4.1. Stationary and Cointegration Analyses

Although the ARDL technique allows testing the presence of long-run connections between variables with different orders of integration, it cannot be used in the presence of variables integrated of order 2 or above. Furthermore, because the conventional and dynamic ARDL simulation models require I (1) variables, it is essential to confirm that the dependent variable is stationary at the first difference. We start by performing the ADF unit root test with bootstrapped critical values. As pointed out by Dorta and Sanchez [

38], the Bootstrap ADF unit root test is more precise than the conventional ADF unit root test. The results are summarized in

Table 1.

When considering variables in levels, the ADF unit root test with 10,000 bootstrap replicates shows that test statistics are higher than the bootstrap critical values. The null hypothesis of unit root cannot be consequently rejected. However, when differentiating variables, the table suggests that all variables become stationary. Moreover, all variables, except the gross domestic product and CO

2 emissions, are stationary at a 1% level. While the ADF unit root test may offer an idea about the stationarity of variables, it may have size distortions and low power in the presence of structural breaks in the data-generating process. To address this issue, we performed the unit root test with two structural breaks developed by Lumsdaine and Papell [

33]. The findings are summarized in

Table 2.

Findings of the Lumsdaine–Papell unit root test with an intercept show that all variables, except carbon dioxide emissions, have a unit root at levels. When the model includes a time trend and an intercept, the table shows that t-statistics associated with levels of almost all variables are lower than the critical values reported at the bottom of

Table 2. Foreign direct investments are the only variable that seems stationary at levels. When taking the first difference, the two variants of the Lumsdaine–Papell unit root test suggest rejecting the null hypothesis of a unit root. Most notably, the two unit root tests confirm the mandatory condition of a strict first-difference stationary dependent variable, i.e., renewable energy consumption. Furthermore, the stationarity analysis suggests that none of the variables considered in the analysis are integrated of order 2 or above, a mandatory condition for implementing the conventional ARDL and dynamic ARDL simulation models.

The next step was to investigate whether there is a cointegrating relationship between renewable energy and the set of explanatory variables, including fossil fuel prices. To this end, we started by implementing the conventional ARDL approach proposed by Pesaran et al. [

16]. The study used the approximate

p-values and critical values suggested by Kripfganz and Schneider [

34] based on response surface regressions. The results are presented in

Table 3.

The computed F-statistics indicate that the null hypothesis of no cointegration should be rejected at the 1% level for the three considered models as its values are higher than the upper bound critical values derived from Kripfganz and Schneider [

34]. Moreover, the null hypothesis is rejected at the 10% level for model 2 and at the 5% level for models 1 and 3 when considering t-statistics. These findings strongly support the long-run linkages between fossil fuel prices and renewable energy use. Our results corroborate some previous studies. For instance, Damette and Marques [

22] focused on 24 European countries using a set of cointegration techniques, including Westerlund and Edgerton [

39], Westerlund [

40], and Pedroni [

41,

42], and revealed the presence of a significant relationship between oil prices and renewable energy in the long run. Furthermore, Murshed and Tanha [

5] concluded that oil prices have a long-run connection with renewable energy in four South Asian oil-importing economies.

4.3. Dynamic ARDL Simulations

We next used the dynamic ARDL simulations approach developed by Philips [

13] and Philips and Jordan [

14] to assess the impacts of fossil fuel prices on renewable energy use. The estimation results associated with the three models are reported in

Table 5.

The error-correction term, which captures the speed with which short-run disequilibrium is adjusted towards long-run equilibrium, is negative and statistically significant at 1% for the three considered models. The negative and significant error-correction terms support our prior findings, indicating the presence of long-run cointegrating linkages between fossil fuel prices and renewable energy in China. Moreover, the dynamic ARDL simulation approach suggests that renewable energy use is affected by gross domestic product for the three considered models in the long run. Thus, the rising economic activity experienced in China over the latest decades has been associated with more clean energy sources. These findings may be explained by the conservation hypothesis, according to which economic growth leads to increased energy use, including renewable energy sources. These results corroborate previous research, suggesting that gross domestic product is a crucial driver of renewable energy in developed and developing countries [

2,

43,

44]. Moreover, focusing on the Chinese economy, Zhao et al. [

45] concluded that gross domestic product positively affects the demand for renewable and non-renewable energy sources. The results show that economic activity has a higher impact on renewable energy demand than on non-renewable energy demand. The table also suggests that the impact of foreign capital on renewable energy consumption is negative and statistically significant in the long run. These findings suggest that FDI flows have been related to a reduction in renewable energy consumption over the previous decades, which might be attributed to foreign investors in China relying more on non-renewable energy sources. Zhao et al. [

