Organizational Factors Influencing the Sustainability Performance of Construction Organizations

Abstract

:1. Introduction

2. Literature Review

2.1. Organizational Sustainability

2.2. Sustainability Performance of Construction Organizations and Their Key Drivers

- What kind of organizational factors should construction organizations focus on in their efforts to improve different dimensions of sustainability performance?

- How could different factors collectively and interactively influence different dimensions of sustainability performance?

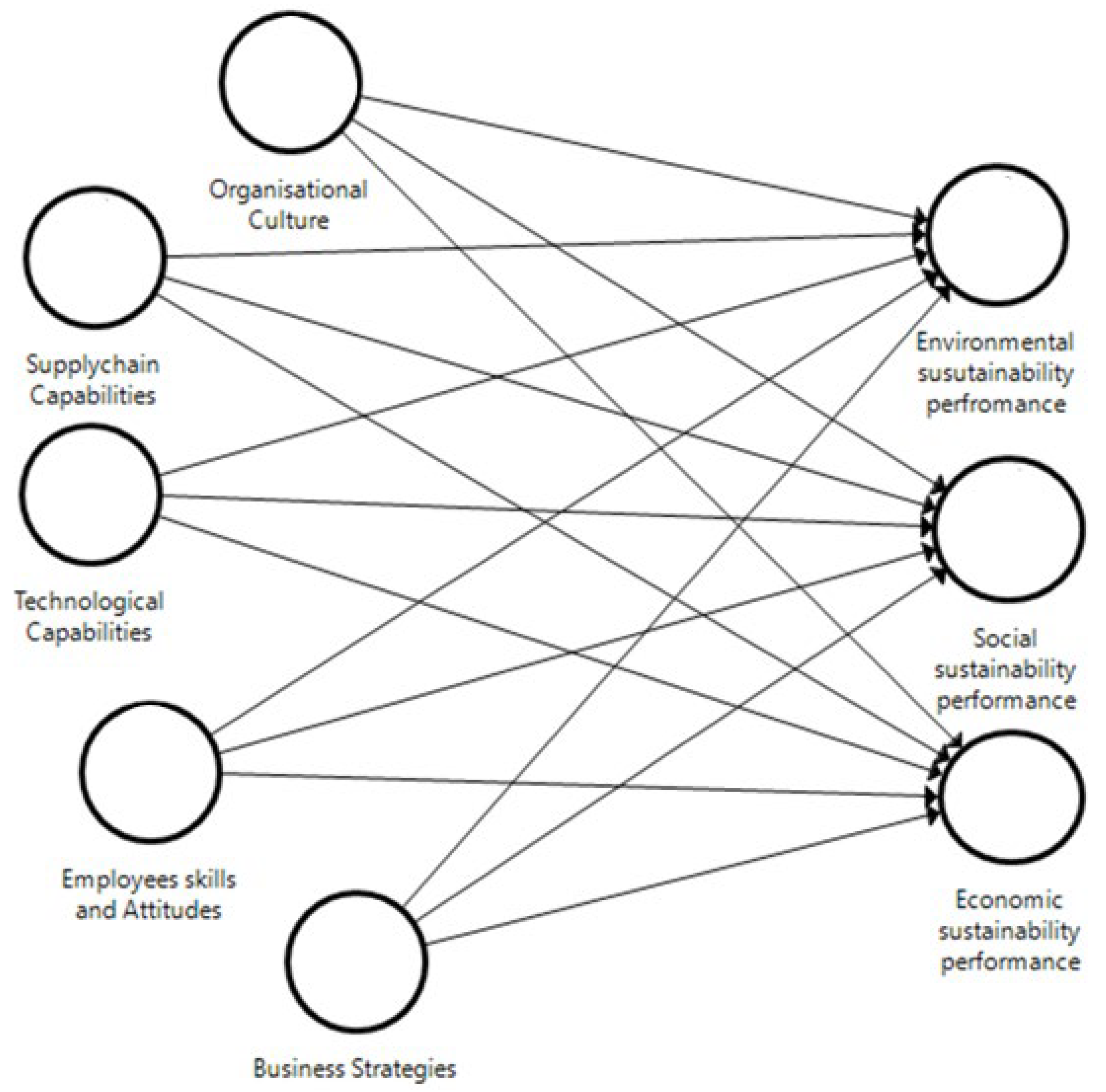

3. Theoretical Framework and Hypothesis Development

3.1. Resource-Based Theory (RBT)

3.1.1. Organizational Culture (OC)

3.1.2. Supply Chain Capabilities (SC)

3.1.3. Technological Capabilities (TC)

3.1.4. Employees’ Skills and Attitudes (ESA)

3.1.5. Business Strategies (BS)

4. Methodology

5. Results

5.1. Measurement Models

5.2. Structural Model

6. Discussions

6.1. Drivers of Environmental Sustainability Performance (ESP)

“… when a sustainability strategy is developed in collaboration with the CEO, General Managers of various departments, and external contractors, we could obtain a better result due to the buy-in from respective stakeholders …”[Respondent 42]

“We like to say we are just behind the cutting edge of current technology …”.[Respondent 09]

“The technological capabilities are something we are trying to establish as it makes performance reporting more efficient”.[Respondent R18]

“We pride ourselves on respectful relationships at all levels of the business and maintaining our strong reputation for fair dealing. We attract and retain high-caliber employees who share this culture. This allows us to be consistent and confident in the way we deliver projects”.[Respondents R09]

6.2. Drivers of Social Sustainability Performance (SSP)

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Australian Bureau of Statistics Report 2018; ABS: Canberra, Australia, 2018.

- Poon, C.S. Management and recycling of demolition waste in Hong Kong. Waste Manag. Res. 1997, 15, 561–572. [Google Scholar] [CrossRef]

- Shen, L.Y.; Zhang, Z.H. China’s urbanization challenging sustainable development. Int. J. Hous. Sci. Its Appl. 2002, 26, 181–193. [Google Scholar]

