Sustainable Development of Chinese Family Firms: A Perspective from Downward Earnings Management before Successions

Abstract

:1. Introduction

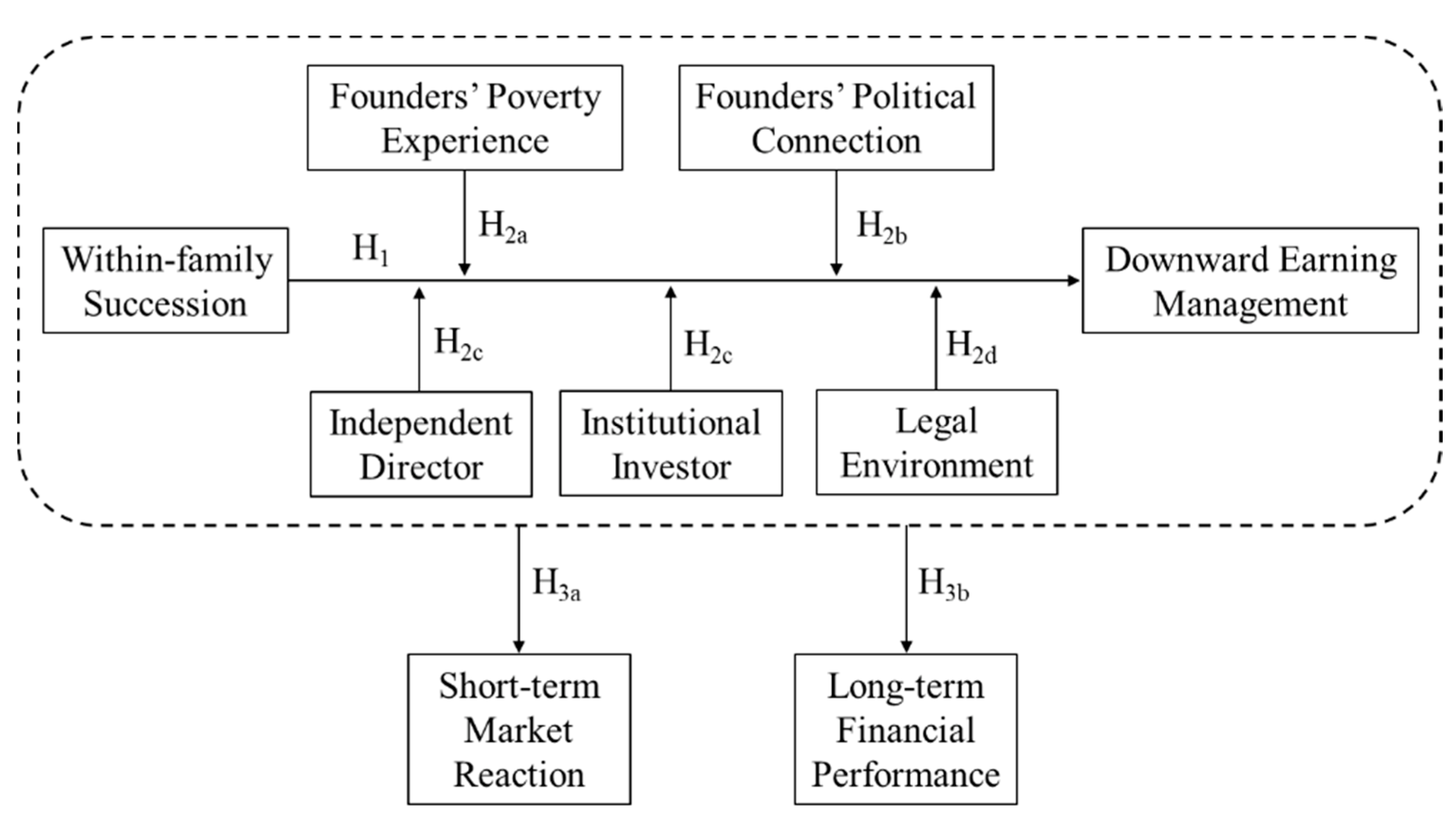

2. Literature Review and Hypothesis Development

2.1. Family Firm and Earnings Management

2.2. Moderating Factors

2.2.1. Founders’ Poverty Experience

2.2.2. Founders’ Political Connection

2.2.3. Independent Director

2.2.4. Institutional Investor

2.2.5. Legal Environment

2.3. The Impact of Downward Earnings Management

3. Data and Research Design

3.1. Data

3.2. Research Design

3.2.1. Measures of Earnings Management

3.2.2. Models

4. Results

4.1. Univariate Results

4.2. Multivariate Analysis

4.3. Additional Analysis

4.4. Robustness Test

4.4.1. Self-Selection Bias

4.4.2. The Alternative Measures of Real Earnings Management

4.4.3. The Alternative Measures of Other Variables

5. Conclusions and Discussion

5.1. Conclusions

5.2. Implications

5.3. Limitations and Future Research

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Borralho, J.M.; Vázquez, D.G.; Hernández-Linares, R. Earnings management in private family versus non-family firms. The moderating effect of family business generation. Span. J. Financ. Account. 2019, 49, 210–233. [Google Scholar] [CrossRef]

