiliate firms of a business group share a sense of group identity [15]. To an affiliate firm, the other affiliate firms are the ones to live with and prosper together rather than compete against. An affiliate firm’s contribution to another affiliate firm in such forms of bailout, equity investment, or lending will be rewarded directly by the firm or indirectly by the other affiliate firms immediately or later on. This generalized reciprocity, accompanied by an extended time horizon of exchange, weakens the win-or-lose mentality and emboldens an affiliate firm to accept any probable short-term loss from exchanging organizational capabilities with other affiliate firms [57,58]. Hence, measurement costs become less significant. Second, such a shared identity, oneness, and collaborative mindset engender inter-affiliate trust. Trust, one elemental form of social capital, is regarded as one effective antidote to, or governance mechanisms for, behavioral uncertainties and opportunism [59,60,61,62,63,64] and hence reduces enforcement costs.

Last but not least, business groups share organizational architecture or infrastructure for the transfer of knowledge and the exchange of ideas. Business groups come into being through a series of setting up new businesses [49,65]. In so doing, the generic template for organizational architecture that business groups have adopted thus far is likely to be reused for new ventures [66]. Besides, continued interactions and communications with other affiliate firms offer the new businesses the opportunity to understand and buy into the group-wide culture, norms, codes, language, vocabulary, organizational structure and processes, and practices. The end result is an increased homogeneity not just in the way they work alone but in the way they interface with other affiliate firms [67], which lays the foundation or infrastructure for the efficient exchange and transfer of know-how or capabilities [22]. This sort of shared infrastructure for communication can mitigate ex-ante uncertainties of values of goods to be exchanged (i.e., measurement costs) and ex-post behavioral uncertainties of the exchange parties involved (i.e., enforcement costs).

Taken together, we maintain that the internal market of business groups can substitute for missing or ill-functioning external markets for organizational capabilities. Stated differently, the relative efficiency of the internal market vis-à-vis the external market is achieved here. Transactions of organizational capabilities in the internal market could benefit affiliate firms on average by reducing the deadweight loss incurred if the affiliate firms had gone solely after the external market. In contrast, standalone firms have no alternative but to bear the deadweight loss. It is noteworthy here that organizational capabilities, similar to other intangible assets, are a non-rival good [25]. An affiliate firm’s organizational capabilities will not lose their value if another affiliate firm simultaneously uses them as long as it is not a direct rival firm. This non-rivalry generally holds in the BG context. So, there is little to lose for affiliate firms but much to gain from the inter-affiliate transactions of organizational capabilities [13,68], which propels the internal market to be a vibrant venue for transacting organizational capabilities. Because such transactions of organizational capabilities necessarily accompany their learning [22,23], affiliate firms’ organizational capabilities will improve and be superior to those of standalone firms (Admittedly, there are also costs to business group affiliation such as agency problems and potentially value-destroying mutual insurance practices mostly stemming from the diverging interest of the ultimate owner of business groups. However, it is worthwhile noting that our theory focuses on the functioning of the internal market for intangible assets that do not confer any immediate gain on the owner at the expense of the other shareholders owing to the non-rival character of intangible assets and modest marginal costs of their sharing. Accordingly, the costs identified by the literature are less likely to materialize in our theoretical context) Thus, we hypothesize:

Hypothesis H1.

Business group affiliation is positively associated with organizational capabilities.

2.3. Moderating Effects of Prior Organizational Capabilities and Firm Age

2.3.1. Prior Organizational Capabilities

Not all firms are equal in terms of their organizational capabilities. Organizational capabilities are an outcome of a firm’s path-dependent process of organizing activities [11,19,69], whether emergent or deliberately planned. An unequal initial condition or heterogeneous resource endowments drive a firm’s internal development process to end up with different outcomes by virtue of the path-dependent nature; consequently, firm capabilities unavoidably grow dissimilar to one another [10,19,70,71]. These heterogeneous capabilities, however, also serve as a guide for affiliate firms to identify and acquire the needed capabilities from other affiliate firms. Underlying this logic is the notion of learning ability and absorptive capacity [35]. As Cohen and Levinthal pointed out, “the ability to evaluate and utilize outside knowledge is largely a function of the level of prior related knowledge” [35] (p. 128). In other words, to better scan, recognize, absorb, and acquire requisite organizational capabilities from other affiliate firms, a firm should have accumulated organizational capabilities in place as an absorptive capacity [72]. Stated differently, the prior organizational capabilities determine the ability to scan and acquire needed organizational capabilities from other affiliate firms. Thus, we hypothesize:

Hypothesis H2.

The main relationship between group affiliation and organizational capabilities is moderated by the prior organizational capabilities, such that the positive relationship becomes stronger as the prior capabilities increase.

2.3.2. Firm Age

Our theory is that business groups can provide affiliate firms with the internal market for organizational capabilities unavailable elsewhere. However, as the preceding discussion implies, gaining access to the internal market is one thing; extracting the argued benefit from it is another. A necessary condition for an affiliate firm to acquire any required organizational capabilities from the internal market or affiliate firms is that its knowledge-sharing interface be consistent with that of its affiliate firms, the donors of organizational capabilities. It is notable here that affiliate firms’ knowledge-sharing interfaces as a whole constitute the knowledge-sharing infrastructure of business groups in that it is a gestalt of information-sharing and communications interfaces, cultural and incentive systems, and social relationships conducive to voluntary collaboration and situated learning for joint utility [22,73].

