Providing a Roadmap for Future Research Agenda: A Bibliometric Literature Review of Sustainability Performance Reporting (SPR)

, , ,

, , ,  ,

,

Abstract

:1. Introduction

2. Overview of Sustainability Performance Reporting (SPR)

2.1. Environmental Sustainability

2.2. Economic Sustainability

2.3. Social Sustainability

3. Theoretical Perspectives on Sustainability Reporting

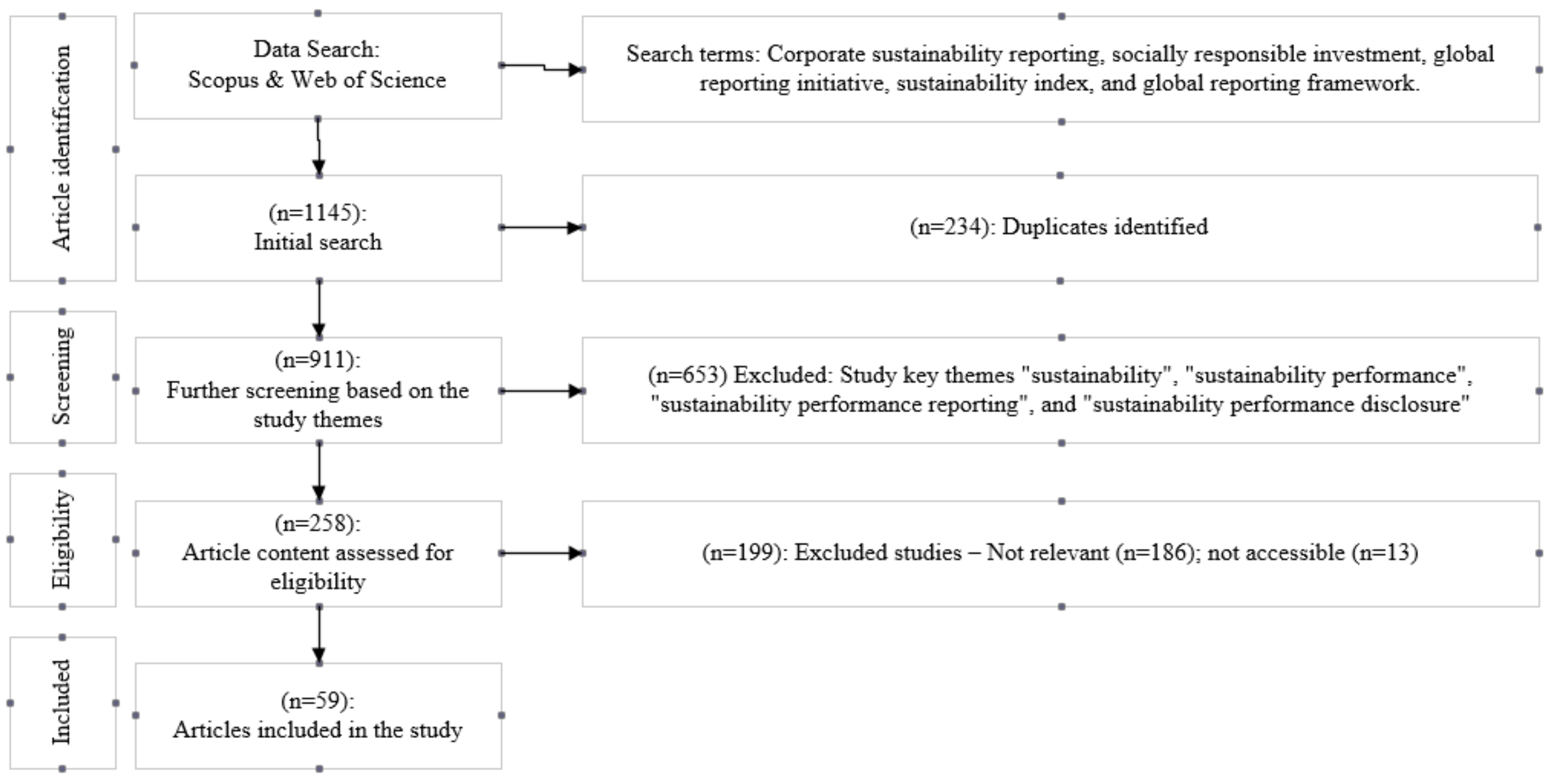

4. Materials and Methods

Data Sources

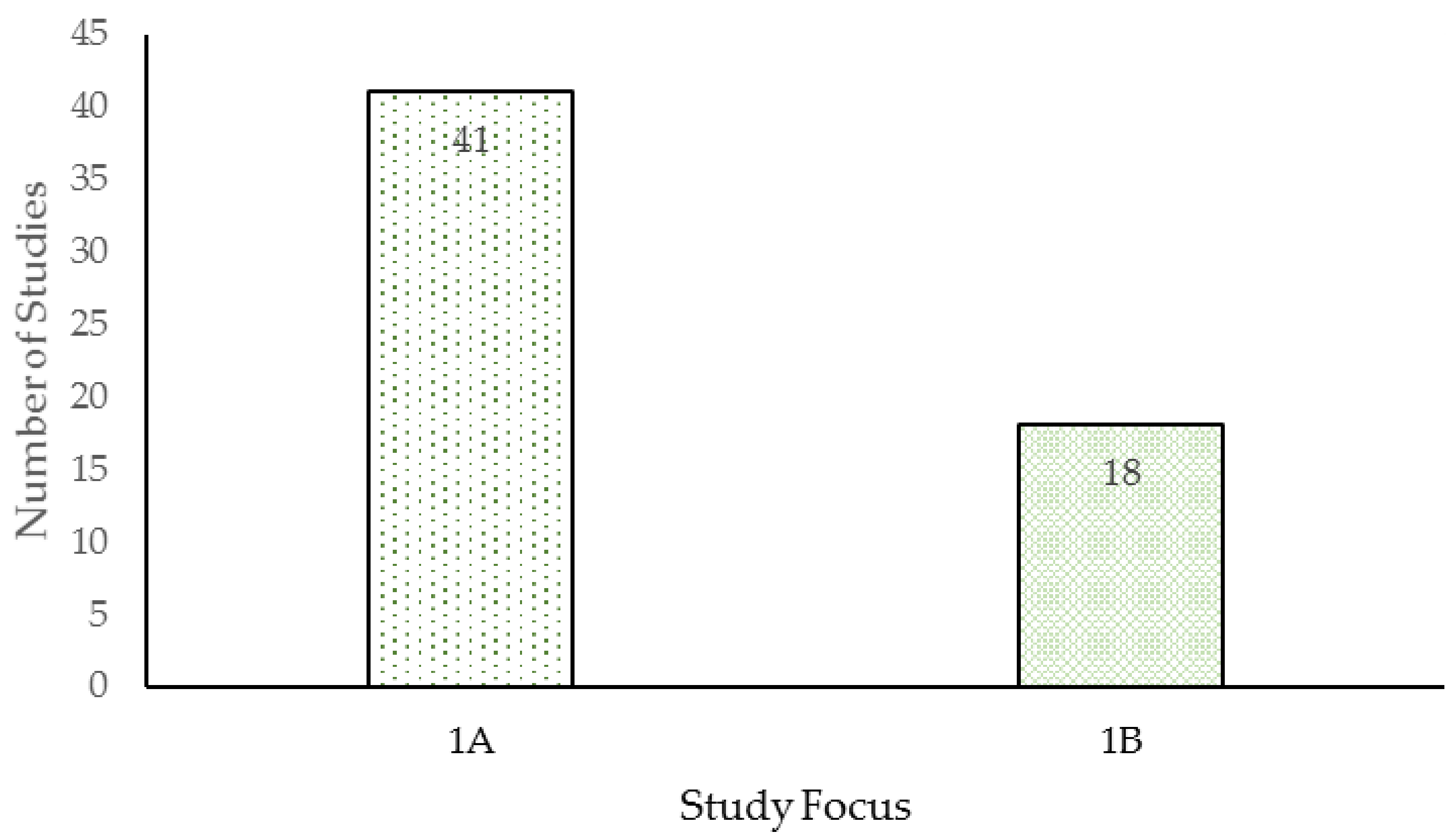

- Study focus, identified as item 1, is coded A to B. This coding focuses on whether the study focuses on sustainability performance reporting or has common themes with sustainability performance reporting.

