Does ISO 14001 and Green Servitization Provide a Push Factor for Sustainable Performance? A Study of Manufacturing Firms

Abstract

:1. Introduction

2. Review of Literature

2.1. Variables Operationalization

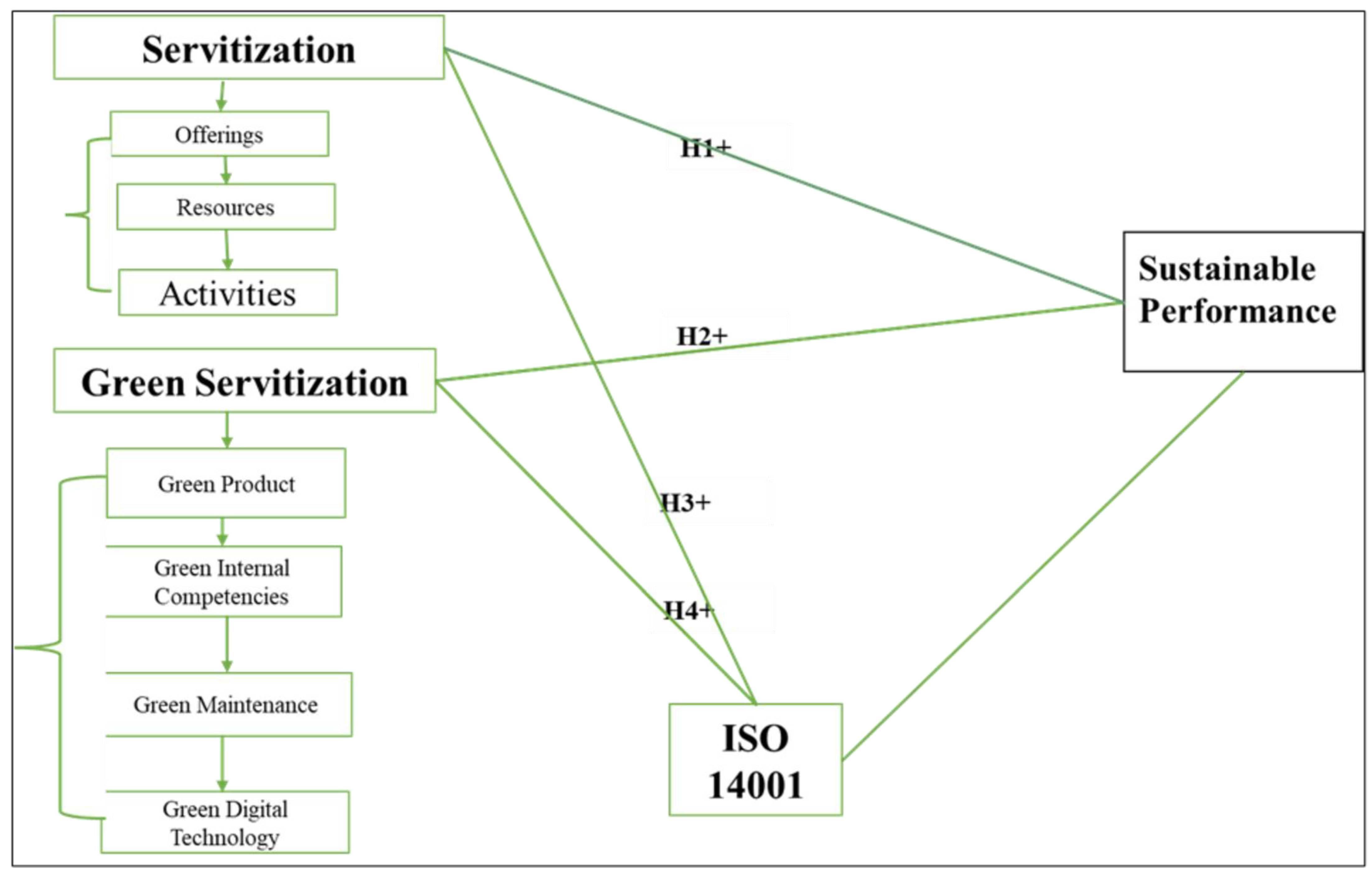

2.1.1. Servitization

Offerings

Resources

Activities

2.1.2. Green Servitization

Green Products

Green Internal Competencies

Green Maintenance

Green Digital Technology

2.1.3. ISO 14001

Operation

Performance Evaluation

2.1.4. Sustainable Performance

2.1.5. Hypotheses Development

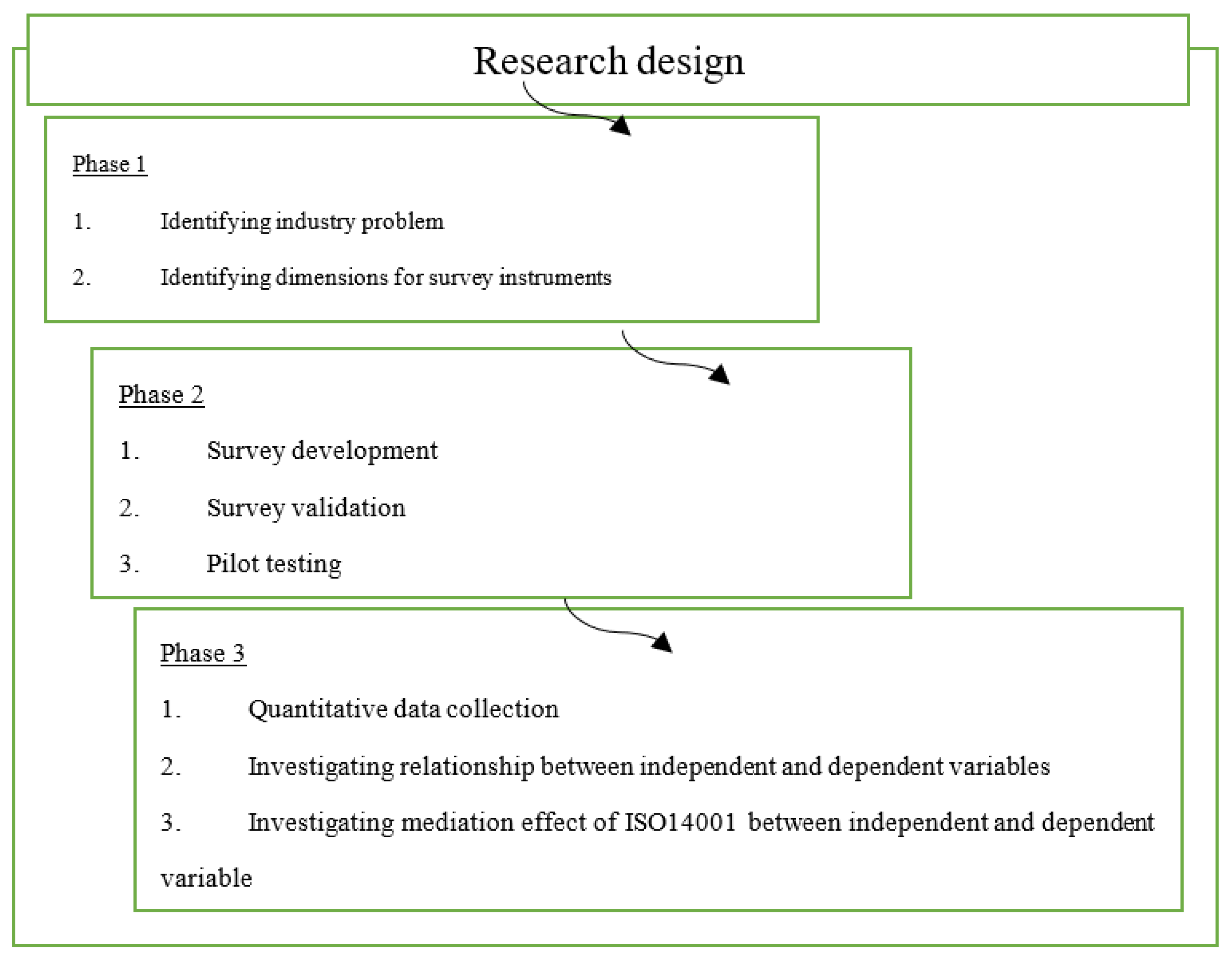

3. Methods

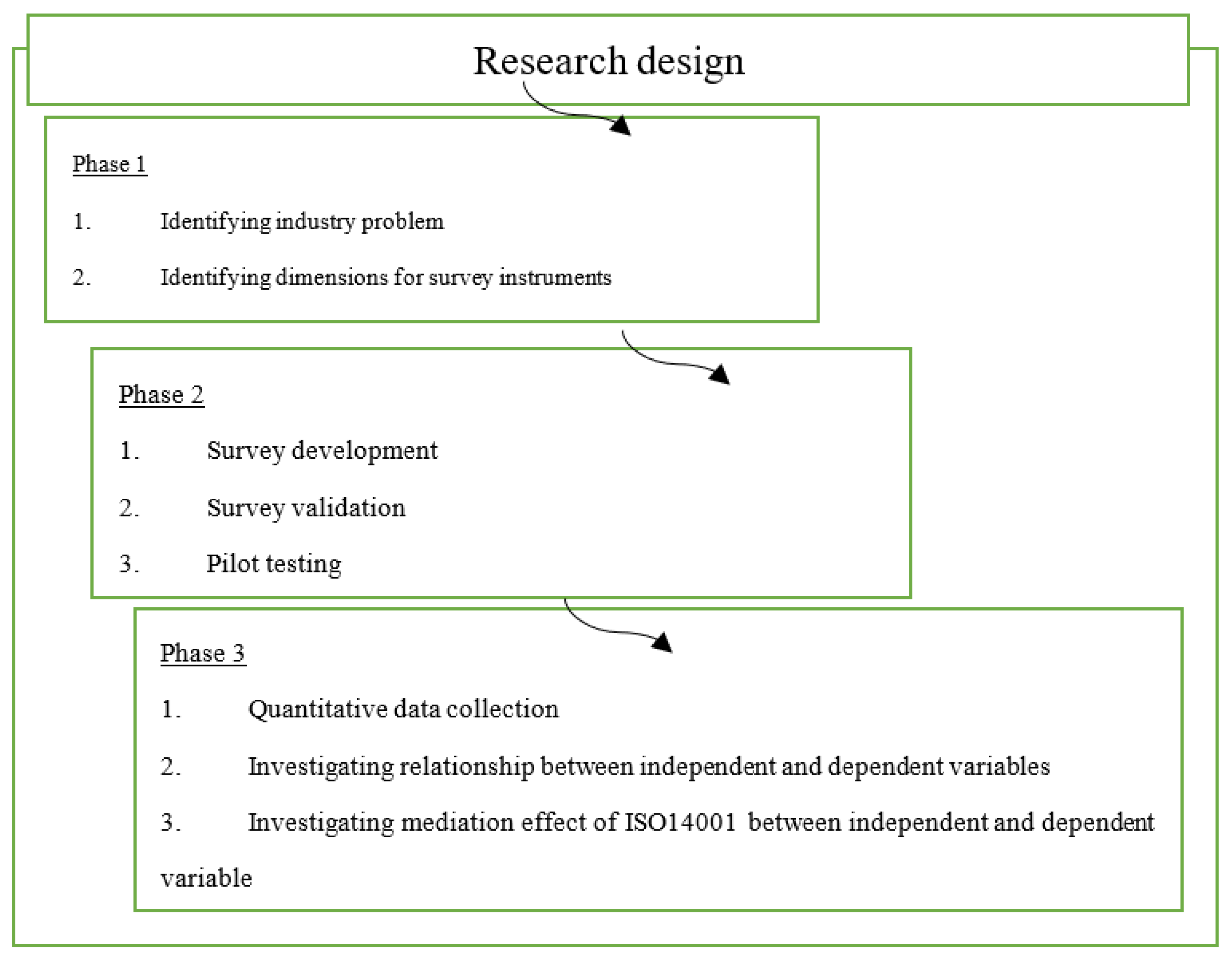

Research Process/Design

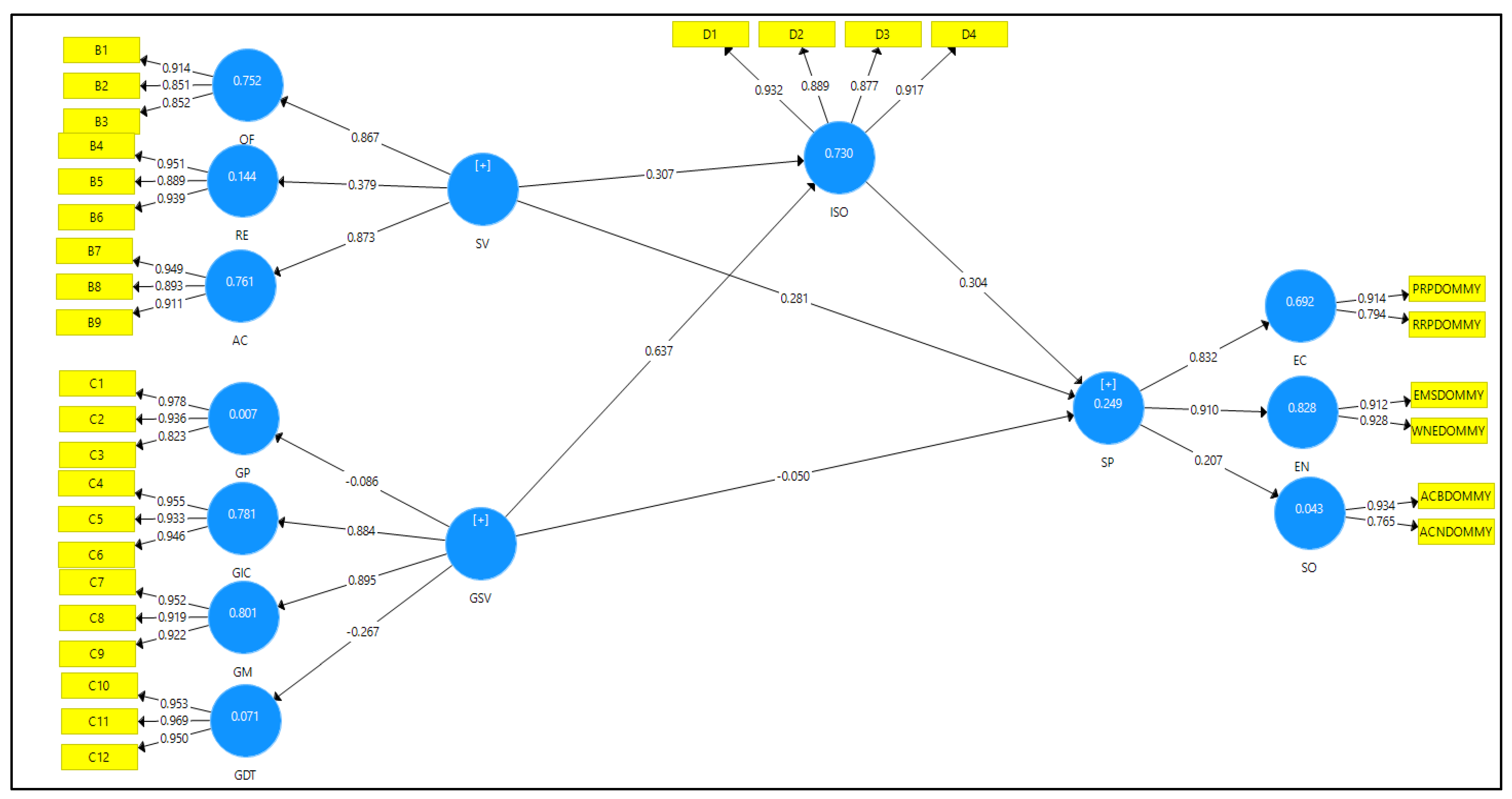

4. Data Analysis

4.1. Validity and Reliability

Measurement and Structural Analysis of Hypotheses

- (a)

- Confirmation of the operational definitions of the multiple items

- (b)

- Expert panel to reduce face validity

- (c)

- Refinement and purification of the items through pilot study

4.2. Results

5. Discussion

6. Conclusions

6.1. Managerial/Practical Implication

6.1.1. Policy Implication

6.1.2. Theoretical Implications

Resource Based View (RBV)

Institutional Theory