Every firm goes through a sequence of development phases over time [71,74]. In its entire life cycle, a firm establishes, develops, and eventually stabilizes its organizational architecture or a set of internal structural elements that undergird its operations [75]. Correspondingly, an affiliate firm in the early stage of development needs to set up the organizational structure and functioning mechanisms guided by the shared group-level templates [49] along various dimensions of authority and responsibility, communication and interaction network, standard operating procedures, organizational routines, boundary-spanning, and the like. So developed structural elements and functioning mechanisms guide intra-organizational interactions and channel and promote inter-affiliate communications, engendering knowledge-sharing routines and communication interfaces. When an affiliate firm is in an inchoate stage, its knowledge-sharing routines and communication interfaces are unlikely to be developed fully. As it ages, however, these become established and stabilized in alignment with those of other affiliate firms, enabling the affiliate firm to readily acquire and assimilate organizational capabilities from other affiliate firms. Put differently, the older affiliate firms are more able to acquire needed organizational capabilities from other brethren firms. Taken together, we hypothesize:

Hypothesis H3.

The main relationship between group affiliation and organizational capabilities is moderated by firm age, such that the positive relationship becomes stronger as the firm ages.

3. Data and Methods

3.1. Sample

We chose Korea as our empirical context during the periods between 2003 and 2016. Korea offers a suitable setting for two reasons. On the one hand, business groups have been prevalent, serving as crucial agents for Korea’s economic development. Accordingly, large business groups, particularly Chaebol, have been extensively studied, offering valuable opportunities for cross-validation. On the other hand, Korea is one of the most innovative countries, allowing intangible assets to play a significant role in business competition. For instance, Korea has taken first place seven times in the last 10 years, according to the Bloomberg innovation index (https://www.bloomberg.com/news/articles/2021-02-03/south-korea-leads-world-in-innovation-u-s-drops-out-of-top-10 accessed on 10 August 2022).

Our sample consists of standalone firms and firms affiliated with large business groups (including Chaebols) annually designated by the Korea Fair Trade Commission. We decided to exclude small business groups because they tend to comprise small-sized firms whose accounting and market information is largely not publicly available, unnecessarily introducing the sample selection bias. We collected information on business group affiliation from the NICE information service and firm-level financial information from the Korea Investors Services (KIS), both of which are equivalent to the COMPUSTAT in the U.S. We also gathered patent information from the Korea Intellectual Property Rights Information Service (KIPRIS) database. We considered only auditory firms for data credibility and excluded firms whose financial or non-financial information is missing. We only included manufacturing firms partly for the sake of comparability and partly because technological capability, our focal construct (see below), is more meaningful for manufacturing firms. After this procedure, our data consisted of 1894 firms, of which 312 firms were from 65 business groups. Since we constructed unbalanced panel data from 2003 to 2016, our final data comprised 9238 firm-year observations.

3.2. Dependent Variable

Technological capability. Among various organizational capabilities, we herein chose to focus on technological capability because it has attracted sustained scholarly attention [31,73,74] and plays a crucial role, a fortiori, in advanced economies. Following prior literature [29,30,31], we operationalized a firm’s technological capability using stochastic frontier estimation [76,77]. In keeping with the Cobb–Douglass production function, we put forward the following transformation function of technology:

where technology outcomes are the number of patents granted, technology stock is the cumulative number of patents granted in the past 5 years, research and development (R&D) expenditure is the cumulative amount of R&D expenditure in the past 5 years, and employees are the number of employees.

In this regard, technological capability is conceived as a transformation efficiency from technology input into technology output. For the calculation of cumulative amounts, we employed a Koyck lag structure with a diminishing weight, 0.4 (For robustness check, we also re-estimated the model using 0.5 and found a similar pattern), into the past, following Dutta and colleagues [30]. This function is translated into the following econometric specification:

where is log output, is a vector of inputs, are iid , and are iid (i.e., half-normal).

Note that this model is the fixed-effects one due to the term that represents a firm’s unobserved heterogeneity or fixed effects [26,27,28,32]. Given that this model is non-linear, its estimation relies on the maximum likelihood estimation. However, this non-linearity poses a serious difficulty in estimation because any linear differencing operations such as group demeaning cannot purge the fixed effects. Alternatively, a brute-force approach likely gives rise to the infamous incidental parameters problem [27,77,78]. Fortunately, several breakthroughs have been made recently in addressing this problem on the basis of the marginal maximum likelihood within estimator [26], the marginal maximum likelihood first-difference estimator [26,32], and the marginal maximum simulated likelihood estimator [32]. In this study, we employed Chen and colleagues’ [26] marginal maximum likelihood within estimator to estimate the true fixed-effects stochastic frontier model. For this, we used the sftfe command with “within,” “robust,” and “hnormal” options specified [79] in Stata [80].

3.3. Independent Variable

Business group affiliation. Business groups are generally defined as “sets of legally independent firms bound together via formal/informal ties” [15] (p. 429). While there are various types of ties that bind the firms, equity ties are the most widely used basis on which to identify business groups [34,81]. So, if two or more firms are tied through equity ownership, they constitute a business group. We collected equity relations of all the audited firms from the NICE information. We operationalized business group affiliation as a dummy variable that is coded as one if a firm is affiliated with a business group and is coded as zero otherwise [82].

3.4. Moderating Variables

We used two moderators: a firm’s (1) prior technological capability and (2) age. The prior technological capability was measured as a 1-year lagged value of the firm’s technological capability. Age was operationalized as the current year minus the firm’s founding year. Then, we took a natural logarithm.

3.5. Control Variables

Firm-level attributes. As R&D and advertising resources can influence technological capability, we controlled for R&D intensity and advertising intensity, which were measured as R&D and advertising expenditure divided by sales, respectively [82,83]. Moreover, organizational slacks are thought to regulate a firm’s search behavior and thereby technological capability. So, we included two organizational slack variables: liquidity and leverage [84]. Following prior literature, we operationalized liquidity as the current ratio or current assets divided by current liabilities and leverage as the debt-to-equity ratio or total debt divided by equity [85]. Finally, we included sales to control for the size effect, where sales were measured as the natural logarithm of sales in thousands of KRW. All the firm-level control variables except for prior technological capability were measured at time t.