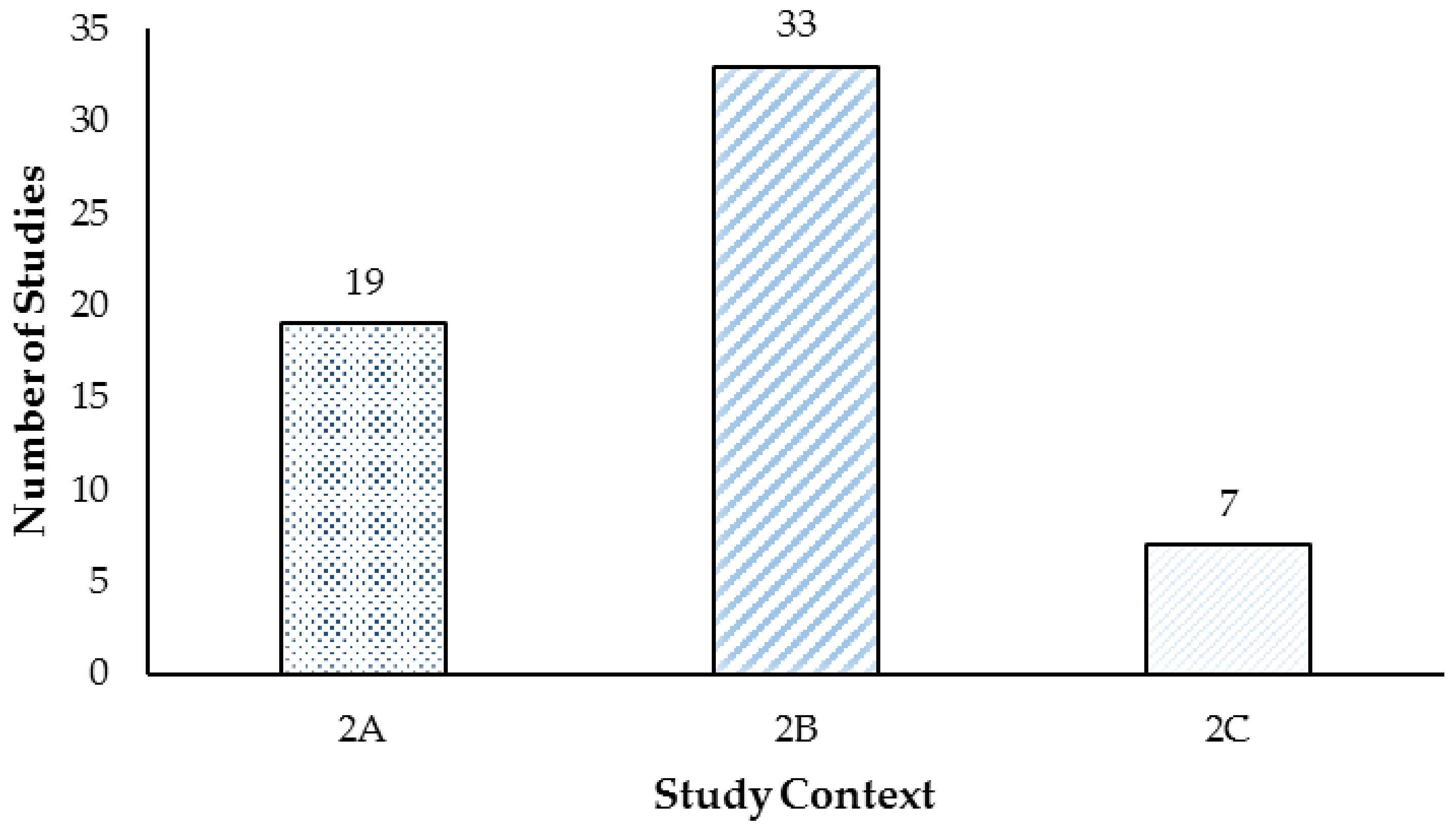

- The study context, classified as item 2, is coded on a scale of A to C.

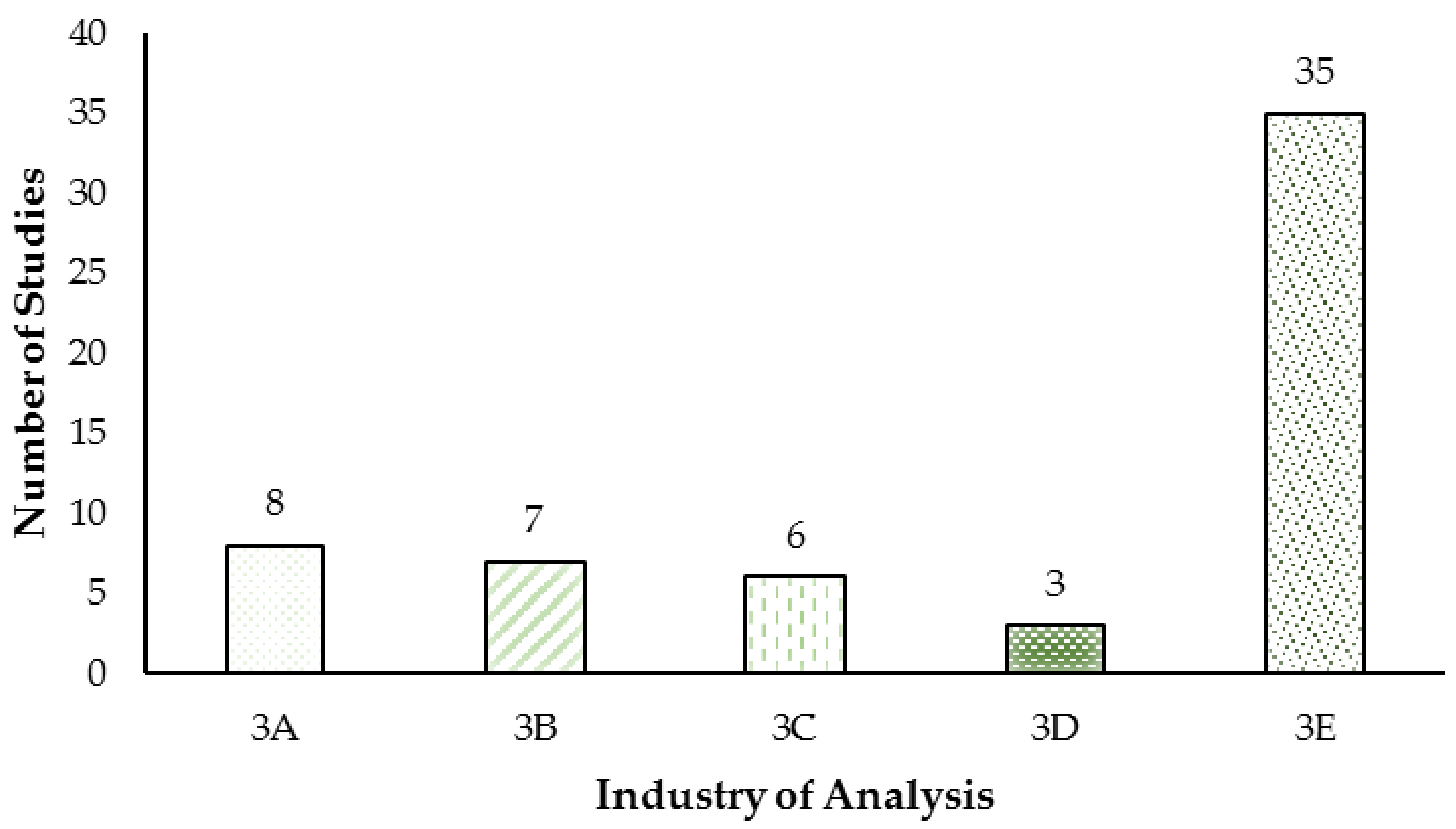

- The industry is classified as item 3 and is coded on a scale of A to E.