45] indicate that non-renewable energy sources, among other things, are attracting foreign investors to China, owing to the low price of coal and energy subsidies provided by local governments. According to the same study, firms engaged in international trade (most foreign) exert a favorable impact on non-renewable energy use while hurting renewable energy. Furthermore, Jun et al. [

46] and Cheng et al. [

47] claim that foreign direct investments have increased environmental deterioration in China, which might be attributed to the heavy usage of non-renewable fossil fuel energy sources in their activities.

Regarding the impact of CO

2 emissions on renewable energy use, the dynamic ARDL simulation estimates suggest the insignificance of the corresponding coefficients for the three considered models. These findings imply that environmental degradation has not driven a shift to clean energy sources in China, despite the worsening of most environmental and ecological indicators in recent decades. Indeed, China is the biggest warming greenhouse gas emitter globally, with about 28% of global CO

2 emissions in 2019 [

1]. Moreover, China is also emitting increased levels of other greenhouse gases, such as methane and sulfur dioxide. Our findings imply that the recent increase in greenhouse gas emissions and the degradation of almost all environmental indicators in China have not led to a shift to clean energy sources. In a recent study, Lu et al. [

48] revealed that nearly 70% of Chinese municipal cities did not fulfil the National Ambient Air Quality Standard requirements. The impact of patents on environmental technologies on renewable energy use is positive and statistically significant at the 1% level in all models, meaning that a rise in the number of patents on environmental technologies boosts renewable energy consumption in China. Indeed, developing new and modern renewable energy technologies enables more effective and relatively low-cost technologies to be implemented. This situation drives firms to switch from non-renewable to renewable energy sources. In a study by Wang et al. [

49], the authors conclude that patents on clean energy technologies contribute to lowering environmental degradation, which is implicitly attributable to the rise in clean energy use. Finally,

Table 5 suggests that all control variables have no significant short-run effects on renewable energy demand. These findings imply that the significant effects previously identified (gross domestic product, foreign direct investments, patent on environmental technologies) are reached only in the long run.

As we move on to the impact of fossil fuel prices on renewable energy, we see in

Table 5 that the oil price coefficient is positive and statistically significant at the 10% level. Moreover, if oil prices rise by 1%, renewable energy use will rise by 0.068%. Consequently, a transition from non-renewable to renewable energy sources has occurred. In such a case, renewable energy sources, such as wind, solar, and bioenergy, are considered substitutes for oil in the long run. These findings could be explained by the fact that China has surpassed the U.S. as the world’s largest oil importer, accounting for one-sixth of global oil imports in 2019. Indeed, oil imports increased from 1.893 million barrels per day in 2000 to 11.825 million barrels per day in 2019 [

1]. Any change in international oil prices affects industries that rely heavily on it. The rise in oil prices also affects electricity prices as a considerable share of crude oil is used to generate electricity. In such a case, a continuous rise in oil prices stimulates the use of renewable energy sources. Our findings are consistent with Apergis and Payne [

9], who investigated the effect of oil prices on energy utilization in a sample of Central American developing countries between 1980 and 2010. The fully modified ordinary least squares reveal that a 1% increase in oil prices leads to a 0.285% increase in long-run renewable energy use. Murshed and Tanha [

5] also concluded that oil prices positively affect renewable energy in four net oil-importing South Asian countries after reaching a given threshold level. Contrary to long-run effects, the coefficient associated with oil prices is not significant in the short run. These findings imply that oil price fluctuations have no substantial impact on renewable energy consumption in the short run. This could be related to the fact that the transition to renewable energy sources is a long-run process rather than an immediate response to increased oil prices.