Macro-level attributes. To control for year-specific macroeconomic exogenous shocks, we inserted year dummies. This inclusion is essential to our model because the estimation technique we chose requires that errors be uncorrelated across cross-sectional units [86]. We did not include any time-constant variables or fixed-effects since our estimation technique expunges them automatically as detailed below.

3.6. Estimation Technique

Our model may suffer from endogeneity arising from fixed-effects, partial adjustment, and reverse causality. To address this problem, we modeled our theoretical process as follows:

where represents technology capability, represents a vector of covariates for firm at time , represents the fixed effects or unobserved heterogeneity for firm , represents the random disturbance, and represents the rate of partial adjustment process that lies in the open interval of .

It is notable here that although our DV, technological capability, is bounded between 0 and 1, this is a natural outgrowth from the stochastic frontier estimation as detailed above, not a symptom of censoring or truncation that needs a special econometric treatment such as tobit regression [77]. So, using a linear regression model is appropriate and even preferable in our case (for more detail, refer to) [87].

Given this, it is evident that any chosen estimation technique should be able to address the three sources of endogeneity. First, the estimation technique should handle the unobserved heterogeneity [78] (nonetheless, this is not so much a drawback as an advantage to correct statistical bias from it because addressing the problem of unobserved heterogeneity is difficult in cross-sectional data). Second, the partial adjustment process reflected in the use of the lagged dependent variable as a control variable incurs endogeneity by construction if the first-differencing procedure is chosen [88,89]. Third, this model is likely to suffer from reverse causality or winner-picking [34]. In the analysis of the causal relationship from an ownership variable (i.e., group affiliation in our study) to an economic outcome, the central econometric concern is reverse causality [90,91]. Unless reverse causality is controlled for, we cannot rule out the possibility that an economic outcome causes business group affiliation, not the other way around [77,92]. As a result, coefficient estimates become biased. Even so, the prior literature on business group affiliation largely remained silent on reverse causality, with a notable exception of [34], rendering the empirical findings less reliable [89].

We addressed these concerns using the Arellano–Bond dynamic panel estimator [33]. This estimator deals with unobserved heterogeneity (i.e., fixed effects) by using first-differencing or orthogonal deviation. Further, it controls for endogeneity detailed above by relying on the generalized method of moments (GMM) [88]. Specifically, this estimator instruments endogenous variables with predetermined as well as exogenous variables. Not just exogenous variables such as macroeconomic time effects but also the lagged terms of covariates can serve as valid instruments as long as error terms are not auto-correlated [33,93,94,95,96,97,98]. For the estimation, the Arellano–Bond estimator uses sample moment conditions (or moment restrictions) from instruments, the number of which is generally greater than the number of parameters to be estimated, i.e., over-identified. Since all the moment conditions cannot be met at once, the generalized method of moments (GMM) chooses a solution that minimizes the overall deviations from the orthogonality [99,100]. To control for heteroskedasticity, we report robust standard errors. For estimation, we used the xtabond2 command [86] in STATA 15 [80].

4. Results

Table 1 exhibits descriptive statistics and correlations for all variables. To eliminate non-essential collinearity, all variables used in the interactions were mean-centered [101]. However, their descriptive statistics are reported in their original values for ease of interpretation. To assess the multicollinearity, we calculated variance inflation factors (VIFs). The largest VIF was far below 10 (about 4.2), with the mean VIF being around 2.3. Thus, the concern about multicollinearity was modest.

Table 1.

Descriptive statistics and correlation matrix a,b.

Table 2 presents the Arellano–Bond GMM estimates for technological capability. As with other dynamic panel GMM estimates, the Arellano–Bond estimates should pass a battery of validity tests to be considered consistent. First, the Arellano–Bond (1991) test for AR(2) demonstrated no second-order autocorrelation of residuals (i.e., AR(2)) in all models. In the presence of AR(2), the lagged values are not guaranteed to be valid instruments, however long lags you take. Second, Hansen’s J statistic is insignificant in all models, indicating the joint validity of instruments as a whole. We also confirmed that all instrument groups were valid according to the difference-in-Hansen test. This batch of specification tests suggests that our estimates are consistent, i.e., safe from endogeneity [86,88,89]. Finally, the number of instruments used is far below the number of cross-sectional units, indicating no symptom of the “too many instruments” problem that weakens Hansen’s J test [86,102].

Table 2.

Arellano–Bond GMM estimates for technological capability a,b,c.

Model 1 is a baseline model that includes control variables only. As expected, the coefficient of prior technological capability is strongly significant, indicative of the partial adjustment process. The result that the debt-to-equity ratio is negative and significant is again consistent with our expectation [85]. Sales have a strong positive effect on technological capability, but, interestingly, R&D and advertising intensity have no effects.

Model 2 inserts business group affiliation, our focal variable; model 3 introduces prior technological capability as a moderator of the main relationship between business group affiliation and technological capability; model 4 inserts firm age as another moderator of the main relationship; and model 5 inserts all the variables at once. According to the results, Hypothesis H1 is supported (β = 0.131, p < 0.001). Thus, we found that business group affiliation increases technological capability. Hypothesis H2 is also supported (β = 0.277 at p < 0.05 in model 3; β = 0.276 at p < 0.001 in model 5). So, the positive effect of business group affiliation increases with an affiliate firm’s prior technological capability. However, we failed to find support for Hypothesis H3, although the coefficient’s sign is in the predicted direction. Thus, firm age has no moderating effect on the theoretical process we put forward. In models 3 and 5, the coefficients of business group affiliation lose significance, suggesting that the effect of business group affiliation varies contingent on the previous technological capability.