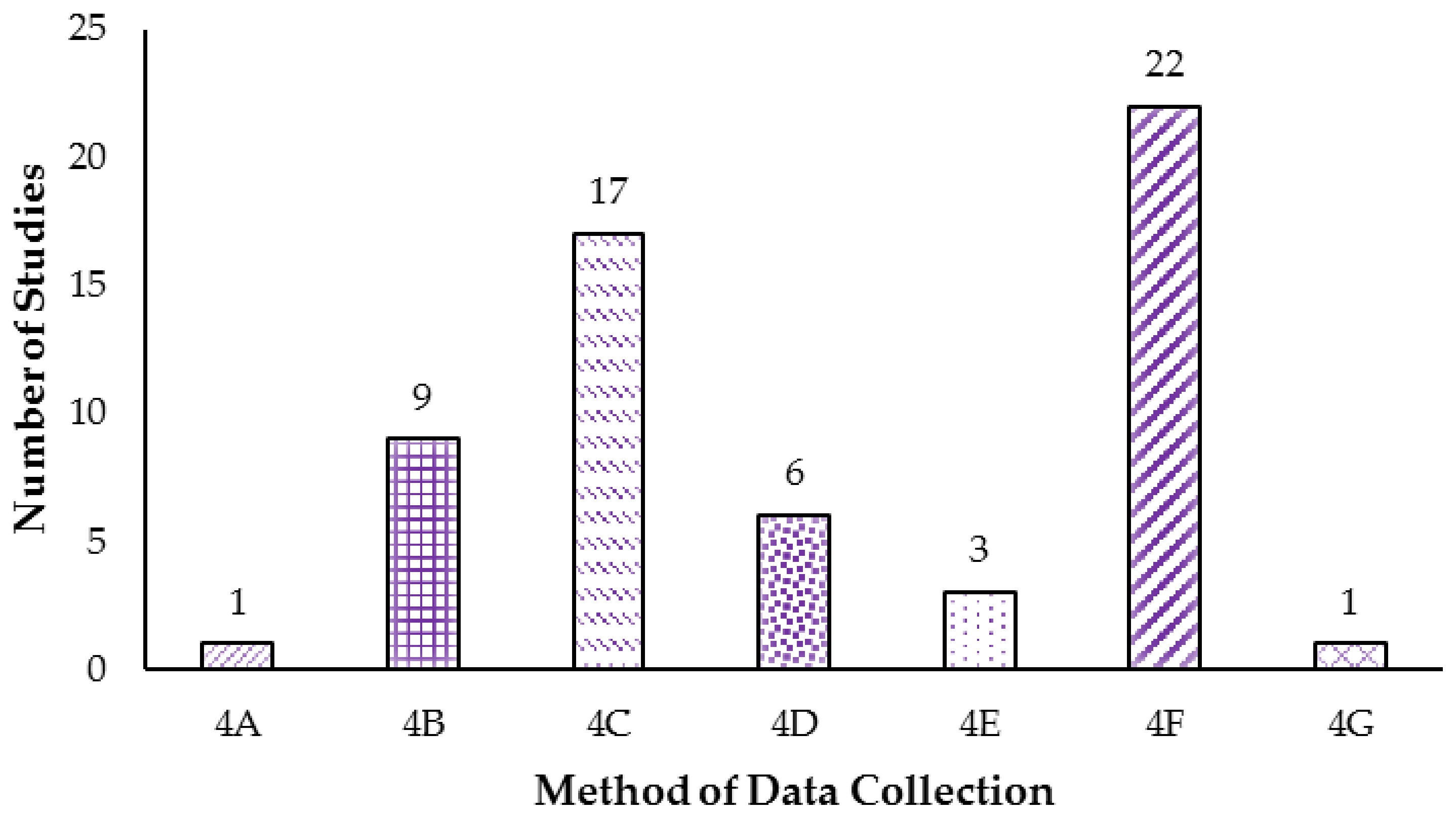

- The method of data collection, identified as item 4, is coded on a scale of A to G.

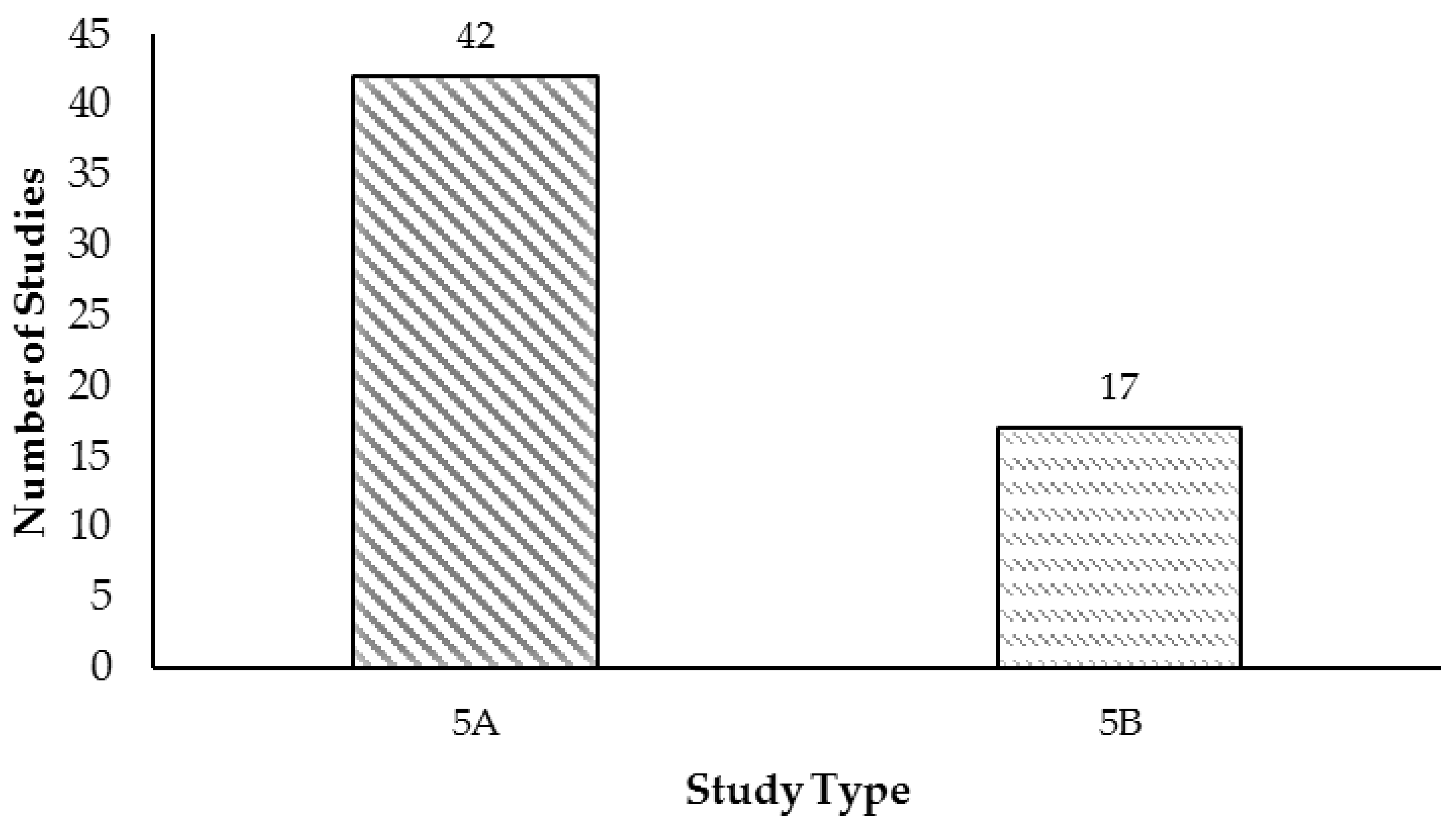

- Likewise, the study type identified as item 5 is coded on a scale of A to B.

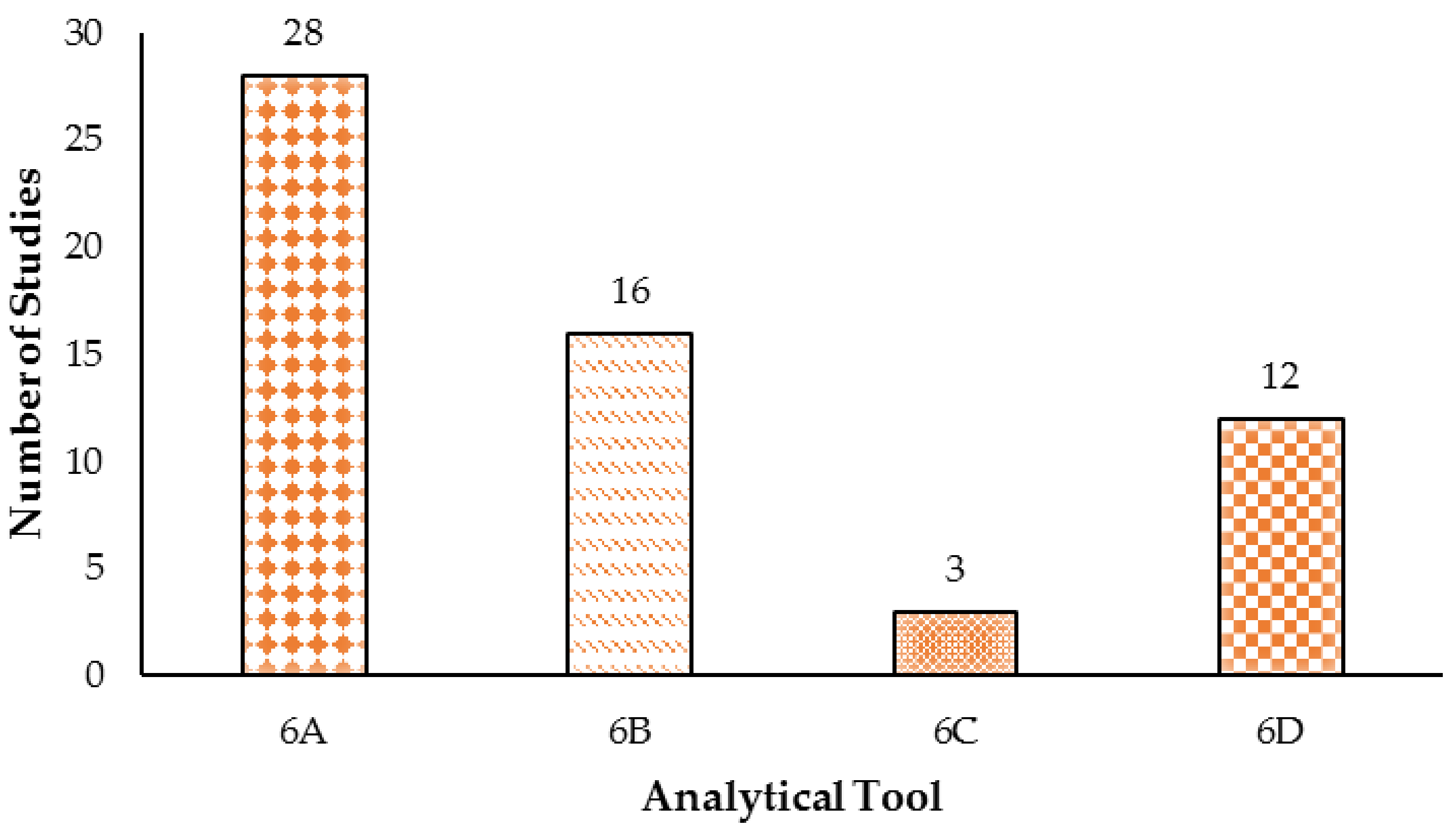

- The analytical tool, identified as item 6, is coded on a scale of A to D.