- Gomez-Mejia, L.R.; Cruz, C.; Berrone, P.; De Castro, J. The bind that ties: Socioemotional wealth preservation in family firms. Acad. Manag. Ann. 2011, 5, 653–707. [Google Scholar] [CrossRef]

- Ansari, I.F.; Goergen, M.; Mira, S. Earnings management around founder CEO reappointments and successions in family firms. Eur. Financ. Manag. 2021, 27, 925–958. [Google Scholar] [CrossRef]

- Braendle, U.C.; Grasser, T.; Noll, J. Corporate governance in China—is economic growth potential hindered by guanxi? Bus. Soc. Rev. 2005, 110, 389–405. [Google Scholar] [CrossRef]

- Bennedsen, M.; Fan, J.P.H.; Jian, M.; Yeh, Y.H. The family business map: Framework, selective survey, and evidence from Chinese family firm succession. J. Corp. Financ. 2015, 33, 212–226. [Google Scholar] [CrossRef]

- Fan, J.P.H.; Wong, T.J.; Zhang, T. Founder succession and accounting properties. Contemp. Account. Res. 2012, 29, 283–311. [Google Scholar] [CrossRef] [Green Version]

- Cao, J.; Cumming, D.; Wang, X. One-child policy and family firms in China. J. Corp. Financ. 2015, 33, 317–329. [Google Scholar] [CrossRef]

- Eshel, I.; Samuelson, L.; Shaked, A. Altruists, egoists, and holligans in a local interaction model. Am. Econ. Rev. 1998, 88, 157–179. [Google Scholar]

- Holtz-Eakin, D.; Joulfian, D.; Rosen, H.S. The Carnagie conjecture: Some empirical evidence. Q. J. Econ. 1993, 108, 413–435. [Google Scholar] [CrossRef] [Green Version]

- Cameron, L.; Erkal, N.; Gangadharan, L.; Meng, X. Little emperors: Behavioral impacts of China’s one-child policy. Sci. Express 2013, 339, 953–957. [Google Scholar] [CrossRef]

- Yang, J. China’s one-child policy and overweight children in the 1990s. Soc. Sci. Med. 2007, 64, 2043–2057. [Google Scholar] [CrossRef] [PubMed]

- Prencipe, A.; Markarian, G.; Pozza, L. Earnings management in family firms: Evidence from R&D cost capitalization in Italy. Fam. Bus. Rev. 2008, 21, 71–88. [Google Scholar]

- Chi, C.W.; Hung, K.; Cheng, H.W.; Tien Lieu, P. Family firms and earnings management in Taiwan: Influence of corporate governance. Int. Rev. Econ. Financ. 2015, 36, 88–98. [Google Scholar] [CrossRef]

- Chrisman, J.; Chua, J.; Sharma, P. Trends and directions in the development of a strategic management theory of the family firm. Entrep. Theory Pract. 2005, 29, 555–576. [Google Scholar] [CrossRef]

- Anderson, R.C.; Reeb, D.M. Board composition: Balancing family influence in S&P 500 firms. Adm. Sci. Q. 2004, 49, 209–237. [Google Scholar]

- Bubolz, M.M. Family as source, user, and builder of social capital. J. Socio-Econ. 2001, 30, 129–131. [Google Scholar] [CrossRef]

- Wang, D. Founding family ownership and earnings quality. J. Account. Res. 2006, 44, 619–656. [Google Scholar] [CrossRef]

- Martin, G.; Campbell, J.T.; Gomez-Mejia, L. Family control, socioemotional wealth and earnings management in publicly traded firms. J. Bus. Ethics 2014, 133, 453–469. [Google Scholar] [CrossRef] [Green Version]

- Fan, J.P.; Wong, T. Corporate ownership structure and the informativeness of accounting earnings in East Asia. J. Account. Econ. 2002, 33, 401–425. [Google Scholar] [CrossRef] [Green Version]

- Mura, L.; Zsigmond, T.; Machová, R. The effects of emotional intelligence and ethics of SME employees on knowledge sharing in Central-European countries. Oeconomia Copernic. 2021, 12, 907–934. [Google Scholar] [CrossRef]