In summary, we found strong support for our hypotheses hinged upon the relative efficiency of the business group’s internal market for intangible assets. The empirical results are consistent with the predicted positive relationship between business group affiliation and technological capability (i.e., Hypothesis H1). Put another way, if a firm is affiliated with a business group, its technological capability excels that of standalone firms. At the same time, this positive effect of business group affiliation strengthens as the prior technological capability of the affiliate firm heightens (i.e., Hypothesis H2). This finding suggests that the prior capability serves as and stands for an absorptive capacity or the ability to learn from other affiliate firms.

Post-Hoc Analysis

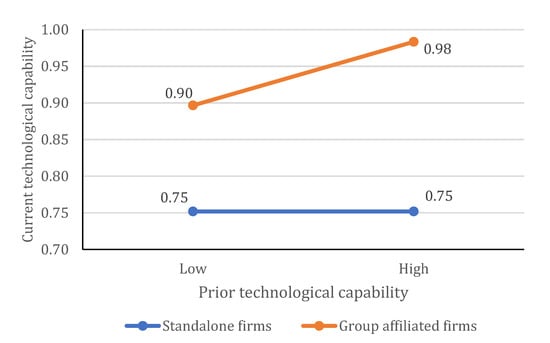

To better understand the practical implication of the moderating effect predicted by Hypothesis H2 in our sample, we offer a graph of the interaction of business group affiliation with prior technological capability in Figure 1 in which we used values one standard deviation above and below the mean for each interacting variable. In the graph, the moderator, prior technological capability, noticeably shifts the relationship in the predicted direction within the data range of our sample.

Figure 1.

Moderation of prior technological capability on the effect of business group affiliation.

5. Discussions and Conclusions

Business groups have been regarded as crucial economic agents, attracting considerable scholarly attention [3,15,103,104,105]. One dominant lens, among others, through which to analyze their ubiquity has been the internal market conjecture rooted in the institutional theory perspective. This conjecture predicts that business groups, a form of organizing economic activities, will disappear when institutions advance enough for the external market to be more efficient than the internal market [7,8,82]. However, research evidence shows no telltale sign of the waning significance of business groups [1,3,6,34,106]. Rather, business groups appear to showcase their prosperity even in advanced economies with near-perfect institutions, where business groups are believed to be eclipsed by the efficient external market [1,3,6,34,106]. This contradictory finding casts doubt on the validity of the internal market conjecture.

This study provides a clue to this contradiction by turning attention from the macro-level institutions to the micro-level organizational assets. Bringing into focus the non-tradability of intangible assets leading to the relative efficiency of the internal market over the external market, we show that business groups can beat the external market and thereby sustain their presence if they center around productive intangible assets and their exchanges among affiliate firms. In this regard, this study offers an institution-free, micro-level explanation of how the internal market of business groups can outperform the external market. By implication, our study also offers an answer to “why do business groups continue to prosper in the advanced economies?”, one important theoretical puzzle in the business group literature.

Our study also found that an affiliate firm’s prior capability moderates the positive effect of business group affiliation. This finding indicates that not all affiliate firms are equally able to extract the benefit from business group affiliation; in other words, group affiliation benefits are not uniform but contingent on the affiliate firm’s attributes. This finding adds further evidence to the literature accentuating within-group heterogeneity [31,37,67,107,108]. Besides, our finding suggests that an affiliate firm’s age has no bearing on the exchange of capabilities within business groups. Therefore, we can infer that the template business groups use for creating new affiliate firms effectively and instantly sets up inter-affiliate interfaces for knowledge-sharing and communication, supposedly assisted by group-level social infrastructure.

Moreover, we empirically contribute to the literature by adopting the two advanced estimation techniques. For one, the literature on business group affiliation has remained silent about and turned a blind eye to the potential endogeneity concerns derived from the partial adjustment process of strategic choices, unobserved heterogeneity, and reverse causality (or winner-picking) [34]. This study addresses these concerns by adopting the Arellano–Bond GMM estimator that offers consistent estimates. Second, to the best of our knowledge, this is one of the first studies to employ the cutting-edge estimation technique for measuring organizational capabilities, the true fixed-effects stochastic frontier estimator [27] with the within marginal maximum likelihood [26]. Using these two advanced econometric techniques, we present statistically preferable ways to acquire consistent estimates for statistical inference.

Relatedly, prior studies that considered technological capability employed R&D intensity as a proxy for it [82,83]. However, R&D intensity cannot precisely capture technological capability as it is an input-based measure, whereas technological capability is conceptually an efficiency with which to transform input into output. Consequently, any inference based on the result from R&D intensity is unlikely to have a sound conceptual and operational basis and should be made with extreme caution.

Our study also holds practical implications for managers of business groups and affiliate firms not just in economies with near-perfect institutions but also in economies experiencing rapid institutional upgrades and market developments. As the institution theory-based perspective predicts, the comparative advantage of business groups may vanish if institutions advance and the market system improves enough as a result. Our study offers one way for managers of business groups to sustain their advantage over the external market in such an environment: to shift focus to non-tradable assets and promote their sharing and transactions across affiliate firms. Moreover, our study suggests that the benefit of access to the internal market for intangible assets and capabilities in particular is not symmetric but accrues more to the one with greater learning ability. So, managers of affiliate firms are advised to pay extra attention to cultivating absorptive capacity to better tap the internal market.