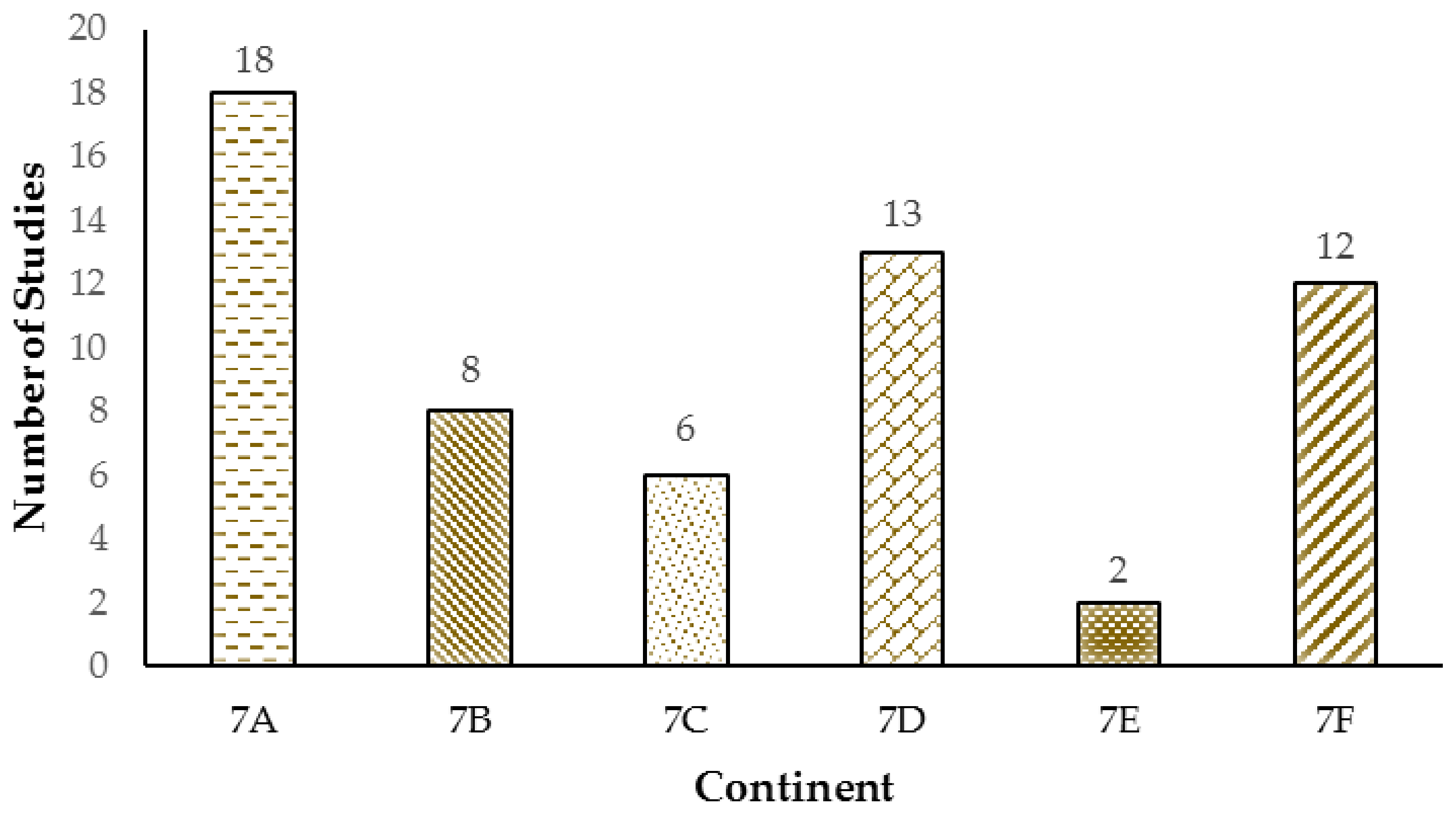

- The study’s continent is classified as item 7 and coded on a scale of A–F.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Classification | Description | Codes |

|---|---|---|

| Study Focus | Sustainability performance reporting as the central theme | 1A |

| Sustainability performance reporting as a supporting theme | 1B | |

| Study Context | Developing countries | 2A |

| Developed countries | 2B | |

| Mixed | 2C | |

| Industry of Analysis | Extraction (Mining, and Oil and gas) | 3A |

| Education/Public Sector | 3B | |

| Manufacturing | 3C | |

| Financial Service/Banking | 3D | |

| Others | 3E | |

| Method of Data Collection | Observation | 4A |

| Surveys | 4B | |

| Case Study | 4C | |

| Interviews | 4D | |

| Case study and Interviews | 4E | |

| Literature review | 4F | |

| Case study and Focus Groups | 4G | |

| Study Type | Empirical | 5A |

| Theoretical | 5B | |

| Analytical Tool | Qualitative | 6A |

| Quantitative | 6B | |

| Mixed | 6C | |

| Not applicable | 6D | |

| Continent | Europe | 7A |

| America | 7B | |

| Africa | 7C | |

| Asia | 7D | |

| Australia | 7E | |

| Mixed | 7F |

5. Results and Discussion

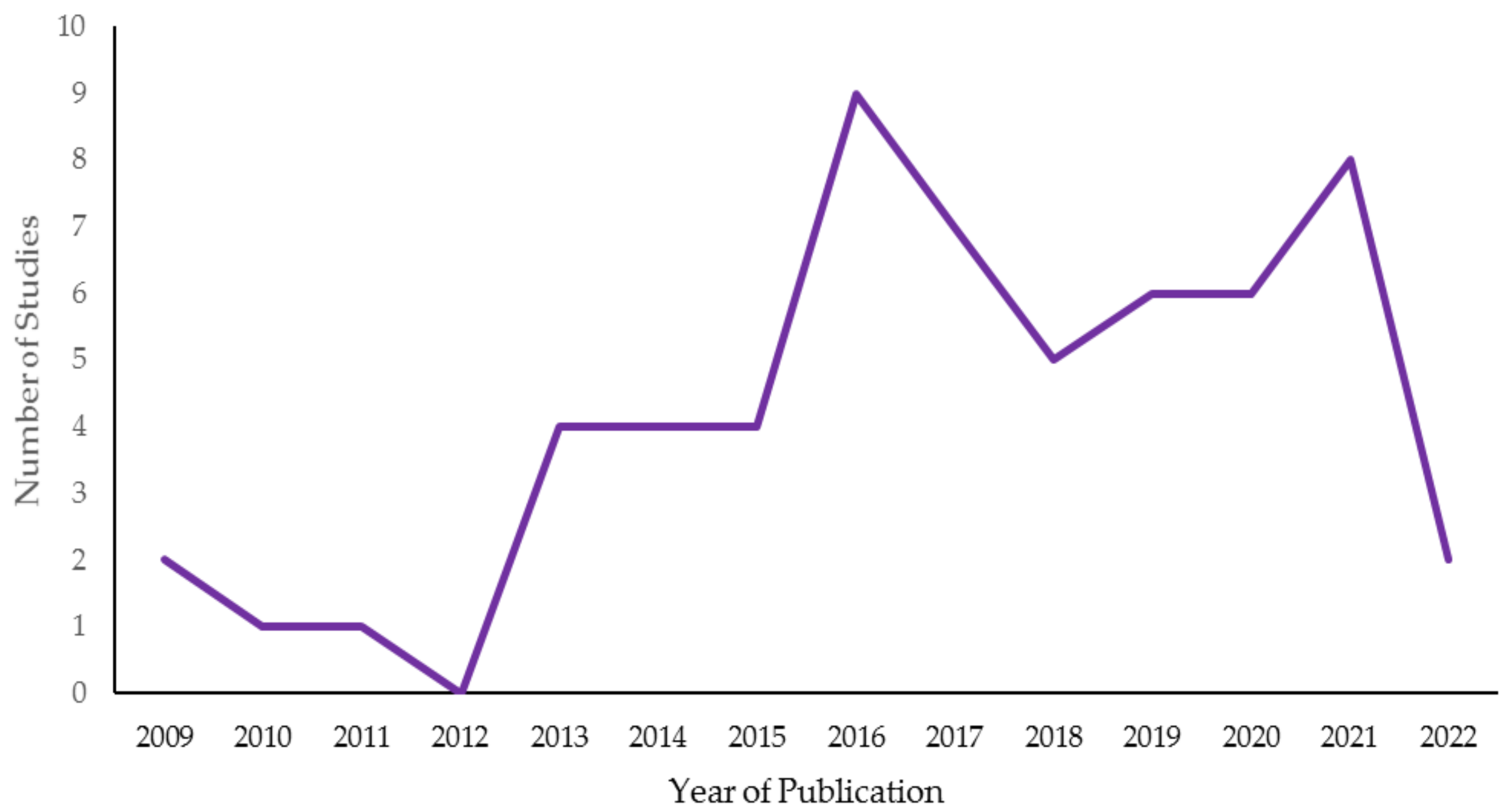

5.1. Overview of Studies

5.2. Studies Focusing on SPR

5.3. Study Context

5.4. Industry of Analysis

5.5. Method of Data Collection

5.6. Study Type

5.7. Study Analytical Method

5.8. Continent of Study

5.9. SPR Indicators

6. Conclusions and Direction for Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

| Journal Name | Number of Articles per Year | Total | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2009 | 2010 | 2011 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | ||