- Khalili, N.R.; Melaragno, W. Strategic Tools for Achieving Long-Term Sustainability. In Practical Sustainability; Palgrave Macmillan: New York, NY, USA, 2011; pp. 23–55. [Google Scholar]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Myers, D. A review of construction companies’ attitudes to sustainability. Constr. Manag. Econ. 2005, 23, 781–785. [Google Scholar] [CrossRef]

- Mills, F.T.; Glass, J. The Construction Design Manager’s Role in Delivering Sustainable Buildings. Arch. Eng. Des. Manag. 2009, 5, 75–90. [Google Scholar] [CrossRef]

- Jones, P.; Comfort, D.; Hillier, D. Corporate social responsibility and the UK construction industry. J. Corp. Real Estate 2006, 8, 134–150. [Google Scholar] [CrossRef] [Green Version]

- Afzal, F.; Lim, B.; Prasad, D. An Investigation of Corporate Approaches to Sustainability in the Construction Industry. Procedia Eng. 2017, 180, 202–210. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why companies go green: A model of ecological responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar]

- Linnenluecke, M.K.; Griffiths, A. Corporate sustainability and organizational culture. J. World Bus. 2010, 45, 357–366. [Google Scholar] [CrossRef]

- Epstein, M.J. Making Sustainability Work: Best Practices in Managing and Measuring Corporate Social, Environmental and Economic Impacts; Routledge: London, UK, 2018. [Google Scholar]

- Banerjee, S.B.; Iyer, E.S.; Kashyap, R.K. Corporate Environmentalism: Antecedents and Influence of Industry Type. J. Mark. 2003, 67, 106–122. [Google Scholar] [CrossRef]

- Robin, C.Y.; Poon, C. Cultural shift towards sustainability in the construction industry of Hong Kong. J. Environ. Manag. 2009, 90, 3616–3628. [Google Scholar] [CrossRef] [PubMed]

- Gadenne, D.L.; Kennedy, J.; McKeiver, C. An Empirical Study of Environmental Awareness and Practices in SMEs. J. Bus. Ethic 2008, 84, 45–63. [Google Scholar] [CrossRef]

- Zhang, Q.; Oo, B.L.; Lim, B.T.H. Linking corporate social responsibility (CSR) practices and organizational performance in the construction industry: A resource collaboration network. Resour. Conserv. Recycl. 2022, 179, 106113. [Google Scholar] [CrossRef]

- Olawumi, T.O.; Chan, D.W. A scientometric review of global research on sustainability and sustainable development. J. Clean. Prod. 2018, 183, 231–250. [Google Scholar] [CrossRef]