6. Limitations and Future Research

As with other studies, our study is not without limitations. First, this study used data from a single country. While using a single-country setting is suited to controlling for other confounders at the national level, such as institutional variance, the results can lose generalizability to some degree. As our theory hinged on an institution-free account of business group advantage should also hold in other countries, further research might benefit from cross-validating our findings using other country data. Second, we confined our analysis to large business groups to reduce the potential sample selection bias arising from missing data and observations. However, our theory may be subject to modification in small business groups, given that their internal market may function differently from large business groups’ internal market. For instance, it could be that social mechanisms such as solidarity, identity, moral economy, and mutual trust are more pronounced and stronger in small business groups due to shorter distances and increased interactions among affiliate firms [15,109]. We believe future research could benefit from corroborating our findings in small business groups. Finally, our theory focuses on identifying an institution-free condition under which business groups continue to prosper even with institutional advancements. However, it may well be that the extent to which the internal market for intangible assets is developed and utilized is smaller in emerging economies than in advanced economies because business groups arguably have less incentive to invest in and rely on intangible assets for competition in emerging economies fraught with market failure. Examining this possibility may extend our understanding by revealing potentially varying mental models and competitive strategies business groups take in reaction to institutional advancements.

Funding

This work was supported by the Ministry of Education of the Republic of Korea and the National Research Foundation of Korea (NRF-2019S1A5A8037686) and GIST Research Institute (GRI) grant funded by the GIST in 2022.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data will be made available on request from the corresponding author.

Acknowledgments

The author is grateful to Stephen Seokhyun Hwang at Hong Kong Baptist University for cogent comments on an earlier version of this paper.

Conflicts of Interest

The author declares no conflict of interest.

References

- Carney, M.; Gedajlovic, E.R.; Heugens, P.; Van Essen, M.; Van Oosterhout, J. Business Group Affiliation, Performance, Context, and Strategy: A Meta-Analysis. Acad. Manag. J. 2011, 54, 437–460. [Google Scholar] [CrossRef]

- Granovetter, M. Business Groups. In The Handbook of Economic Sociology; Smelser, N.J., Swedberg, R., Eds.; Princeton University Press: Princeton, NJ, USA, 1994; pp. 453–475. [Google Scholar]

- Khanna, T.; Yafeh, Y. Business Groups in Emerging Markets: Paragons or Parasites? J. Econ. Lit. 2007, 45, 331–372. [Google Scholar] [CrossRef]

- Yiu, D.W.; Lu, Y.; Bruton, G.D.; Hoskisson, R.E. Business Groups: An Integrated Model to Focus Future Research. J. Manag. Stud. 2007, 44, 1551–1579. [Google Scholar] [CrossRef]

- Khanna, T.; Palepu, K. The Future of Business Groups in Emerging Markets: Long-Run Evidence from Chile. Acad. Manag. J. 2000, 43, 268–285. [Google Scholar]

- Khanna, T.; Rivkin, J.W. Estimating the Performance Effects of Business Groups in Emerging Markets. Strateg. Manag. J. 2001, 22, 45–74. [Google Scholar] [CrossRef]

- Chang, S.J. The Rise and Fall of Chaebols: Financial Crisis and Transformation of Korean Business Groups; Cambridge University Press: Cambridge, UK, 2003. [Google Scholar]

- Khanna, T.; Palepu, K. The Right Way to Restructure Conglomerates in Emerging Markets—Response. Harv. Bus. Rev. 1999, 77, 195–196. [Google Scholar]

- Amit, R.; Schoemaker, P.J.H. Strategic Assets and Organizational Rent. Strateg. Manag. J. 1993, 14, 33–46. [Google Scholar] [CrossRef]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Dierickx, I.; Cool, K. Asset Stock Accumulation and Sustainability of Competitive Advantage. Manag. Sci. 1989, 35, 1504–1511. [Google Scholar] [CrossRef]

- Peteraf, M.A. The Cornerstones of Competitive Advantage: A Resource-Based View. Strateg. Manag. J. 1993, 14, 179–191. [Google Scholar] [CrossRef]

- Szulanski, G. Exploring Internal Stickiness: Impediments to the Transfer of Best Practice within the Firm. Strateg. Manag. J. 1996, 17, 27–43. [Google Scholar] [CrossRef]

- North, D.C. Institutions, Institutional Change and Economic Performance; Cambridge University Press: Cambridge, UK, 1990. [Google Scholar]

- Granovetter, M. Business Groups and Social Organization. In The Handbook of Economic Sociology; Smelser, N.J., Swedberg, R., Eds.; Princeton University Press: Princeton, NJ, USA, 2005; pp. 429–450. [Google Scholar]

- Aral, S.; Weill, P. IT Assets, Organizational Capabilities, and Firm Performance: How Resource Allocations and Organizational Differences Explain Performance Variation. Organ. Sci. 2007, 18, 763–780. [Google Scholar] [CrossRef] [Green Version]

- Collis, D.J. Research Note: How Valuable Are Organizational Capabilities? Strateg. Manag. J. 1994, 15, 143–152. [Google Scholar] [CrossRef]

- Eisenhardt, K.M.; Martin, J.A. Dynamic Capabilities: What Are They? Strateg. Entrep. J. 2000, 21, 1105–1121. [Google Scholar] [CrossRef]

- Nelson, R.R.; Winter, S. An Evolutionary Theory of Economic Change; Harvard University Press: Cambridge, MA, USA, 1982. [Google Scholar]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic Capabilities and Strategic Management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Makadok, R. Toward a Synthesis of the Resource-Based and Dynamic-Capability Views of Rent Creation. Strateg. Manag. J. 2001, 22, 387–401. [Google Scholar] [CrossRef]

- Kogut, B.; Zander, U. Knowldege of the Firm, Combinative Capabilities, and the Replication of Technology. Organ. Sci. 1992, 3, 383–397. [Google Scholar] [CrossRef]