| Business Strategy and the Environment | 1 | 1 | ||||||||||||

| Environmental politics | 1 | 1 | ||||||||||||

| Corporate Social Responsibility and Environmental Management | 1 | 1 | 2 | |||||||||||

| International Journal of Sustainability in Higher Education | 1 | 1 | ||||||||||||

| Journal of Cleaner Production | 2 | 2 | 3 | 1 | 8 | |||||||||

| Accounting and Control for Sustainability | 1 | 1 | ||||||||||||

| Journal of Business Ethics | 2 | 1 | 3 | |||||||||||

| European Journal of Economics and Business Studies | 1 | 1 | ||||||||||||

| Accounting, Auditing & Accountability Journal | 1 | 1 | 1 | 1 | 4 | |||||||||

| Public Relations Review | 1 | 1 | ||||||||||||

| Corporate Reputation Review | 1 | 1 | ||||||||||||

| Communication | 1 | 1 | ||||||||||||

| International Journal of Sustainable Engineering | 1 | 1 | ||||||||||||

| Journal of Corporate Finance | 1 | 1 | ||||||||||||

| Ecological Indicators | 1 | 1 | ||||||||||||

| Journal of Applied Leadership and Management | 1 | 1 | ||||||||||||

| World Scientific News | 1 | 1 | ||||||||||||

| Meditari Accountancy Research | 1 | 1 | ||||||||||||

| International Journal of Innovation and Learning | 1 | 1 | ||||||||||||

| The International Journal of Business in Society | 1 | 1 | ||||||||||||

| Journal of Human Capital Development | 1 | 1 | ||||||||||||

| Journal of Environmental Management | 1 | 1 | 2 | |||||||||||

| Ecological engineering | 1 | 1 | ||||||||||||

| International Journal of Production Economics | 1 | 1 | ||||||||||||

| Asian Review of Accounting | 1 | 1 | ||||||||||||

| Public Management Review | 1 | 1 | ||||||||||||

| Journal of Product Innovation Management | 1 | 1 | ||||||||||||

| Technological and Economic Development of Economy | 1 | 1 | ||||||||||||

| Sustainability | 1 | 1 | 1 | 1 | 4 | |||||||||

| Pacific Accounting Review | 1 | 1 | ||||||||||||

| Indonesian Journal of Sustainability Accounting and Management | 1 | 1 | ||||||||||||

| Human Resource Management Review | 1 | 1 | ||||||||||||

| International Journal of Innovation, Creativity and Change | 1 | 1 | ||||||||||||

| International Journal of Sustainable Development & World Ecology | 1 | 1 | ||||||||||||

| Jindal Journal of Business Research | 1 | 1 | ||||||||||||

| Critical Perspectives on Accounting | 1 | 1 | ||||||||||||

| The TQM Journal | 1 | 1 | ||||||||||||

| Business and Society Review | 1 | 1 | ||||||||||||

| Journal of Intellectual Capital | 1 | 1 | ||||||||||||

| Meditari Accountancy Research | 1 | 1 | ||||||||||||

| Tourism Recreation Research | 1 | 1 | ||||||||||||

| Journal of Global Responsibility | 1 | 1 | ||||||||||||

| Total | 59 | |||||||||||||

References

- D’Adamo, I.; Sassanelli, C. Biomethane community: A research agenda towards sustainability. Sustainability 2022, 14, 4735. [Google Scholar] [CrossRef]

- Roca, L.C.; Searcy, C. An analysis of indicators disclosed in corporate sustainability reports. J. Clean. Prod. 2012, 20, 103–118. [Google Scholar] [CrossRef]

- Gualandris, J.; Golini, R.; Kalchschmidt, M. Do supply management and global sourcing matter for firm sustainability performance? Supply Chain. Manag. Int. J. 2014, 19, 258–274. [Google Scholar] [CrossRef]

- Brown, H.S.; De Jong, M.; Lessidrenska, T. The rise of the Global Reporting Initiative: A case of institutional entrepreneurship. Environ. Politics 2009, 18, 182–200. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R.L. Sustainability accounting for companies: Catchphrase or decision support for business leaders? J. World Bus. 2010, 45, 375–384. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Overell, M.B.; Chapple, L. Environmental reporting and its relation to corporate environmental performance. Abacus 2011, 47, 27–60. [Google Scholar] [CrossRef]

- Valdivia, S.; Bajaj, S.; Sonnemann, G.; Quiros, A.; Ugaya, C.M.L. Mainstreaming life cycle sustainability management in rapidly growing and emerging economies through capacity-building. In Life Cycle Management; Springer: Dordrecht, The Netherlands, 2015; pp. 263–277. [Google Scholar]

- Siano, A.; Conte, F.; Amabile, S.; Vollero, A.; Piciocchi, P. Communicating sustainability: An operational model for evaluating corporate websites. Sustainability 2016, 8, 950. [Google Scholar] [CrossRef] [Green Version]

- Schaltegger, S.; Wagner, M. Integrative management of sustainability performance, measurement and reporting. Int. J. Account. Audit. Perform. Eval. 2006, 3, 1–19. [Google Scholar] [CrossRef]

- Choudhuri, A.; Chakraborty, J. An insight into sustainability reporting. ICFAI J. Manag. Res. 2009, 8, 46–53. [Google Scholar]

- Günther, K. Key Factors for Successful Implementation of a Sustainability Strategy. J. Appl. Leadersh. Manag. 2016, 4, 1–20. [Google Scholar]

- Romero, S.; Fernandez-Feijoo, B.; Ruiz, S. Perceptions of Quality of Assurance Statements for Sustainability Reports. Soc. Responsib. J. 2014, 10, 480–499. [Google Scholar] [CrossRef]

- Ziemann, A. Communication Theory and Sustainability Discourse. In Sustainability Communication–Interdisciplinary Perspectives and Theoretical Foundations; Godemann, J., Michelsen, G., Eds.; Springer: Berlin/Heidelberg, Germany, 2011. [Google Scholar]

- Schaltegger, S.; Burritt, R. Measuring and managing sustainability performance of supply chains. Supply Chain. Manag. Int. J. 2014, 19, 232–241. [Google Scholar] [CrossRef]

- Lozano, R. The State of Sustainability Reporting in Universities. Int. J. Sustain. High. Educ. 2011, 12, 67–78. [Google Scholar] [CrossRef]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a methodology for developing evidence-informed management knowledge by means of systematic review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Mussari, R.; Monfardini, P. Practices of Social Reporting in Public Sector and Non-Profit Organizations. Public Manag. Rev. 2010, 12, 487–492. [Google Scholar] [CrossRef]

- Kolk, A. More Than Words? An Analysis of Sustainability Reports. New Acad. Rev. 2004, 3, 59–75. [Google Scholar]

- Ramos, T.B.; Cecílio, T.; Douglas, C.H.; Caeiro, S. Corporate sustainability reporting and the relations with evaluation and management frameworks: The Portuguese case. J. Clean. Prod. 2013, 52, 317–328. [Google Scholar] [CrossRef]

- Arbačiauskas, V.; Staniškis, J. Sustainability performance indicators for industrial enterprise management. Environ. Res. Eng. Manag. 2009, 48, 42–50. [Google Scholar]

- Global Reporting Initiative (GRI). Sustainability Reporting Guidelines; Global Reporting Initiative: Amsterdam, The Netherlands, 2006. [Google Scholar]

- Fonseca, A.; McAllister, M.L.; Fitzpatrick, P. Sustainability reporting among mining corporations: A constructive critique of the GRI approach. J. Clean. Prod. 2014, 84, 70–83. [Google Scholar] [CrossRef]

- Kocamiş, T.U.; Yildirim, G. Sustainability reporting in Turkey: Analysis of companies in the BIST sustainability index. Eur. J. Econ. Bus. Stud. 2016, 2, 41–51. [Google Scholar] [CrossRef]

- Crouch, E. Chartered Secretary: The governance evolution. Gov. Dir. 2017, 69, 138. [Google Scholar]

- Yılmaz, G.; Nuri İne, M. Assessment of sustainability performances of banks by TOPSIS method and balanced scorecard approach. Int. J. Bus. Appl. Soc. Sci. 2018, 4, 62–75. [Google Scholar]

- Rezaee, Z. Supply chain management and business sustainability synergy: A theoretical and integrated perspective. Sustainability 2018, 10, 275. [Google Scholar] [CrossRef] [Green Version]

- Baumgartner, R. Corporate Sustainability Performance: Methods and Illustrative Example. Int. J. Sustain. Dev. Plan. 2008, 3, 117–131. [Google Scholar] [CrossRef] [Green Version]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. An Overview of Sustainability Assessment Methodologies. Ecol. Indic. 2012, 15, 281–299. [Google Scholar] [CrossRef]