- Barkemeyer, R.; Holt, D.; Preuss, L.; Tsang, S. What Happened to the ‘Development’ in Sustainable Development? Business Guidelines Two Decades After Brundtland. Sustain. Dev. 2014, 22, 15–32. [Google Scholar] [CrossRef] [Green Version]

- Elkington, J. Partnerships from cannibals with forks: The triple bottom line of 21st-century. Environ. Qual. Manag. 1998, 8, 37–51. [Google Scholar] [CrossRef]

- Gray, R. Is accounting for sustainability actually accounting for sustainability and how would we know? An exploration of narratives of Organizations and planet. Account. Organ. Soc. 2010, 35, 47–62. [Google Scholar]

- Chang, R.-D.; Soebarto, V.; Zhao, Z.-Y.; Zillante, G. Facilitating the transition to sustainable construction: China’s policies. J. Clean. Prod. 2016, 131, 534–544. [Google Scholar] [CrossRef]

- Montiel, I. Corporate social responsibility and corporate sustainability: Separate pasts, common futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef] [Green Version]

- Schaltegger, S.; Wagner, M. Integrative management of sustainability performance, measurement and reporting. Int. J. Account. Audit. Perform. Eval. 2006, 3, 1–19. [Google Scholar] [CrossRef]

- Orlitzky, M.; Swanson, D.L. Assessing stakeholder satisfaction: Toward a supplemental measure of corporate social performance as reputation. Corp. Reput. Rev. 2012, 15, 119–137. [Google Scholar] [CrossRef]

- Artiach, T.; Lee, D.; Nelson, D.; Walker, J. The determinants of corporate sustainability performance. Account. Financ. 2010, 50, 31–51. [Google Scholar] [CrossRef]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the Dow Jones Sustain-ability Index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- Montiel, I.; Delgado-Ceballos, J. Defining and measuring corporate sustainability: Are we there yet? Organ. Environ. 2014, 27, 113–139. [Google Scholar] [CrossRef]

- Chang, C.-H. The Determinants of Green Product Innovation Performance. Corp. Soc. Responsib. Environ. Manag. 2014, 23, 65–76. [Google Scholar] [CrossRef]

- Oo, B.-L.; Lim, B.T. A review of Singapore contractors’ attitudes to environmental sustainability. Arch. Sci. Rev. 2011, 54, 335–343. [Google Scholar] [CrossRef]

- Ofori, G.; Briffett, C., IV; Gang, G.; Ranasinghe, M. Impact of ISO 14000 on construction enterprises in Singapore. Constr. Manag. Econ. 2000, 18, 935–947. [Google Scholar] [CrossRef]

- Shen, L.; Tam, V.W. Implementation of environmental management in the Hong Kong construction industry. Int. J. Proj. Manag. 2002, 20, 535–543. [Google Scholar] [CrossRef]

- Tan, Y.; Shen, L.; Yao, H. Sustainable construction practice and contractors’ competitiveness: A preliminary study. Habitat Int. 2011, 35, 225–230. [Google Scholar] [CrossRef]

- Khalfan, M.; Noor, M.A.; Maqsood, T.; Alshanbri, N.; Sagoo, A. Perceptions towards sustainable construction amongst construction contractors in state of Victoria, Australia. J. Econ. Bus. Manag. 2015, 3, 940–947. [Google Scholar] [CrossRef] [Green Version]

- Loosemore, M.; Lim, B.T.H.; Ling, F.Y.Y.; Zeng, H.Y. A comparison of corporate social responsibility practices in the Singapore, Australia and New Zealand construction industries. J. Clean. Prod. 2018, 190, 149–159. [Google Scholar] [CrossRef]

- Lichtenstein, S.; Badu, E.; Owusu-Manu, D.G.; Edwards, D.J.; Holt, G.D. Corporate social responsibility architecture and project alignments: A study of the Ghanaian construction industry. J. Eng. Des. Technol. 2013, 11, 334–353. [Google Scholar] [CrossRef]

- Zhang, Q.; Oo, B.L.; Lim, B.T.H. Drivers, motivations, and barriers to the implementation of corporate social responsibility practices by construction enterprises: A review. J. Clean. Prod. 2019, 2010, 563–584. [Google Scholar] [CrossRef]