- Settles, B.H.; Sheng, X.; Zang, Y.; Zhao, J. The one-child policy and its impact on Chinese families. In International Handbook of Chinese Families; Kwok-bun, C., Ed.; Springer: New York, NY, USA, 2013; pp. 627–646. [Google Scholar] [CrossRef]

- Li, X.C.; Chen, L.; Chua, J.H.; Kirkman, B.L.; Rynes-Weller, S.; Gomez-Mejia, L. Research on Chinese family businesses: Perspectives. Manag. Organ. Rev. 2015, 11, 579–597. [Google Scholar] [CrossRef] [Green Version]

- Rappa, A.; Tan, S.H. Political implications of Confucian familism. Asian Philos. 2003, 13, 87–102. [Google Scholar] [CrossRef]

- Rosenberg, B.G.; Jing, Q. A revolution in family life: The political and social structural impact of china’s one child policy. J. Soc. Issues 1996, 52, 51–69. [Google Scholar] [CrossRef]

- Main, M.; Kaplan, N.; Cassidy, J. Security in Infancy, Childhood, and Adulthood: A Move to the Level of Representation. Monogr. Soc. Res. Child Dev. 1985, 50, 66. [Google Scholar] [CrossRef]

- Kendler, K.S.; Myers, J.; Prescott, C.A. The Etiology of Phobias. Arch. Gen. Psychiatry 2002, 59, 242. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Graham, J.R.; Narasimhan, K. Corporate Survival and Managerial Experiences during the Great Depression; Unpublished Working Paper; Duke University: Durham, NC, USA, 2004. [Google Scholar]

- Bernile, G.; Bhagwat, V.; Rau, P.R. What doesn’t kill you will only make you more risk-loving: Early-life disasters and CEO behavior. J. Financ. 2017, 72, 167–206. [Google Scholar] [CrossRef]

- Cao, X.; Pan, X.; Qian, M.; Tian, G.G. Political capital and CEO entrenchment: Evidence from CEO turnover in Chinese non-SOEs. J. Corp. Financ. 2017, 42, 1–14. [Google Scholar] [CrossRef] [Green Version]

- You, J.; Du, G. Are political connections a blessing or a curse? Evidence from CEO turnover in China. Corp. Gov. Int. Rev. 2011, 20, 179–194. [Google Scholar] [CrossRef]

- Xing, L.; Duan, T.; Hou, W. Do board secretaries influence management earnings forecasts? J. Bus. Ethics 2017, 154, 537–574. [Google Scholar] [CrossRef] [Green Version]

- Fama, E.F. Agency problems and the theory of the firm. J. Political Econ. 1980, 88, 288–307. [Google Scholar] [CrossRef]

- Fama, E.F.; Jensen, M.C. Separation of Ownership and Control. J. Law Econ. 1983, 26, 301–325. [Google Scholar] [CrossRef]

- Roe, M.J. A political theory of American corporate finance. Columbia Law Rev. 1991, 91, 10–67. [Google Scholar] [CrossRef]

- Xie, B.; Davidson, W.N.; Da Dalt, P.J. Earnings management and corporate governance: The role of the board and the audit committee. J. Corp. Financ. 2003, 9, 295–316. [Google Scholar] [CrossRef]

- Klein, A. Audit committee, board of director characteristics, and earnings management. J. Account. Econ. 2002, 33, 375–400. [Google Scholar] [CrossRef] [Green Version]

- Peasnell, K.V.; Pope, P.F.; Young, S. Board Monitoring and earnings management: Do outside directors influence abnormal accruals? J. Bus. Financ. Account. 2005, 32, 1311–1346. [Google Scholar] [CrossRef]

- Bammens, Y.; Voordeckers, W.; Van Gils, A. Boards of directors in family firms: A generational perspective. Small Bus. Econ. 2007, 31, 163–180. [Google Scholar] [CrossRef] [Green Version]

- Chung, R.; Firth, M.; Kim, J.B. Institutional monitoring and opportunistic earnings management. J. Corp. Financ. 2002, 8, 29–48. [Google Scholar] [CrossRef]

- Karamanou, I.; Vefeas, N. The association between corporate boards, audit committees, and management earnings forecasts: An empirical analysis. J. Account. Res. 2005, 43, 453–486. [Google Scholar] [CrossRef]

- Bushee, B. The influence of institutional investors on myopic R&D investment behavior. Account. Rev. 1998, 73, 305–333. [Google Scholar]

- Bange, M.M.; De Bondt, W.F. R&D budgets and corporate earnings targets. J. Corp. Financ. 1998, 4, 153–184. [Google Scholar]

- Skinner, D.J. Why firms voluntarily disclose bad news. J. Account. Res. 1994, 32, 38–60. [Google Scholar] [CrossRef]