- Caraiani, C.; Lungu, C.I.; Dascălu, C.; Cimpoeru, M.V.; Dinu, M. Social and environmental performance indicators: Dimensions of integrated reporting and benefits for responsible management and sustainability. Afr. J. Bus. Manag. 2012, 6, 4990–4997. [Google Scholar]

- Van Niekerk, A.J. Inclusive Economic Sustainability: SDGs and Global Inequality. Sustainability 2020, 12, 5427. [Google Scholar] [CrossRef]

- Åhman, H. Social sustainability-Society at the intersection of development and maintenance. Local Environ. 2013, 18, 1153–1166. [Google Scholar] [CrossRef]

- Alon, A.; Vidovic, M. Sustainability performance and assurance: Influence on reputation. Corp. Reput. Rev. 2015, 18, 337–352. [Google Scholar] [CrossRef]

- Comyns, B.; Figge, F.; Hahn, T.; Barkemeyer, R. Sustainability reporting: The role of “Search”, “Experience” and “Credence” information. Account. Forum 2013, 37, 231–243. [Google Scholar] [CrossRef]

- Cormier, D.; Ledoux, M.; Magnan, M. The Informational Contribution of Social and Environmental Disclosures for Investors. Manag. Decis. 2011, 49, 1276–1304. [Google Scholar] [CrossRef] [Green Version]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does Corporate Social Responsibility Affect the Cost of Capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- De Villiers, C.; Marques, A.W. Corporate Social Responsibility, Country-Level Predispositions, and the Consequences of Choosing a Level of Disclosure. Account. Bus. Res. 2016, 46, 167–195. [Google Scholar] [CrossRef] [Green Version]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Reddy, K.; Gordon, L.W. The Effect of Sustainability Reporting on Financial Performance: An Empirical Study using Listed Companies. J. Asia Entrep. Sustain. 2010, 6, 19–42. [Google Scholar]

- Hohnen, P. The Future of Sustainability Reporting; EEDP Programme Paper; Chatham House: London, UK, 2012. [Google Scholar]

- Jizi, M. The Influence of Board Composition on Sustainable Development Disclosure. Bus. Strategy Environ. 2017, 26, 640–655. [Google Scholar] [CrossRef]

- Kurniawan, P.S. An Implementation Model of Sustainability Reporting in Village-Owned Enterprise and Small and Medium Enterprise. Indones. J. Sustain. Account. Manag. 2018, 2, 90–106. [Google Scholar] [CrossRef]

- Borga, F.; Citterio, A.; Noci, G.; Pizzurno, E. Sustainability report in small enterprises: Case studies in Italian furniture companies. Bus. Strategy Environ. 2009, 18, 162–176. [Google Scholar] [CrossRef]

- Hahn, R.; Lülfs, R. Legitimizing negative aspects in GRI-oriented sustainability reporting: A qualitative analysis of corporate disclosure strategies. J. Bus. Ethics 2014, 123, 401–420. [Google Scholar] [CrossRef]

- Legrand, W.; Huegel, E.B.; Sloan, P. Learning from best practices: Sustainability reporting in international Hotel Chains. In Advances in Hospitality and Leisure; Emerald Group Publishing Limited: Bingley, UK, 2013; pp. 119–134. [Google Scholar]

- Lee, M.D.P. Configuration of External Influences: The Combined Effects of Institutions and Stakeholders on Corporate Social Responsibility Strategies. J. Bus. Ethics 2011, 102, 281–298. [Google Scholar] [CrossRef]

- Hillenbrand, K.; Money, K. Corporate Responsibility and Corporate Reputation: Two Separate Concepts or Two Sides of the Same Coin? Corp. Reput. Rev. 2007, 10, 261–277. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a Theory of Stakeholder Identification and Salience: Defining the Principle of Who and What Really Count. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Hahn, R.; Kühnen, M. Determinants of Sustainability Reporting: A Review of Results, Trends, Theory and Opportunities in An Expanding Field of Research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- Freeman, R. Strategic Management: A Stakeholder’s Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Guzman, F.; Becker-Oslen, K. Strategic Corporate Social Responsibility: A Brand–Building Tool. In Innovative CSR: From Risk Management to Value Creation; Louche, C., Idowu, S.O., Filho, L.W., Eds.; Greenleaf: Sheffield, UK, 2010; pp. 197–219. [Google Scholar]

- Okereke, C.; Wittneben, B.; Bowen, F. Climate change: Challenging business, transforming politics. Bus. Soc. 2012, 51, 7–30. [Google Scholar] [CrossRef]

- Allen, M. Strategic Communication for Sustainable Organizations. Theory and Practice; University of Arkansas: Fayetteville, AR, USA, 2016. [Google Scholar]

- Mariano, E.B.; Sobreiro, V.A.; do Nascimento Rebelatto, D.A. Human development and data envelopment analysis: A structured literature review. Omega 2015, 54, 33–49. [Google Scholar] [CrossRef]

- Govindan, K.; Rajendran, S.; Sarkis, J.; Murugesan, P. Multi-criteria decision making approaches for green supplier evaluation and selection: A literature review. J. Clean. Prod. 2015, 98, 66–83. [Google Scholar] [CrossRef]

- Fahimnia, B.; Sarkis, J.; Davarzani, H. Green supply chain management: A review and bibliometric analysis. Int. J. Prod. Econ. 2015, 162, 101–114. [Google Scholar] [CrossRef]

- Snyder, H. Literature review as a research methodology: An overview and guidelines. J. Bus. Res. 2019, 104, 333–339. [Google Scholar] [CrossRef]

- Fernández, E.F.; Malwé, C. The emergence of the’ planetary boundaries’ concept in international environmental law: A proposal for a framework convention. Rev. Eur. Comp. Int. Environ. Law 2019, 28, 48–56. [Google Scholar] [CrossRef]

- Falagas, M.E.; Pitsouni, E.I.; Malietzis, G.A.; Pappas, G. Comparison of PubMed, Scopus, web of science, and Google scholar: Strengths and weaknesses. FASEB J. 2008, 22, 338–342. [Google Scholar] [CrossRef]

- Fonseca, A. How credible are mining corporations’ sustainability reports? A critical analysis of external assurance under the requirements of the international council on mining and metals. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 355–370. [Google Scholar] [CrossRef]

- Fonseca, A.; Macdonald, A.; Dandy, E.; Valenti, P. The state of sustainability reporting at Canadian universities. Int. J. Sustain. High. Educ. 2011, 12, 22–40. [Google Scholar] [CrossRef]

- Chang, D.S.; Kuo, L.C.R.; Chen, Y.T. Industrial changes in corporate sustainability performance–an empirical overview using data envelopment analysis. J. Clean. Prod. 2013, 56, 147–155. [Google Scholar] [CrossRef]

- Scagnelli, S.D.; Corazza, L.; Cisi, M. How SMEs disclose their sustainability performance. Which variables influence the choice of reporting guidelines? In Accounting and Control for Sustainability; Emerald Group Publishing Limited: Bingley, UK, 2013; pp. 77–114. [Google Scholar]

- Fernandez-Feijoo, B.; Romero, S.; Ruiz, S. Effect of stakeholders’ pressure on transparency of sustainability reports within the GRI framework. J. Bus. Ethics 2014, 122, 53–63. [Google Scholar] [CrossRef]

- Lodhia, S.; Hess, N. Sustainiability accounting and reporting in the mining industry: Current literature and directions for future research. J. Clean. Prod. 2014, 84, 43–50. [Google Scholar] [CrossRef]

- Maubane, P.; Prinsloo, A.; Van Rooyen, N. Sustainability reporting patterns of companies listed on the Johannesburg securities exchange. Public Relat. Rev. 2014, 40, 153–160. [Google Scholar] [CrossRef]

- Hinson, R.; Gyabea, A.; Ibrahim, M. Sustainability reporting among Ghanaian universities. Communication 2015, 41, 22–42. [Google Scholar] [CrossRef]

- Husgafvel, R.; Pajunen, N.; Virtanen, K.; Paavola, I.L.; Päällysaho, M.; Inkinen, V.; Heiskanen, K.; Dahl, O.; Ekroos, A. Social sustainability performance indicators–experiences from process industry. Int. J. Sustain. Eng. 2015, 8, 14–25. [Google Scholar] [CrossRef]

- Ng, A.C.; Rezaee, Z. Business sustainability performance and cost of equity capital. J. Corp. Financ. 2015, 34, 128–149. [Google Scholar] [CrossRef]

- Diaz-Sarachaga, J.M.; Jato-Espino, D.; Alsulami, B.; Castro-Fresno, D. Evaluation of existing sustainable infrastructure rating systems for their application in developing countries. Ecol. Indic. 2016, 71, 491–502. [Google Scholar] [CrossRef] [Green Version]

- Herremans, I.M.; Nazari, J.A.; Mahmoudian, F. Stakeholder relationships, engagement, and sustainability reporting. J. Bus. Ethics 2016, 138, 417–435. [Google Scholar] [CrossRef]

- Long, T.B.; Blok, V.; Coninx, I. Barriers to the adoption and diffusion of technological innovations for climate-smart agriculture in Europe: Evidence from the Netherlands, France, Switzerland and Italy. J. Clean. Prod. 2016, 112, 9–21. [Google Scholar] [CrossRef]