6.1.3. Limitations and Recommendations of the Study

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Tassabehji, R.; Isherwood, A. During Turbulent Times 1. Strateg. Chang. 2014, 23, 63–80. [Google Scholar] [CrossRef]

- Vandermerwe, S.; Rada, J. Servitization of business: Adding value by adding services. Eur. Manag. J. 1988, 6, 314–324. [Google Scholar] [CrossRef]

- Johl, S.K.; Khan, P.A. Firm’s Sustainability and Societal Development from the Lens of Fishbone Eco-Innovation: A Moderating Role of ISO 14001-2015 Environmental. Processes 2020, 8, 1152. [Google Scholar]

- Triguero, A.; Moreno-Mondéjar, L.; Davia, M.A. Drivers of different types of eco-innovation in European SMEs. Ecol. Econ. 2013, 92, 25–33. [Google Scholar] [CrossRef]

- Tsai, K.H.; Liao, Y.C. Sustainability Strategy and Eco-Innovation: A Moderation Model. Bus. Strategy Environ. 2017, 26, 426–437. [Google Scholar] [CrossRef]

- Khan, P.A.; Johl, S.K.; Johl, S.K. Does adoption of ISO 56002-2019 and green innovation reporting enhance the firm sustainable development goal performance? An emerging paradigm. Bus. Strategy Environ. 2021, 30, 2922–2936. [Google Scholar] [CrossRef]