- Skinner, D.J. Earnings disclosures and stockholder lawsuits. J. Account. Econ. 1997, 23, 249–282. [Google Scholar] [CrossRef]

- Francis, J.R.; Wang, D. The joint effect of investor protection and Big 4 audits on earnings quality around the world. Contemp. Account. Res. 2008, 25, 157–191. [Google Scholar] [CrossRef]

- Bhattacharya, U.; Daouk, H.; Welker, M. The World Price of Earnings Opacity; Unpublished working paper; Indiana University: Bloomington, IN, USA, 2002. [Google Scholar]

- Bushman, R.M.; Piotroski, J.D.; Smith, A.J. What determines corporate transparency? J. Account. Res. 2004, 42, 207–252. [Google Scholar] [CrossRef]

- Ball, R.; Kothari, S.; Robin, A. The effect of international institutional factors on properties of accounting earnings. J. Account. Econ. 2000, 29, 1–51. [Google Scholar] [CrossRef] [Green Version]

- Du, X.; Li, X.; Liu, X.; Lai, S. Underwriter–auditor relationship and pre-IPO earnings management: Evidence from China. J. Bus. Ethics 2016, 152, 365–392. [Google Scholar] [CrossRef]

- Smith, B.F.; Amoako-Adu, B. Management succession and financial performance of family controlled firms. J. Corp. Financ. 1999, 5, 341–368. [Google Scholar] [CrossRef]

- Pérez-González, F. Inherited control and firm performance. Am. Econ. Rev. 2006, 96, 1559–1588. [Google Scholar] [CrossRef] [Green Version]

- Bennedsen, M.; Nielsen, K.M.; Perez-Gonzalez, F.; Wolfenzon, D. Inside the family firm: The role of families in succession decisions and performance. Q. J. Econ. 2007, 122, 647–691. [Google Scholar] [CrossRef]

- Bertrand, M.; Johnson, S.; Samphantharak, K.; Schoar, A. Mixing family with business: A study of Thai business groups and the families behind them. J. Financ. Econ. 2008, 88, 466–498. [Google Scholar] [CrossRef] [Green Version]

- McConaughy, D.L.; Walker, M.C.; Henderson, G.V.; Mishra, C.S. Founding family controlled firms: Efficiency and value. Rev. Financ. Econ. 1998, 7, 1–19. [Google Scholar] [CrossRef]

- Xu, N.; Yuan, Q.; Jiang, X.; Chan, K.C. Founder’s political connections, second generation involvement, and family firm performance: Evidence from China. J. Corp. Financ. 2015, 33, 243–259. [Google Scholar] [CrossRef]

- Buchanan, J.M. The Samaritan’s Dilemma. In Altruism, Morality and Economic Theory; Phelps, E.S., Ed.; Russell Sage Foundation: New York, NY, USA, 1975; pp. 52–53. [Google Scholar]

- Francis, B.; Hasan, I.; Li, L. Abnormal real operations, real earnings management, and subsequent crashes in stock prices. Rev. Quant. Financ. Account. 2014, 46, 217–260. [Google Scholar] [CrossRef]

- Andreicovici, I.; Cohen, N.; Ferramosca, S.; Ghio, A. Two wrongs make a “right”? Exploring the ethical calculus of earnings management before large labor dismissals. J. Bus. Ethics 2020, 172, 379–405. [Google Scholar] [CrossRef]

- Jiang, H.; Hu, Y.; Zhang, H.; Zhou, D. Benefits of downward earnings management and political connection: Evidence from government subsidy and market pricing. Int. J. Account. 2018, 53, 255–273. [Google Scholar] [CrossRef]

- Roychowdhury, S. Earnings management through real activities manipulation. J. Account. Econ. 2006, 42, 335–370. [Google Scholar] [CrossRef]

- Pourciau, S. Earnings management and nonroutine executive changes. J. Account. Econ. 1993, 16, 317–336. [Google Scholar] [CrossRef]

- Wells, P. Earnings management surrounding CEO changes. Account. Financ. 2002, 42, 169–193. [Google Scholar] [CrossRef]