The long-run impact of coal price on renewable energy is higher than that associated with the oil price. Indeed, a 1% increase in coal prices induces a 0.135% increase in renewable energy consumption in the long run. These findings align with Apergis and Payne [

9], who found that the demand for renewable energy increases when coal prices rise. Indeed, renewable energy sources are considered substitutes for coal, and any change in its price in the long run affects the demand for renewable energy. These findings are interesting since they reveal that, despite the abundance of coal in China, the persistence of coal price hikes drives more enterprises to migrate to renewable energy sources. Indeed, China has a proven coal reserve of about 141,595 million tons in 2019, representing 13.2% of the global proven coal reserves. Moreover, China produced about 47.6% of global coal in 2019, and at the same time, it imports about 6.4 exajoules of coal, mainly from Australia and Indonesia. Coal is the primary energy source in China, accounting for about 61.23% of total energy consumption and 64.07% of electric power production in 2018. These facts confirm the abundance of coal in China and its importance to the economy. Consequently, any long-term change in the price of coal motivates firms to move toward renewable energy sources. Finally, our results suggest that the coefficient associated with the natural gas price is statistically significant only in the long run. The analysis, however, shows that natural gas prices have no substantial influence on renewable energy use in the short run, which is compatible with our earlier findings on the short-run insensitivity of renewable energy consumption to oil and coal prices. As in the case of oil, the Chinese economy imports natural gas from abroad and is a net natural gas importer. In 2019, China produced about 177.6 billion cubic meters of natural gas, while the economy needs are about 307.3 billion cubic meters. During the same year. Chinese natural gas imports were about 84.8 billion cubic meters of liquefied natural gas, mainly from Australia (39.8), Qatar (11.24), and Malaysia (10), and 47.7 billion cubic meters of natural gas pipelines, mainly from its neighbors, Turkmenistan (31.6), Kazakhstan (6.5), and Uzbekistan (4.9). The situation makes it so that natural gas prices affect the production cost in firms that rely heavily on natural gas in their production process and electricity price. All those factors mean that the rise of natural gas prices induces a switch toward renewable energy sources in the long run.