- Schoemaker, P.J.H.; Heaton, S.; Teece, D. Innovation, dynamic capabilities, and leadership. Calif. Manag. Rev. 2018, 61, 15–42. [Google Scholar] [CrossRef] [Green Version]

- Singh, S.K.; Del Giudice, M.; Chierici, R.; Graziano, D. Green innovation and environmental performance: The role of green transformational leadership and green human resource management. Technol. Forecast. Soc. Chang. 2020, 150, 119762. [Google Scholar] [CrossRef]

- Ab Talib, M.S.; Muniandy, S. Green supply chain initiatives in Malaysia: A conceptual critical success factors framework. World Appl. Sci. J. 2013, 26, 276–281. [Google Scholar]

- Zhu, Q.; Geng, Y.; Fujita, T.; Hashimoto, S. Green supply chain management in leading manufacturers: Case studies in Japanese large companies. Manag. Res. Rev. 2010, 33, 380–392. [Google Scholar] [CrossRef]

- Carter, S.M.; Greer, C.R. Strategic leadership: Values, styles, and organizational performance. J. Leadersh. Organ. 2013, 20, 375–393. [Google Scholar] [CrossRef]

- Lee, C. Manufacturing Performance and Services Inputs: Evidence from Malaysia. Economics Working Paper 2019. Available online: http://hdl.handle.net/11540/9693 (accessed on 30 May 2020).