- Manetti, G.; Bellucci, M. The use of social media for engaging stakeholders in sustainability reporting. Account. Audit. Account. J. 2016, 29, 985–1011. [Google Scholar] [CrossRef] [Green Version]

- Maas, K.; Schaltegger, S.; Crutzen, N. Integrating corporate sustainability assessment, management accounting, control, and reporting. J. Clean. Prod. 2016, 136, 237–248. [Google Scholar] [CrossRef]

- Seele, P. Digitally unified reporting: How XBRL-based real-time transparency helps in combining integrated sustainability reporting and performance control. J. Clean. Prod. 2016, 136, 65–77. [Google Scholar] [CrossRef] [Green Version]

- Thaslim, K.M.; Antony, A.R. Sustainability reporting–Its then, now and the emerging next! World Sci. News 2016, 42, 24–40. [Google Scholar]

- Amoako, K.O.; Lord, B.R.; Dixon, K. Sustainability reporting: Insights from the websites of five plants operated by Newmont Mining Corporation. Meditari Account. Res. 2017, 25, 186–215. [Google Scholar] [CrossRef] [Green Version]

- Anusornnitisarn, P.; Chindavijak, C.; Rassameethes, B.; Meeampol, S.; Kess, P.; Hidayanto, A.N. Development of sustainability’s performance framework: Learning from executive viewpoints. Int. J. Innov. Learn. 2017, 22, 304–321. [Google Scholar] [CrossRef]

- Arthur, C.L.; Wu, J.; Yago, M.; Zhang, J. Investigating performance indicators disclosure in sustainability reports of large mining companies in Ghana. Corp. Gov. Int. J. Bus. Soc. 2017, 17, 643–660. [Google Scholar] [CrossRef] [Green Version]

- Aziz, N.S.A.; Bidin, R.H. A Review on The Indicators Disclosed in Sustainability Reporting of Public Listed Companies in Malaysia. J. Hum. Cap. Dev. 2017, 10, 1–14. [Google Scholar]

- Diouf, D.; Boiral, O. The quality of sustainability reports and impression management: A stakeholder perspective. Account. Audit. Account. J. 2017, 30, 643–667. [Google Scholar] [CrossRef]

- Domingues, A.R.; Lozano, R.; Ceulemans, K.; Ramos, T.B. Sustainability reporting in public sector organisations: Exploring the relation between the reporting process and organisational change management for sustainability. J. Environ. Manag. 2017, 192, 292–301. [Google Scholar] [CrossRef]

- Mickovski, S.B.; Thomson, C.S. Developing a framework for the sustainability assessment of eco-engineering measures. Ecol. Eng. 2017, 109, 145–160. [Google Scholar] [CrossRef] [Green Version]

- Hannibal, C.; Kauppi, K. Third party social sustainability assessment: Is it a multi-tier supply chain solution? Int. J. Prod. Econ. 2018, 217, 78–87. [Google Scholar] [CrossRef]

- Kaur, A.; Lodhia, S. Stakeholder engagement in sustainability accounting and reporting: A study of Australian local councils. Account. Audit. Account. J. 2018, 31, 338–368. [Google Scholar] [CrossRef]

- Laskar, N.; Gopal Maji, S. Disclosure of corporate sustainability performance and firm performance in Asia. Asian Rev. Account. 2018, 26, 414–443. [Google Scholar] [CrossRef]

- Niemann, L.; Hoppe, T. Sustainability reporting by local governments: A magic tool? Lessons on use and usefulness from European pioneers. Public Manag. Rev. 2018, 20, 201–223. [Google Scholar] [CrossRef]

- Watson, R.; Wilson, H.N.; Smart, P.; Macdonald, E.K. Harnessing difference: A capability-based framework for stakeholder engagement in environmental innovation. J. Prod. Innov. Manag. 2018, 35, 254–279. [Google Scholar] [CrossRef] [Green Version]

- Calabrese, A.; Costa, R.; Ghiron, N.L.; Menichini, T. Materiality analysis in sustainability reporting: A tool for directing corporate sustainability towards emerging economic, environmental and social opportunities. Technol. Econ. Dev. Econ. 2019, 25, 1016–1038. [Google Scholar] [CrossRef] [Green Version]

- Carp, M.; Păvăloaia, L.; Afrăsinei, M.B.; Georgescu, I.E. Is Sustainability Reporting a Business Strategy for Firm’s Growth? Empirical Study on the Romanian Capital Market. Sustainability 2019, 11, 30658. [Google Scholar]

- Dissanayake, D.; Tilt, C.; Qian, W. Factors influencing sustainability reporting by Sri Lankan companies. Pac. Account. Rev. 2019, 31, 84–109. [Google Scholar] [CrossRef]

- Semuel, H.; Hatane, S.E.; Fransisca, C.; Tarigan, J.; Dautrey, J.M. A Comparative Study on Financial Performance of the Participants in Indonesia. Indones. J. Sustain. Account. Manag. 2019, 3, 95–108. [Google Scholar]

- Kouloukoui, D.; Sant’Anna, Â.M.O.; da Silva Gomes, S.M.; de Oliveira Marinho, M.M.; de Jong, P.; Kiperstok, A.; Torres, E.A. Factors influencing the level of environmental disclosures in sustainability reports: Case of climate risk disclosure by Brazilian companies. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 791–804. [Google Scholar] [CrossRef]

- Silva, S.; Nuzum, A.K.; Schaltegger, S. Stakeholder expectations on sustainability performance measurement and assessment. A systematic literature review. J. Clean. Prod. 2019, 217, 204–215. [Google Scholar] [CrossRef]

- Poon, T.S.C.; Law, K.K. Sustainable HRM: An extension of the paradox perspective. Hum. Resour. Manag. Rev. 2022, 32, 100818. [Google Scholar] [CrossRef]

- Sari, M.P.; Hajawiyah, A.; Raharja, S.; Pamungkas, I.D. The report of university sustainability in Indonesia. Int. J. Innov. Creat. Chang. 2020, 11, 110–124. [Google Scholar]

- Saeed, M.A.; Kersten, W. Sustainability performance assessment framework: A cross–industry multiple case study. Int. J. Sustain. Dev. World Ecol. 2020, 27, 496–514. [Google Scholar] [CrossRef]

- Khan, H.Z.; Bose, S.; Mollik, A.T.; Harun, H. Green washing “or” authentic effort? An empirical investigation of the quality of sustainability reporting by banks. Account. Audit. Account. J. 2020, 34, 338–369. [Google Scholar] [CrossRef]

- Ionașcu, E.; Mironiuc, M.; Anghel, I.; Huian, M.C. The Involvement of Real Estate Companies in Sustainable Development—An Analysis from the SDGs Reporting Perspective. Sustainability 2020, 12, 798. [Google Scholar] [CrossRef] [Green Version]

- Ceesay, L.B. Exploring the Influence of NGOs in Corporate Sustainability Adoption: Institutional-Legitimacy Perspective. Jindal J. Bus. Res. 2020, 9, 135–147. [Google Scholar] [CrossRef]

- Journeault, M.; Levant, Y.; Picard, C.F. Sustainability performance reporting: A technocratic shadowing and silencing. Crit. Perspect. Account. 2021, 74, 102145. [Google Scholar] [CrossRef]

- Park, A.Y.; Krause, R.M. Exploring the landscape of sustainability performance management systems in US local governments. J. Environ. Manag. 2021, 279, 111764. [Google Scholar] [CrossRef]

- Salehi, M.; Arianpoor, A. The relationship among financial and non-financial aspects of business sustainability performance: Evidence from Iranian panel data. TQM J. 2021, 33, 1447–1468. [Google Scholar] [CrossRef]

- Kumar, K.; Kumari, R.; Kumar, R. The state of corporate sustainability reporting in India: Evidence from environmentally sensitive industries. Bus. Soc. Rev. 2021, 126, 513–538. [Google Scholar] [CrossRef]

- Bananuka, J.; Tauringana, V.; Tumwebaze, Z. Intellectual capital and sustainability reporting practices in Uganda. J. Intellect. Cap. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Ardiana, P.A. Stakeholder engagement in sustainability reporting by Fortune Global 500 companies: A call for embeddedness. Meditari Account. Res. 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Raji, A.; Hassan, A. Sustainability and stakeholder awareness: A case study of a Scottish university. Sustainability 2021, 13, 4186. [Google Scholar] [CrossRef]

- Fennell, D.A.; de Grosbois, D. Communicating sustainability and ecotourism principles by ecolodges: A global analysis. Tour. Recreat. Res. 2021, 1–19. Available online: https://www.tandfonline.com/doi/abs/10.1080/02508281.2021.1920225 (accessed on 10 July 2022).