- Winn, M. Corporate leadership and policies for the natural environment. Res. Corp. Soc. Perform. Policy Suppl. 1995, 1, 127–161. [Google Scholar]

- Lawrence, A.T.; Morell, D. Leading-edge environmental management: Motivation, opportunity, resources, and processes. Res. Corp. Soc. Perform. Policy 1995, 1, 99–127. [Google Scholar]

- Senge, P.M. The fifth discipline, the art and practice of the learning organization. Perform. Instr. 1991, 30, 37. [Google Scholar] [CrossRef]

- Hartmann, A. The context of innovation management in construction firms. Constr. Manag. Econ. 2006, 24, 567–578. [Google Scholar] [CrossRef]

- Naffziger, D.W.; Ahmed, N.U.; Montagno, R.V. Perceptions of environmental consciousness in US small businesses: An empirical study. SAM Adv. Manag. J. 2003, 68, 23–34. [Google Scholar]

- Krause, D.R.; Ragatz, G.L.; Hughley, S. Supplier Development from the Minority Supplier’s Perspective. J. Supply Chain Manag. 1999, 35, 33–41. [Google Scholar] [CrossRef]

- Dao, V.; Langella, I.; Carbo, J. From green to sustainability: Information Technology and an integrated sustainability frame-work. J. Strateg. Inf. Syst. 2011, 20, 63–79. [Google Scholar] [CrossRef]

- Khuntia, J.; Saldanha, T.J.; Mithas, S.; Sambamurthy, V. Information technology and sustainability: Evidence from an emerging economy. Prod. Oper. Manag. 2018, 27, 756–773. [Google Scholar] [CrossRef]

- Hansson, S.O. Technology and the notion of sustainability. Technol. Soc. 2010, 32, 274–279. [Google Scholar] [CrossRef]

- Oyewobi, L.O.; Windapo, A.O.; James, R.O. An empirical analysis of construction organisations’ competitive strategies and performance. Built Environ. Proj. Asset Manag. 2015, 5, 417–431. [Google Scholar] [CrossRef] [Green Version]

- Barney, J.B. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef] [Green Version]

- McWilliams, A.; Van Fleet, D.D.; Cory, K.D. Raising Rivals’ Costs Through Political Strategy: An Extension of Resource-based Theory. J. Manag. Stud. 2002, 39, 707–724. [Google Scholar] [CrossRef]

- Shang, K.C.; Lu, C.S.; Li, S. A taxonomy of green supply chain management capability among electronics-related manufacturing firms in Taiwan. J. Environ. Manag. 2010, 91, 1218–1226. [Google Scholar] [CrossRef]

- Foo, P.Y.; Lee, V.H.; Ooi, K.B.; Tan, G.W.H.; Sohal, A. Unfolding the impact of leadership and management on sustainability performance: Green and lean practices and guanxi as the dual mediators. Bus. Strat. Environ. 2021, 30, 4136–4153. [Google Scholar] [CrossRef]

- Hellriegel, D.; Slocum, J.W. Organizational Behavior (Wydanie 13); Cengage South-Western: Belmont, CA, USA, 2011. [Google Scholar]

- Akintoye, A.; McIntosh, G.; Fitzgerald, E. A survey of supply chain collaboration and management in the UK construction industry. Eur. J. Purch. Supply Manag. 2000, 6, 159–168. [Google Scholar] [CrossRef]

- Green, K.W., Jr.; Zelbst, P.J.; Meacham, J.; Bhadauria, V.S. Green supply chain management practices: Impact on performance. Supply Chain. Manag. Int. J. 2012, 17, 290–305. [Google Scholar] [CrossRef]

- Thoo, A.C.; Hamid, A.; Bakar, A.; Rasli, A.; Zhang, D.W. The Moderating Effect of Enviropreneurship on Green Supply Chain Management Practices and Sustainability Performance. Adv. Mater. Res. 2014, 869–870, 773–776. [Google Scholar] [CrossRef]

- Adetunji, I.; Price, A.D.F.; Fleming, P. Achieving sustainability in the construction supply chain. In Proceedings of the Institution of Civil Engineers-Engineering Sustainability; Thomas Telford Ltd.: London, UK, 2008; Volume 161, pp. 161–172. [Google Scholar]