- Zollo, M.; Winter, S. Deliberate Learning and the Evolution of Dynamic Capabilities. Organ. Sci. 2002, 13, 339–351. [Google Scholar] [CrossRef]

- Aboody, D.; Lev, B. Information Asymmetry, R&D, and Insider Gains. J. Financ. 2000, 55, 2747–2766. [Google Scholar]

- Arrow, K.J. The Limits of Organization; WW Norton & Company: New York, NY, USA, 1974. [Google Scholar]

- Chen, Y.-Y.; Schmidt, P.; Wang, H.-J. Consistent Estimation of the Fixed Effects Stochastic Frontier Model. J. Econom. 2014, 181, 65–76. [Google Scholar] [CrossRef]

- Greene, W. Fixed and Random Effects in Stochastic Frontier Models. J. Product. Anal. 2005, 23, 7–32. [Google Scholar] [CrossRef]

- Greene, W. Reconsidering Heterogeneity in Panel Data Estimators of the Stochastic Frontier Model. J. Econom. 2005, 126, 269–303. [Google Scholar] [CrossRef]

- Dutta, S.; Narasimhan, O.; Rajiv, S. Success in High-Technology Markets: Is Marketing Capability Critical? Mark. Sci. 1999, 18, 547–568. [Google Scholar] [CrossRef] [Green Version]

- Dutta, S.; Narasimhan, O.M.; Rajiv, S. Conceptualizing and Measuring Capabilities: Methodology and Empirical Application. Strateg. Manag. J. 2005, 26, 277–285. [Google Scholar] [CrossRef]

- Mahmood, I.P.; Zhu, H.; Zajac, E.J. Where Can Capabilities Come from? Network Ties and Capability Acquisition in Business Groups. Strateg. Manag. J. 2011, 32, 820–848. [Google Scholar] [CrossRef]

- Belotti, F.; Ilardi, G. Consistent Inference in Fixed-Effects Stochastic Frontier Models. J. Econom. 2018, 202, 161–177. [Google Scholar] [CrossRef]

- Arellano, M.; Bond, S. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef]

- Belenzon, S.; Berkovitz, T. Innovation in Business Groups. Manag. Sci. 2010, 56, 519–535. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Absorptive Capacity: A New Perspective on Learning. Admin. Sci. Quart. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Leff, N.H. Industrial Organization and Entrepreneurship in Developing-Countries—Economic Groups. Econ. Dev. Cult. Change 1978, 26, 661–675. [Google Scholar] [CrossRef]

- Gerlach, M.L. Alliance Capitalism: The Social Organization of Japanese Business; University of California Press: Berkeley, CA, USA, 1992; ISBN 0520076885. [Google Scholar]

- Khanna, T.; Yafeh, Y. Business Groups and Risk Sharing around the World. J. Bus. 2005, 78, 301–340. [Google Scholar] [CrossRef]

- Claessens, S.; Djankov, S.; Fan, J.R.H.; Lang, L.H.P. Disentangling the Incentive and Entrenchment Effects of Large Shareholdings. J. Financ. 2002, 57, 2741–2771. [Google Scholar] [CrossRef]

- Carney, M.; Van Essen, M.; Estrin, S.; Shapiro, D. Business Groups Reconsidered: Beyond Paragons and Parasites. AMP 2018, 32, 493–516. [Google Scholar] [CrossRef] [Green Version]

- Purkayastha, A.; Kumar, V.; Lovallo, D. How Do Business Group Affiliated Firm in Emerging Markets Outperform Standalone Firms? A Knowledge-Based View. J. Knowl. Manag. 2022. ahead of print. [Google Scholar] [CrossRef]

- Gedefaw Birhanu, A.; Wezel, F.C. The Competitive Advantage of Affiliation with Business Groups in the Political Environment: Evidence from the Arab Spring. Strateg. Organ. 2022, 20, 389–411. [Google Scholar] [CrossRef]

- Barney, J.B. Strategic Factor Markets: Expectations, Luck, and Business Strategy. Manag. Sci. 1986, 32, 1231–1241. [Google Scholar] [CrossRef]

- Spulber, D.F. Market Microstructure and Intermediation. J. Econ. Perspect. 1996, 10, 135–152. [Google Scholar] [CrossRef]

- Williamson, O.E. The Economic Institutions of Capitalism; Free Press: New York, NY, USA, 1985. [Google Scholar]

- Caves, R.E. Industrial Organization, Corporate Strategy and Structure. J. Econ. Lit. 1980, 18, 64–92. [Google Scholar]

- Gao, C.; Zuzul, T.; Jones, G.; Khanna, T. Overcoming Institutional Voids: A Reputation-Based View of Long-Run Survival. Strateg. Manag. J. 2017, 38, 2147–2167. [Google Scholar] [CrossRef]

- Dick, A.S.; Basu, K. Customer Loyalty: Toward an Integrated Conceptual Framework. J. Acad. Mark. Sci. 1994, 22, 99–113. [Google Scholar] [CrossRef]

- Guillen, M.F. Business Groups in Emerging Economies: A Resource-Based View. Acad. Manag. J. 2000, 43, 362–380. [Google Scholar]

- Fleming, L.; Sorenson, O. Science as a Map in Technological Search. Strateg. Manag. J. 2004, 25, 909–928. [Google Scholar] [CrossRef]

- Lippman, S.A.; Rumelt, R.P. Uncertain Imitability: An Analysis of Interfirm Differences in Efficiency Under Competition. Bell J. Econ. 1982, 13, 418–438. [Google Scholar] [CrossRef]

- Scott, W.R. Institutions and Organizations, 2nd ed.; Sage Publications: Thousand Oaks, CA, USA, 2001; ISBN 0761920005. [Google Scholar]