- Wilson, M.; Wang, L.W. Earnings management following chief executive officer changes: The effect of contemporaneous chairperson and chief financial officer appointments. Account. Financ. 2009, 50, 447–480. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Definition |

|---|---|

| AEM | Accrual earnings management, measured as the signed value of discretionary accruals |

| ABSAEM | Accrual earnings management, measured by the variable consisting of the absolute value of the negative abnormal discretionary accruals and zero for positive abnormal discretionary accruals |

| REM | Real earnings management, measured by the sum of the negative value of the abnormal cash flow from operations, the abnormal production costs and the negative value of abnormal discretionary expenses |

| ABSREM | Real earnings management, measured by the variable consisting of the absolute value of the negative real earnings management and zero for positive REM |

| CAR | Firms’ cumulative market-adjusted return for the three days centered on the day of the official announcement of chairman appointment |

| AVEROA | The average value of firms’ ROA from the 3rd to 5th year after family firm successions |

| SUCCESSION | A dummy variable equaling one if family business is inherited by family successors, and zero if the firm is succeeded by outside professionals |

| POVERTY | A dummy variable equaling one if the founder has poverty experiences in childhood and zero otherwise. It is deemed that the founder has poverty experience if he/she experienced the Three Years of Natural Disasters in childhood (0 to 14 years old), that is, the founder was born from 1947 to 1961 |

| PC | A dummy variable equaling one if the founder is currently holding or previously held a position in the People’s Congress, Chinese People’s Consultative Conference, has received honors from the government, or is a party member of Chinese Communist Party, and zero otherwise |

| INDIR | The proportion of independent directors on the board |

| INST | The percentage of institutional shareholdings |

| LEGAL | An index of market intermediaries development and institutional environment from Fan et al. (2011), and the index captures the development of market intermediaries, such as lawyers, auditors and various industry associations, the efficiency of the local courts, and the protection of property rights |

| SIZE | The natural logarithm of total assets |

| LEV | Total liabilities/total assets |

| ROA | Net profit/the average value of total assets at the beginning of the fiscal year and total assets at the end of the fiscal year |

| LOSS | A dummy variable that equals one if ROA is negative and zero otherwise |

| MVBV | Market value of equity/book value of equity |

| FIRMAGE | List years, equaling to the number of years a company has been listed |

| AUDITOR | A dummy variable equaling one if the company is audited by one of the Big-4 auditors and zero otherwise |

| DUAL | A dummy variable equaling one if the CEO and chairman are the same person and zero otherwise |

| FSR | The percentage of shares held by the largest shareholder, calculated as the number of shares held by the largest shareholder divided by the number of total shares |