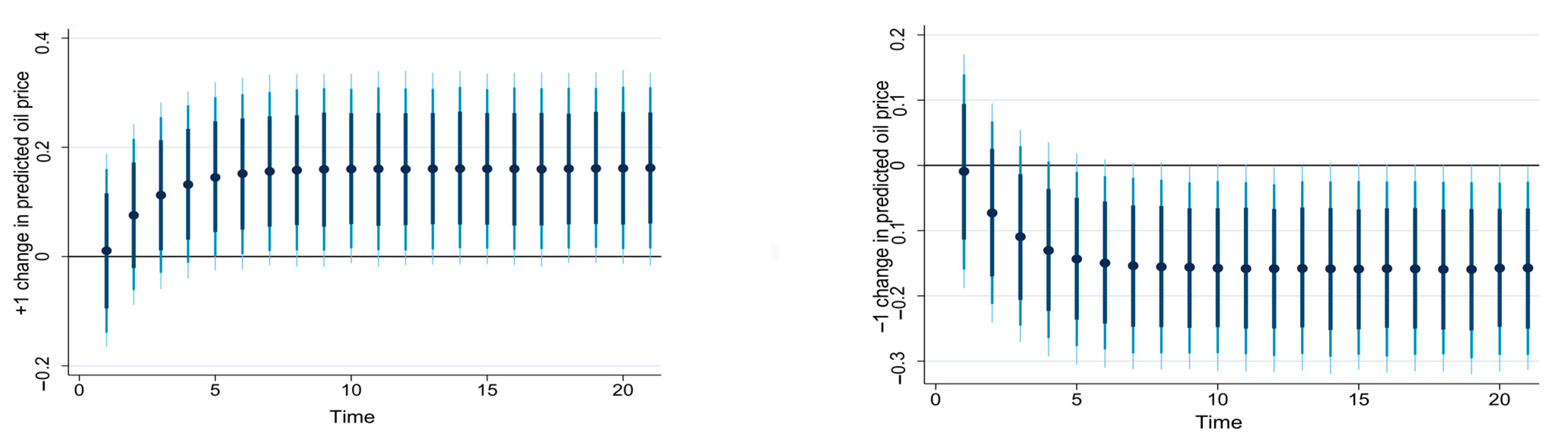

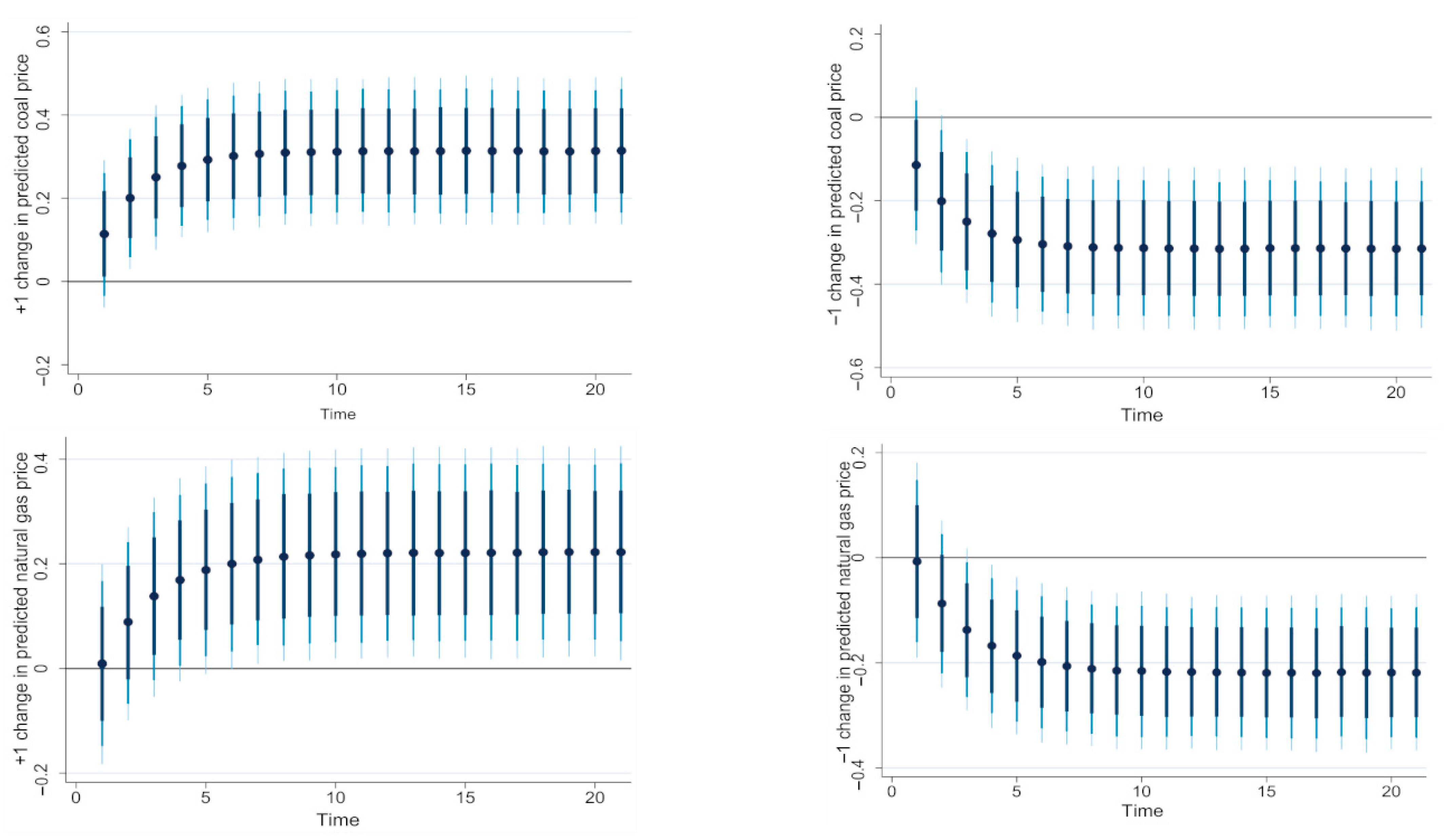

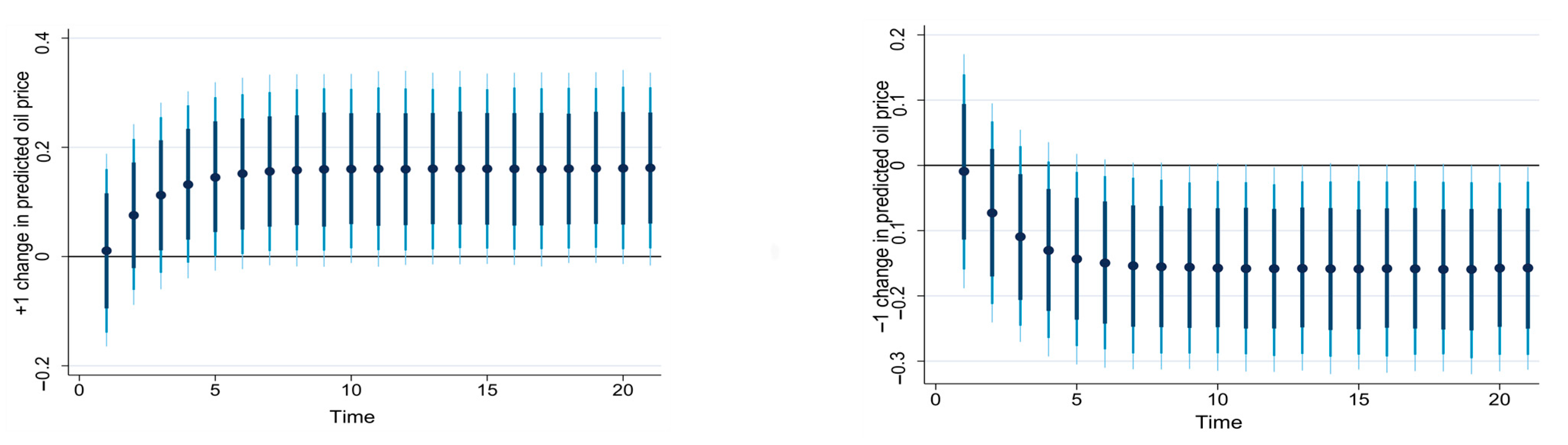

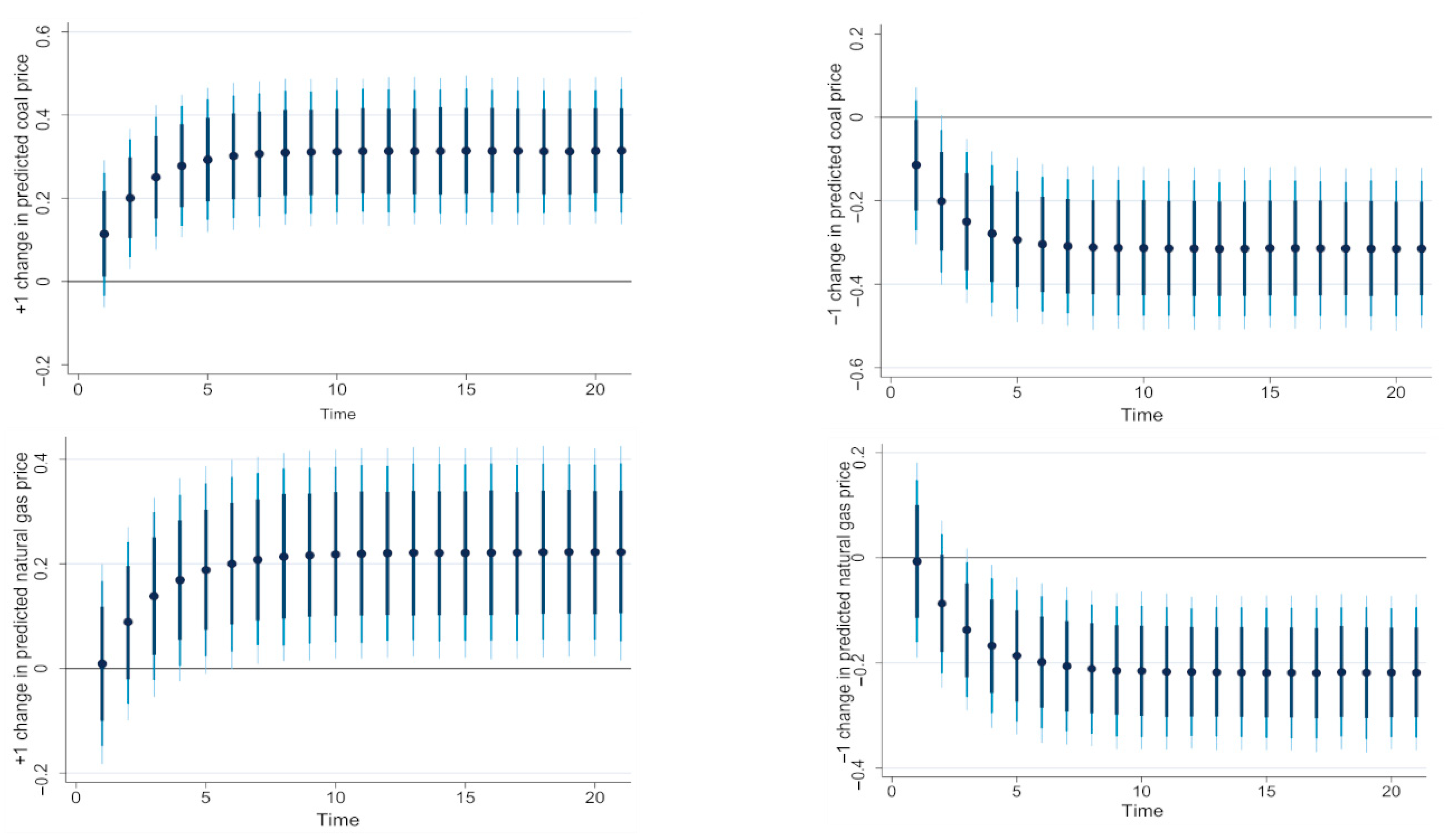

To better understand how renewable energy consumption responds to changes in fossil fuel prices, we used a new feature of the dynamic ARDL simulation model to predict, simulate, and plot the impact of a counterfactual change in the explanatory variable (fossil fuel prices) on the dependent variable (renewable energy consumption) while keeping other explanatory variables unchanged. In other words, the graphs allow plotting the impulse response of renewable energy consumption to fossil fuel prices in the short and long run.

Figure 1 separately plots the response of renewable energy consumption to a ±1% change in predicted oil price, coal price, and natural gas price.

As shown, a 1% increase in oil prices has a long-run positive effect on renewable energy consumption. The short-run impact of oil increase is weak and not statistically significant. Starting from about t = 5, the impact of oil price increases is stabilized. Likewise, a 1% decline in oil prices negatively affects renewable energy only in the long run. Nevertheless, the same plot reveals the absence of significant short-run effects of oil price changes (increase and decrease).