- Andries, P.; Stephan, U. Environmental innovation and firm performance: How firm size and motives matter. Sustainaibility 2019, 11, 3585. [Google Scholar] [CrossRef] [Green Version]

- Ar, I.M. The Impact of Green Product Innovation on Firm Performance and Competitive Capability: The Moderating Role of Managerial Environmental Concern. Procedia Soc. Behav. Sci. 2012, 62, 854–864. [Google Scholar] [CrossRef] [Green Version]

- Müller, R.; Turner, R. Leadership competency profiles of successful project managers. Int. J. Constr. Proj. Manag. 2010, 28, 437–448. [Google Scholar] [CrossRef]

- Annarelli, A.; Battistella, C.; Nonino, F. The Road to Servitization; Springer: Cham, Switzerland, 2019. [Google Scholar]

- Lay, G. Servitization in Industry; Springer: Berlin/Heidelberg, Germany, 2014; Volume 9783319069, pp. 1–349. [Google Scholar]

- Schneider, M. A stakeholder model of organizational leadership. Organ. Sci. 2002, 13, 209–220. [Google Scholar] [CrossRef] [Green Version]

- Marić, J.; Opazo-Basáez, M. Green Servitization for Flexible and Sustainable Supply Chain Operations: A Review of Reverse Logistics Services in Manufacturing. Glob. J. Flex. Syst. Manag. 2019, 20, 65–80. [Google Scholar] [CrossRef]

- Fernando, Y.; Chiappetta Jabbour, C.J.; Wah, W.X. Pursuing green growth in technology firms through the connections between environmental innovation and sustainable business performance: Does service capability matter? Resour. Conserv. Recycl. 2019, 141, 8–20. [Google Scholar] [CrossRef]

- Humbeck, P.; Pfähler, K.; Wiedenmann, M.; Herzwurm, G. The impact of servitization and digital transformation-a conceptual extension of the ipoo-framework. Procedia CIRP 2019, 81, 914–919. [Google Scholar] [CrossRef]

- Oyewale, O.I.; Johl, S.K. The effect of green servitization on malaysian manufacturing firm sustainability: A moderating role of iso 14001:2015 environmental management system. Ann. Romanian Soc. Cell Biol. 2021, 25, 4563–4570. [Google Scholar]

- Zhang, W.; Banerji, S. Challenges of servitization: A systematic literature review. Ind. Mark. Manag. 2017, 65, 217–227. [Google Scholar]

- Bustinza, O.F.; Vendrell-Herrero, F.; Baines, T. Service implementation in manufacturing: An organisational transformation perspective. Int. J. Prod. Econ. 2017, 192, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Hao, Z.; Goh, M.; Jiao, J.; Liu, C.G. Buyer-supplier dyad on performance and sustainability. J. Manuf. Technol. Manag. 2022; in press. [Google Scholar] [CrossRef]

- Ahmad, K.; Zabri, S.M. The Application of Non-Financial Performance Measurement in Malaysian Manufacturing Firms. Procedia Econ. Financ. 2016, 35, 476–484. [Google Scholar] [CrossRef] [Green Version]

- Naz, F.; Ijaz, F.; Naqvi, F. Financial Performance of Firms: Evidence from Pakistan Cement Industry. J. Teach. Educ. 2016, 5, 81–94. [Google Scholar]

- Parida, V.; George, N.M.; Lahti, T.; Wincent, J. Influence of subjective interpretation, causation, and effectuation on initial venture sale. J. Bus. Res. 2016, 69, 4815–4819. [Google Scholar] [CrossRef]

- Baumgartner, R.J.; Rauter, R. Strategic perspectives of corporate sustainability management to develop a sustainable organization. J. Clean. Prod. 2017, 140, 81–92. [Google Scholar] [CrossRef]

- Adeyemi, I.G. Servitize, Design and Co-Create Values through Social Media. Master’s Thesis, University of Vaasa, Vaasa, Finland, 2015. [Google Scholar]

- Nishitani, K.; Kaneko, S.; Komatsu, S.; Fujii, H. How does a firm’s management of greenhouse gas emissions influence its economic performance? Analyzing effects through demand and productivity in Japanese manufacturing firms. J. Product. Anal. 2014, 42, 355–366. [Google Scholar] [CrossRef]

- Ayala, N.F.; Gerstlberger, W.; Frank, A.G. Managing servitization in product companies: The moderating role of service suppliers. Int. J. Oper. Prod. Man. 2019, 39, 43–74. [Google Scholar] [CrossRef]

- Carrión-Flores, C.E.; Innes, R. Environmental innovation and environmental performance. J. Environ. Econ. Manag. 2010, 59, 27–42. [Google Scholar] [CrossRef]

- Adrodegari, F.; Bacchetti, A.; Saccani, N.; Arnaiz, A.; Meiren, T. The transition towards service-oriented business models: A European survey on capital goods manufacturers. Int. J. Eng. Bus. Manag. 2018, 10, 1847979018754469. [Google Scholar] [CrossRef]

- Jimenez, B.; Angelov, B.; Rao, B. Service Absorptive Capacity: Its Evolution and Implications for Innovation. J. Knowl. Econ. 2012, 3, 142–163. [Google Scholar] [CrossRef]

- Crozet, M.; Milet, E. Should everybody be in services? The effect of servitization on manufacturing firm performance. J. Econ. Manag. Strat. 2017, 26, 820–841. [Google Scholar] [CrossRef]

- Kowalkowski, C.; Gebauer, H.; Kamp, B.; Parry, G. Servitization and deservitization: Overview, concepts, and definitions. Ind. Mark. Manag. 2017, 60, 4–10. [Google Scholar] [CrossRef]

- Wang, W.; Lai, K.H.; Shou, Y. The impact of servitization on firm performance: A meta-analysis. Int. J. Oper. Prod. Manag. 2018, 38, 1562–1588. [Google Scholar] [CrossRef]

- Holmström, J.; Liotta, G.; Chaudhuri, A. Sustainability outcomes through direct digital manufacturing-based operational practices: A design theory approach. J. Clean. Prod. 2017, 167, 951–961. [Google Scholar] [CrossRef]

- Kowalkowski, C.; Kindström, D.; Alejandro, T.B.; Brege, S.; Biggemann, S. Service infusion as agile incrementalism in action. J. Bus. Res. 2012, 65, 765–772. [Google Scholar] [CrossRef] [Green Version]

- Manan, Z.A.; Mohd Nawi, W.N.R.; Wan Alwi, S.R.; Klemeš, J.J. Advances in Process Integration research for CO2 emission reduction—A review. J. Clean. Prod. 2017, 167, 1–13. [Google Scholar] [CrossRef]

- Sharma, S.; Prakash, G.; Kumar, A.; Mussada, E.K.; Antony, J.; Luthra, S. Analysing the relationship of adaption of green culture, innovation, green performance for achieving sustainability: Mediating role of employee commitment. J. Clean. Prod. 2021, 303, 127039. [Google Scholar] [CrossRef]

- Baines, T.; Ziaee Bigdeli, A.; Bustinza, O.F.; Shi, V.G.; Baldwin, J.; Ridgway, K. Servitization: Revisiting the state-of-the-art and research priorities. Int. J. Oper. Prod. Man. 2017, 37, 256–278. [Google Scholar] [CrossRef]

- Bustinza, O.F.; Gomes, E.; Vendrell-Herrero, F.; Baines, T. Product–service innovation and performance: The role of collaborative partnerships and R&D intensity. R D Manag. 2019, 49, 33–45. [Google Scholar]