| HEIRAGE | The age of family firm heirs |

| Panel A: Descriptive Statistics | ||||||||

|---|---|---|---|---|---|---|---|---|

| Variables | N | Mean | S.D. | Min | Max | |||

| AEM | 524 | 0.0387 | 0.1419 | −0.2598 | 0.6239 | |||

| ABSAEM | 524 | 0.0319 | 0.0585 | 0 | 0.2598 | |||

| REM | 524 | 0.0311 | 0.2063 | −0.4509 | 0.6264 | |||

| ABSREM | 524 | 0.0604 | 0.1106 | 0 | 0.4509 | |||

| SUCCESSION | 524 | 0.3607 | 0.502 | 0 | 1 | |||

| POVERTY | 524 | 0.55 | 0.501 | 0 | 1 | |||

| PC | 524 | 0.81 | 0.397 | 0 | 1 | |||

| INDIR | 524 | 0.3752 | 0.0638 | 0.2353 | 0.5 | |||

| INST | 524 | 36.6322 | 24.5746 | 0.3563 | 84.2238 | |||

| LEGAL | 524 | 10.1423 | 5.508 | 1.84 | 20.61 | |||

| SIZE | 524 | 21.609 | 0.9665 | 20.2 | 24.4 | |||

| LEV | 524 | 0.412 | 0.2015 | 0.0408 | 0.7631 | |||

| ROA | 524 | 0.0411 | 0.0573 | −0.1035 | 0.1947 | |||

| LOSS | 524 | 0.12 | 0.322 | 0 | 1 | |||

| MVBV | 524 | 4.5117 | 3.2095 | 0.822 | 15.1385 | |||

| FIRMAGE | 524 | 14.76 | 5.583 | 5 | 26 | |||

| AUDITOR | 524 | 0.01 | 0.113 | 0 | 1 | |||

| DUAL | 524 | 0.17 | 0.375 | 0 | 1 | |||

| FSR | 524 | 30.7182 | 11.4895 | 11.83 | 56.76 | |||

| CAR | 182 | 0.0146 | 0.0387 | −0.0481 | 0.0887 | |||

| AVEROA | 178 | 0.0453 | 0.0426 | −0.0391 | 0.1249 | |||

| HEIRAGE | 182 | 35.81 | 5.736 | 27 | 48 | |||

| Panel B: Univariate Analysis of Hypothesis 1 | ||||||||

| Group | Mean of AEM | Mean of ABSAEM | Mean of REM | Mean of ABSREM | ||||

| Mean | t-stat | Mean | t-stat | Mean | t-stat | Mean | t-stat | |

| SUCCESSION = 1 (N = 189) | −0.0115 | −2.212 *** | 0.0588 | 2.001 *** | −0.0254 | −2.298 *** | 0.0917 | 2.391 *** |

| SUCCESSION = 0 (N = 335) | 0.067 | 0.0167 | 0.063 | 0.0427 | ||||

| Panel C: Univariate Analysis of Hypothesis 3 | ||||||||

| Group | Mean of CAR | Mean of AVEROA | ||||||

| N | Mean | t-stat | N | Mean | t-stat | |||

| Lower AEM | 106 | 0.031 | 2.591 *** | 80 | 0.0251 | −2.386 *** | ||

| Higher AEM | 76 | −0.0083 | 98 | 0.007 | ||||

| Higher ABSAEM | 47 | 0.0292 | 2.014 ** | 68 | 0.02 | −2.328 *** | ||

| Lower ABSAEM | 135 | 0.0095 | 110 | 0.0863 | ||||

| Lower REM | 106 | 0.0212 | 2.348 ** | 80 | 0.028 | −3.133 *** | ||

| Higher REM | 76 | 0.0054 | 98 | 0.0665 | ||||

| Higher ABSREM | 51 | 0.0199 | 2.442 ** | 67 | 0.03 | −2.99 *** | ||

| Lower ABSREM | 131 | 0.001 | 111 | 0.0701 | ||||

| (1) AEM | (2) ABSAEM | (3) REM | (4) ABSREM | |

|---|---|---|---|---|

| SUCCESSION | −0.0278 *** (−2.65) | 0.0086 *** (3.49) | −0.0584 *** (−2.97) | 0.024 *** (2.84) |

| SIZE | 0.0349 *** (2.5) | −0.0024 ** (−2.25) | 0.0354 * (2.08) | −0.0284 * (−1.84) |

| LEV | −0.1686 *** (−2.45) | 0.055 ** (2.15) | −0.2402 ** (−2.46) | 0.1266 * (1.73) |

| ROA | 0.0222 ** (2.05) | −0.0372 ** (−2.19) | 1.8016 *** (2.71) | −1.5562 *** (−4.95) |

| LOSS | −0.123 *** (−2.58) | 0.0772 *** (2.75) | −0.0927 *** (−2.97) | 0.0541 *** (2.92) |

| MVBV | 0.008 * (1.82) | −0.0012 (−1.38) | 0.0129 (1.21) | −0.0075 (−1.48) |

| FIRMAGE | −0.0023(−0.72) | 0.0006 (0.47) | −0.004 (−0.88) | 0.0014 (0.67) |

| AUDITOR | 0.0502 ** (2.3) | −0.0453 *** (−2.66) | 0.275 ** (2.17) | −0.1717 * (1.84) |

| DUAL | −0.0012 *** (−3.02) | 0.0079 *** (2.83) | −0.0169 *** (−2.52) | 0.0111 *** (2.43) |

| FSR | −0.0007 *** (−2.43) | 0.0003 *** (3.42) | −0.0012 *** (−2.5) | 0.002 *** (2.69) |

| Intercept | −0.8514 * (−1.78) | 0.1099 ** (2.56) | −0.5257 ** (−2.18) | 0.4725 * (1.84) |