Figure 1 also shows that a 1% increase in coal price affects renewable energy use in the short- and long-run. However, the short-run effect is weak and increases to reach its maximum in the long run. The decline in coal price by 1% reduces the demand for renewable energy in the short and long run. Finally, the impact of natural gas price increases (decreases) is positive (negative) and results in a rise (decline) in renewable energy consumption in the long run. Another important remark that might emerge from

Figure 1 is that the long-run impact of coal price upturns (decreases) is higher than that of oil prices and natural gas prices.

4.4. Dynamic ARDL Simulations with Structural Breaks

In this section, we check the validity of our prior findings when structural breaks are considered. To this end, a two-stage procedure was followed. First, we identified the dates of breakpoints in fossil fuel prices using the Bai–Perron multiple breakpoint test. Then, we re-used the dynamic ARDL simulations approach by introducing time dummies corresponding to breakpoints obtained from the Bai–Perron test. The results of the Bai–Perron multiple breakpoint test are reported in

Table 6. The maximum number of breakpoints was limited to five. The number and dates of significant breakpoints were endogenously determined based on the sequential testing of

l + 1 vs.

l breaks proposed by Bai and Perron [

17,

18]. The null hypothesis of

l breakpoint was tested against the alternative of

l + 1 breakpoint at year

t.

As shown, the findings of the sequential test suggest rejecting the null of 0, 1, and 2 breakpoints in favor of the alternative of 1, 2, and 3 breakpoints for oil and natural gas prices, and rejecting the null of 0 and 1 breakpoints in favor of the alternative of 1 and 2 breakpoints for coal price. Therefore, the table suggests the presence of three significant breakpoints for oil price (2005, 1986, and 1999), two significant breakpoints for coal price (2007 and 1986), and three significant breakpoints for the natural gas price (2000, 1987, and 2014). The breakpoints mentioned above are significant at the 1% level for oil, coal, and natural gas prices.