- Balasubramanian, S.; Shukla, V. Green supply chain management: An empirical investigation on the construction sector. Supply Chain Manag. Int. J. 2017, 22, 58–81. [Google Scholar] [CrossRef] [Green Version]

- Goulding, J.S.; Alshawi, M. Generic and specific IT training: A process protocol model for construction. Constr. Manag. Econ. 2002, 20, 493–505. [Google Scholar] [CrossRef]

- Thrope, D.; Ryan, N.; Charles, M.B. Environmental sustainability-a driver for innovation in construction SMES? In Proceedings of the 3rd International Conference Cooperative Research Centre (CRC) for Construction Innovation, Surfers Paradise, Australia, 12–14 March 2008. [Google Scholar]

- Stadel, A.; Eboli, J.; Ryberg, A.; Mitchell, J.; Spatari, S. Intelligent Sustainable Design: Integration of Carbon Accounting and Building Information Modeling. J. Prof. Issues Eng. Educ. Pract. 2011, 137, 51–54. [Google Scholar] [CrossRef]

- Pfeffer, J. Building sustainable organizations: The human factor. Acad. Manag. Perspect. 2010, 24, 34–45. [Google Scholar]

- Chen, Y.-S. The Positive Effect of Green Intellectual Capital on Competitive Advantages of Firms. J. Bus. Ethic. 2007, 77, 271–286. [Google Scholar] [CrossRef]

- Yong, J.Y.; Yusliza, M.-Y.; Ramayah, T.; Fawehinmi, O. Nexus between green intellectual capital and green human resource management. J. Clean. Prod. 2019, 215, 364–374. [Google Scholar] [CrossRef]

- Singh, A. Achieving Sustainability Through Internal Communication and Soft Skills. IUP J. Soft Ski. 2013, 7, 21. [Google Scholar]

- Hamadamin, H.H.; Atan, T. The impact of strategic human resource management practices on competitive advantage sus-tainability: The mediation of human capital development and employee commitment. Sustainability 2019, 11, 5782. [Google Scholar] [CrossRef] [Green Version]

- Barney, J.B. Gaining and Sustaining Competitive Advantage; Pearson: New York, NY, USA, 1997. [Google Scholar]

- Epstein, M.J.; Roy, M.-J. Sustainability in Action: Identifying and Measuring the Key Performance Drivers. Long Range Plan. 2001, 34, 585–604. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The Sustainability Balanced Scorecard-linking sustainability management to business strategy. Bus. Strat. Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E.G. Business cases for sustainability: The role of business model innovation for corporate sustainability. Int. J. Innov. Sustain. Dev. 2012, 6, 95–119. [Google Scholar] [CrossRef]

- Bansal, P.; DesJardine, M.R. Business sustainability: It is about time. Strat. Organ. 2014, 12, 70–78. [Google Scholar] [CrossRef]

- Creswell, J.W.; Plano Clark, V.L.; Gutmann, M.L.; Hanson, W.E. Advanced mixed methods research designs. In Handbook of Mixed Methods in Social and Behavioral Research; Sage Publications: Los Angeles, CA, USA, 2003; Volume 209, p. 240. [Google Scholar]

- Lim, T.B.H.; Linf, Y.Y.F.; Raphael, B.; Ibbs, W.; Ofori, G. An empirical analysis of the determinants of organizational flexibility in construction business. J. Constr. Eng. Manag. 2011, 137, 225–237. [Google Scholar] [CrossRef]

- Mojtahedi, M.; Oo, B.L. The impact of stakeholder attributes on performance of disaster recovery projects: The case of transport infrastructure. Int. J. Proj. Manag. 2017, 35, 841–852. [Google Scholar] [CrossRef]

- Loosemore, M.; Lim, B.T.H. Linking corporate social responsibility and organizational performance in the construction industry. Constr. Manag. Econ. 2017, 35, 90–105. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: Thousand Oaks, CA, USA, 2016. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sinkovics, R.R. The Use of Partial Least Squares Path Modeling in International Marketing. In New Challenges to International Marketing; Emerald Group Publishing Limited: Bingley, UK, 2009; pp. 277–319. [Google Scholar]

- Fornell, C.; Johnson, M.D.; Anderson, E.W.; Cha, J.; Bryant, B.E. The American customer satisfaction index: Nature, purpose, and findings. J. Mark. 1996, 60, 7–18. [Google Scholar] [CrossRef] [Green Version]