- Groenewegen, J.; Spithoven, A.H.G.M.; Spithoven, A.; den Berg, A.V. Institutional Economics: An Introduction; Macmillan Education: London, UK, 2010; ISBN 978-0-230-55073-5. [Google Scholar]

- Hart, O. Economist’s Perspective on the Theory of the Firm, An. Colum. L. Rev. 1989, 89, 1757–1774. [Google Scholar] [CrossRef]

- Milgrom, P.; Roberts, J. Economics, Organization and Management; Prentice Hall: Upper Saddle River, NJ, USA, 1992. [Google Scholar]

- Voigt, S. Institutional Economics: An Introduction; Cambridge University Press: Cambridge, UK, 2019. [Google Scholar]

- Baker, W.E.; Bulkley, N. Paying It Forward vs. Rewarding Reputation: Mechanisms of Generalized Reciprocity. Organ. Sci. 2014, 25, 1493–1510. [Google Scholar] [CrossRef] [Green Version]

- Yamagishi, T.; Kiyonari, T. The Group as the Container of Generalized Reciprocity. Soc. Psychol. Q. 2000, 63, 116–132. [Google Scholar] [CrossRef]

- Adler, P.S. Market, Hierarchy, and Trust: The Knowledge Economy and the Future of Capitalism. Organ. Sci. 2001, 12, 215–234. [Google Scholar] [CrossRef]

- Adler, P.S.; Kwon, S.-W. Social Capital: Prospects for a New Concept. Acad. Manag. Rev. 2002, 27, 17–40. [Google Scholar] [CrossRef]

- Fukuyama, F. Trust: The Social Virtues and the Creation of Prosperity; Simon and Schuster: New York, NY, USA, 1996. [Google Scholar]

- Granovetter, M. Economic Action and Social Structure: A Theory of Embeddedness. Am. J. Sociol. 1985, 91, 481–510. [Google Scholar] [CrossRef]

- Uzzi, B. The Sources and Consequences of Embeddedness for the Economic Performance of Organizations: The Network Effect. Am. Sociol. Rev. 1996, 61, 674–698. [Google Scholar] [CrossRef]

- Uzzi, B. Social Structure and Competition in Interfirm Networks: The Paradox of Embeddedness. Admin. Sci. Quart. 1997, 42, 35–67. [Google Scholar] [CrossRef]

- Schmidt, T.; Braun, T.; Sydow, J. Copying Routines for New Venture Creation: How Replication Can Support Entrepreneurial Innovation. In Routine Dynamics in Action: Replication and Transformation (Research in the Sociology of Organizations, Vol. 61); Emerald Publishing Limited: Bingley, UK, 2019; pp. 55–78. [Google Scholar]

- Pentland, B.T.; Rueter, H.H. Organizational Routines as Grammars of Action. Adm. Sci. Q. 1994, 39, 484–510. [Google Scholar] [CrossRef]

- Chang, S.J.; Hong, J. How Much Does the Business Group Matter in Korea? Strateg. Manag. J. 2002, 23, 265–274. [Google Scholar] [CrossRef]

- Ghoshal, S.; Korine, H.; Szulanski, G. Interunit Communication in Multinational Corporations. Manag. Sci. 1994, 40, 96–110. [Google Scholar] [CrossRef]

- Feldman, M.S.; Pentland, B.T. Reconceptualizing Organizational Routines as a Source of Flexibility and Change. Adm. Sci. Q. 2003, 48, 94–118. [Google Scholar] [CrossRef] [Green Version]

- Hannan, M.T.; Freeman, J. Population Ecology of Organizations. Am. J. Sociol. 1977, 82, 929–964. [Google Scholar] [CrossRef]

- Stinchcombe, A.S. Organizations and Social Structure. In Handbook of Organizations; March, J.G., Ed.; RandMcNally: Chicago, IL, USA, 1965; pp. 153–193. [Google Scholar]

- Levinthal, D.A.; March, J.G. The Myopia of Learning. Strateg. Manag. J. 1993, 14, 95–112. [Google Scholar] [CrossRef]

- Lave, J.; Wenger, E. Situated Learning: Legitimate Peripheral Participation; Cambridge University Press: Cambridge, UK, 1991. [Google Scholar]

- Freeman, J.; Carroll, G.R.; Hannan, M.T. The Liability of Newness: Age Dependence in Organizational Death Rates. Am. Sociol. Rev. 1983, 48, 692–710. [Google Scholar] [CrossRef]

- Hill, C.W.; McShane, S.L. Principles of Management; McGraw-Hill/Irwin: New York, NY, USA, 2008. [Google Scholar]

- Mahmood, I.P.; Zheng, W.T. Whether and How: Effects of International Joint Ventures on Local Innovation in an Emerging Economy. Res. Policy 2009, 38, 1489–1503. [Google Scholar] [CrossRef]

- Greene, W.H. Econometric Analysis, 7th ed.; Prentice Hall: Boston, MA, USA, 2012; ISBN 0-13-139538-6. [Google Scholar]

- Wooldridge, J.M. Econometric Analysis of Cross Section and Panel Data, 2nd ed.; MIT Press: Cambridge, MA, USA, 2010; ISBN 9780262232586. [Google Scholar]

- Belotti, F.; Ilardi, G. sftfe: A Stata Command for Fixed-Effects Stochastic Frontier Models Estimation. In Proceedings of the Italian Stata Users’ Group Meetings 2014, Milan, Italy, 13 November 2014. [Google Scholar]

- StataCorp. Stata 15; StataCorp: College Station, TX, USA, 2017. [Google Scholar]

- Khanna, T.; Rivkin, J.W. Interorganizational Ties and Business Group Boundaries: Evidence from an Emerging Economy. Organ. Sci. 2006, 17, 333–352. [Google Scholar] [CrossRef]