| Year fixed effects | Yes | Yes | Yes | Yes |

| Industry fixed effects | Yes | Yes | Yes | Yes |

| Adj. R-sq | 0.207 | 0.2713 | 0.2276 | 0.2183 |

| N | 524 | 524 | 524 | 524 |

| (1) AEM | (2) ABSAEM | (3) REM | (4) ABSREM | |

|---|---|---|---|---|

| SUCCESSION | −0.0469 *** (−3.16) | 0.0917 *** (2.73) | −0.6629 *** (−2.8) | 0.2118 ** (2.16) |

| POVERTY | −0.0259 (−0.46) | 0.0033 (1.14) | −0.0129 (−1.18) | 0.0216 (0.62) |

| SUCCESSION * POVERTY | −0.0289 ** (−2.31) | 0.0302 ** (2.07) | −0.1279 *** (−3.1) | 0.0739 ** (2.28) |

| PC | 0.1456 * (1.9) | −0.0322 * (−1.99) | 0.0606 (1.63) | −0.0246 * (−1.72) |

| SUCCESSION * PC | −0.002 ** (−2.02) | 0.001 ** (2.02) | −0.0821 *** (−2.57) | 0.0814 ** (2.13) |

| INDIR | −0.157 (−0.35) | 0.0538 (1.28) | −0.0541 (−1.1) | 0.0334 (1.12) |

| SUCCESSION * INDIR | 0.1871 (1.29) | −0.2084 (−0.75) | 2.3108 (0.83) | −0.9053 (−1.24) |

| INST | 0.0016 (1.03) | −0.0003 * (−1.73) | 0.0029 * (1.74) | −0.0001 * (−1.91) |

| SUCCESSION * INST | 0.0005 *** (3.32) | −0.0004 ** (−2.5) | 0.0008 ** (2.39) | −0.0007 *** (−2.62) |

| LEGAL | −0.0025 (−1.36) | 0.0024 ** (2.15) | −0.0146 * (−1.68) | 0.0004 (1.1) |

| SUCCESSION * LEGAL | 0.0001 ** (2.13) | −0.001 ** (−2.29) | 0.0129 *** (2.82) | −0.0019 *** (−2.39) |

| SIZE | 0.0571 * (1.9) | −0.003 ** (−2.23) | 0.0429 ** (2.14) | −0.0107 * (−1.75) |

| LEV | −0.246 * (−1.89) | 0.0548 * (1.99) | −0.3252 ** (−1.99) | 0.113 * (1.85) |

| ROA | 0.0994 ** (2.18) | −0.0826 * (−1.66) | 1.6707 ** (2.44) | −1.52 *** (−2.49) |

| LOSS | −0.045 *** (−2.53) | 0.0951 *** (2.64) | −0.0037 *** (−2.53) | 0.0746 *** (2.82) |

| MVBV | 0.0096 (1.14) | −0.0007 (−1.21) | 0.0127 (1.21) | −0.0071 (−1.36) |

| FIRMAGE | −0.0028 (−0.74) | 0.0016 (0.97) | −0.004 (−0.85) | 0.0023 (0.98) |

| AUDITOR | 0.058 * (1.87) | −0.064 * (−1.84) | 0.323 * (1.74) | −0.1315 * (−1.81) |

| DUAL | −0.0366 *** (−2.65) | 0.0086 *** (2.63) | −0.0263 *** (−2.37) | −0.0263 *** (−2.75) |

| FSR | −0.0033 *** (−2.51) | 0.0002 *** (2.52) | −0.0055 *** (−3.03) | −0.0027 *** (−3.05) |

| Intercept | −1.1999 * (−1.89) | −0.0291 ** (−2.11) | −0.698 * (−1.88) | 0.1029 ** (2.26) |

| Year fixed effects | Yes | Yes | Yes | Yes |

| Industry fixed effects | Yes | Yes | Yes | Yes |

| Adj. R-sq | 0.2509 | 0.2091 | 0.2967 | 0.2994 |

| N | 524 | 524 | 524 | 524 |

| CAR | AVEROA | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| AEM | −0.8589 *** (−2.65) | 0.4798 *** (3.96) | ||||||

| ABSAEM | 0.5188 ** (2.25) | −0.7091 *** (−3.41) | ||||||

| REM | −0.0157 ** (−2.38) | 1.0089 *** (2.79) | ||||||

| ABSREM | 0.0237 ** (2.43) | −0.1516 ** (−2.25) | ||||||

| SIZE | 0.0238 ** (2.18) | 0.0222 **(2.14) | 0.0232 ** (2.12) | 0.0232 ** (2.13) | 0.0321 *** (3.8) | 0.0336 *** (3.62) | 0.0188 * (1.82) | 0.0135 ** (2.31) |

| LEV | −0.0248 (−1.4) | −0.016 (−1.27) | −0.0432 (−0.64) | −0.0403 (−0.63) | −0.2279 *** (−4.04) | −0.2467 *** (−4.04) | −0.1813 ** (−2.44) | −0.1778 ** (−2.52) |

| MVBV | 0.0008 * (1.97) | 0.0012 ** (2.26) | 0.0009 ** (2.18) | 0.001 ** (2.22) | 0.0034 ** (2.51) | 0.0047 *** (2.66) | 0.0002 ** (2.03) | −0.0044 ** (−2.53) |

| FIRMAGE | 0.0008 * (1.79) | 0.0011 ** (2.59) | 0.0005 ** (2.26) | 0.0004 ** (2.23) | 0.0016 ** (2.28) | 0.0016 * (2.16) | 0.0012 * (1.76) | 0.0016 * (2.04) |

| HEIRAGE | 0.0034 ** (2.21) | 0.0032 ** (2.29) | 0.0031 * (2.08) | 0.0031 * (2.05) | 0.0024 ** (2.33) | 0.002 * (1.9) | 0.0015 * (1.71) | 0.0013 ** (2.15) |

| INDIR | −0.1317 (−1.1) | −0.1234 (−1.07) | −0.1395 (−1.15) | −0.1418 (−1.16) | 0.052 (0.38) | 0.0111 (1.08) | −0.0657 (−0.36) | −0.0787 (−0.45) |

| INST | 0.0005 ** (2.11) | 0.0005 ** (2.12) | 0.0005 ** (2.22) | 0.0005 ** (2.23) | 0.0007 * (1.84) | 0.0007 * (1.83) | 0.0002 ** (2.32) | 0.0002 ** (2.38) |