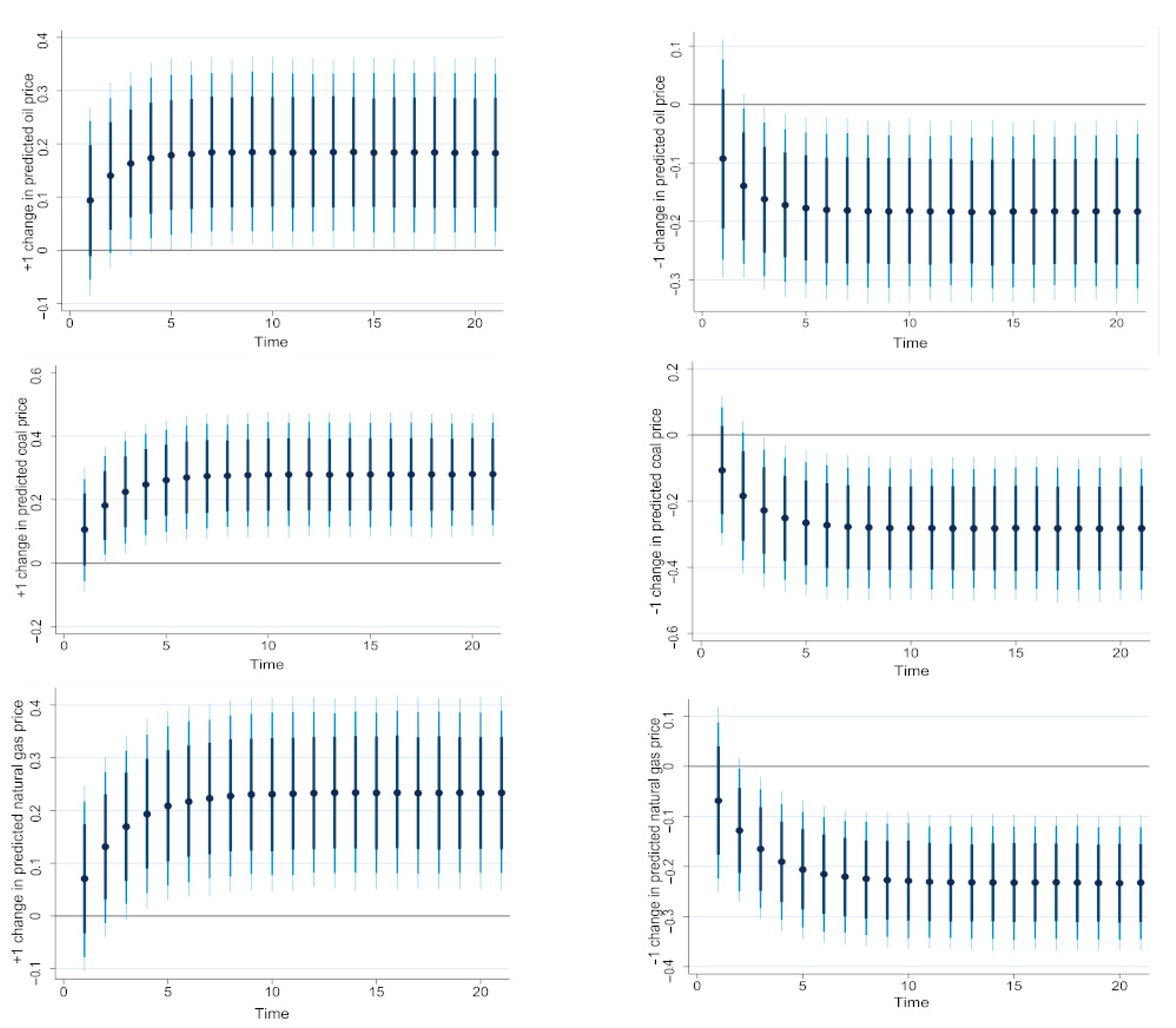

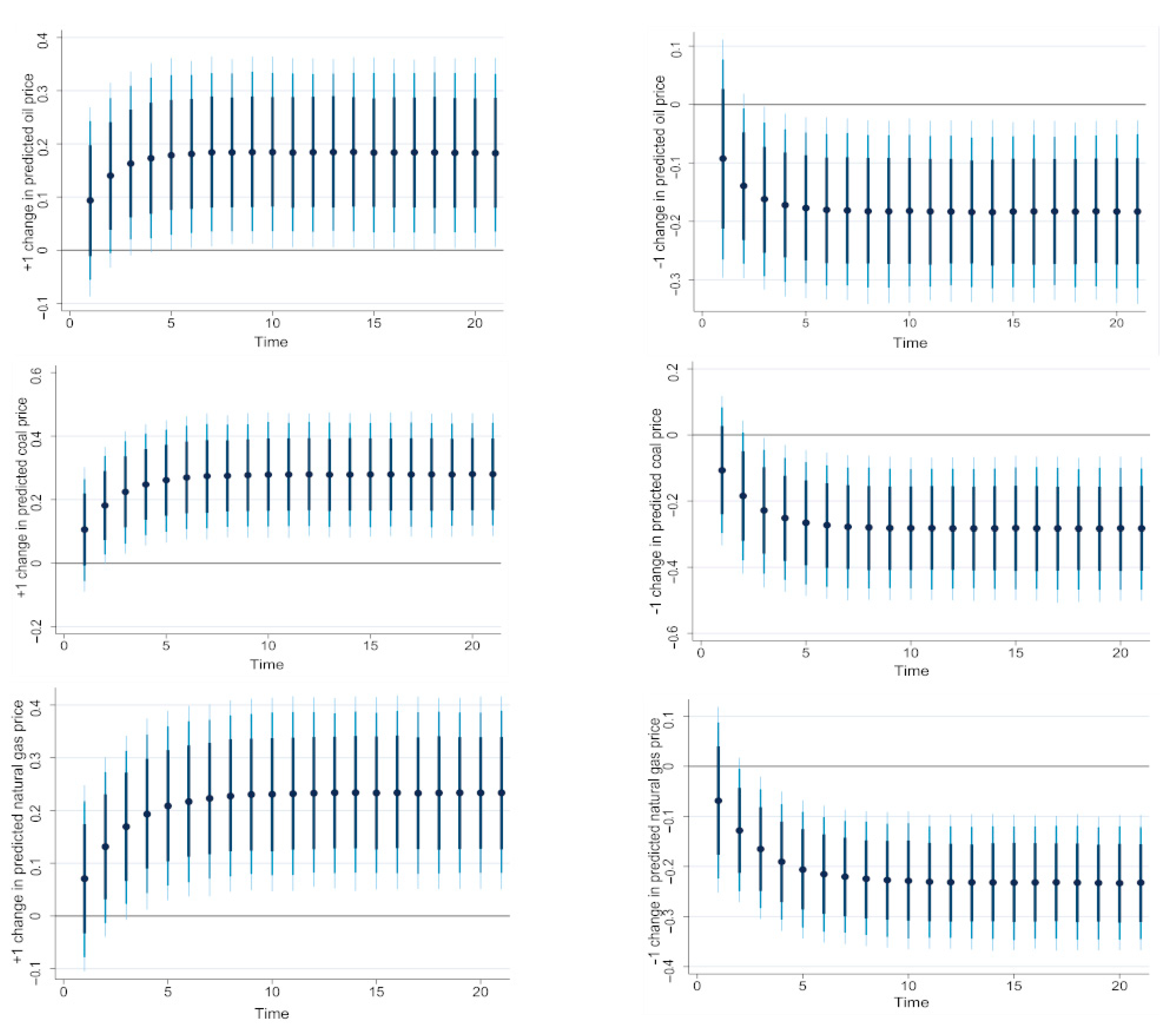

We then introduced the endogenously determined breakpoint dates in models 1–3 and re-estimated them using the dynamic ARDL simulations. The results are reported in

Table 7. The table suggests the validity of previous results. Indeed, the long-run impact of oil prices on renewable energy use is positive and statistically significant at the 5% level, whereas no significant impact was identified in the short run. The findings also indicate that natural gas price positively and significantly affects renewable energy consumption in the long run with a coefficient of 0.085. Finally, the coefficient associated with coal price is also positive and weakly significant in the long run. However, the impacts of natural gas and coal prices are not statistically significant in the short run. Furthermore, the analysis suggests that following the introduction of time dummies, the long-run effects of oil prices and natural gas prices on renewable energy have been amplified and became more significant, while the magnitude and significance of the impact of coal prices fell. Finally, the error-correction terms associated with all models are significant at 1% and negative, confirming the long-run relationships between fossil fuel prices and renewable energy consumption. As in

Table 6, patents on environmental technologies and gross domestic products positively affect renewable energy in the long run, while foreign direct investments are negatively associated with renewable energy.

Overall, considering structural breaks did not affect the main results of the dynamic ARDL simulation procedure, which indicates that rising fossil fuel prices boost renewable energy consumption in the long run. To better detect the effects of fossil fuel prices on renewable energy consumption through the augmented dynamic ARDL simulation procedure, we plotted the prediction of changes of an explanatory variable and its outcome on the dependent variable, all else being equal.

Figure 2 plots the response of renewable energy use to a 1% increase and decrease in oil, coal, and natural gas prices. The figure confirms the findings previously reached. Indeed, a 1% increase (decreases) in oil, coal, and natural gas prices positively (negatively) affects renewable energy only in the long run. These effects are not found to be significant in the short run.

,

,

{kind=link}

{kind=link}

{kind=link}