- Chang, S.-J.; Chung, C.-N.; Mahmood, I.P. When and How Does Business Group Affiliation Promote Firm Innovation? A Tale of Two Emerging Economies. Organ. Sci. 2006, 17, 637–656. [Google Scholar] [CrossRef]

- Chatterjee, S.; Wernerfelt, B. The Link Between Resources and Type of Diversification: Theory and Evidence. Strateg. Manag. J. 1991, 12, 33–48. [Google Scholar] [CrossRef]

- Chang, S.J.; Hong, J. Economic Performance of Group-Affiliated Companies in Korea: Intragroup Resource Sharing and Internal Business Transactions. Acad. Manag. J. 2000, 43, 429–448. [Google Scholar]

- Greve, H.R. A Behavioral Theory of R&D Expenditures and Innovations: Evidence from Shipbuilding. Acad. Manag. J. 2003, 46, 685–702. [Google Scholar]

- Roodman, D. How to Do Xtabond2: An Introduction to Difference and System GMM in Stata. Stata J. 2009, 9, 86–136. [Google Scholar] [CrossRef]

- Angrist, J.D.; Pischke, J.-S. Mostly Harmless Econometrics; Princeton University Press: Princeton, NJ, USA, 2008. [Google Scholar]

- Arellano, M. Panel Data Econometrics; Advanced Texts in Econometrics; Oxford University Press: Oxford, UK; New York, NY, USA, 2003; ISBN 0199245282. [Google Scholar]

- Baltagi, B.H. Econometric Analysis of Panel Data, 4th ed.; John Wiley & Sons: Chichester, UK; Hoboken, NJ, USA, 2008; ISBN 0470518863. [Google Scholar]

- Almeida, H.; Park, S.Y.; Subrahmanyam, M.G.; Wolfenzon, D. The Structure and Formation of Business Groups: Evidence from Korean Chaebols. J. Financ. Econ. 2011, 99, 447–475. [Google Scholar] [CrossRef]

- Demsetz, H.; Lehn, K. The Structure of Corporate-Ownership—Causes and Consequences. J. Political Econ. 1985, 93, 1155–1177. [Google Scholar] [CrossRef]

- Wang, K.; Shailer, G. Ownership Concentration and Firm Performance in Emerging Markets: A Meta-Analysis. J. Econ. Surv. 2015, 29, 199–229. [Google Scholar] [CrossRef]

- Ahn, S.C.; Schmidt, P. Efficient Estimation of Models for Dynamic Panel-Data. J. Econom. 1995, 68, 5–27. [Google Scholar] [CrossRef]

- Ahn, S.C.; Schmidt, P. Efficient Estimation of Dynamic Panel Data Models: Alternative Assumptions and Simplified Estimation. J. Econom. 1997, 76, 309–321. [Google Scholar] [CrossRef]

- Anderson, T.W.; Hsiao, C. Estimation of Dynamic-Models with Error-Components. J. Am. Stat. Assoc. 1981, 76, 598–606. [Google Scholar] [CrossRef]

- Arellano, M.; Bover, O. Another Look at the Instrumental Variable Estimation of Error-Components Models. J. Econom. 1995, 68, 29–51. [Google Scholar] [CrossRef]

- Blundell, R.; Bond, S. Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. J. Econom. 1998, 87, 115–143. [Google Scholar] [CrossRef]

- Holtz-Eakin, D.; Newey, W.; Rosen, H.S. Estimating Vector Autoregressions with Panel Data. Econometrica 1988, 56, 1371–1395. [Google Scholar] [CrossRef]

- Hansen, L.P. Large Sample Properties of Generalized-Method of Moments Estimators. Econometrica 1982, 50, 1029–1054. [Google Scholar] [CrossRef]

- Hayashi, F. Econometrics; Princeton University Press: Princeton, NJ, USA, 2000; ISBN 0691010188. [Google Scholar]

- Cohen, J.; Cohen, P.; West, P.W.; Aiken, L.S. Applied Multiple Regression/Correlation Analysis for the Behavioral Sciences, 3rd ed.; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 2003. [Google Scholar]

- Roodman, D. A Note on the Theme of Too Many Instruments. Oxf. Bull. Econ. Stat. 2009, 71, 135–158. [Google Scholar] [CrossRef]

- Carney, M. Asian Business Groups: Context, Governance and Performance; Chandos Publishing: Oxford, UK, 2008. [Google Scholar]

- Colpan, A.M.; Hikino, T.; Lincoln, J.R. The Oxford Handbook of Business Groups; Oxford University Press: Oxford, UK, 2010; ISBN 978-0-19-955286-3. [Google Scholar]

- Orru, M.; Biggart, N.W.; Hamilton, G.G. The Economic Organization of East Asian Capitalism; Sage Publications: Thousand Oaks, CA, USA, 1997. [Google Scholar]

- Blanchard, P.; Huiban, J.-P.; Sevestre, P. R&D and Productivity in Corporate Groups: An Empirical Investigation Using a Panel of French Firms. Ann. Econ. Stat. 2005, 79/80, 461–485. [Google Scholar]

- Jin, K.; Park, C. Separation of Cash Flow and Voting Rights and Firm Performance in Large Family Business Groups in Korea. Corp. Gov. Int. Rev. 2015, 23, 434–451. [Google Scholar] [CrossRef]

- Jin, K.; Park, C.; Lee, J. Structural Positions within Business Group Equity Networks and Performance of Affiliate Firms. Acad. Manag. Proc. 2011, 2011, 1–6. [Google Scholar] [CrossRef]

- Gulati, R. Does Familiarity Breed Trust? The Implications of Repeated Ties for Contractual Choice in Alliances. Acad. Manag. J. 1995, 38, 85–112. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).