| FSR | −0.0017 * (−1.78) | −0.0019 * (−2.09) | −0.0016 (−1.61) | −0.0015 (−1.58) | 0.0002 *** (2.86) | 0.0002 *** (2.83) | 0.0005 *** (2.95) | 0.0005 *** (2.52) |

| Intercept | 0.5659 ** (2.56) | 0.5813 ** (2.73) | 0.5654 ** (2.53) | 0.5691 ** (2.55) | −0.6886 *** (−3.28) | −0.6267 *** (−2.85) | −0.3072 ** (−2.24) | −0.1896 * (−1.77) |

| Year fixed effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry fixed effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Adj. R-sq | 0.1376 | 0.2055 | 0.1195 | 0.1223 | 0.2705 | 0.2308 | 0.1809 | 0.2525 |

| N | 182 | 182 | 182 | 182 | 178 | 178 | 178 | 178 |

| (1) AEM | (2) ABSAEM | |

|---|---|---|

| SUCCESSION | 0.0068 * (1.71) | −0.0008 * (−1.82) |

| SIZE | 0.0136 *** (2.83) | −0.0085 ** (−2.15) |

| LEV | −0.0233 ** (−2.26) | 0.0015 ** (2.04) |

| ROA | 0.6774 ** (2.49) | −0.3713 *** (−3.00) |

| LOSS | −0.0782 *** (−2.95) | 0.0191 *** (2.85) |

| MVBV | 0.0056 (1.23) | −0.0027 (−1.31) |

| FIRMAGE | 0.0001 (1.04) | −0.0001 (−1.08) |

| AUDITOR | 0.0207 ** (2.26) | −0.0234 * (−1.65) |

| DUAL | −0.0198 *** (−2.74) | 0.0176 *** (2.95) |

| FSR | −0.0013 *** (−3.08) | 0.0006 *** (3.17) |

| STAY | 0.0081 (0.29) | −0.0086 (−0.67) |

| Intercept | 0.2754 ** (2.18) | −0.1441 (−0.9) |

| Year fixed effects | Yes | Yes |

| Industry fixed effects | Yes | Yes |

| Adj. R-sq | 0.1491 | 0.1873 |

| N | 558 | 558 |

| First Stage Probit | DV = SUCCESSION | Second Stage OLS | DV = AEM |

|---|---|---|---|

| FOUNDERAGE | 0.2474 *** (3.27) | SUCCESSION | −0.0296 *** (−2.66) |

| SIZE | −0.7931 * (−1.6) | SIZE | 0.0401 * (1.64) |

| LEV | 2.2574 (1.08) | LEV | −0.1835 *** (−2.52) |

| ROA | 14.3024 * (1.73) | ROA | 0.1054 ** (2.21) |

| LOSS | −1.7818 * (−1.93) | LOSS | −0.1486 * (−1.93) |

| MVBV | −0.6815 *** (−2.65) | MVBV | 0.0077 * (1.76) |

| FIRMAGE | 0.0176 (0.31) | FIRMAGE | −0.0024 (−0.73) |

| AUDITOR | 0.4765 (0.72) | AUDITOR | 0.0481 ** (2.25) |

| DUAL | 0.6023 *** (2.8) | DUAL | −0.0046 *** (−3.09) |

| FSR | 0.027 *** (2.82) | FSR | −0.0016 *** (−2.85) |

| IMR | 0.0013 (0.5) | ||

| Intercept | −4.0716 ** (−2.01) | 0.1099 ** (2.56) | −0.9594 * (−1.92) |

| Year fixed effects | Yes | Year fixed effects | Yes |

| Industry fixed effects | Yes | Industry fixed effects | Yes |

| Pseudo R-sq | 0.2661 | Adj. R-sq | 0.1062 |

| N | 450 | N | 450 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Guo, C. Sustainable Development of Chinese Family Firms: A Perspective from Downward Earnings Management before Successions. Sustainability 2022, 14, 9344. https://doi.org/10.3390/su14159344

Guo C. Sustainable Development of Chinese Family Firms: A Perspective from Downward Earnings Management before Successions. Sustainability. 2022; 14(15):9344. https://doi.org/10.3390/su14159344

Chicago/Turabian StyleGuo, Chan. 2022. "Sustainable Development of Chinese Family Firms: A Perspective from Downward Earnings Management before Successions" Sustainability 14, no. 15: 9344. https://doi.org/10.3390/su14159344

APA StyleGuo, C. (2022). Sustainable Development of Chinese Family Firms: A Perspective from Downward Earnings Management before Successions. Sustainability, 14(15), 9344. https://doi.org/10.3390/su14159344