- Zhu, Q.; Sarkis, J.; Lai, K.H. Green supply chain management innovation diffusion and its relationship to organizational improvement: An ecological modernization perspective. J. Eng. Technol. Manag. 2012, 29, 168–185. [Google Scholar] [CrossRef]

- Klewitz, J.; Hansen, E.G. Sustainability-oriented innovation of SMEs: A systematic review. J. Clean. Prod. 2014, 65, 57–75. [Google Scholar] [CrossRef]

- Klewitz, J.; Zeyen, A.; Hansen, E.G. Intermediaries driving eco-innovation in SMEs: A qualitative investigation. Eur. J. Innov. Manag. 2012, 15, 442–467. [Google Scholar] [CrossRef] [Green Version]

- Bryman, A.; Collinson, D.; Grint, K.; Jackson, B.; Uhl-Bien, M. The SAGE Handbook of Leadership; Sage: London, UK, 2011. [Google Scholar]

- Hosseinpou, M.; Mohamed, Z.; Rezai, G.; Shamsudin, M.N.; AbdLatif, I. How Go Green Campaign Effects on Malaysian Intention towards Green Behaviour. J. Appl. Sci. 2015, 15, 929–933. [Google Scholar] [CrossRef]

- Kastalli, I.V.; Van Looy, B. Servitization: Disentangling the impact of service business model innovation on manufacturing firm performance. JOM 2013, 31, 169–180. [Google Scholar] [CrossRef] [Green Version]

- Evans, S.; Vladimirova, D.; Holgado, M.; Van Fossen, K.; Yang, M.; Silva, E.A.; Barlow, C.Y. Business Model Innovation for Sustainability: Towards a Unified Perspective for Creation of Sustainable Business Models. Bus. Strategy Environ. 2017, 26, 597–608. [Google Scholar] [CrossRef]

- Polzin, F.; von Flotow, P.; Nolden, C. Exploring the Role of Servitization to Overcome Barriers for Innovative Energy Efficiency Technologies The Case of Public LED Street Lighting in German Municipalities. SSRN Electron. J. 2016, 7. [Google Scholar] [CrossRef] [Green Version]

- Ambroise, L.; Prim-Allaz, I.; Teyssier, C. Financial performance of servitized manufacturing firms: A configuration issue between servitization strategies and customer-oriented organizational design. Ind. Mark. Manag. 2018, 71, 54–68. [Google Scholar] [CrossRef]

- García-Morales, V.J.; Jiménez-Barrionuevo, M.M.; Gutiérrez-Gutiérrez, L. Transformational leadership influence on organizational performance through organizational learning and innovation. J. Bus. Res. 2012, 65, 1040–1050. [Google Scholar] [CrossRef]

- Helms, T. Asset transformation and the challenges to servitize a utility business model. Energy Policy 2016, 91, 98–112. [Google Scholar] [CrossRef]

- Benedettini, O.; Neely, A.; Swink, M. Why do servitized firms fail? A risk-based explanation. Int. J. Oper. Prod. Man. 2015, 35, 946–979. [Google Scholar] [CrossRef]

- Szász, L.; Seer, L. Towards an operations strategy model of servitization: The role of sustainability pressure. Oper. Manga. Res. 2018, 11, 51–66. [Google Scholar] [CrossRef]

- Baines, T.; Lightfoot, H.; Smart, P.; Fletcher, S. Servitization of manufacture: Exploring the deployment and skills of people critical to the delivery of advanced services. J. Manuf. Technol. Manag. 2013, 24, 637–646. [Google Scholar] [CrossRef] [Green Version]

- Doni, F.; Corvino, A.; Bianchi Martini, S. Servitization and sustainability actions. Evidence from European manufacturing companies. J. Environ. Manag. 2019, 234, 367–378. [Google Scholar]

- Raddats, C.; Kowalkowski, C.; Benedettini, O.; Burton, J.; Gebauer, H. Servitization: A contemporary thematic review of four major research streams. Ind. Mark. Manag. 2019, 83, 207–223. [Google Scholar] [CrossRef]

- Opazo-Basáez, M.; Vendrell-Herrero, F.; Bustinza, O.F. Uncovering productivity gains of digital and green servitization: Implications from the automotive industry. Sustainability 2018, 10, 1524. [Google Scholar] [CrossRef] [Green Version]

- Martín-Peña, M.L.; Sánchez-López, J.M.; Díaz-Garrido, E. Servitization and digitalization in manufacturing: The influence on firm performance. J. Bus. Ind. Mark. 2019, 35, 564–574. [Google Scholar] [CrossRef]

- Maheepala, D.S.R.; Warnakulasooriya, B.N.F.; Banda, Y.K. Servitization in Manufacturing Firms and Business Performance: A Systematic Literature Review Maheepala. Int. J. Bus. Soc. Sci. 2016, 7, 200–210. [Google Scholar]

- Charter, M.; Young, A.; Kielkiewicz-Young, A.; Belmane, I. Integrated product policy and eco-product development. In Sustainable Solutions: Developing Products and Services for the Future; Routledge: Abingdon-on-Thames, UK, 2017; pp. 98–116. [Google Scholar]

- Sustainable, T.; Goals, D. The Sustainable Development Goals Report. SDGs. 2016. Available online: https://books.google.com.my/books?hl=en&lr=&id=-A4LDgAAQBAJ&oi=fnd&pg=PP1&dq=65.%09Sustainable,+T.%3B+Goals,+D.+The+Sustainable+Development+Goals+report.+SDGs.+2016&ots=dcml1QagCD&sig=EaKBlanE8EHnlOQ843fZCQZEjc0#v=onepage&q&f=false (accessed on 20 March 2021).

- Thun, J.H.; Müller, A. An empirical analysis of green supply chain management in the german automotive industry. Bus. Strategy Environ. 2010, 19, 119–132. [Google Scholar] [CrossRef]

- Andersén, J. A relational natural-resource-based view on product innovation: The influence of green product innovation and green suppliers on differentiation advantage in small manufacturing firms. Technovation 2021, 104, 102254. [Google Scholar] [CrossRef]

- Björkdahl, J. Strategies for Digitalization in Manufacturing Firms. Calif. Manag. Rev. 2020, 62, 17–36. [Google Scholar] [CrossRef]

- Rehman, S.U.; Kraus, S.; Shah, S.A.; Khanin, D.; Mahto, R.V. Analyzing the relationship between green innovation and environmental performance in large manufacturing firms. Technol. Forecast. Soc. Chang. 2021, 163, 120481. [Google Scholar] [CrossRef]

- Mijatović, M.D.; Uzelac, O.; Stoiljković, A. Effects of human resources management on the manufacturing firm performance: Sustainable development approach. J. Ind. Eng. Manag. 2020, 11, 205–212. [Google Scholar] [CrossRef]