- Oke, A.; Walumbwa, F.O.; Myers, A. Innovation strategy, human resource policy, and firms’ revenue growth: The roles of environmental uncertainty and innovation performance. Decis. Sci. 2012, 43, 273–302. [Google Scholar] [CrossRef]

- Aibinu, A.A.; Al-Lawati, A.M. Using PLS-SEM technique to model construction organizations’ willingness to participate in e-bidding. Autom. Constr. 2010, 19, 714–724. [Google Scholar] [CrossRef]

- Fornell, C.; Bookstein, F.L. Two structural equation models: LISREL and PLS applied to consumer exit-voice theory. J. Mark. Res. 1982, 19, 440–452. [Google Scholar] [CrossRef] [Green Version]

- Fornell, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

{kind=link}

| Description | Frequency | Percentage |

|---|---|---|

| Characteristics of companies | ||

| Type of organization | ||

| Publicly owned | 9 | 21.4% |

| Privately owned | 33 | 78.6% |

| Scope of construction business | ||

| Residential construction | 8 | 19% |

| Residential and Commercial | 14 | 33.3% |

| Commercial | 10 | 23.8% |

| Residential/Commercial/Infrastructure | 3 | 7.1% |

| Commercial/Infrastructure | 7 | 7.1% |

| Age | ||

| <20 years | 9 | 21.4% |

| 21–50 years | 18 | 42.9% |

| >50 years | 15 | 35.7% |

| Size of workforce | ||

| Small (0–20) | 0 | 0 |

| Medium (20–200) | 30 | 71.42% |

| Large (>200) | 12 | 28.58% |

| Characteristics of respondents | ||

| Designation | ||

| Director (i.e., managing director, executive director) | 8 | 19% |

| General Manager | 2 | 4.8% |

| Senior Manager (senior project manager, development manager, sustainability manager) | 31 | 73.8% |

| Construct | Measurement Items | Description | Factor Loading | Cronbach’s Alpha | Composite Reliability (CR) | Average Variance Extracted (AVE) |

|---|---|---|---|---|---|---|

| Organizational culture (OC) | OC1 | The leadership always inform employees on organization’s business objectives | 0.742 | 0.931 | 0.934 | 0.667 |

| OC2 | There is an atmosphere of trust and respect amongst top management and employees | 0.756 | ||||

| OC3 | My organization encourages employee participation in decision making | 0.78 | ||||

| OC4 | My organization provides support to employees to achieve individual and organisational goals | 0.856 | ||||

| OC5 | Employee’s training is seen as an investment | 0.884 | ||||

| OC6 | My organization promotes open conversation between supervisors and subordinates | 0.782 | ||||

| OC7 | Sustainability is top priority of organizations’ leadership | 0.873 | ||||

| OC8 | My organization encourages cultural changes to incorporate sustainability in all organisational levels | 0.89 | ||||

| Supply chain capabilities (SC) | SC1 | Always focuses on green purchasing (recycle, reuse and reduction in material | 0.929 | 0.683 | 0.858 | 0.752 |

| SC2 | Audits the suppliers to evaluate their social and environmental performance | 0.932 | ||||

| SC3 | Works with suppliers to help them reduce environmental impacts through change in product design and material use | 0.949 | ||||

| SC4 | Provides training to the procurement officer about performance evaluation and monitoring of suppliers | 0.926 | ||||

| Technological capabilities (TC) | TC1 | Uses new innovative methods to reduce material use | 0.862 | 0.831 | 0.965 | 0.873 |

| TC2 | Uses latest technology for employee’s safety (for example using RFID/GPS for tracking employees on complex sites | 0.776 | ||||

| TC3 | Has efficient system to communicate and share real time information with employees | 0.718 | ||||

| TC4 | Has capacity to monitor its sustainability performance | 0.894 | ||||

| Business strategies (BS) | BS1 | Forms partnership with clients to improve sustainability performance | 0.902 | 0.926 | 0.944 | 0.771 |

| BS2 | Forms partnership with sub-contractors to improve sustainability performance | 0.893 | ||||

| BS3 | Creates business case for sustainability through reuse and recycling of material | 0.893 | ||||