- Afolabi, H.; Ram, R.; Rimmel, G. Harmonization of Sustainability Reporting Regulation: Analysis of a Contested Arena. Sustainability 2022, 14, 5517. [Google Scholar] [CrossRef]

- Tumwebaze, Z.; Bananuka, J.; Orobia, L.A.; Kinatta, M.M. Board role performance and sustainability reporting practices: Managerial perception-based evidence from Uganda. J. Glob. Responsib. 2022, 13, 317–337. [Google Scholar] [CrossRef]

- Amrina, E.; Vilsi, A.L. Key performance indicators for sustainable manufacturing evaluation in cement industry. Procedia CIRP 2015, 26, 19–23. [Google Scholar] [CrossRef] [Green Version]

- Wisdom, J.; Creswell, J.W. Mixed methods: Integrating quantitative and qualitative data collection and analysis while studying patient-centered medical home models. Agency Healthc. Res. Qual. 2013, 13, 1–5. [Google Scholar]

- Emerald Group Publishing. How to Conduct Empirical Research. 2019. Available online: https://www.emeraldgrouppublishing.com/how-to/research-methods/conduct-empirical-research#theoretical-framework (accessed on 5 January 2020).

- Alghamdi, N. Sustainability reporting in higher education institutions: What, why, and how. In International Business, Trade and Institutional Sustainability; Springer: Cham, Switzerland, 2020; pp. 975–989. [Google Scholar]

- D’Adamo, I.; Gastaldi, M.; Morone, P.; Rosa, P.; Sassanelli, C.; Settembre-Blundo, D.; Shen, Y. Bioeconomy of sustainability: Drivers, opportunities and policy implications. Sustainability 2021, 14, 200. [Google Scholar] [CrossRef]

| Four Sequential Stages | Adopted Article Selection Stages |

|---|---|

| 1. Perform a literature review of the available studies on the topic. | 1. Identifying journal articles that relate to sustainable performance reporting. |

| 2. Based on pre-determined criteria, develop a classification framework. | 2. Journal articles were coded into seven themes. |

| 3. Tabulate and segregate the literature based on the framework. | |

| 4. Using the classification framework, present and organise the review. | 3. Present the findings of the literature review using the coding framework. |

| 5. Review analysis and presentation of suggestions for future work. | 4. Discussions and proposed framework to address the current gap in knowledge. |

| Author(s). | Study Focus | Study Context | Industry of Analysis | Data Collection Method | Study Type | Analytical Tool | Continent |

|---|---|---|---|---|---|---|---|

| Brown et al. [4] | 1B | 2B | 3E | 4D | 5A | 6D | 7F |

| Günther [11] | 1B | 2C | 3C | 4B | 5A | 6A | 7F |

| Ramos et al. [19] | 1A | 2B | 3E | 4B | 5A | 6A | 7A |

| Fonseca et al. [22] | 1A | 2C | 3A | 4D | 5A | 6A | 7B |

| Kocamiş and Yildirim [23] | 1A | 2A | 3E | 4F | 5B | 6D | 7D |

| Alon and Vidovic [32] | 1B | 2C | 3E | 4C | 5A | 6B | 7F |

| Borga et al. [42] | 1A | 2B | 3C | 4E | 5A | 6A | 7A |

| Hahn and Lülfs [43] | 1A | 2B | 3E | 4F | 5A | 6A | 7F |

| Fonseca [59] | 1A | 2B | 3A | 4F | 5B | 6D | 7B |

| Fonseca et al. [60] | 1A | 2B | 3B | 4G | 5A | 6A | 7B |

| Chang et al. [61] | 1B | 2B | 3E | 4C | 5A | 6B | 7D |

| Scagnelli et al. [62] | 1A | 2B | 3E | 4C | 5A | 6D | 7A |

| Fernandez-Feijoo et al. [63] | 1A | 2C | 3E | 4F | 5A | 6B | 7F |

| Lodhia and Hess [64] | 1A | 2B | 3A | 4F | 5B | 6A | 7E |

| Maubane et al. [65] | 1A | 2A | 3E | 4C | 5A | 6A | 7C |

| Hinson, Gyabea and Ibrahim [66] | 1A | 2A | 3B | 4F | 5B | 6A | 7C |

| Husgafvel et al. [67] | 1B | 2B | 3C | 4B | 5A | 6B | 7A |

| Ng and Rezaee [68] | 1B | 2B | 3E | 4C | 5A | 6A | 7F |

| Diaz-Sarachaga et al. [69] | 1B | 2B | 3E | 4F | 5B | 6D | 7F |

| Herremans, Nazari and Mahmoudian [70] | 1B | 2B | 3A | 4A | 5A | 6A | 7B |

| Long et al. [71] | 1B | 2B | 3E | 4D | 5A | 6A | 7A |

| Manetti and Bellucci [72] | 1B | 2B | 3E | 4F | 5B | 6A | 7A |

| Maas et al. [73] | 1B | 2B | 3E | 4F | 5B | 6D | 7A |

| Seele [74] | 1B | 2B | 3E | 4F | 5B | 6A | 7A |

| Thaslim and Antony [75] | 1A | 2A | 3E | 4F | 5B | 6B | 7D |

| Amoako, Lord and Dixon [76] | 1A | 2C | 3A | 4C | 5A | 6A | 7F |

| Anusornnitisarn et al. [77] | 1B | 2A | 3C | 4B | 5A | 6B | 7D |

| Arthur et al. [78] | 1A | 2A | 3A | 4C | 5A | 6A | 7C |

| Aziz, and Bidin [79] | 1A | 2A | 3E | 4F | 5B | 6A | 7D |

| Diouf and Boiral [80] | 1A | 2B | 3E | 4D | 5A | 6A | 7B |

| Domingues et al. [81] | 1A | 2B | 3B | 4B | 5A | 6A | 7F |

| Mickovski and Thomson [82] | 1A | 2B | 3C | 4E | 5A | 6A | 7A |

| Hannibal and Kauppi [83] | 1B | 2B | 3C | 4D | 5A | 6A | 7A |

| Kaur and Lodhia [84] | 1A | 2B | 3E | 4E | 5A | 6A | 7E |

| Laskar and Gopal Maji [85] | 1A | 2C | 3E | 4C | 5A | 6D | 7D |

| Niemann and Hoppe [86] | 1A | 2B | 3B | 4C | 5A | 6A | 7A |

| Watson et al. [87] | 1B | 2B | 3E | 4F | 5B | 6D | 7A |

| Calabrese et al. [88] | 1A | 2B | 3E | 4F | 5B | 6A | 7A |

| Carp et al. [89] | 1A | 2A | 3E | 4C | 5A | 6B | 7A |

| Dissanayake et al. [90] | 1A | 2A | 3E | 4C | 5A | 6B | 7D |

| Semuel et al. [91] | 1A | 2A | 3E | 4F | 5B | 6B | 7D |

| Kouloukoui et al. [92] | 1A | 2A | 3E | 4C | 5A | 6C | 7B |

| Silva et al. [93] | 1B | 2B | 3E | 4F | 5B | 6D | 7A |

| Poon and Law [94] | 1B | 2B | 3E | 4F | 5B | 6D | 7D |

| Sari et al. [95] | 1A | 2A | 3B | 4C | 5A | 6B | 7D |

| Saeed and Kersten [96] | 1B | 2B | 3E | 4F | 5A | 6B | 7A |

| Khan et al. [97] | 1A | 2A | 3D | 4F | 5A | 6A | 7D |

| Ionașcu et al. [98] | 1A | 2B | 3E | 4F | 5A | 6B | 7F |

| Ceesay [99] | 1A | 2A | 3E | 4F | 5B | 6D | 7C |

| Journeault et al. [100] | 1A | 2B | 3A | 4C | 5A | 6A | 7B |

| Park and Krause [101] | 1A | 2B | 3B | 4B | 5A | 6B | 7B |

| Salehi and Arianpoor [102] | 1A | 2A | 3E | 4B | 5A | 6B | 7D |

| Kumar et al. [103] | 1A | 2A | 3A | 4C | 5A | 6A | 7D |

| Bananuka et al. [104] | 1A | 2A | 3D | 4B | 5A | 6B | 7C |

| Ardiana [105] | 1A | 2B | 3E | 4C | 5A | 6C | 7F |

| Raji and Hassan [106] | 1A | 2B | 3B | 4D | 5A | 6A | 7A |

| Fennell and de Grosbois [107] | 1A | 2C | 3E | 4C | 5A | 6C | 7F |

| Afolabi et al. [108] | 1A | 2B | 3E | 4F | 5B | 6D | 7A |

| Tumwebaze et al. [109] | 1A | 2A | 3D | 4B | 5A | 6B | 7C |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Osobajo, O.A.; Oke, A.; Lawani, A.; Omotayo, T.S.; Ndubuka-McCallum, N.; Obi, L. Providing a Roadmap for Future Research Agenda: A Bibliometric Literature Review of Sustainability Performance Reporting (SPR). Sustainability 2022, 14, 8523. https://doi.org/10.3390/su14148523

Osobajo OA, Oke A, Lawani A, Omotayo TS, Ndubuka-McCallum N, Obi L. Providing a Roadmap for Future Research Agenda: A Bibliometric Literature Review of Sustainability Performance Reporting (SPR). Sustainability. 2022; 14(14):8523. https://doi.org/10.3390/su14148523

Chicago/Turabian StyleOsobajo, Oluyomi A., Adekunle Oke, Ama Lawani, Temitope S. Omotayo, Nkeiruka Ndubuka-McCallum, and Lovelin Obi. 2022. "Providing a Roadmap for Future Research Agenda: A Bibliometric Literature Review of Sustainability Performance Reporting (SPR)" Sustainability 14, no. 14: 8523. https://doi.org/10.3390/su14148523