- Oyelakin, I.O.; Johl, S.K. Green servitization as a means of sustainable performance: Evidence of listed manufacturing firms. Cogent. Eng. 2022, 9, 2014250. [Google Scholar] [CrossRef]

- Ettlie, J.E. What makes a manufacturing firm innovative? Acad. Manag. Perspect. 1990, 4, 7–20. [Google Scholar] [CrossRef]

- Prieto-Sandoval, V.; Jaca, C.; Ormazabal, M. Towards a consensus on the circular economy. J. Clean. Prod. 2018, 179, 605–615. [Google Scholar] [CrossRef]

- Siltori, P.F.S.; Simon Rampasso, I.; Martins, V.W.B.; Anholon, R.; Silva, D.; Souza Pinto, J. Analysis of ISO 9001 certification benefits in Brazilian companies. Total. Qual. Manag. Bus. Excell. 2020, 32, 1614–1632. [Google Scholar] [CrossRef]

- Li, X.; Hamblin, D. Factors impacting on cleaner production: Case studies of Chinese pharmaceutical manufacturers in Tianjin, China. J. Clean. Prod. 2016, 131, 121–132. [Google Scholar] [CrossRef]

- Afriyie, S.; Du, J.; Ibn Musah, A.-A. Innovation and marketing performance of SME in an emerging economy: The moderating effect of transformational leadership. J. Glob. Entrep. Res. 2019, 9, 40. [Google Scholar] [CrossRef] [Green Version]

- Afriyie, S.; Du, J.; Musah, A.A.I. Innovation and Knowledge Sharing of Sme in an Emerging Economy; The Moderating Effect of Transformational Leadership Style. Int. J. Innov. Manag. 2020, 24, 2050034. [Google Scholar] [CrossRef]

- Adams, R.; Jeanrenaud, S.; Bessant, J.; Denyer, D.; Overy, P. Sustainability-oriented Innovation: A Systematic Review. Int. J. Manag. Rev. 2016, 18, 180–205. [Google Scholar] [CrossRef]

- Kobayashi, H. Strategic evolution of eco-products: A product life cycle planning methodology. Res. Eng. Des. 2005, 16, 1–16. [Google Scholar] [CrossRef]

- de Marchi, V.; Grandinetti, R. Knowledge strategies for environmental innovations: The case of Italian manufacturing firms. J. Knowl. Manag. 2013, 17, 569–582. [Google Scholar] [CrossRef]

- Smith, L.; Maull, R.; Ng, I.C.L. Servitization and operations management: A service dominant-logic approach. Int. J. Oper. Prod. Manag. 2014, 34, 242–269. [Google Scholar] [CrossRef]

- Malaysian Standard 2400-2:2019; Halal Supply Chain Management System-Part 2: Warehousing-General Requirements. Department of Standard Malaysia: Cyberjaya, Malaysia, 2015; pp. 1–15.

- Campos, L.M.S.; De Melo Heizen, D.A.; Verdinelli, M.A.; Cauchick Miguel, P.A. Environmental performance indicators: A study on ISO 14001 certified companies. J. Clean. Prod. 2015, 99, 286–296. [Google Scholar] [CrossRef]

- Karabulut, A.T. Effects of Innovation Types on Performance of Manufacturing Firms in Turkey. Procedia Soc. Behav. Sci. 2015, 195, 1355–1364. [Google Scholar] [CrossRef] [Green Version]

- Chardine-Baumann, E.; Botta-Genoulaz, V. A framework for sustainable performance assessment of supply chain management practices. Comput. Ind. Eng. 2014, 76, 138–147. [Google Scholar] [CrossRef]

- Willis, K. The Sustainable Development Goals. In The Routledge Handbook of Latin American Development; Routledge: Abingdon-on-Thames, UK, 2019; pp. 121–131. [Google Scholar]

- Bursa Malaysia. Sustainability Reporting Guide; Bursa Malaysia: Kuala Lumpur, Malaysia, 2015; pp. 1–76. [Google Scholar]

- Valtakoski, A. Explaining servitization failure and deservitization: A knowledge-based perspective. Ind. Mark. Manag. 2017, 60, 138–150. [Google Scholar] [CrossRef]

- Ong, H.C.; Mahlia, T.M.I.; Masjuki, H.H. A review on energy scenario and sustainable energy in Malaysia. Renew. Sust. Energ. Rev. 2011, 15, 639–647. [Google Scholar] [CrossRef]

- Rahman Mohamed, A.; Lee, K.T. Energy for sustainable development in Malaysia: Energy policy and alternative energy. Energy Policy 2006, 34, 2388–2397. [Google Scholar] [CrossRef]

- Stavropoulos, S.; Wall, R.; Xu, Y. Environmental regulations and industrial competitiveness: Evidence from China. Appl. Econ. 2018, 50, 1378–1394. [Google Scholar] [CrossRef] [Green Version]

- Mastrogiacomo, L.; Barravecchia, F.; Franceschini, F. Definition of a conceptual scale of servitization: Proposal and preliminary results. CIRP. J. Manuf. Sci. Technol. 2020, 29, 141–156. [Google Scholar] [CrossRef]

- Hojnik, J.; Ruzzier, M. Does it pay to be eco? The mediating role of competitive benefits and the effect of ISO 14001. Eur. Manag. J. 2017, 35, 581–594. [Google Scholar] [CrossRef]

- Salim, H.K.; Padfield, R.; Hansen, S.B.; Mohamad, S.E.; Yuzir, A.; Syayuti, K.; Tham, M.H.; Papargyropoulou, E. Global trends in environmental management system and ISO 14001 research. J. Clean. Prod. 2018, 170, 645–653. [Google Scholar] [CrossRef] [Green Version]

- Krejcie, R.V.; Morgan, D.W. Determining Sample Size for Research Activities. Educ. Psychol. Meas. 1970, 30, 607–610. [Google Scholar] [CrossRef]

- Israel, G.D. Determining Sample Size. Fact Sheet PEOD. 1992. Available online: https://www.academia.edu/21353552/Determining_Sample_Size_1 (accessed on 17 May 2021).