| BS4 | Formally measure and report sustainability | 0.856 | ||||

| BS5 | Encourages clients to pay a little extra to achieve long term sustainability | 0.844 | ||||

| Employee Skills and Attitudes (ESA) | ESA1 | Positive attitude on sustainability | 0.901 | 0.886 | 0.922 | 0.747 |

| ESA2 | Employees’ knowledge and skills in using IT | 0.927 | ||||

| ESA3 | Employees’ knowledge and skills in material and equipment handling | 0.877 | ||||

| ESA4 | Training to upgrade employees’ knowledge on new health and safety regulations | 0.741 | ||||

| Environmental Sustainability Performance (ESP) | ESP1 | Assesses and manages the environmental impacts of its activities | 0.9 | 0.903 | 0.944 | 0.705 |

| ESP2 | Uses renewable energy | 0.8 | ||||

| ESP3 | Considers land use and biodiversity in business decision | 0.866 | ||||

| ESP4 | Makes an effort to minimize air, water, and other forms of pollutions | 0.793 | ||||

| ESP5 | Seeks to improve energy efficiency in product and services | 0.831 | ||||

| ESP9 | Tries to reuse and recycle materials | 0.799 | ||||

| ESP10 | Makes initiatives to reduce direct and indirect greenhouse gas emissions | 0.859 | ||||

| Social Sustainability Performance (SSP) | SSP5 | Works with community organisations to organize social and fundraising events | 0.876 | 0.906 | 0.931 | 0.732 |

| SSP6 | Sponsors sports events and other community causes | 0.902 | ||||

| SSP7 | Donates cash to support community in difficult situations | 0.935 | ||||

| SSP8 | Encourages employees to do volunteer work during working hours | 0.78 | ||||

| SSP10 | Works on projects to involve local communities | 0.77 | ||||

| Economic sustainability Performance (ECSP) | ECSP1 | Has increased the market share | 0.851 | 0.667 | 0.841 | 0.604 |

| ECSP2 | Has increased the profit margin | 0.72 | ||||

| ECSP4 | Has increased returns to shareholders | 0.88 |

| Hypothesis | Relationship | Path Coefficient | R2 | f2 | Inference |

|---|---|---|---|---|---|

| Environmental sustainability performance | |||||

| H1a | OC-ESP | 0.205 * | 0.833 ** | 0.058 * | S |

| H2a | SC-ESP | 0.304 | 0.059 | NS | |

| H3a | TC-ESP | 0.141 * | 0.252 | S | |

| H4a | ESA-ESP | −0.194 | 0.031 | NS | |

| H5a | BS-ESP | 0.486 * | 0.14 | S | |

| Social sustainability performance | |||||

| H1b | OC-SSP | 0.589 * | 0.682 ** | 0.206 | S |

| H2b | SC-SSP | 0.255 | 0.033 | NS | |

| H3b | TC-SSP | −0.245 | 0.024 | NS | |

| H4b | ESA-SSP | −0.22 | 0.016 | NS | |

| H5b | BS-SSP | 0.504 * | 0.16 | S | |

| Economic sustainability performance | |||||

| H1c | OC-ECSP | 0.15 | 0.461 * | 0.021 | NS |

| H2c | SC-ECSP | 0.304 | 0.016 | NS | |

| H3c | TC-ECSP | 0.141 | 0.003 | NS | |

| H4c | ESA-ECSP | −0.384 | 0.064 | NS | |

| H5c | BS-ECSP | 0.317 | 0.13 | NS | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Afzal, F.; Lim, B. Organizational Factors Influencing the Sustainability Performance of Construction Organizations. Sustainability 2022, 14, 10449. https://doi.org/10.3390/su141610449

Afzal F, Lim B. Organizational Factors Influencing the Sustainability Performance of Construction Organizations. Sustainability. 2022; 14(16):10449. https://doi.org/10.3390/su141610449

Chicago/Turabian StyleAfzal, Fatima, and Benson Lim. 2022. "Organizational Factors Influencing the Sustainability Performance of Construction Organizations" Sustainability 14, no. 16: 10449. https://doi.org/10.3390/su141610449

APA StyleAfzal, F., & Lim, B. (2022). Organizational Factors Influencing the Sustainability Performance of Construction Organizations. Sustainability, 14(16), 10449. https://doi.org/10.3390/su141610449