- Hair, J.F.; Ringle, C.M.; Sarstedt. Partial Least Squares Structural Equation Modeling: Rigorous Applications, Better Results and Higher Acceptance. Long Range Plan. 2013, 46, 1–12. [Google Scholar] [CrossRef]

- Nitzl, C. The use of partial least squares structural equation modelling (PLS-SEM) in management accounting research: Directions for future theory development. J. Account. Lit. 2016, 37, 19–35. [Google Scholar] [CrossRef]

- Hair, J.; Hollingsworth, C.L.; Randolph, A.B.; Chong, A.Y.L. An updated and expanded assessment of PLS-SEM in information systems research. Ind. Manag. Data Syst. 2017, 117, 442–458. [Google Scholar] [CrossRef]

- Hair, J.F.; Howard, M.C.; Nitzl, C. Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. J. Bus. Res. 2020, 109, 101–110. [Google Scholar] [CrossRef]

- Vickery, B.; Vickery, A. An application of language processing for a search interface. J. Doc. 1992, 48, 255–275. [Google Scholar] [CrossRef]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Churchill, G.A. A Paradigm for Developing Better Measures of Marketing Constructs. J. Mark. Res. 1979, 16, 64–73. [Google Scholar] [CrossRef]

- Paiola, M.; Schiavone, F.; Grandinetti, R.; Chen, J. Digital servitization and sustainability through networking: Some evidences from IoT-based business models. J. Bus. Res. 2021, 132, 507–516. [Google Scholar] [CrossRef]

- Kazi, A.M.; Khalid, W. Questionnaire designing and validation Introduction and Objectives. J. Pak. Med. Assoc. 2012, 62, 514. [Google Scholar] [PubMed]

- Leeflang, P.S.H.; Wieringa, J.E.; Bijmolt, T.H.A.; Pauwels, K.H. Advanced Methods for Modeling Markets; Springer: Cham, Switzerland, 2017; pp. 671–683. [Google Scholar]

- Megel, M.E.; Heermann, J.A. Methods of data collection. Plast. Surg. Nurs. 1994, 14, 109–110. [Google Scholar] [PubMed]

- Selvam, M.; Gayathri, J.; Vasanth, V.; Lingaraja, K.; Marxiaoli, S. Determinants of Firm Performance: A Subjective Model. Int. J. Soc. Sci. 2016, 4, 90–100. [Google Scholar] [CrossRef] [Green Version]

- Mcneish, D.; Mcneish, D. Psychological Methods Thanks Coefficient Alpha, We’ll Take It from Here Thanks Coefficient Alpha, We’ll Take It from Here. Psychol. Methods 2018, 23, 412–433. [Google Scholar] [CrossRef]

- Baron, S.; Warnaby, G.; Hunter-Jones, P. Service(s) marketing research: Developments and directions. Int. J. Manag. Rev. 2014, 16, 150–171. [Google Scholar] [CrossRef]

- Hair, J.F.; Matthews, L.M.; Matthews, R.L.; Sarstedt, M. PLS-SEM or CB-SEM: Updated guidelines on which method to use. Int. J. Multivar. Data Anal. 2017, 1, 107. [Google Scholar] [CrossRef]

- Ringle, C.M.; Sarstedt, M.; Straub, D.W. The Editor’s Corner Request Permissions/Order Reprints. MIS Q. 2012, 36, 3–14. [Google Scholar]

- Kowalkowski, C.; Kindström, D. Servitization in Manufacturing Firms: A business model perspective. In Proceedings of the Spring Servitization Conference (SSC2013), Birmingham, UK, 20–21 May 2013. [Google Scholar]

- Lightfoot, H.; Baines, T.; Smart, P. The servitization of manufacturing: Investigating contributions to knowledge production. Int. J. Oper. Prod. Manag. 2013, 33, 1408–1434. [Google Scholar] [CrossRef] [Green Version]

- Pistoni, A.; Songini, L. Servitization strategy: Key features and implementation issues. Stud. Manag. Fin. Acc. 2017, 32, 37–110. [Google Scholar]

- Bititci, U.S.; Ackermann, F.; Ates, A.; Davies, J.; Garengo, P.; Gibb, S.; MacBryde, J.; Mackay, D.; Maguire, C.; van der Meer, R.; et al. Managerial processes: Business process that sustain performance. Int. J. Oper. Prod. Man. 2022, 31, 851–891. [Google Scholar] [CrossRef]

- Khan, N.U.; Saufi, R.A.; Rasli, A.M. Green Human Resource Management Practices among ISO 14001-certified Malaysian Manufacturing Firms. In Green Behavior and Corporate Social Responsibility in Asia; Emerald Publishing Limited: Bingley, UK, 2019; pp. 73–79. [Google Scholar]

- Barney, J.B. Is the resource-based “view” a useful perspective for strategic management research? Yes. Acad. Manag. Rev. 2001, 26, 41–56. [Google Scholar]

- Yee, F.M.; Shaharudin, M.R.; Ma, G.; Mohamad Zailani, S.H.; Kanapathy, K. Green purchasing capabilities and practices towards Firm’s triple bottom line in Malaysia. J. Clean. Prod. 2021, 307, 127268. [Google Scholar] [CrossRef]

- Camilleri, M.A. The rationale for ISO 14001 certification: A systematic review and a cost–benefit analysis. Corp. Soc. Responsib. Environ. 2022, 29, 1067–1083. [Google Scholar] [CrossRef]

- Risi, D.; Vigneau, L.; Bohn, S.; Wickert, C. Institutional theory-based research on corporate social responsibility: Bringing values back in. Int. J. Manag. Rev. 2022, 1–21. [Google Scholar] [CrossRef]

- Ministry of Economic Affairs. The Malaysian Economy in Figures 2019—Southeast Asian Affairs; Ministry of Economic Affairs: Putrajaya, Malaysian, 2018; pp. 207–222. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Servitization [32,53] | |

| Offerings Competitive and differentiation advantage Customer need Value added Customer orientation | Resources Knowledge Expertise Capabilities and Flexibility |

| Activities Customer integration Further business units’ integration | |

| Green Servitization [19,32,61] | |

| Green Product Cost saving Efficient Safety | Green Internal Competencies Knowledge Expertise Capabilities and Flexibility |

| Green Maintenance Technical Requirement Service Requirement Sales Requirement | Green Digital Technology Digital interactions with product Digital value creation to product |

| ISO 14001 [82,83] | |

| Operations Planning and control Emergency preparedness and response | Performance Evaluation Monitory and measurement Analysis and evaluation |

| No | Items | No of Items | Cronbach α |

|---|---|---|---|

| 1 | Servitization | ||

| i | Offerings | 3 | 0.931 |

| ii | Resources | 3 | 0.924 |

| iii | Activities | 3 | 0.800 |

| 2 | Green-Servitization | ||

| i | Product | 3 | 0.890 |

| ii | Internal Competencies | 3 | 0.879 |

| iii | Maintenance | 3 | 0.942 |

| iv | Digital Technology | 3 | 0.938 |

| 3 | ISO 14001 | ||

| i | Operations | 2 | 0.961 |

| ii | Performance Evaluation | 2 | 0.961 |

| Total | 26 | 0.809 |

| Cronbach’s Alpha | rho_A | Composite Reliability | Average Variance Extracted (AVE) | |

|---|---|---|---|---|

| AC | 0.906 | 0.911 | 0.941 | 0.843 |

| EC | 0.748 | 0.720 | 0.845 | 0.733 |

| EN | 0.820 | 0.825 | 0.917 | 0.847 |

| GDT | 0.955 | 0.980 | 0.971 | 0.917 |

| GIC | 0.940 | 0.940 | 0.961 | 0.892 |

| GM | 0.923 | 0.923 | 0.951 | 0.867 |

| GP | 0.906 | 0.997 | 0.939 | 0.837 |

| GSV | 0.787 | 0.912 | 0.843 | 0.540 |

| ISO | 0.925 | 0.930 | 0.947 | 0.817 |

| OF | 0.843 | 0.844 | 0.906 | 0.762 |

| RE | 0.919 | 0.958 | 0.948 | 0.859 |

| SO | 0.652 | 0.807 | 0.841 | 0.728 |

| SP | 0.768 | 0.803 | 0.854 | 0.700 |

| SV | 0.852 | 0.867 | 0.890 | 0.545 |

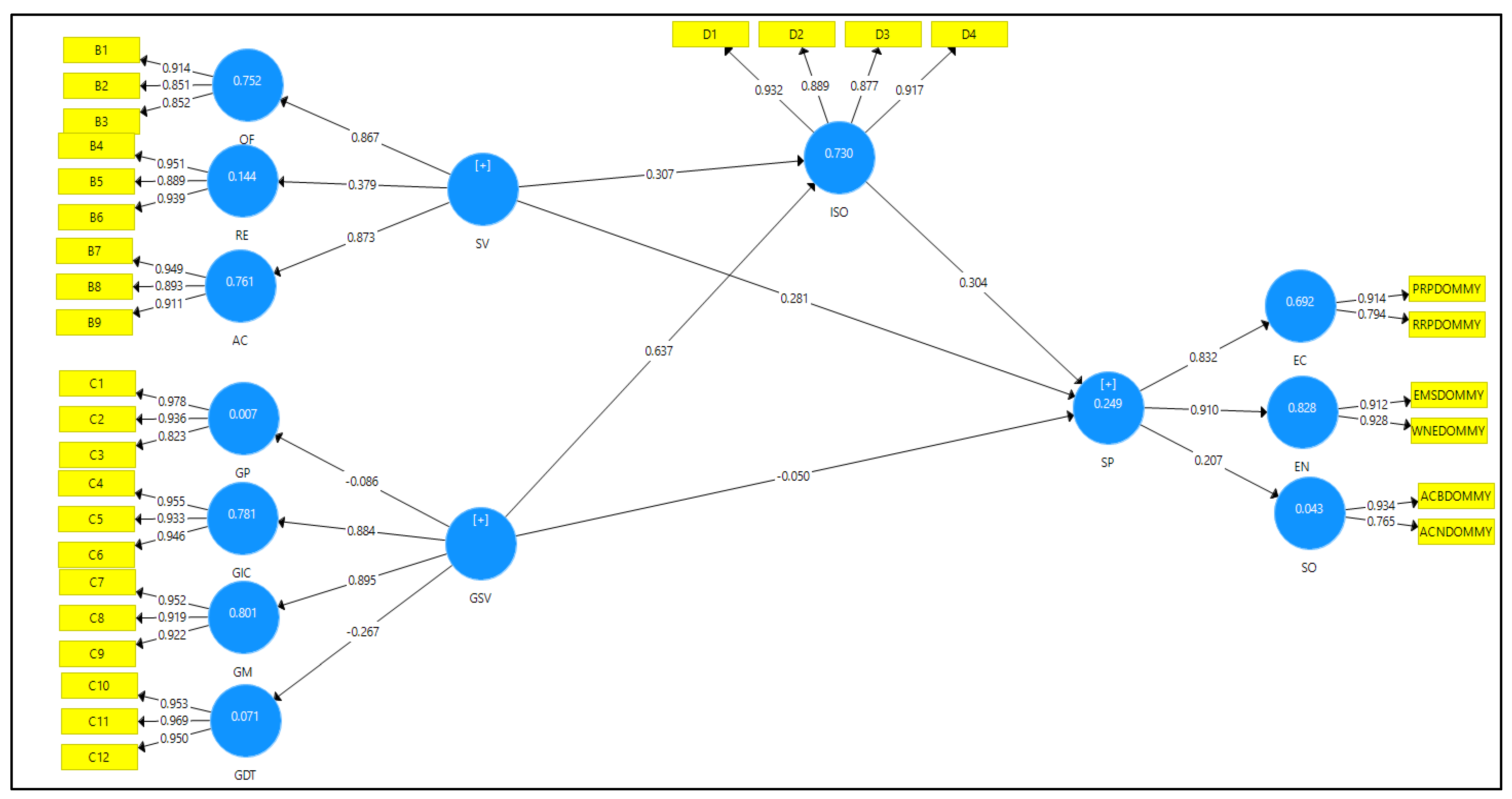

| Hypotheses | β-Value | T-Statistics | Confidence Interval (CI) | p Values | Result | |

|---|---|---|---|---|---|---|

| 2.50% | 97.50% | |||||

| SV -> SP | 0.281 | 3.564 | −0.244 | 0.150 | 0.001 | Supported |

| GSV -> SP | −0.050 | 0.499 | 0.129 | 0.438 | 0.618 | Not Supported |

| GSV -> ISO -> SP | 0.194 | 2.842 | 0.066 | 0.333 | 0.005 | Supported |

| SV -> ISO -> SP | 0.094 | 2.741 | 0.031 | 0.166 | 0.006 | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oyelakin, I.O.; Johl, S.K. Does ISO 14001 and Green Servitization Provide a Push Factor for Sustainable Performance? A Study of Manufacturing Firms. Sustainability 2022, 14, 9784. https://doi.org/10.3390/su14159784

Oyelakin IO, Johl SK. Does ISO 14001 and Green Servitization Provide a Push Factor for Sustainable Performance? A Study of Manufacturing Firms. Sustainability. 2022; 14(15):9784. https://doi.org/10.3390/su14159784

Chicago/Turabian StyleOyelakin, Idris Oyewale, and Satirenjit Kaur Johl. 2022. "Does ISO 14001 and Green Servitization Provide a Push Factor for Sustainable Performance? A Study of Manufacturing Firms" Sustainability 14, no. 15: 9784. https://doi.org/10.3390/su14159784

APA StyleOyelakin, I. O., & Johl, S. K. (2022). Does ISO 14001 and Green Servitization Provide a Push Factor for Sustainable Performance? A Study of Manufacturing Firms. Sustainability, 14(15), 9784. https://doi.org/10.3390/su14159784